Australian Taxation Law: Deductions, GST, and Case Analysis

VerifiedAdded on 2019/11/20

|17

|2908

|261

Homework Assignment

AI Summary

This assignment solution delves into key aspects of Australian Taxation Law, analyzing various scenarios related to permissible deductions and GST implications. The document addresses issues such as whether the cost of relocating machinery is a deductible expense, the eligibility of costs incurred in revaluing assets for insurance purposes, the deductibility of legal expenditures in opposing a winding-up petition, and the tax treatment of legal expenses for business clients. The solution also examines the input tax credit for a company's advertisement expenditures, considering relevant legislation, case law, and taxation rulings, including the GST Act 1999 and the GSTR 2006/3 ruling. The analysis incorporates the application of legal principles and case precedents to provide a comprehensive understanding of the tax implications in each situation, concluding whether the expenses qualify as permissible deductions or input tax credits under Australian tax law.

Running head: AUSTRALIAN TAXATION LAW

Australian Taxation Law

Name of the Student

Name of the University

Student ID

Author Note

Australian Taxation Law

Name of the Student

Name of the University

Student ID

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUSTRALIAN TAXATION LAW

Table of Contents

Answer to Question 1:.....................................................................................................................2

Answer 1:.....................................................................................................................................2

Issue:........................................................................................................................................2

Legislations:.............................................................................................................................2

Application:.............................................................................................................................2

Conclusion:..............................................................................................................................3

Answer 2:.....................................................................................................................................3

Issue:........................................................................................................................................3

Legislation:..............................................................................................................................3

Application:.............................................................................................................................3

Conclusion:..............................................................................................................................4

Answer 3:.....................................................................................................................................4

Issue:........................................................................................................................................4

Legislation:..............................................................................................................................4

Application:.............................................................................................................................5

Answer 4:.....................................................................................................................................5

Issue:........................................................................................................................................5

Legislations:.............................................................................................................................6

Application:.............................................................................................................................6

Conclusion:..............................................................................................................................6

Table of Contents

Answer to Question 1:.....................................................................................................................2

Answer 1:.....................................................................................................................................2

Issue:........................................................................................................................................2

Legislations:.............................................................................................................................2

Application:.............................................................................................................................2

Conclusion:..............................................................................................................................3

Answer 2:.....................................................................................................................................3

Issue:........................................................................................................................................3

Legislation:..............................................................................................................................3

Application:.............................................................................................................................3

Conclusion:..............................................................................................................................4

Answer 3:.....................................................................................................................................4

Issue:........................................................................................................................................4

Legislation:..............................................................................................................................4

Application:.............................................................................................................................5

Answer 4:.....................................................................................................................................5

Issue:........................................................................................................................................5

Legislations:.............................................................................................................................6

Application:.............................................................................................................................6

Conclusion:..............................................................................................................................6

2AUSTRALIAN TAXATION LAW

Answer to Question 2:.....................................................................................................................7

Issue:............................................................................................................................................7

Legislation:..................................................................................................................................7

Application:.................................................................................................................................7

Conclusion:..................................................................................................................................9

Answer to Question 3:...................................................................................................................10

Answer to Question 4:...................................................................................................................12

References......................................................................................................................................13

Answer to Question 2:.....................................................................................................................7

Issue:............................................................................................................................................7

Legislation:..................................................................................................................................7

Application:.................................................................................................................................7

Conclusion:..................................................................................................................................9

Answer to Question 3:...................................................................................................................10

Answer to Question 4:...................................................................................................................12

References......................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUSTRALIAN TAXATION LAW

Answer to Question 1:

Answer 1:

Issue:

In the concerned issue, it is taken into account as to whether the cost which is incurred by

an enterprise to move its machinery from one site to operation to a new site, shall be considered

as permissible deductions with respect to the “section 8-1 of the ITAA 1997”.

