Holmes Institute HI6028: Australian Tax Law and Legislation Report

VerifiedAdded on 2022/10/12

|13

|2820

|137

Report

AI Summary

This report provides a comprehensive overview of Australian tax law, focusing on income tax, CGT (Capital Gains Tax), GST (Goods and Services Tax), and FBT (Fringe Benefit Tax). It covers the principles of a good tax system, including neutrality, certainty, efficiency, equity, and simplicity. The report delves into the specifics of income and deductions, anti-avoidance provisions, and income tax administration. Practical applications are demonstrated through case studies involving Emma and City Sky Co Ltd, illustrating how tax legislations are applied in real-world scenarios. The report also examines resident and non-resident taxation, withholding tax, and self-assessment tax systems. Additionally, the report explains the application of Goods and Service Tax benefit and anti-avoidance rules under various circumstances.

1

AUSTRALIAN TAX LAW

Australian Income Tax

Institution

Date

AUSTRALIAN TAX LAW

Australian Income Tax

Institution

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

AUSTRALIAN TAX LAW

EXECUTIVE SUMMARY

The objective of this report is to equip the student with the knowledge and understanding of

concepts of income deduction, FBT(Fringe Benefit Tax),GST(Goods and Service Tax),

CGT(Capital Gain Tax), anti avoidance provisions and income administration according to the

Australian income tax system. The report also aims at enabling the learner to demonstrate and

understand the principles of a good tax system.

A practical approach to the concepts and tax legislations has been shown by Emma and City Sky

Co ltd.

AUSTRALIAN TAX LAW

EXECUTIVE SUMMARY

The objective of this report is to equip the student with the knowledge and understanding of

concepts of income deduction, FBT(Fringe Benefit Tax),GST(Goods and Service Tax),

CGT(Capital Gain Tax), anti avoidance provisions and income administration according to the

Australian income tax system. The report also aims at enabling the learner to demonstrate and

understand the principles of a good tax system.

A practical approach to the concepts and tax legislations has been shown by Emma and City Sky

Co ltd.

3

AUSTRALIAN TAX LAW

Table of Contents

EXECUTIVE SUMMARY.........................................................................................................................2

INTRODUCTION.......................................................................................................................................3

INCOME TAX........................................................................................................................................3

CGT-CAPITAL GAIN TAX...................................................................................................................3

Resident Individual..............................................................................................................................4

Non Resident.......................................................................................................................................4

GST-GOODS AND SERVICE TAX......................................................................................................4

FBT-FRINGE BENEFIT TAX................................................................................................................5

AUSTRALIA TAX SYSTEM.................................................................................................................5

Withholding tax...................................................................................................................................5

Self assessment tax..............................................................................................................................5

Anti - avoidance provisions under GST...............................................................................................6

TAX LEGISLATION..................................................................................................................................6

TAXATION PRINCIPLES.........................................................................................................................9

REFERENCES..........................................................................................................................................10

AUSTRALIAN TAX LAW

Table of Contents

EXECUTIVE SUMMARY.........................................................................................................................2

INTRODUCTION.......................................................................................................................................3

INCOME TAX........................................................................................................................................3

CGT-CAPITAL GAIN TAX...................................................................................................................3

Resident Individual..............................................................................................................................4

Non Resident.......................................................................................................................................4

GST-GOODS AND SERVICE TAX......................................................................................................4

FBT-FRINGE BENEFIT TAX................................................................................................................5

AUSTRALIA TAX SYSTEM.................................................................................................................5

Withholding tax...................................................................................................................................5

Self assessment tax..............................................................................................................................5

Anti - avoidance provisions under GST...............................................................................................6

TAX LEGISLATION..................................................................................................................................6

TAXATION PRINCIPLES.........................................................................................................................9

REFERENCES..........................................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

AUSTRALIAN TAX LAW

INTRODUCTION

The federal government has the mandate to oblige tax to residents of Australia and foreigners

residing in Australia .the tax charge apply to those non residents who work in Australia and

whose tax is within the taxable income bracket. The Australian legislation has rules and

regulation on how to identify a resident individual or a company. In addition, the law also

determines the source of income if it is within Australia or outside. Generally; taxation is levied

from the location or place of work. Resident and source rule is commonly used in many

countries; however it has its challenges. Individual or a company’s earning may experience

double taxation (taxed in two countries).in order to avoid double taxation, Australian government

approved double tax agreement with other countries. The purpose of double tax assent is to

ensure income is levied once.

