BFA714: Griffith University Australian Tax Law Assignment 1, 2019

VerifiedAdded on 2022/10/10

|13

|2175

|126

Homework Assignment

AI Summary

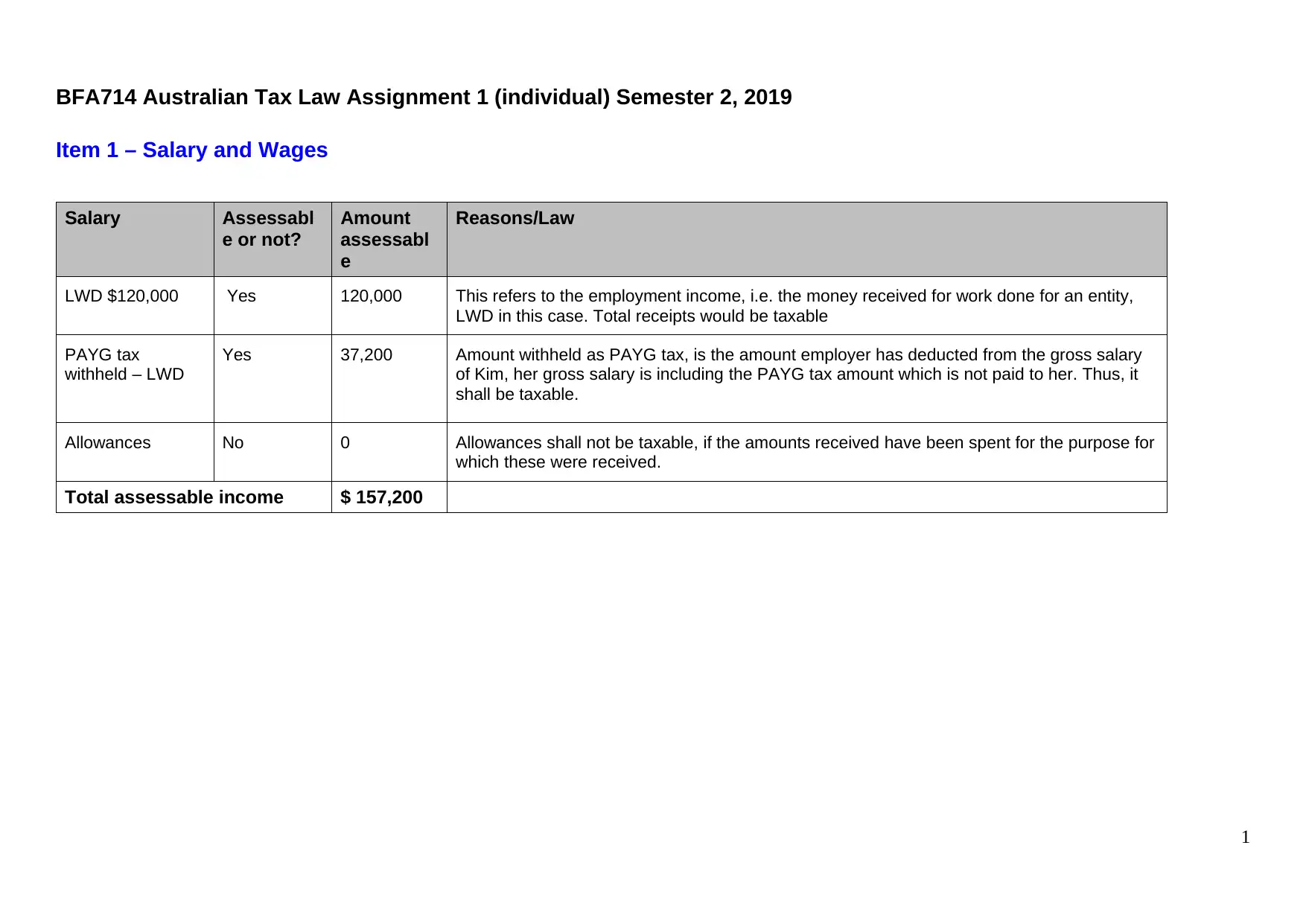

