BFA714 Australian Tax Law Assignment 1 - Income Tax Assessment 2019

VerifiedAdded on 2022/10/10

|13

|2199

|107

Homework Assignment

AI Summary

This document presents a comprehensive solution to BFA714 Australian Tax Law Assignment 1 for Semester 2, 2019, focusing on the income tax assessment of an individual, Kim Smith. The assignment analyzes various income sources, including salary and wages, allowances, interest, and royalty income, determining their assessability under the Income Tax Assessment Act 1997. It also examines work-related expenses such as travel, uniforms, and other costs, evaluating their deductibility based on relevant tax rulings. Furthermore, the solution addresses the Medicare levy and surcharge, calculating the total tax payable. The analysis incorporates relevant case law and tax rulings to justify each assessment and deduction, providing a detailed understanding of the Australian tax system.

BFA714 Australian Tax Law Assignment 1 (individual) Semester 2, 2019

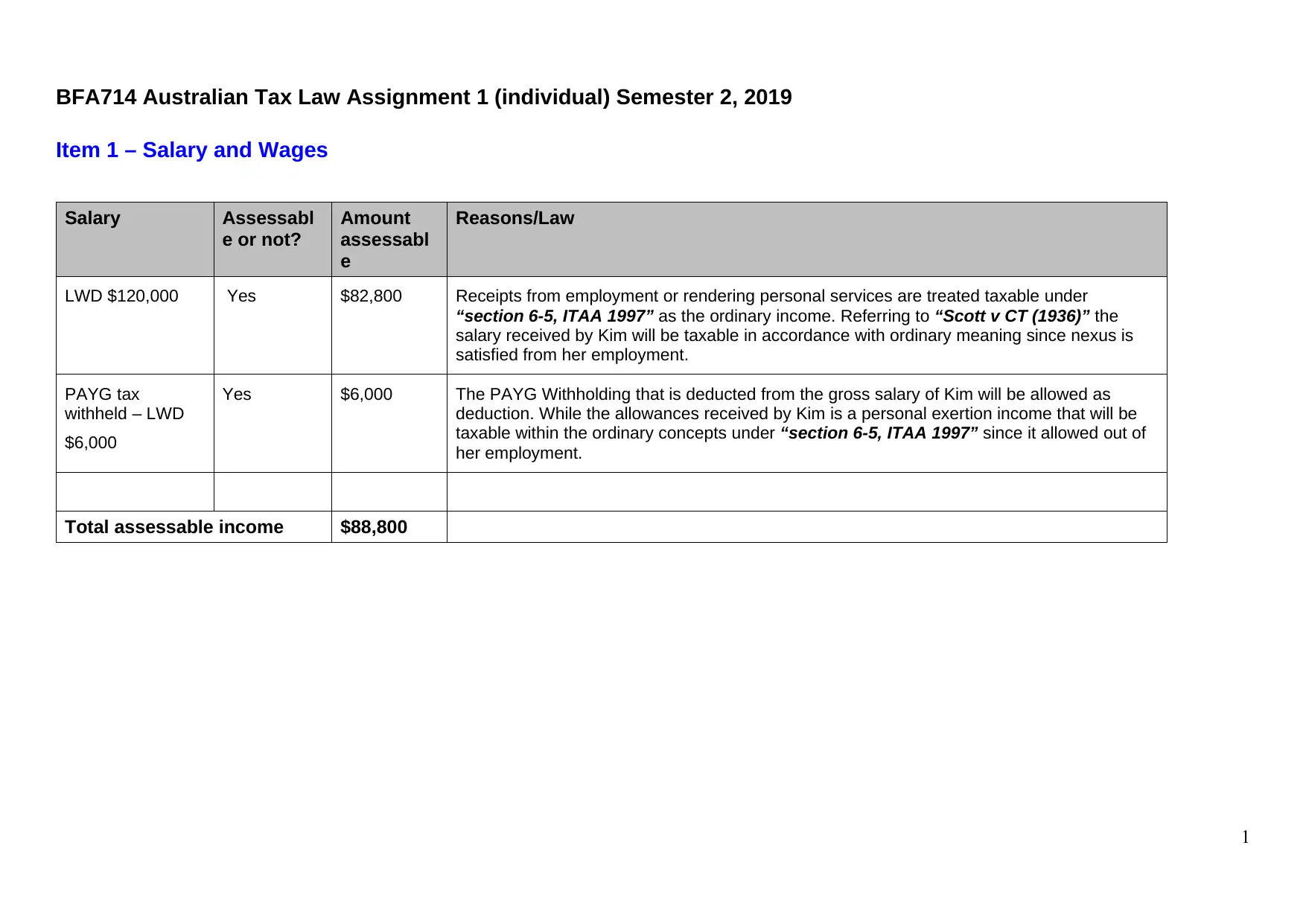

Item 1 – Salary and Wages

Salary Assessabl

e or not?

Amount

assessabl

e

Reasons/Law

LWD $120,000 Yes $82,800 Receipts from employment or rendering personal services are treated taxable under

“section 6-5, ITAA 1997” as the ordinary income. Referring to “Scott v CT (1936)” the

salary received by Kim will be taxable in accordance with ordinary meaning since nexus is

satisfied from her employment.

PAYG tax

withheld – LWD

$6,000

Yes $6,000 The PAYG Withholding that is deducted from the gross salary of Kim will be allowed as

deduction. While the allowances received by Kim is a personal exertion income that will be

taxable within the ordinary concepts under “section 6-5, ITAA 1997” since it allowed out of

her employment.

Total assessable income $88,800

1

Item 1 – Salary and Wages

Salary Assessabl

e or not?

Amount

assessabl

e

Reasons/Law

LWD $120,000 Yes $82,800 Receipts from employment or rendering personal services are treated taxable under

“section 6-5, ITAA 1997” as the ordinary income. Referring to “Scott v CT (1936)” the

salary received by Kim will be taxable in accordance with ordinary meaning since nexus is

satisfied from her employment.

PAYG tax

withheld – LWD

$6,000

Yes $6,000 The PAYG Withholding that is deducted from the gross salary of Kim will be allowed as

deduction. While the allowances received by Kim is a personal exertion income that will be

taxable within the ordinary concepts under “section 6-5, ITAA 1997” since it allowed out of

her employment.

