Comprehensive Analysis of Australian Income Tax: Cases and Provisions

VerifiedAdded on 2023/03/31

|11

|2156

|406

Report

AI Summary

This report delves into the intricacies of Australian income tax, examining capital gains tax, income from personal exertion, and assessable income through a series of case studies. The first question focuses on capital gains tax (CGT) concerning the sale of various assets, including an antique impressionism painting, a historical sculpture, an antique jewelry piece, and a picture, applying the indexation method to determine taxable gains or losses. The second question explores Barbara's income under two scenarios, classifying payments for writing a book and selling manuscripts as income from personal exertion. The third question analyzes the tax implications of a loan arrangement between Patrick and his son, considering the assessable income arising from the loan repayment and interest earned. The report references relevant Australian Income Tax Act provisions and case laws to support its analysis.

TAXATION, THEORY AND

PRACTICES

PRACTICES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCITON......................................................................................................................................3

QUESTION 1.............................................................................................................................................3

1). Capital Gain Tax regarding antique impressionism painting.....................................................4

2). Capital Gain Tax regarding historical sculpture..........................................................................4

3). Capital Gain Tax regarding antique jewellery piece...................................................................4

4). Capital Gain Tax regarding picture...............................................................................................5

Question 2................................................................................................................................................6

1). Discuss Barbara ‘s income under the case scenario.................................................................6

2). Discuss Barbara ‘s income under the alternative scenario........................................................7

Question 3................................................................................................................................................8

Discuss the effect of these arrangement on the assessable income of Patrick...........................8

Conclusion...............................................................................................................................................9

REFERENCES........................................................................................................................................10

INTRODUCITON......................................................................................................................................3

QUESTION 1.............................................................................................................................................3

1). Capital Gain Tax regarding antique impressionism painting.....................................................4

2). Capital Gain Tax regarding historical sculpture..........................................................................4

3). Capital Gain Tax regarding antique jewellery piece...................................................................4

4). Capital Gain Tax regarding picture...............................................................................................5

Question 2................................................................................................................................................6

1). Discuss Barbara ‘s income under the case scenario.................................................................6

2). Discuss Barbara ‘s income under the alternative scenario........................................................7

Question 3................................................................................................................................................8

Discuss the effect of these arrangement on the assessable income of Patrick...........................8

Conclusion...............................................................................................................................................9

REFERENCES........................................................................................................................................10

INTRODUCITON

This report is based upon taxation, theory and practice of Australian income tax Act. It

highlights the Australian accounting systems, concept of income form personal

exertions and adjustment of income.Here, three questions are given which are related

to the income tax provisions of Australia. First question emphasises upon the capital

gain provisions, while second is based upon the income from personal exertion and

their question is based on the adjustment of assessable income.

QUESTION 1

Income tax Act of the country have the provisions related to capital gain tax. CGT is the

tax which arise after selling movable or immovable asset at a price more than the

purchase price (Smith, 2015). According to Australian Income Tax Act, this is rightly

said that the CGT is calculated via two methods which are namely: discounted method

and indexation method. However, Australian tax authorities does not prescribe the CGT

rate for capital gain (Income tax: residency status of individuals entering Australia,

2016). In the cited case, Helen dispose off its assets during current financial year. So,

any of the capital gain arise would be liable to pay tax in this year, or loss arise would

be set off for next assessment year. If the assesse retains the asset for at least 12

months or more then in that case, if assessee earn capital gain by dispose off that

asset, then he is liable to pay 23.5% tax (Minas, Lim and Evans, 2018). This rate is

applicable only when the discount method is applied and asset is purchased after 21st

September, 1999. Any of the asset which is purchased before aforementioned date,

then the indexation method is applied (Paolella and Durand, 2016). In the provided

case, all the assets were purchased before 21st September 1999 which simply means

that indexation method will be levied in order to calculate the capital gain tax (Consumer

price index, 2016). Indexation method is described as under:

Indexation method: This is the method under which techniques are used in order to link

prices and asset values due to inflation (Filatova, 2014 ). It is done by connecting

adjustments made to the value of a product, service or other metric, to a forecasted

This report is based upon taxation, theory and practice of Australian income tax Act. It

highlights the Australian accounting systems, concept of income form personal

exertions and adjustment of income.Here, three questions are given which are related

to the income tax provisions of Australia. First question emphasises upon the capital

gain provisions, while second is based upon the income from personal exertion and

their question is based on the adjustment of assessable income.

