Australian Taxation Law Report: Net Income, FBT and Tax Implications

VerifiedAdded on 2020/12/30

|11

|3267

|274

Report

AI Summary

This report analyzes Australian taxation law, focusing on the determination of net income for a partnership and the implications of Fringe Benefits Tax (FBT). The report begins with an introduction to taxation and its application in Australia, including income tax and state taxes. It then delves into a specific case study, calculating the net income for a partnership for the year ended 30 June 2017. The analysis includes detailed calculations of business sales, cost of sales, gross profit, allowable and disallowed expenses, depreciation, and tax liability. Working papers are provided to support the calculations, including depreciation schedules and debtor/creditor accounts. The report also addresses FBT consequences, explaining the nature of FBT, its application to employee benefits, and the relevant legislation. The report concludes with a discussion of how employers should advise employees about FBT implications, including the benefits that can be provided and the tax implications for both the employer and employee. Finally, the report also includes a discussion on how fringe benefits are taxed and the role of FBT in retaining quality staff, and the importance of registering with FBT, keeping records, and reporting benefits on employee payment summaries.

AUSTRALIAN TAXATION

LAW

LAW

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

Determination of net income for partnership.........................................................................1

QUESTION 2...................................................................................................................................4

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

Determination of net income for partnership.........................................................................1

QUESTION 2...................................................................................................................................4

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION

Taxation is referred as term when authority of taxing generally a government which

levies and imposes tax. It applies to every type of involuntary levies through income to capital

gains for stating taxes. There are various business taxes like income tax is gathered through

Australian government via Australian tax Office. With context to different instances, it also

applies with state taxes and commonly for purpose of payroll tax. Australia also handles

numerous tax treaties along with other nations for purpose of preventing double taxation of

foreign organization which are operating in Australia. The present report will discuss about

identifying net income for partnership for the year ended 30 June 2017 with its partnership tax

return. In the similar aspect, John's employer would be advised about FBT consequences related

to remuneration package.

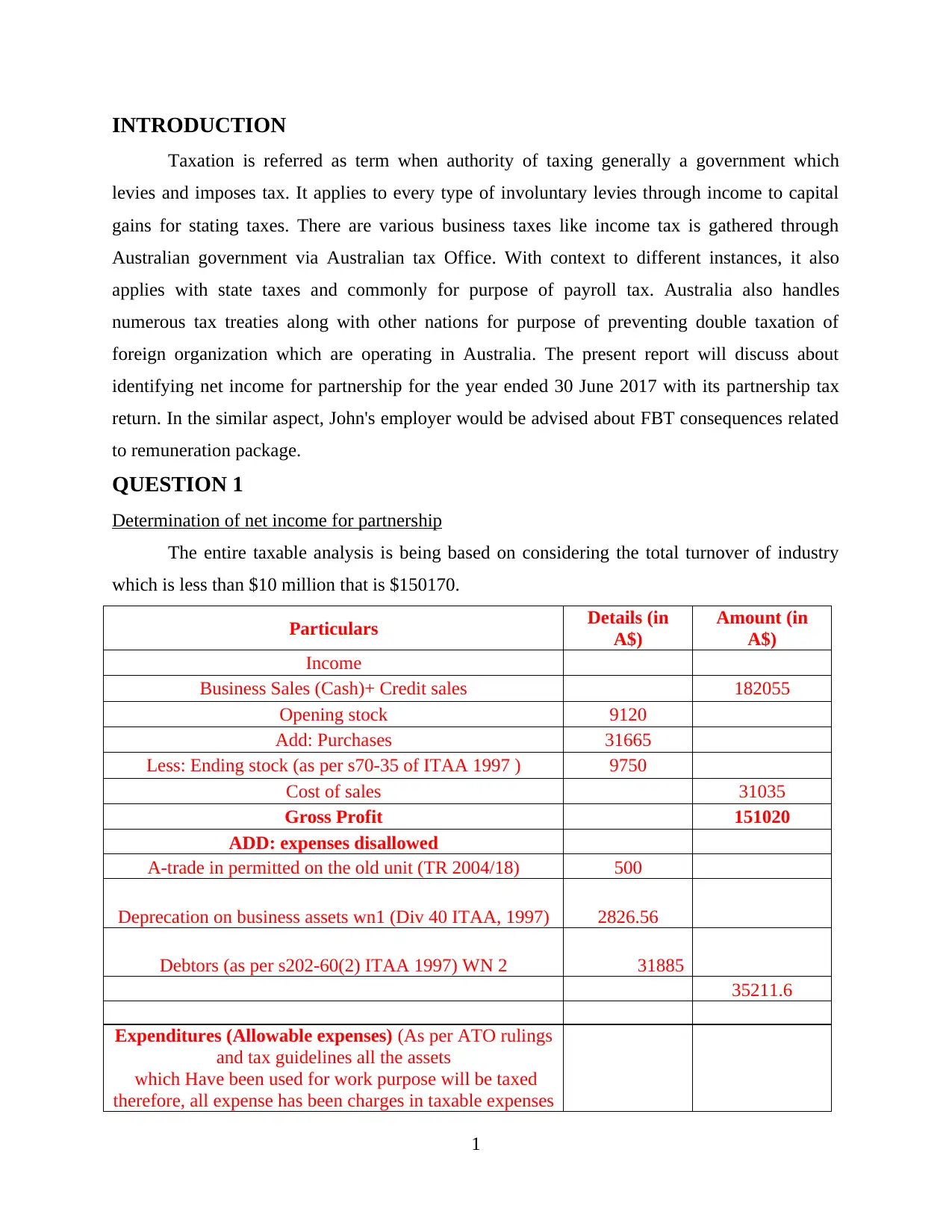

QUESTION 1

Determination of net income for partnership

The entire taxable analysis is being based on considering the total turnover of industry

which is less than $10 million that is $150170.