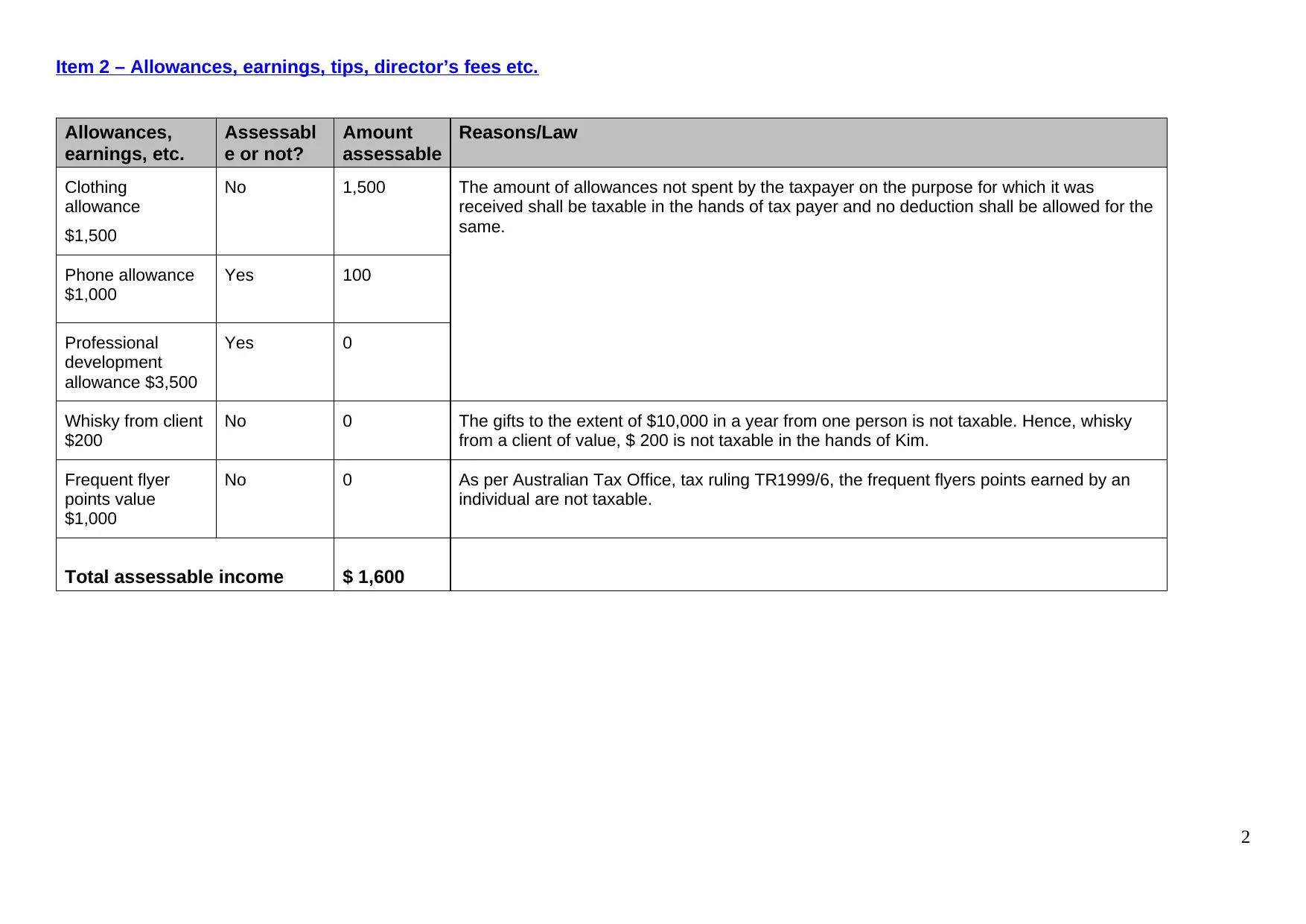

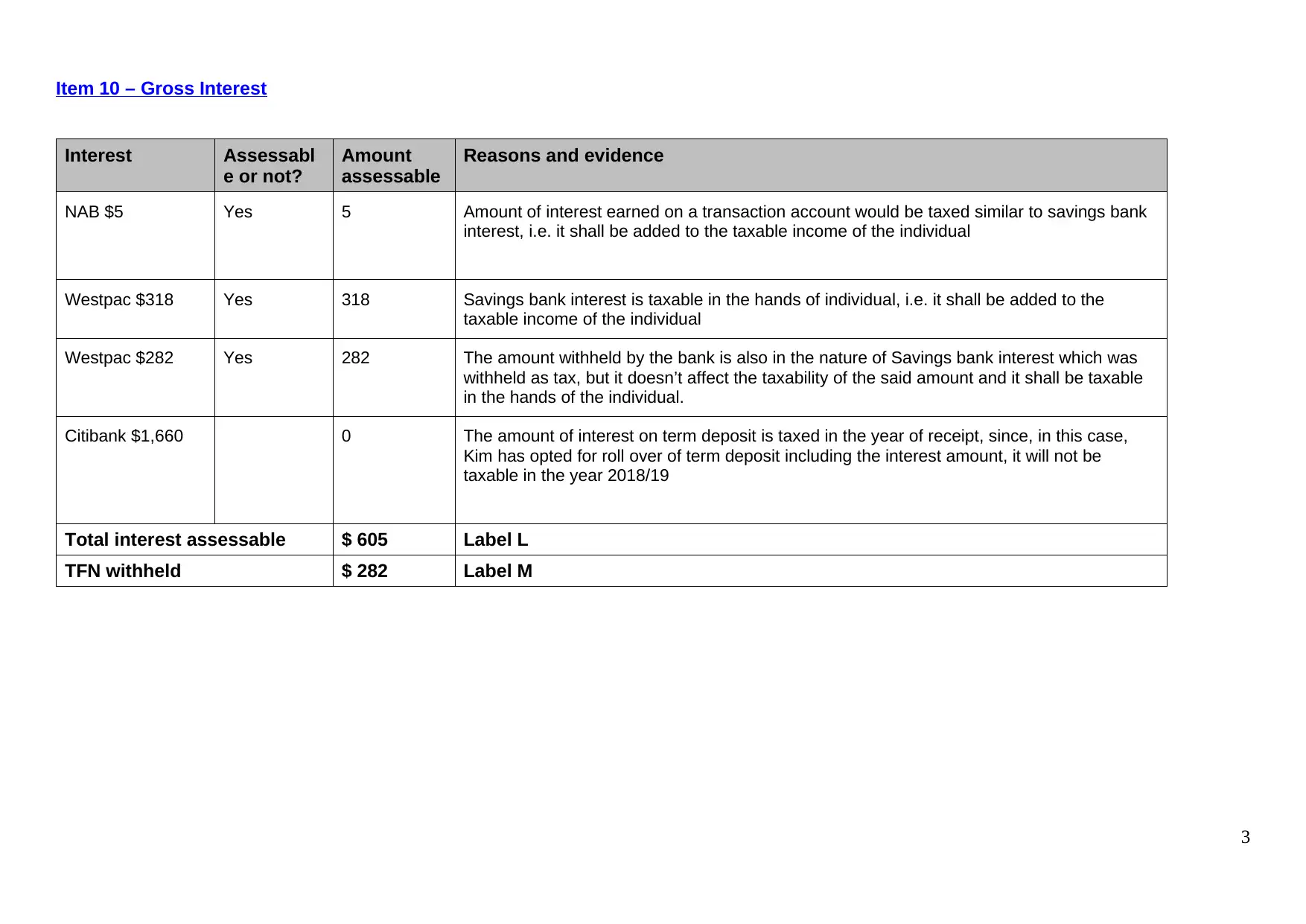

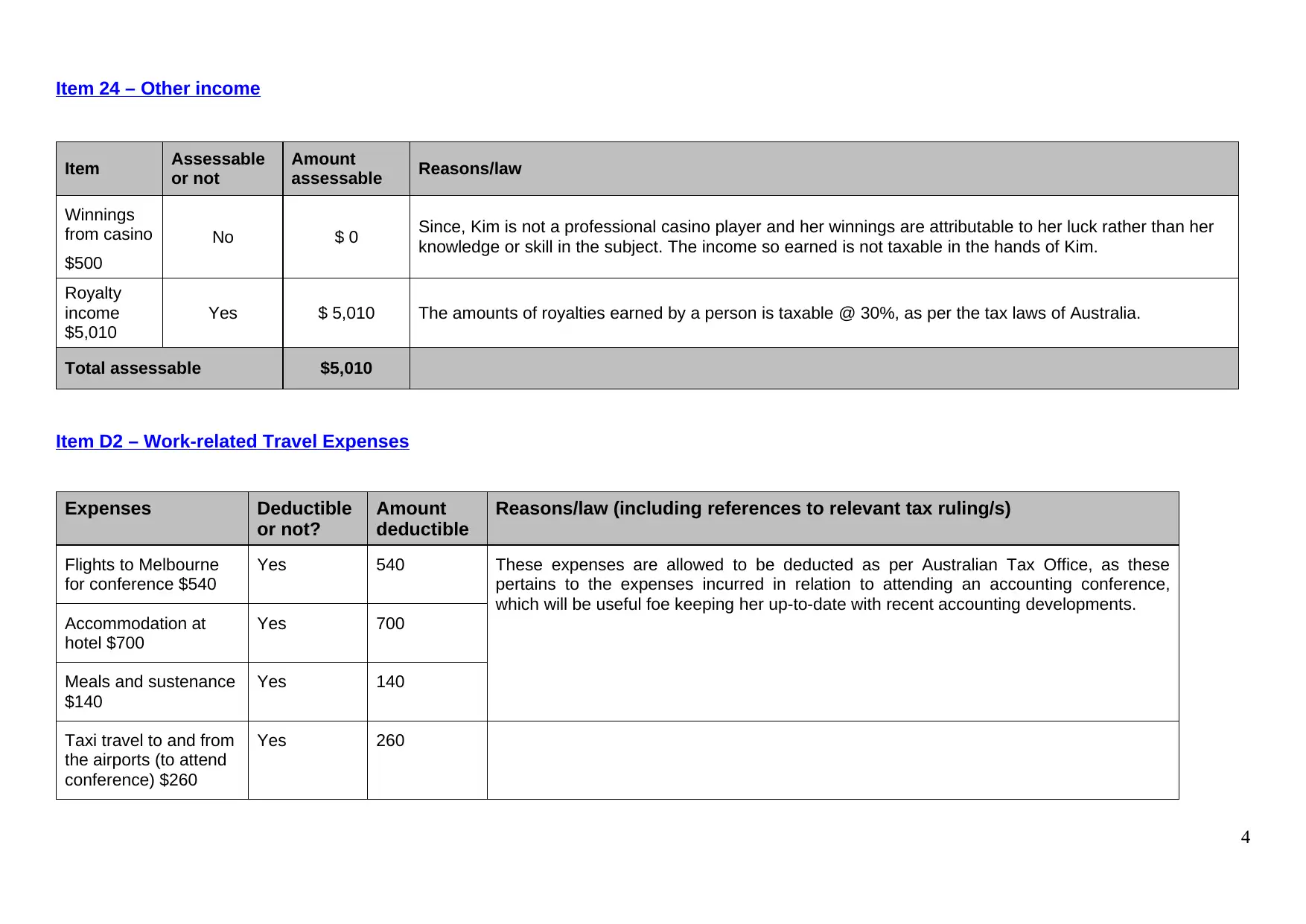

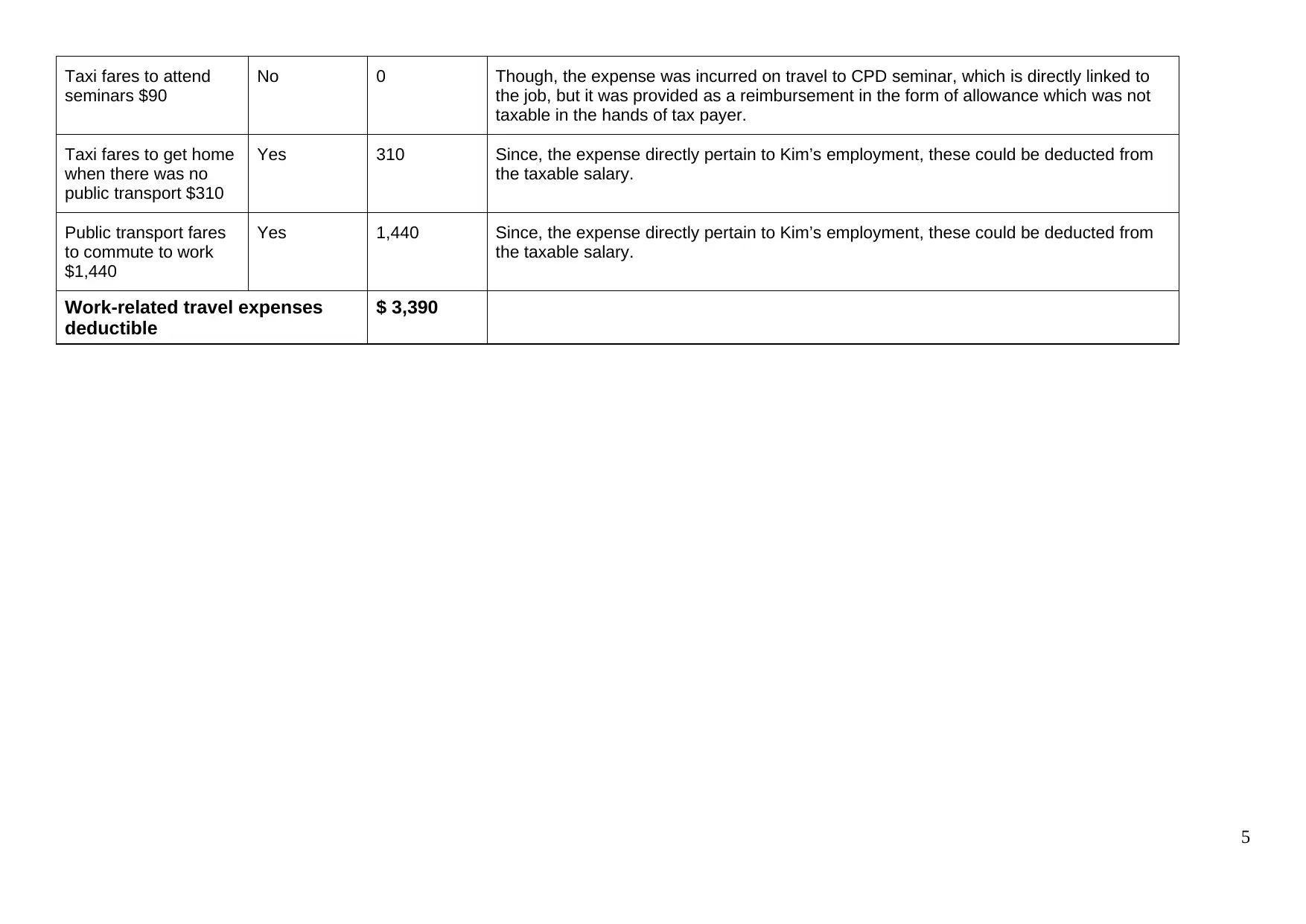

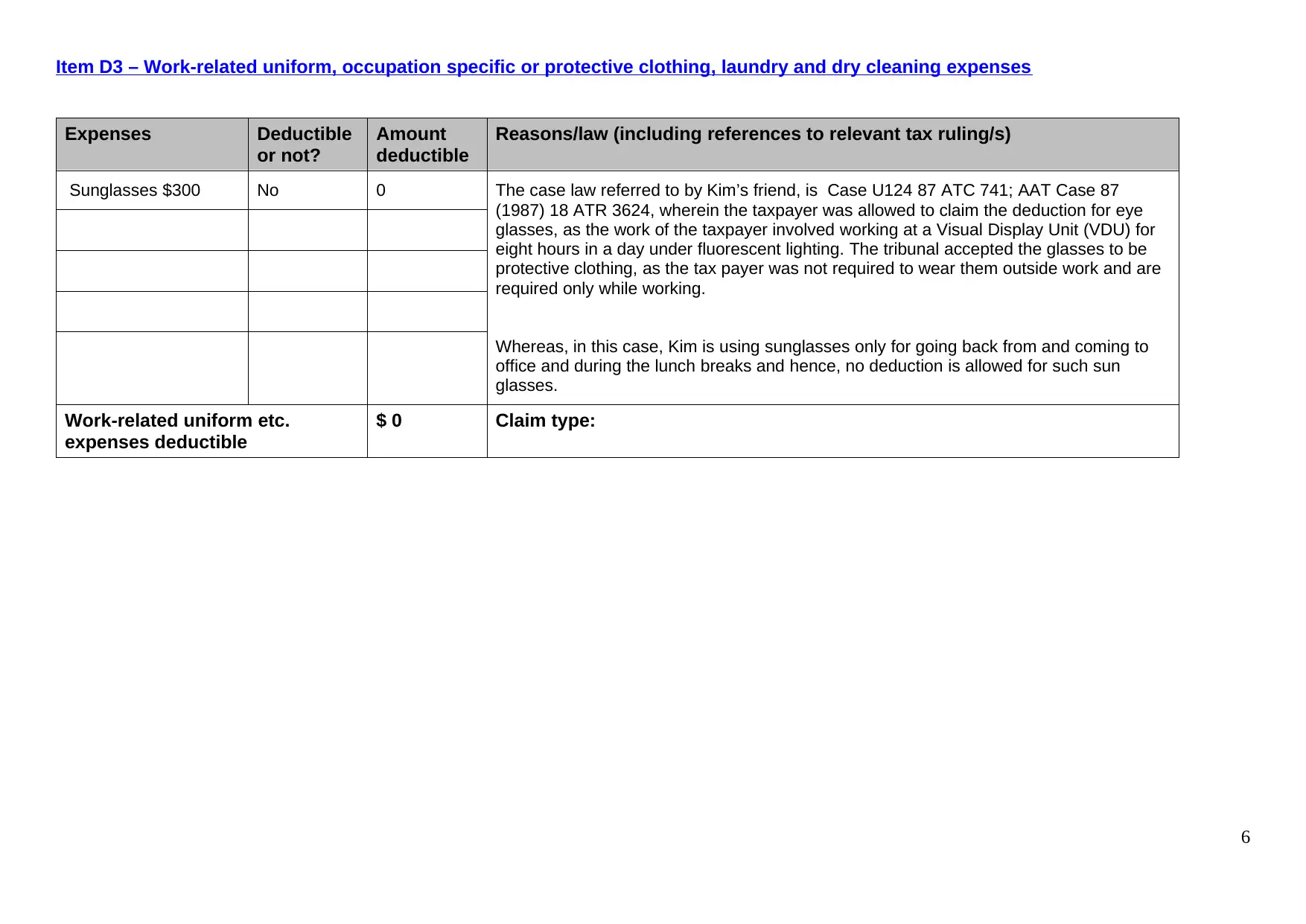