QUESTION 1

Income tax Act of the country have the provisions related to capital gain tax. CGT is the

tax which arise after selling movable or immovable asset at a price more than the

purchase price (Smith, 2015). According to Australian Income Tax Act, this is rightly

said that the CGT is calculated via two methods which are namely: discounted method

and indexation method. However, Australian tax authorities does not prescribe the CGT

rate for capital gain (Income tax: residency status of individuals entering Australia,

2016). In the cited case, Helen dispose off its assets during current financial year. So,

any of the capital gain arise would be liable to pay tax in this year, or loss arise would

be set off for next assessment year. If the assesse retains the asset for at least 12

months or more then in that case, if assessee earn capital gain by dispose off that

asset, then he is liable to pay 23.5% tax (Minas, Lim and Evans, 2018). This rate is

applicable only when the discount method is applied and asset is purchased after 21st

September, 1999. Any of the asset which is purchased before aforementioned date,

then the indexation method is applied (Paolella and Durand, 2016). In the provided

case, all the assets were purchased before 21st September 1999 which simply means

that indexation method will be levied in order to calculate the capital gain tax (Consumer

price index, 2016). Indexation method is described as under:

Indexation method: This is the method under which techniques are used in order to link

prices and asset values due to inflation (Filatova, 2014 ). It is done by connecting

adjustments made to the value of a product, service or other metric, to a forecasted

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

index. This needs the recognition of a price index and whether a connection of value to

price index, would complete company goals (ATO Tax Calculator, 2016). This is often

used with wages at a high inflation environment.

The details of each transaction is mentioned hereunder:

1). Capital Gain Tax regarding antique impressionism painting

Helen purchased the asset before 21st September, 1985 that simply comes under the

Australian Income tax exemption list. She brought such asset on February, 1985 when

Australian income tax was not incorporated. Hence, on this asset no tax will be made

due to the exemption list.

2). Capital Gain Tax regarding historical sculpture

The historical sculpture was purchased before 21st September, 1999. Hence, the capital

gain is calculated by using indexation method. Capital gain/loss is calculated as under:

Particulars Amount $

Selling Price 6000

Purchased price 10120

Capital loss/gain (4120)

Working Note:

By using indexation method, brought up value is recognized so that the capital gain/

loss is easily identified. Buying cost is identified:

Cost of buying assets: 6/61.2= 1.838*5500=10120

The asset were brought at $5500 on 1993 which was raised to $10120 by using

indexation method. Hence, this selling price is less than the price of purchase assets

after indexation thus the loss of the $4120 is occurred.

3). Capital Gain Tax regarding antique jewellery piece

Helen brought Jewellery at $14000 during October, 1987. Hence indexation method is

applied due to the asset purchased before 21st September, 1999. The calculation is

mentioned as under:

price index, would complete company goals (ATO Tax Calculator, 2016). This is often

used with wages at a high inflation environment.

The details of each transaction is mentioned hereunder:

1). Capital Gain Tax regarding antique impressionism painting

Helen purchased the asset before 21st September, 1985 that simply comes under the

Australian Income tax exemption list. She brought such asset on February, 1985 when

Australian income tax was not incorporated. Hence, on this asset no tax will be made

due to the exemption list.