Particulars Details (in

A$)

Amount (in

A$)

Income

Business Sales (Cash)+ Credit sales 182055

Opening stock 9120

Add: Purchases 31665

Less: Ending stock (as per s70-35 of ITAA 1997 ) 9750

Cost of sales 31035

Gross Profit 151020

ADD: expenses disallowed

A-trade in permitted on the old unit (TR 2004/18) 500

Deprecation on business assets wn1 (Div 40 ITAA, 1997) 2826.56

Debtors (as per s202-60(2) ITAA 1997) WN 2 31885

35211.6

Expenditures (Allowable expenses) (As per ATO rulings

and tax guidelines all the assets

which Have been used for work purpose will be taxed

therefore, all expense has been charges in taxable expenses

1

Taxation is referred as term when authority of taxing generally a government which

levies and imposes tax. It applies to every type of involuntary levies through income to capital

gains for stating taxes. There are various business taxes like income tax is gathered through

Australian government via Australian tax Office. With context to different instances, it also

applies with state taxes and commonly for purpose of payroll tax. Australia also handles

numerous tax treaties along with other nations for purpose of preventing double taxation of

foreign organization which are operating in Australia. The present report will discuss about

identifying net income for partnership for the year ended 30 June 2017 with its partnership tax

return. In the similar aspect, John's employer would be advised about FBT consequences related

to remuneration package.

QUESTION 1

Determination of net income for partnership

The entire taxable analysis is being based on considering the total turnover of industry

which is less than $10 million that is $150170.

Particulars Details (in

A$)

Amount (in

A$)

Income

Business Sales (Cash)+ Credit sales 182055

Opening stock 9120

Add: Purchases 31665

Less: Ending stock (as per s70-35 of ITAA 1997 ) 9750

Cost of sales 31035

Gross Profit 151020

ADD: expenses disallowed

A-trade in permitted on the old unit (TR 2004/18) 500

Deprecation on business assets wn1 (Div 40 ITAA, 1997) 2826.56

Debtors (as per s202-60(2) ITAA 1997) WN 2 31885

35211.6

Expenditures (Allowable expenses) (As per ATO rulings

and tax guidelines all the assets

which Have been used for work purpose will be taxed

therefore, all expense has been charges in taxable expenses

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

as per their proportionate uses in the business. Partnership

Act, 1892)

Council rates (div 8 of ITAA 1997) 517

shop painting (Div. 25 ITAA, 1997) 150

refrigerator motor replacement (TR 97/23) (s25-10(1) of

ITAA 1997 ) 140

depreciation of CAR-SUV( 60% used for business

purpose) wn1 1516.44

Electricity bill (80 %) (div 8 of ITAA 1997) 1176

mobile bills (90% used for business purpose) one can

claim as per div 8 of ITAA 1997 634

account charge (div 8 of ITAA 1997) 595

business insurance (div 8 of ITAA 1997) 1250

union fees (div 8 of ITAA 1997) 284

account charge (ANZ Bank) (div 8 of ITAA 1997) 595

Creditors (as per s202-60(2) ITAA 1997) WN 3 510 7367.44

Net income 178864

Tax liability @27.5% (as per Treasury laws amendment

(enterprise tax plan base

Rate entities) Act 2018, all the entities which has turnover

Less than $10 million will be charged tax at 27.5%) 49187.6

Net tax payable 129676

Interpretation: On the basis of above table it can be interpretation that the taxable

income of the partners was $178864. There has been adjustment of various costs and revenue

retained by the business in the respective period. However, the depreciation on various assets

associated with business. Thus, they have been charged on the basis of proportionate use of these

assets in the business activities. While for the personal uses these assets were exempted as these

are the personal liabilities of the partners to make payment on their income tax provisions.

Moreover, with reference to such adjustments there have been various working notes were

2

Act, 1892)

Council rates (div 8 of ITAA 1997) 517

shop painting (Div. 25 ITAA, 1997) 150

refrigerator motor replacement (TR 97/23) (s25-10(1) of

ITAA 1997 ) 140

depreciation of CAR-SUV( 60% used for business

purpose) wn1 1516.44

Electricity bill (80 %) (div 8 of ITAA 1997) 1176

mobile bills (90% used for business purpose) one can

claim as per div 8 of ITAA 1997 634

account charge (div 8 of ITAA 1997) 595

business insurance (div 8 of ITAA 1997) 1250

union fees (div 8 of ITAA 1997) 284

account charge (ANZ Bank) (div 8 of ITAA 1997) 595

Creditors (as per s202-60(2) ITAA 1997) WN 3 510 7367.44

Net income 178864

Tax liability @27.5% (as per Treasury laws amendment

(enterprise tax plan base

Rate entities) Act 2018, all the entities which has turnover

Less than $10 million will be charged tax at 27.5%) 49187.6

Net tax payable 129676

Interpretation: On the basis of above table it can be interpretation that the taxable

income of the partners was $178864. There has been adjustment of various costs and revenue

retained by the business in the respective period. However, the depreciation on various assets

associated with business. Thus, they have been charged on the basis of proportionate use of these

assets in the business activities. While for the personal uses these assets were exempted as these

are the personal liabilities of the partners to make payment on their income tax provisions.