Total assessable income $88,800

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

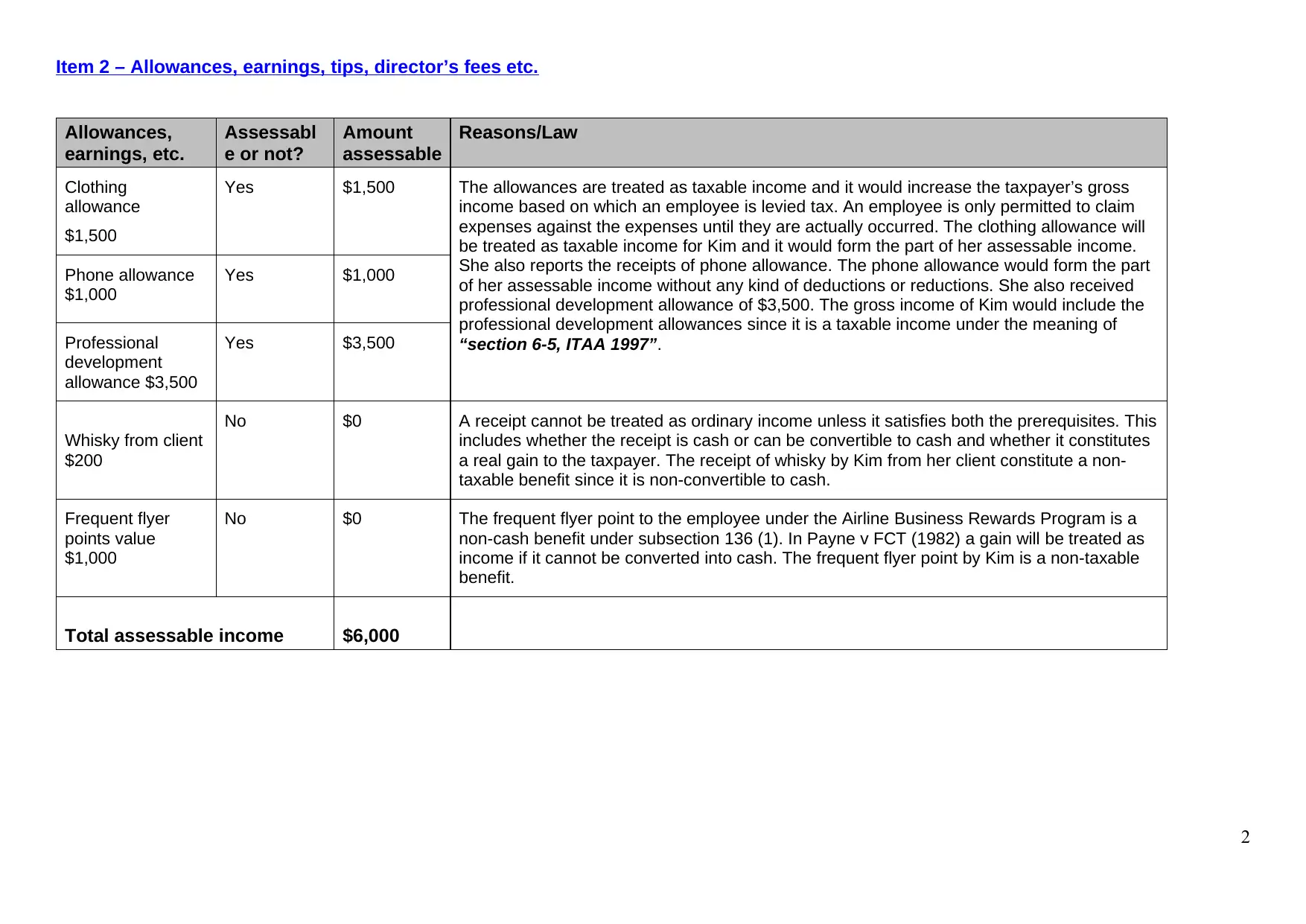

Item 2 – Allowances, earnings, tips, director’s fees etc.

Allowances,

earnings, etc.

Assessabl

e or not?

Amount

assessable

Reasons/Law

Clothing

allowance

$1,500

Yes $1,500 The allowances are treated as taxable income and it would increase the taxpayer’s gross

income based on which an employee is levied tax. An employee is only permitted to claim

expenses against the expenses until they are actually occurred. The clothing allowance will

be treated as taxable income for Kim and it would form the part of her assessable income.

She also reports the receipts of phone allowance. The phone allowance would form the part

of her assessable income without any kind of deductions or reductions. She also received

professional development allowance of $3,500. The gross income of Kim would include the

professional development allowances since it is a taxable income under the meaning of

“section 6-5, ITAA 1997”.

Phone allowance

$1,000

Yes $1,000

Professional

development

allowance $3,500

Yes $3,500

Whisky from client

$200

No $0 A receipt cannot be treated as ordinary income unless it satisfies both the prerequisites. This

includes whether the receipt is cash or can be convertible to cash and whether it constitutes

a real gain to the taxpayer. The receipt of whisky by Kim from her client constitute a non-

taxable benefit since it is non-convertible to cash.

Frequent flyer

points value

$1,000

No $0 The frequent flyer point to the employee under the Airline Business Rewards Program is a

non-cash benefit under subsection 136 (1). In Payne v FCT (1982) a gain will be treated as

income if it cannot be converted into cash. The frequent flyer point by Kim is a non-taxable

benefit.

Total assessable income $6,000

2

Allowances,

earnings, etc.

Assessabl

e or not?

Amount

assessable

Reasons/Law

Clothing

allowance

$1,500

Yes $1,500 The allowances are treated as taxable income and it would increase the taxpayer’s gross

income based on which an employee is levied tax. An employee is only permitted to claim

expenses against the expenses until they are actually occurred. The clothing allowance will

be treated as taxable income for Kim and it would form the part of her assessable income.

She also reports the receipts of phone allowance. The phone allowance would form the part

of her assessable income without any kind of deductions or reductions. She also received

professional development allowance of $3,500. The gross income of Kim would include the

professional development allowances since it is a taxable income under the meaning of

“section 6-5, ITAA 1997”.

Phone allowance

$1,000

Yes $1,000

Professional

development

allowance $3,500

Yes $3,500

Whisky from client

$200

No $0 A receipt cannot be treated as ordinary income unless it satisfies both the prerequisites. This

includes whether the receipt is cash or can be convertible to cash and whether it constitutes

a real gain to the taxpayer. The receipt of whisky by Kim from her client constitute a non-

taxable benefit since it is non-convertible to cash.

Frequent flyer

points value

$1,000

No $0 The frequent flyer point to the employee under the Airline Business Rewards Program is a

non-cash benefit under subsection 136 (1). In Payne v FCT (1982) a gain will be treated as

income if it cannot be converted into cash. The frequent flyer point by Kim is a non-taxable

benefit.

Total assessable income $6,000

2

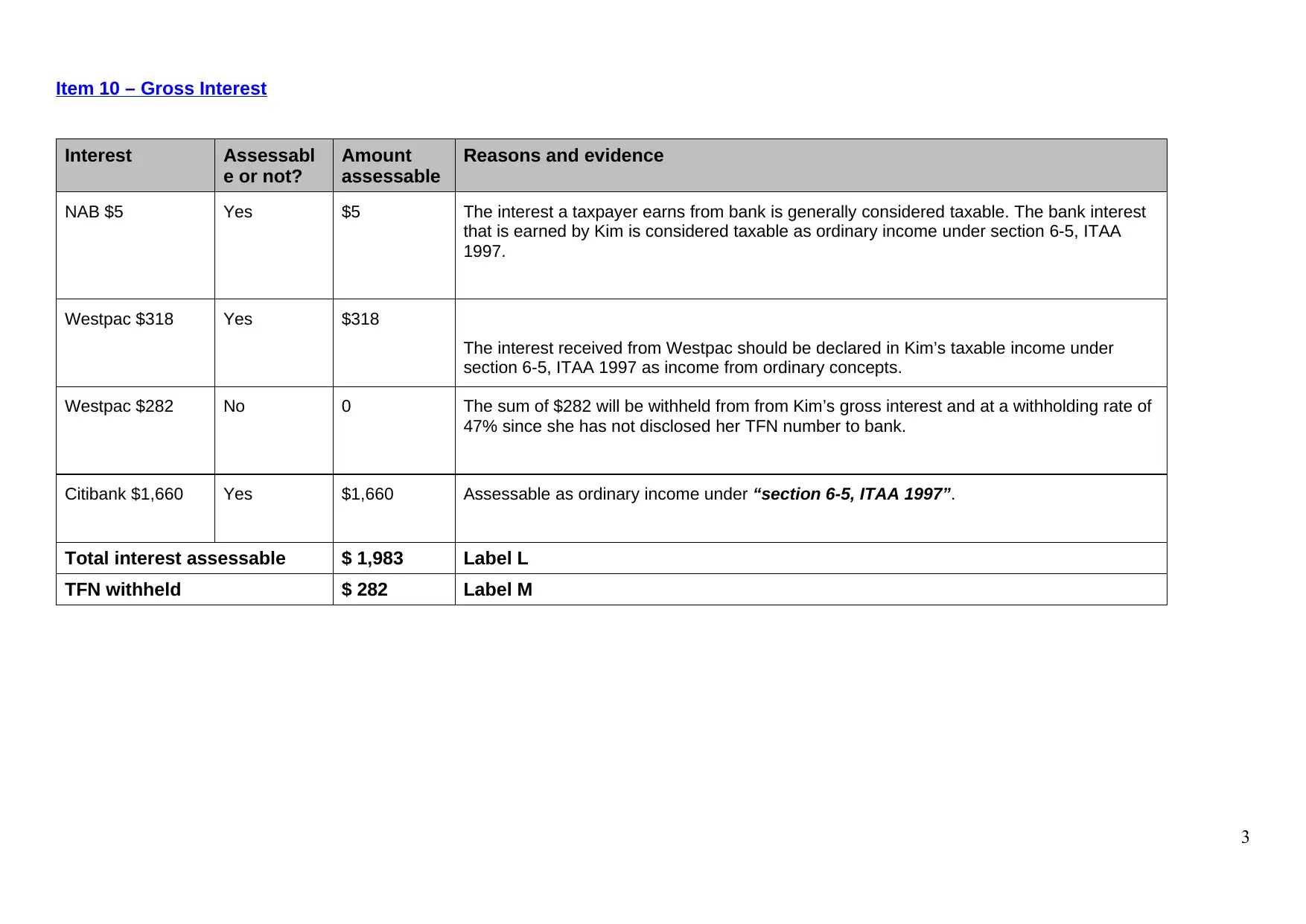

Item 10 – Gross Interest

Interest Assessabl

e or not?

Amount

assessable

Reasons and evidence

NAB $5 Yes $5 The interest a taxpayer earns from bank is generally considered taxable. The bank interest

that is earned by Kim is considered taxable as ordinary income under section 6-5, ITAA

1997.