2). Capital Gain Tax regarding historical sculpture

The historical sculpture was purchased before 21st September, 1999. Hence, the capital

gain is calculated by using indexation method. Capital gain/loss is calculated as under:

Particulars Amount $

Selling Price 6000

Purchased price 10120

Capital loss/gain (4120)

Working Note:

By using indexation method, brought up value is recognized so that the capital gain/

loss is easily identified. Buying cost is identified:

Cost of buying assets: 6/61.2= 1.838*5500=10120

The asset were brought at $5500 on 1993 which was raised to $10120 by using

indexation method. Hence, this selling price is less than the price of purchase assets

after indexation thus the loss of the $4120 is occurred.

3). Capital Gain Tax regarding antique jewellery piece

Helen brought Jewellery at $14000 during October, 1987. Hence indexation method is

applied due to the asset purchased before 21st September, 1999. The calculation is

mentioned as under:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

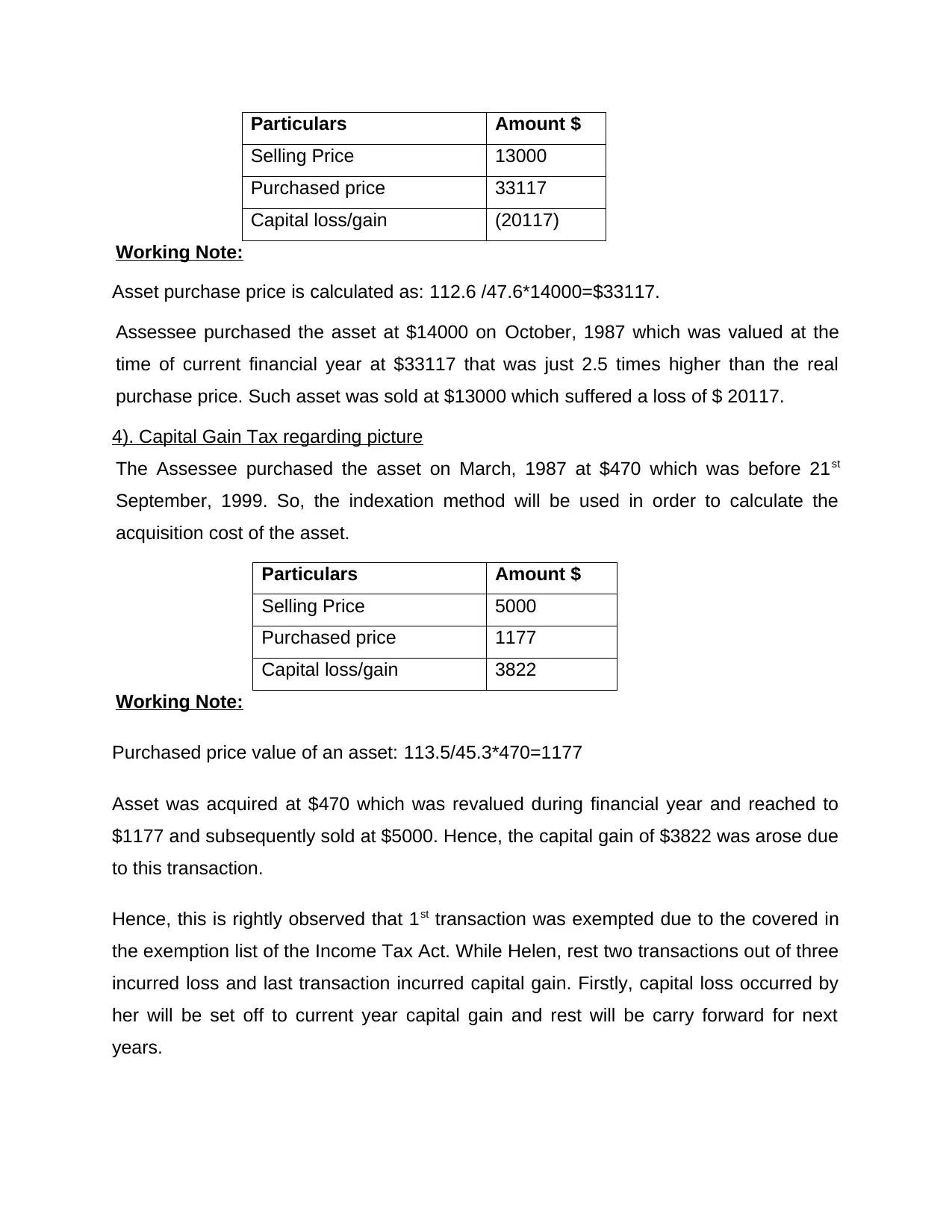

Particulars Amount $

Selling Price 13000

Purchased price 33117

Capital loss/gain (20117)