Moreover, with reference to such adjustments there have been various working notes were

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

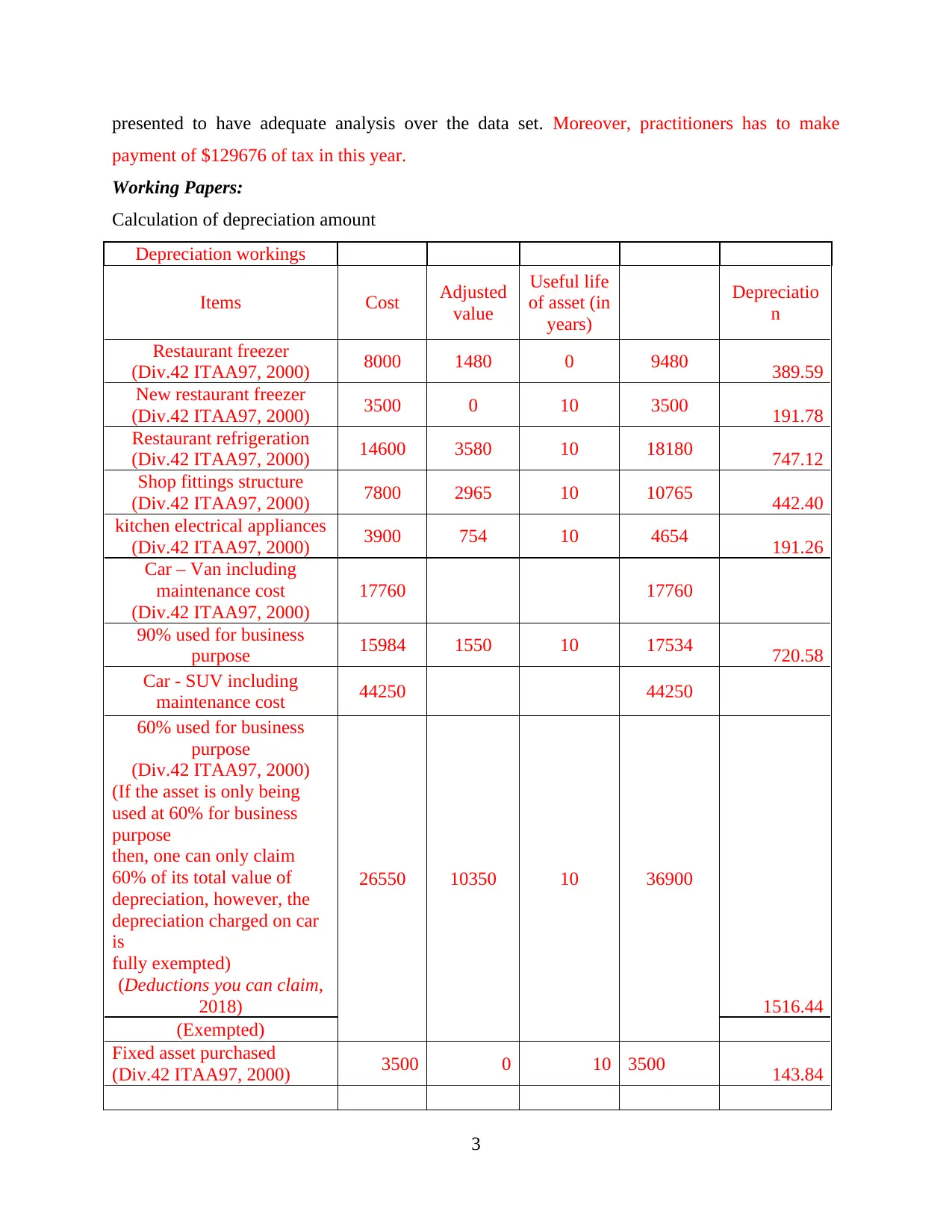

presented to have adequate analysis over the data set. Moreover, practitioners has to make

payment of $129676 of tax in this year.

Working Papers:

Calculation of depreciation amount

Depreciation workings

Items Cost Adjusted

value

Useful life

of asset (in

years)

Depreciatio

n

Restaurant freezer

(Div.42 ITAA97, 2000) 8000 1480 0 9480 389.59

New restaurant freezer

(Div.42 ITAA97, 2000) 3500 0 10 3500 191.78

Restaurant refrigeration

(Div.42 ITAA97, 2000) 14600 3580 10 18180 747.12

Shop fittings structure

(Div.42 ITAA97, 2000) 7800 2965 10 10765 442.40

kitchen electrical appliances

(Div.42 ITAA97, 2000) 3900 754 10 4654 191.26

Car – Van including

maintenance cost

(Div.42 ITAA97, 2000)

17760 17760

90% used for business

purpose 15984 1550 10 17534 720.58

Car - SUV including

maintenance cost 44250 44250

60% used for business

purpose

(Div.42 ITAA97, 2000)

(If the asset is only being

used at 60% for business

purpose

then, one can only claim

60% of its total value of

depreciation, however, the

depreciation charged on car

is

fully exempted)

(Deductions you can claim,

2018)

26550 10350 10 36900

1516.44

(Exempted)

Fixed asset purchased

(Div.42 ITAA97, 2000) 3500 0 10 3500 143.84

3

payment of $129676 of tax in this year.

Working Papers:

Calculation of depreciation amount

Depreciation workings

Items Cost Adjusted

value

Useful life

of asset (in

years)

Depreciatio

n

Restaurant freezer

(Div.42 ITAA97, 2000) 8000 1480 0 9480 389.59

New restaurant freezer

(Div.42 ITAA97, 2000) 3500 0 10 3500 191.78

Restaurant refrigeration

(Div.42 ITAA97, 2000) 14600 3580 10 18180 747.12

Shop fittings structure

(Div.42 ITAA97, 2000) 7800 2965 10 10765 442.40

kitchen electrical appliances

(Div.42 ITAA97, 2000) 3900 754 10 4654 191.26

Car – Van including

maintenance cost

(Div.42 ITAA97, 2000)

17760 17760

90% used for business

purpose 15984 1550 10 17534 720.58

Car - SUV including

maintenance cost 44250 44250

60% used for business

purpose

(Div.42 ITAA97, 2000)

(If the asset is only being

used at 60% for business

purpose

then, one can only claim

60% of its total value of

depreciation, however, the

depreciation charged on car

is

fully exempted)

(Deductions you can claim,

2018)

26550 10350 10 36900

1516.44

(Exempted)