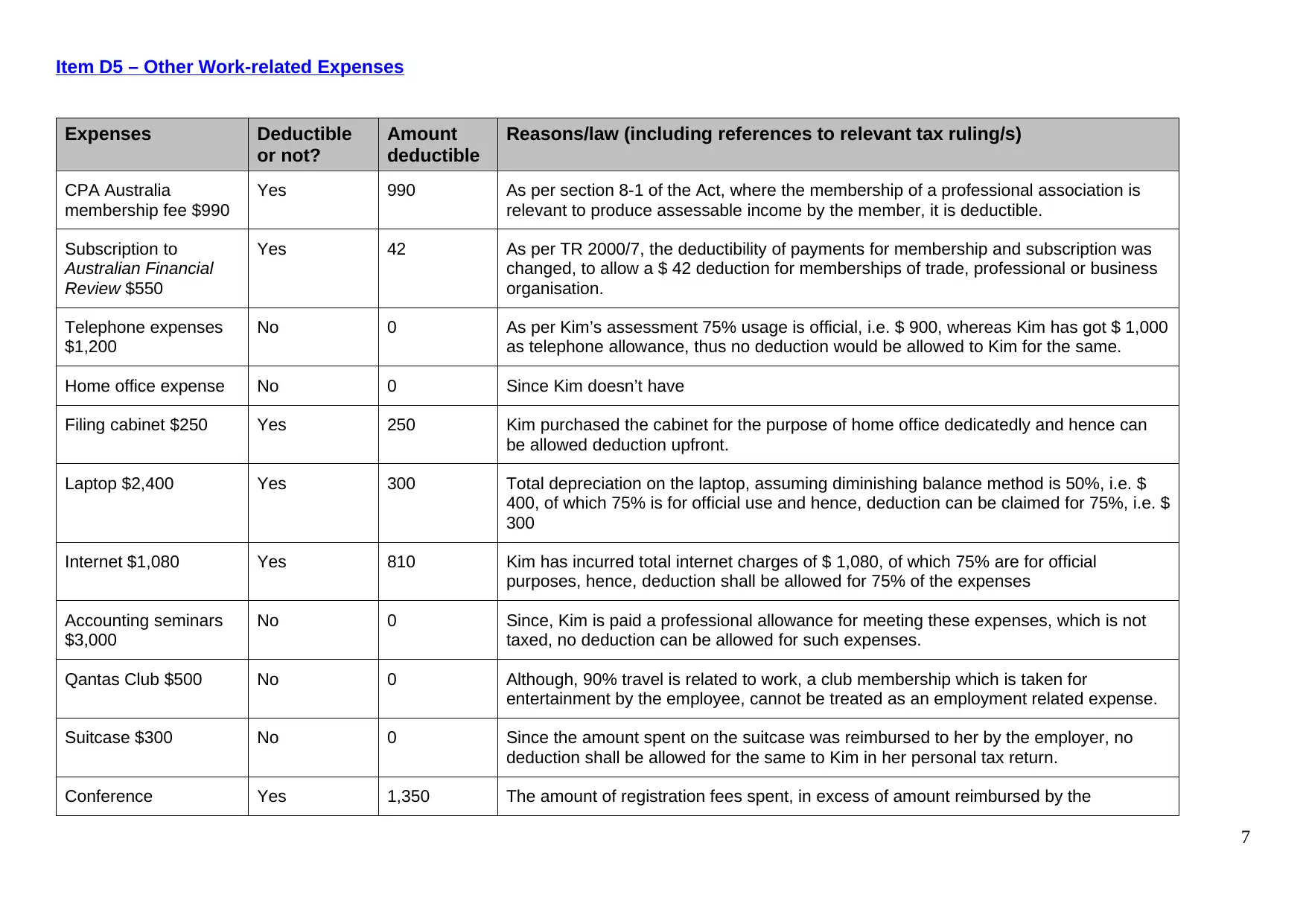

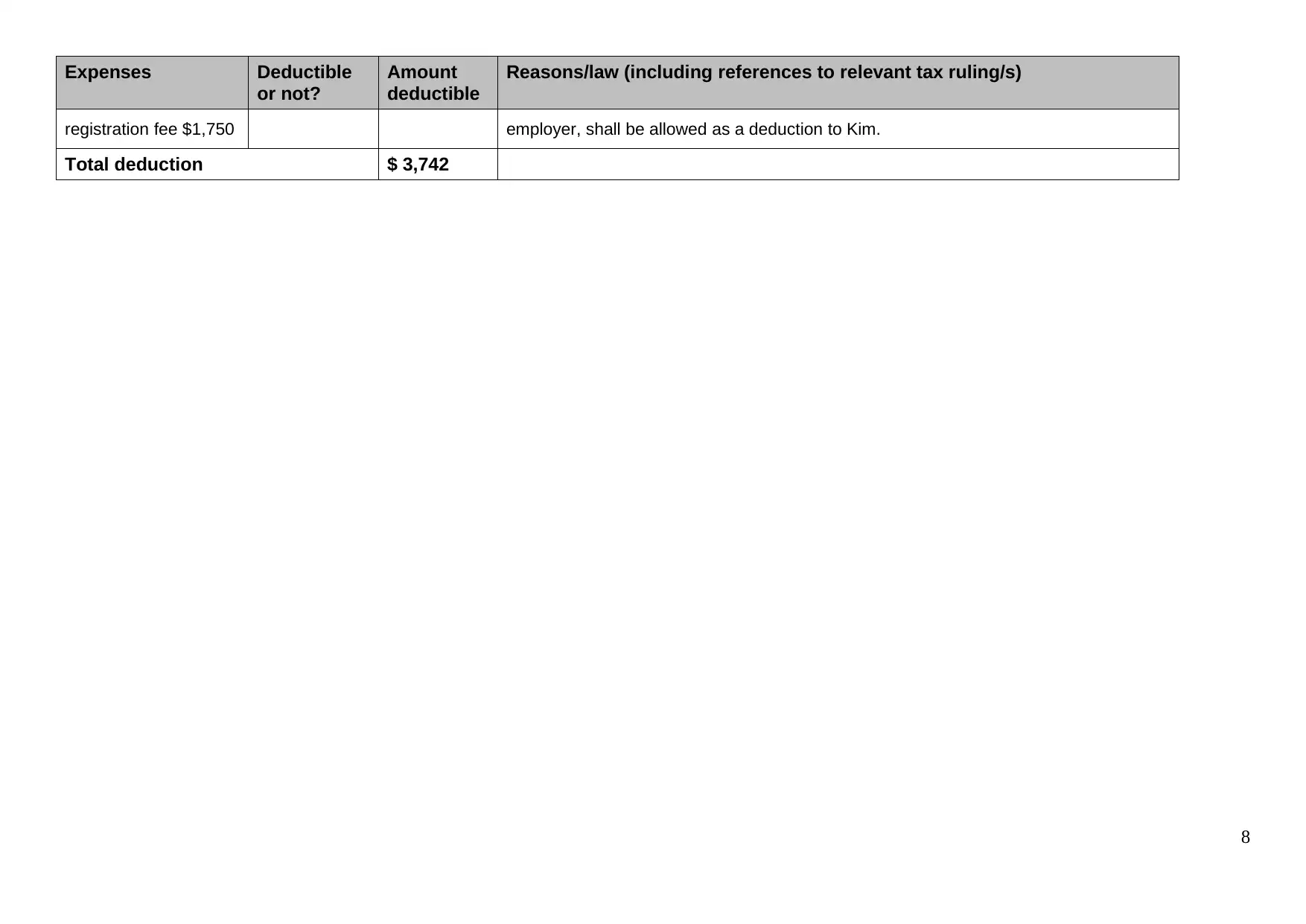

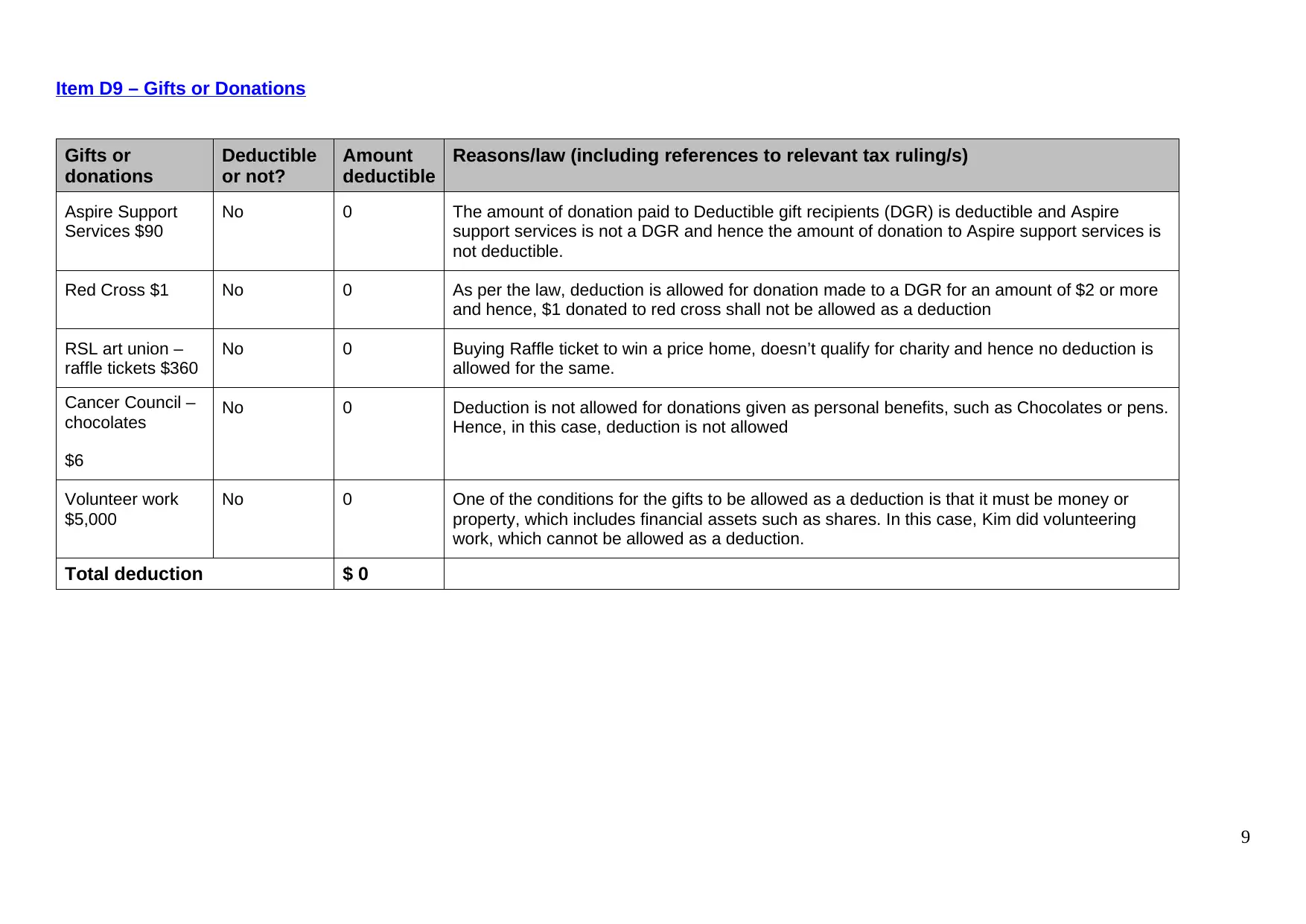

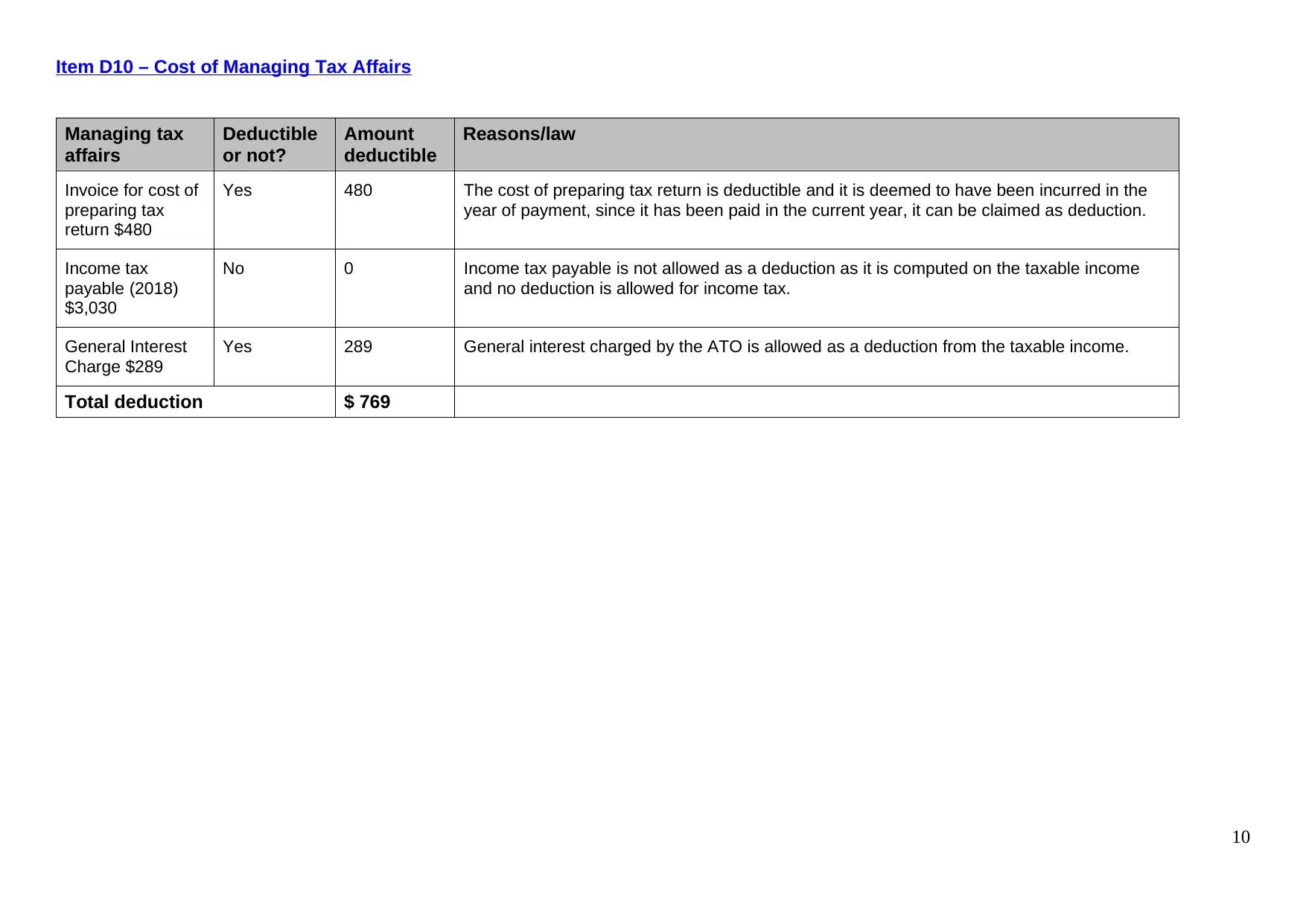

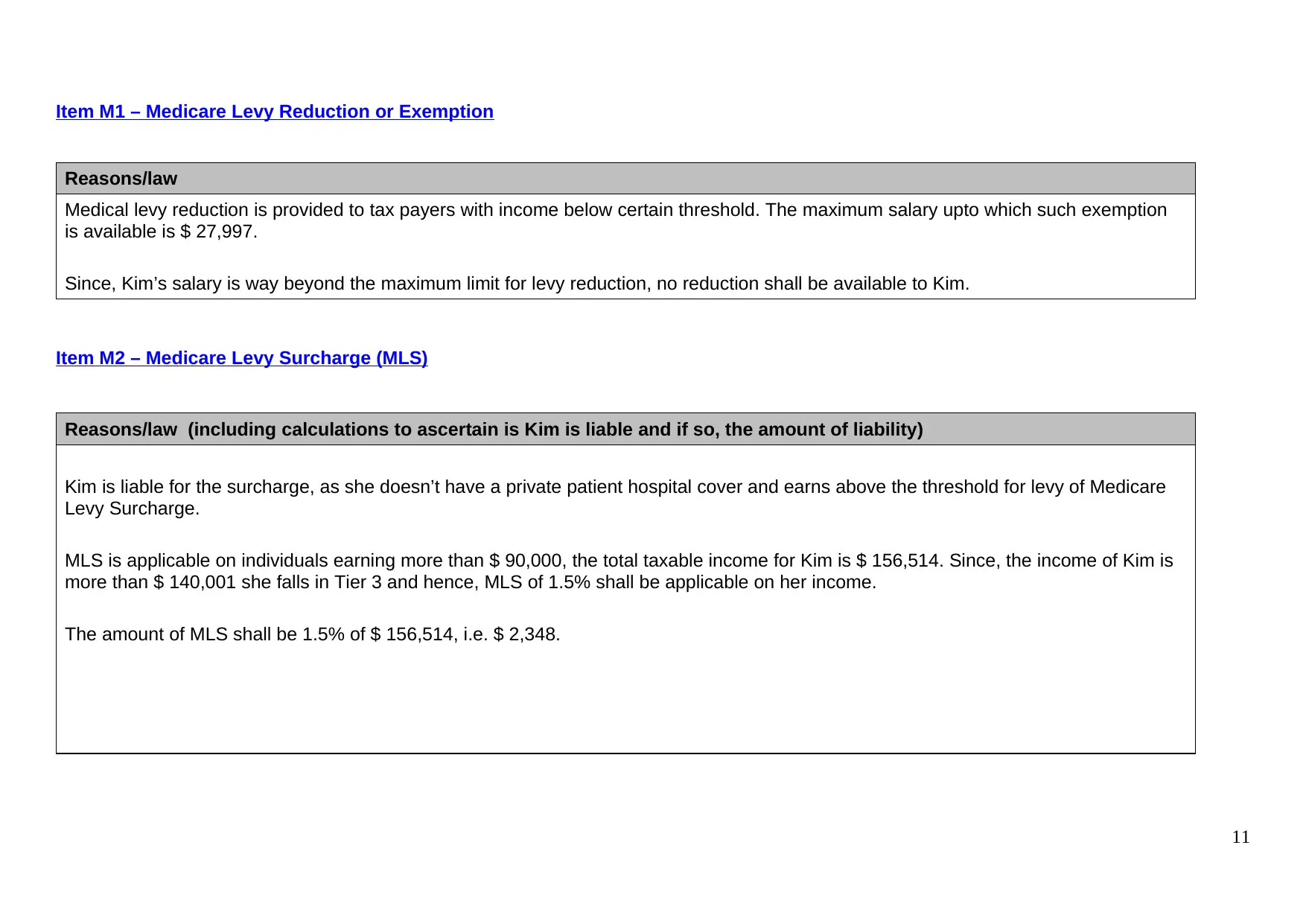

