BA317: Exploring Deduction Rules & Income Tax Regimes in Australia

VerifiedAdded on 2023/06/04

|10

|674

|267

Report

AI Summary

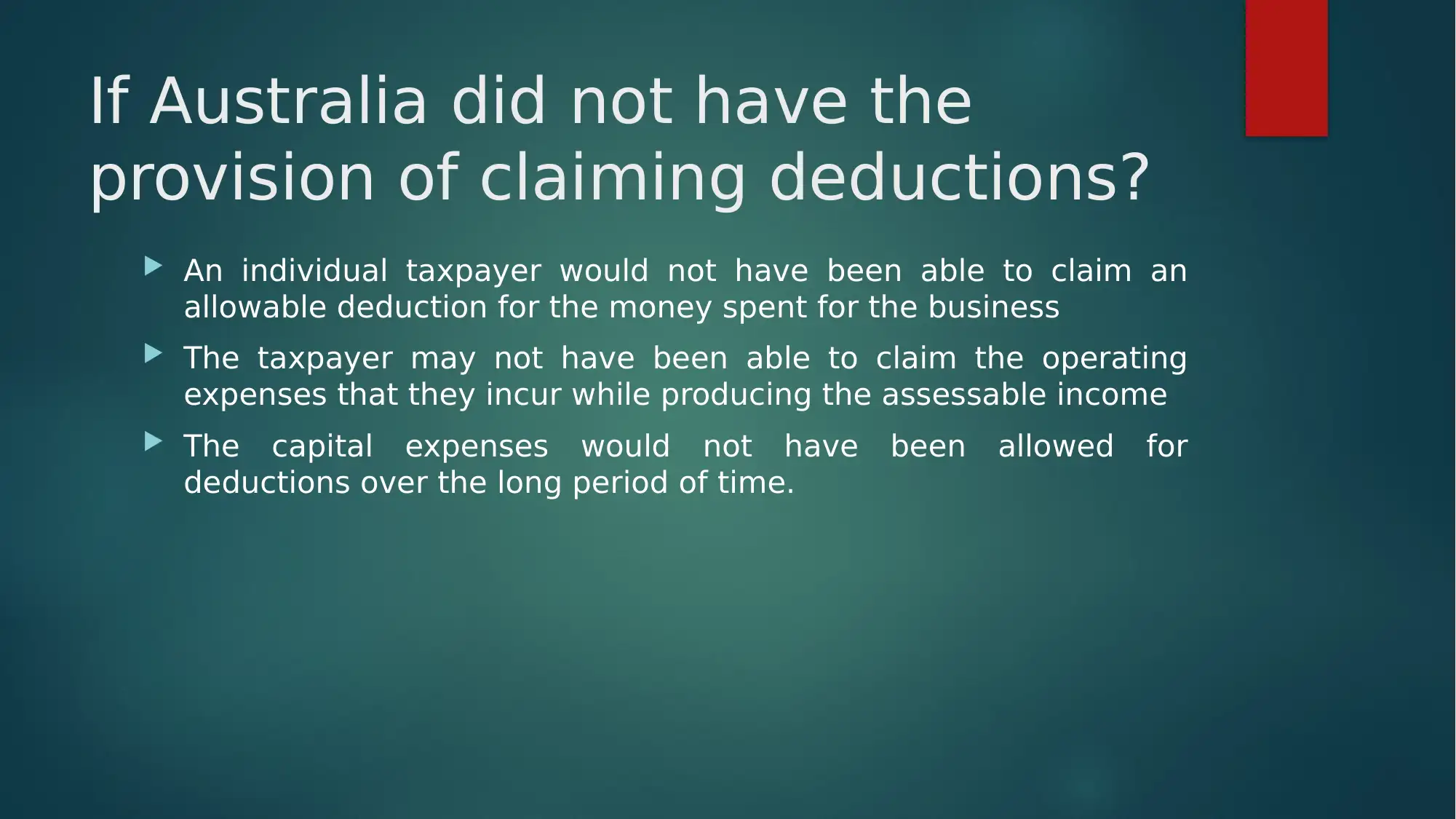

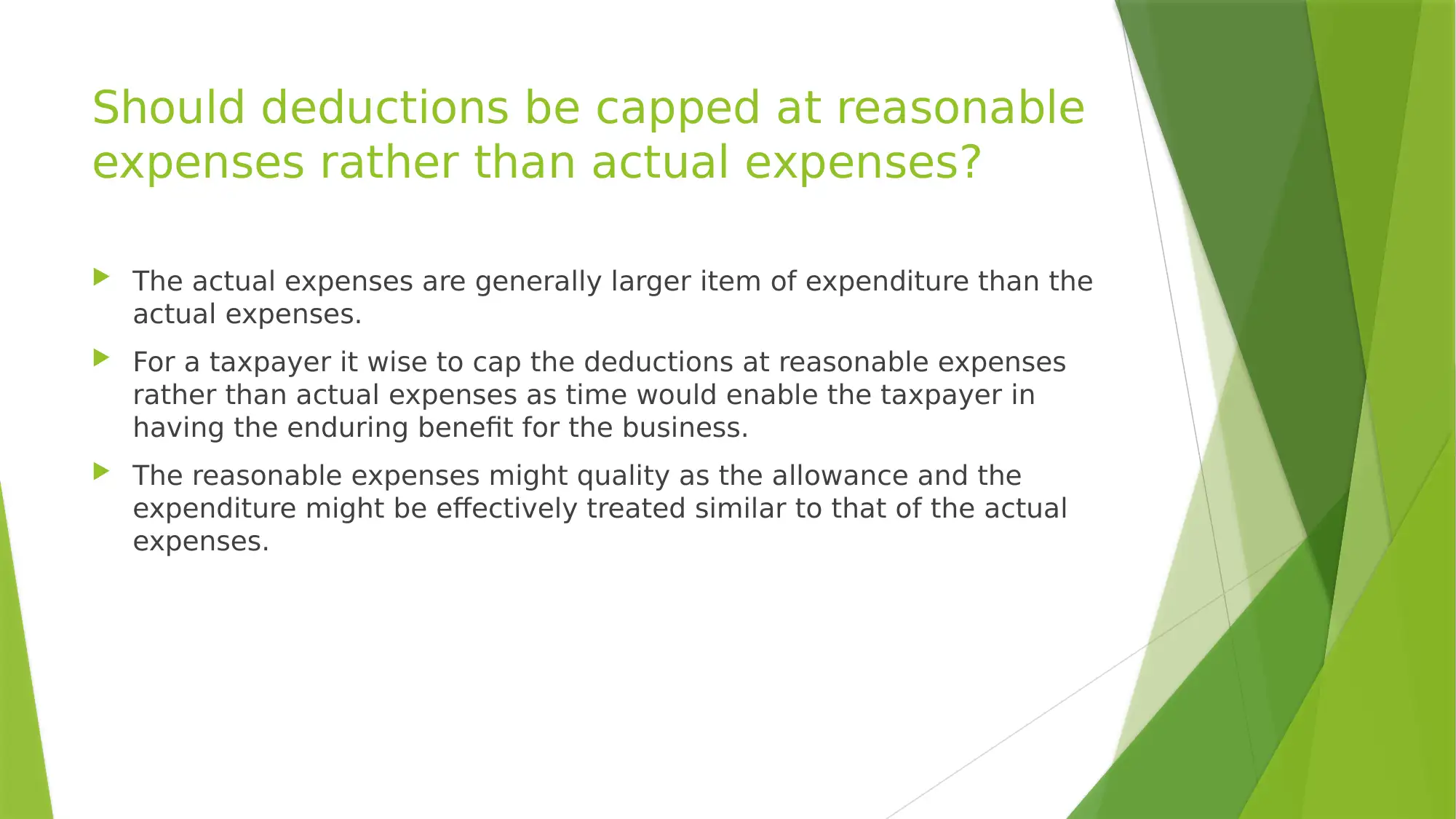

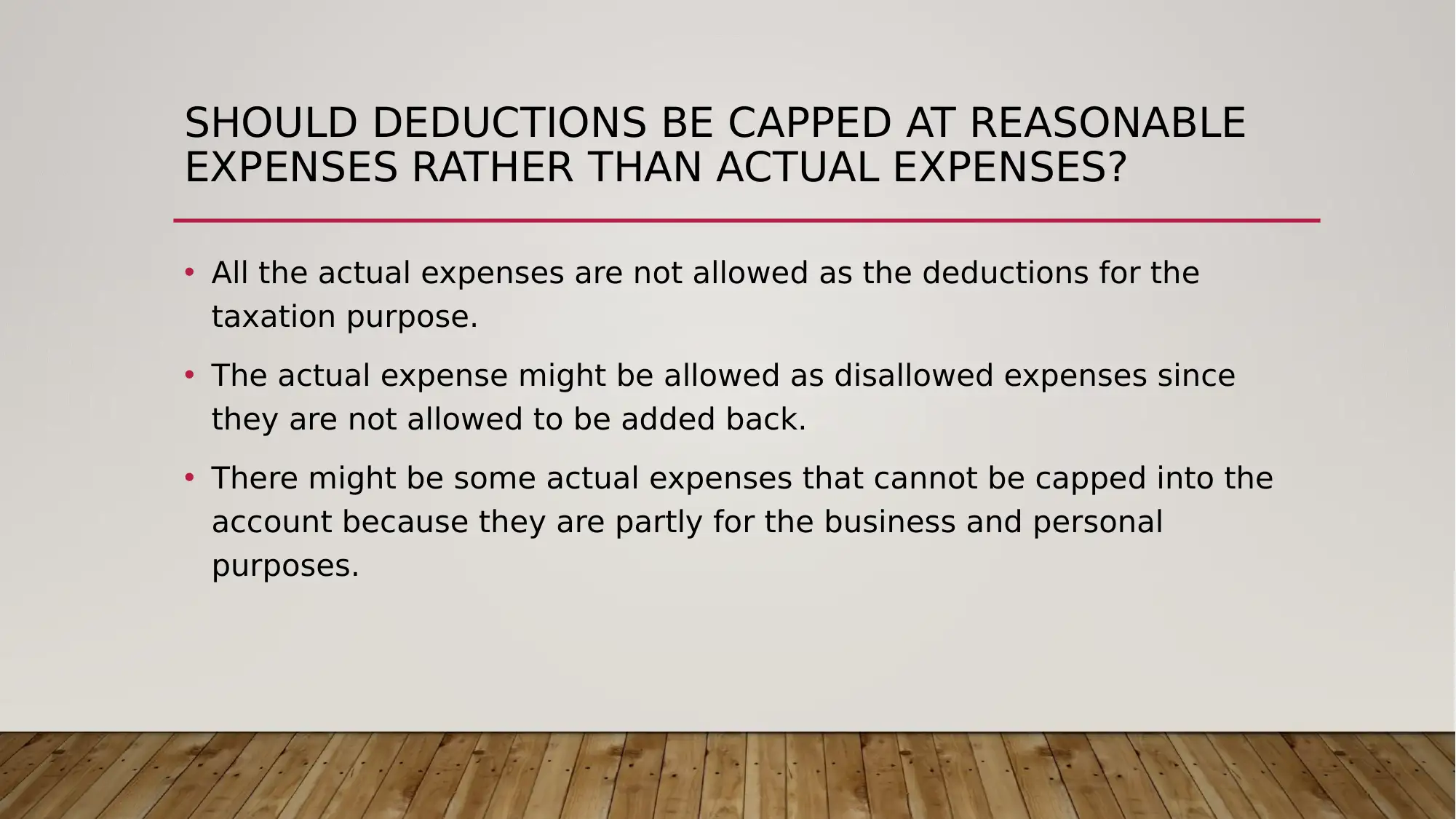

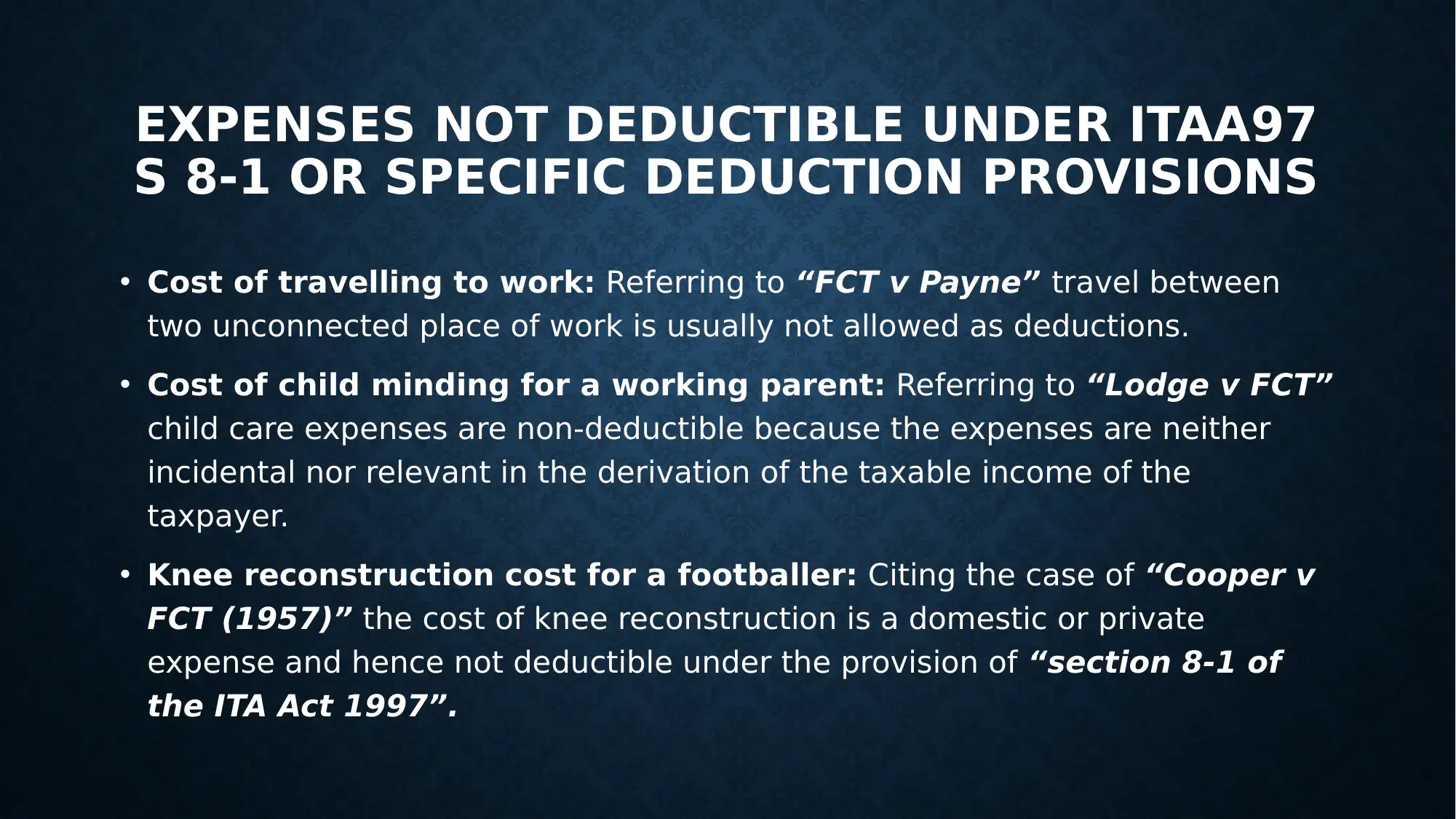

