Taxation Law Assignment - Assessment of Tax Liability for Individuals

VerifiedAdded on 2020/03/16

|11

|1743

|145

Homework Assignment

AI Summary

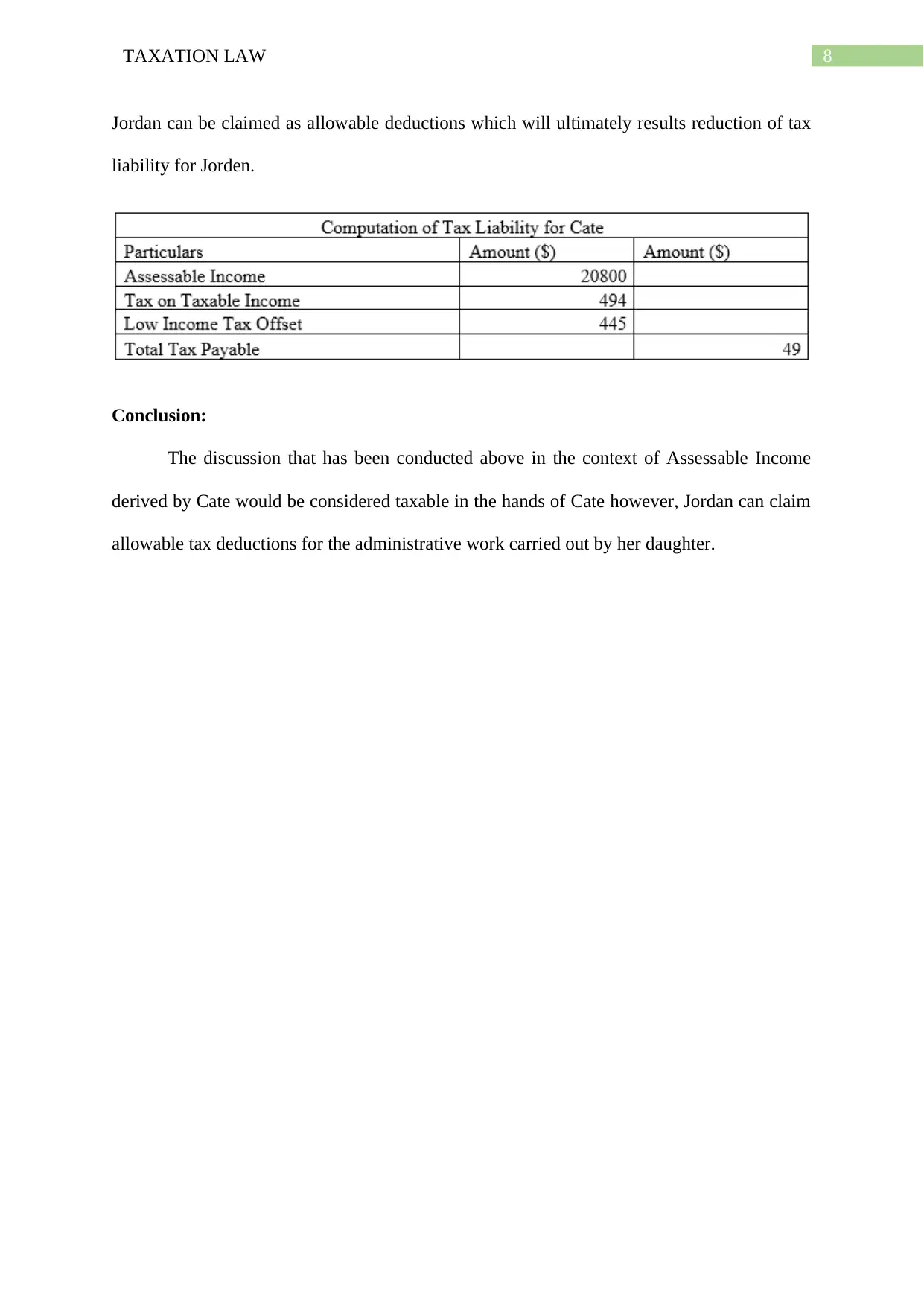

This taxation law assignment analyzes the tax liabilities of Jordan, Cameron, and Cate, focusing on income, deductions, and relevant tax rulings in Australia. The assignment addresses the assessable income of Jordan and Cameron, including salary, fringe benefits, and rental income, considering the implications of the ITAA 1997. It examines allowable deductions such as work-related expenses, interest on investment properties, and the non-deductibility of child care and private living expenses. The assignment also explores the tax implications for Cate, a minor, and the deductibility of expenses related to employing her for administrative work. The analysis considers various cases and rulings, including Hayley v. FC of T, Jayatilake v FC of T, and IT 2489, to determine the tax liabilities and permissible deductions. The assignment provides a comprehensive overview of Australian taxation law, covering key concepts such as assessable income, allowable deductions, and the application of relevant tax legislation.

1 out of 11

Related Documents

![Taxation Law: Spriggs v Federal Commissioner of Taxation [2007]](/_next/image/?url=https%3A%2F%2Fdesklib.com%2Fmedia%2Fdocument%2Fpages%2Fspriggs-taxation-law-case-page-2.jpg&w=256&q=75)

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.