Griffith University BFA714: Australian Tax Law Assignment 1 Analysis

VerifiedAdded on 2022/09/29

|13

|2209

|22

Homework Assignment

AI Summary

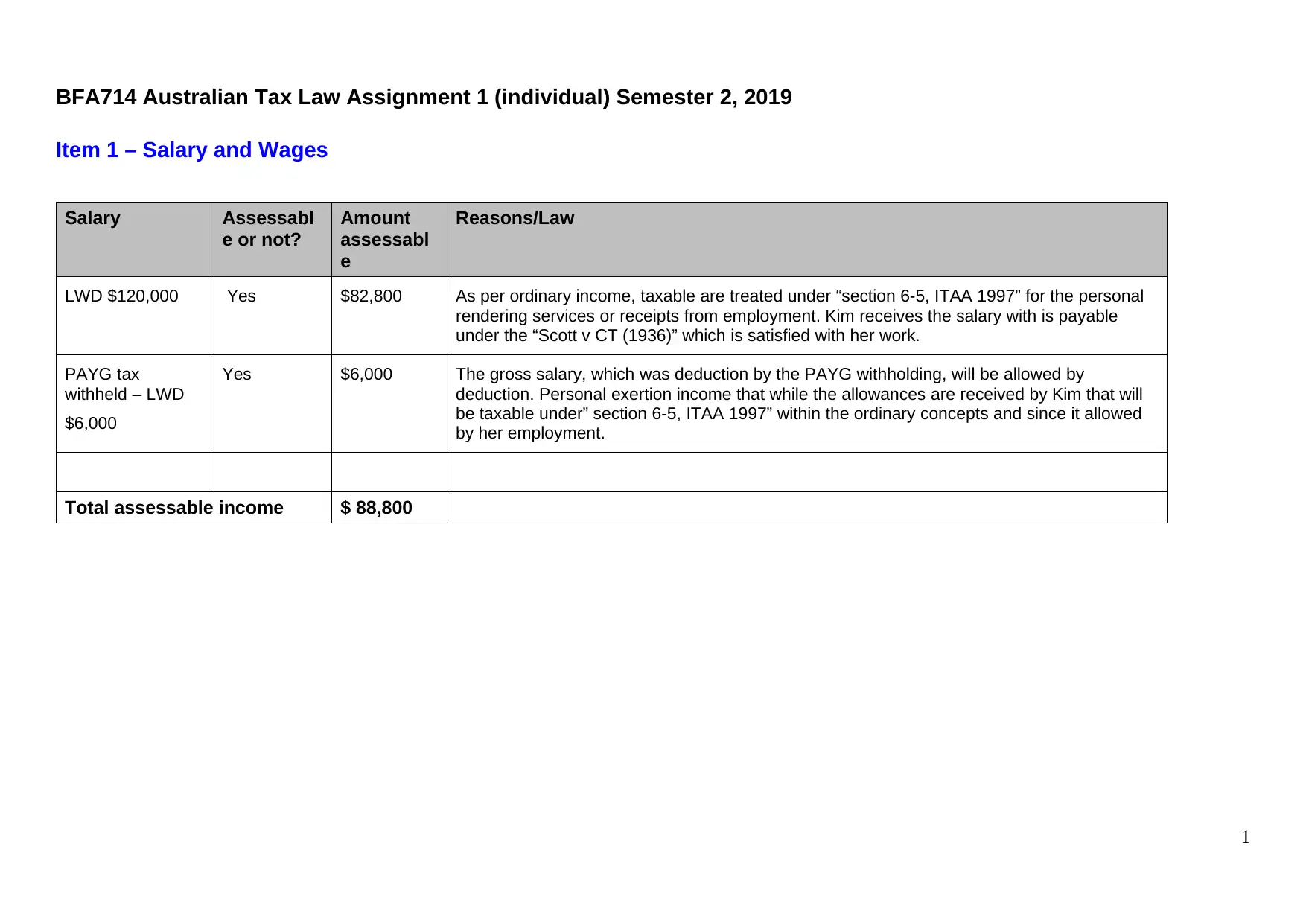

