Taxation Theory, Practice: Asset Tax Liability Analysis Report

VerifiedAdded on 2020/11/23

|12

|3325

|48

Report

AI Summary

This report provides a comprehensive analysis of Australian taxation, focusing on the tax liabilities of an antique collector. It examines various assets, including vacant land, an antique bed, a painting, shares, and a violin, applying relevant Australian tax laws and regulations. The report delves into capital gains tax (CGT) calculations, considering indexation, cost bases, and sale proceeds for each asset. It also addresses pre-CGT assets and the implications of insurance claims. Furthermore, the report analyzes the tax consequences of share portfolios, including the calculation of capital gains and losses. The analysis extends to the valuation of assets and the application of relevant sections of the Income Tax Assessment Act 1997. The report serves as a practical guide to understanding taxation theory and practice in the Australian context, offering insights for tax consultants and investors alike.

Taxation Theory,

Practice

Practice

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

a. Block of vacant land................................................................................................................1

b. Antique bed.............................................................................................................................2

c. Painting....................................................................................................................................3

d. Shares......................................................................................................................................4

e. Violin.......................................................................................................................................7

QUESTION 2...................................................................................................................................8

a. Advise Rapid Heat on FBT consequences..............................................................................8

b. Variation in ascertainment of FBT consequences..................................................................9

CONCLUSION................................................................................................................................9

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

a. Block of vacant land................................................................................................................1

b. Antique bed.............................................................................................................................2

c. Painting....................................................................................................................................3

d. Shares......................................................................................................................................4

e. Violin.......................................................................................................................................7

QUESTION 2...................................................................................................................................8

a. Advise Rapid Heat on FBT consequences..............................................................................8

b. Variation in ascertainment of FBT consequences..................................................................9

CONCLUSION................................................................................................................................9

INTRODUCTION

Taxation is a process of levying tax on organisations which governmental authority

imposes on individuals and organisations. Main aim of this project report is to build an

understanding about the concept of tax and taxation practice in Australia. In this project report,

various assets are analysed in order to determine their tax liability and taxable income. Several

appropriate rules and regulations are applied in this report such as capital gains tax, fringe benefit

tax and index number taxation. As a tax consultant in Mayfield, NSW tax liability of certain

clients are ascertained. Taxation law of Australia is examined in this report in order to facilitate

various clients (Cato, 2012).

QUESTION 1

In this case scenario, tax liability of a client which is a antique collector is needed to be

ascertained by examining client's various assets and collections. As a tax consultant in Mayfield,

NSW tax liability of client is determined. From the given scenario, it has been observed that

client is an investor and antique collector which does not carrying any business. Due to which all

the tax liabilities will be imposed as an individual and tax law of Australia will be applied.

a. Block of vacant land

Case Scenario:

According to the given scenario, client decided to sell their block of vacant land and

signed a contract on 3 June for 320000 dollars. Client has acquired this land in January 2001 for

$100000 and incurred 20000$ in local council, water and sewerage rates and land taxes. The

signed contract states that client will be provided 20000 dollars at the signing date and remaining

amount will be payable to her when change of ownership will be registered (Dafflon, 2015).

Related regulations and laws:

According to rules and regulations of Australian taxation office, vacant land (either for

private purpose or as an investment) it's usually considered a capital asset which is subject to

capital gains tax (CGT) when anyone sell land in Australia. Expenses incurred while acquiring

the land and ongoing expenses such as council rates and loan interest these expenses can't be

claimed as an income tax deduction because the land does not generate income. Instead these

expenses can be added to the cost base of land for the purpose of calculating capital gain or loss

when client actually sells it. Law which is applicable in this case is Income tax assessment act

1

Taxation is a process of levying tax on organisations which governmental authority

imposes on individuals and organisations. Main aim of this project report is to build an

understanding about the concept of tax and taxation practice in Australia. In this project report,

various assets are analysed in order to determine their tax liability and taxable income. Several

appropriate rules and regulations are applied in this report such as capital gains tax, fringe benefit

tax and index number taxation. As a tax consultant in Mayfield, NSW tax liability of certain

clients are ascertained. Taxation law of Australia is examined in this report in order to facilitate

various clients (Cato, 2012).

QUESTION 1

In this case scenario, tax liability of a client which is a antique collector is needed to be

ascertained by examining client's various assets and collections. As a tax consultant in Mayfield,

NSW tax liability of client is determined. From the given scenario, it has been observed that

client is an investor and antique collector which does not carrying any business. Due to which all

the tax liabilities will be imposed as an individual and tax law of Australia will be applied.

a. Block of vacant land

Case Scenario:

According to the given scenario, client decided to sell their block of vacant land and

signed a contract on 3 June for 320000 dollars. Client has acquired this land in January 2001 for

$100000 and incurred 20000$ in local council, water and sewerage rates and land taxes. The

signed contract states that client will be provided 20000 dollars at the signing date and remaining

amount will be payable to her when change of ownership will be registered (Dafflon, 2015).

Related regulations and laws:

According to rules and regulations of Australian taxation office, vacant land (either for

private purpose or as an investment) it's usually considered a capital asset which is subject to

capital gains tax (CGT) when anyone sell land in Australia. Expenses incurred while acquiring

the land and ongoing expenses such as council rates and loan interest these expenses can't be

claimed as an income tax deduction because the land does not generate income. Instead these

expenses can be added to the cost base of land for the purpose of calculating capital gain or loss

when client actually sells it. Law which is applicable in this case is Income tax assessment act

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1997 of Australia and regulations are implied of capital gains. According to section 104(35) of

ITA act 1997, ascertainment of tax liability which should be implied on client is determined

below by considering indexation base and related tax slab (Kaplow, 2011).

Calculation of Cost base on 3/06

Acquisition Cost of Vacant land 100000

Add Statutory Rates And taxes 20000

Non indexed Cost Base 120000

Calculation of Sale Proceeds

Particulars Amount

Sale income from land 320000

Less: Index Cost of acquisition 120000

Gain for next year 200000

Justification and Interpretation:

From the above calculation it has been ascertained that gain which is considered to be

received in the next year is determined as 200000. this amount is calculated by comparing

indexation cost base of acquisition of land and value of land which is sold.

b. Antique bed

Case Scenario:

According to the given case, it has observed that client has an antique bed valued as

25000 dollars which was purchased at 3500 on 21 July 1986 and has incurred few expenses

amounting as 1500 on 29 October 1986. This antique bed was stolen from her house due to

which client lodged claim for insurance. Due to nature of insurance policy, client only received

claim of 11000 dollars as household content policy.

Related rules and legislations:

According to Australian taxation office, ancient bed is considered as capital gain which is

taxable under capital gain taxes. CGT started from 20 September 1985 and this asset was

purchased on 21 July 1986. As this asset was acquired before 1999, indexation tax rate will be

applicable. Despite of the fact this asset was stolen, still tax will be applicable to the amount

which is received by Insurance company as insurance claim (Molle, 2017). This tax is applicable

2

ITA act 1997, ascertainment of tax liability which should be implied on client is determined

below by considering indexation base and related tax slab (Kaplow, 2011).

