Taxation Report: Capital Gains, Fringe Benefits, and Tax Law

VerifiedAdded on 2020/07/22

|12

|2898

|34

Report

AI Summary

This report delves into the intricacies of Australian taxation, employing the IRAC (Issue, Rule, Application, Conclusion) approach to analyze various case studies. It begins by examining capital gains and losses for an individual, Eric, detailing the calculation of net capital gain from the sale of assets. The report then investigates fringe benefits, calculating the taxable value and tax payable for Brian, a bank executive, based on a provided loan. Furthermore, it addresses loss allocation for tax purposes in a scenario involving Jack and Jill, exploring their property investment and the implications of their agreement. The report also explains the principles established in IRCA v Duke of Westminster, including the concepts of DOTAS, TAARS, and GAAR. Finally, it presents a case study related to Bill and a parcel of land, analyzing the tax implications of timber harvesting investments. Through these case studies, the report provides a comprehensive understanding of Australian taxation principles and their practical application, offering valuable insights into tax planning and compliance.

TAXATION

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

1) CAPITAL NET GAIN/LOSS FOR ERIC...................................................................................1

2) TAXABLE VALUE OF FRINGE BENEFIT FOR 2016/17 FBT YEAR (CASE STUDY

RELATED TO BRIAN)..................................................................................................................2

3) LOSS ALLOCATED FOR TAX PURPOSES FOR JACK........................................................3

4) PRINCIPLES ESTABLISHED IN IRCA V DUKE OF WESTMINSTER [1936] AC 1..........4

5) CASE STUDY RELATED TO BILL REGARDING PARCEL................................................6

CONCLUSION................................................................................................................................6

REFERENCE...................................................................................................................................8

INTRODUCTION...........................................................................................................................1

1) CAPITAL NET GAIN/LOSS FOR ERIC...................................................................................1

2) TAXABLE VALUE OF FRINGE BENEFIT FOR 2016/17 FBT YEAR (CASE STUDY

RELATED TO BRIAN)..................................................................................................................2

3) LOSS ALLOCATED FOR TAX PURPOSES FOR JACK........................................................3

4) PRINCIPLES ESTABLISHED IN IRCA V DUKE OF WESTMINSTER [1936] AC 1..........4

5) CASE STUDY RELATED TO BILL REGARDING PARCEL................................................6

CONCLUSION................................................................................................................................6

REFERENCE...................................................................................................................................8

INDEX OF TABLES

Table 1: Capital gain for Eric on selling assets for Eric..................................................................1

Table 2: Fringe benefit for Brian.....................................................................................................3

Table 1: Capital gain for Eric on selling assets for Eric..................................................................1

Table 2: Fringe benefit for Brian.....................................................................................................3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ILLUSTRATION INDEX

Illustration 1: Fringe benefit tax rates in Australia..........................................................................2

Illustration 1: Fringe benefit tax rates in Australia..........................................................................2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

Government of Australia raise revenue through tax from any individual according to set

planning policies. It affects market and economic position of the country as implementing IRAC

approach and making decisions regarding further business activities. The present report is based

on understanding IRAC approach for taxation in Australia stands for issue, rule, application and

conclusion. In this regard, monetary position of businesses and individuals through different

cases can be described. However, good understanding with capital gain and fringe benefit

concepts are to increased in the case studies of ERIC and Brain. Similarly, taxable amount on

parcel of land in case scenario of Bill and tax purposes for Jack will be introduced affect their

financial positions and further decisions relating to business operations. Thus, students are able

to acquire knowledge regarding taxation in Australia with the help of case scenarios using IRAC

approach effectively through this assignment.

1) CAPITAL NET GAIN/LOSS FOR ERIC

Capital gain or loss for any organisation is evaluated through considering result on selling

assets. It is useful to analyse company's financial position on which further decisions are made

on business operations. However, investment income in the form of cash flow is recognised by

purchasing and selling both assets as tangible and intangible (Kim and et.al., 2013). In the case

scenario, Eric has sold company's antique vase, chair, painting, sound system and shares by

which actual monetary position of the entity can be identified. Therefore, net capital gain on

selling these items by comparing with its investment amount is to be evaluated as below:

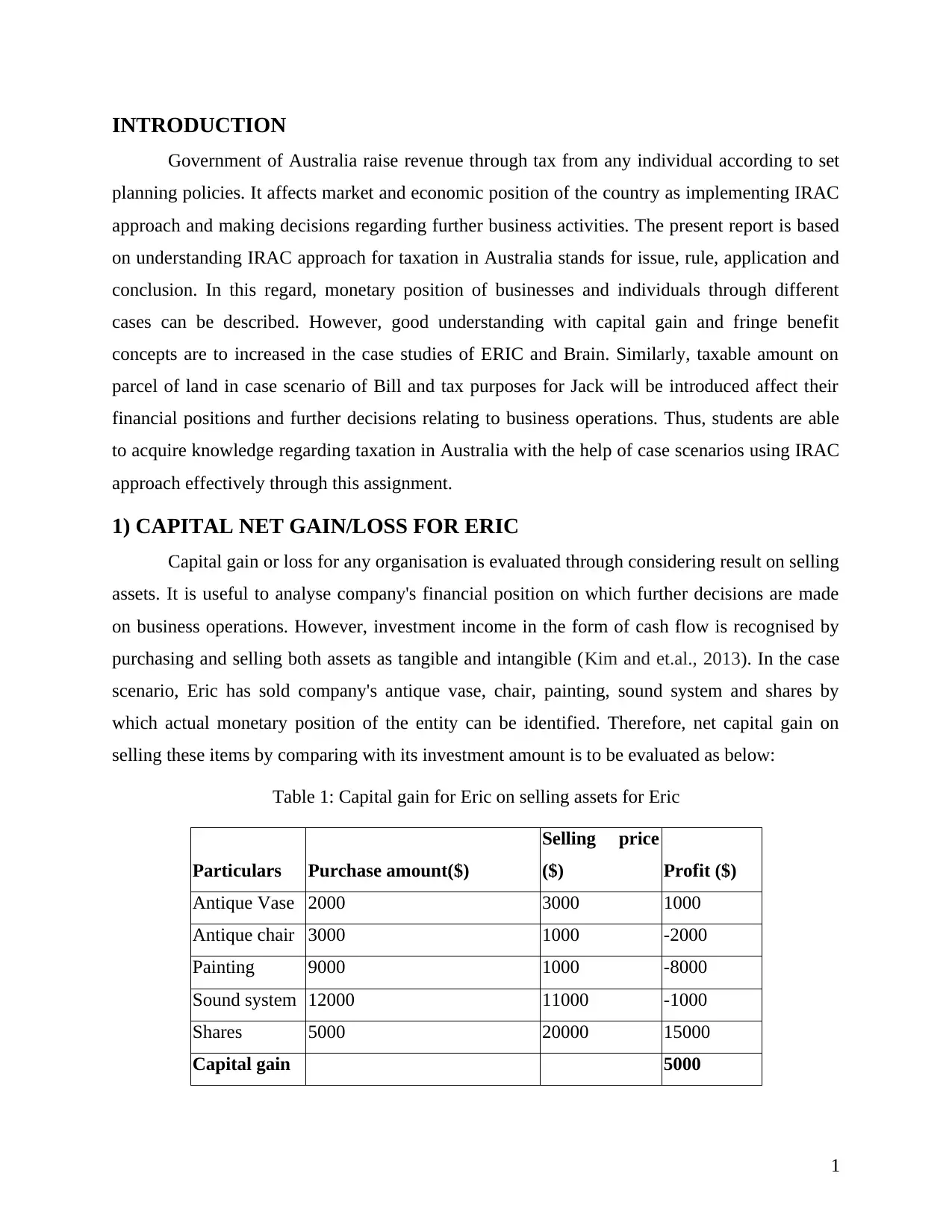

Table 1: Capital gain for Eric on selling assets for Eric

Particulars Purchase amount($)

Selling price

($) Profit ($)

Antique Vase 2000 3000 1000

Antique chair 3000 1000 -2000

Painting 9000 1000 -8000

Sound system 12000 11000 -1000

Shares 5000 20000 15000

Capital gain 5000

1

Government of Australia raise revenue through tax from any individual according to set

planning policies. It affects market and economic position of the country as implementing IRAC

approach and making decisions regarding further business activities. The present report is based

on understanding IRAC approach for taxation in Australia stands for issue, rule, application and

conclusion. In this regard, monetary position of businesses and individuals through different

cases can be described. However, good understanding with capital gain and fringe benefit

concepts are to increased in the case studies of ERIC and Brain. Similarly, taxable amount on

parcel of land in case scenario of Bill and tax purposes for Jack will be introduced affect their

financial positions and further decisions relating to business operations. Thus, students are able

to acquire knowledge regarding taxation in Australia with the help of case scenarios using IRAC

approach effectively through this assignment.

