Taxation Law: Analysis of Practical Cases Under Australian Law

VerifiedAdded on 2023/06/03

|15

|3606

|165

Report

AI Summary

This report provides a detailed analysis of taxation law in Australia through several case studies. The first case examines lottery winnings and whether they constitute taxable income under the Income Tax Assessment Act 1997. The second case calculates the taxable income of a pharmacy using accrual accounting, considering various revenue and expenditure items. The third case discusses the landmark Inland Revenue Commissioners v Duke of Westminster case, analyzing its relevance to modern Australian tax law. Finally, the fourth case addresses the apportionment of rental property losses and capital gains between joint owners. The report applies relevant legal principles and provisions to each scenario, offering clear conclusions based on Australian tax law.

Running head: TAXATION LAW

Taxation Law

Name of the Student:

Name of the University:

Authors Note:

Taxation Law

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

TAXATION LAW

Contents

Introduction:....................................................................................................................................2

Answer to question 1:......................................................................................................................2

Answer to question 2:......................................................................................................................4

Answer to question 3:......................................................................................................................7

Answer to question 4:......................................................................................................................9

References:....................................................................................................................................12

TAXATION LAW

Contents

Introduction:....................................................................................................................................2

Answer to question 1:......................................................................................................................2

Answer to question 2:......................................................................................................................4

Answer to question 3:......................................................................................................................7

Answer to question 4:......................................................................................................................9

References:....................................................................................................................................12

2

TAXATION LAW

Introduction:

One of main sources of revenue for a country is the taxes that it collects from its citizens

including individual, corporate and other entities. In order to regulate the taxation matters in the

country each and every country has respective legislations. In Australia, earlier it was Income

Tax Assessment Act, 1936 that used to govern the provisions related to imposition and collection

of income tax by the country on tax payers. At present the Income Tax assessment Act, 1997,

here in after to be mentioned only as the act in this document, must be referred to in tax related

matters in the country. The provisions of the act along with other appropriate rules and

regulations shall be followed in dissecting the practical case studies that have been provided in

this document.

Answer to question 1:

Issue:

The first case study provides information about lottery winnings by a person. Whether the annual

payments received by the winner of the lottery contest conducted by the Lottery Commission of

Australia is income to the recipient is to be discussed here.

Rules:

As per the Income Tax Assessment Act, 1997 an individual will be liable to pay income tax on

the amount of his taxable income calculated as per the provisions of the act. The act further

clarified that the taxable income of an individual includes the following:

I. Income arising from salaries and wages.

II. Income received from commission.

TAXATION LAW

Introduction:

One of main sources of revenue for a country is the taxes that it collects from its citizens

including individual, corporate and other entities. In order to regulate the taxation matters in the

country each and every country has respective legislations. In Australia, earlier it was Income

Tax Assessment Act, 1936 that used to govern the provisions related to imposition and collection

of income tax by the country on tax payers. At present the Income Tax assessment Act, 1997,

here in after to be mentioned only as the act in this document, must be referred to in tax related

matters in the country. The provisions of the act along with other appropriate rules and

regulations shall be followed in dissecting the practical case studies that have been provided in

this document.

Answer to question 1:

Issue:

The first case study provides information about lottery winnings by a person. Whether the annual

payments received by the winner of the lottery contest conducted by the Lottery Commission of

Australia is income to the recipient is to be discussed here.

Rules:

As per the Income Tax Assessment Act, 1997 an individual will be liable to pay income tax on

the amount of his taxable income calculated as per the provisions of the act. The act further

clarified that the taxable income of an individual includes the following:

I. Income arising from salaries and wages.

II. Income received from commission.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

TAXATION LAW

III. Business income.

IV. Income from profession.

V. Capital gain, in case of capital loss the same shall be deducted only from capital gain amount

and not any other heads of income.

VI. Other income (Hoopes, Robinson and Slemrod, 2018).

Australian Taxation Office (ATO) has made it amply clear that a taxpayer must pay income tax

as per the applicable rate of income tax, based on his taxable income. In case a taxpayer

contravenes with the provisions of income tax as provided in the act then necessary penalty and

fines shall be imposed on the amount of income tax liability (Vann, 2016). ATO while defining

other income has specified in its website that other income as defined by the act shall include the

amount of prizes, awards and winnings from lottery provided the contest was held by any of the

following person:

I. The banker of the taxpayer.

II. The building society in which the taxpayer

III. Other investment body of the taxpayer.

IV. Credit union of the taxpayer (White and Townsend, 2018).

However, in case the lottery contest is ordinary lottery contest and drawn by any of the above

bodies then the winnings from such lottery contests will not be considered as ordinary income. In

such case the winnings from lottery will not be subjected to income tax.

