Comprehensive Analysis of Australian Income Tax Laws and Legislations

VerifiedAdded on 2022/10/15

|13

|2707

|146

Report

AI Summary

This report provides a detailed analysis of Australian taxation, focusing on income tax, capital gains tax (CGT), goods and services tax (GST), fringe benefit tax (FBT), withholding tax, self-assessment tax, and anti-avoidance rules. It examines income tax rates for residents and non-residents, and includes case studies on Emma's capital gain tax and City Sky Company's GST to demonstrate real-world application of these concepts. The report also covers key tax legislations and principles like efficiency, equity, neutrality, and simplicity. It explores the application of GST and CGT in specific scenarios, and provides a comprehensive overview of the Australian tax system. The report aims to equip students with a thorough understanding of tax concepts, deductions, and their practical implications.

1

Australian Tax Legislations

Australian Income Tax Laws

Institution

Date

Australian Tax Legislations

Australian Income Tax Laws

Institution

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Australian Tax Legislations

Executive summary

The aim of this report is to analyze various aspects of taxation concepts such as the income tax

and the rules applied on the same and how they can be applied in real life. The report also

intends to equip the student with the understanding and knowledge on various deductions

concerning income ax both in Australia and Diaspora.

A case study on Emma’s capital gain tax and city sky company‘s goods and service tax

demonstrate best approaches to GST and CGT issues. Finally, the report contain s the taxation

principles which illustrates what a tax system should demonstrate.

Australian Tax Legislations

Executive summary

The aim of this report is to analyze various aspects of taxation concepts such as the income tax

and the rules applied on the same and how they can be applied in real life. The report also

intends to equip the student with the understanding and knowledge on various deductions

concerning income ax both in Australia and Diaspora.

A case study on Emma’s capital gain tax and city sky company‘s goods and service tax

demonstrate best approaches to GST and CGT issues. Finally, the report contain s the taxation

principles which illustrates what a tax system should demonstrate.

3

Australian Tax Legislations

Table of Contents

Executive summary.....................................................................................................................................2

Introduction.................................................................................................................................................4

Income Tax Rates In Australia....................................................................................................................4

Australian residents (2019-2020 tax rates less 2% Medicare tax)............................................................4

Nonresident (2019-2020 tax rates less Medicare tax)..............................................................................5

Capital gain tax........................................................................................................................................5

Goods and service tax..............................................................................................................................6

Fringe benefit tax.....................................................................................................................................6

Withholding tax.......................................................................................................................................6

Self assessment tax..................................................................................................................................6

Anti avoidance rules................................................................................................................................7

LEGISLATIONS.........................................................................................................................................7

REFERENCES..........................................................................................................................................12

Australian Tax Legislations

Table of Contents

Executive summary.....................................................................................................................................2

Introduction.................................................................................................................................................4

Income Tax Rates In Australia....................................................................................................................4

Australian residents (2019-2020 tax rates less 2% Medicare tax)............................................................4

Nonresident (2019-2020 tax rates less Medicare tax)..............................................................................5

Capital gain tax........................................................................................................................................5

Goods and service tax..............................................................................................................................6

Fringe benefit tax.....................................................................................................................................6

Withholding tax.......................................................................................................................................6

Self assessment tax..................................................................................................................................6

Anti avoidance rules................................................................................................................................7

LEGISLATIONS.........................................................................................................................................7

REFERENCES..........................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

Australian Tax Legislations

Introduction

In Australia, income tax is the most important form of tax the federal government is collecting in

Australia through ATO-Australian Taxation Office. The function of the federal government is to

collect goods and service tax proceeds before its distribution to states in Australia. For income

tax purposes, an entity in Australia is a resident if its incorporation was done in Australia or if it

conducts its operation or business in Australia. In addition, an entity qualifies to be an Australian

resident if the shareholders who control the voting powers are Australian residents or the control

and overall management is in Australia

Income Tax Rates In Australia.