INCOME TAX

Income tax is an individual or company’s assessable pay after acceptable deductions. Wages,

business earnings, salaries, dividends and interests are some of the assessable income (Evans,

2019, pg.217).expenses and costs incurred on the process of creating an income are deducted.

Personal and capital expenses however are not deductible. A deduction on such expenses

happens only when certain conditions are met (Anesa et al.2019, pg.79).

CGT

(Capita gain tax )

Capital Gain Tax is levied on proceeds gained from selling an asset. CGT is charged on Fixed

and current assets however assets like homes and motor vehicles have exemptions. For non

residents, assets like real properties are subject to capital gains. In Australia, a resident is allowed

a discount 50% tax on assets held by a company or an individual for more than 12 months.

After the amendment made to ‘capital gain tax rule’, foreign taxpayers were given capital

earnings as a compensation to capital loss instead of 50% discount on tax.

One is legally obliged to pay duties on capital income or gains as stipulated in the

rules .Australian residents and non residents have the responsibility of paying CGT- capital gain

AUSTRALIAN TAX LAW

INTRODUCTION

The federal government has the mandate to oblige tax to residents of Australia and foreigners

residing in Australia .the tax charge apply to those non residents who work in Australia and

whose tax is within the taxable income bracket. The Australian legislation has rules and

regulation on how to identify a resident individual or a company. In addition, the law also

determines the source of income if it is within Australia or outside. Generally; taxation is levied

from the location or place of work. Resident and source rule is commonly used in many

countries; however it has its challenges. Individual or a company’s earning may experience

double taxation (taxed in two countries).in order to avoid double taxation, Australian government

approved double tax agreement with other countries. The purpose of double tax assent is to

ensure income is levied once.

INCOME TAX

Income tax is an individual or company’s assessable pay after acceptable deductions. Wages,

business earnings, salaries, dividends and interests are some of the assessable income (Evans,

2019, pg.217).expenses and costs incurred on the process of creating an income are deducted.

Personal and capital expenses however are not deductible. A deduction on such expenses

happens only when certain conditions are met (Anesa et al.2019, pg.79).

CGT

(Capita gain tax )

Capital Gain Tax is levied on proceeds gained from selling an asset. CGT is charged on Fixed

and current assets however assets like homes and motor vehicles have exemptions. For non

residents, assets like real properties are subject to capital gains. In Australia, a resident is allowed

a discount 50% tax on assets held by a company or an individual for more than 12 months.

After the amendment made to ‘capital gain tax rule’, foreign taxpayers were given capital

earnings as a compensation to capital loss instead of 50% discount on tax.

One is legally obliged to pay duties on capital income or gains as stipulated in the

rules .Australian residents and non residents have the responsibility of paying CGT- capital gain