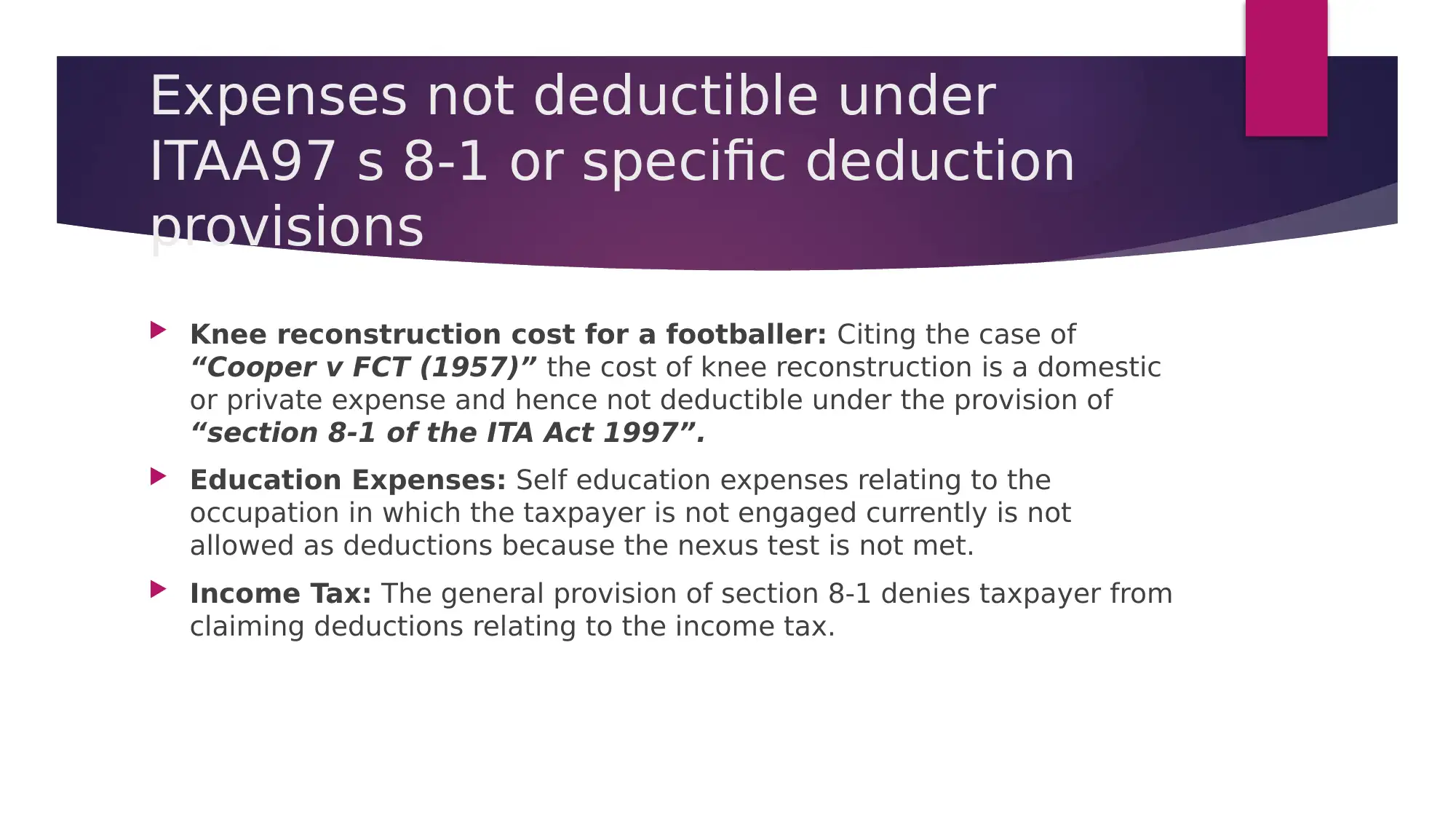

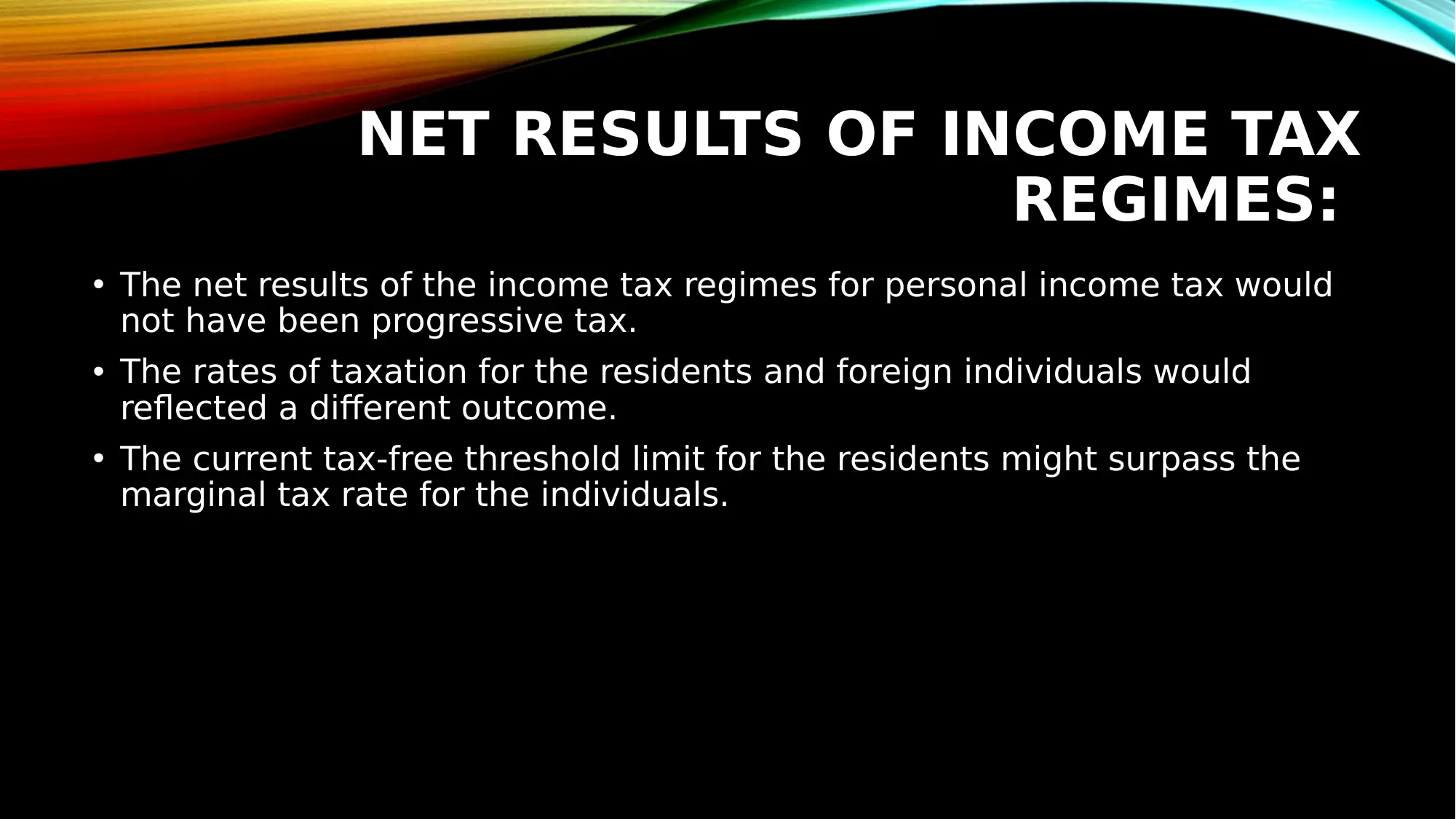

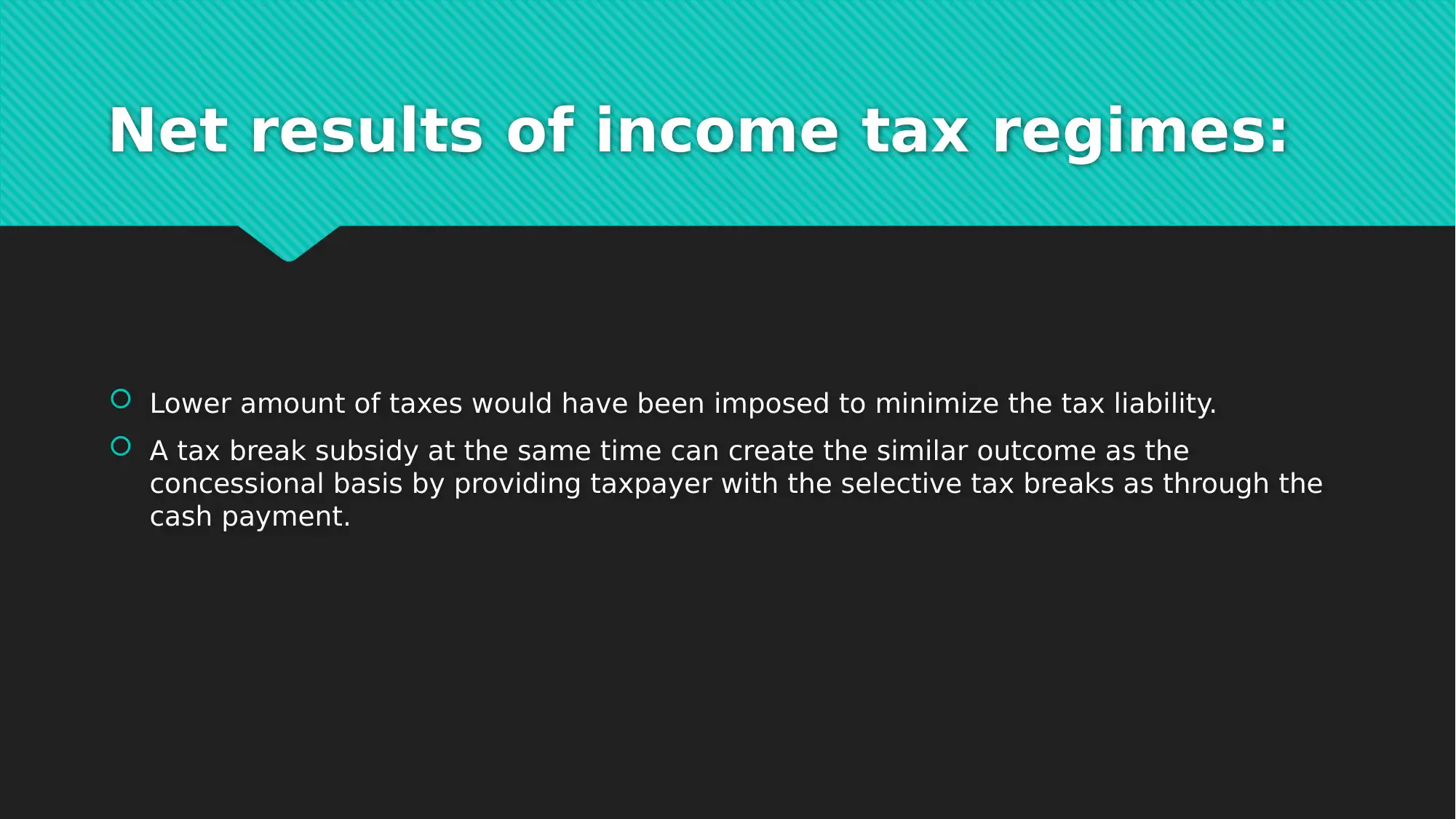

This report provides an analysis of deduction provisions in Australian taxation law. It discusses the implications of not having deduction provisions, the capping of deductions at reasonable expenses, and expenses not deductible under ITAA97 s 8-1, citing relevant case laws such as FCT v Payne and Cooper v FCT (1957). The report also examines the net results of income tax regimes, the impact of tax breaks, and the role of the tax-free threshold in minimizing tax liability. It concludes by emphasizing the importance of the tax-free threshold in addressing taxpayer liabilities.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.