Taxation Law Report: Australian Residency and Income Tax Implications

VerifiedAdded on 2020/06/06

|12

|3154

|32

Report

AI Summary

This report delves into the principles of Australian taxation law, examining the concept of residency and its implications for income tax. It analyzes the rules and regulations governing residency tests, including the domicile test, the 183-day test, and the superannuation test, and how these determine a person's tax obligations. The report further explores the taxation of different income types, such as ordinary and statutory income, and discusses the tax rates applicable to residents and non-residents. It also addresses the concept of temporary residency and its specific tax implications, including relevant legislation such as the Migration Act 1958. Additionally, the report examines specific scenarios, such as the tax treatment of lump-sum payments and annual salaries, and references relevant case law to illustrate key principles. The report concludes by summarizing the tax liabilities of individuals under Australian law, offering a comprehensive overview of the subject.

PRINCIPLE OF TAXATION

LAW

LAW

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

QUESTION 1...................................................................................................................................3

QUESTION 2...................................................................................................................................7

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................3

QUESTION 1...................................................................................................................................3

QUESTION 2...................................................................................................................................7

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Resident is the person who lives permanently in one country. In case person

resides in one country but he is citizen of another then they have to live equal to number

of days which are mentioned under law of taxation. This law is able to define residential

status of person and income which is taxable or not. Every person is bound to pay tax

on his income on annual basis 1. Australian taxation law implies on person in order to

identify their residential status. Through legal authorities are able to evaluate their

taxable income.

QUESTION 1

There are many rules and regulations which are framed by government regarding

the taxation of income of person. With reference to given case scenario, firstly it is

essential to identify their residency test (PRINCIPLES OF TAXATION LAW 2017.

2017). If Jenny resides in Australia, then it is significant to considered her income for tax

purpose and for this any other residency test will not apply. Here are three statutory

tests which has be satisfy by Jenny to considered her as Australian resident.

Domicile test – Person will be considered as Australian resident if place of

permanent is in Australia.

183-day test – If a person is staying in Australia more than half of income year,

whether continuously or breaks. So it can also be said as constructive residence

in Australia.

Superannuation test – This ensures that Australian government employees who

are working at Australian posts will be also treated as resident.

The law of taxation is able to decide residential status of each and every person who

resides whether in his home country or foreign 2. On the other hand, the rate of tax is also

1 Bartel, R. and Barclay, E., 2011. Motivational postures and compliance with

environmental law in Australian agriculture. Journal of Rural Studies. 27(2).

pp.153-170.

2 Brilmayer, L., 2010. The New Extraterritoriality: Morrison v. National Australia

Bank, Legislative Supremacy, and the Presumption Against Extraterritorial

Application of American Law. Sw. L. Rev.. 40. p.655.

1

Resident is the person who lives permanently in one country. In case person

resides in one country but he is citizen of another then they have to live equal to number

of days which are mentioned under law of taxation. This law is able to define residential

status of person and income which is taxable or not. Every person is bound to pay tax

on his income on annual basis 1. Australian taxation law implies on person in order to

identify their residential status. Through legal authorities are able to evaluate their

taxable income.

QUESTION 1

There are many rules and regulations which are framed by government regarding

the taxation of income of person. With reference to given case scenario, firstly it is

essential to identify their residency test (PRINCIPLES OF TAXATION LAW 2017.

2017). If Jenny resides in Australia, then it is significant to considered her income for tax

purpose and for this any other residency test will not apply. Here are three statutory

tests which has be satisfy by Jenny to considered her as Australian resident.

Domicile test – Person will be considered as Australian resident if place of

permanent is in Australia.

183-day test – If a person is staying in Australia more than half of income year,

whether continuously or breaks. So it can also be said as constructive residence

in Australia.

Superannuation test – This ensures that Australian government employees who

are working at Australian posts will be also treated as resident.

The law of taxation is able to decide residential status of each and every person who

resides whether in his home country or foreign 2. On the other hand, the rate of tax is also

1 Bartel, R. and Barclay, E., 2011. Motivational postures and compliance with

environmental law in Australian agriculture. Journal of Rural Studies. 27(2).

pp.153-170.

2 Brilmayer, L., 2010. The New Extraterritoriality: Morrison v. National Australia

Bank, Legislative Supremacy, and the Presumption Against Extraterritorial

Application of American Law. Sw. L. Rev.. 40. p.655.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

applies on them on the basis of their residential status. People are bound to pay tax equal

to the amount imposed on them and rate of income tax which is imposed on them.