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

AUSTRALIAN TAX LAW

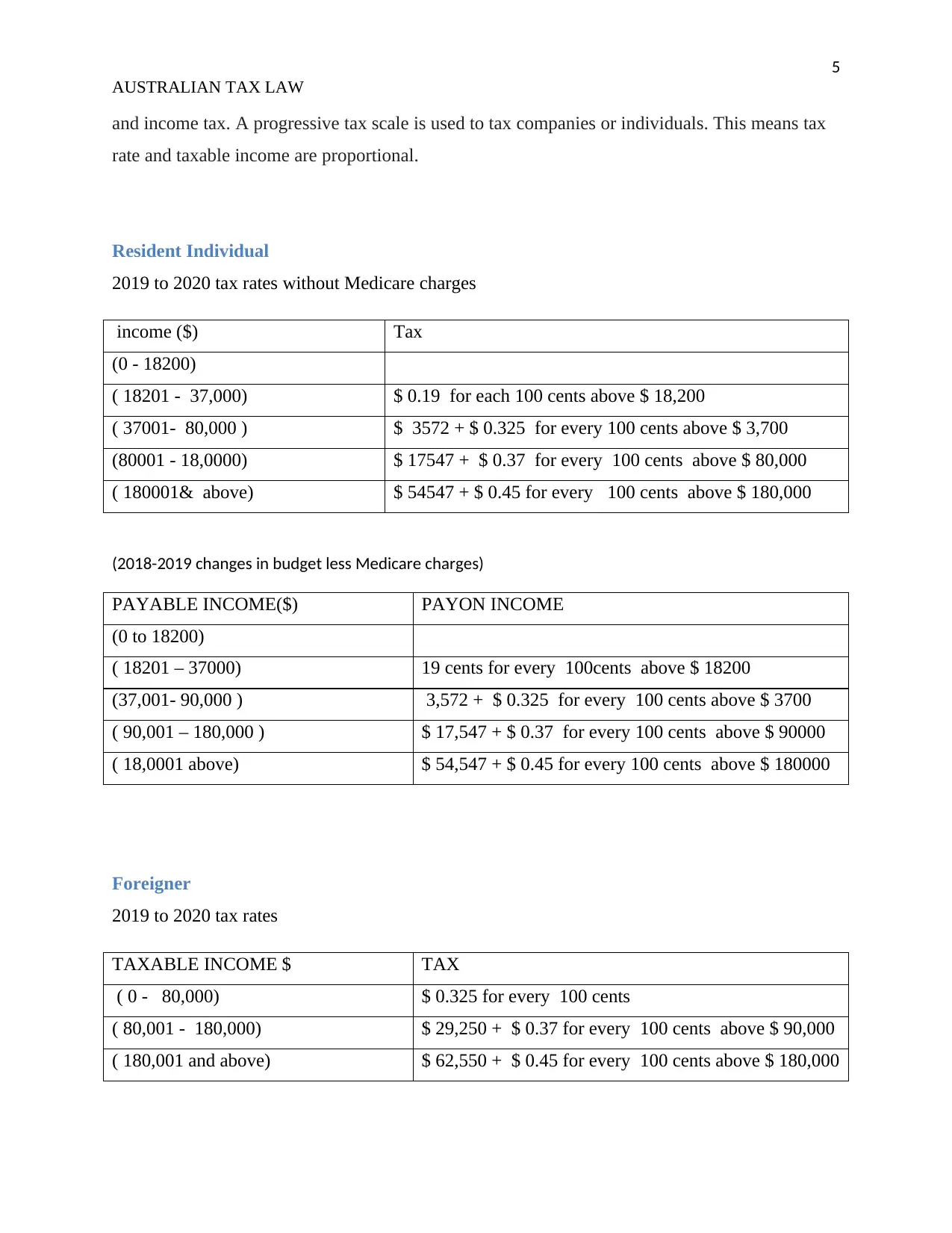

and income tax. A progressive tax scale is used to tax companies or individuals. This means tax

rate and taxable income are proportional.

Resident Individual

2019 to 2020 tax rates without Medicare charges

income ($) Tax

(0 - 18200)

( 18201 - 37,000) $ 0.19 for each 100 cents above $ 18,200

( 37001- 80,000 ) $ 3572 + $ 0.325 for every 100 cents above $ 3,700

(80001 - 18,0000) $ 17547 + $ 0.37 for every 100 cents above $ 80,000

( 180001& above) $ 54547 + $ 0.45 for every 100 cents above $ 180,000

(2018-2019 changes in budget less Medicare charges)

PAYABLE INCOME($) PAYON INCOME

(0 to 18200)

( 18201 – 37000) 19 cents for every 100cents above $ 18200

(37,001- 90,000 ) 3,572 + $ 0.325 for every 100 cents above $ 3700

( 90,001 – 180,000 ) $ 17,547 + $ 0.37 for every 100 cents above $ 90000

( 18,0001 above) $ 54,547 + $ 0.45 for every 100 cents above $ 180000

Foreigner

2019 to 2020 tax rates

TAXABLE INCOME $ TAX

( 0 - 80,000) $ 0.325 for every 100 cents

( 80,001 - 180,000) $ 29,250 + $ 0.37 for every 100 cents above $ 90,000

( 180,001 and above) $ 62,550 + $ 0.45 for every 100 cents above $ 180,000

AUSTRALIAN TAX LAW

and income tax. A progressive tax scale is used to tax companies or individuals. This means tax

rate and taxable income are proportional.