Westpac $318 Yes $318

The interest received from Westpac should be declared in Kim’s taxable income under

section 6-5, ITAA 1997 as income from ordinary concepts.

Westpac $282 No 0 The sum of $282 will be withheld from from Kim’s gross interest and at a withholding rate of

47% since she has not disclosed her TFN number to bank.

Citibank $1,660 Yes $1,660 Assessable as ordinary income under “section 6-5, ITAA 1997”.

Total interest assessable $ 1,983 Label L

TFN withheld $ 282 Label M

3

Interest Assessabl

e or not?

Amount

assessable

Reasons and evidence

NAB $5 Yes $5 The interest a taxpayer earns from bank is generally considered taxable. The bank interest

that is earned by Kim is considered taxable as ordinary income under section 6-5, ITAA

1997.

Westpac $318 Yes $318

The interest received from Westpac should be declared in Kim’s taxable income under

section 6-5, ITAA 1997 as income from ordinary concepts.

Westpac $282 No 0 The sum of $282 will be withheld from from Kim’s gross interest and at a withholding rate of

47% since she has not disclosed her TFN number to bank.

Citibank $1,660 Yes $1,660 Assessable as ordinary income under “section 6-5, ITAA 1997”.

Total interest assessable $ 1,983 Label L

TFN withheld $ 282 Label M

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

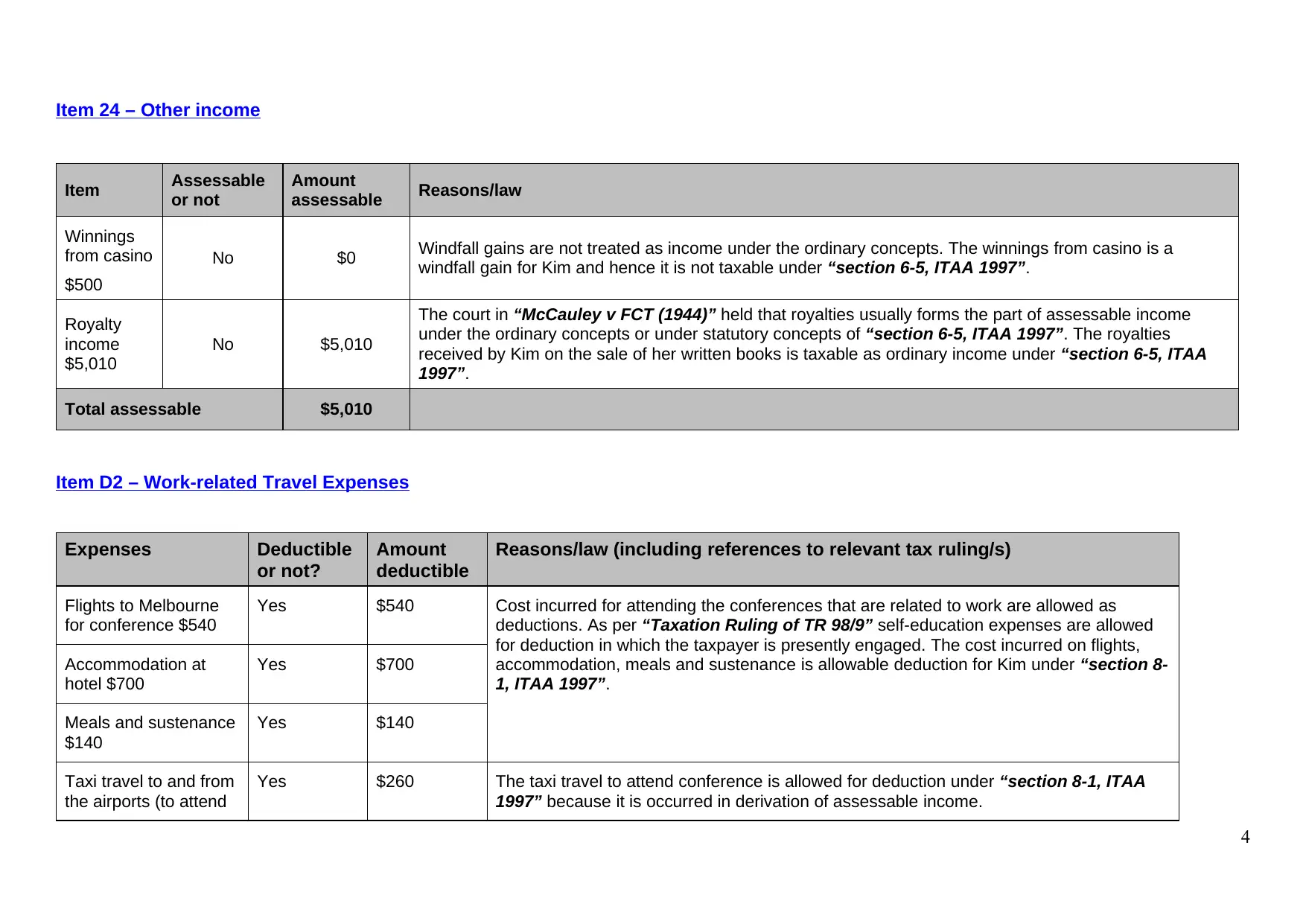

Item 24 – Other income

Item Assessable

or not

Amount

assessable Reasons/law

Winnings

from casino

$500

No $0 Windfall gains are not treated as income under the ordinary concepts. The winnings from casino is a

windfall gain for Kim and hence it is not taxable under “section 6-5, ITAA 1997”.

Royalty

income

$5,010

No $5,010

The court in “McCauley v FCT (1944)” held that royalties usually forms the part of assessable income

under the ordinary concepts or under statutory concepts of “section 6-5, ITAA 1997”. The royalties

received by Kim on the sale of her written books is taxable as ordinary income under “section 6-5, ITAA

1997”.

Total assessable $5,010

Item D2 – Work-related Travel Expenses

Expenses Deductible

or not?

Amount

deductible

Reasons/law (including references to relevant tax ruling/s)

Flights to Melbourne

for conference $540

Yes $540 Cost incurred for attending the conferences that are related to work are allowed as

deductions. As per “Taxation Ruling of TR 98/9” self-education expenses are allowed

for deduction in which the taxpayer is presently engaged. The cost incurred on flights,

accommodation, meals and sustenance is allowable deduction for Kim under “section 8-

1, ITAA 1997”.

Accommodation at

hotel $700

Yes $700

Meals and sustenance

$140

Yes $140

Taxi travel to and from

the airports (to attend

Yes $260 The taxi travel to attend conference is allowed for deduction under “section 8-1, ITAA

1997” because it is occurred in derivation of assessable income.

4

Item Assessable

or not

Amount

assessable Reasons/law

Winnings

from casino

$500

No $0 Windfall gains are not treated as income under the ordinary concepts. The winnings from casino is a

windfall gain for Kim and hence it is not taxable under “section 6-5, ITAA 1997”.

Royalty

income

$5,010

No $5,010

The court in “McCauley v FCT (1944)” held that royalties usually forms the part of assessable income

under the ordinary concepts or under statutory concepts of “section 6-5, ITAA 1997”. The royalties

received by Kim on the sale of her written books is taxable as ordinary income under “section 6-5, ITAA

1997”.