Personal income tax is imposed to individuals at the federal level. It is the Australian’s one of the

most important source of revenue levied progressively. This means high income is proportional

to high rates (Evans, 2019, pg 217).

Australian residents (2019-2020 tax rates less 2% Medicare tax)

Taxable income Tax on this income

0 to $ 18200

$ 18,201 to $ 37,000 19c for @ 100 c over $18,200

$ 37,001 to $ 90,000 $3,572 + 32.5 c for @ 100 c over $37,000

$ 90,001 to $ 180,000 $20,797 + 37 c for @ 100c over $90,000

$ 180,001 and over $54,097 + 45 c for @ 100c over $180,000

Australian residents (2018-2019 tax rates less 2% Medicare tax)

Taxable income Tax on this income

0 to $18200

$ 18,201 to $37,000 19 c for @ 100 c over $18,200

Australian Tax Legislations

Introduction

In Australia, income tax is the most important form of tax the federal government is collecting in

Australia through ATO-Australian Taxation Office. The function of the federal government is to

collect goods and service tax proceeds before its distribution to states in Australia. For income

tax purposes, an entity in Australia is a resident if its incorporation was done in Australia or if it

conducts its operation or business in Australia. In addition, an entity qualifies to be an Australian

resident if the shareholders who control the voting powers are Australian residents or the control

and overall management is in Australia

Income Tax Rates In Australia.

Personal income tax is imposed to individuals at the federal level. It is the Australian’s one of the

most important source of revenue levied progressively. This means high income is proportional

to high rates (Evans, 2019, pg 217).

Australian residents (2019-2020 tax rates less 2% Medicare tax)

Taxable income Tax on this income

0 to $ 18200

$ 18,201 to $ 37,000 19c for @ 100 c over $18,200

$ 37,001 to $ 90,000 $3,572 + 32.5 c for @ 100 c over $37,000

$ 90,001 to $ 180,000 $20,797 + 37 c for @ 100c over $90,000

$ 180,001 and over $54,097 + 45 c for @ 100c over $180,000

Australian residents (2018-2019 tax rates less 2% Medicare tax)