Working Note:

Asset purchase price is calculated as: 112.6 /47.6*14000=$33117.

Assessee purchased the asset at $14000 on October, 1987 which was valued at the

time of current financial year at $33117 that was just 2.5 times higher than the real

purchase price. Such asset was sold at $13000 which suffered a loss of $ 20117.

4). Capital Gain Tax regarding picture

The Assessee purchased the asset on March, 1987 at $470 which was before 21st

September, 1999. So, the indexation method will be used in order to calculate the

acquisition cost of the asset.

Particulars Amount $

Selling Price 5000

Purchased price 1177

Capital loss/gain 3822

Working Note:

Purchased price value of an asset: 113.5/45.3*470=1177

Asset was acquired at $470 which was revalued during financial year and reached to

$1177 and subsequently sold at $5000. Hence, the capital gain of $3822 was arose due

to this transaction.

Hence, this is rightly observed that 1st transaction was exempted due to the covered in

the exemption list of the Income Tax Act. While Helen, rest two transactions out of three

incurred loss and last transaction incurred capital gain. Firstly, capital loss occurred by

her will be set off to current year capital gain and rest will be carry forward for next

years.

Selling Price 13000

Purchased price 33117

Capital loss/gain (20117)

Working Note:

Asset purchase price is calculated as: 112.6 /47.6*14000=$33117.

Assessee purchased the asset at $14000 on October, 1987 which was valued at the

time of current financial year at $33117 that was just 2.5 times higher than the real

purchase price. Such asset was sold at $13000 which suffered a loss of $ 20117.

4). Capital Gain Tax regarding picture

The Assessee purchased the asset on March, 1987 at $470 which was before 21st

September, 1999. So, the indexation method will be used in order to calculate the

acquisition cost of the asset.

Particulars Amount $

Selling Price 5000

Purchased price 1177

Capital loss/gain 3822

Working Note:

Purchased price value of an asset: 113.5/45.3*470=1177

Asset was acquired at $470 which was revalued during financial year and reached to

$1177 and subsequently sold at $5000. Hence, the capital gain of $3822 was arose due

to this transaction.

Hence, this is rightly observed that 1st transaction was exempted due to the covered in

the exemption list of the Income Tax Act. While Helen, rest two transactions out of three

incurred loss and last transaction incurred capital gain. Firstly, capital loss occurred by

her will be set off to current year capital gain and rest will be carry forward for next

years.