Various types of exemptions are also available for them through which are exempted

from tax. Lots of tax rebates provided to them which is imposed on the basis of situation

of them. The residents of Australia are usually taxed on the worldwide income which is

received from different sources. Furthermore, temporary resident person of cited country

as well as foreign resident person is normally taxed on the basis of their Australian source

of income. Like they earn money from Australia. The residential status of person is

different from one another. As they have to pay tax according to rules and regulation

which is mentioned under such law.

There are two types of person resides such as Resident and non-resident. It has

been decided on the basis of days which they live in different country. Resident is the

person who permanently reside in one country and non-resident is person who not live

permanently in one country. On the basis of rule of taxation law person who defined as

resident if any of the following mentioned conditions are applied which are as aligned

below-

Person must be domiciled in country Australia also does not hold

permanent place of abode abroad.

Person may not be domiciled but have to resides in Australia for 183

days or more during financial year either on continuous basis or not.

Person goes abroad for the purpose of work which is related to

employment for the time less than 2 years. After that returning to

home country as well.

Some other facts which needs to be fulfil are as aligned below-

Having permanent house in Australia.

Habitual Abode in country Australia.

Individual called as non residents after fulfilling some situation which as aligned below-

Income has been received through branch of Australia and which is

owned by person who is called as non-resident person.

Income has been accepted from Australian agent on the basis of legal

contract. Such money accepted on behalf of non-resident individual.

1

to the amount imposed on them and rate of income tax which is imposed on them.

Various types of exemptions are also available for them through which are exempted

from tax. Lots of tax rebates provided to them which is imposed on the basis of situation

of them. The residents of Australia are usually taxed on the worldwide income which is

received from different sources. Furthermore, temporary resident person of cited country

as well as foreign resident person is normally taxed on the basis of their Australian source

of income. Like they earn money from Australia. The residential status of person is

different from one another. As they have to pay tax according to rules and regulation

which is mentioned under such law.

There are two types of person resides such as Resident and non-resident. It has

been decided on the basis of days which they live in different country. Resident is the

person who permanently reside in one country and non-resident is person who not live

permanently in one country. On the basis of rule of taxation law person who defined as

resident if any of the following mentioned conditions are applied which are as aligned

below-

Person must be domiciled in country Australia also does not hold

permanent place of abode abroad.

Person may not be domiciled but have to resides in Australia for 183

days or more during financial year either on continuous basis or not.

Person goes abroad for the purpose of work which is related to

employment for the time less than 2 years. After that returning to

home country as well.

Some other facts which needs to be fulfil are as aligned below-

Having permanent house in Australia.

Habitual Abode in country Australia.

Individual called as non residents after fulfilling some situation which as aligned below-

Income has been received through branch of Australia and which is

owned by person who is called as non-resident person.

Income has been accepted from Australian agent on the basis of legal

contract. Such money accepted on behalf of non-resident individual.

1

A person who is known as non-resident having permission as well as visas to

work. But he must have to maintain Tax File Number (TFN) which is important

document for all individuals 3. If in case person not hold such significant document then

tax will be deducted from their wages. Australia has been framed double taxation

agreement with different other countries. Through which several employees of several

categories have to pay tax on the basis of terms and condition of their own country.

Each and every resident in responsible to follow all rules, regulation and policies which

are imposed on them. They have to comply with such taxation rules as such legal term

binding individuals.

Temporary residents

The taxation law is able to exempts as we temporary resident individual from

income tax of country Australia. Income has been considered as ordinary as well as

statutory income from various other sources. For the purpose of tax which is related to

capital gains the temporary resident has been considered as non-resident Person must

be not considered as Australian resident as per the rule of Social Security Act 1991.

Also they must be single or not having spouse 4. As temporary resident is the person

which is not permanent resident of country. They are liable to pay tax accordingly. As

they follow rules and regulation which are imposed on them. The individual is

considered as temporary resident person if fulfil various conditions which are as aligned

below-

Individual not having spouse as they must be single and considered as

Australian resident.

Person not considered as Australian resident which is related to provision

of social security.

Person have to hold temporary visa according to Migration Act 1958, this

act is able to permit them.

3 Crawford, J., 2012. Brownlie's principles of public international law. Oxford

University Press.

4 Dolzer, R. and Schreuer, C., 2012. Principles of international investment law.

Oxford University Press.