Taxable income Tax on this income

0 to $18200

$ 18,201 to $37,000 19 c for @ 100 c over $18,200

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

Australian Tax Legislations

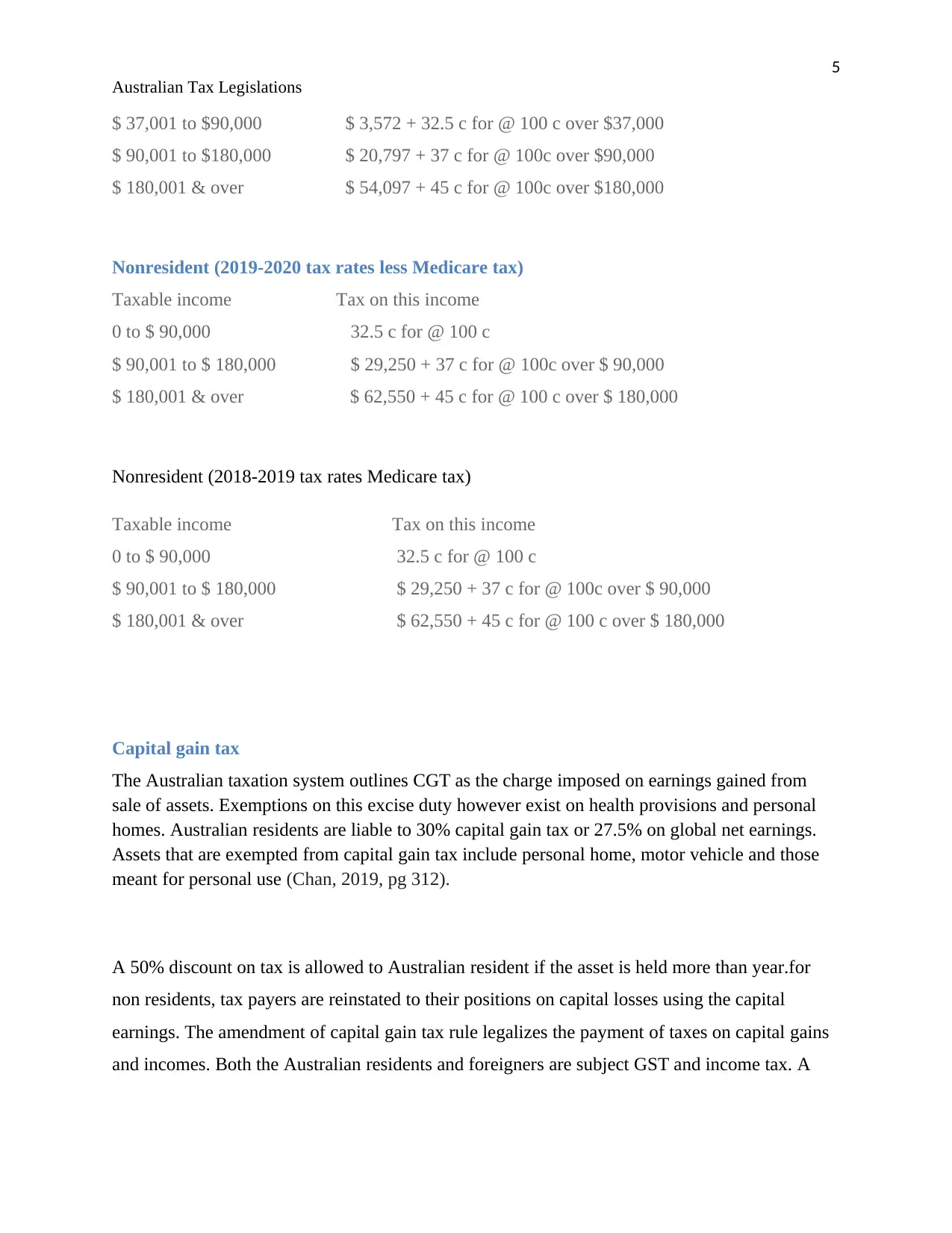

$ 37,001 to $90,000 $ 3,572 + 32.5 c for @ 100 c over $37,000

$ 90,001 to $180,000 $ 20,797 + 37 c for @ 100c over $90,000

$ 180,001 & over $ 54,097 + 45 c for @ 100c over $180,000

Nonresident (2019-2020 tax rates less Medicare tax)

Taxable income Tax on this income

0 to $ 90,000 32.5 c for @ 100 c

$ 90,001 to $ 180,000 $ 29,250 + 37 c for @ 100c over $ 90,000

$ 180,001 & over $ 62,550 + 45 c for @ 100 c over $ 180,000

Nonresident (2018-2019 tax rates Medicare tax)

Taxable income Tax on this income

0 to $ 90,000 32.5 c for @ 100 c

$ 90,001 to $ 180,000 $ 29,250 + 37 c for @ 100c over $ 90,000

$ 180,001 & over $ 62,550 + 45 c for @ 100 c over $ 180,000

Capital gain tax

The Australian taxation system outlines CGT as the charge imposed on earnings gained from

sale of assets. Exemptions on this excise duty however exist on health provisions and personal

homes. Australian residents are liable to 30% capital gain tax or 27.5% on global net earnings.

Assets that are exempted from capital gain tax include personal home, motor vehicle and those

meant for personal use (Chan, 2019, pg 312).