Application:

‘Set for life’ is a lottery contest drawn by the Lottery Commission of Australia that will pay the

winner $50,000 immediately after the declaration of lottery contest. In addition the winner will

TAXATION LAW

III. Business income.

IV. Income from profession.

V. Capital gain, in case of capital loss the same shall be deducted only from capital gain amount

and not any other heads of income.

VI. Other income (Hoopes, Robinson and Slemrod, 2018).

Australian Taxation Office (ATO) has made it amply clear that a taxpayer must pay income tax

as per the applicable rate of income tax, based on his taxable income. In case a taxpayer

contravenes with the provisions of income tax as provided in the act then necessary penalty and

fines shall be imposed on the amount of income tax liability (Vann, 2016). ATO while defining

other income has specified in its website that other income as defined by the act shall include the

amount of prizes, awards and winnings from lottery provided the contest was held by any of the

following person:

I. The banker of the taxpayer.

II. The building society in which the taxpayer

III. Other investment body of the taxpayer.

IV. Credit union of the taxpayer (White and Townsend, 2018).

However, in case the lottery contest is ordinary lottery contest and drawn by any of the above

bodies then the winnings from such lottery contests will not be considered as ordinary income. In

such case the winnings from lottery will not be subjected to income tax.

Application:

‘Set for life’ is a lottery contest drawn by the Lottery Commission of Australia that will pay the

winner $50,000 immediately after the declaration of lottery contest. In addition the winner will

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

TAXATION LAW

also receive annual payment of $50,000 each year for next 19 years. The first of which shall be

paid immediately after a year from the date of payment of $50,000 immediately after the winner

of lottery contest was declared (Somers and Eynaud, 2015).

The above facts make it clear that the lottery contest was not drawn by the Lottery Commission

of Australia hence, the annual payment of $50,000 and also the initial amount of $50,000 paid

immediately after declaration of winner of the contest will not be taxable in the hands of the

winner of the contest or the recipient of the amount (Pistone, 2016).

Conclusion:

ATO has made it clear that the other income shall include lottery winnings provided the lottery

contest was held and drawn by the specific persons as mentioned, i.e. the bank, housing society,

investment bodies and credit unions of the tax payer. In this case since the lottery contest was

held by the Lottery Commission of Australia thus, the winnings is not subjected to income tax.

Hence, annual payment of $50,000 is not income to the winner or to the person receiving such

payment (Gainsbury, 2017).

Comment: Annual payment is not income.

Answer to question 2:

Assuming that the Corner Pharmacy uses accrual basis of accounting and it is allowed for

taxation purpose, the taxable amount of income of the pharmacy is calculated in the table below:

Items of revenue and expenditures Amount ($) Amount ($) Amount ($)

Revenue from cash sales 300,000.00

TAXATION LAW

also receive annual payment of $50,000 each year for next 19 years. The first of which shall be

paid immediately after a year from the date of payment of $50,000 immediately after the winner

of lottery contest was declared (Somers and Eynaud, 2015).

The above facts make it clear that the lottery contest was not drawn by the Lottery Commission

of Australia hence, the annual payment of $50,000 and also the initial amount of $50,000 paid

immediately after declaration of winner of the contest will not be taxable in the hands of the

winner of the contest or the recipient of the amount (Pistone, 2016).

Conclusion:

ATO has made it clear that the other income shall include lottery winnings provided the lottery

contest was held and drawn by the specific persons as mentioned, i.e. the bank, housing society,

investment bodies and credit unions of the tax payer. In this case since the lottery contest was

held by the Lottery Commission of Australia thus, the winnings is not subjected to income tax.

Hence, annual payment of $50,000 is not income to the winner or to the person receiving such

payment (Gainsbury, 2017).

Comment: Annual payment is not income.