Legislations:

a. “Section 8-1 of the Income Tax Assessment Act 1997”

b. “British Insulated & Helsby Cables”

Application:

As considered under the “section 8-1 of the ITAA 1997”, the expenditures of the firms,

which are incurred by the organization, in order to relocate its machinery from one site to

another site are in general in the form of capital expenditures and therefore, these type of

expenditures are not eligible for deductions. However, if the purpose of depreciation is taken,

then the relocation of machineries to another site increases the cost of asset. The costs of moving

machineries, which represents that type of cost, which occurs from the small changes, are

allowed as deductions under the same section. The reason behind this consideration of the

expenses as permissible deductions is that these are parts of business expenditures, which occur

in daily commercial activities (Ato.gov.au, 2017).

In this context, the case verdict of the “British Insulated & Helsby Cables”, can be taken

into account. According to this case study, the cost of transporting of the machineries is a

representation of benefits in the commercial premises, which occurs due to the relocation of the

Answer to Question 1:

Answer 1:

Issue:

In the concerned issue, it is taken into account as to whether the cost which is incurred by

an enterprise to move its machinery from one site to operation to a new site, shall be considered

as permissible deductions with respect to the “section 8-1 of the ITAA 1997”.

Legislations:

a. “Section 8-1 of the Income Tax Assessment Act 1997”

b. “British Insulated & Helsby Cables”

Application:

As considered under the “section 8-1 of the ITAA 1997”, the expenditures of the firms,

which are incurred by the organization, in order to relocate its machinery from one site to

another site are in general in the form of capital expenditures and therefore, these type of

expenditures are not eligible for deductions. However, if the purpose of depreciation is taken,

then the relocation of machineries to another site increases the cost of asset. The costs of moving

machineries, which represents that type of cost, which occurs from the small changes, are

allowed as deductions under the same section. The reason behind this consideration of the

expenses as permissible deductions is that these are parts of business expenditures, which occur

in daily commercial activities (Ato.gov.au, 2017).

In this context, the case verdict of the “British Insulated & Helsby Cables”, can be taken

into account. According to this case study, the cost of transporting of the machineries is a

representation of benefits in the commercial premises, which occurs due to the relocation of the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUSTRALIAN TAXATION LAW

depreciable assets. As can be seen with respect to “Taxation Ruling of TD 93/126”, the cost of

relocation or movement of the machineries by any company and the installation of the same for

commercial purposes and the cost to bring these machineries in operation is considered to be

under revenue (Frecknall-Hughes, 2014) . As can be seen from the above discussion, in the

present case scenario, as the cost of shifting the machineries by the concerned enterprise, falls in

the category of capital expenditure, therefore, the same will not be considered as a permissible

deduction under the “section 8-1 of the ITAA 1997”.

Conclusion:

Therefore, it can be concluded that in the present scenario, the cost, which is incurred by

the company, in moving their machineries from one site to a new site, is of the nature of capital

expenditure and therefore, these expenses will not be considered permissible deductions under

the section 8-1 of the Income Tax Assessment Act 1997.

Answer 2:

Issue:

In this situation, the issue of the eligibility of those costs, which are incurred in revaluing

assets to affect the cover of insurance, as the permissible deductions under the section 8-1 of the

Income Tax Assessment Act 1997.

Legislation:

a. “ Section 8-1 of the Income Tax Assessment Act 1997”

Application:

The expenditures in the concerned scenario, as can be derived from the above discussion,

is seen to be associated with the fixed form of assets. In this context, therefore, it is necessary to

depreciable assets. As can be seen with respect to “Taxation Ruling of TD 93/126”, the cost of

relocation or movement of the machineries by any company and the installation of the same for

commercial purposes and the cost to bring these machineries in operation is considered to be

under revenue (Frecknall-Hughes, 2014) . As can be seen from the above discussion, in the

present case scenario, as the cost of shifting the machineries by the concerned enterprise, falls in

the category of capital expenditure, therefore, the same will not be considered as a permissible

deduction under the “section 8-1 of the ITAA 1997”.

Conclusion:

Therefore, it can be concluded that in the present scenario, the cost, which is incurred by

the company, in moving their machineries from one site to a new site, is of the nature of capital

expenditure and therefore, these expenses will not be considered permissible deductions under

the section 8-1 of the Income Tax Assessment Act 1997.