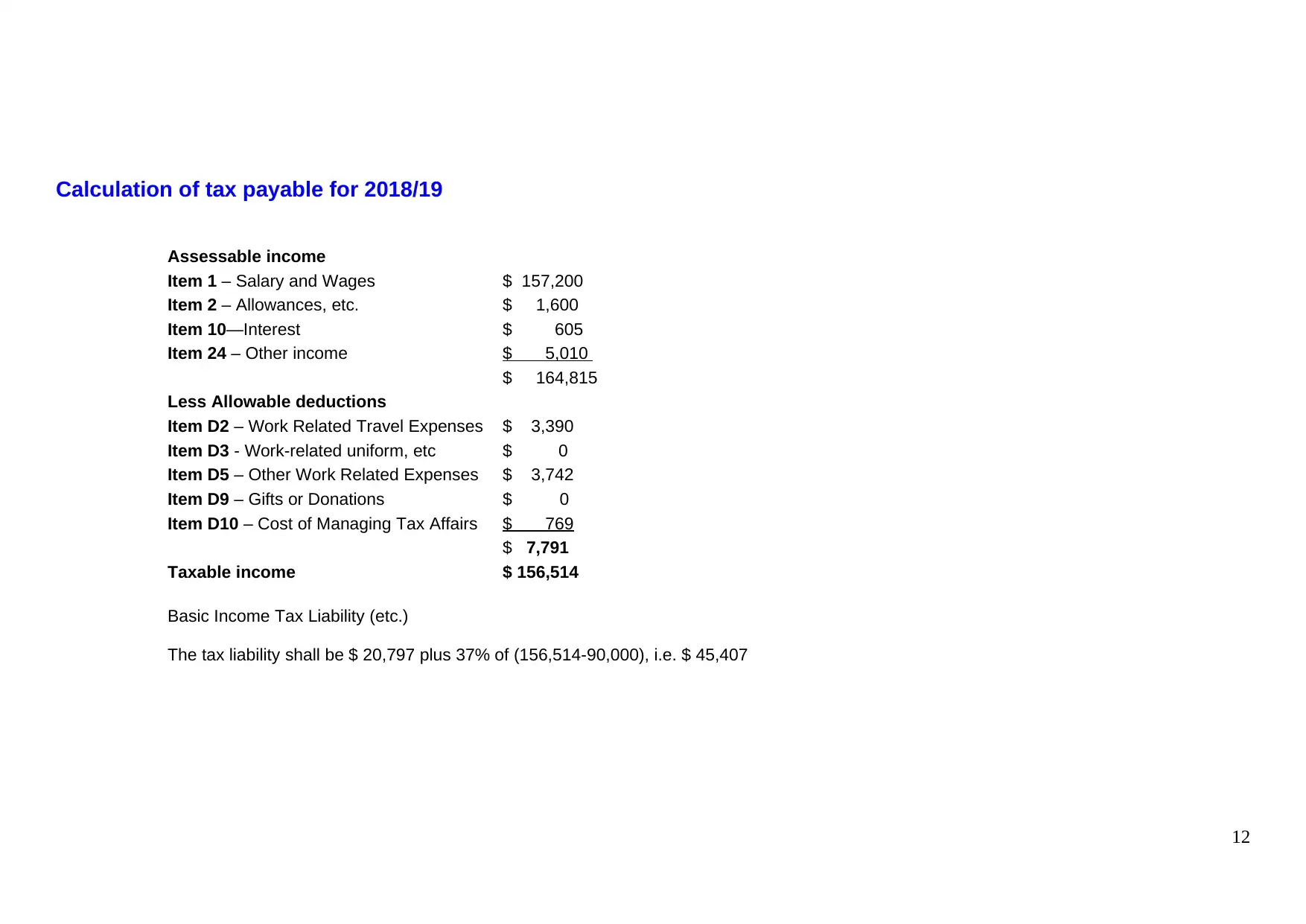

This document presents a comprehensive solution to an individual Australian Tax Law assignment (BFA714) for the 2019 financial year. It meticulously analyzes Kim Smith's financial data, determining assessable income from salary, wages, allowances, interest, and royalty income. The solution addresses various deductions, including work-related travel expenses, uniform expenses, other work-related expenses, gifts, and the cost of managing tax affairs. Each item is assessed with detailed reasons and references to relevant tax rulings. The assignment also calculates the Medicare Levy Surcharge (MLS) and the final tax liability. The analysis includes a breakdown of each item's tax implications, ensuring a thorough understanding of Australian tax law principles. The solution is designed to provide clarity on complex tax concepts and practical application of tax regulations, making it a valuable resource for students studying Australian taxation.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.