Answer to question 2:

Assuming that the Corner Pharmacy uses accrual basis of accounting and it is allowed for

taxation purpose, the taxable amount of income of the pharmacy is calculated in the table below:

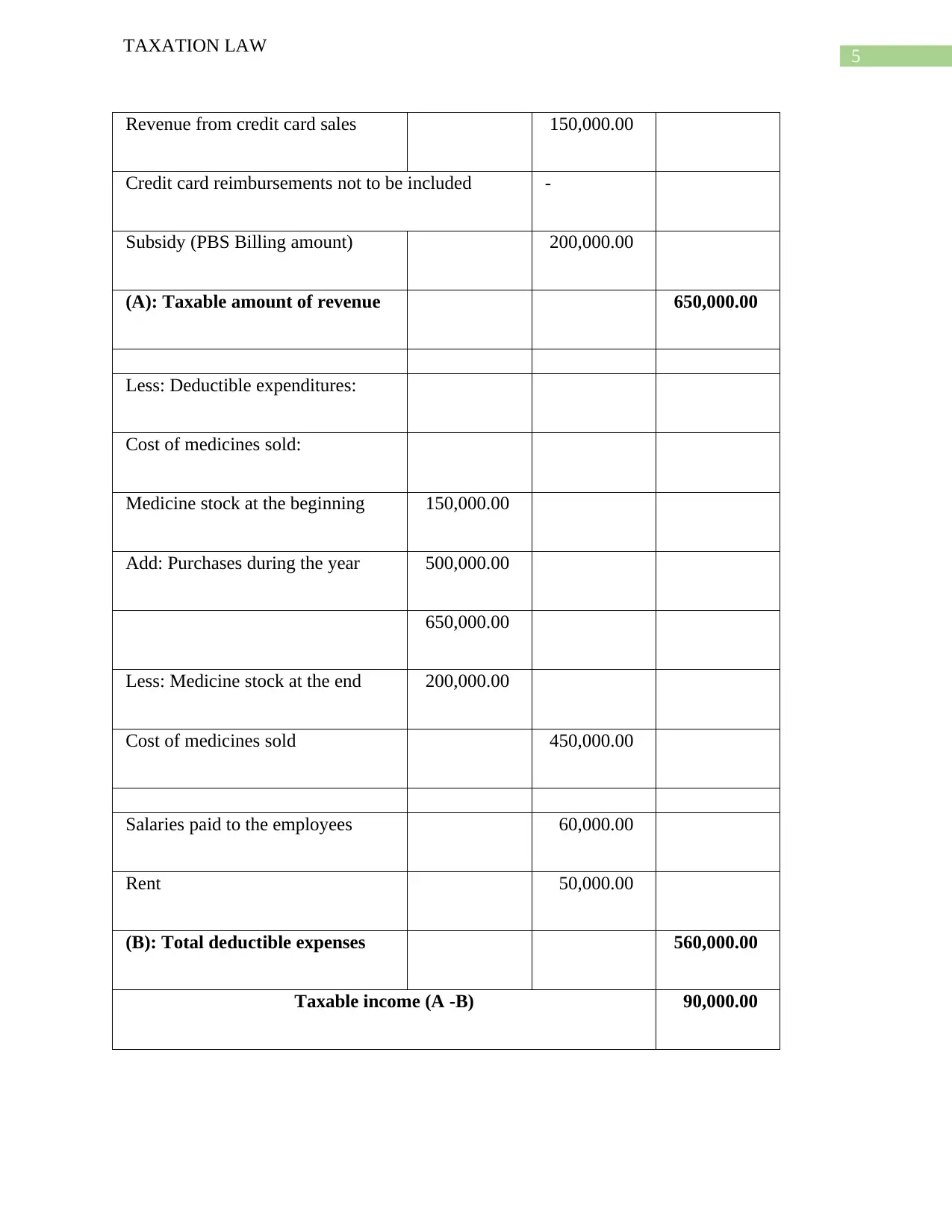

Items of revenue and expenditures Amount ($) Amount ($) Amount ($)

Revenue from cash sales 300,000.00

5

TAXATION LAW

Revenue from credit card sales 150,000.00

Credit card reimbursements not to be included -

Subsidy (PBS Billing amount) 200,000.00

(A): Taxable amount of revenue 650,000.00

Less: Deductible expenditures:

Cost of medicines sold:

Medicine stock at the beginning 150,000.00

Add: Purchases during the year 500,000.00

650,000.00

Less: Medicine stock at the end 200,000.00

Cost of medicines sold 450,000.00

Salaries paid to the employees 60,000.00

Rent 50,000.00

(B): Total deductible expenses 560,000.00

Taxable income (A -B) 90,000.00

TAXATION LAW

Revenue from credit card sales 150,000.00

Credit card reimbursements not to be included -

Subsidy (PBS Billing amount) 200,000.00

(A): Taxable amount of revenue 650,000.00

Less: Deductible expenditures:

Cost of medicines sold:

Medicine stock at the beginning 150,000.00

Add: Purchases during the year 500,000.00

650,000.00

Less: Medicine stock at the end 200,000.00

Cost of medicines sold 450,000.00

Salaries paid to the employees 60,000.00

Rent 50,000.00

(B): Total deductible expenses 560,000.00

Taxable income (A -B) 90,000.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

TAXATION LAW

Taxable income of Corner Pharmacy shop is $90,000 as per the accrual basis of accounting.

Thus, the pharmacy shop must pay tax on the amount of taxable income as per the rates

applicable to such income.

Important notes:

Revenue recognition for tax purposes:

Cash sales: Since the pharmacy follows accrual basis of accounting hence, sales of any kind has

to be included in determination of taxable income hence, the amount received from cash sales

has been included in determination of taxable income of the shop (Slemrod, 2016).

Sales on credit card: As mentioned in accrual basis of accounting the amount of revenue is

recognized as and when earned. Credit sales has been included to calculate the amount of taxable

income of the shop.

Credit card reimbursement: Reimbursement of credit card sales will not be included since credit

card sales has already been included to determine the amount of taxable income. Inclusion of

credit card reimbursement would have resulted in double taxation of revenue (Trad and

Freudenberg, 2018).

Subsidy under PBS scheme: Only the billing amount of PBS is to be considered for calculation

of taxable income due to accrual basis of accounting.

Deductible expenditures:

The Income Tax Assessment Act, 1997 provides that while computing the income from business

certain expenditures will be allowed as deduction. The expenditures that have been incurred

TAXATION LAW

Taxable income of Corner Pharmacy shop is $90,000 as per the accrual basis of accounting.

Thus, the pharmacy shop must pay tax on the amount of taxable income as per the rates

applicable to such income.

Important notes:

Revenue recognition for tax purposes:

Cash sales: Since the pharmacy follows accrual basis of accounting hence, sales of any kind has

to be included in determination of taxable income hence, the amount received from cash sales

has been included in determination of taxable income of the shop (Slemrod, 2016).

Sales on credit card: As mentioned in accrual basis of accounting the amount of revenue is

recognized as and when earned. Credit sales has been included to calculate the amount of taxable

income of the shop.

Credit card reimbursement: Reimbursement of credit card sales will not be included since credit

card sales has already been included to determine the amount of taxable income. Inclusion of

credit card reimbursement would have resulted in double taxation of revenue (Trad and

Freudenberg, 2018).

Subsidy under PBS scheme: Only the billing amount of PBS is to be considered for calculation

of taxable income due to accrual basis of accounting.

Deductible expenditures:

The Income Tax Assessment Act, 1997 provides that while computing the income from business

certain expenditures will be allowed as deduction. The expenditures that have been incurred

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

TAXATION LAW

exclusively to earn business income shall be fully allowed as deduction to ascertain the taxable

income from business (Menk, Nagle and Coss, 2017).

Cost of medicines sold: Cost of medicines sold is calculated by using the following formula.

{(opening stock + purchases) – closing stock} = cost goods sold.

Since cost of goods sold is directly related to the business and incurred wholly for the purpose of

business hence, the amount of cost of goods sold has been deducted from the amount of revenue

to calculate the taxable income of pharmacy shop.

Salaries: Corner Pharmacy has three assistants to run the day to day affairs in the working shop.

Assuming that the salaries amount of $60,000 is paid to the three assistants, the entire amount

shall be deducted from revenue of the business to ascertain taxable income of the pharmacy

(Miller-Nobles, Mattison and Matsumura, 2016).

Rent: Assuming the payment of rent is for the business premises, i.e. the pharmacy shop, it shall

be deducted fully from business revenue to calculate taxable income of the shop.

Answer to question 3:

INLAND REVENUE COMMISSIONERS V DUKE OF WESTMINSTER:

Almost 84 years have elapsed since Lord Tomil decided the case, IRC v Duke of Westminster

[1936] AC 1, in favour of the Duke of Westminster. However, the judgement till date remains a landmark

judgment due to the impact that was created subsequent to the delivery of the judgment (Goncharov and

Jacob, 2014).