Answer 2:

Issue:

In this situation, the issue of the eligibility of those costs, which are incurred in revaluing

assets to affect the cover of insurance, as the permissible deductions under the section 8-1 of the

Income Tax Assessment Act 1997.

Legislation:

a. “ Section 8-1 of the Income Tax Assessment Act 1997”

Application:

The expenditures in the concerned scenario, as can be derived from the above discussion,

is seen to be associated with the fixed form of assets. In this context, therefore, it is necessary to

5AUSTRALIAN TAXATION LAW

analyze whether the expenses, which are occurring for revaluing the assets, are being done only

for the protection of the assets or are done with the purpose of increasing the capacity of revenue

production (Oats, 2012). In case of the former one, if the benefits of temporary nature occur,

provided the expenditures are of repetitive type, then these costs will be eligible to be considered

as deductions under the “section 8-1 of the Income Tax Assessment Act 1997”.

Therefore, in the present scenario, as the cost incurred for the revaluation of the assets to

effect cover of insurance, is of repetitive in nature in all probabilities and therefore, it will be

considered as allowable deduction under the “section 8-1 of the Income Tax Assessment Act

1997” (Ato.gov.au, 2017) .

Conclusion:

It can be therefore, concluded that the above mentioned cost of insurance cover, being

probably recurring in nature, shall be eligible to be considered as permissible deduction under

the same section of ITAA 1997.

Answer 3:

Issue:

The issue in this scenario is to analyze the eligibility of the legal expenditures, which are

incurred by a company to oppose the winding up petition, as a permissible deduction, with

respect to the “section 8-1 of the ITAA 1997”.

Legislation:

a. “Section 8-1 of the Income Tax Assessment Act 1997”

b. “FC of T v Snowden and Wilson Pty Ltd (1958) 99 CLR 431)”

analyze whether the expenses, which are occurring for revaluing the assets, are being done only

for the protection of the assets or are done with the purpose of increasing the capacity of revenue

production (Oats, 2012). In case of the former one, if the benefits of temporary nature occur,

provided the expenditures are of repetitive type, then these costs will be eligible to be considered

as deductions under the “section 8-1 of the Income Tax Assessment Act 1997”.

Therefore, in the present scenario, as the cost incurred for the revaluation of the assets to

effect cover of insurance, is of repetitive in nature in all probabilities and therefore, it will be

considered as allowable deduction under the “section 8-1 of the Income Tax Assessment Act

1997” (Ato.gov.au, 2017) .

Conclusion:

It can be therefore, concluded that the above mentioned cost of insurance cover, being

probably recurring in nature, shall be eligible to be considered as permissible deduction under

the same section of ITAA 1997.

Answer 3:

Issue:

The issue in this scenario is to analyze the eligibility of the legal expenditures, which are

incurred by a company to oppose the winding up petition, as a permissible deduction, with

respect to the “section 8-1 of the ITAA 1997”.

Legislation:

a. “Section 8-1 of the Income Tax Assessment Act 1997”

b. “FC of T v Snowden and Wilson Pty Ltd (1958) 99 CLR 431)”

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUSTRALIAN TAXATION LAW

Application:

The costs which are generally incurred by the business organizations in winding up their

business are normally categorized under the business operations of the concerned organizations

and are therefore, are not considered as allowable deductions, under the “section 8-1 of the

Income Tax Assessment Act 1997”. However, as the “taxation ruling of ID 2004/367”

suggests, the legal costs, which are incurred in business operations, which in turn enables the

concerned company or individual to produce taxable proceeds, shall be considered for

permissible deductions (Mellon, 2016).

The case reference of “FC of T v Snowden and Wilson Pty Ltd (1958)” is being

considered in this context. According to the verdict, in case of unusual expenses the taxpayers do

not need to commence that of the lawful actions as this does not prevent the expenditure to get

eligible to be considered as deductible ones (Barkoczy, 2016).

In this context, therefore, the legal expenses of the organization, which has to be incurred

by the company, to oppose the winding up petition, shall not be allowed to be considered as

permissible deductions as the expenses fall under the domain of capital expenditures and the

expenditures are related to the commercial operations of the company (Fleurbaey & Maniquet,

2015).