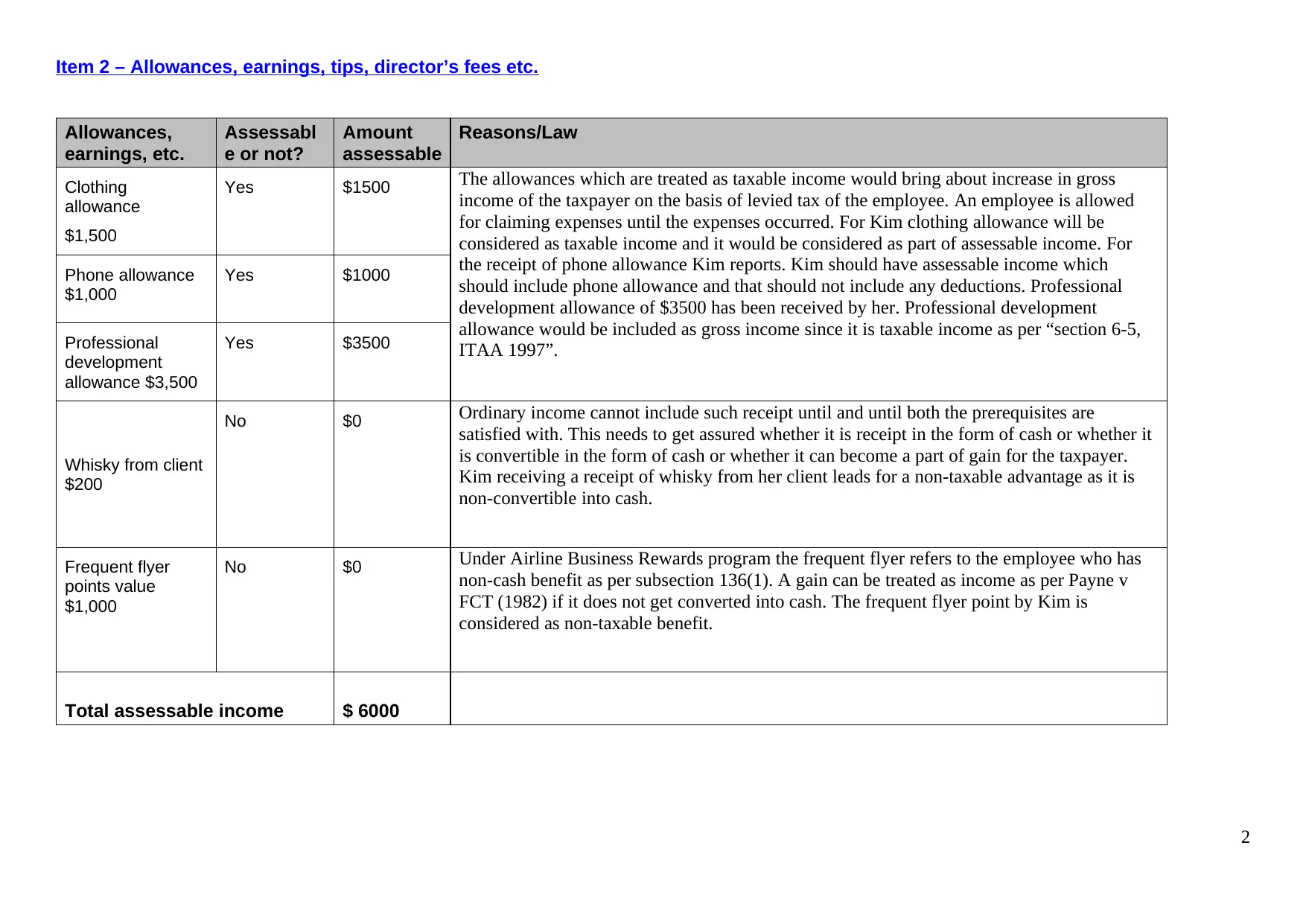

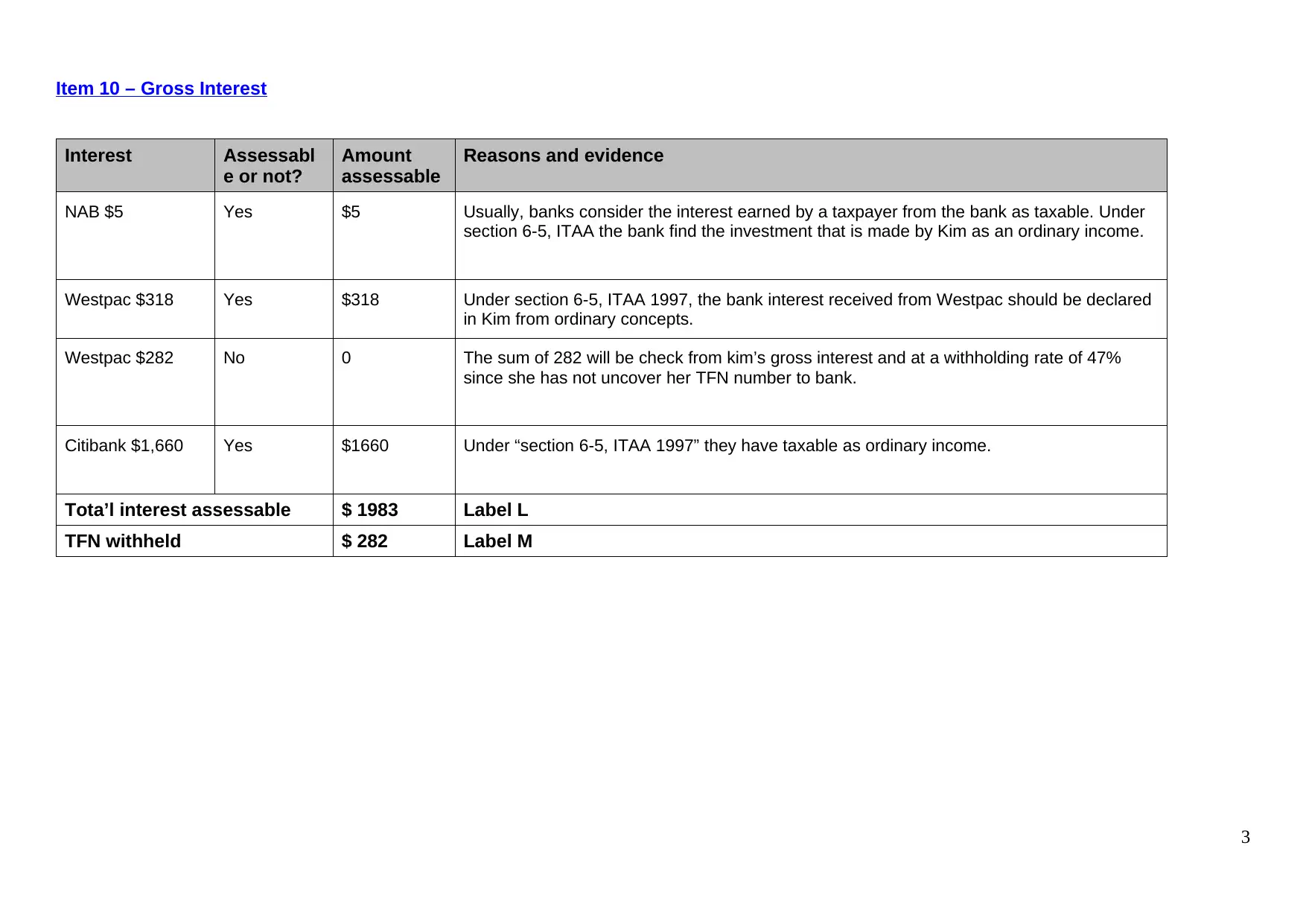

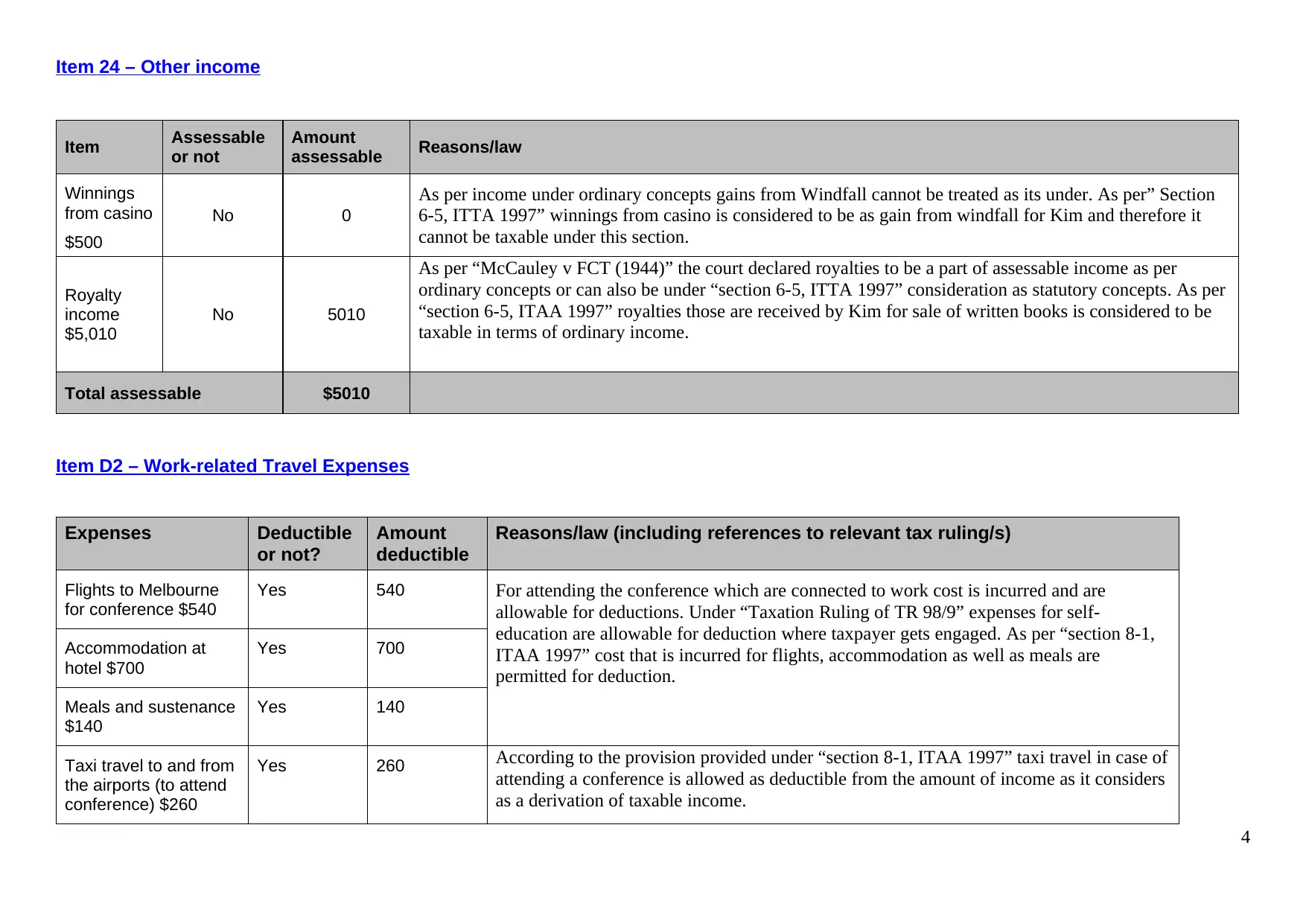

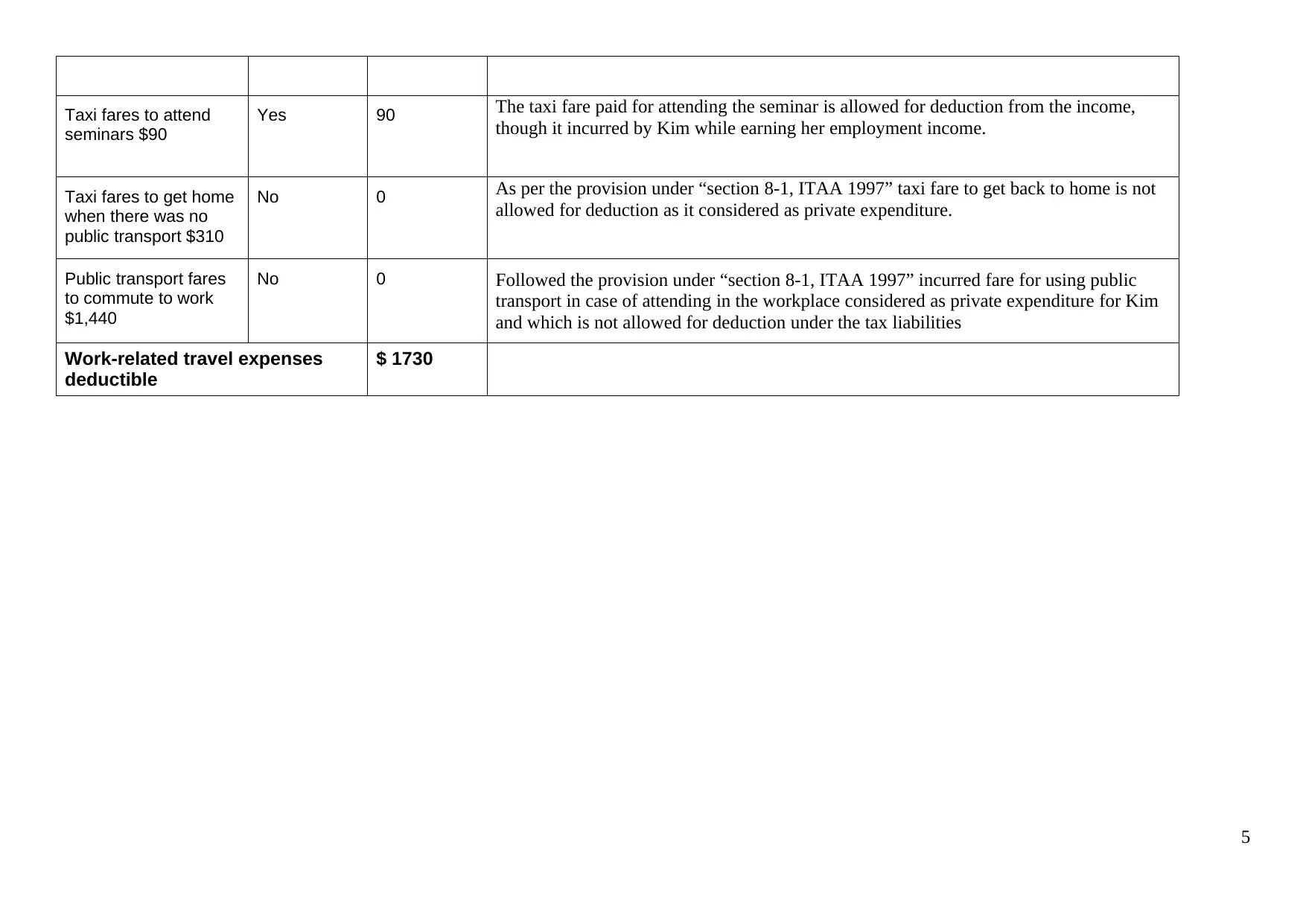

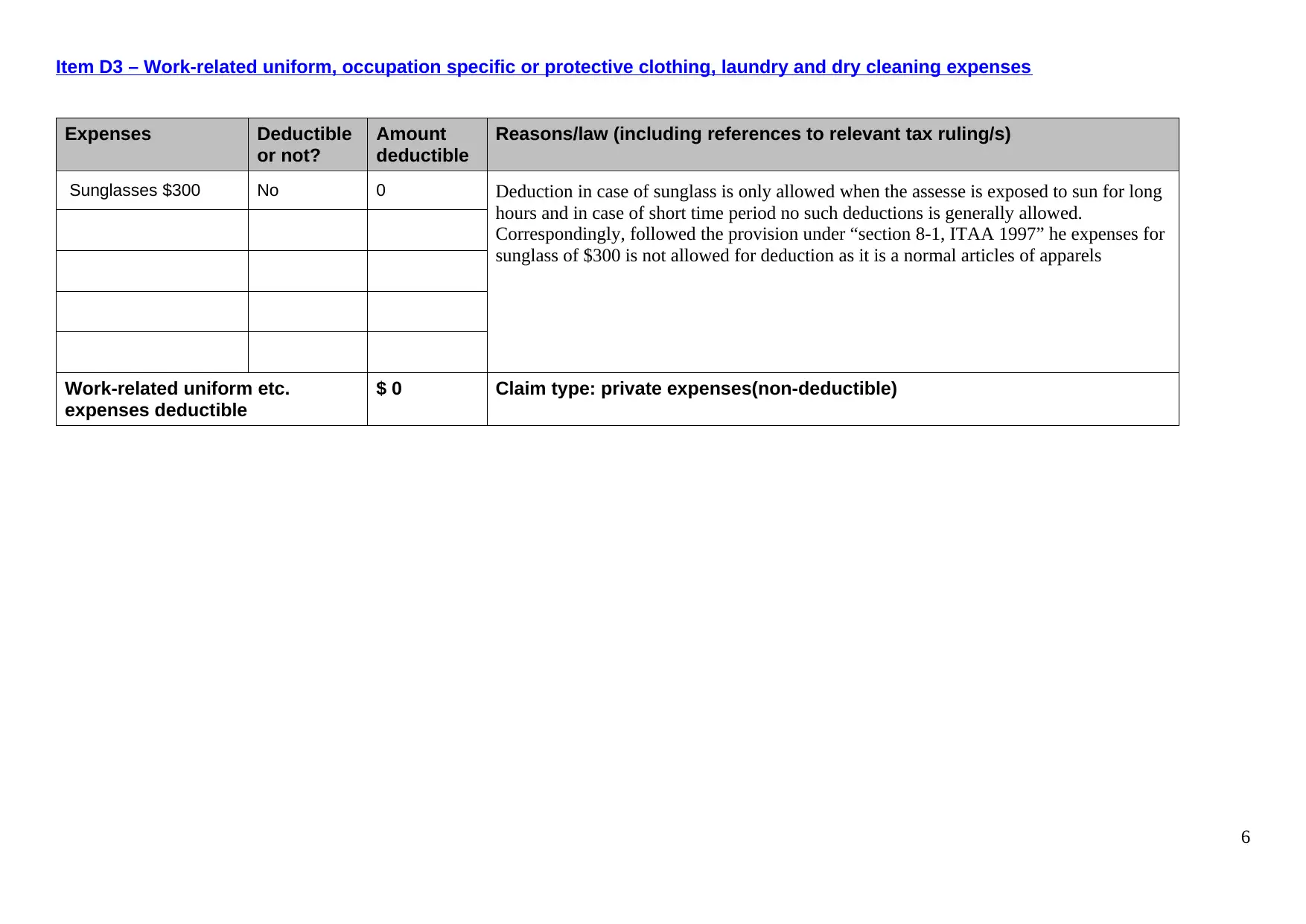

