Australian Taxation Report: Residency, Investment, and Property

VerifiedAdded on 2020/10/23

|11

|3215

|178

Report

AI Summary

This report delves into the intricacies of the Australian taxation system, examining key administrative components, principles of income tax, GST, and fringe benefits tax. It addresses two primary questions: firstly, it analyzes the residency status of Minh, considering his Malaysian investment income and business, applying legal precedents like the Dempsey v FC OF T case to determine his tax obligations. Secondly, it explores the tax implications for Penny concerning the sale of three townhouses, including the calculation of assessable income, capital gains tax, and the application of relevant legislation and exemptions. The report evaluates various scenarios, considering the holding period of the properties and the application of CGT rules, providing a comprehensive analysis of tax liabilities and potential outcomes for both individuals.

TAXATION

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

1. Advising Minh's with context of tax purpose with application of legal precedent............1

2. Explaining Minh's residency status impact assessability of Malaysian investment income

and business............................................................................................................................3

QUESTION 2...................................................................................................................................5

ISSUES:..................................................................................................................................5

RULES AND LEGISLATION...............................................................................................5

APPLICATION OF LAWS AND FACTS............................................................................6

CONCLUSION......................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

1. Advising Minh's with context of tax purpose with application of legal precedent............1

2. Explaining Minh's residency status impact assessability of Malaysian investment income

and business............................................................................................................................3

QUESTION 2...................................................................................................................................5

ISSUES:..................................................................................................................................5

RULES AND LEGISLATION...............................................................................................5

APPLICATION OF LAWS AND FACTS............................................................................6

CONCLUSION......................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION

The Australian taxation system is combination of direct and indirect taxes levied through

both state and Commonwealth government, depends on tax type. Generally, Australian taxation

is based on model of self assessment where taxpayers are highly responsible for purpose of

lodging own return of taxation. The present report will give brief discussion about key

administrative components of Australian Taxation system along with their basic principles of

Australian income tax, goods and service tax and fringe benefits taxation legislation. In this

aspect, there will be identification of issues and outlining relevant cases and legislation along

with evaluation of facts and law through ATO and position of taxpayers. Furthermore, this report

will discuss, analyse and resolve issues on basis of determination of allowable deductions and

assessable income.

QUESTION 1

1. Advising Minh's with context of tax purpose with application of legal precedent.

Issue: Minh would be regarded for tax purpose or not for being and Australian resident

with its explanation of legal precedent. Furthermore, residency status of Minh will impact

assessability of his investment income and Malaysian business or not.

For identifying residency for purpose of tax, there are various tests for undertaking it as

first is resides test. In this, if one live in Australia and replicated as Australian resident for tax so

no test will be applied. Further, resides test is not satisfied, then there will be application of three

statutory test such as domicile, 183 day and superannuation test. Minh fails to resides test and

then there will be application of statutory test.

Ruling:

The 183 day test is one of statutory test where Minh has spent 120 days in Australia.

From 30 June 2018, he has not established and not even started business in Australia. With this

context, he failed to 183 day test and other two tests are superannuation and domicile test

(Residency tests, 2019). Superannuation test is framed for ensuring employees of commonwealth

government who are operating in Australian posts overseas and directly considered as Australian

residents.

In this case, behaviour of Minh during in Australia is traced for organising economic and

domestic affairs as contributing life as very influential factor for identifying residency status. For

consideration of Australia resident, any regular activities are similar to behaviour prior to

1

The Australian taxation system is combination of direct and indirect taxes levied through

both state and Commonwealth government, depends on tax type. Generally, Australian taxation

is based on model of self assessment where taxpayers are highly responsible for purpose of

lodging own return of taxation. The present report will give brief discussion about key

administrative components of Australian Taxation system along with their basic principles of

Australian income tax, goods and service tax and fringe benefits taxation legislation. In this

aspect, there will be identification of issues and outlining relevant cases and legislation along

with evaluation of facts and law through ATO and position of taxpayers. Furthermore, this report

will discuss, analyse and resolve issues on basis of determination of allowable deductions and

assessable income.

QUESTION 1

1. Advising Minh's with context of tax purpose with application of legal precedent.

Issue: Minh would be regarded for tax purpose or not for being and Australian resident

with its explanation of legal precedent. Furthermore, residency status of Minh will impact

assessability of his investment income and Malaysian business or not.