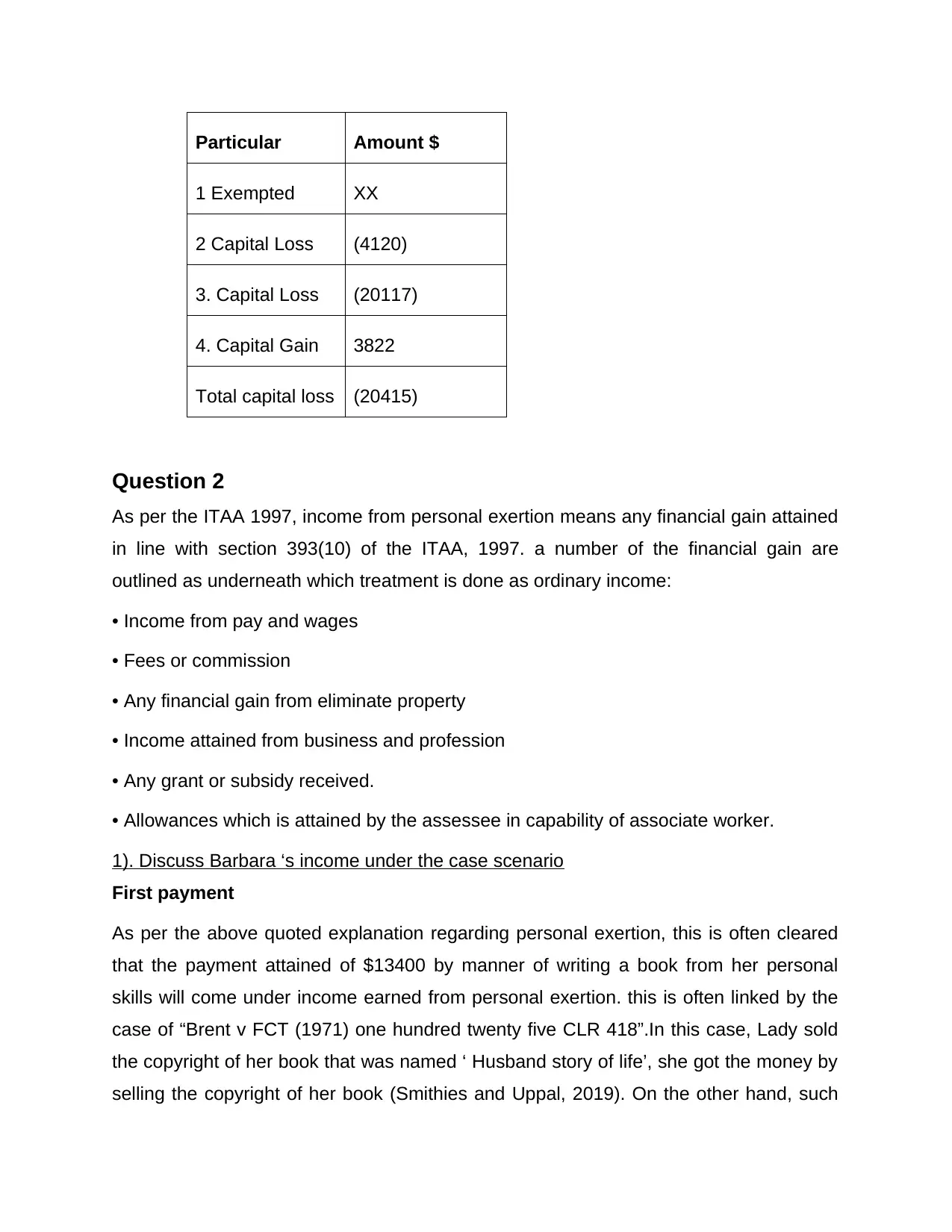

Particular Amount $

1 Exempted XX

2 Capital Loss (4120)

3. Capital Loss (20117)

4. Capital Gain 3822

Total capital loss (20415)

Question 2

As per the ITAA 1997, income from personal exertion means any financial gain attained

in line with section 393(10) of the ITAA, 1997. a number of the financial gain are

outlined as underneath which treatment is done as ordinary income:

• Income from pay and wages

• Fees or commission

• Any financial gain from eliminate property

• Income attained from business and profession

• Any grant or subsidy received.

• Allowances which is attained by the assessee in capability of associate worker.

1). Discuss Barbara ‘s income under the case scenario

First payment

As per the above quoted explanation regarding personal exertion, this is often cleared

that the payment attained of $13400 by manner of writing a book from her personal

skills will come under income earned from personal exertion. this is often linked by the

case of “Brent v FCT (1971) one hundred twenty five CLR 418”.In this case, Lady sold

the copyright of her book that was named ‘ Husband story of life’, she got the money by

selling the copyright of her book (Smithies and Uppal, 2019). On the other hand, such

1 Exempted XX

2 Capital Loss (4120)

3. Capital Loss (20117)

4. Capital Gain 3822

Total capital loss (20415)

Question 2

As per the ITAA 1997, income from personal exertion means any financial gain attained

in line with section 393(10) of the ITAA, 1997. a number of the financial gain are

outlined as underneath which treatment is done as ordinary income:

• Income from pay and wages

• Fees or commission

• Any financial gain from eliminate property

• Income attained from business and profession

• Any grant or subsidy received.