1) CAPITAL NET GAIN/LOSS FOR ERIC

Capital gain or loss for any organisation is evaluated through considering result on selling

assets. It is useful to analyse company's financial position on which further decisions are made

on business operations. However, investment income in the form of cash flow is recognised by

purchasing and selling both assets as tangible and intangible (Kim and et.al., 2013). In the case

scenario, Eric has sold company's antique vase, chair, painting, sound system and shares by

which actual monetary position of the entity can be identified. Therefore, net capital gain on

selling these items by comparing with its investment amount is to be evaluated as below:

Table 1: Capital gain for Eric on selling assets for Eric

Particulars Purchase amount($)

Selling price

($) Profit ($)

Antique Vase 2000 3000 1000

Antique chair 3000 1000 -2000

Painting 9000 1000 -8000

Sound system 12000 11000 -1000

Shares 5000 20000 15000

Capital gain 5000

1

Interpretation: It is identified that Eric had invested for purchasing antique vase, antique

chair, painting, sound system and shares as $2000, $3000, $9000, $12000 and $5000

respectively. On which selling price on each item is determined as $3000, $1000, $1000, $11000

and $12000 sequentially. Therefore, he gains total $16000 profit on selling antique vase and

shares as well $11000 of loss on selling other mentioned assets. As per this calculation, for

evaluating net capital gain, sum total of overall results is done by which actual financial position

and profitability can be recognised (Bird, 2015). Thus, net capital gain on this business operation

is calculated as $5000 which is quite effective and forecasts for gaining profit in the future time

effectively.

2) TAXABLE VALUE OF FRINGE BENEFIT FOR 2016/17 FBT YEAR

(CASE STUDY RELATED TO BRIAN)

Fringe benefit is considered as extra tax benefits to an individual provided by employer to

employee or associate of any company in Australia. It includes several types of benefits such as

salary, wages and home allowances, employee relocation expenditures, minor benefits etc. In the

given case study, Brian who is a bank executive and as a part of his remuneration package, his

employer provided him loan of $1 m at the rate of 1% per annum for 3 years (Griffith, Hines and

Sørensen, 2013).

2

chair, painting, sound system and shares as $2000, $3000, $9000, $12000 and $5000

respectively. On which selling price on each item is determined as $3000, $1000, $1000, $11000

and $12000 sequentially. Therefore, he gains total $16000 profit on selling antique vase and

shares as well $11000 of loss on selling other mentioned assets. As per this calculation, for

evaluating net capital gain, sum total of overall results is done by which actual financial position

and profitability can be recognised (Bird, 2015). Thus, net capital gain on this business operation

is calculated as $5000 which is quite effective and forecasts for gaining profit in the future time

effectively.

2) TAXABLE VALUE OF FRINGE BENEFIT FOR 2016/17 FBT YEAR

(CASE STUDY RELATED TO BRIAN)

Fringe benefit is considered as extra tax benefits to an individual provided by employer to

employee or associate of any company in Australia. It includes several types of benefits such as

salary, wages and home allowances, employee relocation expenditures, minor benefits etc. In the

given case study, Brian who is a bank executive and as a part of his remuneration package, his

employer provided him loan of $1 m at the rate of 1% per annum for 3 years (Griffith, Hines and

Sørensen, 2013).

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Further, he used its 40% for borrowing funds for the purpose of income producing.