Calculation of Cost base on 3/06

Acquisition Cost of Vacant land 100000

Add Statutory Rates And taxes 20000

Non indexed Cost Base 120000

Calculation of Sale Proceeds

Particulars Amount

Sale income from land 320000

Less: Index Cost of acquisition 120000

Gain for next year 200000

Justification and Interpretation:

From the above calculation it has been ascertained that gain which is considered to be

received in the next year is determined as 200000. this amount is calculated by comparing

indexation cost base of acquisition of land and value of land which is sold.

b. Antique bed

Case Scenario:

According to the given case, it has observed that client has an antique bed valued as

25000 dollars which was purchased at 3500 on 21 July 1986 and has incurred few expenses

amounting as 1500 on 29 October 1986. This antique bed was stolen from her house due to

which client lodged claim for insurance. Due to nature of insurance policy, client only received

claim of 11000 dollars as household content policy.

Related rules and legislations:

According to Australian taxation office, ancient bed is considered as capital gain which is

taxable under capital gain taxes. CGT started from 20 September 1985 and this asset was

purchased on 21 July 1986. As this asset was acquired before 1999, indexation tax rate will be

applicable. Despite of the fact this asset was stolen, still tax will be applicable to the amount

which is received by Insurance company as insurance claim (Molle, 2017). This tax is applicable

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

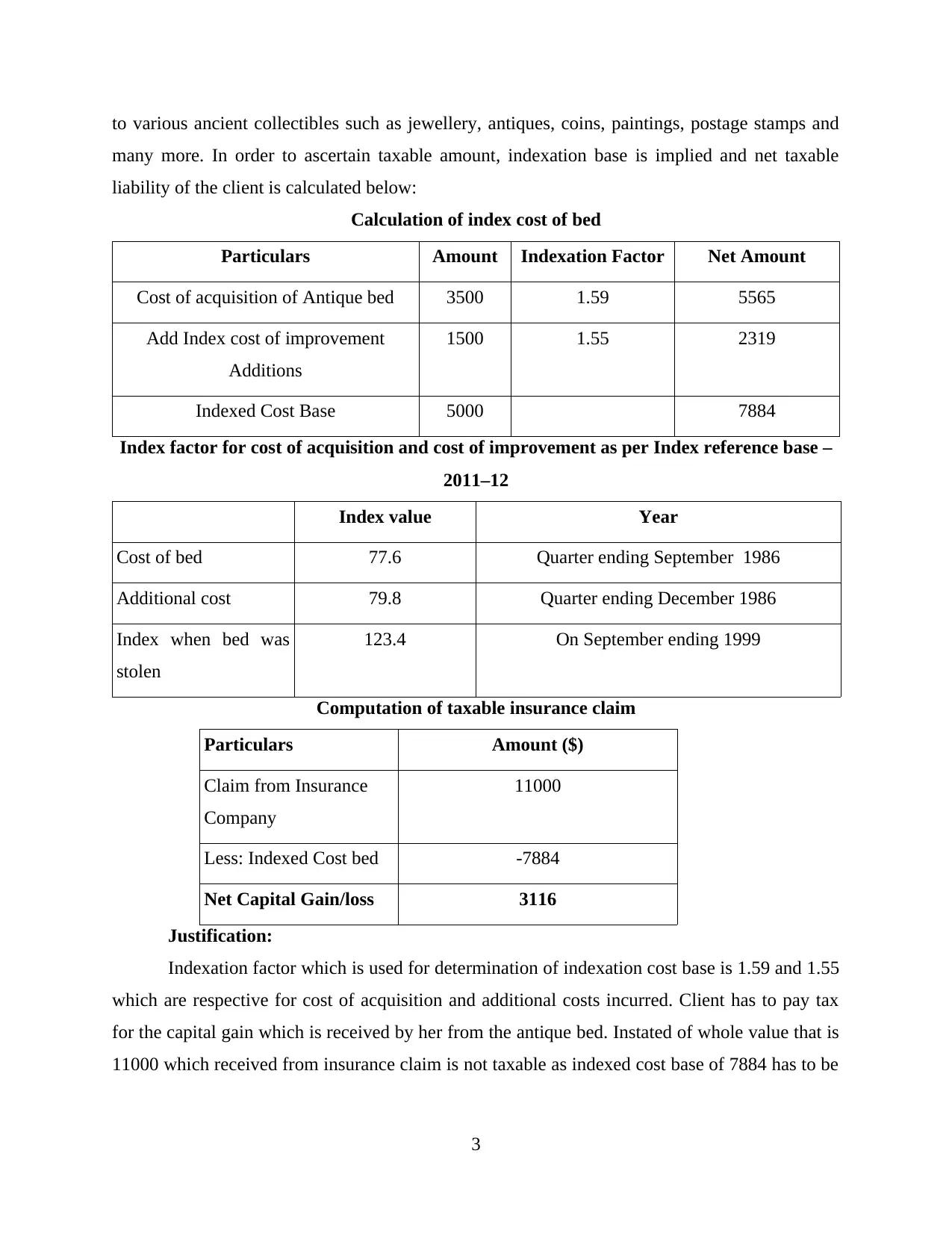

to various ancient collectibles such as jewellery, antiques, coins, paintings, postage stamps and

many more. In order to ascertain taxable amount, indexation base is implied and net taxable

liability of the client is calculated below:

Calculation of index cost of bed

Particulars Amount Indexation Factor Net Amount

Cost of acquisition of Antique bed 3500 1.59 5565

Add Index cost of improvement

Additions

1500 1.55 2319

Indexed Cost Base 5000 7884

Index factor for cost of acquisition and cost of improvement as per Index reference base –

2011–12

Index value Year

Cost of bed 77.6 Quarter ending September 1986

Additional cost 79.8 Quarter ending December 1986

Index when bed was

stolen

123.4 On September ending 1999

Computation of taxable insurance claim

Particulars Amount ($)

Claim from Insurance

Company

11000

Less: Indexed Cost bed -7884

Net Capital Gain/loss 3116

Justification:

Indexation factor which is used for determination of indexation cost base is 1.59 and 1.55

which are respective for cost of acquisition and additional costs incurred. Client has to pay tax

for the capital gain which is received by her from the antique bed. Instated of whole value that is

11000 which received from insurance claim is not taxable as indexed cost base of 7884 has to be

3

many more. In order to ascertain taxable amount, indexation base is implied and net taxable

liability of the client is calculated below:

Calculation of index cost of bed

Particulars Amount Indexation Factor Net Amount

Cost of acquisition of Antique bed 3500 1.59 5565

Add Index cost of improvement

Additions

1500 1.55 2319

Indexed Cost Base 5000 7884

Index factor for cost of acquisition and cost of improvement as per Index reference base –

2011–12

Index value Year

Cost of bed 77.6 Quarter ending September 1986

Additional cost 79.8 Quarter ending December 1986

Index when bed was

stolen

123.4 On September ending 1999

Computation of taxable insurance claim

Particulars Amount ($)

Claim from Insurance

Company

11000

Less: Indexed Cost bed -7884

Net Capital Gain/loss 3116

Justification:

Indexation factor which is used for determination of indexation cost base is 1.59 and 1.55

which are respective for cost of acquisition and additional costs incurred. Client has to pay tax

for the capital gain which is received by her from the antique bed. Instated of whole value that is

11000 which received from insurance claim is not taxable as indexed cost base of 7884 has to be

3

deducted according to taxation office guidelines. This ultimately gives net taxable income as

3116.