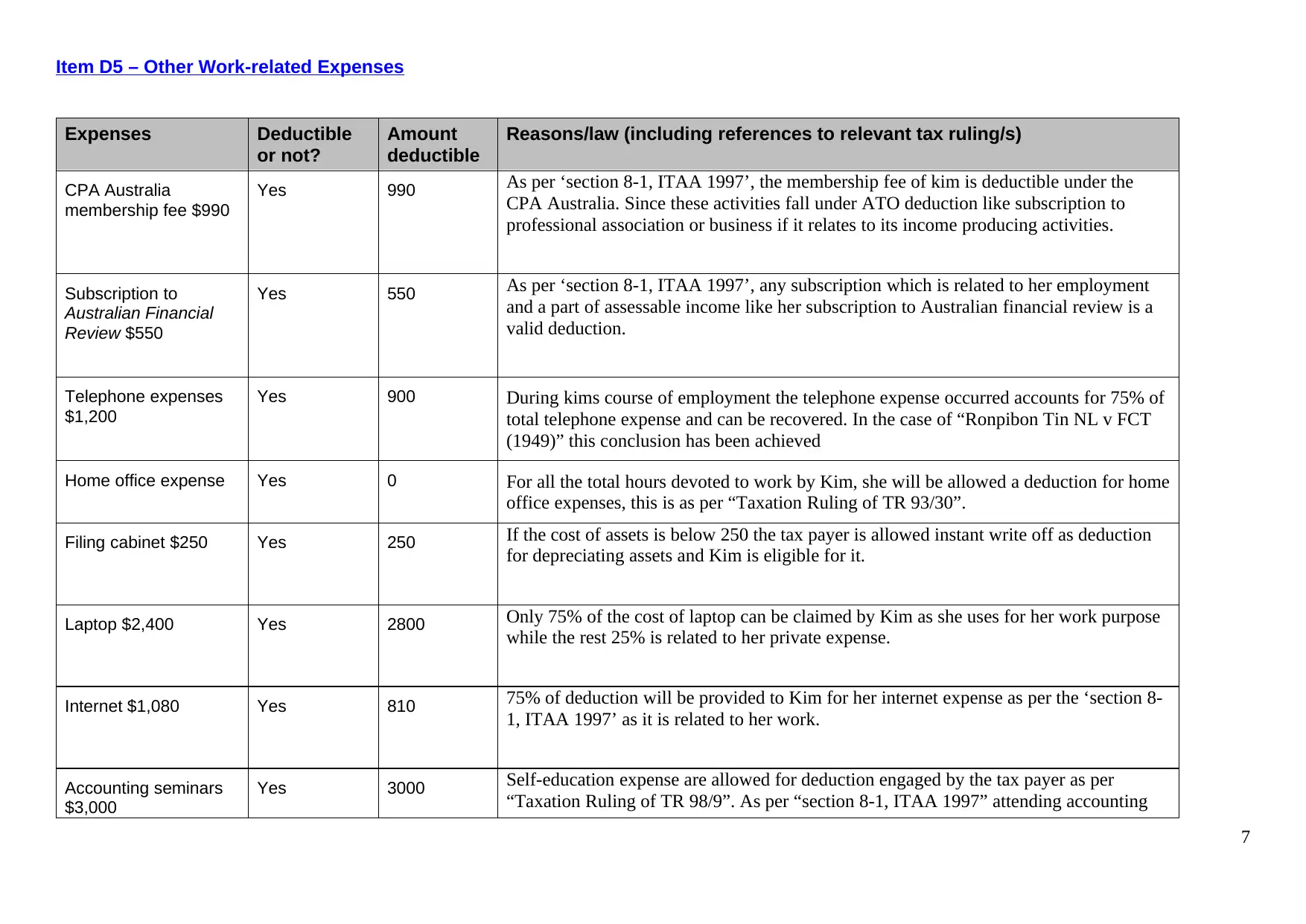

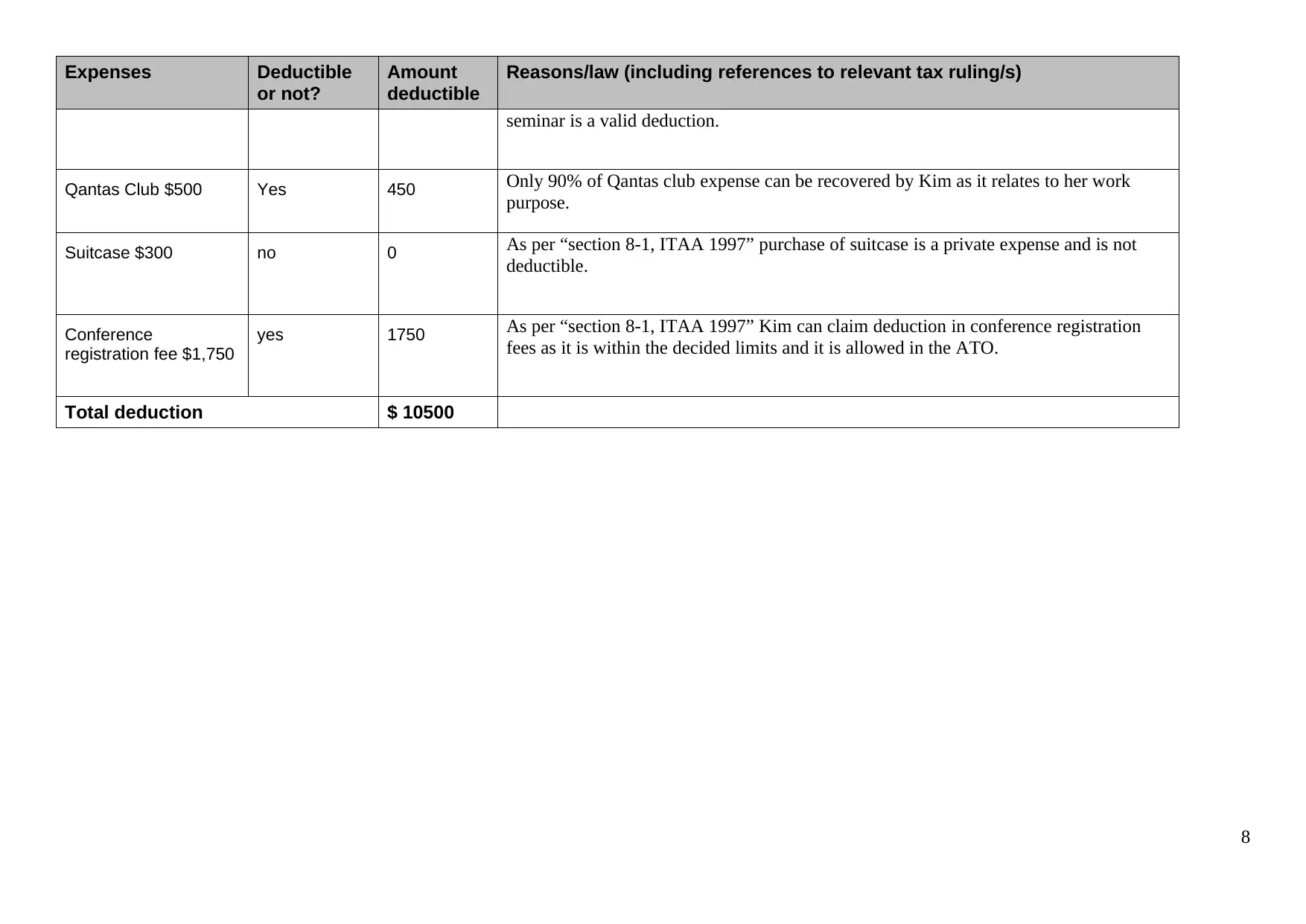

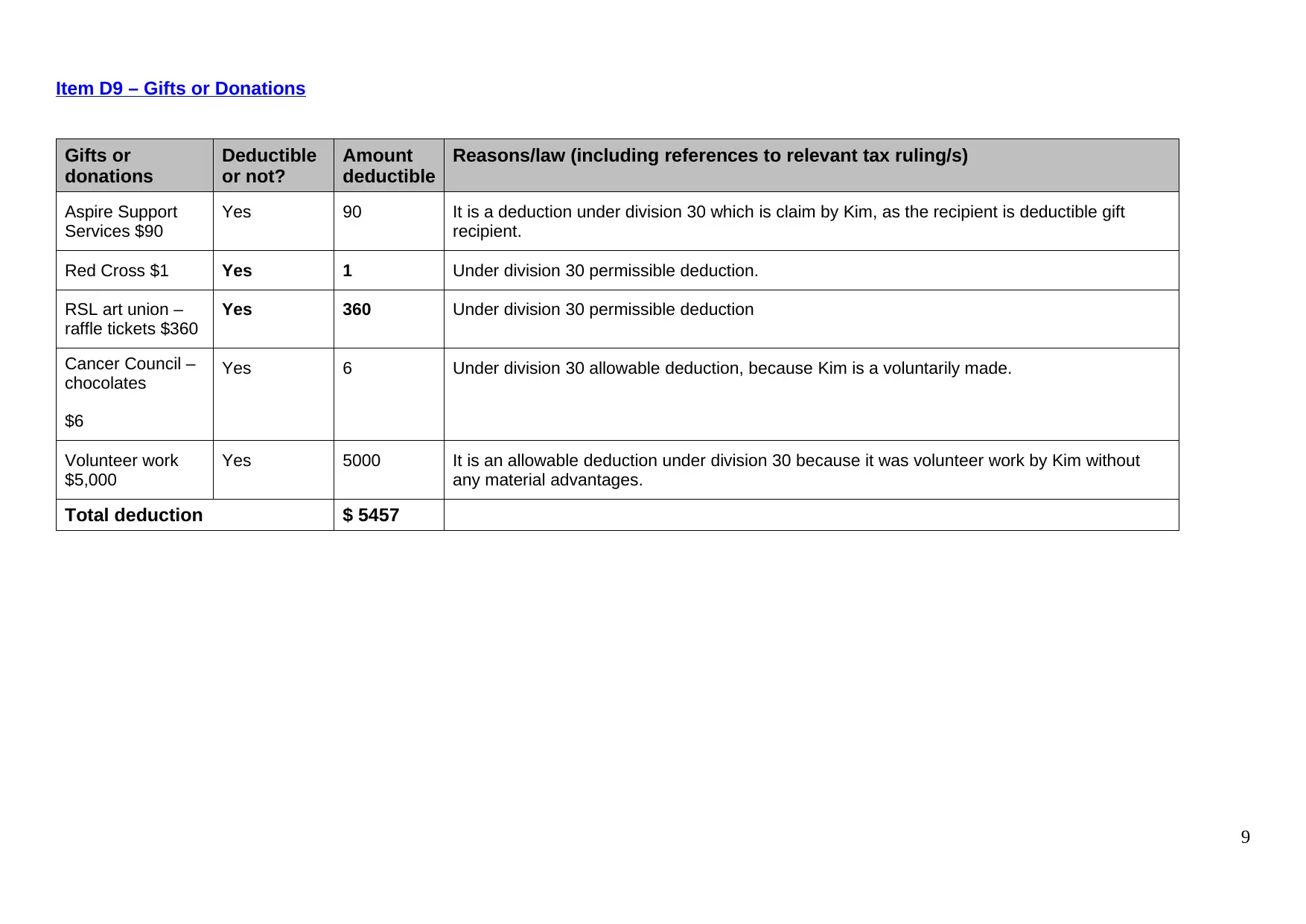

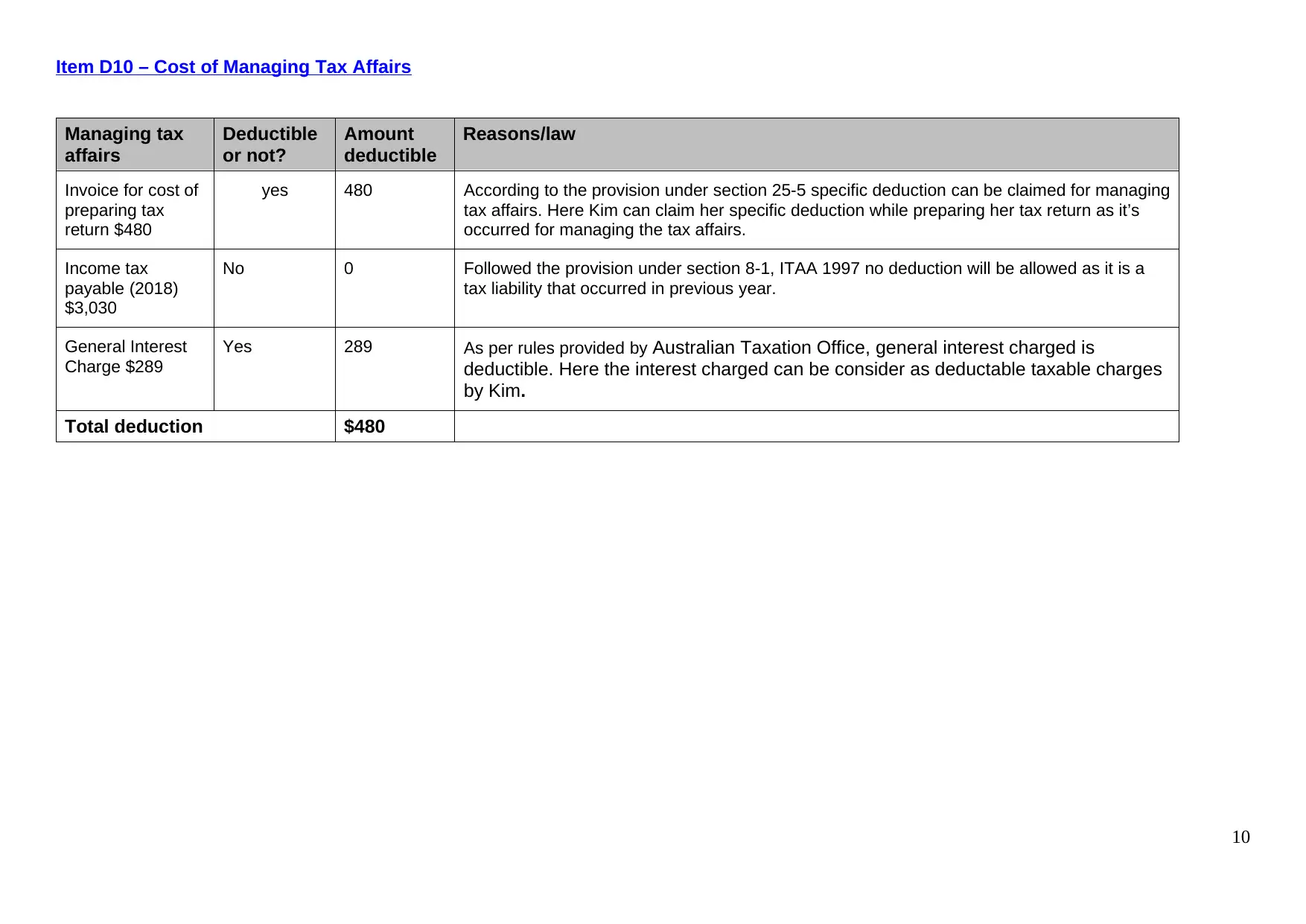

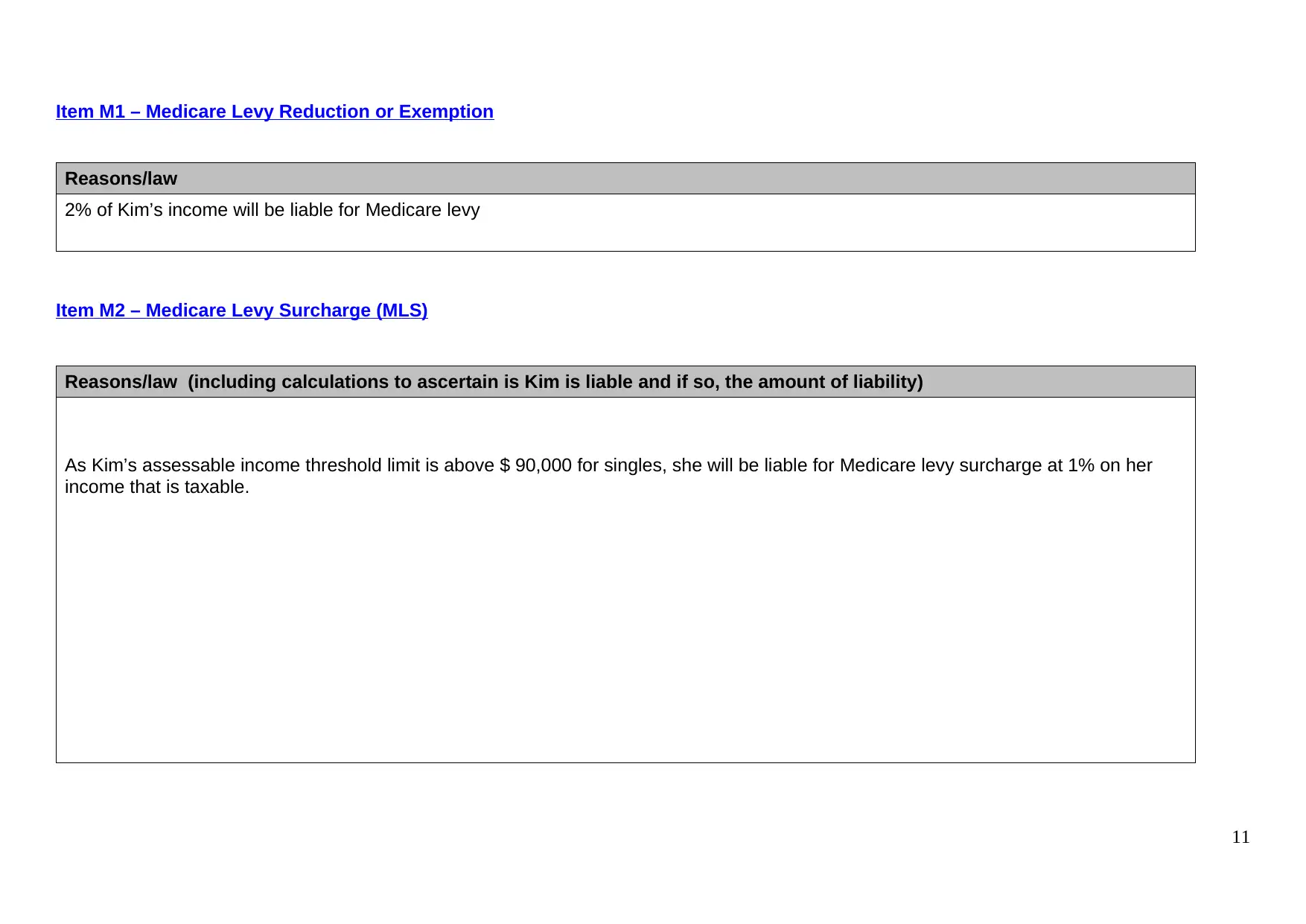

