Acc306: Australian Taxation Report: Income Tax, Medicare Levy Analysis

VerifiedAdded on 2020/06/03

|14

|2939

|41

Report

AI Summary

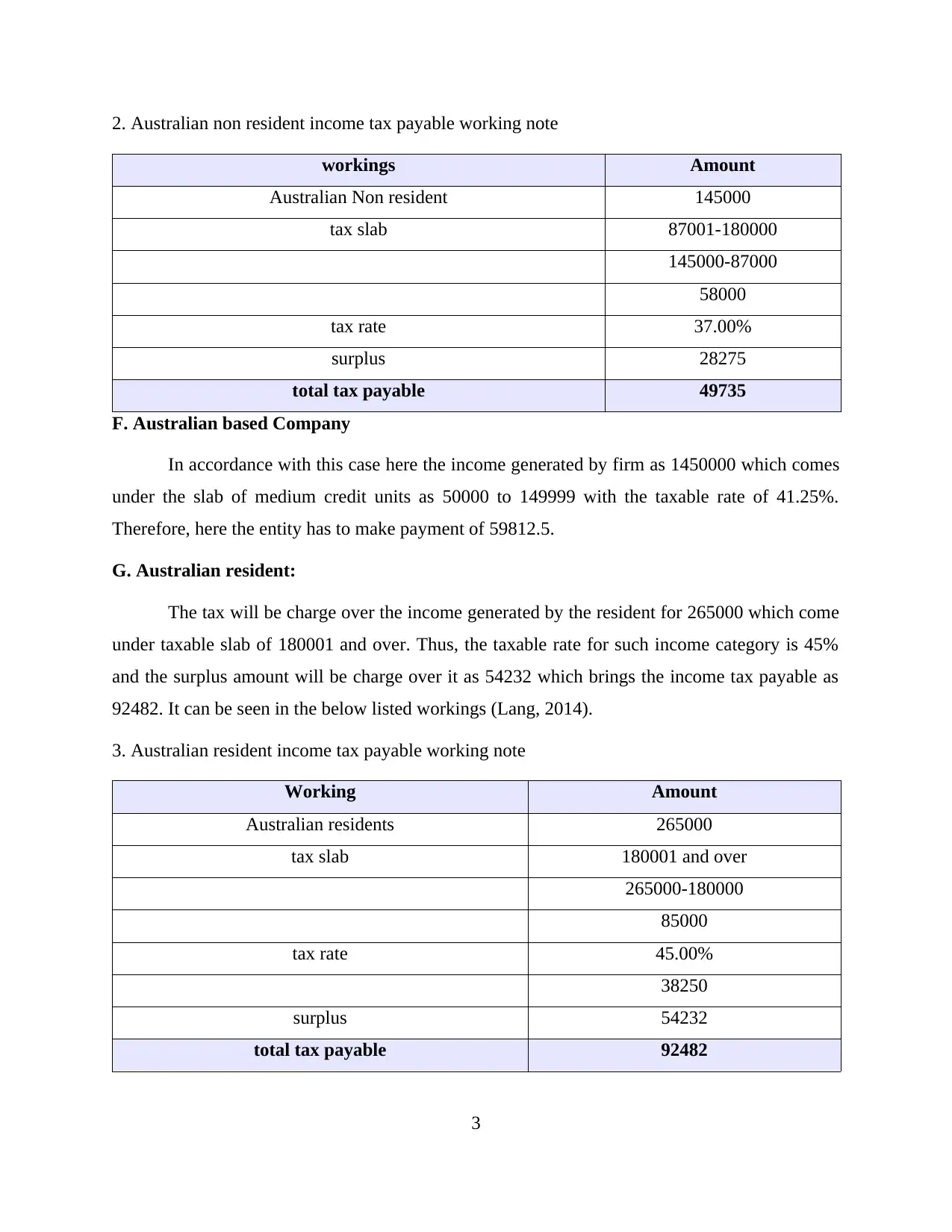

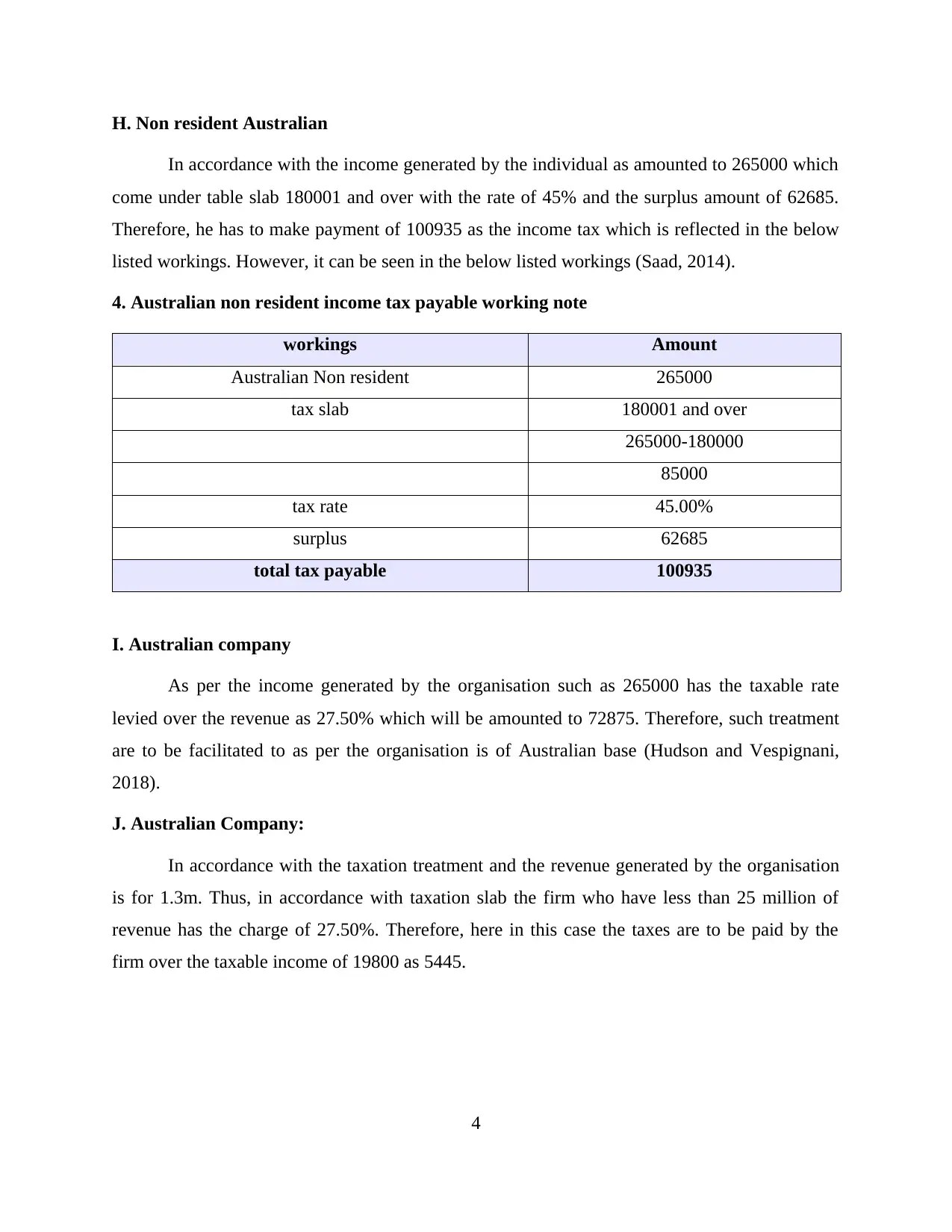

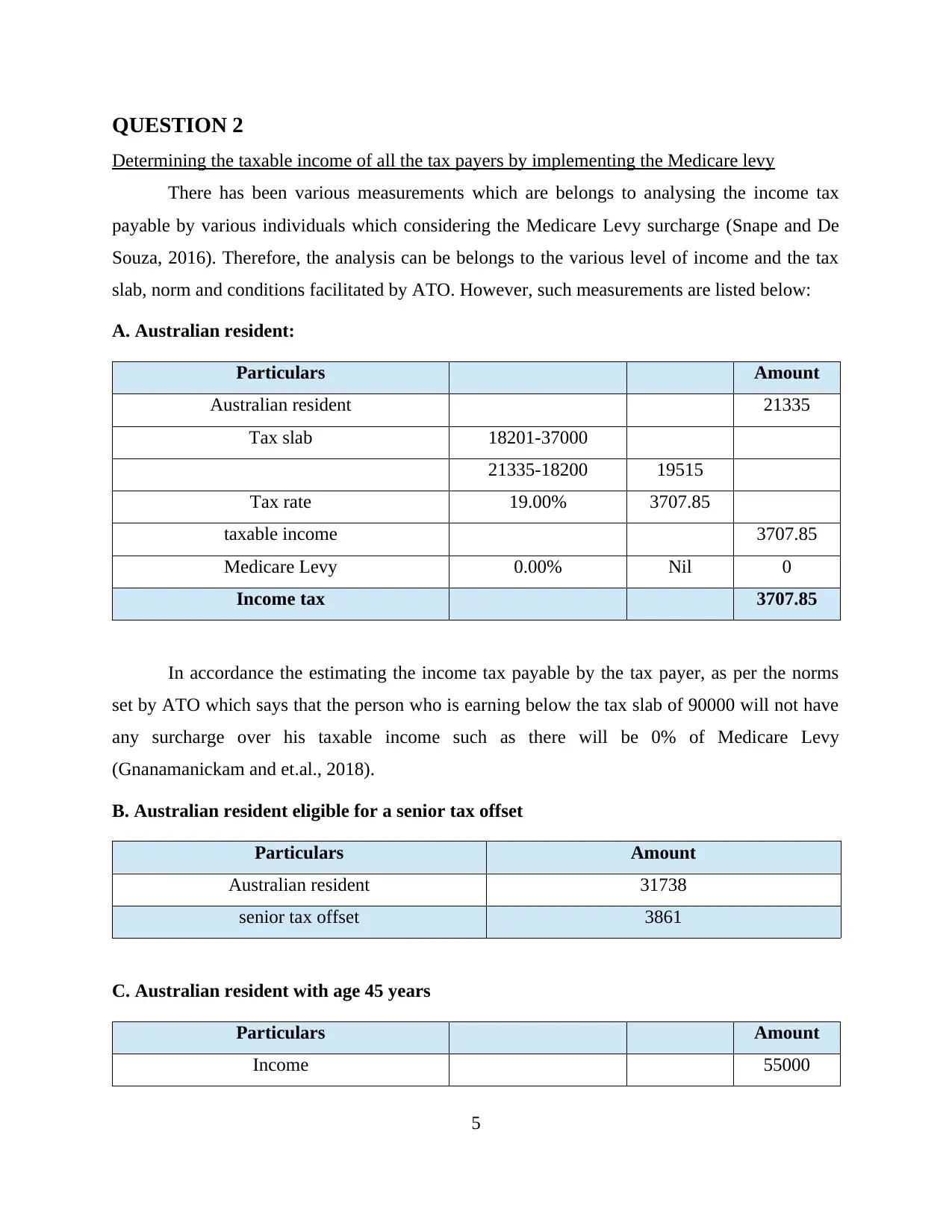

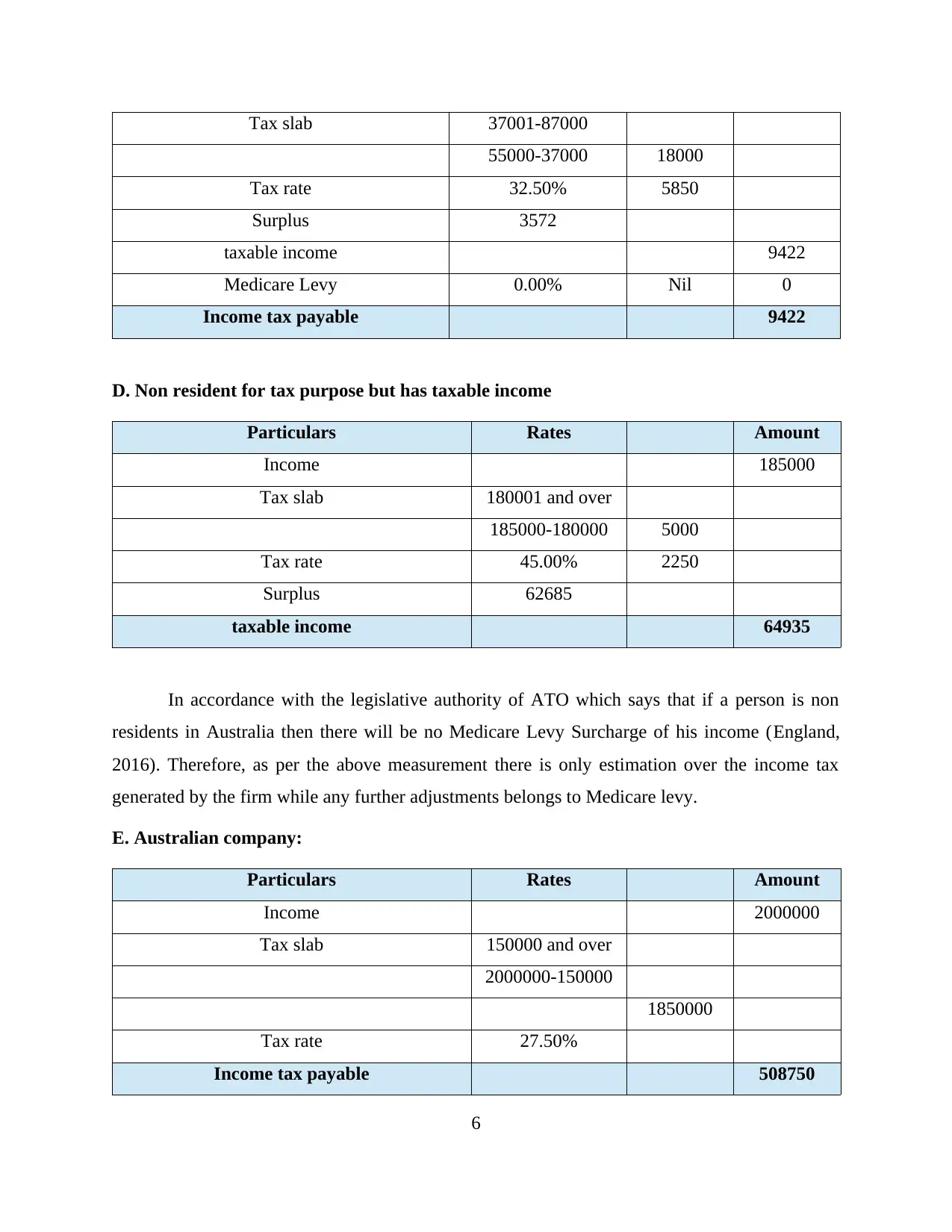

This report, prepared for Acc306, provides a comprehensive analysis of the Australian taxation system. It delves into the calculation of income tax for Australian residents, non-residents, and companies, considering different income levels and tax slabs. The report meticulously calculates tax payable, taking into account the Medicare levy and various scenarios, including those with and without private health insurance. It also examines specific cases, such as calculating income tax refunds and payments for individuals and couples. Furthermore, the report includes a discounted cash flow valuation for General Mills, Inc. The report utilizes working notes to illustrate the calculations and applies relevant tax rates and regulations to determine taxable income and tax liabilities. Overall, the report serves as a practical guide to understanding the complexities of Australian income tax and its impact on different entities and individuals.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.