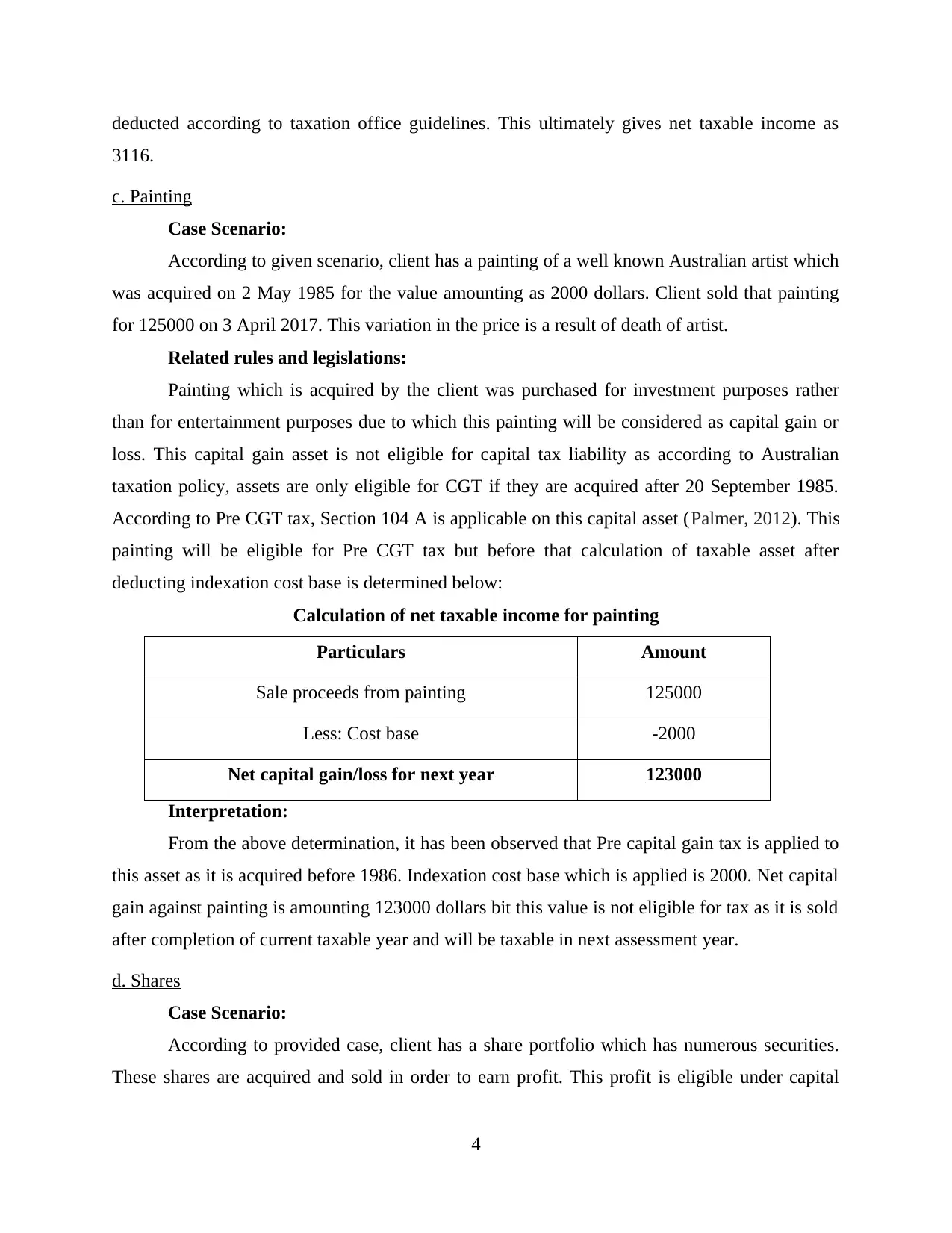

c. Painting

Case Scenario:

According to given scenario, client has a painting of a well known Australian artist which

was acquired on 2 May 1985 for the value amounting as 2000 dollars. Client sold that painting

for 125000 on 3 April 2017. This variation in the price is a result of death of artist.

Related rules and legislations:

Painting which is acquired by the client was purchased for investment purposes rather

than for entertainment purposes due to which this painting will be considered as capital gain or

loss. This capital gain asset is not eligible for capital tax liability as according to Australian

taxation policy, assets are only eligible for CGT if they are acquired after 20 September 1985.

According to Pre CGT tax, Section 104 A is applicable on this capital asset (Palmer, 2012). This

painting will be eligible for Pre CGT tax but before that calculation of taxable asset after

deducting indexation cost base is determined below:

Calculation of net taxable income for painting

Particulars Amount

Sale proceeds from painting 125000

Less: Cost base -2000

Net capital gain/loss for next year 123000

Interpretation:

From the above determination, it has been observed that Pre capital gain tax is applied to

this asset as it is acquired before 1986. Indexation cost base which is applied is 2000. Net capital

gain against painting is amounting 123000 dollars bit this value is not eligible for tax as it is sold

after completion of current taxable year and will be taxable in next assessment year.

d. Shares

Case Scenario:

According to provided case, client has a share portfolio which has numerous securities.

These shares are acquired and sold in order to earn profit. This profit is eligible under capital

4

3116.

c. Painting

Case Scenario:

According to given scenario, client has a painting of a well known Australian artist which

was acquired on 2 May 1985 for the value amounting as 2000 dollars. Client sold that painting

for 125000 on 3 April 2017. This variation in the price is a result of death of artist.

Related rules and legislations:

Painting which is acquired by the client was purchased for investment purposes rather

than for entertainment purposes due to which this painting will be considered as capital gain or

loss. This capital gain asset is not eligible for capital tax liability as according to Australian

taxation policy, assets are only eligible for CGT if they are acquired after 20 September 1985.

According to Pre CGT tax, Section 104 A is applicable on this capital asset (Palmer, 2012). This

painting will be eligible for Pre CGT tax but before that calculation of taxable asset after

deducting indexation cost base is determined below:

Calculation of net taxable income for painting

Particulars Amount

Sale proceeds from painting 125000

Less: Cost base -2000

Net capital gain/loss for next year 123000

Interpretation:

From the above determination, it has been observed that Pre capital gain tax is applied to

this asset as it is acquired before 1986. Indexation cost base which is applied is 2000. Net capital

gain against painting is amounting 123000 dollars bit this value is not eligible for tax as it is sold

after completion of current taxable year and will be taxable in next assessment year.

d. Shares

Case Scenario:

According to provided case, client has a share portfolio which has numerous securities.