1

work. But he must have to maintain Tax File Number (TFN) which is important

document for all individuals 3. If in case person not hold such significant document then

tax will be deducted from their wages. Australia has been framed double taxation

agreement with different other countries. Through which several employees of several

categories have to pay tax on the basis of terms and condition of their own country.

Each and every resident in responsible to follow all rules, regulation and policies which

are imposed on them. They have to comply with such taxation rules as such legal term

binding individuals.

Temporary residents

The taxation law is able to exempts as we temporary resident individual from

income tax of country Australia. Income has been considered as ordinary as well as

statutory income from various other sources. For the purpose of tax which is related to

capital gains the temporary resident has been considered as non-resident Person must

be not considered as Australian resident as per the rule of Social Security Act 1991.

Also they must be single or not having spouse 4. As temporary resident is the person

which is not permanent resident of country. They are liable to pay tax accordingly. As

they follow rules and regulation which are imposed on them. The individual is

considered as temporary resident person if fulfil various conditions which are as aligned

below-

Individual not having spouse as they must be single and considered as

Australian resident.

Person not considered as Australian resident which is related to provision

of social security.

Person have to hold temporary visa according to Migration Act 1958, this

act is able to permit them.

3 Crawford, J., 2012. Brownlie's principles of public international law. Oxford

University Press.