Application:

The costs which are generally incurred by the business organizations in winding up their

business are normally categorized under the business operations of the concerned organizations

and are therefore, are not considered as allowable deductions, under the “section 8-1 of the

Income Tax Assessment Act 1997”. However, as the “taxation ruling of ID 2004/367”

suggests, the legal costs, which are incurred in business operations, which in turn enables the

concerned company or individual to produce taxable proceeds, shall be considered for

permissible deductions (Mellon, 2016).

The case reference of “FC of T v Snowden and Wilson Pty Ltd (1958)” is being

considered in this context. According to the verdict, in case of unusual expenses the taxpayers do

not need to commence that of the lawful actions as this does not prevent the expenditure to get

eligible to be considered as deductible ones (Barkoczy, 2016).

In this context, therefore, the legal expenses of the organization, which has to be incurred

by the company, to oppose the winding up petition, shall not be allowed to be considered as

permissible deductions as the expenses fall under the domain of capital expenditures and the

expenditures are related to the commercial operations of the company (Fleurbaey & Maniquet,

2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUSTRALIAN TAXATION LAW

Answer 4:

Issue:

In this scenario, the issue of eligibility of the legal expenditures, which are incurred by

any company, for availing the services of a solicitor for different types of operations of the

business clients, as permissible deductions with reference to the “section 8-1 of the ITAA 1997”.

Legislations:

a. Section 8-1 of the Income Tax Assessment Act 1997

Application:

The “section 8-1 of the Income Tax Assessment Act 1997”, suggests that when a legal

expenditure, on part of the companies, occurs in the aspects of business activities which are

targeted to generate revenues, shall be eligible to be treated as that of a permissible deduction.

However, in this context, several exceptions do exist in the cost structures, which are not

included in the domain of permissible deductions for the concerned organization. The legal

expenditures incurred by the company, fall under the domain of private as well as of domestic

expenditures and these are incurred in the production of non-chargeable non-exempt proceeds

and the exempt proceeds (Stiglitz, 2014) .

The above discussion asserts that, the legal expenditures which occur on part if an

individual or a company, might not be considered to be a permissible deductions, provided that

the expenditures do not have any kind of association with the generation of the taxable type of

income. Therefore, with respect to the above discussion, in the given scenario, the legal

expenditures, which are incurred by the concerned individual, have associations with those

business activities which are in turn involved in generating taxable income and are therefore

Answer 4:

Issue:

In this scenario, the issue of eligibility of the legal expenditures, which are incurred by

any company, for availing the services of a solicitor for different types of operations of the

business clients, as permissible deductions with reference to the “section 8-1 of the ITAA 1997”.

Legislations:

a. Section 8-1 of the Income Tax Assessment Act 1997

Application:

The “section 8-1 of the Income Tax Assessment Act 1997”, suggests that when a legal

expenditure, on part of the companies, occurs in the aspects of business activities which are

targeted to generate revenues, shall be eligible to be treated as that of a permissible deduction.

However, in this context, several exceptions do exist in the cost structures, which are not

included in the domain of permissible deductions for the concerned organization. The legal

expenditures incurred by the company, fall under the domain of private as well as of domestic

expenditures and these are incurred in the production of non-chargeable non-exempt proceeds

and the exempt proceeds (Stiglitz, 2014) .

The above discussion asserts that, the legal expenditures which occur on part if an

individual or a company, might not be considered to be a permissible deductions, provided that

the expenditures do not have any kind of association with the generation of the taxable type of

income. Therefore, with respect to the above discussion, in the given scenario, the legal

expenditures, which are incurred by the concerned individual, have associations with those

business activities which are in turn involved in generating taxable income and are therefore

8AUSTRALIAN TAXATION LAW

eligible to be taken as allowable deductions under the “8-1 of the ITAA 1997” (Fleurbaey &

Maniquet, 2015).

Conclusion:

As can be concluded from the above discussion, in the current scenario, the legal

expenditures of the individual, being occurred with respect of commercial activities, which in

turn produces taxable income, are eligible to be considered as allowable deductions under the

section 8-1 of the ITAA 1997.