These shares are acquired and sold in order to earn profit. This profit is eligible under capital

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

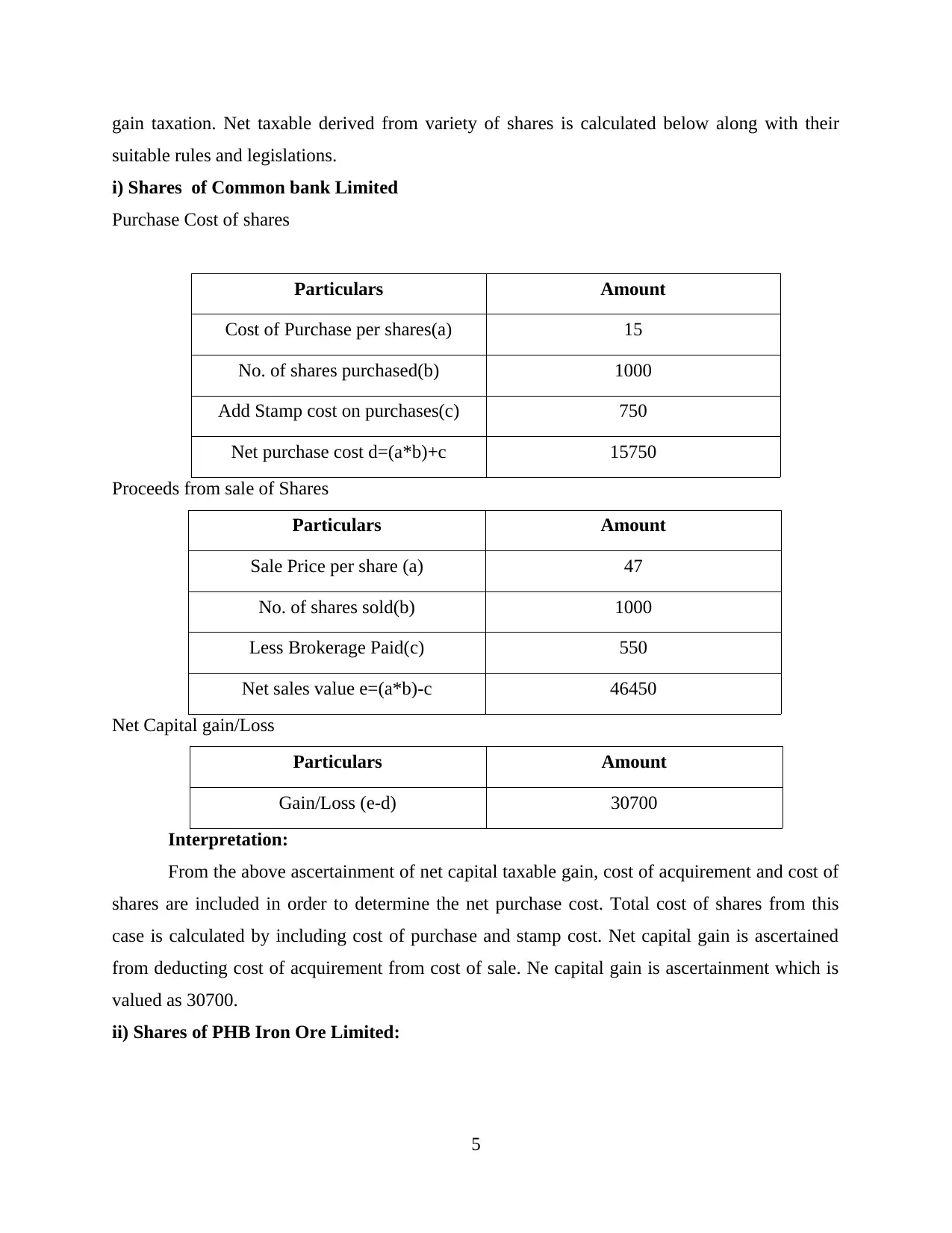

gain taxation. Net taxable derived from variety of shares is calculated below along with their

suitable rules and legislations.

i) Shares of Common bank Limited

Purchase Cost of shares

Particulars Amount

Cost of Purchase per shares(a) 15

No. of shares purchased(b) 1000

Add Stamp cost on purchases(c) 750

Net purchase cost d=(a*b)+c 15750

Proceeds from sale of Shares

Particulars Amount

Sale Price per share (a) 47

No. of shares sold(b) 1000

Less Brokerage Paid(c) 550

Net sales value e=(a*b)-c 46450

Net Capital gain/Loss

Particulars Amount

Gain/Loss (e-d) 30700

Interpretation:

From the above ascertainment of net capital taxable gain, cost of acquirement and cost of

shares are included in order to determine the net purchase cost. Total cost of shares from this

case is calculated by including cost of purchase and stamp cost. Net capital gain is ascertained

from deducting cost of acquirement from cost of sale. Ne capital gain is ascertainment which is

valued as 30700.

ii) Shares of PHB Iron Ore Limited:

5

suitable rules and legislations.

i) Shares of Common bank Limited

Purchase Cost of shares

Particulars Amount

Cost of Purchase per shares(a) 15

No. of shares purchased(b) 1000

Add Stamp cost on purchases(c) 750

Net purchase cost d=(a*b)+c 15750

Proceeds from sale of Shares

Particulars Amount

Sale Price per share (a) 47

No. of shares sold(b) 1000

Less Brokerage Paid(c) 550

Net sales value e=(a*b)-c 46450

Net Capital gain/Loss

Particulars Amount

Gain/Loss (e-d) 30700

Interpretation:

From the above ascertainment of net capital taxable gain, cost of acquirement and cost of

shares are included in order to determine the net purchase cost. Total cost of shares from this

case is calculated by including cost of purchase and stamp cost. Net capital gain is ascertained

from deducting cost of acquirement from cost of sale. Ne capital gain is ascertainment which is

valued as 30700.

ii) Shares of PHB Iron Ore Limited:

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

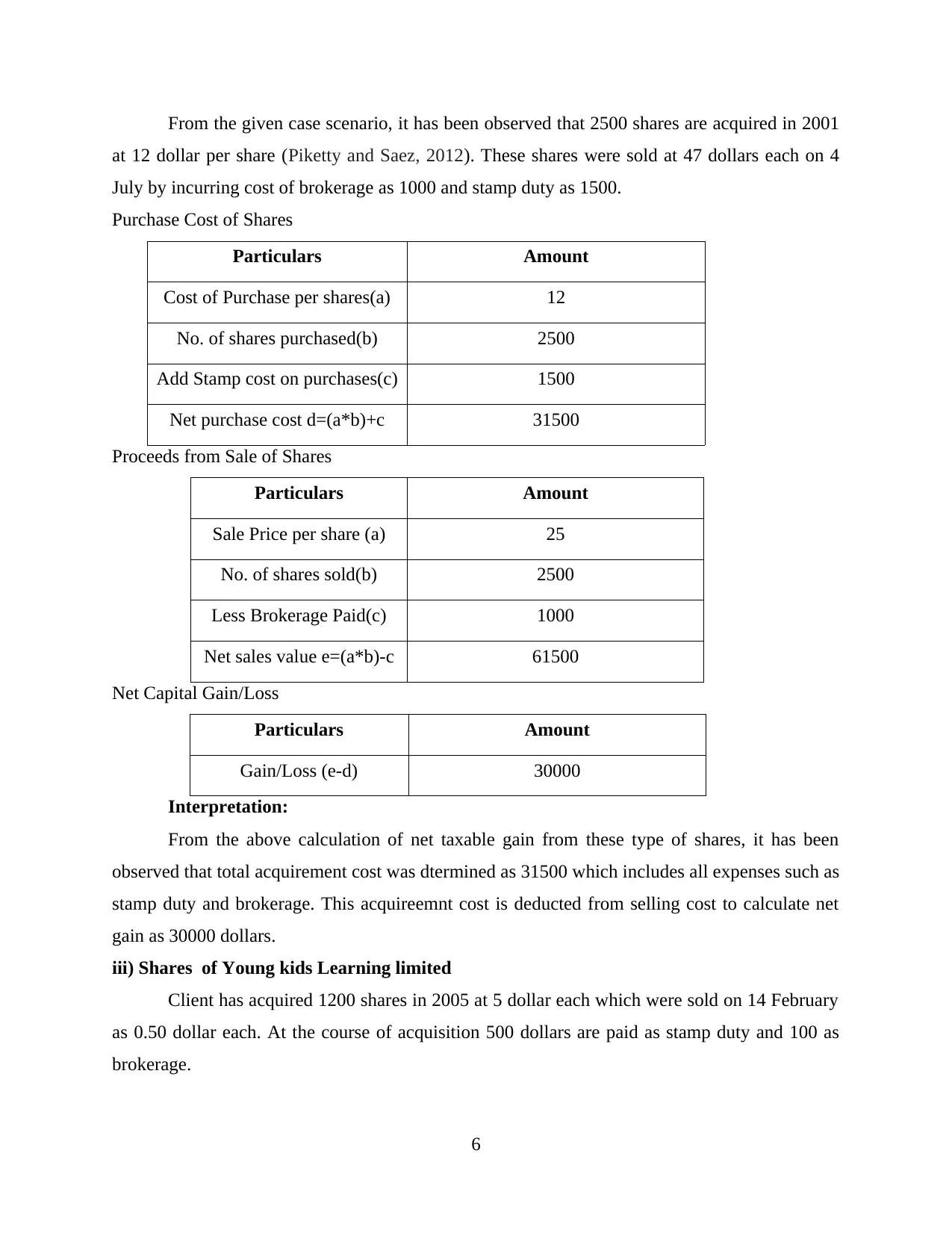

From the given case scenario, it has been observed that 2500 shares are acquired in 2001

at 12 dollar per share (Piketty and Saez, 2012). These shares were sold at 47 dollars each on 4

July by incurring cost of brokerage as 1000 and stamp duty as 1500.

Purchase Cost of Shares

Particulars Amount

Cost of Purchase per shares(a) 12

No. of shares purchased(b) 2500

Add Stamp cost on purchases(c) 1500

Net purchase cost d=(a*b)+c 31500

Proceeds from Sale of Shares

Particulars Amount

Sale Price per share (a) 25

No. of shares sold(b) 2500

Less Brokerage Paid(c) 1000

Net sales value e=(a*b)-c 61500

Net Capital Gain/Loss

Particulars Amount

Gain/Loss (e-d) 30000

Interpretation:

From the above calculation of net taxable gain from these type of shares, it has been

observed that total acquirement cost was dtermined as 31500 which includes all expenses such as

stamp duty and brokerage. This acquireemnt cost is deducted from selling cost to calculate net

gain as 30000 dollars.

iii) Shares of Young kids Learning limited

Client has acquired 1200 shares in 2005 at 5 dollar each which were sold on 14 February

as 0.50 dollar each. At the course of acquisition 500 dollars are paid as stamp duty and 100 as

brokerage.

6

at 12 dollar per share (Piketty and Saez, 2012). These shares were sold at 47 dollars each on 4

July by incurring cost of brokerage as 1000 and stamp duty as 1500.

Purchase Cost of Shares

Particulars Amount

Cost of Purchase per shares(a) 12

No. of shares purchased(b) 2500

Add Stamp cost on purchases(c) 1500

Net purchase cost d=(a*b)+c 31500

Proceeds from Sale of Shares

Particulars Amount

Sale Price per share (a) 25

No. of shares sold(b) 2500

Less Brokerage Paid(c) 1000

Net sales value e=(a*b)-c 61500

Net Capital Gain/Loss

Particulars Amount

Gain/Loss (e-d) 30000

Interpretation:

From the above calculation of net taxable gain from these type of shares, it has been

observed that total acquirement cost was dtermined as 31500 which includes all expenses such as

stamp duty and brokerage. This acquireemnt cost is deducted from selling cost to calculate net

gain as 30000 dollars.

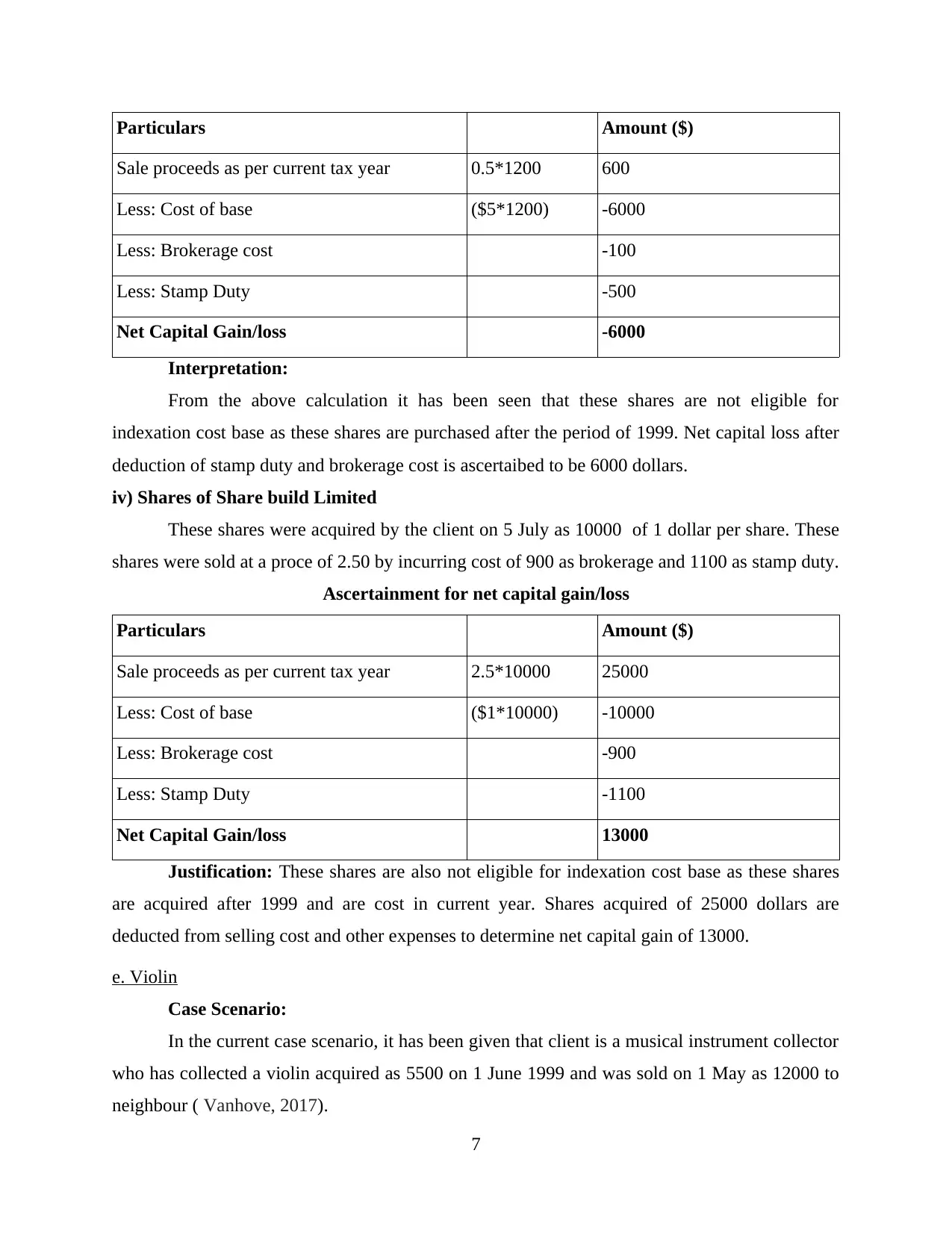

iii) Shares of Young kids Learning limited

Client has acquired 1200 shares in 2005 at 5 dollar each which were sold on 14 February

as 0.50 dollar each. At the course of acquisition 500 dollars are paid as stamp duty and 100 as

brokerage.