4 Dolzer, R. and Schreuer, C., 2012. Principles of international investment law.

Oxford University Press.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

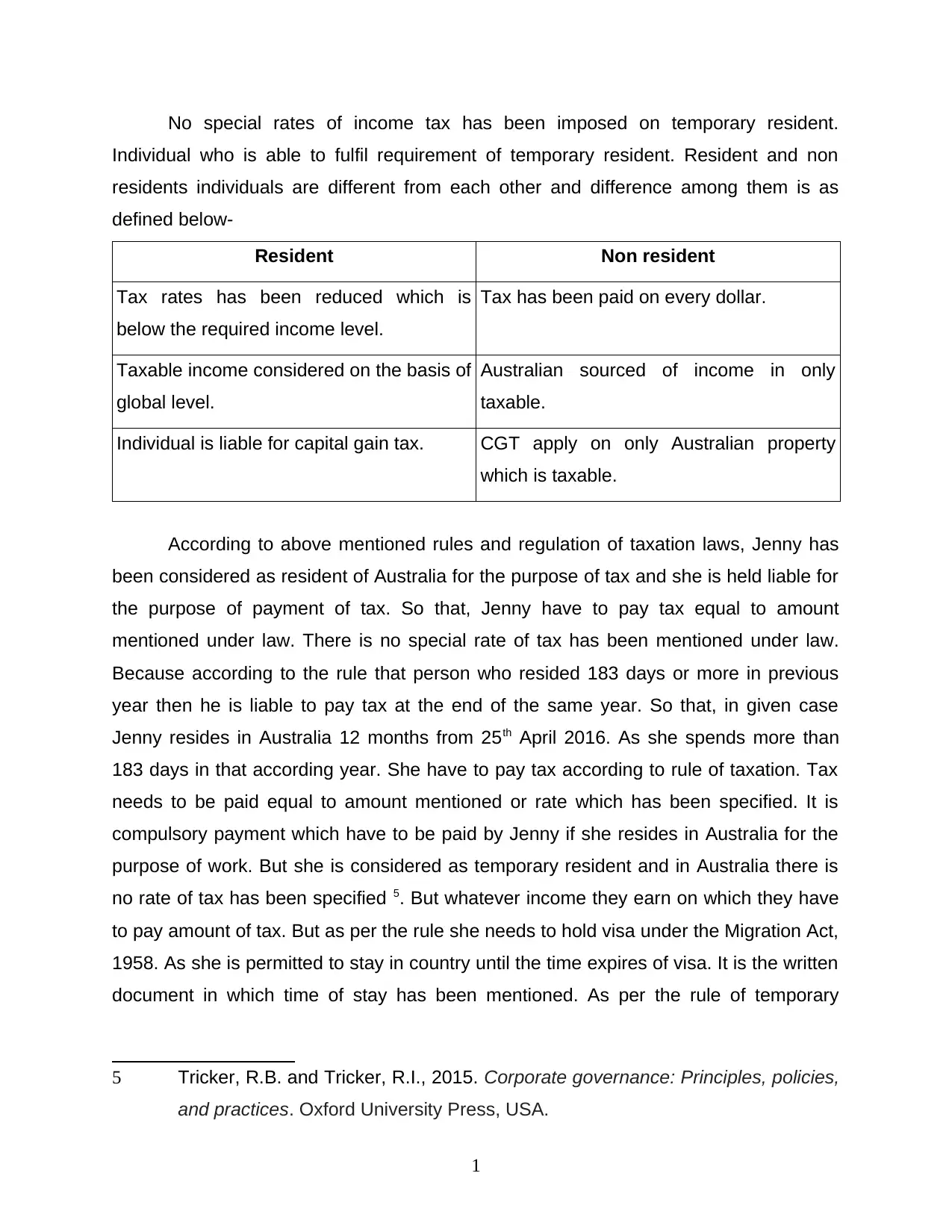

No special rates of income tax has been imposed on temporary resident.

Individual who is able to fulfil requirement of temporary resident. Resident and non

residents individuals are different from each other and difference among them is as

defined below-

Resident Non resident

Tax rates has been reduced which is

below the required income level.

Tax has been paid on every dollar.

Taxable income considered on the basis of

global level.

Australian sourced of income in only

taxable.

Individual is liable for capital gain tax. CGT apply on only Australian property

which is taxable.

According to above mentioned rules and regulation of taxation laws, Jenny has

been considered as resident of Australia for the purpose of tax and she is held liable for

the purpose of payment of tax. So that, Jenny have to pay tax equal to amount

mentioned under law. There is no special rate of tax has been mentioned under law.

Because according to the rule that person who resided 183 days or more in previous

year then he is liable to pay tax at the end of the same year. So that, in given case

Jenny resides in Australia 12 months from 25th April 2016. As she spends more than

183 days in that according year. She have to pay tax according to rule of taxation. Tax

needs to be paid equal to amount mentioned or rate which has been specified. It is

compulsory payment which have to be paid by Jenny if she resides in Australia for the

purpose of work. But she is considered as temporary resident and in Australia there is

no rate of tax has been specified 5. But whatever income they earn on which they have

to pay amount of tax. But as per the rule she needs to hold visa under the Migration Act,

1958. As she is permitted to stay in country until the time expires of visa. It is the written

document in which time of stay has been mentioned. As per the rule of temporary

5 Tricker, R.B. and Tricker, R.I., 2015. Corporate governance: Principles, policies,

and practices. Oxford University Press, USA.

1

Individual who is able to fulfil requirement of temporary resident. Resident and non

residents individuals are different from each other and difference among them is as

defined below-

Resident Non resident

Tax rates has been reduced which is

below the required income level.

Tax has been paid on every dollar.

Taxable income considered on the basis of

global level.

Australian sourced of income in only

taxable.

Individual is liable for capital gain tax. CGT apply on only Australian property

which is taxable.

According to above mentioned rules and regulation of taxation laws, Jenny has

been considered as resident of Australia for the purpose of tax and she is held liable for

the purpose of payment of tax. So that, Jenny have to pay tax equal to amount

mentioned under law. There is no special rate of tax has been mentioned under law.

Because according to the rule that person who resided 183 days or more in previous

year then he is liable to pay tax at the end of the same year. So that, in given case

Jenny resides in Australia 12 months from 25th April 2016. As she spends more than

183 days in that according year. She have to pay tax according to rule of taxation. Tax

needs to be paid equal to amount mentioned or rate which has been specified. It is

compulsory payment which have to be paid by Jenny if she resides in Australia for the

purpose of work. But she is considered as temporary resident and in Australia there is

no rate of tax has been specified 5. But whatever income they earn on which they have

to pay amount of tax. But as per the rule she needs to hold visa under the Migration Act,

1958. As she is permitted to stay in country until the time expires of visa. It is the written

document in which time of stay has been mentioned. As per the rule of temporary

5 Tricker, R.B. and Tricker, R.I., 2015. Corporate governance: Principles, policies,

and practices. Oxford University Press, USA.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

resident Jenny is an single or not having spouse. So that, she is considered as

temporary resident of Australia.

According to the Mallalieu v Drummond, 1983, in this case it has been stated that

taxpayer is female who is act as practising barrister and spent lots of amount of money

on replacing as well as laundering court attire. The costs of court dress has been fully

deductible expenses which is allowable under provisions of law.