Fixed asset purchased

(Div.42 ITAA97, 2000) 3500 0 10 3500 143.84

3

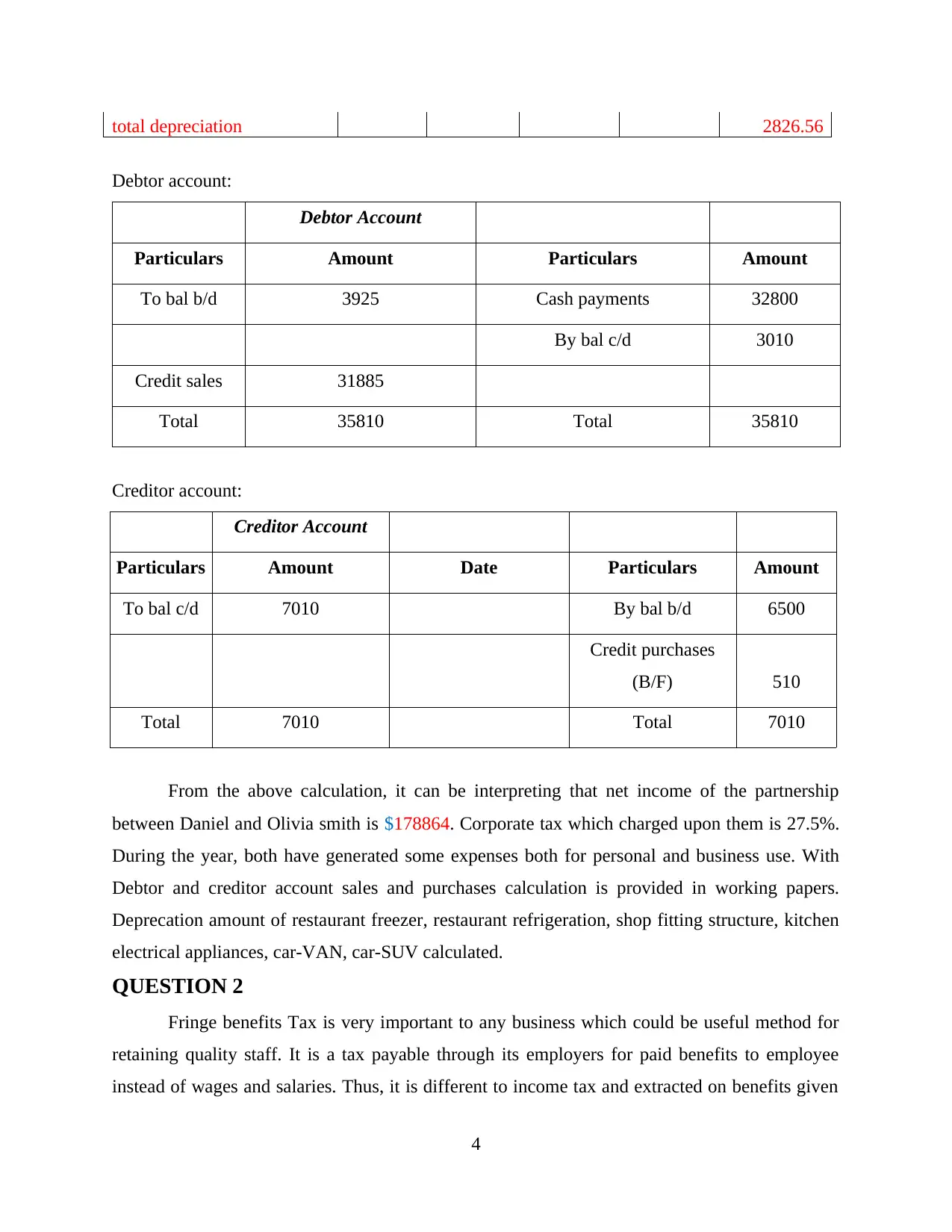

total depreciation 2826.56

Debtor account:

Debtor Account

Particulars Amount Particulars Amount

To bal b/d 3925 Cash payments 32800

By bal c/d 3010

Credit sales 31885

Total 35810 Total 35810

Creditor account:

Creditor Account

Particulars Amount Date Particulars Amount

To bal c/d 7010 By bal b/d 6500

Credit purchases

(B/F) 510

Total 7010 Total 7010

From the above calculation, it can be interpreting that net income of the partnership

between Daniel and Olivia smith is $178864. Corporate tax which charged upon them is 27.5%.

During the year, both have generated some expenses both for personal and business use. With

Debtor and creditor account sales and purchases calculation is provided in working papers.

Deprecation amount of restaurant freezer, restaurant refrigeration, shop fitting structure, kitchen

electrical appliances, car-VAN, car-SUV calculated.

QUESTION 2

Fringe benefits Tax is very important to any business which could be useful method for

retaining quality staff. It is a tax payable through its employers for paid benefits to employee

instead of wages and salaries. Thus, it is different to income tax and extracted on benefits given

4

Debtor account:

Debtor Account

Particulars Amount Particulars Amount

To bal b/d 3925 Cash payments 32800

By bal c/d 3010

Credit sales 31885

Total 35810 Total 35810

Creditor account:

Creditor Account

Particulars Amount Date Particulars Amount

To bal c/d 7010 By bal b/d 6500

Credit purchases

(B/F) 510

Total 7010 Total 7010

From the above calculation, it can be interpreting that net income of the partnership

between Daniel and Olivia smith is $178864. Corporate tax which charged upon them is 27.5%.

During the year, both have generated some expenses both for personal and business use. With

Debtor and creditor account sales and purchases calculation is provided in working papers.

Deprecation amount of restaurant freezer, restaurant refrigeration, shop fitting structure, kitchen

electrical appliances, car-VAN, car-SUV calculated.

QUESTION 2

Fringe benefits Tax is very important to any business which could be useful method for

retaining quality staff. It is a tax payable through its employers for paid benefits to employee

instead of wages and salaries. Thus, it is different to income tax and extracted on benefits given

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

on taxable value of fringe benefits. As per legislation of Fringe benefits tax, fringe benefit is

given in context of employment and this effectively signifies benefit given to anybody as they

are employee of business unit (Brinkley, 2018). The employee might be future of former

employee.