6

Particulars Amount ($)

Sale proceeds as per current tax year 0.5*1200 600

Less: Cost of base ($5*1200) -6000

Less: Brokerage cost -100

Less: Stamp Duty -500

Net Capital Gain/loss -6000

Interpretation:

From the above calculation it has been seen that these shares are not eligible for

indexation cost base as these shares are purchased after the period of 1999. Net capital loss after

deduction of stamp duty and brokerage cost is ascertaibed to be 6000 dollars.

iv) Shares of Share build Limited

These shares were acquired by the client on 5 July as 10000 of 1 dollar per share. These

shares were sold at a proce of 2.50 by incurring cost of 900 as brokerage and 1100 as stamp duty.

Ascertainment for net capital gain/loss

Particulars Amount ($)

Sale proceeds as per current tax year 2.5*10000 25000

Less: Cost of base ($1*10000) -10000

Less: Brokerage cost -900

Less: Stamp Duty -1100

Net Capital Gain/loss 13000

Justification: These shares are also not eligible for indexation cost base as these shares

are acquired after 1999 and are cost in current year. Shares acquired of 25000 dollars are

deducted from selling cost and other expenses to determine net capital gain of 13000.

e. Violin

Case Scenario:

In the current case scenario, it has been given that client is a musical instrument collector

who has collected a violin acquired as 5500 on 1 June 1999 and was sold on 1 May as 12000 to

neighbour ( Vanhove, 2017).

7

Sale proceeds as per current tax year 0.5*1200 600

Less: Cost of base ($5*1200) -6000

Less: Brokerage cost -100

Less: Stamp Duty -500

Net Capital Gain/loss -6000

Interpretation:

From the above calculation it has been seen that these shares are not eligible for

indexation cost base as these shares are purchased after the period of 1999. Net capital loss after

deduction of stamp duty and brokerage cost is ascertaibed to be 6000 dollars.

iv) Shares of Share build Limited

These shares were acquired by the client on 5 July as 10000 of 1 dollar per share. These

shares were sold at a proce of 2.50 by incurring cost of 900 as brokerage and 1100 as stamp duty.

Ascertainment for net capital gain/loss

Particulars Amount ($)

Sale proceeds as per current tax year 2.5*10000 25000

Less: Cost of base ($1*10000) -10000

Less: Brokerage cost -900

Less: Stamp Duty -1100

Net Capital Gain/loss 13000

Justification: These shares are also not eligible for indexation cost base as these shares

are acquired after 1999 and are cost in current year. Shares acquired of 25000 dollars are

deducted from selling cost and other expenses to determine net capital gain of 13000.

e. Violin

Case Scenario:

In the current case scenario, it has been given that client is a musical instrument collector

who has collected a violin acquired as 5500 on 1 June 1999 and was sold on 1 May as 12000 to

neighbour ( Vanhove, 2017).

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

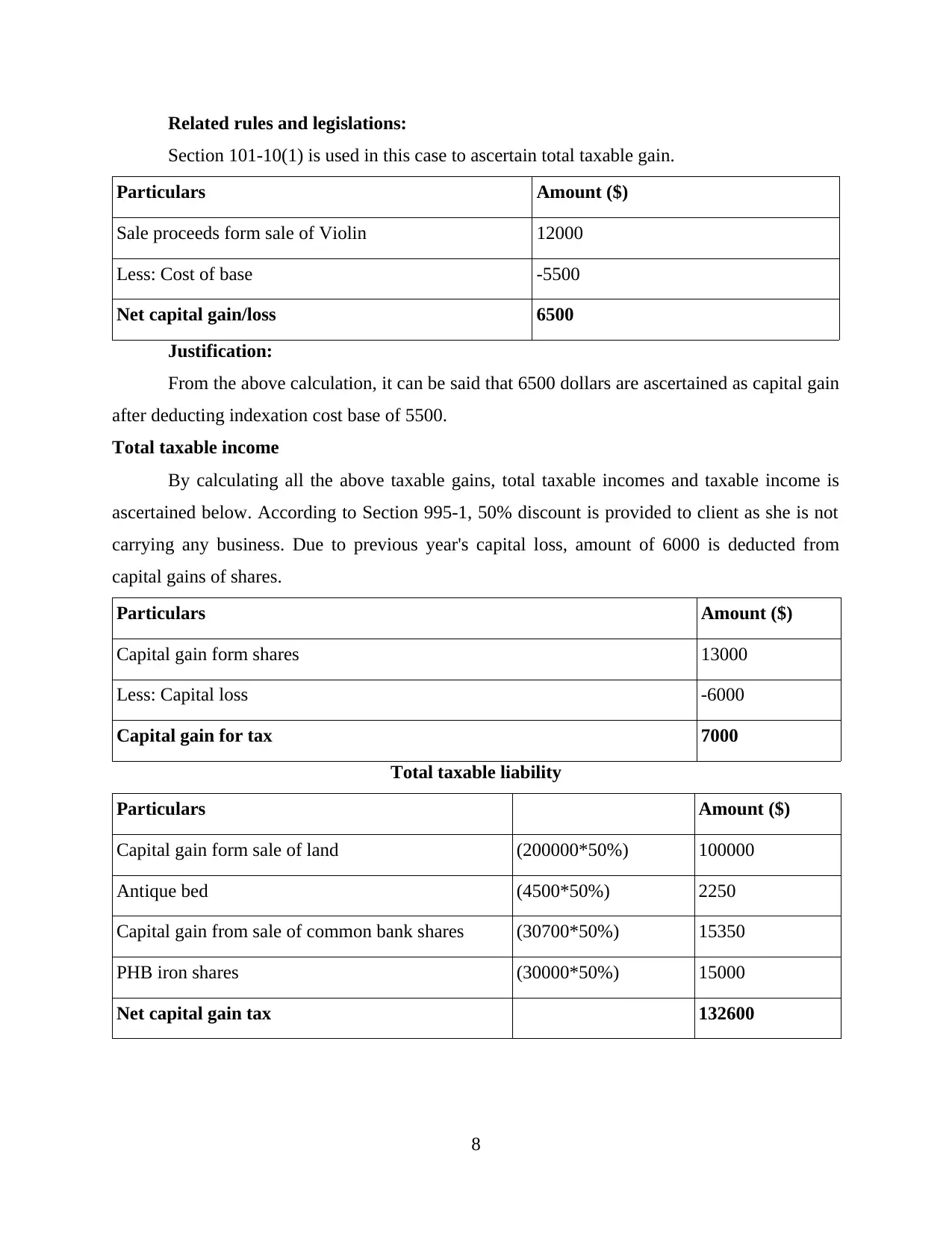

Related rules and legislations:

Section 101-10(1) is used in this case to ascertain total taxable gain.

Particulars Amount ($)

Sale proceeds form sale of Violin 12000

Less: Cost of base -5500

Net capital gain/loss 6500

Justification:

From the above calculation, it can be said that 6500 dollars are ascertained as capital gain

after deducting indexation cost base of 5500.

Total taxable income

By calculating all the above taxable gains, total taxable incomes and taxable income is

ascertained below. According to Section 995-1, 50% discount is provided to client as she is not

carrying any business. Due to previous year's capital loss, amount of 6000 is deducted from

capital gains of shares.