The facts:

TAXATION LAW

exclusively to earn business income shall be fully allowed as deduction to ascertain the taxable

income from business (Menk, Nagle and Coss, 2017).

Cost of medicines sold: Cost of medicines sold is calculated by using the following formula.

{(opening stock + purchases) – closing stock} = cost goods sold.

Since cost of goods sold is directly related to the business and incurred wholly for the purpose of

business hence, the amount of cost of goods sold has been deducted from the amount of revenue

to calculate the taxable income of pharmacy shop.

Salaries: Corner Pharmacy has three assistants to run the day to day affairs in the working shop.

Assuming that the salaries amount of $60,000 is paid to the three assistants, the entire amount

shall be deducted from revenue of the business to ascertain taxable income of the pharmacy

(Miller-Nobles, Mattison and Matsumura, 2016).

Rent: Assuming the payment of rent is for the business premises, i.e. the pharmacy shop, it shall

be deducted fully from business revenue to calculate taxable income of the shop.

Answer to question 3:

INLAND REVENUE COMMISSIONERS V DUKE OF WESTMINSTER:

Almost 84 years have elapsed since Lord Tomil decided the case, IRC v Duke of Westminster

[1936] AC 1, in favour of the Duke of Westminster. However, the judgement till date remains a landmark

judgment due to the impact that was created subsequent to the delivery of the judgment (Goncharov and

Jacob, 2014).

The facts:

8

TAXATION LAW

The facts of the above case was about payment to gardener. Duke of Westminster used to pay weekly to

the gardener for his services. The substantial amount of payment made to the gardener was from after tax

income of the Duke. As a result the Duke was unable to take tax benefit on such amount. Later knowing

the existing provisions that allows such expenditure to be deducted. The Duke of Westminster drew up a

covenant to pay equivalent amount annually. As a result such annual payment was allowed as deduction

to compute taxable income of the Duke. However, Inland Revenue challenged the practice of the Duke of

Westminster by alleging that it was a tax avoidance strategy by the Duke of Westminster (Dhaliwal et.

al. 2017).

Decision:

Lord Tomlin decided the case in favour of the Duke by stating that a tax payer has the right to make use

of the existing tax provisions to minimize the tax liability by using proper means. There is nothing wrong

if the tax payer uses valid provisions of the income tax law to minimize the amount of income tax liability

of his or her. It would not correct to hold the person liable of tax avoidance practices for using income tax

provisions existing in the country would be grossly injustice. The Duke of Westminster has paid gardener

for his services and the same is allowed as the payment was made under a covenant thus, the entire

payment would be allowed as deduction for computation of Duke’s taxable income (Sikka, 2017).

In Lord Tomlin’s own word, “Every man is allowed to use valid tax provisions to reduce taxes under

appropriate acts. Such acts will not be equated with tax avoidance.” Thus, the allegation of Inland

Revenue that the Duke of Westminster is involved in tax evasion by drawing up covenant to pay

equivalent weekly wages at the end of the services is not correct.

The judgement in the above case made headlines and huge impact at that time paving a way for tax

savings by use of existing taxation provisions. Thus, the above case established the principle to

differentiate between tax savings and tax evasion at that time. The principle established since then has

been used in number of cases to avoid payment of taxes legally (Dridi and Boubaker, 2015).

TAXATION LAW

The facts of the above case was about payment to gardener. Duke of Westminster used to pay weekly to

the gardener for his services. The substantial amount of payment made to the gardener was from after tax

income of the Duke. As a result the Duke was unable to take tax benefit on such amount. Later knowing

the existing provisions that allows such expenditure to be deducted. The Duke of Westminster drew up a

covenant to pay equivalent amount annually. As a result such annual payment was allowed as deduction

to compute taxable income of the Duke. However, Inland Revenue challenged the practice of the Duke of

Westminster by alleging that it was a tax avoidance strategy by the Duke of Westminster (Dhaliwal et.

al. 2017).

Decision:

Lord Tomlin decided the case in favour of the Duke by stating that a tax payer has the right to make use

of the existing tax provisions to minimize the tax liability by using proper means. There is nothing wrong

if the tax payer uses valid provisions of the income tax law to minimize the amount of income tax liability

of his or her. It would not correct to hold the person liable of tax avoidance practices for using income tax

provisions existing in the country would be grossly injustice. The Duke of Westminster has paid gardener

for his services and the same is allowed as the payment was made under a covenant thus, the entire

payment would be allowed as deduction for computation of Duke’s taxable income (Sikka, 2017).