However, fringe benefit in this case for Brian for 2016/17 can be calculated as below:

Table 2: Fringe benefit for Brian

Particulars Figures

Fringe interest rate 5.65% - 1% = 4.65%

Fringe benefit (in $) 400000 * 4.65% = 18600

FBT tax rates 49%

Taxable amount of fringe benefit 18600 / (1- 49%) = 36470.59

3

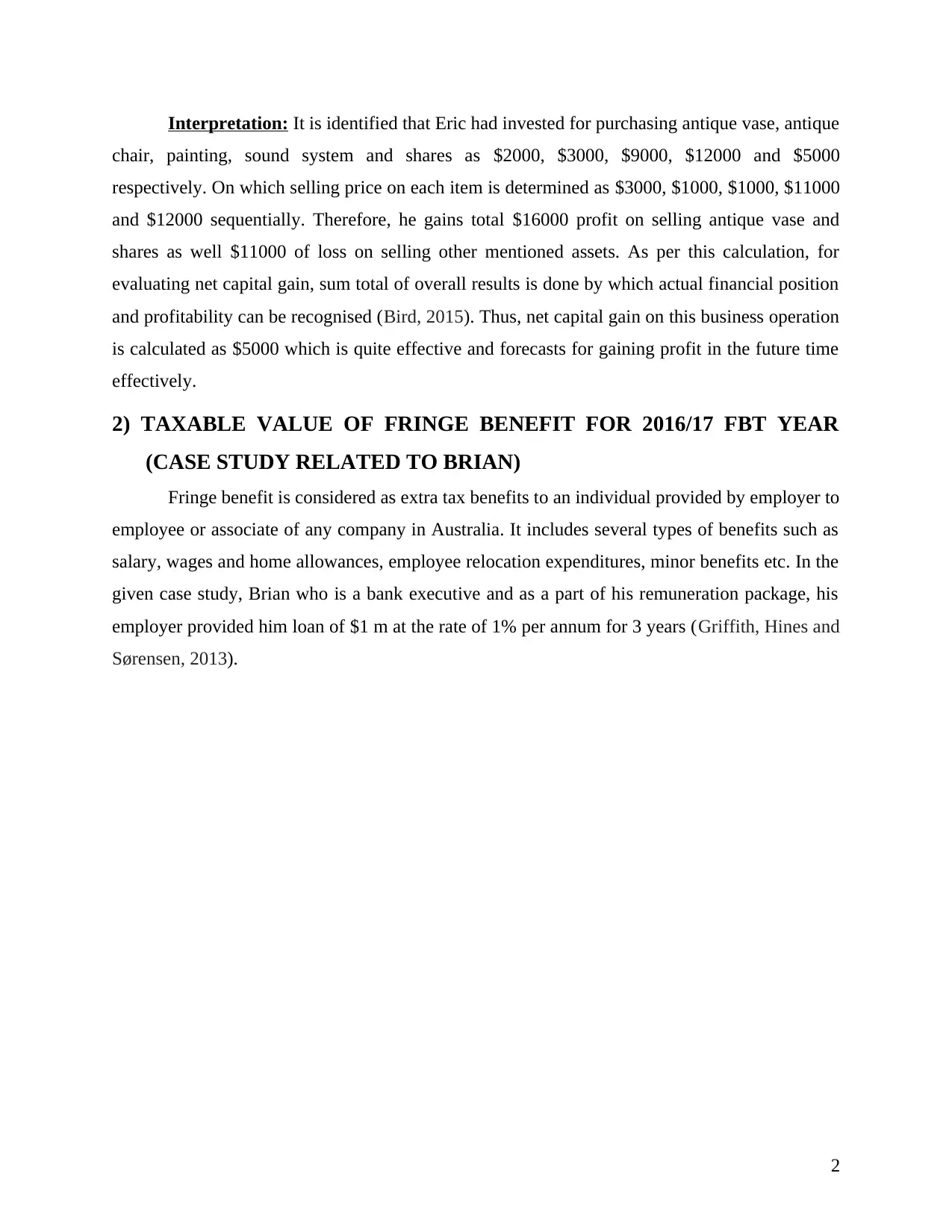

Illustration 1: Fringe benefit tax rates in Australia

(Source: Fringe benefit tax rates in Australia, 2017).

However, fringe benefit in this case for Brian for 2016/17 can be calculated as below:

Table 2: Fringe benefit for Brian

Particulars Figures

Fringe interest rate 5.65% - 1% = 4.65%

Fringe benefit (in $) 400000 * 4.65% = 18600

FBT tax rates 49%

Taxable amount of fringe benefit 18600 / (1- 49%) = 36470.59

3

Illustration 1: Fringe benefit tax rates in Australia

(Source: Fringe benefit tax rates in Australia, 2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Amount of tax payable (Fringe benefits

taxable amount * rate of tax)

36470.59 * 49% = 17870.59

Interpretation: It is recognised that fringe interest rate in Australia for 2017 is 5.65%

and employer provided loan of 100000 at the rate of 1%. Therefore, fringe interest benefit on

400000 at the interest rate of 4.65% is 18600. However, at present FBT tax rate in the country is

49% on which taxable amount is evaluated. Thus, taxable amount on fringe benefit for Brian is

calculated as 36470.59 which is multiplied by tax rate. Overall, amount of tax payable for him is

17870.59.

