HI6028 Taxation: Partnership Income, Deductions & Fringe Benefits

VerifiedAdded on 2023/04/25

|9

|2117

|85

Homework Assignment

AI Summary

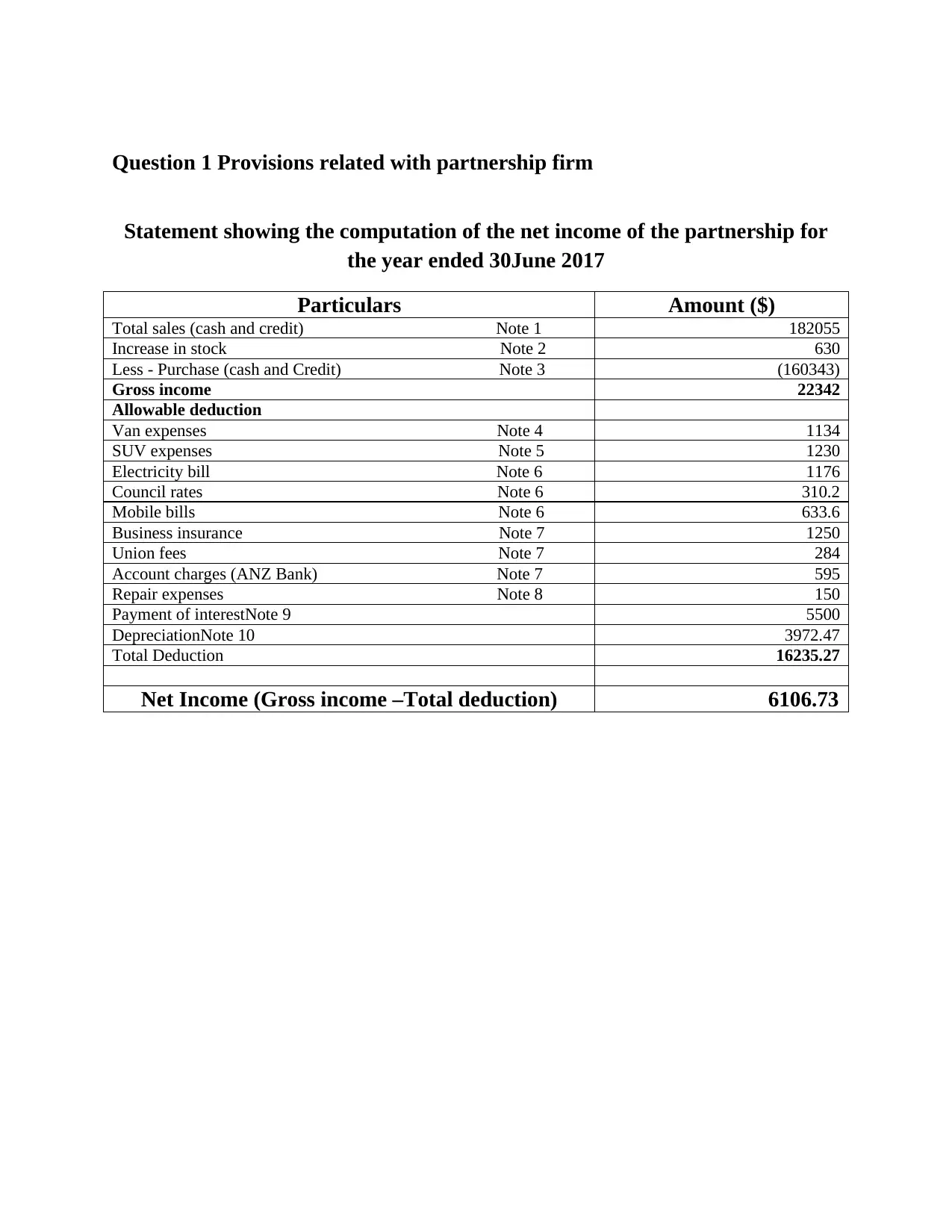

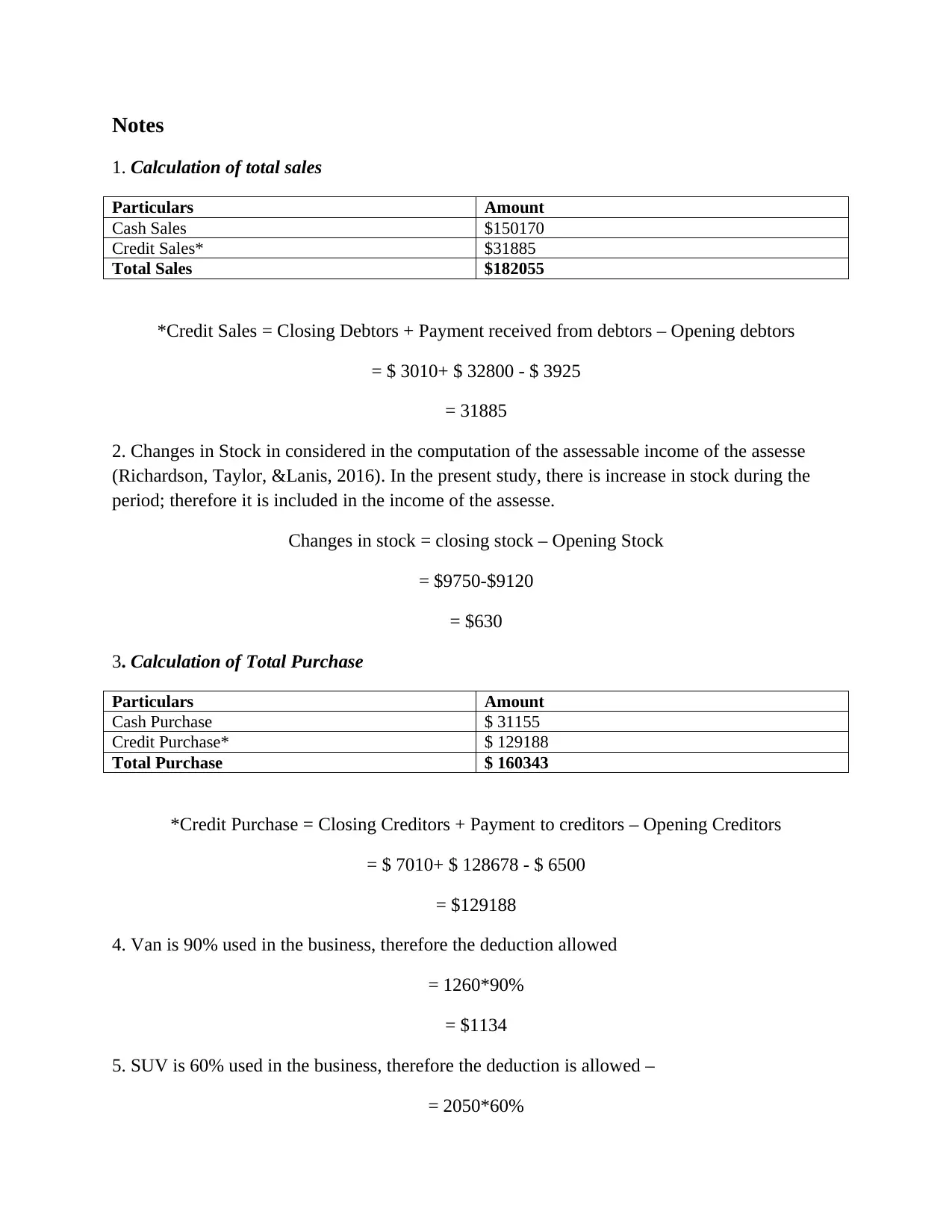