QUESTION 2

The ordinary income has been defined under section 6 – 5 of ITAA97. As per the

given scenario, there is television personality pay 4,00,000 dollar as lump sum amount

in order to encourage new television network. It has been done in order to comply with

rules and regulation which are mentioned under law. Such amount needs to be add in

her taxable income on which she have to pay tax equal to the amount mentioned under

rules of taxation law 6. It has been considered as her ordinary income. Also he have to

pay tax on such lump sum amount which is mentioned under provision of law. So that,

such offer has been accepted by her and able to received 1,00,000 dollar as annual

salary. Such amount is in addition of previous lump sum amount. Taxpayer have to pay

amount of tax as per inducement to enter into contract. Through which they are able to

provide services in future with the help of establishment of nexus as well as try to

making it ordinary income. Section 15 – 2 is the relevant law which consists sufficient

facts to deny with the amount of 4,00,000 dollars which is considered ordinary income.

This amount has been considered as statutory income in section 15 – 2 if it constitute a

benefit etc. which is in the respect of services. With the case of Smith v FCT (1987) 19

ATR 274 it has been stated that suggestion must be discussed which provide nexus test

under section 15-2 which is easier to meet section 6-5. At this point of time such

payments must be considered as inducement in order to enter into employement

contract which would be arise in future services.

In accordance with rules of taxation act 1936, 1,00,000 dollar annual salary is

clearly considered as ordinary income on the basis of clear nexus through services

6 Wang, J., Ayres, H. and Huyton, J., 2010. Is tourism education meeting the

needs of the tourism industry? An Australian case study. Journal of Hospitality &

Tourism Education. 22(1). pp.8-14.

1

temporary resident of Australia.

According to the Mallalieu v Drummond, 1983, in this case it has been stated that

taxpayer is female who is act as practising barrister and spent lots of amount of money

on replacing as well as laundering court attire. The costs of court dress has been fully

deductible expenses which is allowable under provisions of law.

QUESTION 2

The ordinary income has been defined under section 6 – 5 of ITAA97. As per the

given scenario, there is television personality pay 4,00,000 dollar as lump sum amount

in order to encourage new television network. It has been done in order to comply with

rules and regulation which are mentioned under law. Such amount needs to be add in

her taxable income on which she have to pay tax equal to the amount mentioned under

rules of taxation law 6. It has been considered as her ordinary income. Also he have to

pay tax on such lump sum amount which is mentioned under provision of law. So that,

such offer has been accepted by her and able to received 1,00,000 dollar as annual

salary. Such amount is in addition of previous lump sum amount. Taxpayer have to pay

amount of tax as per inducement to enter into contract. Through which they are able to

provide services in future with the help of establishment of nexus as well as try to

making it ordinary income. Section 15 – 2 is the relevant law which consists sufficient

facts to deny with the amount of 4,00,000 dollars which is considered ordinary income.

This amount has been considered as statutory income in section 15 – 2 if it constitute a

benefit etc. which is in the respect of services. With the case of Smith v FCT (1987) 19

ATR 274 it has been stated that suggestion must be discussed which provide nexus test

under section 15-2 which is easier to meet section 6-5. At this point of time such

payments must be considered as inducement in order to enter into employement

contract which would be arise in future services.

In accordance with rules of taxation act 1936, 1,00,000 dollar annual salary is

clearly considered as ordinary income on the basis of clear nexus through services

6 Wang, J., Ayres, H. and Huyton, J., 2010. Is tourism education meeting the

needs of the tourism industry? An Australian case study. Journal of Hospitality &

Tourism Education. 22(1). pp.8-14.

1

provided. Such receipt of amount shows large number of indicia of income such as

regular, nexus which is related with personal services and much more. On the other

hand, 4,00,000 dollar has been taxable according to the regulation.

On the the basis of section 6(1) of Income Tax Assessment Act 1936, income of

resident person has been considered as taxable if it is equal to the rate of tax

mentioned under rule. As individuals are responsible to pay tax equal to amount

mentioned under law with in stipulated time period as mentioned law. As they have to

follow rules, policies and procedure which are imposed on them.