Resident Individual

2019 to 2020 tax rates without Medicare charges

income ($) Tax

(0 - 18200)

( 18201 - 37,000) $ 0.19 for each 100 cents above $ 18,200

( 37001- 80,000 ) $ 3572 + $ 0.325 for every 100 cents above $ 3,700

(80001 - 18,0000) $ 17547 + $ 0.37 for every 100 cents above $ 80,000

( 180001& above) $ 54547 + $ 0.45 for every 100 cents above $ 180,000

(2018-2019 changes in budget less Medicare charges)

PAYABLE INCOME($) PAYON INCOME

(0 to 18200)

( 18201 – 37000) 19 cents for every 100cents above $ 18200

(37,001- 90,000 ) 3,572 + $ 0.325 for every 100 cents above $ 3700

( 90,001 – 180,000 ) $ 17,547 + $ 0.37 for every 100 cents above $ 90000

( 18,0001 above) $ 54,547 + $ 0.45 for every 100 cents above $ 180000

Foreigner

2019 to 2020 tax rates

TAXABLE INCOME $ TAX

( 0 - 80,000) $ 0.325 for every 100 cents

( 80,001 - 180,000) $ 29,250 + $ 0.37 for every 100 cents above $ 90,000

( 180,001 and above) $ 62,550 + $ 0.45 for every 100 cents above $ 180,000

6

AUSTRALIAN TAX LAW

Every single income received by companies in Australia adds up to taxable income. The same

rule applies to individuals. In addition, Flat rate tax of 30% on income level is levied on profits

earned by companies however the liberal party agitated for a 1.5% reduction to 28.5% in the year

2015.

Dividends given by companies to shareholders are subject to tax. Such dividends are factored in

a Dividend Imputation System. Its purpose is to make sure that shareholders are paid dividends

using the applicable income tax rates eventually (Kirchler & Hoelzl, 2018, pg.255).

GST(GOODS AND SERVICE TAX)

Is a duty charged on sale of Australian goods and service and foreign goods and services

imported to Australia .this kind of tax is also known as Value Added Tax in other regions . A flat

rate of 10% is imposed on GST. Services like food, health, exports and education however are

not liable to goods and service tax (Freebairn, 2018, pg.263).

FBT-FRINGE BENEFIT TAX

This is an excise duty charged on non cash benefits received by employees from their

employers. Generally fringe tax benefit is levied at a constant rate of 45.5% on the employer or

can also be deducted from employees’ taxable income (Butler &Alcott, 2018, pg.672).

AUSTRALIA TAX SYSTEM

Withholding tax

These are levies imposed on payments at a constant rate subject to payment in question. The

withholding rate in Australia is 30 percent for unfranked dividends and 10 percent interest rate

for interest payments. The rate applies to all tax payers except if the billing is made to a foreigner

whose country has a treaty or an agreement with Australia. The main aim of withholding tax is to

make sure revenue collection is done continuously and within the stated time. The receiver and

not the payer of funds is the one responsible for withholding (Jacob, 2018, pg. 20).

AUSTRALIAN TAX LAW

Every single income received by companies in Australia adds up to taxable income. The same

rule applies to individuals. In addition, Flat rate tax of 30% on income level is levied on profits

earned by companies however the liberal party agitated for a 1.5% reduction to 28.5% in the year

2015.

Dividends given by companies to shareholders are subject to tax. Such dividends are factored in

a Dividend Imputation System. Its purpose is to make sure that shareholders are paid dividends

using the applicable income tax rates eventually (Kirchler & Hoelzl, 2018, pg.255).

GST(GOODS AND SERVICE TAX)

Is a duty charged on sale of Australian goods and service and foreign goods and services

imported to Australia .this kind of tax is also known as Value Added Tax in other regions . A flat

rate of 10% is imposed on GST. Services like food, health, exports and education however are

not liable to goods and service tax (Freebairn, 2018, pg.263).

FBT-FRINGE BENEFIT TAX

This is an excise duty charged on non cash benefits received by employees from their

employers. Generally fringe tax benefit is levied at a constant rate of 45.5% on the employer or

can also be deducted from employees’ taxable income (Butler &Alcott, 2018, pg.672).

AUSTRALIA TAX SYSTEM

Withholding tax

These are levies imposed on payments at a constant rate subject to payment in question. The

withholding rate in Australia is 30 percent for unfranked dividends and 10 percent interest rate

for interest payments. The rate applies to all tax payers except if the billing is made to a foreigner

whose country has a treaty or an agreement with Australia. The main aim of withholding tax is to

make sure revenue collection is done continuously and within the stated time. The receiver and

not the payer of funds is the one responsible for withholding (Jacob, 2018, pg. 20).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

AUSTRALIAN TAX LAW

The amount of tax withheld is paid to Australian Tax office in installment within the year.