A 50% discount on tax is allowed to Australian resident if the asset is held more than year.for

non residents, tax payers are reinstated to their positions on capital losses using the capital

earnings. The amendment of capital gain tax rule legalizes the payment of taxes on capital gains

and incomes. Both the Australian residents and foreigners are subject GST and income tax. A

Australian Tax Legislations

$ 37,001 to $90,000 $ 3,572 + 32.5 c for @ 100 c over $37,000

$ 90,001 to $180,000 $ 20,797 + 37 c for @ 100c over $90,000

$ 180,001 & over $ 54,097 + 45 c for @ 100c over $180,000

Nonresident (2019-2020 tax rates less Medicare tax)

Taxable income Tax on this income

0 to $ 90,000 32.5 c for @ 100 c

$ 90,001 to $ 180,000 $ 29,250 + 37 c for @ 100c over $ 90,000

$ 180,001 & over $ 62,550 + 45 c for @ 100 c over $ 180,000

Nonresident (2018-2019 tax rates Medicare tax)

Taxable income Tax on this income

0 to $ 90,000 32.5 c for @ 100 c

$ 90,001 to $ 180,000 $ 29,250 + 37 c for @ 100c over $ 90,000

$ 180,001 & over $ 62,550 + 45 c for @ 100 c over $ 180,000

Capital gain tax

The Australian taxation system outlines CGT as the charge imposed on earnings gained from

sale of assets. Exemptions on this excise duty however exist on health provisions and personal

homes. Australian residents are liable to 30% capital gain tax or 27.5% on global net earnings.

Assets that are exempted from capital gain tax include personal home, motor vehicle and those

meant for personal use (Chan, 2019, pg 312).

A 50% discount on tax is allowed to Australian resident if the asset is held more than year.for

non residents, tax payers are reinstated to their positions on capital losses using the capital

earnings. The amendment of capital gain tax rule legalizes the payment of taxes on capital gains

and incomes. Both the Australian residents and foreigners are subject GST and income tax. A

6

Australian Tax Legislations

progressive tax basis or scale system is used by individuals when taxes. In other words, the level

of income is directly proportional to the rate and amount of tax paid.

Goods and service tax

This is a 10 % value added tax levied on disposal of goods and sale services within Australia.

Education, food, exports and health care are however exempted from GST. It is mandatory for

resident entities to register for GST if their income surpasses the least threshold required.

Businesses liable to GST are entitled to input tax credits on costs incurred on capital acquisition

and expenses resulting from payment of goods and services (Jacob, Vashishtha &

Venkatachalam, 2019).

Fringe benefit tax

Fringe benefit is a supplement benefit on top of salary received by employees from their

employer. The tax levied on such benefits is known as fringe benefits tax (FBT). Such benefits

include private health care, housing loans and company vehicles. Benefits like remote area

housing allowance, relocation allowance, wages and salary allowance, pension contributions and

work related items like cell phones and protective garments are however exempted from FBT

(Ehling, Tompaidis & Yang, 2019).

.

Withholding tax

This is an income tax charged on the income payer and not the receiver. The tax is retained from

the recipient’s income. Normally; withholding tax is levied at a constant rate on expenditures or

payments. The Australian withholding tax rate is 30% and 10% on unfranked interests and

interest payments respectively. The payers are charged at the rates above except non residents

whose countries have signed double tax consent with Australia. The purpose of this retention tax

is to combat evasion of taxes and to ensure continuous collection of the same (Braithwaite,

2019).

Self assessment tax

In Self assessment tax system, the Australia Taxation Offices that the information provided by

the tax payer when filing taxes is believed to be true. Therefore, the obligation will be directly

transferred to the tax payer whom should ensure that the returns are lodged as per the Australian

Australian Tax Legislations

progressive tax basis or scale system is used by individuals when taxes. In other words, the level

of income is directly proportional to the rate and amount of tax paid.

Goods and service tax

This is a 10 % value added tax levied on disposal of goods and sale services within Australia.

Education, food, exports and health care are however exempted from GST. It is mandatory for

resident entities to register for GST if their income surpasses the least threshold required.

Businesses liable to GST are entitled to input tax credits on costs incurred on capital acquisition

and expenses resulting from payment of goods and services (Jacob, Vashishtha &

Venkatachalam, 2019).