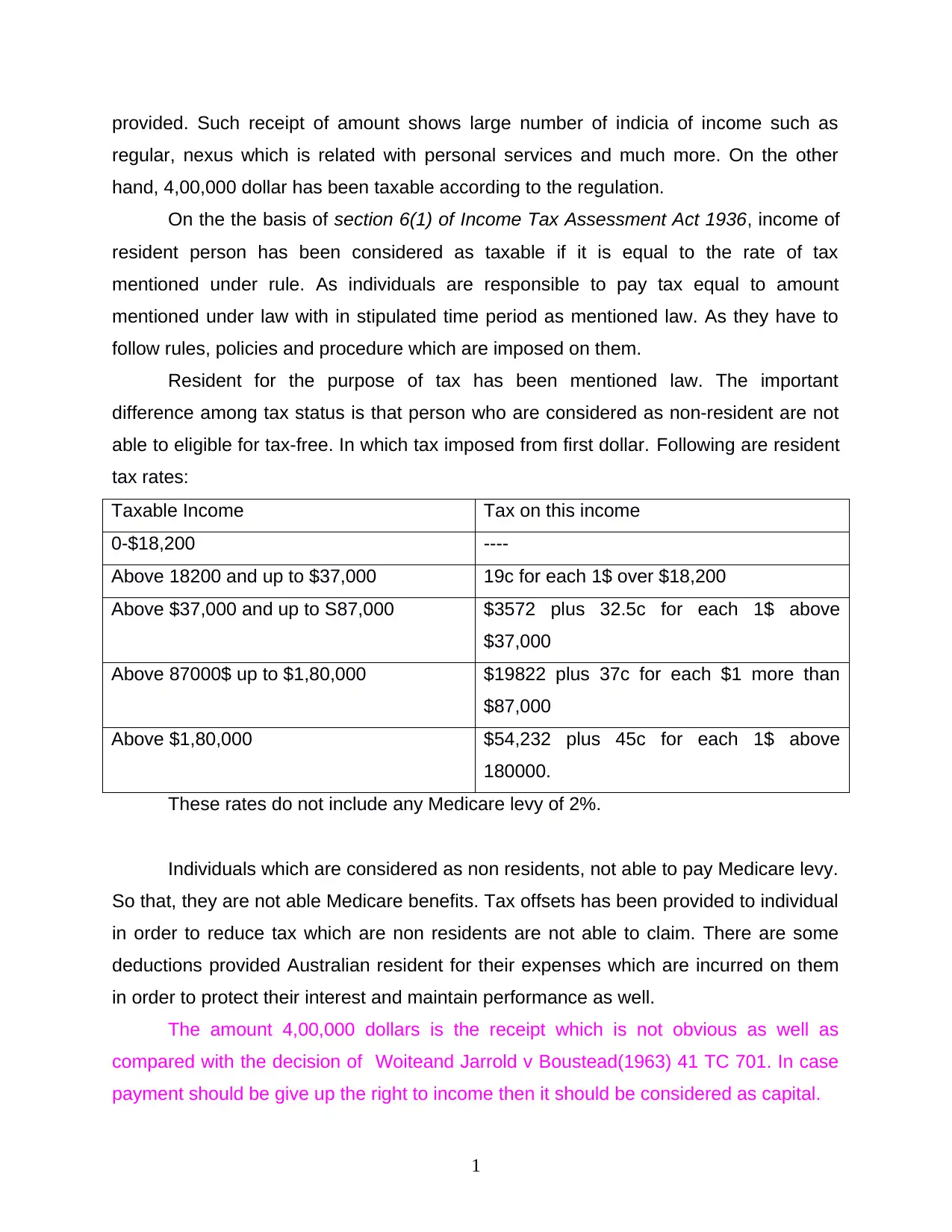

Resident for the purpose of tax has been mentioned law. The important

difference among tax status is that person who are considered as non-resident are not

able to eligible for tax-free. In which tax imposed from first dollar. Following are resident

tax rates:

Taxable Income Tax on this income

0-$18,200 ----

Above 18200 and up to $37,000 19c for each 1$ over $18,200

Above $37,000 and up to S87,000 $3572 plus 32.5c for each 1$ above

$37,000

Above 87000$ up to $1,80,000 $19822 plus 37c for each $1 more than

$87,000

Above $1,80,000 $54,232 plus 45c for each 1$ above

180000.

These rates do not include any Medicare levy of 2%.

Individuals which are considered as non residents, not able to pay Medicare levy.

So that, they are not able Medicare benefits. Tax offsets has been provided to individual

in order to reduce tax which are non residents are not able to claim. There are some

deductions provided Australian resident for their expenses which are incurred on them

in order to protect their interest and maintain performance as well.