Australian companies or individuals will be required to withhold tax if they pay interests

dividends or royalties to non-resident individual or a company. The same entities are liable to

withholding tax if they fail to provide Tax File Number –TFN pr Australian Business Number

where applicable (Mangioni, 2019).

Pay As You Go tax (PAYG) exists in Australia .it is taxed from employees’ salaries and wages

remitted to Australian Tax Office (ATO).if one fails to indicate Australian Business Number

when dealing with payments in his entity, he will automatically be liable to pay as you go tax

(Sandford, 2018).

Self assessment tax

Self taxation system works well in Australia. It is referred to self – assessment model whereby

the tax payers file their own tax returns .this kind of self assessment by taxpayers is believed to

be true and therefore Australian Tax Office (ATO) does not review all taxes in Australia. For the

same reason again, ATO rarely conducts audit to check if the actual tax is tallying with

taxpayers’ self assessment (Mohamed et al.2019, pg .281) .

Anti - avoidance provisions under GST

The provisions of income tax are similar with those in Goods and Service Tax. Such provisions

are made in a way that the alteration of GST timing and reduction of goods and service tax

payable is more beneficial. The target of anti – avoidance provisions is artificial

schemes .scheme is either promises, arrangements, understandings, deeds and any other

agreements expressed or implied (Shome, 2019, pg. 335).

Anti – avoidance rules are applicable under the following circumstances;

a) Existence of Goods and Service Tax benefit .The benefit as a result of the scheme ought

to exist if the company is not required to pay Goods and Service Tax, entity’s entitlement

to GST refund exist, the entity has ever received previous GST refunds and the entity’s

ability to push its payments to a certain time in future.

AUSTRALIAN TAX LAW

The amount of tax withheld is paid to Australian Tax office in installment within the year.

Australian companies or individuals will be required to withhold tax if they pay interests

dividends or royalties to non-resident individual or a company. The same entities are liable to

withholding tax if they fail to provide Tax File Number –TFN pr Australian Business Number

where applicable (Mangioni, 2019).

Pay As You Go tax (PAYG) exists in Australia .it is taxed from employees’ salaries and wages

remitted to Australian Tax Office (ATO).if one fails to indicate Australian Business Number

when dealing with payments in his entity, he will automatically be liable to pay as you go tax

(Sandford, 2018).

Self assessment tax

Self taxation system works well in Australia. It is referred to self – assessment model whereby

the tax payers file their own tax returns .this kind of self assessment by taxpayers is believed to

be true and therefore Australian Tax Office (ATO) does not review all taxes in Australia. For the

same reason again, ATO rarely conducts audit to check if the actual tax is tallying with

taxpayers’ self assessment (Mohamed et al.2019, pg .281) .

Anti - avoidance provisions under GST

The provisions of income tax are similar with those in Goods and Service Tax. Such provisions

are made in a way that the alteration of GST timing and reduction of goods and service tax

payable is more beneficial. The target of anti – avoidance provisions is artificial

schemes .scheme is either promises, arrangements, understandings, deeds and any other

agreements expressed or implied (Shome, 2019, pg. 335).

Anti – avoidance rules are applicable under the following circumstances;

a) Existence of Goods and Service Tax benefit .The benefit as a result of the scheme ought

to exist if the company is not required to pay Goods and Service Tax, entity’s entitlement

to GST refund exist, the entity has ever received previous GST refunds and the entity’s

ability to push its payments to a certain time in future.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

AUSTRALIAN TAX LAW

b) The availability of a scheme. A legal and binding agreement must be there. Also an

alternative approach to amend or restructure the agreement in case the arrangement is not

sealed. Appropriate time should be taken into consideration in this case.

c) The benefit received should be part of the scheme.

d) The benefit received should be out of mere choice or elections. The law underlying the

scheme should stipulate the rightful steps followed for an entity to receive a GST

benefits, it should not be attributed to one’s intentions or choice.

TAX LEGISLATION

City sky Co Ltd case

City sky Co Ltd became eligible to input tax upon its registration. The company intends to put up

15 apartments on its vacant land located in south of Brisbane. Since land is a fixed asset, it is

neither categorized as service or good and therefore Goods and Service Tax cannot be levied on

unused land. Also the black credit provisions cannot compel City sky Co Ltd to pay tax if it has a

plan of putting up the apartments (Fitzpatrick& Kevin, 2019).