Total assessable $5,010

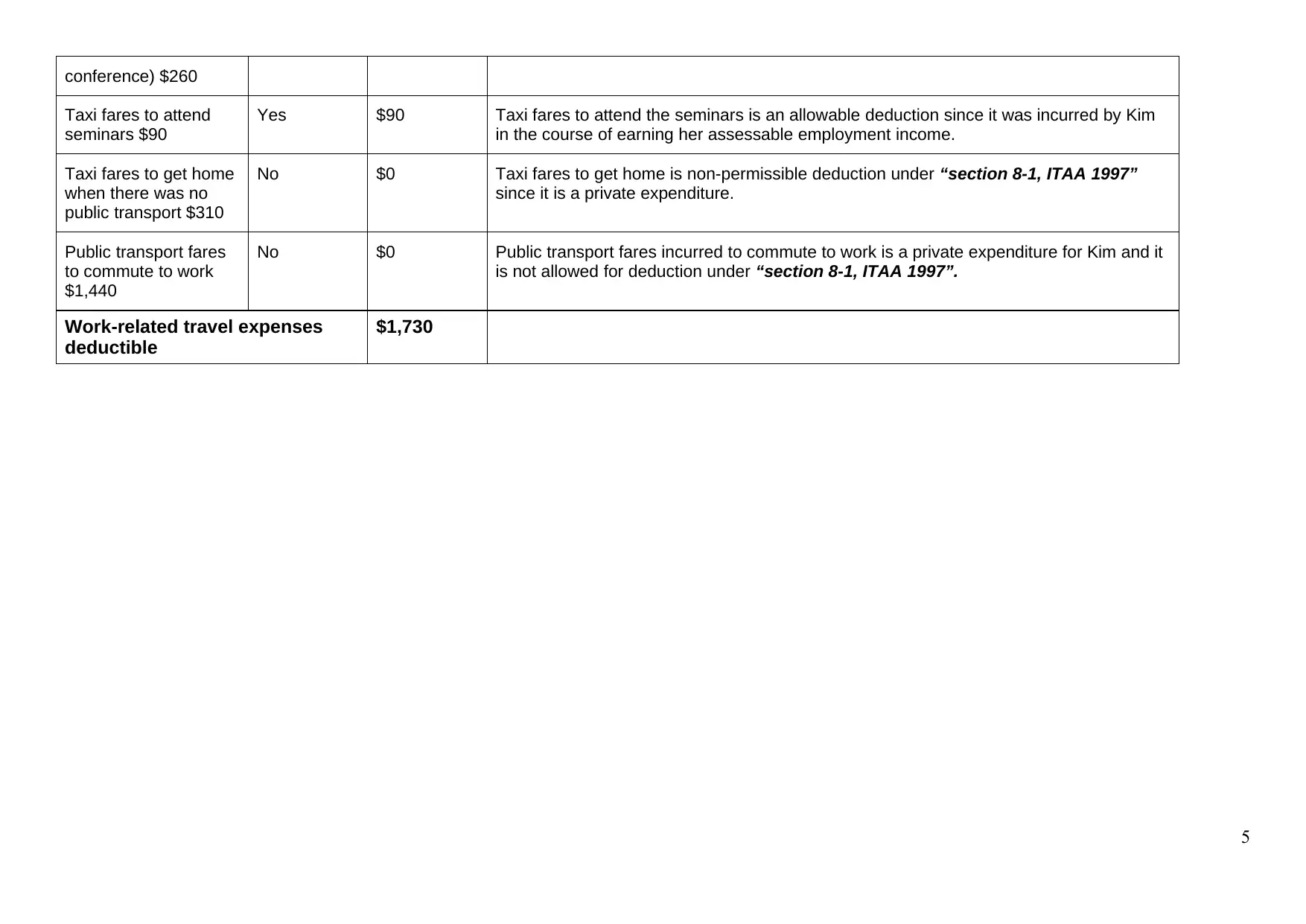

Item D2 – Work-related Travel Expenses

Expenses Deductible

or not?

Amount

deductible

Reasons/law (including references to relevant tax ruling/s)

Flights to Melbourne

for conference $540

Yes $540 Cost incurred for attending the conferences that are related to work are allowed as

deductions. As per “Taxation Ruling of TR 98/9” self-education expenses are allowed

for deduction in which the taxpayer is presently engaged. The cost incurred on flights,

accommodation, meals and sustenance is allowable deduction for Kim under “section 8-

1, ITAA 1997”.

Accommodation at

hotel $700

Yes $700

Meals and sustenance

$140

Yes $140

Taxi travel to and from

the airports (to attend

Yes $260 The taxi travel to attend conference is allowed for deduction under “section 8-1, ITAA

1997” because it is occurred in derivation of assessable income.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

conference) $260

Taxi fares to attend

seminars $90

Yes $90 Taxi fares to attend the seminars is an allowable deduction since it was incurred by Kim

in the course of earning her assessable employment income.

Taxi fares to get home

when there was no

public transport $310

No $0 Taxi fares to get home is non-permissible deduction under “section 8-1, ITAA 1997”

since it is a private expenditure.

Public transport fares

to commute to work

$1,440

No $0 Public transport fares incurred to commute to work is a private expenditure for Kim and it

is not allowed for deduction under “section 8-1, ITAA 1997”.

Work-related travel expenses

deductible

$1,730

5

Taxi fares to attend

seminars $90

Yes $90 Taxi fares to attend the seminars is an allowable deduction since it was incurred by Kim

in the course of earning her assessable employment income.

Taxi fares to get home

when there was no

public transport $310

No $0 Taxi fares to get home is non-permissible deduction under “section 8-1, ITAA 1997”

since it is a private expenditure.

Public transport fares

to commute to work

$1,440

No $0 Public transport fares incurred to commute to work is a private expenditure for Kim and it

is not allowed for deduction under “section 8-1, ITAA 1997”.

Work-related travel expenses

deductible

$1,730

5

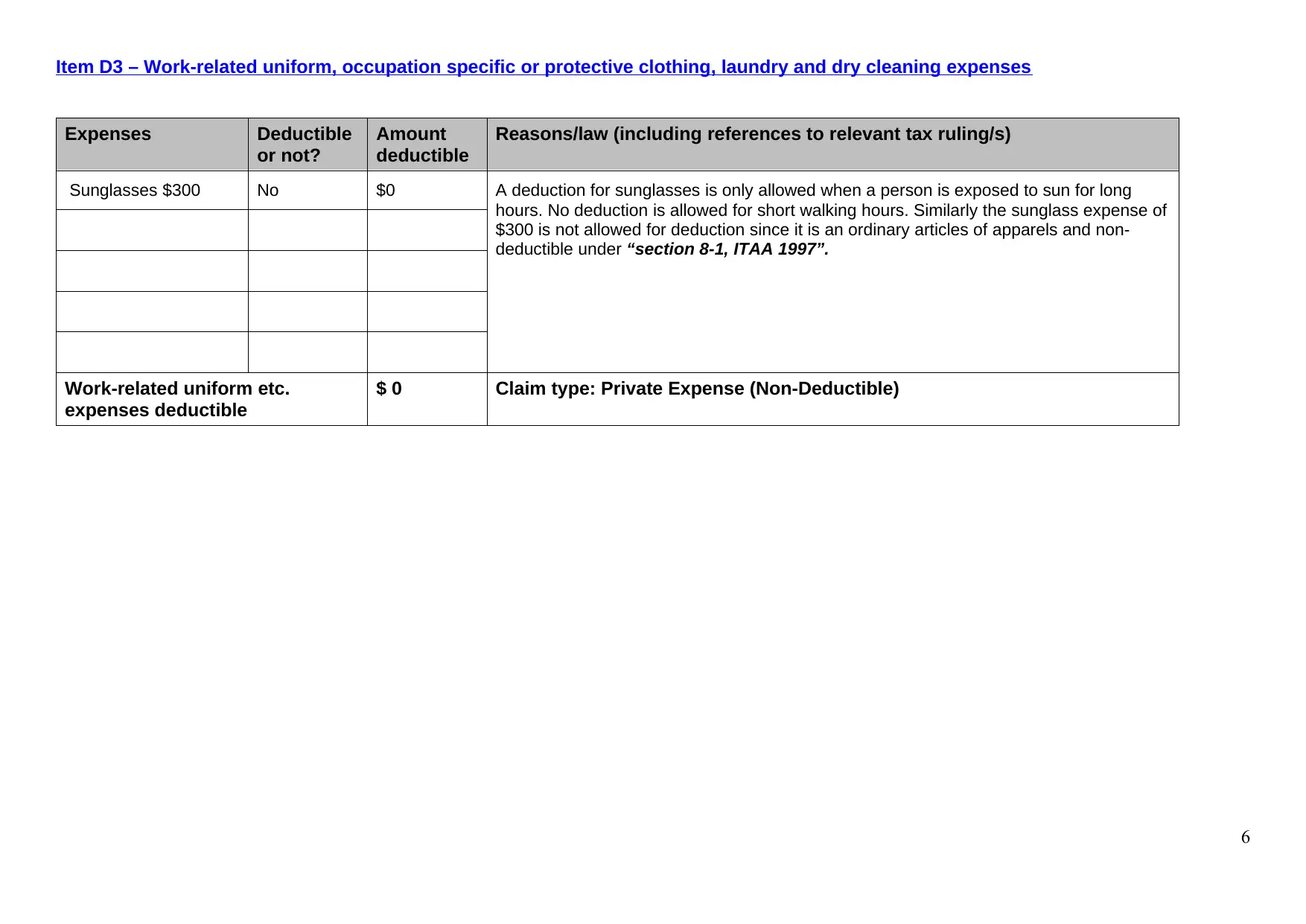

Item D3 – Work-related uniform, occupation specific or protective clothing, laundry and dry cleaning expenses

Expenses Deductible

or not?