Fringe benefit tax

Fringe benefit is a supplement benefit on top of salary received by employees from their

employer. The tax levied on such benefits is known as fringe benefits tax (FBT). Such benefits

include private health care, housing loans and company vehicles. Benefits like remote area

housing allowance, relocation allowance, wages and salary allowance, pension contributions and

work related items like cell phones and protective garments are however exempted from FBT

(Ehling, Tompaidis & Yang, 2019).

.

Withholding tax

This is an income tax charged on the income payer and not the receiver. The tax is retained from

the recipient’s income. Normally; withholding tax is levied at a constant rate on expenditures or

payments. The Australian withholding tax rate is 30% and 10% on unfranked interests and

interest payments respectively. The payers are charged at the rates above except non residents

whose countries have signed double tax consent with Australia. The purpose of this retention tax

is to combat evasion of taxes and to ensure continuous collection of the same (Braithwaite,

2019).

Self assessment tax

In Self assessment tax system, the Australia Taxation Offices that the information provided by

the tax payer when filing taxes is believed to be true. Therefore, the obligation will be directly

transferred to the tax payer whom should ensure that the returns are lodged as per the Australian

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

Australian Tax Legislations

taxation laws. Australia Taxation Office rarely do audits to confirm if the self assessment taxes

filed by the payer match with the real tax.

Withholding tax applies to resident individuals who fail to quote ABN and TFN where

applicable. Pay as you go (PAYG) tax retention also applies to payment of funds to entities who

fail to quote ABN when dealing with another business (Mitchell et al.2019).

Anti avoidance rules

Anti avoidance provisions in income tax and GST have no difference. They are similar in that,

modifications of payment timing and reduction of GST is more beneficial. An ant avoidance rule

gives the tax commissioner more powers to handle schemes. These schemes can be promises,

arrangements, expressed or implied deeds and agreements. For this rule to apply, a binding and

legally enforceable consent must be there and its provisions to amendments or restructuring if

incase the consent had not been agreed upon. In addition, the scheme as a result of GST benefit

must either be the company’s entitlement to goods and service tax refund and ability to make

payments at any time in future or exemption to GST obligations (Yue,Khandelwal & Nguyen,

2019 ,pg 6).

The benefits enjoyed must be part of the agreement or arrangement laid down else anti avoidance

rule would not be applicable. Finally, the same benefit must be legally enforceable and binding

as per the scheme.

LEGISLATIONS

City Sky Co’s case

Incorporated companies in Australia are subject to input credit .City Sky Co is registered and

therefore it is entitled to input tax credit. The firm is planning to put up a 15 structure apartments

on its vacant land located in southern Brisbane. The unused land cannot be categorized as a good

or service because it is a fixed asset. Therefore GST cannot be levied on City Sky Company’s

Australian Tax Legislations

taxation laws. Australia Taxation Office rarely do audits to confirm if the self assessment taxes

filed by the payer match with the real tax.

Withholding tax applies to resident individuals who fail to quote ABN and TFN where

applicable. Pay as you go (PAYG) tax retention also applies to payment of funds to entities who

fail to quote ABN when dealing with another business (Mitchell et al.2019).

Anti avoidance rules

Anti avoidance provisions in income tax and GST have no difference. They are similar in that,

modifications of payment timing and reduction of GST is more beneficial. An ant avoidance rule

gives the tax commissioner more powers to handle schemes. These schemes can be promises,

arrangements, expressed or implied deeds and agreements. For this rule to apply, a binding and

legally enforceable consent must be there and its provisions to amendments or restructuring if

incase the consent had not been agreed upon. In addition, the scheme as a result of GST benefit

must either be the company’s entitlement to goods and service tax refund and ability to make

payments at any time in future or exemption to GST obligations (Yue,Khandelwal & Nguyen,

2019 ,pg 6).

The benefits enjoyed must be part of the agreement or arrangement laid down else anti avoidance

rule would not be applicable. Finally, the same benefit must be legally enforceable and binding

as per the scheme.