3) LOSS ALLOCATED FOR TAX PURPOSES FOR JACK

Jack and Jill who were joint tenants borrowed some money and purchased a property on

rent. They signed an agreement in which it was return that jack was holding 10% share in the

property whereas Jill was holding 90% of the property benefits. Under the agreement it was

stated that, if the property turned out with loss then its bearer will only be jack and the other

partner Jill will not be responsible for any loss or jack will bear 100% loss (Da, Giacomo and

Sembenelli, 2014). However, the capital gain or capital loss required for the account can be

understood by applying IRAC approach as described below:

Issue: In the case scenario, occurred issue is related to borrowing money for rented house

by Jack and Jill in which entitled 10% profit will be in share of Jack. Similarly, in case of

loss, Jack will be liable to face all loss occurred (Zelinsky, 2013). Further, they got loss

of 10000 then allocated money for tax purposes is to recognise. Including this, there is

also condition of in case of selling the property, how much gain or loss can be occurred.

Rule: Accoridng to Tax Act in Australia, it is mentioned that partners are not tax payers

but an individual partner has to pay tax. Thus, this rule is to be implemented on tax and

paying on occurred loss (Blundell, Bozio and Laroque, 2013).

Application: Above mentioned rule is to be implemented in the case scenario and no

taxable amount is determined for Jill while for Jack, taxable amount is to be evaluated.

Further, in case of selling the property, proper gain can be obtained affect their income

properly (Brand, Anable and Tran, 2013).

4

taxable amount * rate of tax)

36470.59 * 49% = 17870.59

Interpretation: It is recognised that fringe interest rate in Australia for 2017 is 5.65%

and employer provided loan of 100000 at the rate of 1%. Therefore, fringe interest benefit on

400000 at the interest rate of 4.65% is 18600. However, at present FBT tax rate in the country is

49% on which taxable amount is evaluated. Thus, taxable amount on fringe benefit for Brian is

calculated as 36470.59 which is multiplied by tax rate. Overall, amount of tax payable for him is

17870.59.

3) LOSS ALLOCATED FOR TAX PURPOSES FOR JACK

Jack and Jill who were joint tenants borrowed some money and purchased a property on

rent. They signed an agreement in which it was return that jack was holding 10% share in the

property whereas Jill was holding 90% of the property benefits. Under the agreement it was

stated that, if the property turned out with loss then its bearer will only be jack and the other

partner Jill will not be responsible for any loss or jack will bear 100% loss (Da, Giacomo and

Sembenelli, 2014). However, the capital gain or capital loss required for the account can be

understood by applying IRAC approach as described below:

Issue: In the case scenario, occurred issue is related to borrowing money for rented house

by Jack and Jill in which entitled 10% profit will be in share of Jack. Similarly, in case of

loss, Jack will be liable to face all loss occurred (Zelinsky, 2013). Further, they got loss

of 10000 then allocated money for tax purposes is to recognise. Including this, there is

also condition of in case of selling the property, how much gain or loss can be occurred.

Rule: Accoridng to Tax Act in Australia, it is mentioned that partners are not tax payers

but an individual partner has to pay tax. Thus, this rule is to be implemented on tax and

paying on occurred loss (Blundell, Bozio and Laroque, 2013).

Application: Above mentioned rule is to be implemented in the case scenario and no

taxable amount is determined for Jill while for Jack, taxable amount is to be evaluated.

Further, in case of selling the property, proper gain can be obtained affect their income

properly (Brand, Anable and Tran, 2013).

4

Conclusion: It is concluded from this case study that Jack is liable to pay on occurred

loss and through selling this property, proper profit can be gained. Therefore, according

to Taxation Law of Australia, it is determined that individual tax will be paid on this loss

by Jack and it will be better to sell the property by which effective income can be earned

effectively (Kosonen, 2014).