Maurice Blackburn is a local advocate who has been contracted by to provide legal service to

City sky Co Ltd at a fee of $ 33000. The GST on Maurice Blackburn services is levied on the

recipient because the advocate’s services are taken as ‘reverse tax mechanism’. if the service is

deliberately intended for its business, City sky Co Ltd will claim input tax credit on GST since

purpose of Maurice Blackburn services were intended to the business only(Storm & Coetzee,

2018, pg151).

Emma’s case

An obligation to pay tax applies when one’s income tax exceeds the standard or basic exemption.

The exemption differs from one assessee to the other .an example is an assessee who is 60years

of age and below is entitled to a 250000 exemption. This exemption however excludes long term

capital gains. In addition, 20 percent taxes are imposed against assessee for long term capital

gains. Such assets are considered to be long capital gains if the period the asset has been held

surpasses 3 years and 2 years for shares respectively.

AUSTRALIAN TAX LAW

b) The availability of a scheme. A legal and binding agreement must be there. Also an

alternative approach to amend or restructure the agreement in case the arrangement is not

sealed. Appropriate time should be taken into consideration in this case.

c) The benefit received should be part of the scheme.

d) The benefit received should be out of mere choice or elections. The law underlying the

scheme should stipulate the rightful steps followed for an entity to receive a GST

benefits, it should not be attributed to one’s intentions or choice.

TAX LEGISLATION

City sky Co Ltd case

City sky Co Ltd became eligible to input tax upon its registration. The company intends to put up

15 apartments on its vacant land located in south of Brisbane. Since land is a fixed asset, it is

neither categorized as service or good and therefore Goods and Service Tax cannot be levied on

unused land. Also the black credit provisions cannot compel City sky Co Ltd to pay tax if it has a

plan of putting up the apartments (Fitzpatrick& Kevin, 2019).

Maurice Blackburn is a local advocate who has been contracted by to provide legal service to

City sky Co Ltd at a fee of $ 33000. The GST on Maurice Blackburn services is levied on the

recipient because the advocate’s services are taken as ‘reverse tax mechanism’. if the service is

deliberately intended for its business, City sky Co Ltd will claim input tax credit on GST since

purpose of Maurice Blackburn services were intended to the business only(Storm & Coetzee,

2018, pg151).

Emma’s case

An obligation to pay tax applies when one’s income tax exceeds the standard or basic exemption.

The exemption differs from one assessee to the other .an example is an assessee who is 60years

of age and below is entitled to a 250000 exemption. This exemption however excludes long term

capital gains. In addition, 20 percent taxes are imposed against assessee for long term capital

gains. Such assets are considered to be long capital gains if the period the asset has been held

surpasses 3 years and 2 years for shares respectively.

9

AUSTRALIAN TAX LAW

Emma’s capital gains computation

Land value

Value after sale - $ 1000,000

Purchase consideration -$ 265,000

Costs incurred -$ 57,500

Gross Long Term gain - ($ 1000, 000- $ 265,000- $ 57,500)

= 677,500

Value of Shares:

Acquisition cost = ( 3.5×1000) =$ 3500

Expenses incurred on sale= (0.02 ×50,850) =1017

Sale value = (1000 shares × $ 50.85) = $ 50850

Gross Long Term Capital on shares =$ 46333

Stamp Collection

Value on Sale = ($ 50,000)

Costs incurred = ($5000)

Purchase value = ($60000)

Gross Loss = (50,000 minus 60,000 minus5, 000)

= - $ 15,000

AUSTRALIAN TAX LAW

Emma’s capital gains computation

Land value

Value after sale - $ 1000,000

Purchase consideration -$ 265,000

Costs incurred -$ 57,500

Gross Long Term gain - ($ 1000, 000- $ 265,000- $ 57,500)

= 677,500

Value of Shares:

Acquisition cost = ( 3.5×1000) =$ 3500

Expenses incurred on sale= (0.02 ×50,850) =1017

Sale value = (1000 shares × $ 50.85) = $ 50850

Gross Long Term Capital on shares =$ 46333

Stamp Collection

Value on Sale = ($ 50,000)

Costs incurred = ($5000)

Purchase value = ($60000)

Gross Loss = (50,000 minus 60,000 minus5, 000)

= - $ 15,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

AUSTRALIAN TAX LAW

Total Loss on stamp sales = $ (-15,000)

Piano

Purchase value = $ (80,000)

After Sale value =$ (30,000)

Gross Loss = (80,000 minus 30,000)

= (50,000)

Total Loss=$ -50,000

Long term capital gain

= (677500 -50000-46333 – 15000)

= $ 566,167

Tax levied on long term gain for the year 2015

= (20/100× 566167)

= $ 113233.