LEGISLATIONS

City Sky Co’s case

Incorporated companies in Australia are subject to input credit .City Sky Co is registered and

therefore it is entitled to input tax credit. The firm is planning to put up a 15 structure apartments

on its vacant land located in southern Brisbane. The unused land cannot be categorized as a good

or service because it is a fixed asset. Therefore GST cannot be levied on City Sky Company’s

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

Australian Tax Legislations

vacant land. City Sky Co’s plan to construct houses will deny it the entitlement of input tax

credit. This is as a result of black credit provisions.

Maurice Blackburn is an advocate offering development services to City Sky Co at a charge of

$ 33000.normally ,services given by advocates or lawyers are under ‘ reverse charge mechanism’

and therefore the charge is imposed to the recipient and not the giver of the service. Entities that

use the services purposely for their business only are entitled to input tax credit.

Emma’s case

A GST is imposed to an assessee whose income surpasses tax exemptions. These exemptions

differ from one assessee to another. An assessee who is above 60years is not entitled to basic

exemptions because this age exceeds the standard age for exemption.normaly, assessee who are

below 60 years can claim 250,000 exemptions. For long-term capital gains, exemptions are not

applicable and instead the assessee is obligated a 20% duty on such income.ann asset is

considered as a long term capital gain if it has been held for at least 3 years and 2 years for

shares.

Calculations; Emma’s capital gains the year 2015

Value of land

Disposal value = $ 1000000

Acquisition consideration = $ 265000

Expenses = $ 57500

Gross Long Term gain = ($ 1000000- $ 265000- $ 57500)

= 677500

Share value:

Acquisition value = $ 3.5 × 1,000 shares =$ 3,500

Australian Tax Legislations

vacant land. City Sky Co’s plan to construct houses will deny it the entitlement of input tax

credit. This is as a result of black credit provisions.

Maurice Blackburn is an advocate offering development services to City Sky Co at a charge of

$ 33000.normally ,services given by advocates or lawyers are under ‘ reverse charge mechanism’

and therefore the charge is imposed to the recipient and not the giver of the service. Entities that

use the services purposely for their business only are entitled to input tax credit.

Emma’s case

A GST is imposed to an assessee whose income surpasses tax exemptions. These exemptions

differ from one assessee to another. An assessee who is above 60years is not entitled to basic

exemptions because this age exceeds the standard age for exemption.normaly, assessee who are

below 60 years can claim 250,000 exemptions. For long-term capital gains, exemptions are not

applicable and instead the assessee is obligated a 20% duty on such income.ann asset is

considered as a long term capital gain if it has been held for at least 3 years and 2 years for

shares.

Calculations; Emma’s capital gains the year 2015

Value of land

Disposal value = $ 1000000

Acquisition consideration = $ 265000

Expenses = $ 57500

Gross Long Term gain = ($ 1000000- $ 265000- $ 57500)

= 677500

Share value:

Acquisition value = $ 3.5 × 1,000 shares =$ 3,500

9

Australian Tax Legislations

Costs incurred on sale= 0.02 × 50850 = $ 1017

Disposal value = 1000 (shares) × 50.85

= $ 50850

Gross Long Term share Capital =$ 46333

Stamp Collection

Disposal value = $ 50000

Expenses incurred = $ 5000

Acquisition value = $ 60000

Gross Loss = 50000 - 60,000 - 5 000

= - $ 15000

Total Loss on stamp disposal= $ -15000

Piano

Acquisition value = $ 80000

Disposal value =$ 30000

Gross Loss = 80000 - 30000

= (50,000)

Total Loss=$ 50000

Long term capital gain

= ($ 677500 - $ 50000- $ 46333 – $ 15000)