4) PRINCIPLES ESTABLISHED IN IRCA V DUKE OF WESTMINSTER

[1936] AC 1

Duke of Westminister was gardener in Australia who reduced to pay tax on his income

for which IRAC approach is applied on taxation for an individual. It stands for issue, rule,

application and conclusion for reducing any occurred problems. However, several principles

mentioned in this approach can be described as below:

Issue: It is related with analysing negligence on paying tax and information sought by

solicitor for intending purchaser land etc. Similarly, issue of measuring damages for

negligent mis statement (Scheve and Stasavage, 2016) Therefore, government of

Australia makes policy plans for reducing these issues to increase revenue and country's

effectiveness.

Rule: Through identifying issues, different rules are made to reduce issues and following

on different plans. In this regard, these rules are made under common law and related to

court case. It is also considered that these rules are helpful to reduce issues occurred for

making correct legal analysis (Australia's Future Taxation system, 2017). Thus, rules for

tax payees and following on its provisions are recognised affect legal system of the

country.

Application: It is one of the essential section of IRAC in which rules are applied to

reduce issues and implementing legal system of the country (Genders, 2016). According

to facts and rules made through court's decision, mentioned rules are applied efficiently

affect country's effectiveness.

Conclusion: In this process, facts and rules made through court's decision and various

results are obtained which are followed on in the future time. However, decision is based

on the implementing rules regarding each issue (Boczko, 2016). Therefore, tax related

5

loss and through selling this property, proper profit can be gained. Therefore, according

to Taxation Law of Australia, it is determined that individual tax will be paid on this loss

by Jack and it will be better to sell the property by which effective income can be earned

effectively (Kosonen, 2014).

4) PRINCIPLES ESTABLISHED IN IRCA V DUKE OF WESTMINSTER

[1936] AC 1

Duke of Westminister was gardener in Australia who reduced to pay tax on his income

for which IRAC approach is applied on taxation for an individual. It stands for issue, rule,

application and conclusion for reducing any occurred problems. However, several principles

mentioned in this approach can be described as below:

Issue: It is related with analysing negligence on paying tax and information sought by

solicitor for intending purchaser land etc. Similarly, issue of measuring damages for

negligent mis statement (Scheve and Stasavage, 2016) Therefore, government of

Australia makes policy plans for reducing these issues to increase revenue and country's

effectiveness.

Rule: Through identifying issues, different rules are made to reduce issues and following

on different plans. In this regard, these rules are made under common law and related to

court case. It is also considered that these rules are helpful to reduce issues occurred for

making correct legal analysis (Australia's Future Taxation system, 2017). Thus, rules for

tax payees and following on its provisions are recognised affect legal system of the

country.

Application: It is one of the essential section of IRAC in which rules are applied to

reduce issues and implementing legal system of the country (Genders, 2016). According

to facts and rules made through court's decision, mentioned rules are applied efficiently

affect country's effectiveness.

Conclusion: In this process, facts and rules made through court's decision and various

results are obtained which are followed on in the future time. However, decision is based

on the implementing rules regarding each issue (Boczko, 2016). Therefore, tax related

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

issue is also reduced in this way impact on overall management and other implements for

the further years.

However, under IRCA V DUKE OF WESTMINSTER [1936] AC 1, following principles

are determined for tax planning and reducing tax avoidance as:

Disclosure of tax avoidance scheme (DOTAS): Under this principles, rules and

regulations for reducing tax avoidance are made if TAARS remain unfair. In this regard,

it is considered that an individual employee must disclose his income including money

from foreign. Including this, in case of negligence on paying tax, warning and other

penalties are also ruled for reducing it. Thus, DOTAS promotes an individual to pay tax

and disclosing details of earned income and allowances effectively.

Targeted anti-avoidence rules (TAARS): It is targeted to reduce tax under this

provision impacts on revenue of the country on which decisions are made for its

development. Therefore, through following on rules amended in this provision would be

able to encourage public for not avoiding paying tax (inclair, W. and Lipkin, 2016).

GAAR: It is more specific in comparison to general for tax regime rules in process and is

to be come into force soon. It also includes tax planning and implementing provisions for

paying tax. In this regard, different rules are to be made for tax benefits for reducing

business risks (Zelinsky, 2013). Hence, GAAR remains effective for paying tax and

implementing plans for tax payers effectively.