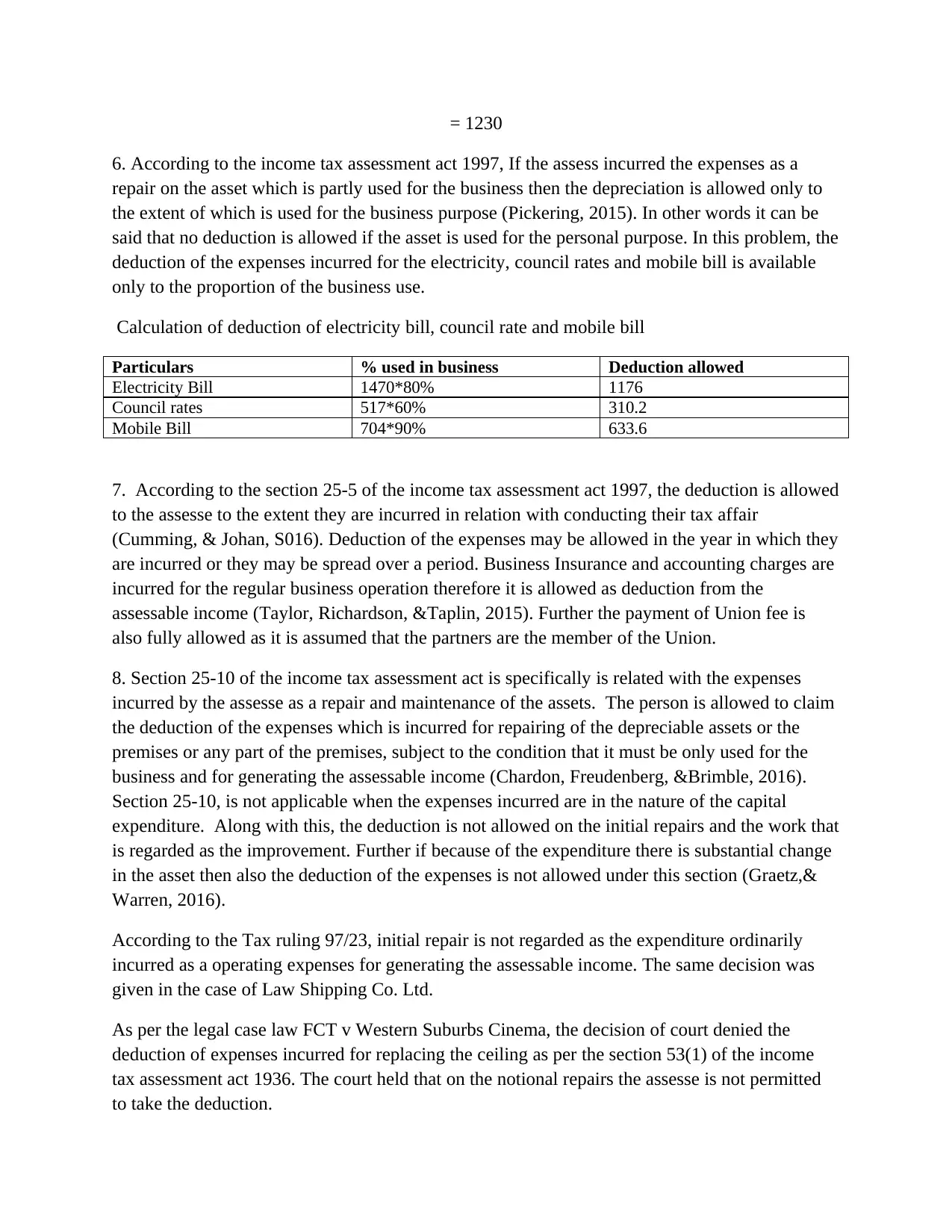

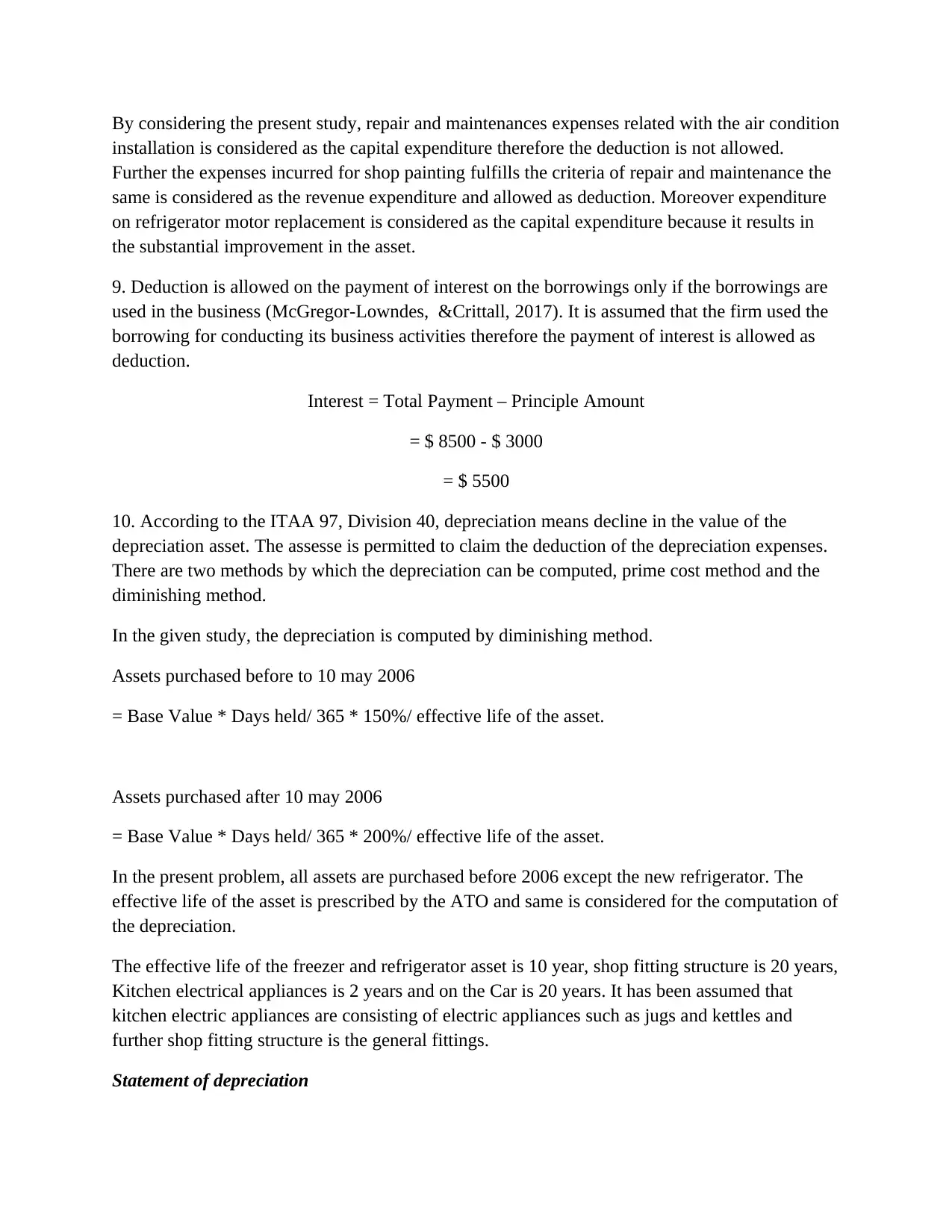

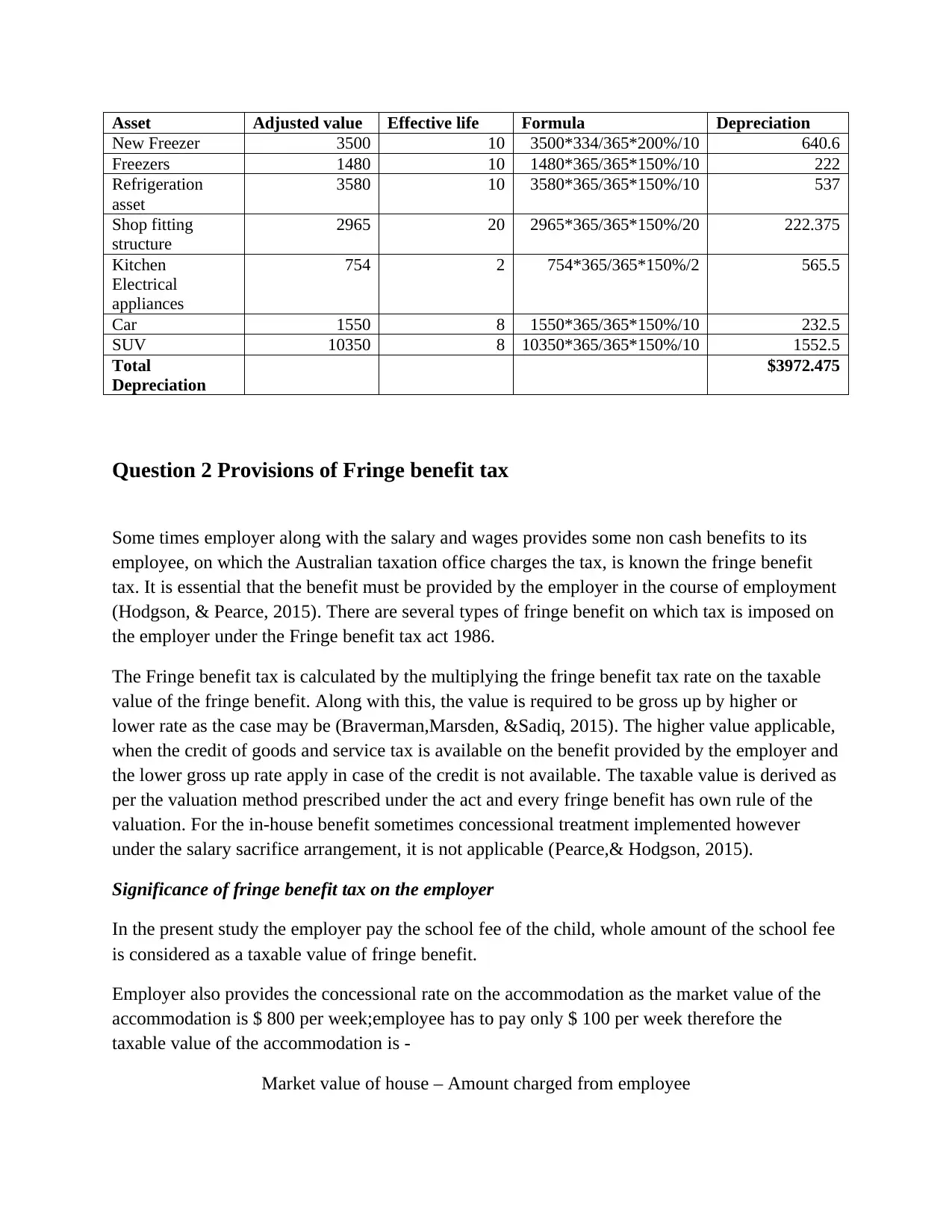

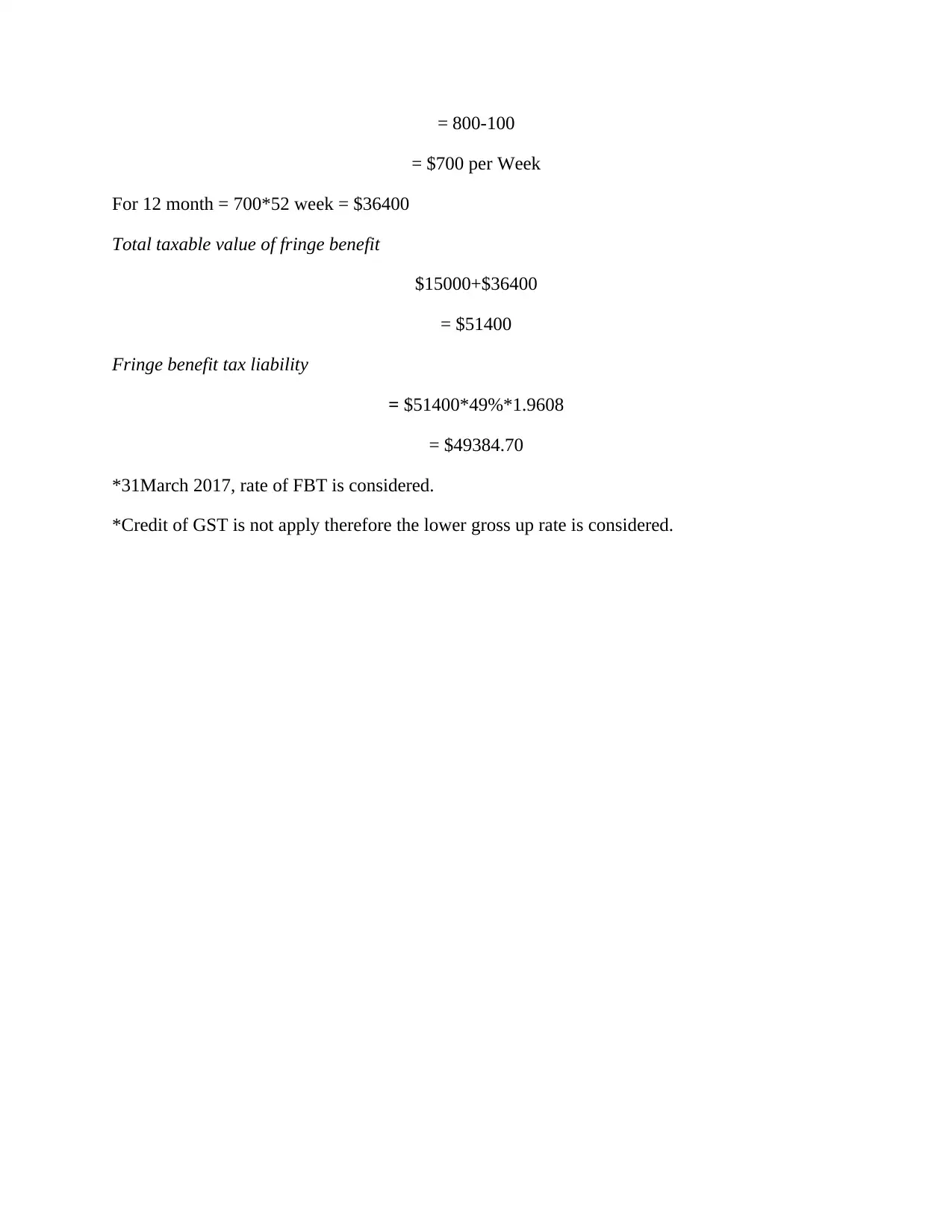

This assignment provides a detailed analysis of Australian taxation, focusing on partnership firms and fringe benefit tax (FBT). It includes a comprehensive computation of net income for a partnership, considering various income sources, allowable deductions, and depreciation methods as per the Income Tax Assessment Act 1997. The assignment also delves into the provisions of FBT, explaining its significance and calculation, including taxable values and gross-up rates. Specific scenarios, such as school fee payments and concessional accommodation, are analyzed to determine FBT liabilities. The document uses relevant sections of the ITAA and tax rulings to support its analysis, offering a practical understanding of Australian tax law. Desklib provides this and many other solved assignments for students.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.