• Allowances which is attained by the assessee in capability of associate worker.

1). Discuss Barbara ‘s income under the case scenario

First payment

As per the above quoted explanation regarding personal exertion, this is often cleared

that the payment attained of $13400 by manner of writing a book from her personal

skills will come under income earned from personal exertion. this is often linked by the

case of “Brent v FCT (1971) one hundred twenty five CLR 418”.In this case, Lady sold

the copyright of her book that was named ‘ Husband story of life’, she got the money by

selling the copyright of her book (Smithies and Uppal, 2019). On the other hand, such

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

income earned by the assesse will be covered under the income earned from personal

exertion and this would not be counted as the ordinary income. By applying identical

case law, income earned by the Barbara would be considered as the income earned

from personal exertion.

Second Payment

$4,350 earned by Barbara for the selling of “Economics Principles” book manuscript to

the Eco Books Ltd.’s library also considered to be a part of her income from personal

exertion. This statement had been cleared within the above-mentioned case, within

which a woman sold the story of her husband life to the newspaper agency (Woellner,

and et al., 2014).

Third Payment

$3,200 received by her on gathering many interview manuscripts whereas writing the

book on economics is additionally a part of her personal exertion income (Weber, 2014).

Such income is gained by the Barbara on gathering helpful manuscripts that facilitate

her in writing a book. Hence, it is considered as the income earned from personal

exertion.

2). Discuss Barbara ‘s income under the alternative scenario

Where Barbara 1st wrote the book on Economic Principles and sold it later to the Eco

Books Ltd.; then an equivalent treatment that was explained on top, will implement

during this case as income would here also counted as the personal exertion which was

earned by her personal labour or efforts (Faccio and Xu, 2015). It doesn't matter

whether or not Barbara received financial gain before or when sign language a contract.

She received financial gain for her own efforts whether or not these efforts square

measure done before/ after signing a contract.

Question 3.

Discuss the effect of these arrangement on the assessable income of Patrick

According to the Australian Taxation Authority (ATO) “If any loan or money is provided

by the parent to his son/ daughter and reciprocally if such son/ daughter pays back to

his or her parent then the financial gain transferred by the son or girl to his or her parent

exertion and this would not be counted as the ordinary income. By applying identical

case law, income earned by the Barbara would be considered as the income earned

from personal exertion.

Second Payment

$4,350 earned by Barbara for the selling of “Economics Principles” book manuscript to

the Eco Books Ltd.’s library also considered to be a part of her income from personal

exertion. This statement had been cleared within the above-mentioned case, within

which a woman sold the story of her husband life to the newspaper agency (Woellner,

and et al., 2014).

Third Payment

$3,200 received by her on gathering many interview manuscripts whereas writing the

book on economics is additionally a part of her personal exertion income (Weber, 2014).

Such income is gained by the Barbara on gathering helpful manuscripts that facilitate

her in writing a book. Hence, it is considered as the income earned from personal

exertion.

2). Discuss Barbara ‘s income under the alternative scenario

Where Barbara 1st wrote the book on Economic Principles and sold it later to the Eco

Books Ltd.; then an equivalent treatment that was explained on top, will implement

during this case as income would here also counted as the personal exertion which was

earned by her personal labour or efforts (Faccio and Xu, 2015). It doesn't matter

whether or not Barbara received financial gain before or when sign language a contract.

She received financial gain for her own efforts whether or not these efforts square

measure done before/ after signing a contract.

Question 3.

Discuss the effect of these arrangement on the assessable income of Patrick

According to the Australian Taxation Authority (ATO) “If any loan or money is provided

by the parent to his son/ daughter and reciprocally if such son/ daughter pays back to

his or her parent then the financial gain transferred by the son or girl to his or her parent

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

are a taxable income which would be taxable in parent hand (Evans, Minas and Lim,

2015).