Answer to Question 2:

Issue:

In the current situation, the condition of the Big Bank is considered. The enterprise has

more than 50 branches with a nation-wide operational base and is also registered for the GST

purposes. The current issue is to determine the input tax credit with respect to the advertisement

expenditures of the company, which the company has already incurred, under the “GSTR Act

1999” (Hemmings & Tuske, 2015).

Legislation:

a. “ GST Act 1999”

b. “Goods and Service taxation ruling of GSTR 2006/3”

c. “subsection 15-25”

d. “paragraphs 11-5 and 15-5”

e. “Ronpibon Tin NL v. FC of T”

eligible to be taken as allowable deductions under the “8-1 of the ITAA 1997” (Fleurbaey &

Maniquet, 2015).

Conclusion:

As can be concluded from the above discussion, in the current scenario, the legal

expenditures of the individual, being occurred with respect of commercial activities, which in

turn produces taxable income, are eligible to be considered as allowable deductions under the

section 8-1 of the ITAA 1997.

Answer to Question 2:

Issue:

In the current situation, the condition of the Big Bank is considered. The enterprise has

more than 50 branches with a nation-wide operational base and is also registered for the GST

purposes. The current issue is to determine the input tax credit with respect to the advertisement

expenditures of the company, which the company has already incurred, under the “GSTR Act

1999” (Hemmings & Tuske, 2015).

Legislation:

a. “ GST Act 1999”

b. “Goods and Service taxation ruling of GSTR 2006/3”

c. “subsection 15-25”

d. “paragraphs 11-5 and 15-5”

e. “Ronpibon Tin NL v. FC of T”

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUSTRALIAN TAXATION LAW

Application:

The taxation ruling of the “GSTR 2006/3”, have the provisions for the guidelines which

are associated to the mode of operations which are appropriate to be implemented in the

determination of the input tax credit, with the administration for the changes which can be used

under the new “GST Act 1999” system of tax, by financial supplies. The taxation ruling also is

inclusive of the extent of that of the creditable purposes and the application in the actual context,

of the ruling under the divisions 11, 15 and that of 129 of the same GST Act (Huang & Liu,

2012). However, the taxation ruling, in a general framework, is applied to the units that are

eligible to taxation and are registered or are mandatorily needed to be registered to acquire

financial supplies and which surpass the threshold level of the acquisition, in financial terms and

who are eligible for input tax credit or reduced input tax credit (Law.ato.gov.au, 2017).

In the present situation, it can be seen that the Big Bank Limited has incurred an

expenditure of the amount of 1,650,000 dollars as GST, which had in it the advertisement

expenditures of the enterprise in the previous year. In this context, for the Big Bank, the taxation

ruling that falls under the “GSTR 2006/3”, is applicable for the concerned enterprise as Big

Bank becomes qualified for the input tax credit and lowered tax credit. According to the taxing

rules, the GST shall be applicable and payable for those organizations which are either registered

or are required to obtain the registration; the tax is payable for these organizations in order to

make or acquire taxable supplies (Law.ato.gov.au, 2017). Under the GST legislation, an

individual or a business unit is needed to make input tax credit claims for those supplies, which

are GST inclusive, which is import for the concerned unit. However, if the concerned individual

or unit exceeds the threshold of the financial acquisition, then in that case, the concerned unit

shall not be eligible to recover the GST as a whole and can only recover a part of it (Carling,

2015).

Application:

The taxation ruling of the “GSTR 2006/3”, have the provisions for the guidelines which

are associated to the mode of operations which are appropriate to be implemented in the

determination of the input tax credit, with the administration for the changes which can be used

under the new “GST Act 1999” system of tax, by financial supplies. The taxation ruling also is

inclusive of the extent of that of the creditable purposes and the application in the actual context,

of the ruling under the divisions 11, 15 and that of 129 of the same GST Act (Huang & Liu,

2012). However, the taxation ruling, in a general framework, is applied to the units that are

eligible to taxation and are registered or are mandatorily needed to be registered to acquire

financial supplies and which surpass the threshold level of the acquisition, in financial terms and

who are eligible for input tax credit or reduced input tax credit (Law.ato.gov.au, 2017).