It is the type of benefit which needs to provide to employees for retaining them in

organization. Such benefits include, a car, car parking, low interest loans and payment of private

expenses. It will be provided by calculating amount to FBT which needs to pay, by registering

with FBT, by keeping necessary records, reporting this benefits on employees' payment

summaries and by understanding benefits which is exempt from FBT. This is introduced with the

Finance Bill of 2005 and set at 30% of cost benefits. In recent times, it provides an sizeable relief

to employees so that they get retain for long term in organisation and will provide their best

efforts in order to achieve organisational objectives. It is a type of benefit which provided by

employers which supplement wages and salaries of workers. It is based on the assumption that

employer being taxed at marginal tax rate. It is payable at specific rate on values of benefits

which provided to employees. Its rate is calculated on net expenses which are not segregated

between paid to employee and paid to outsiders. In case of employer, FBT is applicable when

employers is engaged in two or more business activities and it is not payable on advance paid.

Therefore, it is considered as expenditure on income and is cannot be recovered from employees.

Any type of firm, company, association of persons, body of individuals, local authority and

artificial judicial person are able to provide FBT tax to their business employees.

In the similar aspect, employee is referred as person for attaining wages and salaries

instead of wages and salaries. Benefits given in context to someone who died is not fringe

benefits as reduced person does not accomplish as employee in legislation of FBT. The term

fringe benefit and benefit have presence of broad meaning for purpose of FBT as benefits

considers services, privileges and rights as well (Clemens, Kahn and Meer, 2018). Fringe

benefits tax is payable through employer on fringe benefits to its employees and on the contrary,

any cost of FBT incurred through employer will be attained through remuneration package of

any employee.

Fringe benefits are attributable and valued to individual employees must be directly taxed

via PAYG system. The other fringe benefits along with particular incidental to employment of

individual must be taxed to its major employers on top marginal rate and non reportable with

5

given in context of employment and this effectively signifies benefit given to anybody as they

are employee of business unit (Brinkley, 2018). The employee might be future of former

employee.

It is the type of benefit which needs to provide to employees for retaining them in

organization. Such benefits include, a car, car parking, low interest loans and payment of private

expenses. It will be provided by calculating amount to FBT which needs to pay, by registering

with FBT, by keeping necessary records, reporting this benefits on employees' payment

summaries and by understanding benefits which is exempt from FBT. This is introduced with the

Finance Bill of 2005 and set at 30% of cost benefits. In recent times, it provides an sizeable relief

to employees so that they get retain for long term in organisation and will provide their best

efforts in order to achieve organisational objectives. It is a type of benefit which provided by

employers which supplement wages and salaries of workers. It is based on the assumption that

employer being taxed at marginal tax rate. It is payable at specific rate on values of benefits

which provided to employees. Its rate is calculated on net expenses which are not segregated

between paid to employee and paid to outsiders. In case of employer, FBT is applicable when

employers is engaged in two or more business activities and it is not payable on advance paid.

Therefore, it is considered as expenditure on income and is cannot be recovered from employees.

Any type of firm, company, association of persons, body of individuals, local authority and

artificial judicial person are able to provide FBT tax to their business employees.

In the similar aspect, employee is referred as person for attaining wages and salaries

instead of wages and salaries. Benefits given in context to someone who died is not fringe

benefits as reduced person does not accomplish as employee in legislation of FBT. The term

fringe benefit and benefit have presence of broad meaning for purpose of FBT as benefits

considers services, privileges and rights as well (Clemens, Kahn and Meer, 2018). Fringe

benefits tax is payable through employer on fringe benefits to its employees and on the contrary,

any cost of FBT incurred through employer will be attained through remuneration package of

any employee.

Fringe benefits are attributable and valued to individual employees must be directly taxed

via PAYG system. The other fringe benefits along with particular incidental to employment of

individual must be taxed to its major employers on top marginal rate and non reportable with

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

perspective of its employees (Jones, 2018). The scope of fringe benefits is directly subjected to

tax and must be simplified whereas market value must be generally used for valuing fringe

benefits with context to appropriate adjustment on basis of employee contribution. Each

exemption of fringe benefit tax must be reviewed for identifying its continuing appropriateness.

In the same series, for improving simplicity and consideration must be given to exclude fringe

benefits through tax where compliance cost outweigh equity and consideration of tax integrity

(Whiteford and Heron, 2018). Broadly, fringe benefits in FBT law could be directly reviewed for

excluding essential work items like stationery, toilets and chairs. On basis of fringe benefits

which are taxed by employers where small de minimis threshold under fringe benefits are

exempted through tax must be implied. Furthermore, threshold could directly vary on depending

numerous employees in any business unit. Henceforth, not for profit entities where FBT

Concessions must be reconfigured and FBT exemptions of members of defence area must be

appropriately replaced with context of direct remuneration raises the affected personnel.

There is consideration of case of Rosie who is employed through accountancy practice

which gives advice about taxation to different soccer teams along with players. Often, these team

arranges free tickets for Rosie and partner for attending matches along with corporate function

which helps in preceding itself on match days. The accounting practice partners encourage for

undertaking these offers as they give opportunity for purpose of networking its innovative

business opportunities. It is likely to given benefit through third party and arises with context to

employment of Rosie as they will create advantage with context of provisions of FBT with

outcome in employer with liability of FBT (Dickinson and Hobbs, 2018). The Australian

taxation law has ruled multiple examples of benefits in family arrangements which are deemed at

outside to scope of law of FBT. Thus, it had considered various things such as birthday gift to

child who operates in business run through parents, wedding gift to parents to any adult child

who had worked after school in family business.

Furthermore, very important aspect is interest-free or concessional loan provided to child

for studies and fee payment. The rental value of farm homestead occupied through family where

private company conducts business of farming where they work and hold title of homestead.