In Lord Tomlin’s own word, “Every man is allowed to use valid tax provisions to reduce taxes under

appropriate acts. Such acts will not be equated with tax avoidance.” Thus, the allegation of Inland

Revenue that the Duke of Westminster is involved in tax evasion by drawing up covenant to pay

equivalent weekly wages at the end of the services is not correct.

The judgement in the above case made headlines and huge impact at that time paving a way for tax

savings by use of existing taxation provisions. Thus, the above case established the principle to

differentiate between tax savings and tax evasion at that time. The principle established since then has

been used in number of cases to avoid payment of taxes legally (Dridi and Boubaker, 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

TAXATION LAW

Relevance of the principle in Australia at present:

At the time when the verdict was given on the above case the ruling was very attractive. Number of cases

followed that tried to use the principle laid down in the above case to avoid payment of taxes. However,

with passage of time the courts started looking at the overall impact of tax practices by the tax payers to

determine whether certain provisions apply to the tax payers. Tax payers started using the complex tax

structures to avoid payment of valid income taxes by using the principle of Inland Revenue and The duke

of Westminster (Daly, 2017).

Thus, the principle established by the above case not very relevant in Australia at present. The courts as

well as income tax authorities now use more restrictive approach to determine the income tax liabilities of

tax payers in the country.

Answer to question 4:

Issue:

There are not one but two issues that must be discussed in this case. These are as following:

I. Firstly, the loss of $40,000 from the rental property jointly owned by Joseph and Jane has to

be apportioned between the joint owners of the property correctly. Thus, the correct

proportion such loss between Joseph and Jane has to be determined.

II. In case of capital gain or loss arising from sale of the property in case the rental property is

sold by the owners, how would the capital gain or loss to be apportioned between the owners

(Mulheron, 2016).

Rules:

In case of jointly owned rental property, the Income Tax assessment Act, 1997 provides that income or

loss from such property shall be apportioned as per the agreement between the joint owners. The act

TAXATION LAW

Relevance of the principle in Australia at present:

At the time when the verdict was given on the above case the ruling was very attractive. Number of cases

followed that tried to use the principle laid down in the above case to avoid payment of taxes. However,

with passage of time the courts started looking at the overall impact of tax practices by the tax payers to

determine whether certain provisions apply to the tax payers. Tax payers started using the complex tax

structures to avoid payment of valid income taxes by using the principle of Inland Revenue and The duke

of Westminster (Daly, 2017).

Thus, the principle established by the above case not very relevant in Australia at present. The courts as

well as income tax authorities now use more restrictive approach to determine the income tax liabilities of

tax payers in the country.

Answer to question 4:

Issue:

There are not one but two issues that must be discussed in this case. These are as following:

I. Firstly, the loss of $40,000 from the rental property jointly owned by Joseph and Jane has to

be apportioned between the joint owners of the property correctly. Thus, the correct

proportion such loss between Joseph and Jane has to be determined.

II. In case of capital gain or loss arising from sale of the property in case the rental property is

sold by the owners, how would the capital gain or loss to be apportioned between the owners

(Mulheron, 2016).

Rules:

In case of jointly owned rental property, the Income Tax assessment Act, 1997 provides that income or

loss from such property shall be apportioned as per the agreement between the joint owners. The act

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

TAXATION LAW

further states that the agreement must be valid in order to be effective thus, in case an agreement is made

between the relatives to apportion profit and loss by coalition to avoid or reduce payment of income tax

then such agreement shall not be effective. In such case only the valid terms and conditions of the

agreement shall be effective and considered in determining various implications of jointly owned rental

property (Mumford, 2017).

Australian Taxation Office (ATO) has further explained that if a property has been brought by two or

more parties and they have signed an agreement between themselves to divide income and losses from

such property without any prejudice to any one or more of the joint of owner / owners of the property

then such agreement shall be valid. It is also possible to have an agreement that provides different terms

and conditions for apportionment of profit and apportionment of losses from such property. In such case

as long as the terms and conditions are fair and there is no coalition between the joint owners to defeat

any provision of law then such agreement shall be effective and valid. In such case the income and losses

from such rental property shall be distributed between the joint owners of the property as per the

agreement (Johnston, 2017).