Particulars Amount ($)

Capital gain form shares 13000

Less: Capital loss -6000

Capital gain for tax 7000

Total taxable liability

Particulars Amount ($)

Capital gain form sale of land (200000*50%) 100000

Antique bed (4500*50%) 2250

Capital gain from sale of common bank shares (30700*50%) 15350

PHB iron shares (30000*50%) 15000

Net capital gain tax 132600

8

Section 101-10(1) is used in this case to ascertain total taxable gain.

Particulars Amount ($)

Sale proceeds form sale of Violin 12000

Less: Cost of base -5500

Net capital gain/loss 6500

Justification:

From the above calculation, it can be said that 6500 dollars are ascertained as capital gain

after deducting indexation cost base of 5500.

Total taxable income

By calculating all the above taxable gains, total taxable incomes and taxable income is

ascertained below. According to Section 995-1, 50% discount is provided to client as she is not

carrying any business. Due to previous year's capital loss, amount of 6000 is deducted from

capital gains of shares.

Particulars Amount ($)

Capital gain form shares 13000

Less: Capital loss -6000

Capital gain for tax 7000

Total taxable liability

Particulars Amount ($)

Capital gain form sale of land (200000*50%) 100000

Antique bed (4500*50%) 2250

Capital gain from sale of common bank shares (30700*50%) 15350

PHB iron shares (30000*50%) 15000

Net capital gain tax 132600

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

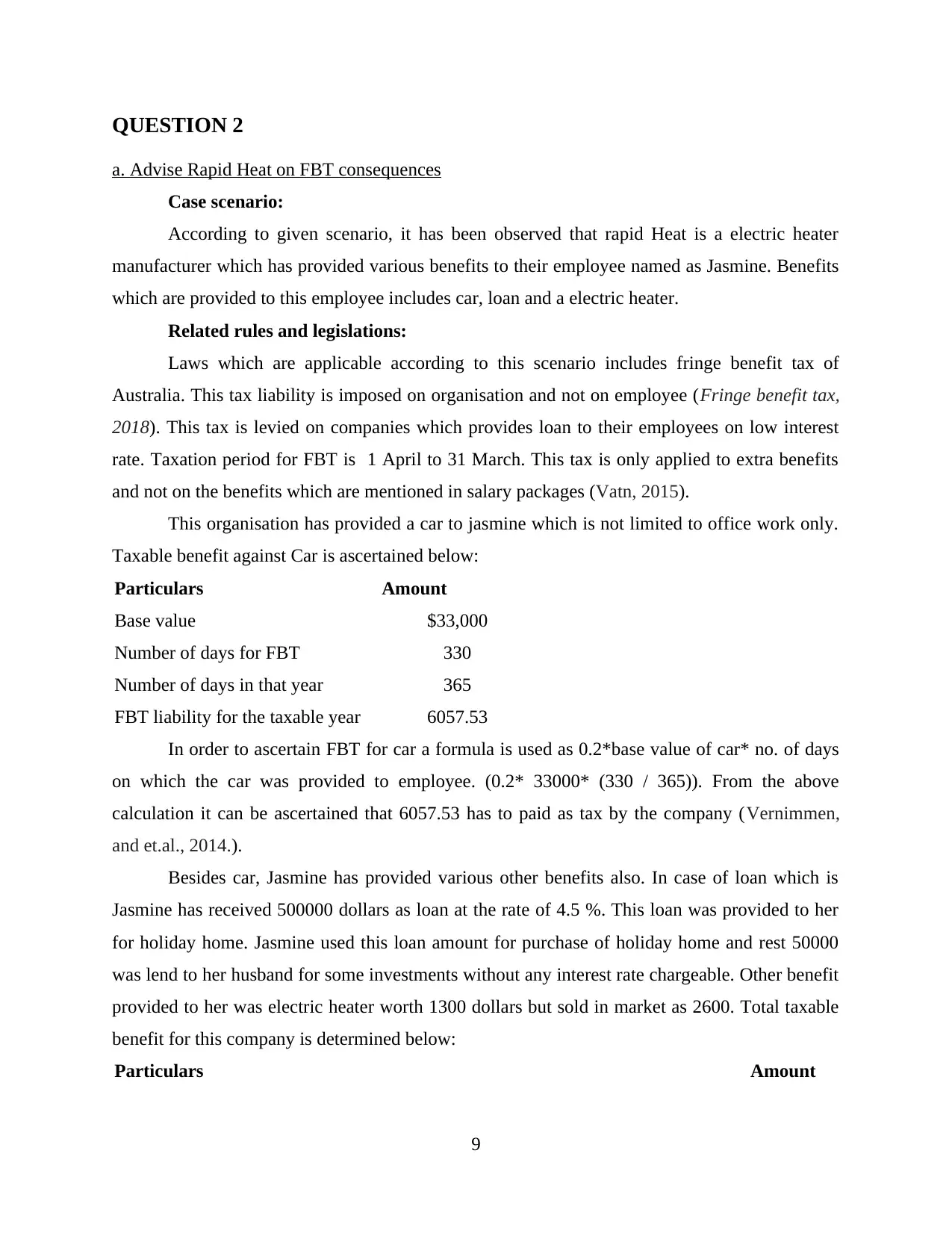

QUESTION 2

a. Advise Rapid Heat on FBT consequences

Case scenario:

According to given scenario, it has been observed that rapid Heat is a electric heater

manufacturer which has provided various benefits to their employee named as Jasmine. Benefits

which are provided to this employee includes car, loan and a electric heater.

Related rules and legislations:

Laws which are applicable according to this scenario includes fringe benefit tax of

Australia. This tax liability is imposed on organisation and not on employee (Fringe benefit tax,

2018). This tax is levied on companies which provides loan to their employees on low interest

rate. Taxation period for FBT is 1 April to 31 March. This tax is only applied to extra benefits

and not on the benefits which are mentioned in salary packages (Vatn, 2015).

This organisation has provided a car to jasmine which is not limited to office work only.

Taxable benefit against Car is ascertained below:

Particulars Amount

Base value $33,000

Number of days for FBT 330

Number of days in that year 365

FBT liability for the taxable year 6057.53

In order to ascertain FBT for car a formula is used as 0.2*base value of car* no. of days

on which the car was provided to employee. (0.2* 33000* (330 / 365)). From the above

calculation it can be ascertained that 6057.53 has to paid as tax by the company (Vernimmen,

and et.al., 2014.).

Besides car, Jasmine has provided various other benefits also. In case of loan which is

Jasmine has received 500000 dollars as loan at the rate of 4.5 %. This loan was provided to her

for holiday home. Jasmine used this loan amount for purchase of holiday home and rest 50000

was lend to her husband for some investments without any interest rate chargeable. Other benefit

provided to her was electric heater worth 1300 dollars but sold in market as 2600. Total taxable

benefit for this company is determined below:

Particulars Amount

9

a. Advise Rapid Heat on FBT consequences

Case scenario:

According to given scenario, it has been observed that rapid Heat is a electric heater

manufacturer which has provided various benefits to their employee named as Jasmine. Benefits

which are provided to this employee includes car, loan and a electric heater.

Related rules and legislations:

Laws which are applicable according to this scenario includes fringe benefit tax of

Australia. This tax liability is imposed on organisation and not on employee (Fringe benefit tax,

2018). This tax is levied on companies which provides loan to their employees on low interest

rate. Taxation period for FBT is 1 April to 31 March. This tax is only applied to extra benefits

and not on the benefits which are mentioned in salary packages (Vatn, 2015).