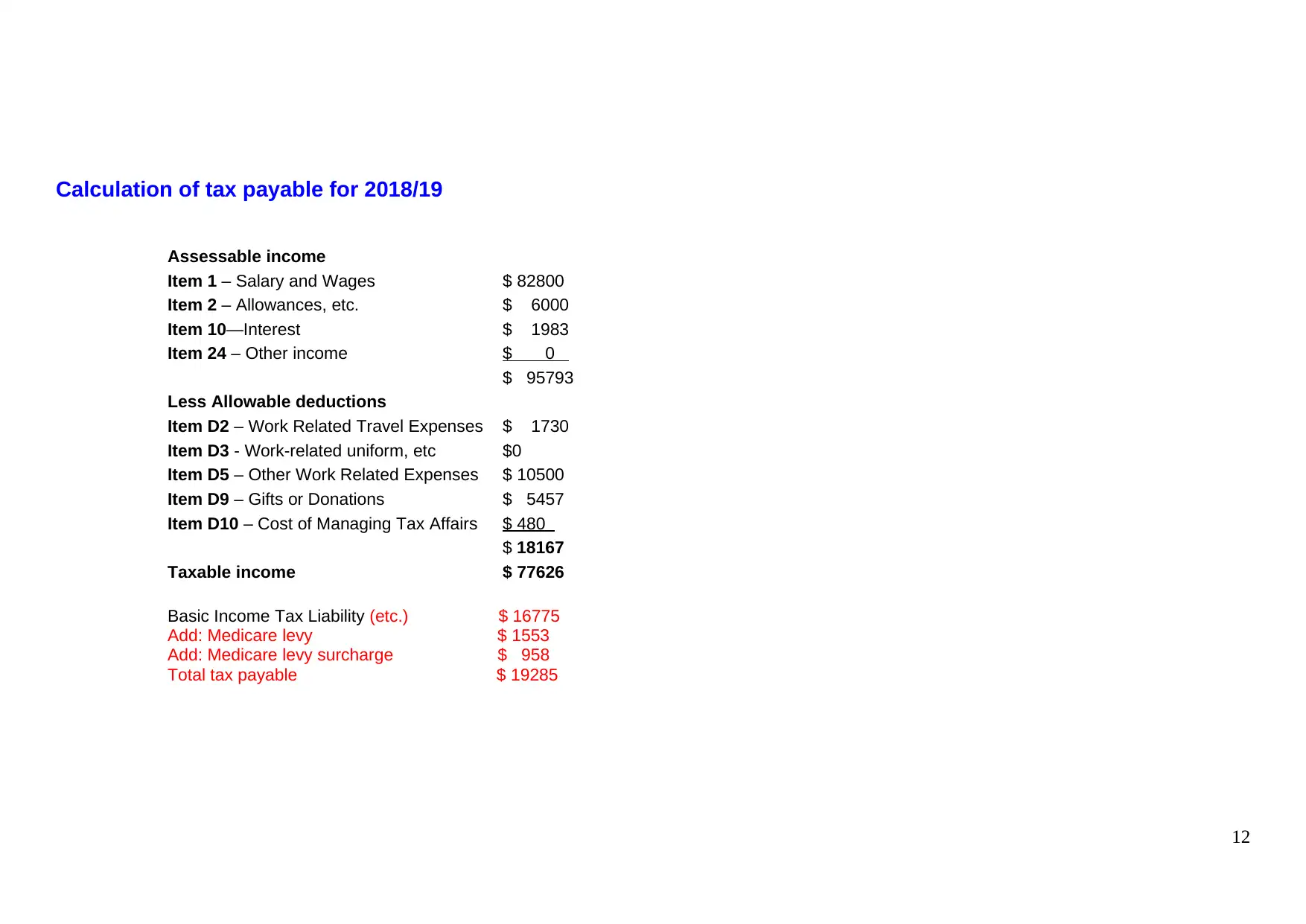

This document presents a comprehensive solution to an individual Australian Tax Law assignment (BFA714) from Griffith University, Semester 2, 2019. The assignment requires a detailed analysis of Kim Smith's income and deductions for the 2018/19 financial year. The solution meticulously categorizes various income sources, including salary, allowances, interest, and other income, determining their assessability based on relevant tax laws and rulings. It also analyzes work-related expenses such as travel, uniforms, and other work-related expenses, gifts or donations, and the cost of managing tax affairs to determine their deductibility. The document further calculates Kim's taxable income, basic income tax liability, Medicare levy, and Medicare levy surcharge, providing a complete overview of her tax obligations. The analysis includes relevant references to the Income Tax Assessment Act 1997 (ITAA 1997) and other tax rulings to support the conclusions.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.