John as senior executive of printing company as contribution to remuneration package of its

employer pay fees of his child school at private school costing $15000. In the similar aspect,

accommodation is also given to him at Sydney apartment by his employer throughout FBT year

6

tax and must be simplified whereas market value must be generally used for valuing fringe

benefits with context to appropriate adjustment on basis of employee contribution. Each

exemption of fringe benefit tax must be reviewed for identifying its continuing appropriateness.

In the same series, for improving simplicity and consideration must be given to exclude fringe

benefits through tax where compliance cost outweigh equity and consideration of tax integrity

(Whiteford and Heron, 2018). Broadly, fringe benefits in FBT law could be directly reviewed for

excluding essential work items like stationery, toilets and chairs. On basis of fringe benefits

which are taxed by employers where small de minimis threshold under fringe benefits are

exempted through tax must be implied. Furthermore, threshold could directly vary on depending

numerous employees in any business unit. Henceforth, not for profit entities where FBT

Concessions must be reconfigured and FBT exemptions of members of defence area must be

appropriately replaced with context of direct remuneration raises the affected personnel.

There is consideration of case of Rosie who is employed through accountancy practice

which gives advice about taxation to different soccer teams along with players. Often, these team

arranges free tickets for Rosie and partner for attending matches along with corporate function

which helps in preceding itself on match days. The accounting practice partners encourage for

undertaking these offers as they give opportunity for purpose of networking its innovative

business opportunities. It is likely to given benefit through third party and arises with context to

employment of Rosie as they will create advantage with context of provisions of FBT with

outcome in employer with liability of FBT (Dickinson and Hobbs, 2018). The Australian

taxation law has ruled multiple examples of benefits in family arrangements which are deemed at

outside to scope of law of FBT. Thus, it had considered various things such as birthday gift to

child who operates in business run through parents, wedding gift to parents to any adult child

who had worked after school in family business.

Furthermore, very important aspect is interest-free or concessional loan provided to child

for studies and fee payment. The rental value of farm homestead occupied through family where

private company conducts business of farming where they work and hold title of homestead.

John as senior executive of printing company as contribution to remuneration package of its

employer pay fees of his child school at private school costing $15000. In the similar aspect,

accommodation is also given to him at Sydney apartment by his employer throughout FBT year

6

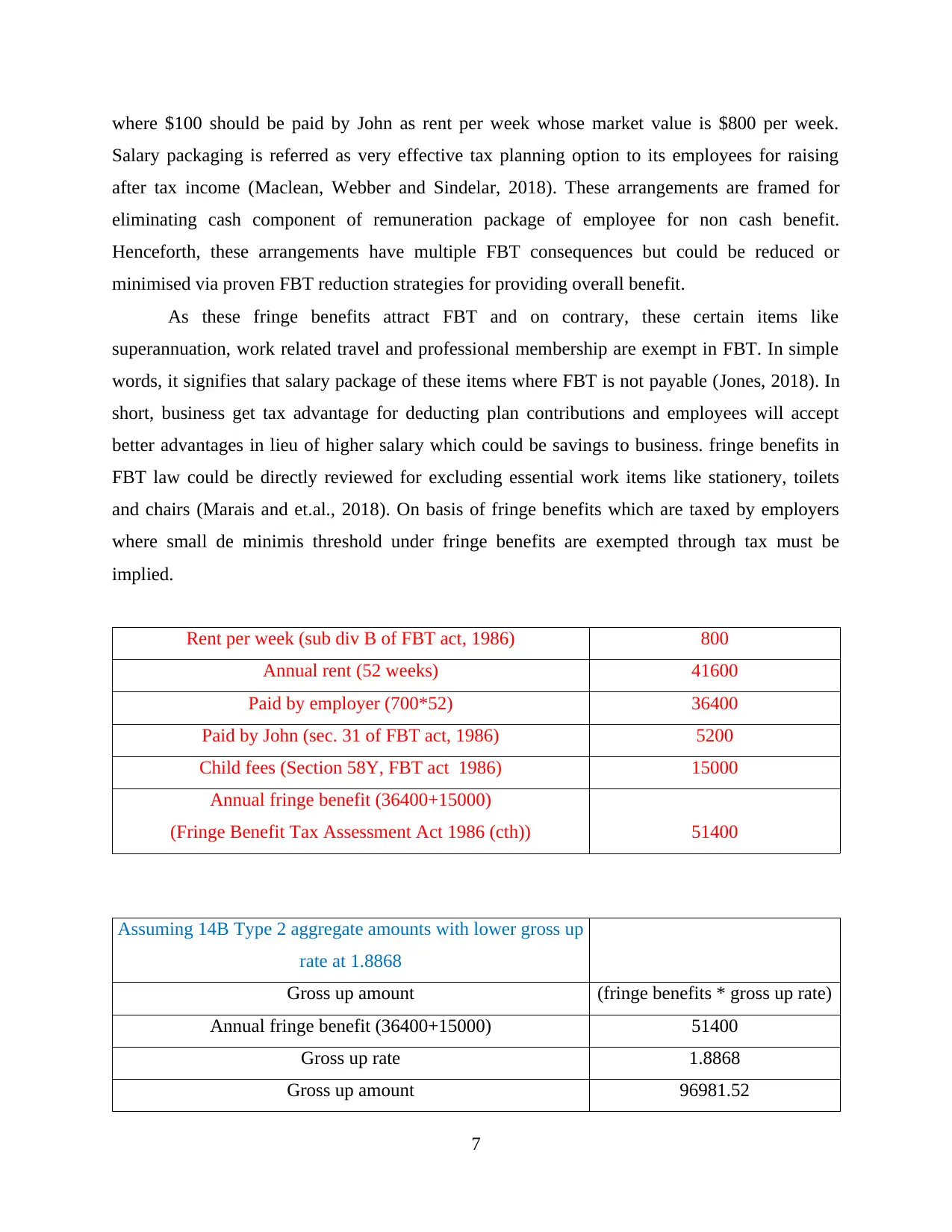

where $100 should be paid by John as rent per week whose market value is $800 per week.