The amount 4,00,000 dollars is the receipt which is not obvious as well as

compared with the decision of Woiteand Jarrold v Boustead(1963) 41 TC 701. In case

payment should be give up the right to income then it should be considered as capital.

1

regular, nexus which is related with personal services and much more. On the other

hand, 4,00,000 dollar has been taxable according to the regulation.

On the the basis of section 6(1) of Income Tax Assessment Act 1936, income of

resident person has been considered as taxable if it is equal to the rate of tax

mentioned under rule. As individuals are responsible to pay tax equal to amount

mentioned under law with in stipulated time period as mentioned law. As they have to

follow rules, policies and procedure which are imposed on them.

Resident for the purpose of tax has been mentioned law. The important

difference among tax status is that person who are considered as non-resident are not

able to eligible for tax-free. In which tax imposed from first dollar. Following are resident

tax rates:

Taxable Income Tax on this income

0-$18,200 ----

Above 18200 and up to $37,000 19c for each 1$ over $18,200

Above $37,000 and up to S87,000 $3572 plus 32.5c for each 1$ above

$37,000

Above 87000$ up to $1,80,000 $19822 plus 37c for each $1 more than

$87,000

Above $1,80,000 $54,232 plus 45c for each 1$ above

180000.

These rates do not include any Medicare levy of 2%.

Individuals which are considered as non residents, not able to pay Medicare levy.

So that, they are not able Medicare benefits. Tax offsets has been provided to individual

in order to reduce tax which are non residents are not able to claim. There are some

deductions provided Australian resident for their expenses which are incurred on them

in order to protect their interest and maintain performance as well.

The amount 4,00,000 dollars is the receipt which is not obvious as well as

compared with the decision of Woiteand Jarrold v Boustead(1963) 41 TC 701. In case

payment should be give up the right to income then it should be considered as capital.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Person who is bound to pay tax needs to receive some knowledge about

payment of tax. They have to calculate their own income in order to pay tax. Information

related to tax has been received from legal advisors and have to pay tax accordingly.

Try to follow all rules and policies which are imposed on them. Also receive knowledge

of exemption which are provide by legal rules to tax payer. But exemption is based on

situation of condition of income of person 7. Residential status must be determine on the

basis of time which they spend in particular company. There are various types of rules

mentioned under legal document which are related to payment of tax. On the other

hand, citizenship as well as nationality of person is not able to determine or evaluate

liability for income tax of country Australia as it is calculated by taxable income. But

citizen is able to determine residential status of person and also evaluate in which

country his income has been taxable. In the case of Deputy Commissioner of Taxation

v. Nugawela, order to court were held that order which has been stay by registrar is

dismissed on the basis of that application were stay due to interim of respondents 8.

CONCLUSION

From the above report, it has been depicted that person who complete 183 days

or more in previous year then he is considered as resident of Australia. It is essential for

person to complete specified days in country in order to fulfil the requirement of law

which are stated by government. Income which is considered as ordinary income on

which tax needs to be paid by tax payer. Citizen of person needs to be calculated on the

basis of their stay period in order to consider taxable their income. It is not determine for

the purpose of evaluate liability.

7 Wang, J., Ayres, H. and Huyton, J., 2010. Is tourism education meeting the

needs of the tourism industry? An Australian case study. Journal of Hospitality &

Tourism Education. 22(1). pp.8-14.

8 Subedi, S.P., 2016. International investment law: reconciling policy and

principle. Bloomsbury Publishing.

1

payment of tax. They have to calculate their own income in order to pay tax. Information

related to tax has been received from legal advisors and have to pay tax accordingly.

Try to follow all rules and policies which are imposed on them. Also receive knowledge

of exemption which are provide by legal rules to tax payer. But exemption is based on

situation of condition of income of person 7. Residential status must be determine on the

basis of time which they spend in particular company. There are various types of rules

mentioned under legal document which are related to payment of tax. On the other

hand, citizenship as well as nationality of person is not able to determine or evaluate

liability for income tax of country Australia as it is calculated by taxable income. But

citizen is able to determine residential status of person and also evaluate in which

country his income has been taxable. In the case of Deputy Commissioner of Taxation

v. Nugawela, order to court were held that order which has been stay by registrar is

dismissed on the basis of that application were stay due to interim of respondents 8.