= $ 566167

Australian Tax Legislations

Costs incurred on sale= 0.02 × 50850 = $ 1017

Disposal value = 1000 (shares) × 50.85

= $ 50850

Gross Long Term share Capital =$ 46333

Stamp Collection

Disposal value = $ 50000

Expenses incurred = $ 5000

Acquisition value = $ 60000

Gross Loss = 50000 - 60,000 - 5 000

= - $ 15000

Total Loss on stamp disposal= $ -15000

Piano

Acquisition value = $ 80000

Disposal value =$ 30000

Gross Loss = 80000 - 30000

= (50,000)

Total Loss=$ 50000

Long term capital gain

= ($ 677500 - $ 50000- $ 46333 – $ 15000)

= $ 566167

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

Australian Tax Legislations

Tax charged on long term gain in 2015

= 0.02× 566167

= $ 113233.

The assessee can be entitled to set off loss on long-term capital gains with earnings gained from

long term capital. For individuals, tax returns are filed before every 31st of July on yearly basis

according to the 1961 income tax act of Australia (Shome, 2019, pg 355).

.

TAX PRINCIPLES IN AUSTRALIA

A good tax system should demonstrate basic values like efficiency, equity, neutrality and

simplicity.

Neutrality is one of the significant fundamental elements essential in a tax system. Payers should

not feel the effect on their choice to pay the tax imposed on them. The principle of certainty

states that the tax payers should be made aware of their tax responsibility before they make any

plans to meet the provisions (Storm & Coetzee, 2018, pg 151).

A good tax system should also be clear and easily understood by the tax payers and the

population responsible for the tax burden. Payers should understand their tax responsibility.

The principle of equity is concerned with the distribution of tax burden to the population.

Allocation should be fair to every tax payer. The obligation can be done vertically, horizontally

and on benefit principle. .For horizontal distribution, assessee are taxed based on their equal

level of income. It perceives that equally paid individuals are supposed to be taxed equally;

however this kind of principle is difficult to put into practice .Vertical equity on the other hand,

tax payers are charged based on their income levels. The able payers are supposed to pay

maximum taxes according to this principle. On broader perspective, vertical tax principle implies

that a fair tax system is where taxes are paid to government based on one’s financial ability (Tran

& Zakariyya, 2019).

Australian Tax Legislations

Tax charged on long term gain in 2015

= 0.02× 566167

= $ 113233.

The assessee can be entitled to set off loss on long-term capital gains with earnings gained from

long term capital. For individuals, tax returns are filed before every 31st of July on yearly basis

according to the 1961 income tax act of Australia (Shome, 2019, pg 355).

.

TAX PRINCIPLES IN AUSTRALIA

A good tax system should demonstrate basic values like efficiency, equity, neutrality and

simplicity.

Neutrality is one of the significant fundamental elements essential in a tax system. Payers should

not feel the effect on their choice to pay the tax imposed on them. The principle of certainty

states that the tax payers should be made aware of their tax responsibility before they make any

plans to meet the provisions (Storm & Coetzee, 2018, pg 151).

A good tax system should also be clear and easily understood by the tax payers and the

population responsible for the tax burden. Payers should understand their tax responsibility.

The principle of equity is concerned with the distribution of tax burden to the population.

Allocation should be fair to every tax payer. The obligation can be done vertically, horizontally

and on benefit principle. .For horizontal distribution, assessee are taxed based on their equal

level of income. It perceives that equally paid individuals are supposed to be taxed equally;

however this kind of principle is difficult to put into practice .Vertical equity on the other hand,

tax payers are charged based on their income levels. The able payers are supposed to pay

maximum taxes according to this principle. On broader perspective, vertical tax principle implies

that a fair tax system is where taxes are paid to government based on one’s financial ability (Tran

& Zakariyya, 2019).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

Australian Tax Legislations

The benefit principle is concept of fair taxation which a times might violate the perspective of

vertical equity principle. Benefit principle says that the aim of taxation is to collect revenues to

government for its services. People should pay dues according to the services they receive from

government. It is however difficult to implement this principle since the ATO should formulates

tax rates based on how each person benefits from government services (Yong et al.2019.pg 55).