Amount

deductible

Reasons/law (including references to relevant tax ruling/s)

Sunglasses $300 No $0 A deduction for sunglasses is only allowed when a person is exposed to sun for long

hours. No deduction is allowed for short walking hours. Similarly the sunglass expense of

$300 is not allowed for deduction since it is an ordinary articles of apparels and non-

deductible under “section 8-1, ITAA 1997”.

Work-related uniform etc.

expenses deductible

$ 0 Claim type: Private Expense (Non-Deductible)

6

Expenses Deductible

or not?

Amount

deductible

Reasons/law (including references to relevant tax ruling/s)

Sunglasses $300 No $0 A deduction for sunglasses is only allowed when a person is exposed to sun for long

hours. No deduction is allowed for short walking hours. Similarly the sunglass expense of

$300 is not allowed for deduction since it is an ordinary articles of apparels and non-

deductible under “section 8-1, ITAA 1997”.

Work-related uniform etc.

expenses deductible

$ 0 Claim type: Private Expense (Non-Deductible)

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

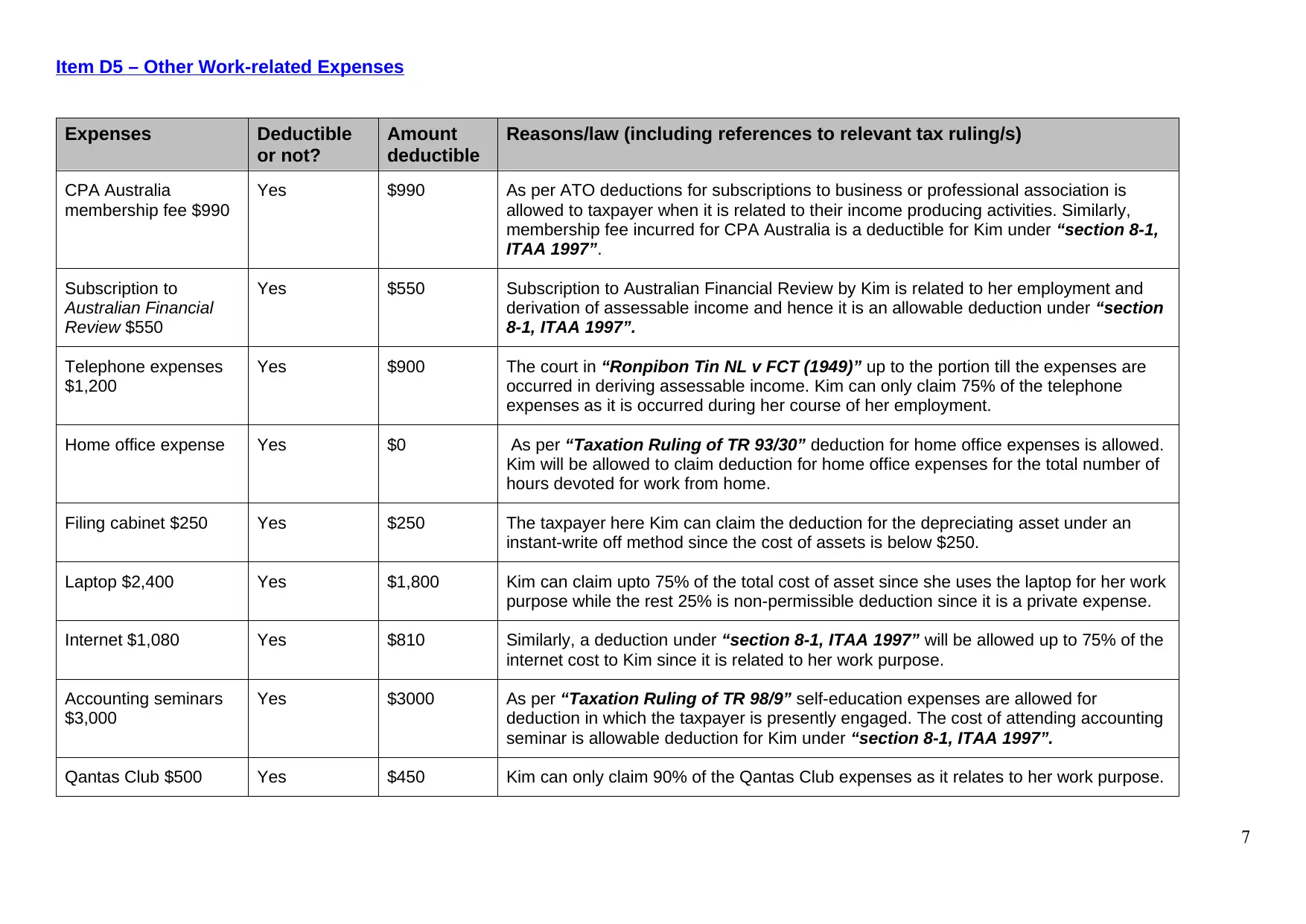

Item D5 – Other Work-related Expenses

Expenses Deductible

or not?

Amount

deductible

Reasons/law (including references to relevant tax ruling/s)

CPA Australia

membership fee $990

Yes $990 As per ATO deductions for subscriptions to business or professional association is

allowed to taxpayer when it is related to their income producing activities. Similarly,

membership fee incurred for CPA Australia is a deductible for Kim under “section 8-1,

ITAA 1997”.

Subscription to

Australian Financial

Review $550

Yes $550 Subscription to Australian Financial Review by Kim is related to her employment and

derivation of assessable income and hence it is an allowable deduction under “section

8-1, ITAA 1997”.

Telephone expenses

$1,200

Yes $900 The court in “Ronpibon Tin NL v FCT (1949)” up to the portion till the expenses are

occurred in deriving assessable income. Kim can only claim 75% of the telephone

expenses as it is occurred during her course of her employment.

Home office expense Yes $0 As per “Taxation Ruling of TR 93/30” deduction for home office expenses is allowed.

Kim will be allowed to claim deduction for home office expenses for the total number of

hours devoted for work from home.

Filing cabinet $250 Yes $250 The taxpayer here Kim can claim the deduction for the depreciating asset under an

instant-write off method since the cost of assets is below $250.

Laptop $2,400 Yes $1,800 Kim can claim upto 75% of the total cost of asset since she uses the laptop for her work

purpose while the rest 25% is non-permissible deduction since it is a private expense.

Internet $1,080 Yes $810 Similarly, a deduction under “section 8-1, ITAA 1997” will be allowed up to 75% of the

internet cost to Kim since it is related to her work purpose.

Accounting seminars

$3,000

Yes $3000 As per “Taxation Ruling of TR 98/9” self-education expenses are allowed for

deduction in which the taxpayer is presently engaged. The cost of attending accounting

seminar is allowable deduction for Kim under “section 8-1, ITAA 1997”.

Qantas Club $500 Yes $450 Kim can only claim 90% of the Qantas Club expenses as it relates to her work purpose.

7

Expenses Deductible

or not?

Amount

deductible

Reasons/law (including references to relevant tax ruling/s)

CPA Australia

membership fee $990

Yes $990 As per ATO deductions for subscriptions to business or professional association is

allowed to taxpayer when it is related to their income producing activities. Similarly,

membership fee incurred for CPA Australia is a deductible for Kim under “section 8-1,

ITAA 1997”.

Subscription to

Australian Financial

Review $550

Yes $550 Subscription to Australian Financial Review by Kim is related to her employment and

derivation of assessable income and hence it is an allowable deduction under “section

8-1, ITAA 1997”.

Telephone expenses

$1,200

Yes $900 The court in “Ronpibon Tin NL v FCT (1949)” up to the portion till the expenses are

occurred in deriving assessable income. Kim can only claim 75% of the telephone

expenses as it is occurred during her course of her employment.

Home office expense Yes $0 As per “Taxation Ruling of TR 93/30” deduction for home office expenses is allowed.

Kim will be allowed to claim deduction for home office expenses for the total number of

hours devoted for work from home.

Filing cabinet $250 Yes $250 The taxpayer here Kim can claim the deduction for the depreciating asset under an

instant-write off method since the cost of assets is below $250.

Laptop $2,400 Yes $1,800 Kim can claim upto 75% of the total cost of asset since she uses the laptop for her work

purpose while the rest 25% is non-permissible deduction since it is a private expense.

Internet $1,080 Yes $810 Similarly, a deduction under “section 8-1, ITAA 1997” will be allowed up to 75% of the

internet cost to Kim since it is related to her work purpose.

Accounting seminars

$3,000

Yes $3000 As per “Taxation Ruling of TR 98/9” self-education expenses are allowed for

deduction in which the taxpayer is presently engaged. The cost of attending accounting

seminar is allowable deduction for Kim under “section 8-1, ITAA 1997”.