CONCLUSION

From the above report, it has been depicted that person who complete 183 days

or more in previous year then he is considered as resident of Australia. It is essential for

person to complete specified days in country in order to fulfil the requirement of law

which are stated by government. Income which is considered as ordinary income on

which tax needs to be paid by tax payer. Citizen of person needs to be calculated on the

basis of their stay period in order to consider taxable their income. It is not determine for

the purpose of evaluate liability.

7 Wang, J., Ayres, H. and Huyton, J., 2010. Is tourism education meeting the

needs of the tourism industry? An Australian case study. Journal of Hospitality &

Tourism Education. 22(1). pp.8-14.

8 Subedi, S.P., 2016. International investment law: reconciling policy and

principle. Bloomsbury Publishing.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Bartel, R. and Barclay, E., 2011. Motivational postures and compliance with

environmental law in Australian agriculture. Journal of Rural Studies. 27(2).

pp.153-170.

Brilmayer, L., 2010. The New Extraterritoriality: Morrison v. National Australia Bank,

Legislative Supremacy, and the Presumption Against Extraterritorial Application

of American Law. Sw. L. Rev.. 40. p.655.

Crawford, J., 2012. Brownlie's principles of public international law. Oxford University

Press.

Dolzer, R. and Schreuer, C., 2012. Principles of international investment law. Oxford

University Press.

Du Plessis, J.J., Hargovan, A. and Bagaric, M., 2010. Principles of contemporary

corporate governance. Cambridge University Press.

Gitman, L.J., Juchau, R. and Flanagan, J., 2015. Principles of managerial finance.

Pearson Higher Education AU.

Gurran, N., 2011. Australian urban land use planning: Principles, systems and practice.

Sydney University Press.

Subedi, S.P., 2016. International investment law: reconciling policy and principle.

Bloomsbury Publishing.

Tricker, R.B. and Tricker, R.I., 2015. Corporate governance: Principles, policies, and

practices. Oxford University Press, USA.

Wang, J., Ayres, H. and Huyton, J., 2010. Is tourism education meeting the needs of the

tourism industry? An Australian case study. Journal of Hospitality & Tourism

Education. 22(1). pp.8-14.

Online

PRINCIPLES OF TAXATION LAW 2017. 2017. [Online]. Available through:

<https://studentvip.com.au/textbooks/isbn/9780455239309>. [Accessed on 19th August

2017].

1

Books and Journals

Bartel, R. and Barclay, E., 2011. Motivational postures and compliance with

environmental law in Australian agriculture. Journal of Rural Studies. 27(2).

pp.153-170.

Brilmayer, L., 2010. The New Extraterritoriality: Morrison v. National Australia Bank,

Legislative Supremacy, and the Presumption Against Extraterritorial Application

of American Law. Sw. L. Rev.. 40. p.655.

Crawford, J., 2012. Brownlie's principles of public international law. Oxford University

Press.

Dolzer, R. and Schreuer, C., 2012. Principles of international investment law. Oxford

University Press.

Du Plessis, J.J., Hargovan, A. and Bagaric, M., 2010. Principles of contemporary

corporate governance. Cambridge University Press.

Gitman, L.J., Juchau, R. and Flanagan, J., 2015. Principles of managerial finance.

Pearson Higher Education AU.

Gurran, N., 2011. Australian urban land use planning: Principles, systems and practice.

Sydney University Press.

Subedi, S.P., 2016. International investment law: reconciling policy and principle.

Bloomsbury Publishing.

Tricker, R.B. and Tricker, R.I., 2015. Corporate governance: Principles, policies, and

practices. Oxford University Press, USA.

Wang, J., Ayres, H. and Huyton, J., 2010. Is tourism education meeting the needs of the

tourism industry? An Australian case study. Journal of Hospitality & Tourism

Education. 22(1). pp.8-14.

Online

PRINCIPLES OF TAXATION LAW 2017. 2017. [Online]. Available through:

<https://studentvip.com.au/textbooks/isbn/9780455239309>. [Accessed on 19th August

2017].

1

Nugawela v Deputy Commissioner of Taxation (2016) FCA 578 <https://jade.io/j/?

a=outline&id=478315>

MALLALIEU V DRUMMOND: HL 27 JUL (1983) <http://swarb.co.uk/mallalieu-v-

drummond-hl-27-jul-1983/>

1

a=outline&id=478315>

MALLALIEU V DRUMMOND: HL 27 JUL (1983) <http://swarb.co.uk/mallalieu-v-

drummond-hl-27-jul-1983/>

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.