In the present situation, it can be seen that the Big Bank Limited has incurred an

expenditure of the amount of 1,650,000 dollars as GST, which had in it the advertisement

expenditures of the enterprise in the previous year. In this context, for the Big Bank, the taxation

ruling that falls under the “GSTR 2006/3”, is applicable for the concerned enterprise as Big

Bank becomes qualified for the input tax credit and lowered tax credit. According to the taxing

rules, the GST shall be applicable and payable for those organizations which are either registered

or are required to obtain the registration; the tax is payable for these organizations in order to

make or acquire taxable supplies (Law.ato.gov.au, 2017). Under the GST legislation, an

individual or a business unit is needed to make input tax credit claims for those supplies, which

are GST inclusive, which is import for the concerned unit. However, if the concerned individual

or unit exceeds the threshold of the financial acquisition, then in that case, the concerned unit

shall not be eligible to recover the GST as a whole and can only recover a part of it (Carling,

2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUSTRALIAN TAXATION LAW

The doctrine of the case of “Ronpibon Tin NL v. FC of T”, can be considered in this

context, where the rule of ‘extent” and “to the extent” is used in order to analyze the GST

legislation. This is inclusive of the obligations, which adopts the appropriate and feasible

apportion method, which are practically applicable for the concerned organization. According to

the “paragraph 11-5 and 15-5”, an acquisition is credible acquisition if it is creditable wholly or

at least partially. The paragraphs also have another requirement for the acquisition to be

considered as a creditable acquisition or credible importation, according to which the purpose of

the acquisition should be for the creditable purposes. However, if the acquisitions are partially

for the creditable purposes, then the degree of the creditable purposes should be mandatorily

determined (Sadiq et al., 2012).

The subsection 15-25 views an import as creditable if it is for the creditable purpose

partially. According to the section 11-15 or 15-10, the acquisition becomes creditable if the

concerned unit supplies for the input tax credit claiming purposes.

Given the above discussion, it can be argued that the expenses of the concerned unit in

this case, that is the Big Bank, was for creditable acquisition purposes. As has been mentioned in

the “GSTR ruling of 2006/3”, the enterprise has exceeded its threshold and therefore, the invoice

of the company will be considered for the credits of input tax for those GST inclusive supplies

(Eccleston, 2013).

Conclusion:

From the above discussion, it can be concluded that the Big Bank, in this case, will be

considered to be permissible for claiming the input tax credit with respect to that of the GSTR

2006/13, as the expenditures, being in the form of advertising expenses, which were made for

creditable acquisition purposes.

The doctrine of the case of “Ronpibon Tin NL v. FC of T”, can be considered in this

context, where the rule of ‘extent” and “to the extent” is used in order to analyze the GST

legislation. This is inclusive of the obligations, which adopts the appropriate and feasible

apportion method, which are practically applicable for the concerned organization. According to

the “paragraph 11-5 and 15-5”, an acquisition is credible acquisition if it is creditable wholly or

at least partially. The paragraphs also have another requirement for the acquisition to be

considered as a creditable acquisition or credible importation, according to which the purpose of

the acquisition should be for the creditable purposes. However, if the acquisitions are partially

for the creditable purposes, then the degree of the creditable purposes should be mandatorily

determined (Sadiq et al., 2012).

The subsection 15-25 views an import as creditable if it is for the creditable purpose

partially. According to the section 11-15 or 15-10, the acquisition becomes creditable if the

concerned unit supplies for the input tax credit claiming purposes.

Given the above discussion, it can be argued that the expenses of the concerned unit in

this case, that is the Big Bank, was for creditable acquisition purposes. As has been mentioned in

the “GSTR ruling of 2006/3”, the enterprise has exceeded its threshold and therefore, the invoice

of the company will be considered for the credits of input tax for those GST inclusive supplies

(Eccleston, 2013).

Conclusion:

From the above discussion, it can be concluded that the Big Bank, in this case, will be

considered to be permissible for claiming the input tax credit with respect to that of the GSTR

2006/13, as the expenditures, being in the form of advertising expenses, which were made for

creditable acquisition purposes.