In case of jointly owned properties if an agreement does not provide specifically the proportion of

ownership of different owners then it will be assumed for capital gain and loss purposes that the joint

owners have equal rights on the property. Accordingly, as per the Income Tax Assessment Act, 1997, the

amount of capital gain accruing from sale of such property would be equally distributed between the joint

owners (Dixon and Nassios, 2016).

Application:

Joseph and Jane are husband and wife, have entered into an agreement to purchase a rental property as

joint tenants. They signed an agreement to apportion the profit in 20 to 80 ratio where Joseph would

receive 20% profit and Jane would receive 80% profit from the rental property. The agreement has also

provided that in case of loss arising from such rental property Joseph would bear the loss completely. It is

TAXATION LAW

further states that the agreement must be valid in order to be effective thus, in case an agreement is made

between the relatives to apportion profit and loss by coalition to avoid or reduce payment of income tax

then such agreement shall not be effective. In such case only the valid terms and conditions of the

agreement shall be effective and considered in determining various implications of jointly owned rental

property (Mumford, 2017).

Australian Taxation Office (ATO) has further explained that if a property has been brought by two or

more parties and they have signed an agreement between themselves to divide income and losses from

such property without any prejudice to any one or more of the joint of owner / owners of the property

then such agreement shall be valid. It is also possible to have an agreement that provides different terms

and conditions for apportionment of profit and apportionment of losses from such property. In such case

as long as the terms and conditions are fair and there is no coalition between the joint owners to defeat

any provision of law then such agreement shall be effective and valid. In such case the income and losses

from such rental property shall be distributed between the joint owners of the property as per the

agreement (Johnston, 2017).

In case of jointly owned properties if an agreement does not provide specifically the proportion of

ownership of different owners then it will be assumed for capital gain and loss purposes that the joint

owners have equal rights on the property. Accordingly, as per the Income Tax Assessment Act, 1997, the

amount of capital gain accruing from sale of such property would be equally distributed between the joint

owners (Dixon and Nassios, 2016).

Application:

Joseph and Jane are husband and wife, have entered into an agreement to purchase a rental property as

joint tenants. They signed an agreement to apportion the profit in 20 to 80 ratio where Joseph would

receive 20% profit and Jane would receive 80% profit from the rental property. The agreement has also

provided that in case of loss arising from such rental property Joseph would bear the loss completely. It is

11

TAXATION LAW

clear that the agreement is a coalition between the husband and wife to reduce the income tax liability of

Joseph as it provides for 100% attachment of loss to Joseph only. Thus, agreement is not effective as far

as the distribution of loss is concerned (Woellner et. al. 2016).

In case the property is sold by the joint tenants then the capital gain would be taxed in the hands of both

the owners.

Conclusion:

Taking into consideration the discussion above it can be said that the loss of $40,000 from rental property

shall be divided in 20: 80 ratio between Joseph and Jane and not to be attached fully to Joseph. This is

because the terms and conditions in profit and loss distribution must be same until unless there is justified

reason for any difference in such ratios (Eslake, 2015).

There is no specific mention of proportion of ownership right on the rental property. In such situation the

property belongs to the owners equally. Hence, in case the property is sold then the resultant capital gain

shall be apportioned between the two owners Joseph and Jane in 1: 1 ratio in the absence of a specific

agreement to such effect.

TAXATION LAW

clear that the agreement is a coalition between the husband and wife to reduce the income tax liability of

Joseph as it provides for 100% attachment of loss to Joseph only. Thus, agreement is not effective as far

as the distribution of loss is concerned (Woellner et. al. 2016).

In case the property is sold by the joint tenants then the capital gain would be taxed in the hands of both

the owners.

Conclusion:

Taking into consideration the discussion above it can be said that the loss of $40,000 from rental property

shall be divided in 20: 80 ratio between Joseph and Jane and not to be attached fully to Joseph. This is

because the terms and conditions in profit and loss distribution must be same until unless there is justified

reason for any difference in such ratios (Eslake, 2015).

There is no specific mention of proportion of ownership right on the rental property. In such situation the

property belongs to the owners equally. Hence, in case the property is sold then the resultant capital gain

shall be apportioned between the two owners Joseph and Jane in 1: 1 ratio in the absence of a specific

agreement to such effect.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.