The result on the assessable financial gain of the Patrick relating to $52,000 that was

borrowed by David for the aim to begin a brand new business and also the excess

payments attained by Patrick from his son as an interest of five years i.e. $6,000

($58,000 -$52,000) will additionally attract tax. Henceforth, the loan was clearly not

considered as gift because it was to be repaid (Edmonds, 2015).

On the other hand, $52,000 wouldn't only a part of the assessable income of the Patrick

but also additional interest earned by him will be counted as the income and will be

considered in Patrick account.

Re-examining matters under which the Patrick provided loan to his son while not

creating a proper contract or not demanded any security and with a verbal preceding of

the interest financial gain, then the capital compensation of $52,000 wouldn't be

considered within the hands of David but also payable under Patrick hand. It additionally

not attracts any tax liability.

But the loan was repaid by his son after two years along with interest of $2,400(S6,

000/5*2) received by him, it will considered as taxable income which is taxable within

the hands of Patrick. The interest attained by the Patrick would be assessable for tax

after two years once it had been truly attained by the Patrick

Mode of payment, during this case, was cheque that doesn't have an effect on the

access liability of financial gain, what matters is that the intention of the parties that was

thought by the income tax authority (Auerbach and Hassett, 2015). In that case, the gift

tax liability might additionally have an effect on the payment of pension that was

received by the parent may additionally increase the assessable financial gain of patron

saint. The Patrick may additionally avail the tax limit of $10,000 annually, or $30,000 in

5 years whichever is a smaller amount. Any payment or gift created on top of this

prescribed limit then it'd be an area of assessable financial gain of the parent within the

assessment year.

2015).

The result on the assessable financial gain of the Patrick relating to $52,000 that was

borrowed by David for the aim to begin a brand new business and also the excess

payments attained by Patrick from his son as an interest of five years i.e. $6,000

($58,000 -$52,000) will additionally attract tax. Henceforth, the loan was clearly not

considered as gift because it was to be repaid (Edmonds, 2015).

On the other hand, $52,000 wouldn't only a part of the assessable income of the Patrick

but also additional interest earned by him will be counted as the income and will be

considered in Patrick account.

Re-examining matters under which the Patrick provided loan to his son while not

creating a proper contract or not demanded any security and with a verbal preceding of

the interest financial gain, then the capital compensation of $52,000 wouldn't be

considered within the hands of David but also payable under Patrick hand. It additionally

not attracts any tax liability.

But the loan was repaid by his son after two years along with interest of $2,400(S6,

000/5*2) received by him, it will considered as taxable income which is taxable within

the hands of Patrick. The interest attained by the Patrick would be assessable for tax

after two years once it had been truly attained by the Patrick

Mode of payment, during this case, was cheque that doesn't have an effect on the

access liability of financial gain, what matters is that the intention of the parties that was

thought by the income tax authority (Auerbach and Hassett, 2015). In that case, the gift

tax liability might additionally have an effect on the payment of pension that was

received by the parent may additionally increase the assessable financial gain of patron

saint. The Patrick may additionally avail the tax limit of $10,000 annually, or $30,000 in

5 years whichever is a smaller amount. Any payment or gift created on top of this

prescribed limit then it'd be an area of assessable financial gain of the parent within the

assessment year.

Conclusion

From the above mentioned report, this is rightly observed that the whole project

consists of income tax provisions which were along with the income from person

exertion and other income. All the cases in the assignment covers the income tax

provisions of Australia. In the first question, Helen capital gain tax was calculated on her

each transaction. While in second question, income from person exertion is calculated.

On the other hand, third question covers adjustment related to assessable income is

elaborated under this.

From the above mentioned report, this is rightly observed that the whole project

consists of income tax provisions which were along with the income from person

exertion and other income. All the cases in the assignment covers the income tax

provisions of Australia. In the first question, Helen capital gain tax was calculated on her

each transaction. While in second question, income from person exertion is calculated.