11AUSTRALIAN TAXATION LAW

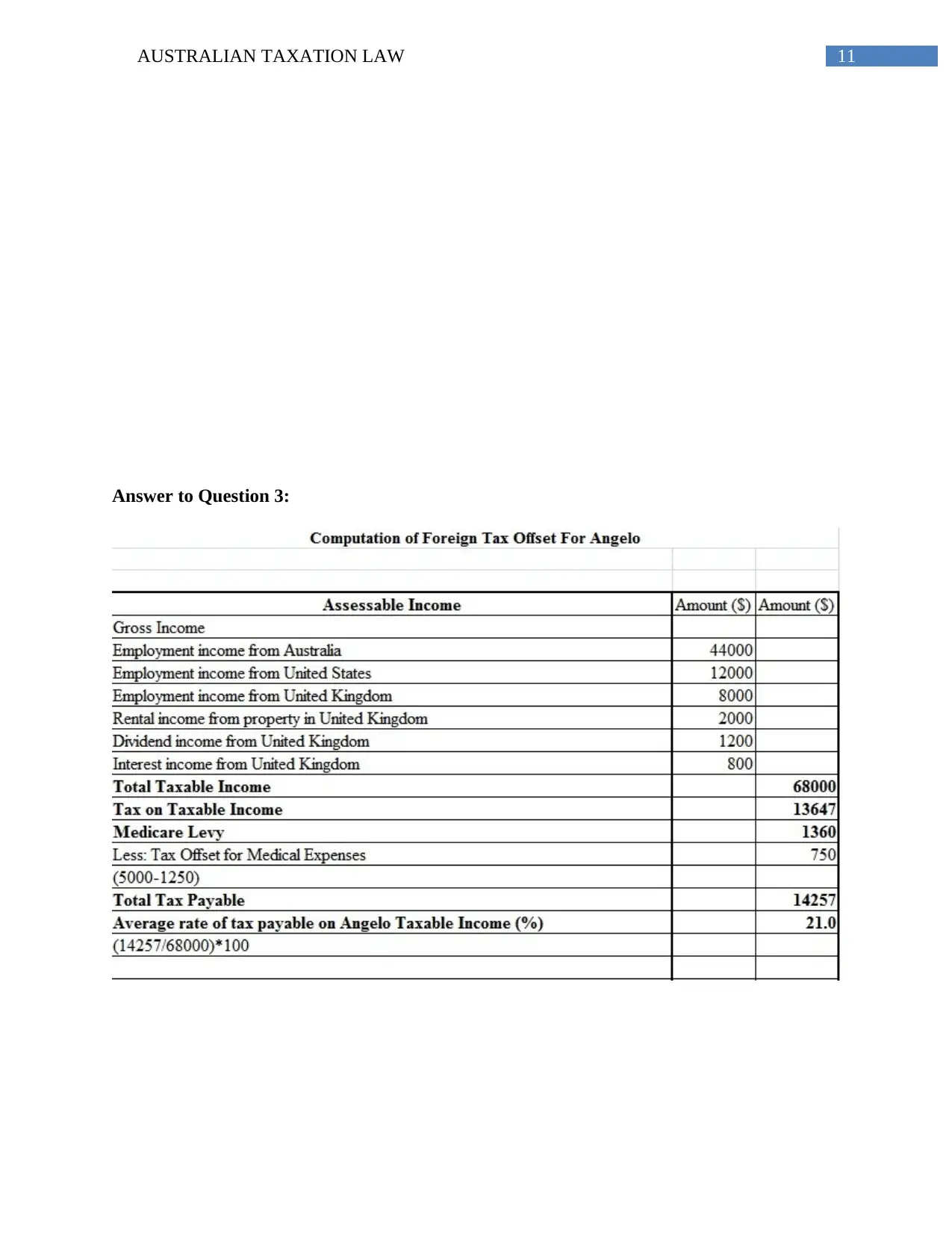

Answer to Question 3:

Answer to Question 3:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.