Salary packaging is referred as very effective tax planning option to its employees for raising

after tax income (Maclean, Webber and Sindelar, 2018). These arrangements are framed for

eliminating cash component of remuneration package of employee for non cash benefit.

Henceforth, these arrangements have multiple FBT consequences but could be reduced or

minimised via proven FBT reduction strategies for providing overall benefit.

As these fringe benefits attract FBT and on contrary, these certain items like

superannuation, work related travel and professional membership are exempt in FBT. In simple

words, it signifies that salary package of these items where FBT is not payable (Jones, 2018). In

short, business get tax advantage for deducting plan contributions and employees will accept

better advantages in lieu of higher salary which could be savings to business. fringe benefits in

FBT law could be directly reviewed for excluding essential work items like stationery, toilets

and chairs (Marais and et.al., 2018). On basis of fringe benefits which are taxed by employers

where small de minimis threshold under fringe benefits are exempted through tax must be

implied.

Rent per week (sub div B of FBT act, 1986) 800

Annual rent (52 weeks) 41600

Paid by employer (700*52) 36400

Paid by John (sec. 31 of FBT act, 1986) 5200

Child fees (Section 58Y, FBT act 1986) 15000

Annual fringe benefit (36400+15000)

(Fringe Benefit Tax Assessment Act 1986 (cth)) 51400

Assuming 14B Type 2 aggregate amounts with lower gross up

rate at 1.8868

Gross up amount (fringe benefits * gross up rate)

Annual fringe benefit (36400+15000) 51400

Gross up rate 1.8868

Gross up amount 96981.52

7

Salary packaging is referred as very effective tax planning option to its employees for raising

after tax income (Maclean, Webber and Sindelar, 2018). These arrangements are framed for

eliminating cash component of remuneration package of employee for non cash benefit.

Henceforth, these arrangements have multiple FBT consequences but could be reduced or

minimised via proven FBT reduction strategies for providing overall benefit.

As these fringe benefits attract FBT and on contrary, these certain items like

superannuation, work related travel and professional membership are exempt in FBT. In simple

words, it signifies that salary package of these items where FBT is not payable (Jones, 2018). In

short, business get tax advantage for deducting plan contributions and employees will accept

better advantages in lieu of higher salary which could be savings to business. fringe benefits in

FBT law could be directly reviewed for excluding essential work items like stationery, toilets

and chairs (Marais and et.al., 2018). On basis of fringe benefits which are taxed by employers

where small de minimis threshold under fringe benefits are exempted through tax must be

implied.

Rent per week (sub div B of FBT act, 1986) 800

Annual rent (52 weeks) 41600

Paid by employer (700*52) 36400

Paid by John (sec. 31 of FBT act, 1986) 5200

Child fees (Section 58Y, FBT act 1986) 15000

Annual fringe benefit (36400+15000)

(Fringe Benefit Tax Assessment Act 1986 (cth)) 51400

Assuming 14B Type 2 aggregate amounts with lower gross up

rate at 1.8868

Gross up amount (fringe benefits * gross up rate)