5) CASE STUDY RELATED TO BILL REGARDING PARCEL

Bill is an owner of a large parcel of land which is full of pine trees in which he intends to

use the land for grazing sheep. Now he wants to have the field to be cleared so that he can

discover logging company which will cost him around $1000 for every 100 meters of timber

which they can take from the land (Boczko, 2016). It can be understood with the help of IRAC

approach as described below:

Issue: It is recognised that on paying 1000 for every 100 meter, Bill will have to pay

100000 on which tax redemptions and allowances can be gained. While, on the other

hand, he is also planning to invest 50000 in lump sum which would also be effective for

6

the further years.

However, under IRCA V DUKE OF WESTMINSTER [1936] AC 1, following principles

are determined for tax planning and reducing tax avoidance as:

Disclosure of tax avoidance scheme (DOTAS): Under this principles, rules and

regulations for reducing tax avoidance are made if TAARS remain unfair. In this regard,

it is considered that an individual employee must disclose his income including money

from foreign. Including this, in case of negligence on paying tax, warning and other

penalties are also ruled for reducing it. Thus, DOTAS promotes an individual to pay tax

and disclosing details of earned income and allowances effectively.

Targeted anti-avoidence rules (TAARS): It is targeted to reduce tax under this

provision impacts on revenue of the country on which decisions are made for its

development. Therefore, through following on rules amended in this provision would be

able to encourage public for not avoiding paying tax (inclair, W. and Lipkin, 2016).

GAAR: It is more specific in comparison to general for tax regime rules in process and is

to be come into force soon. It also includes tax planning and implementing provisions for

paying tax. In this regard, different rules are to be made for tax benefits for reducing

business risks (Zelinsky, 2013). Hence, GAAR remains effective for paying tax and

implementing plans for tax payers effectively.

5) CASE STUDY RELATED TO BILL REGARDING PARCEL

Bill is an owner of a large parcel of land which is full of pine trees in which he intends to

use the land for grazing sheep. Now he wants to have the field to be cleared so that he can

discover logging company which will cost him around $1000 for every 100 meters of timber

which they can take from the land (Boczko, 2016). It can be understood with the help of IRAC

approach as described below:

Issue: It is recognised that on paying 1000 for every 100 meter, Bill will have to pay

100000 on which tax redemptions and allowances can be gained. While, on the other

hand, he is also planning to invest 50000 in lump sum which would also be effective for

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

required timber from his land (Genders, 2016). Therefore, taking appropriate decision on

this investment is required,

Rule: According to Tax Act in Australia, it is mentioned that through incurring cost on

timber of land, appropriate allowance can be gained which consider as income. However,

through incurring 100000 will be useful on which effective income can be earned (Da,

Giacomo and Sembenelli, 2014).

Application: By implementing above mentioned rule, it will be good for Bill to invest

10000 for taking effective redemption and proper advantage of tax rules of Australia.

Conclusion: Through calculating both investments as 10000 and 50000, it is concluded

that Bill can gain effective profit of tax allowances (Kosonen, 2014). Therefore, for

taking adequate advantage of tax policies, it will be good decision for Bill to invest 1000

per 100 meters for timber as required.

CONCLUSION

It is concluded that tax policies are effective for reducing its avoidance and increasing

government's fund in Australia. In this regard, deep understanding towards IRAC approach has

been increased. However, different case study related to taxable amount and fringe benefits are

described through this assignment. In addition to this, solutions for an individual regarding

paying tax and increasing income is described. Thus, all tax policies and rules for implementing

strategies has been understood through this report.

7

this investment is required,

Rule: According to Tax Act in Australia, it is mentioned that through incurring cost on

timber of land, appropriate allowance can be gained which consider as income. However,

through incurring 100000 will be useful on which effective income can be earned (Da,

Giacomo and Sembenelli, 2014).

Application: By implementing above mentioned rule, it will be good for Bill to invest

10000 for taking effective redemption and proper advantage of tax rules of Australia.

Conclusion: Through calculating both investments as 10000 and 50000, it is concluded

that Bill can gain effective profit of tax allowances (Kosonen, 2014). Therefore, for

taking adequate advantage of tax policies, it will be good decision for Bill to invest 1000

per 100 meters for timber as required.