TAXATION PRINCIPLES

Taxation principles are the basic values or elements a good tax system should exhibit. Such

values include neutrality, certainty, efficiency, equity and simplicity (Yong et al.2019).

Equity is the fair distribution or allocation of tax obligation to the intended population.

Distribution of tax responsibility is either horizontal or vertical equity. Horizontal equity is

where payers on same level are levied equally while in vertical equity, tax is levied depending on

the level of the tax payer (Tran & Zakariyya, 2019, pg.5).

Efficiency principle should be demonstrated by a system by sticking to the decisions made

concerning distribution and allocation of resource in the economy.

AUSTRALIAN TAX LAW

Total Loss on stamp sales = $ (-15,000)

Piano

Purchase value = $ (80,000)

After Sale value =$ (30,000)

Gross Loss = (80,000 minus 30,000)

= (50,000)

Total Loss=$ -50,000

Long term capital gain

= (677500 -50000-46333 – 15000)

= $ 566,167

Tax levied on long term gain for the year 2015

= (20/100× 566167)

= $ 113233.

TAXATION PRINCIPLES

Taxation principles are the basic values or elements a good tax system should exhibit. Such

values include neutrality, certainty, efficiency, equity and simplicity (Yong et al.2019).

Equity is the fair distribution or allocation of tax obligation to the intended population.

Distribution of tax responsibility is either horizontal or vertical equity. Horizontal equity is

where payers on same level are levied equally while in vertical equity, tax is levied depending on

the level of the tax payer (Tran & Zakariyya, 2019, pg.5).

Efficiency principle should be demonstrated by a system by sticking to the decisions made

concerning distribution and allocation of resource in the economy.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

AUSTRALIAN TAX LAW

Simplicity is also among f the basic values of a good tax system. Payers should easily understand

their tax responsibility.

Neutrality principle is where the tax charged on tax payers has no effect on their choices. Finally,

certainty principle states that the assessee should be aware of the tax responsibility and the plan

on how the provisions are met.

REFERENCES

Anesa, M., Gillespie, N., Spee, A.P. and Sadiq, K., 2019. The legitimation of corporate tax

minimization. Accounting, Organizations and Society, 75, pp.17-39.

Butler, C. and Calcott, P., 2018. Optimal fringe benefit taxes: the implications of business

use. International Tax and Public Finance, 25(3), pp.654-672.

Evans, A.C., 2019. Why we use private trusts in Australia: The income tax dimension

explained. Sydney L. Rev., 41, p.217.

Fitzpatrick, Kevin. "The Australian Taxation Office's approaches to aggressive tax planning."

In Centre for Tax System Integrity Third International Conference on'Responsive Regulation:

International perspectives on taxation'. Canberra, 24-25 July 2003. Centre for Tax System

Integrity (CTSI), Research School of Social Sciences, The Australian National University, 2019.

Freebairn, J., 2018. Federalism and Tax reform. Australian Economic Review, 51(2), pp.262-

268.

Jacob, M., 2018. Tax regimes and capital gains realizations. European Accounting

Review, 27(1), pp.1-21.

Kirchler, E. and Hoelzl, E., 2018. 16 Tax Behaviour. CENTRE FOR DECISION RESEARCH,

UNIVERSITY OF LEEDS, UK, p.255.

AUSTRALIAN TAX LAW

Simplicity is also among f the basic values of a good tax system. Payers should easily understand

their tax responsibility.

Neutrality principle is where the tax charged on tax payers has no effect on their choices. Finally,

certainty principle states that the assessee should be aware of the tax responsibility and the plan

on how the provisions are met.

REFERENCES

Anesa, M., Gillespie, N., Spee, A.P. and Sadiq, K., 2019. The legitimation of corporate tax

minimization. Accounting, Organizations and Society, 75, pp.17-39.