Qantas Club $500 Yes $450 Kim can only claim 90% of the Qantas Club expenses as it relates to her work purpose.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

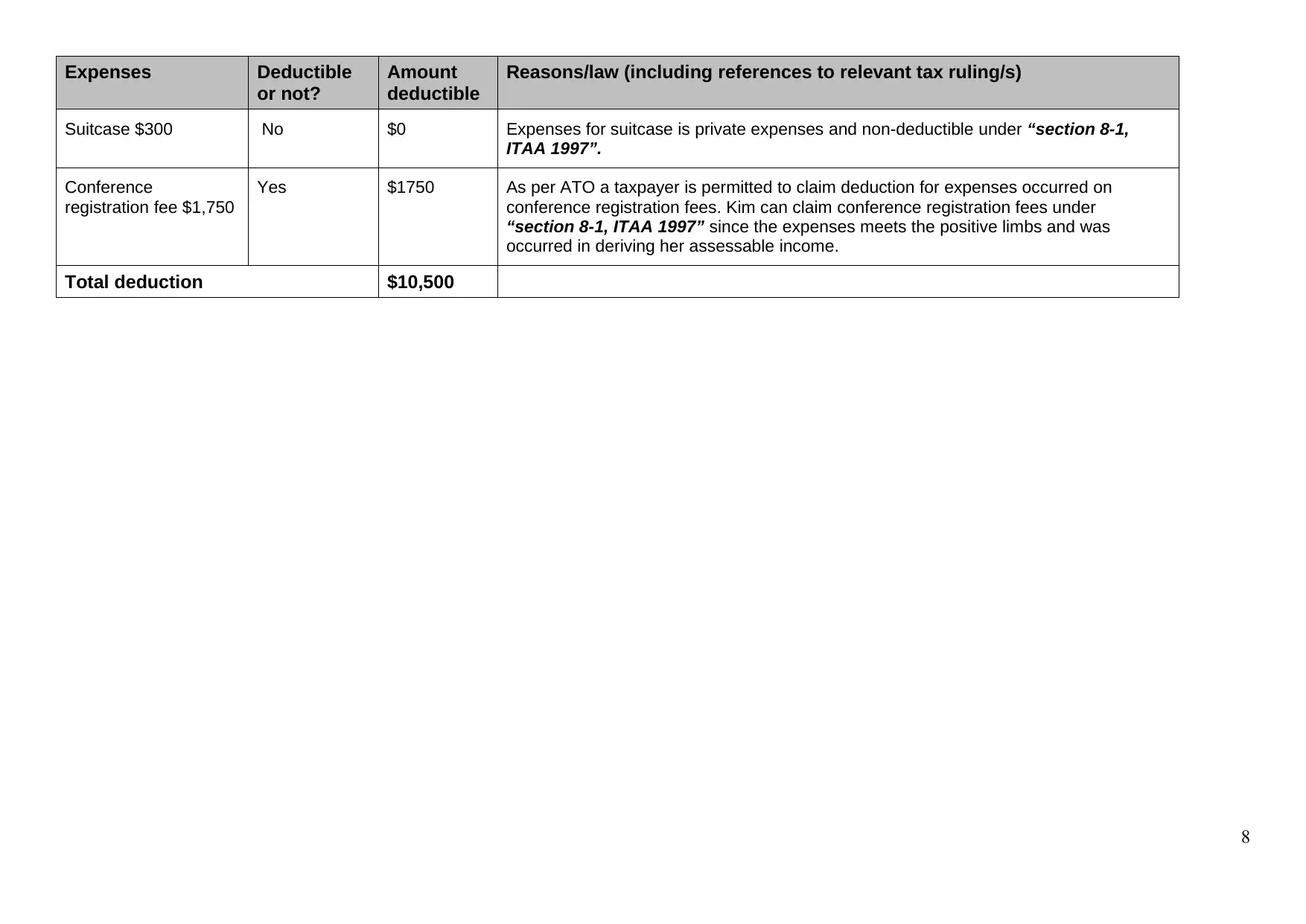

Expenses Deductible

or not?

Amount

deductible

Reasons/law (including references to relevant tax ruling/s)

Suitcase $300 No $0 Expenses for suitcase is private expenses and non-deductible under “section 8-1,

ITAA 1997”.

Conference

registration fee $1,750

Yes $1750 As per ATO a taxpayer is permitted to claim deduction for expenses occurred on

conference registration fees. Kim can claim conference registration fees under

“section 8-1, ITAA 1997” since the expenses meets the positive limbs and was

occurred in deriving her assessable income.

Total deduction $10,500

8

or not?

Amount

deductible

Reasons/law (including references to relevant tax ruling/s)

Suitcase $300 No $0 Expenses for suitcase is private expenses and non-deductible under “section 8-1,

ITAA 1997”.

Conference

registration fee $1,750

Yes $1750 As per ATO a taxpayer is permitted to claim deduction for expenses occurred on

conference registration fees. Kim can claim conference registration fees under

“section 8-1, ITAA 1997” since the expenses meets the positive limbs and was

occurred in deriving her assessable income.

Total deduction $10,500

8

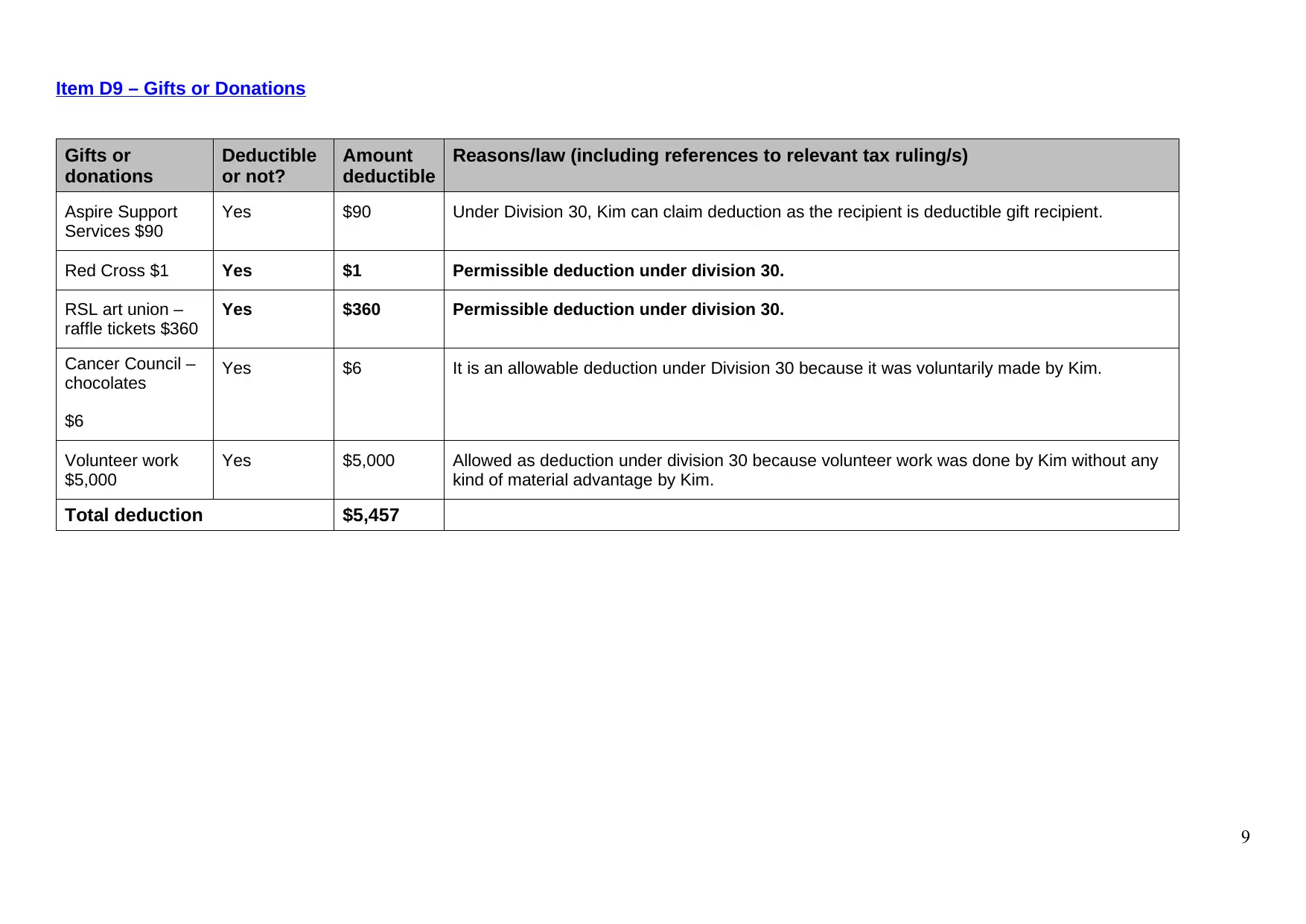

Item D9 – Gifts or Donations

Gifts or

donations

Deductible

or not?