CONCLUSION

It is concluded that tax policies are effective for reducing its avoidance and increasing

government's fund in Australia. In this regard, deep understanding towards IRAC approach has

been increased. However, different case study related to taxable amount and fringe benefits are

described through this assignment. In addition to this, solutions for an individual regarding

paying tax and increasing income is described. Thus, all tax policies and rules for implementing

strategies has been understood through this report.

7

REFERENCE

Books and Journal

Bird, R.M., 2015. Subnational taxation in developing countries: a review of the literature.

Journal of International Commerce, Economics and Policy. 2(1). pp. 139-161.

Blundell, R., Bozio, A. and Laroque, G., 2013. Extensive and intensive margins of labour

supply: work and working hours in the US, the UK and France. Fiscal Studies. 34(1). pp.

1-29.

Boczko, T., 2016. Managing Your Money: A Practical Guide to Personal Finance. Palgrave

Macmillan.

Brand, C., Anable, J. and Tran, M., 2013. Accelerating the transformation to a low carbon

passenger transport system: The role of car purchase taxes, feebates, road taxes and

scrappage incentives in the UK. Transportation Research Part A: Policy and Practice.

49(2). pp. 132-148.

Da Rin, Giacomo, M. and Sembenelli, A., 2014. Entrepreneurship, firm entry, and the taxation

of corporate income: Evidence from Europe. Journal of public economics. 95(5). pp.

1048-1066.

Genders, D., 2016. The Daily Telegraph Tax Guide 2016: Understanding the Tax System,

Completing Your Tax Return and Planning How to Become More Tax Efficient. Kogan

Page Publishers.

Griffith, R., Hines, J. and Sørensen, P.B., 2013. International capital taxation. Dimensions of Tax

Design: The Mirrlees Review. 6(3). pp. 914-996.

Kim, J. and et.al., 2013. Attitudes towards road pricing and environmental taxation among US

and UK students. Transportation Research Part A: Policy and Practice. 48(3). pp. 50-62.

Kosonen, K., 2014. Regressivity of environmental taxation: myth or reality?. Handbook of

Research on Environmental Taxation, Cheltenham: Edward Elgar Publishing. 5(4). pp.

161-174.

Scheve, K. and Stasavage, D., 2016. The conscription of wealth: mass warfare and the demand

for progressive taxation. International Organization. 64(4). pp. 529-561.

8

Books and Journal

Bird, R.M., 2015. Subnational taxation in developing countries: a review of the literature.

Journal of International Commerce, Economics and Policy. 2(1). pp. 139-161.

Blundell, R., Bozio, A. and Laroque, G., 2013. Extensive and intensive margins of labour

supply: work and working hours in the US, the UK and France. Fiscal Studies. 34(1). pp.

1-29.

Boczko, T., 2016. Managing Your Money: A Practical Guide to Personal Finance. Palgrave

Macmillan.

Brand, C., Anable, J. and Tran, M., 2013. Accelerating the transformation to a low carbon

passenger transport system: The role of car purchase taxes, feebates, road taxes and

scrappage incentives in the UK. Transportation Research Part A: Policy and Practice.

49(2). pp. 132-148.

Da Rin, Giacomo, M. and Sembenelli, A., 2014. Entrepreneurship, firm entry, and the taxation

of corporate income: Evidence from Europe. Journal of public economics. 95(5). pp.

1048-1066.

Genders, D., 2016. The Daily Telegraph Tax Guide 2016: Understanding the Tax System,

Completing Your Tax Return and Planning How to Become More Tax Efficient. Kogan

Page Publishers.

Griffith, R., Hines, J. and Sørensen, P.B., 2013. International capital taxation. Dimensions of Tax

Design: The Mirrlees Review. 6(3). pp. 914-996.

Kim, J. and et.al., 2013. Attitudes towards road pricing and environmental taxation among US

and UK students. Transportation Research Part A: Policy and Practice. 48(3). pp. 50-62.

Kosonen, K., 2014. Regressivity of environmental taxation: myth or reality?. Handbook of

Research on Environmental Taxation, Cheltenham: Edward Elgar Publishing. 5(4). pp.

161-174.

Scheve, K. and Stasavage, D., 2016. The conscription of wealth: mass warfare and the demand

for progressive taxation. International Organization. 64(4). pp. 529-561.

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.