On the other hand, third question covers adjustment related to assessable income is

elaborated under this.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Auerbach, A.J. and Hassett, K., 2015. Capital taxation in the twenty-first

century. American Economic Review, 105(5), pp.38-42. Australia, 53(8), p.420.

Edmonds, R., 2015. Structural tax reform: What should be brought to the table. Austl.

Tax F., 30, p.393.

Evans, C., Minas, J. and Lim, Y., 2015. Taxing personal capital gains in Australia: an

alternative way forward. Austl. Tax F., 30, p.735

Faccio, M. and Xu, J., 2015. Taxes and capital structure. Journal of Financial and

Quantitative Analysis, 50(3), pp.277-300.

Filatova, T., 2014. Market-based instruments for flood risk management: a review of

theory, practice and perspectives for climate adaptation policy. Environmental science

& policy, 37, pp.227-242.

Minas, J., Lim, Y. and Evans, C., 2018, August. The impact of tax rate changes on

capital gains realisations: evidence from Australia. In Australian Tax Forum (Vol. 33,

No. 4).

Paolella, L. and Durand, R., 2016. Category spanning, evaluation, and performance:

Revised theory and test on the corporate law market. Academy of Management

Journal, 59(1), pp.330-351.

Smith, J.P., 2015. Australian state income taxation: A historical perspective. Austl. Tax

F., 30,p.679.

Smithies, J. and Uppal, S., 2019. Australia. In Cultural Governance in a Global

Context (pp.127-158).

Weber, R., 2014. Tax increment financing in theory and practice. In Financing economic

development in the 21st century (pp. 297-315). Routledge.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2014. Australian

Taxation Law 2014 (pp. 1-81).

Online

Auerbach, A.J. and Hassett, K., 2015. Capital taxation in the twenty-first

century. American Economic Review, 105(5), pp.38-42. Australia, 53(8), p.420.

Edmonds, R., 2015. Structural tax reform: What should be brought to the table. Austl.

Tax F., 30, p.393.

Evans, C., Minas, J. and Lim, Y., 2015. Taxing personal capital gains in Australia: an

alternative way forward. Austl. Tax F., 30, p.735

Faccio, M. and Xu, J., 2015. Taxes and capital structure. Journal of Financial and

Quantitative Analysis, 50(3), pp.277-300.

Filatova, T., 2014. Market-based instruments for flood risk management: a review of

theory, practice and perspectives for climate adaptation policy. Environmental science

& policy, 37, pp.227-242.

Minas, J., Lim, Y. and Evans, C., 2018, August. The impact of tax rate changes on

capital gains realisations: evidence from Australia. In Australian Tax Forum (Vol. 33,

No. 4).

Paolella, L. and Durand, R., 2016. Category spanning, evaluation, and performance:

Revised theory and test on the corporate law market. Academy of Management

Journal, 59(1), pp.330-351.

Smith, J.P., 2015. Australian state income taxation: A historical perspective. Austl. Tax

F., 30,p.679.

Smithies, J. and Uppal, S., 2019. Australia. In Cultural Governance in a Global

Context (pp.127-158).

Weber, R., 2014. Tax increment financing in theory and practice. In Financing economic

development in the 21st century (pp. 297-315). Routledge.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2014. Australian

Taxation Law 2014 (pp. 1-81).

Online

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Income tax: residency status of individuals entering Australia, 2016. [Online] Available

at: .

ATO Tax Calculator, 2016. [Online]. Available at: http://atotaxcalculator.com.au/.

Consumer price index, 2016 [Online]. Available at:

<https://www.ato.gov.au/Rates/Consumer-price-index/.

at: .

ATO Tax Calculator, 2016. [Online]. Available at: http://atotaxcalculator.com.au/.

Consumer price index, 2016 [Online]. Available at:

<https://www.ato.gov.au/Rates/Consumer-price-index/.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.