Amount

deductible

Reasons/law (including references to relevant tax ruling/s)

Aspire Support

Services $90

Yes $90 Under Division 30, Kim can claim deduction as the recipient is deductible gift recipient.

Red Cross $1 Yes $1 Permissible deduction under division 30.

RSL art union –

raffle tickets $360

Yes $360 Permissible deduction under division 30.

Cancer Council –

chocolates

$6

Yes $6 It is an allowable deduction under Division 30 because it was voluntarily made by Kim.

Volunteer work

$5,000

Yes $5,000 Allowed as deduction under division 30 because volunteer work was done by Kim without any

kind of material advantage by Kim.

Total deduction $5,457

9

Gifts or

donations

Deductible

or not?

Amount

deductible

Reasons/law (including references to relevant tax ruling/s)

Aspire Support

Services $90

Yes $90 Under Division 30, Kim can claim deduction as the recipient is deductible gift recipient.

Red Cross $1 Yes $1 Permissible deduction under division 30.

RSL art union –

raffle tickets $360

Yes $360 Permissible deduction under division 30.

Cancer Council –

chocolates

$6

Yes $6 It is an allowable deduction under Division 30 because it was voluntarily made by Kim.

Volunteer work

$5,000

Yes $5,000 Allowed as deduction under division 30 because volunteer work was done by Kim without any

kind of material advantage by Kim.

Total deduction $5,457

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

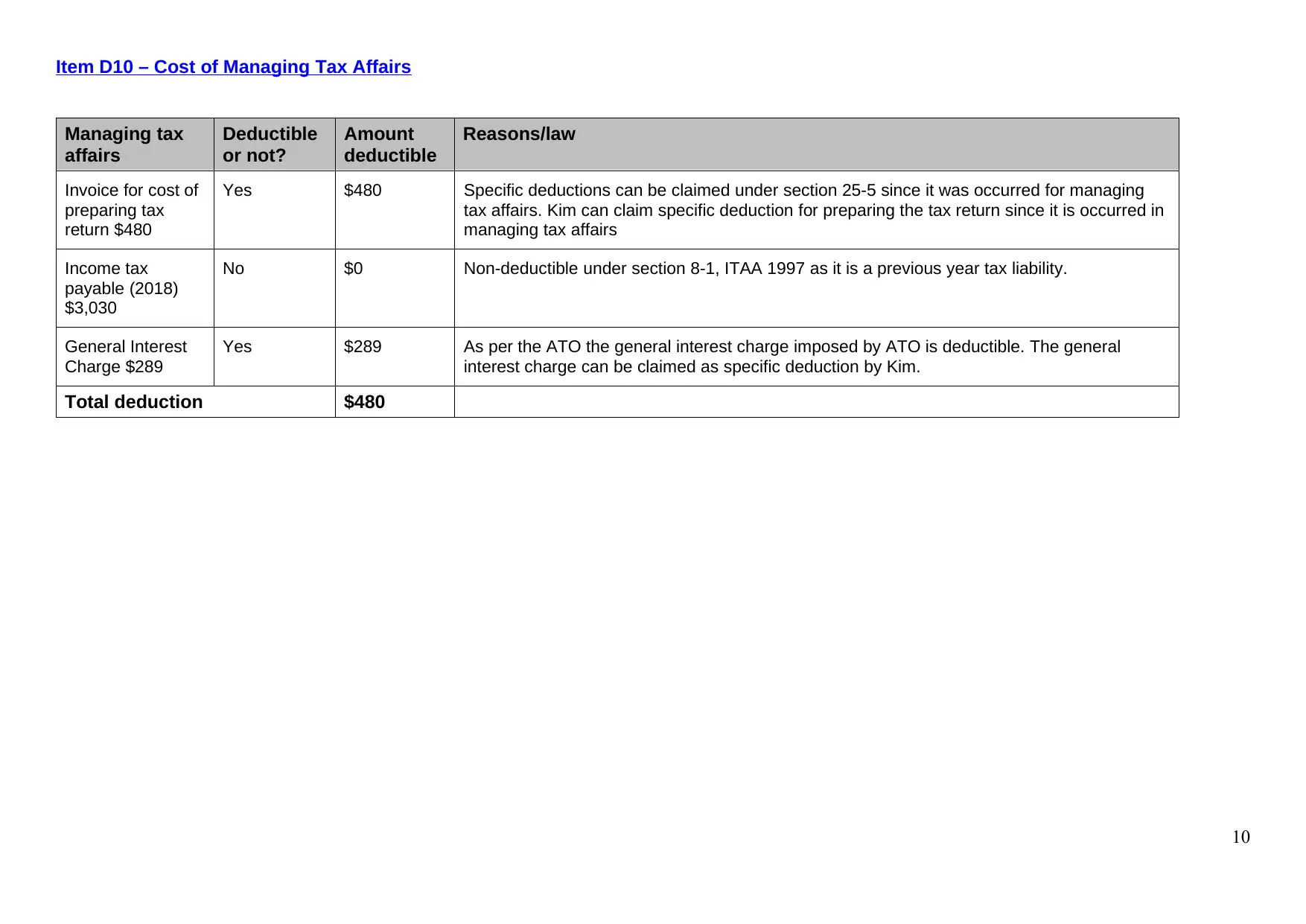

Item D10 – Cost of Managing Tax Affairs

Managing tax

affairs

Deductible

or not?

Amount

deductible

Reasons/law

Invoice for cost of

preparing tax

return $480

Yes $480 Specific deductions can be claimed under section 25-5 since it was occurred for managing

tax affairs. Kim can claim specific deduction for preparing the tax return since it is occurred in

managing tax affairs

Income tax

payable (2018)

$3,030

No $0 Non-deductible under section 8-1, ITAA 1997 as it is a previous year tax liability.

General Interest

Charge $289

Yes $289 As per the ATO the general interest charge imposed by ATO is deductible. The general

interest charge can be claimed as specific deduction by Kim.

Total deduction $480

10

Managing tax

affairs

Deductible

or not?

Amount

deductible

Reasons/law

Invoice for cost of

preparing tax

return $480

Yes $480 Specific deductions can be claimed under section 25-5 since it was occurred for managing

tax affairs. Kim can claim specific deduction for preparing the tax return since it is occurred in

managing tax affairs

Income tax

payable (2018)

$3,030

No $0 Non-deductible under section 8-1, ITAA 1997 as it is a previous year tax liability.

General Interest

Charge $289

Yes $289 As per the ATO the general interest charge imposed by ATO is deductible. The general

interest charge can be claimed as specific deduction by Kim.