Finally, a good tax system should demonstrate the element of efficiency by sticking to the

distribution decisions made regarding allocation of resources in the economy.

Australian Tax Legislations

The benefit principle is concept of fair taxation which a times might violate the perspective of

vertical equity principle. Benefit principle says that the aim of taxation is to collect revenues to

government for its services. People should pay dues according to the services they receive from

government. It is however difficult to implement this principle since the ATO should formulates

tax rates based on how each person benefits from government services (Yong et al.2019.pg 55).

Finally, a good tax system should demonstrate the element of efficiency by sticking to the

distribution decisions made regarding allocation of resources in the economy.

12

Australian Tax Legislations

REFERENCES

Braithwaite, V., 2019. Attitudes to tax policy: Politics, self-interest and social values.

Chan, E.Y., 2019. Exposure to national flags reduces tax evasion: Evidence from the United

States, Australia, and Britain. European Journal of Social Psychology, 49(2), pp.300-312.

Ehling, P., Tompaidis, S. and Yang, C., 2019. Tax Collection from Realized Capital Gains on

Equity. Available at SSRN 3349058.

Evans, A.C., 2019. Why we use private trusts in Australia: The income tax dimension

explained. Sydney L. Rev., 41, p.217.

He, E., Jacob, M., Vashishtha, R. and Venkatachalam, M., 2019. The effect of capital gains tax

policy changes on long-term investments. Available at SSRN 3383649.

Mitchell, A.D., Voon, T. and Hepburn, J., 2019. Taxing Tech: Risks of an Australian Digital

Services Tax under International Economic Law. Melbourne Journal of International Law,

Forthcoming.

Shome, P., 2019. General Anti-Avoidance Rules (GAAR): A Critical Analysis. Revista de

Direito Internacional Econômico e Tributário, 13(1), pp.331-355.

Storm, A. and Coetzee, K., 2018. Towards Improving South Africa's Legislation On Tax

Evasion: A Comparison of Legislation On Tax Evasion of The USA, UK, Australia and South

Africa. Journal of Applied Business Research, 34(1), p.151.

Tran, C. and Zakariyya, N., 2019. Tax Progressivity in Australia: Facts, Measurements and

Estimates. Tax and Transfer Policy Institute, Working paper, 5.

Australian Tax Legislations

REFERENCES

Braithwaite, V., 2019. Attitudes to tax policy: Politics, self-interest and social values.

Chan, E.Y., 2019. Exposure to national flags reduces tax evasion: Evidence from the United

States, Australia, and Britain. European Journal of Social Psychology, 49(2), pp.300-312.

Ehling, P., Tompaidis, S. and Yang, C., 2019. Tax Collection from Realized Capital Gains on

Equity. Available at SSRN 3349058.

Evans, A.C., 2019. Why we use private trusts in Australia: The income tax dimension

explained. Sydney L. Rev., 41, p.217.

He, E., Jacob, M., Vashishtha, R. and Venkatachalam, M., 2019. The effect of capital gains tax

policy changes on long-term investments. Available at SSRN 3383649.

Mitchell, A.D., Voon, T. and Hepburn, J., 2019. Taxing Tech: Risks of an Australian Digital

Services Tax under International Economic Law. Melbourne Journal of International Law,

Forthcoming.

Shome, P., 2019. General Anti-Avoidance Rules (GAAR): A Critical Analysis. Revista de

Direito Internacional Econômico e Tributário, 13(1), pp.331-355.

Storm, A. and Coetzee, K., 2018. Towards Improving South Africa's Legislation On Tax

Evasion: A Comparison of Legislation On Tax Evasion of The USA, UK, Australia and South

Africa. Journal of Applied Business Research, 34(1), p.151.

Tran, C. and Zakariyya, N., 2019. Tax Progressivity in Australia: Facts, Measurements and

Estimates. Tax and Transfer Policy Institute, Working paper, 5.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.