Butler, C. and Calcott, P., 2018. Optimal fringe benefit taxes: the implications of business

use. International Tax and Public Finance, 25(3), pp.654-672.

Evans, A.C., 2019. Why we use private trusts in Australia: The income tax dimension

explained. Sydney L. Rev., 41, p.217.

Fitzpatrick, Kevin. "The Australian Taxation Office's approaches to aggressive tax planning."

In Centre for Tax System Integrity Third International Conference on'Responsive Regulation:

International perspectives on taxation'. Canberra, 24-25 July 2003. Centre for Tax System

Integrity (CTSI), Research School of Social Sciences, The Australian National University, 2019.

Freebairn, J., 2018. Federalism and Tax reform. Australian Economic Review, 51(2), pp.262-

268.

Jacob, M., 2018. Tax regimes and capital gains realizations. European Accounting

Review, 27(1), pp.1-21.

Kirchler, E. and Hoelzl, E., 2018. 16 Tax Behaviour. CENTRE FOR DECISION RESEARCH,

UNIVERSITY OF LEEDS, UK, p.255.

12

AUSTRALIAN TAX LAW

Mangioni, V., 2019. Value capture taxation: alternate sources of revenue for Sub-Central

government in Australia. Journal of Financial Management of Property and Construction.

Mohamed, S., Hitam, J., Mazlan, N.F. and Aziz, N.A.A., 2019. Case Study of Taxpayers Usage

on E-Filing System. In Proceedings of the Regional Conference on Science, Technology and

Social Sciences (RCSTSS 2016) (pp. 281-290). Springer, Singapore.

Sandford, C.T., 2018. Taxing Personal Wealth: An Analysis of Capital Taxation in the United

Kingdom—History, Present Structure and Future Possibilities. Routledge.

Shome, P., 2019. General Anti-Avoidance Rules (GAAR): A Critical Analysis. Revista de

Direito Internacional Econômico e Tributário, 13(1), pp.331-355.

Storm, A. and Coetzee, K., 2018. Towards Improving South Africa's Legislation On Tax

Evasion: A Comparison of Legislation On Tax Evasion of The USA, UK, Australia and South

Africa. Journal of Applied Business Research, 34(1), p.151.

Tran, C. and Zakariyya, N., 2019. Tax Progressivity in Australia: Facts, Measurements and

Estimates. Tax and Transfer Policy Institute, Working paper, 5.

Yong, L.Y., Yahya, M.H., Noordin, B.A.A. and Selamat, A.I., 2019. The Effect of Goods and

Services Tax (GST) Imposition on Stock Market Overreaction and Trading Volume in Malaysia

and Australia. Jurnal Pengurusan (UKM Journal of Management), 55.

AUSTRALIAN TAX LAW

Mangioni, V., 2019. Value capture taxation: alternate sources of revenue for Sub-Central

government in Australia. Journal of Financial Management of Property and Construction.

Mohamed, S., Hitam, J., Mazlan, N.F. and Aziz, N.A.A., 2019. Case Study of Taxpayers Usage

on E-Filing System. In Proceedings of the Regional Conference on Science, Technology and

Social Sciences (RCSTSS 2016) (pp. 281-290). Springer, Singapore.

Sandford, C.T., 2018. Taxing Personal Wealth: An Analysis of Capital Taxation in the United

Kingdom—History, Present Structure and Future Possibilities. Routledge.

Shome, P., 2019. General Anti-Avoidance Rules (GAAR): A Critical Analysis. Revista de

Direito Internacional Econômico e Tributário, 13(1), pp.331-355.

Storm, A. and Coetzee, K., 2018. Towards Improving South Africa's Legislation On Tax

Evasion: A Comparison of Legislation On Tax Evasion of The USA, UK, Australia and South

Africa. Journal of Applied Business Research, 34(1), p.151.

Tran, C. and Zakariyya, N., 2019. Tax Progressivity in Australia: Facts, Measurements and

Estimates. Tax and Transfer Policy Institute, Working paper, 5.

Yong, L.Y., Yahya, M.H., Noordin, B.A.A. and Selamat, A.I., 2019. The Effect of Goods and

Services Tax (GST) Imposition on Stock Market Overreaction and Trading Volume in Malaysia

and Australia. Jurnal Pengurusan (UKM Journal of Management), 55.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.