Total deduction $480

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

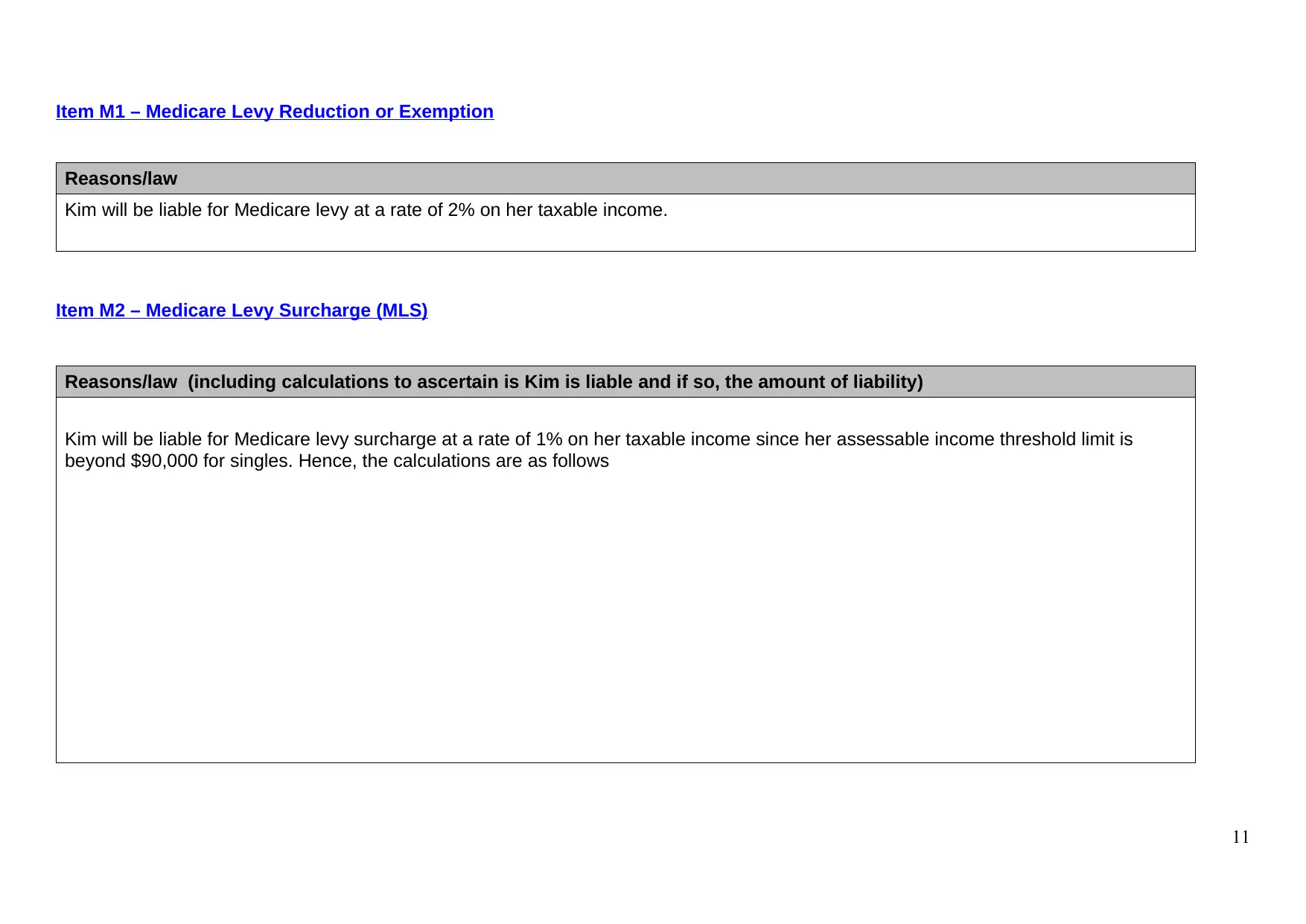

Item M1 – Medicare Levy Reduction or Exemption

Reasons/law

Kim will be liable for Medicare levy at a rate of 2% on her taxable income.

Item M2 – Medicare Levy Surcharge (MLS)

Reasons/law (including calculations to ascertain is Kim is liable and if so, the amount of liability)

Kim will be liable for Medicare levy surcharge at a rate of 1% on her taxable income since her assessable income threshold limit is

beyond $90,000 for singles. Hence, the calculations are as follows

11

Reasons/law

Kim will be liable for Medicare levy at a rate of 2% on her taxable income.

Item M2 – Medicare Levy Surcharge (MLS)

Reasons/law (including calculations to ascertain is Kim is liable and if so, the amount of liability)

Kim will be liable for Medicare levy surcharge at a rate of 1% on her taxable income since her assessable income threshold limit is

beyond $90,000 for singles. Hence, the calculations are as follows

11

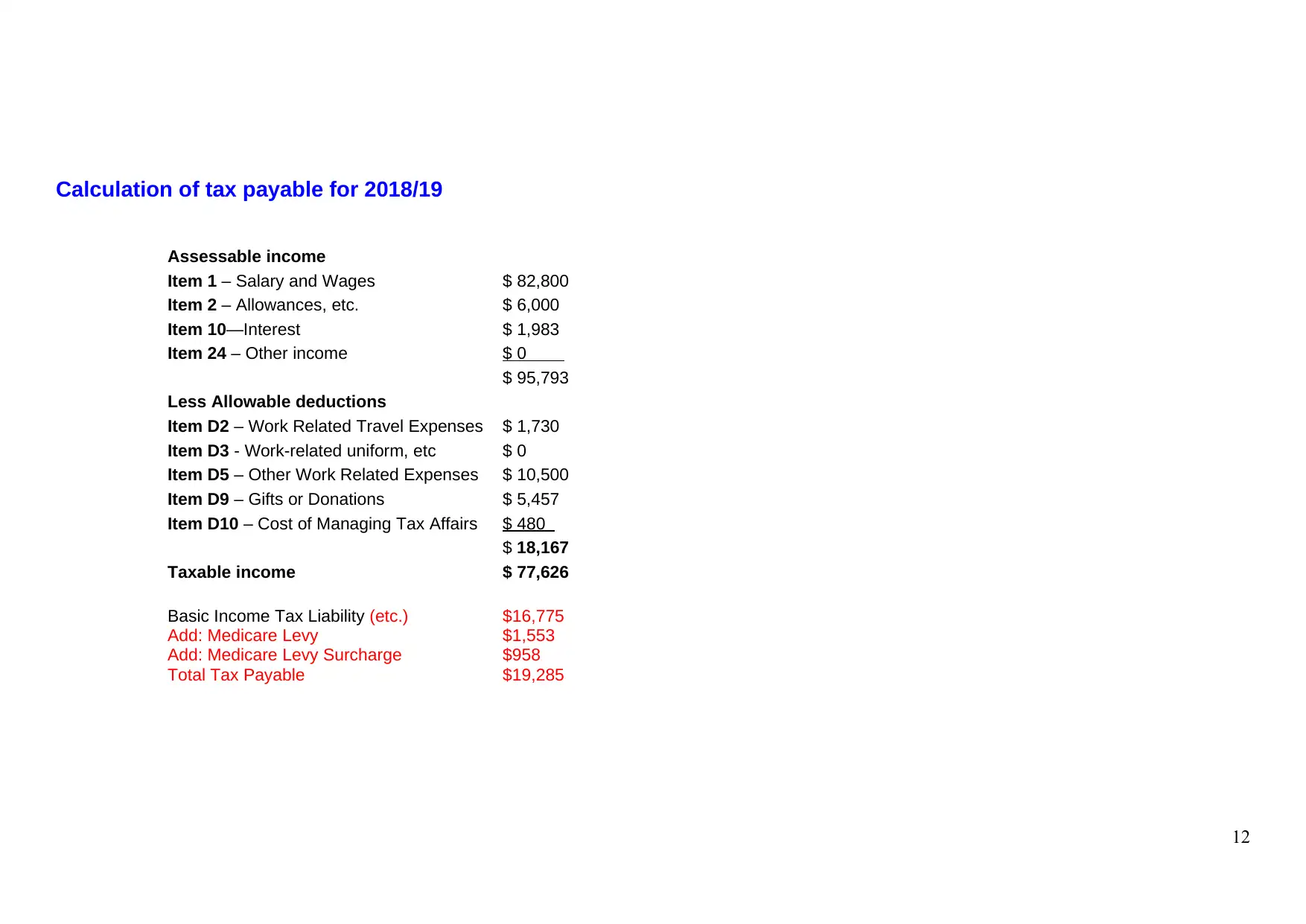

Calculation of tax payable for 2018/19

Assessable income

Item 1 – Salary and Wages $ 82,800

Item 2 – Allowances, etc. $ 6,000

Item 10—Interest $ 1,983

Item 24 – Other income $ 0

$ 95,793

Less Allowable deductions

Item D2 – Work Related Travel Expenses $ 1,730

Item D3 - Work-related uniform, etc $ 0

Item D5 – Other Work Related Expenses $ 10,500

Item D9 – Gifts or Donations $ 5,457

Item D10 – Cost of Managing Tax Affairs $ 480

$ 18,167

Taxable income $ 77,626

Basic Income Tax Liability (etc.) $16,775

Add: Medicare Levy $1,553

Add: Medicare Levy Surcharge $958

Total Tax Payable $19,285

12

Assessable income

Item 1 – Salary and Wages $ 82,800

Item 2 – Allowances, etc. $ 6,000

Item 10—Interest $ 1,983

Item 24 – Other income $ 0

$ 95,793

Less Allowable deductions

Item D2 – Work Related Travel Expenses $ 1,730

Item D3 - Work-related uniform, etc $ 0

Item D5 – Other Work Related Expenses $ 10,500

Item D9 – Gifts or Donations $ 5,457

Item D10 – Cost of Managing Tax Affairs $ 480

$ 18,167

Taxable income $ 77,626

Basic Income Tax Liability (etc.) $16,775

Add: Medicare Levy $1,553

Add: Medicare Levy Surcharge $958

Total Tax Payable $19,285

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.