Annual fringe benefit (36400+15000) 51400

Gross up rate 1.8868

Gross up amount 96981.52

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

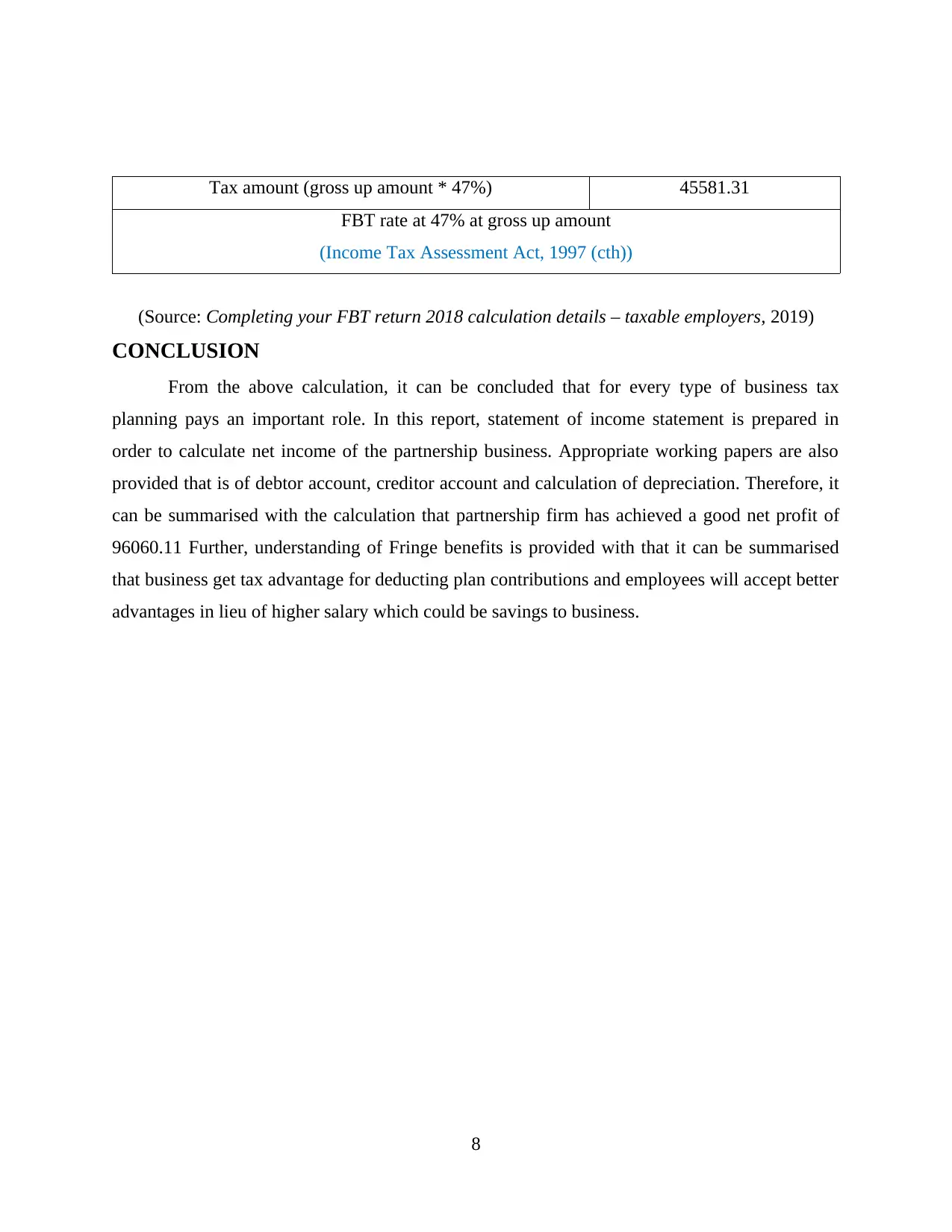

Tax amount (gross up amount * 47%) 45581.31

FBT rate at 47% at gross up amount

(Income Tax Assessment Act, 1997 (cth))

(Source: Completing your FBT return 2018 calculation details – taxable employers, 2019)

CONCLUSION

From the above calculation, it can be concluded that for every type of business tax

planning pays an important role. In this report, statement of income statement is prepared in

order to calculate net income of the partnership business. Appropriate working papers are also

provided that is of debtor account, creditor account and calculation of depreciation. Therefore, it

can be summarised with the calculation that partnership firm has achieved a good net profit of

96060.11 Further, understanding of Fringe benefits is provided with that it can be summarised

that business get tax advantage for deducting plan contributions and employees will accept better

advantages in lieu of higher salary which could be savings to business.

8

FBT rate at 47% at gross up amount

(Income Tax Assessment Act, 1997 (cth))

(Source: Completing your FBT return 2018 calculation details – taxable employers, 2019)

CONCLUSION

From the above calculation, it can be concluded that for every type of business tax

planning pays an important role. In this report, statement of income statement is prepared in

order to calculate net income of the partnership business. Appropriate working papers are also

provided that is of debtor account, creditor account and calculation of depreciation. Therefore, it

can be summarised with the calculation that partnership firm has achieved a good net profit of

96060.11 Further, understanding of Fringe benefits is provided with that it can be summarised

that business get tax advantage for deducting plan contributions and employees will accept better

advantages in lieu of higher salary which could be savings to business.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Brinkley, C., (2018). Fringe benefits: adding rugosity to the urban interface in theory and

practice. Journal of Planning Literature. 33(2). pp.143-154.

Clemens, J., Kahn, L. B. and Meer, J., (2018). The Minimum Wage, Fringe Benefits, and Worker

Welfare (No. w24635). National Bureau of Economic Research.

Dickinson, D. C. and Hobbs, R. J., 2018. The unseen green: nonmaterial benefits from urban

green space in Perth, Western Australia. THESIS DECLARATION, p.51.

Jones, D., 2018. Complexity of tax residency attracts review. Taxation in Australia. 53(6).

p.296.

Maclean, J. C., Webber, D. and Sindelar, J. L., (2018). Immigration and access to fringe

benefits: Evidence from the Tobacco Use Supplements. Industrial Relations: A Journal of

Economy and Society. 57(2). pp.235-259.

Marais, L. and et.al., 2018. The changing nature of mining towns: Reflections from Australia,

Canada and South Africa. Land Use Policy. 76. pp.779-788.

Whiteford, P. and Heron, A., 2018. Australia: providing social protection to non-standard

workers with tax financing.

Online

Completing your FBT return 2018 calculation details – taxable employers. 2019. [Online].

Available through <https://www.ato.gov.au/forms/completing-your-2018-fringe-benefits-

tax-return/?page=4>.

Repairs and maintenance. 2018. [Online]. Available through :<

https://www.ato.gov.au/Individuals/myTax/2018/In-detail/rent/?page=14>.

Deductions you can claim. 2018. [Online]. Available through :<

https://www.ato.gov.au/Individuals/Income-and-deductions/Deductions-you-can-claim/>.

9

Books and Journals

Brinkley, C., (2018). Fringe benefits: adding rugosity to the urban interface in theory and

practice. Journal of Planning Literature. 33(2). pp.143-154.

Clemens, J., Kahn, L. B. and Meer, J., (2018). The Minimum Wage, Fringe Benefits, and Worker

Welfare (No. w24635). National Bureau of Economic Research.

Dickinson, D. C. and Hobbs, R. J., 2018. The unseen green: nonmaterial benefits from urban

green space in Perth, Western Australia. THESIS DECLARATION, p.51.

Jones, D., 2018. Complexity of tax residency attracts review. Taxation in Australia. 53(6).

p.296.

Maclean, J. C., Webber, D. and Sindelar, J. L., (2018). Immigration and access to fringe

benefits: Evidence from the Tobacco Use Supplements. Industrial Relations: A Journal of

Economy and Society. 57(2). pp.235-259.

Marais, L. and et.al., 2018. The changing nature of mining towns: Reflections from Australia,

Canada and South Africa. Land Use Policy. 76. pp.779-788.

Whiteford, P. and Heron, A., 2018. Australia: providing social protection to non-standard

workers with tax financing.

Online

Completing your FBT return 2018 calculation details – taxable employers. 2019. [Online].

Available through <https://www.ato.gov.au/forms/completing-your-2018-fringe-benefits-

tax-return/?page=4>.

Repairs and maintenance. 2018. [Online]. Available through :<

https://www.ato.gov.au/Individuals/myTax/2018/In-detail/rent/?page=14>.

Deductions you can claim. 2018. [Online]. Available through :<

https://www.ato.gov.au/Individuals/Income-and-deductions/Deductions-you-can-claim/>.

9

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.