This organisation has provided a car to jasmine which is not limited to office work only.

Taxable benefit against Car is ascertained below:

Particulars Amount

Base value $33,000

Number of days for FBT 330

Number of days in that year 365

FBT liability for the taxable year 6057.53

In order to ascertain FBT for car a formula is used as 0.2*base value of car* no. of days

on which the car was provided to employee. (0.2* 33000* (330 / 365)). From the above

calculation it can be ascertained that 6057.53 has to paid as tax by the company (Vernimmen,

and et.al., 2014.).

Besides car, Jasmine has provided various other benefits also. In case of loan which is

Jasmine has received 500000 dollars as loan at the rate of 4.5 %. This loan was provided to her

for holiday home. Jasmine used this loan amount for purchase of holiday home and rest 50000

was lend to her husband for some investments without any interest rate chargeable. Other benefit

provided to her was electric heater worth 1300 dollars but sold in market as 2600. Total taxable

benefit for this company is determined below:

Particulars Amount

9

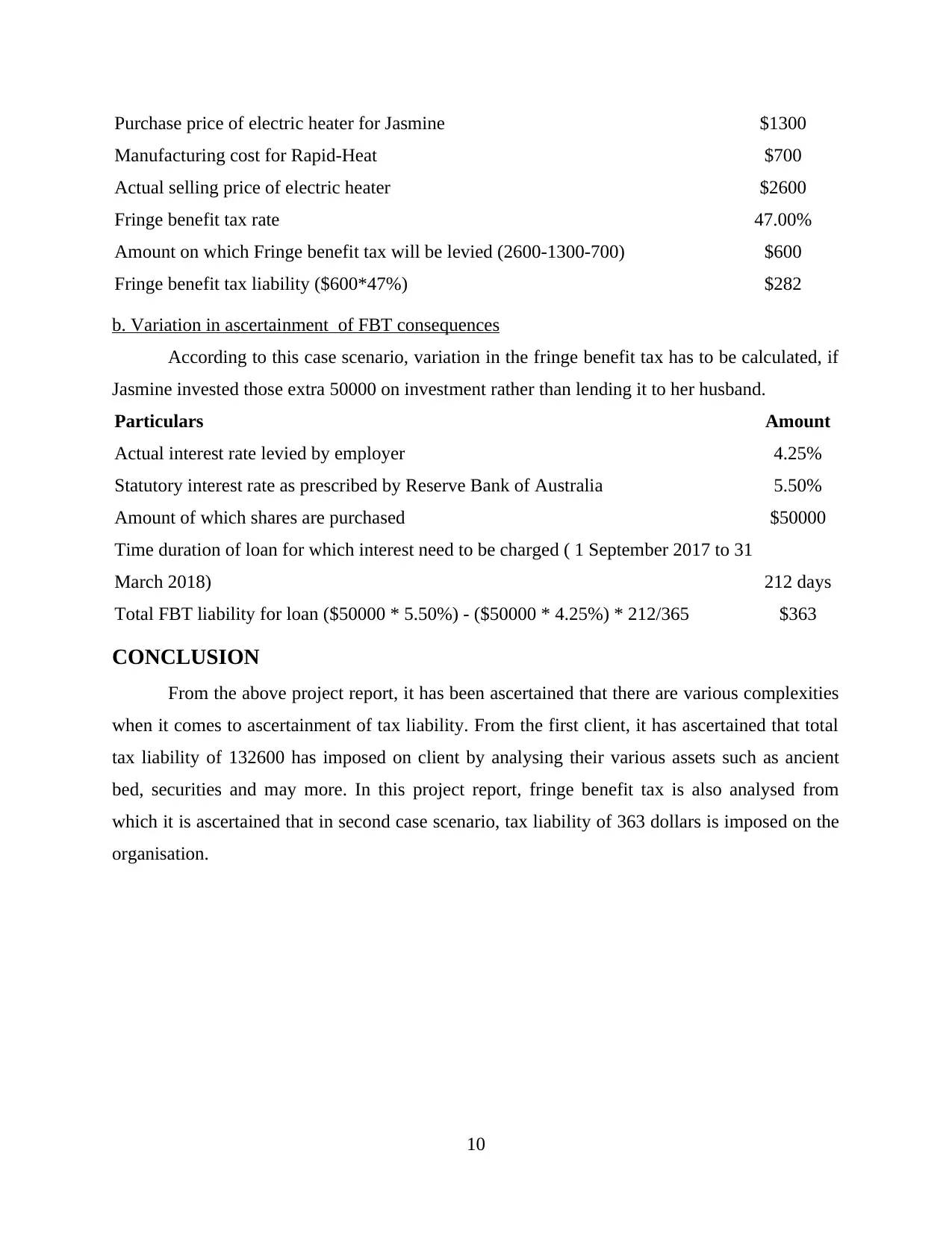

Purchase price of electric heater for Jasmine $1300

Manufacturing cost for Rapid-Heat $700

Actual selling price of electric heater $2600

Fringe benefit tax rate 47.00%

Amount on which Fringe benefit tax will be levied (2600-1300-700) $600

Fringe benefit tax liability ($600*47%) $282

b. Variation in ascertainment of FBT consequences

According to this case scenario, variation in the fringe benefit tax has to be calculated, if

Jasmine invested those extra 50000 on investment rather than lending it to her husband.

Particulars Amount

Actual interest rate levied by employer 4.25%

Statutory interest rate as prescribed by Reserve Bank of Australia 5.50%

Amount of which shares are purchased $50000

Time duration of loan for which interest need to be charged ( 1 September 2017 to 31

March 2018) 212 days

Total FBT liability for loan ($50000 * 5.50%) - ($50000 * 4.25%) * 212/365 $363

CONCLUSION

From the above project report, it has been ascertained that there are various complexities

when it comes to ascertainment of tax liability. From the first client, it has ascertained that total

tax liability of 132600 has imposed on client by analysing their various assets such as ancient

bed, securities and may more. In this project report, fringe benefit tax is also analysed from

which it is ascertained that in second case scenario, tax liability of 363 dollars is imposed on the

organisation.

10

Manufacturing cost for Rapid-Heat $700

Actual selling price of electric heater $2600

Fringe benefit tax rate 47.00%

Amount on which Fringe benefit tax will be levied (2600-1300-700) $600

Fringe benefit tax liability ($600*47%) $282

b. Variation in ascertainment of FBT consequences

According to this case scenario, variation in the fringe benefit tax has to be calculated, if

Jasmine invested those extra 50000 on investment rather than lending it to her husband.

Particulars Amount

Actual interest rate levied by employer 4.25%

Statutory interest rate as prescribed by Reserve Bank of Australia 5.50%

Amount of which shares are purchased $50000

Time duration of loan for which interest need to be charged ( 1 September 2017 to 31

March 2018) 212 days

Total FBT liability for loan ($50000 * 5.50%) - ($50000 * 4.25%) * 212/365 $363

CONCLUSION

From the above project report, it has been ascertained that there are various complexities

when it comes to ascertainment of tax liability. From the first client, it has ascertained that total

tax liability of 132600 has imposed on client by analysing their various assets such as ancient

bed, securities and may more. In this project report, fringe benefit tax is also analysed from

which it is ascertained that in second case scenario, tax liability of 363 dollars is imposed on the

organisation.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.