For identifying residency for purpose of tax, there are various tests for undertaking it as

first is resides test. In this, if one live in Australia and replicated as Australian resident for tax so

no test will be applied. Further, resides test is not satisfied, then there will be application of three

statutory test such as domicile, 183 day and superannuation test. Minh fails to resides test and

then there will be application of statutory test.

Ruling:

The 183 day test is one of statutory test where Minh has spent 120 days in Australia.

From 30 June 2018, he has not established and not even started business in Australia. With this

context, he failed to 183 day test and other two tests are superannuation and domicile test

(Residency tests, 2019). Superannuation test is framed for ensuring employees of commonwealth

government who are operating in Australian posts overseas and directly considered as Australian

residents.

In this case, behaviour of Minh during in Australia is traced for organising economic and

domestic affairs as contributing life as very influential factor for identifying residency status. For

consideration of Australia resident, any regular activities are similar to behaviour prior to

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

entering Australia (Bridgen, 2019). With the case of residency, condition is replicated with

regards of each relevant circumstances and facts. There should be account of numerous factors

for determining any reside such as:

Family and business/ employment ties

Social and living arrangements.

Intention or purpose of presence

Living and social arrangements.

The presence of family in Australia might indicate about residence in Australia but he

lives in Kuala Lumpur and doesn't visit in Australia in financial year and maintains social and

cultural arrangements in Malaysia. With context to intention there was absence of any opinion to

settle on permanent aspect as his behaviour is reflected in contrast to his initial decision. Minh's

family was staying in Australia so he was considered as foreign resident to Australia.

In the similar context, there is other factor to identify status of Minh which is physical

presence in Australia. For purpose of residing in Australia, there is requirement of displaying

behaviour over specific duration which is directly consistent for residing like habit, degree of

continuity and routine. The period one spend is not considered as decisive for purpose of

identifying status of residency. Usually six months is actual time for deciding that behaviour is

consistent for residing as it doesn't mean one lives for less than six months is replicated as

foreign resident and more than this are Australian resident (Residency – the resides test, 2019).

Simultaneously, it is mix of multiple factors of time and behaviour during in Australia will

identify residency status.

Case law: DEMPSEY v FC OF T, Administrative Appeals Tribunal of Australia, 29

May 2014

The Taxpayer Dempsey was directly employed on construction project as project

manager in Saudi Arabia with employment contract of indefinite duration. With context of this

duration, he lived in Saudi Arabia and contract lasted for three years. The main question was

from AAT that Mr Dempsey was Australian resident for income years of 2009 to 2010 so in this

context, his assessable income is comprised and derived through employment in Saudi Arabia for

those particular years (Dempsey and Commissioner of Taxation, 2019).

The decision by Administrative Appeals tribunal was satisfied that taxpayer was

domiciled in Australia with relevant years of income as he was not Australian resident during

2

regards of each relevant circumstances and facts. There should be account of numerous factors

for determining any reside such as:

Family and business/ employment ties

Social and living arrangements.

Intention or purpose of presence

Living and social arrangements.

The presence of family in Australia might indicate about residence in Australia but he

lives in Kuala Lumpur and doesn't visit in Australia in financial year and maintains social and

cultural arrangements in Malaysia. With context to intention there was absence of any opinion to

settle on permanent aspect as his behaviour is reflected in contrast to his initial decision. Minh's

family was staying in Australia so he was considered as foreign resident to Australia.

In the similar context, there is other factor to identify status of Minh which is physical

presence in Australia. For purpose of residing in Australia, there is requirement of displaying

behaviour over specific duration which is directly consistent for residing like habit, degree of

continuity and routine. The period one spend is not considered as decisive for purpose of

identifying status of residency. Usually six months is actual time for deciding that behaviour is

consistent for residing as it doesn't mean one lives for less than six months is replicated as

foreign resident and more than this are Australian resident (Residency – the resides test, 2019).

Simultaneously, it is mix of multiple factors of time and behaviour during in Australia will

identify residency status.

Case law: DEMPSEY v FC OF T, Administrative Appeals Tribunal of Australia, 29

May 2014

The Taxpayer Dempsey was directly employed on construction project as project

manager in Saudi Arabia with employment contract of indefinite duration. With context of this

duration, he lived in Saudi Arabia and contract lasted for three years. The main question was

from AAT that Mr Dempsey was Australian resident for income years of 2009 to 2010 so in this

context, his assessable income is comprised and derived through employment in Saudi Arabia for

those particular years (Dempsey and Commissioner of Taxation, 2019).

The decision by Administrative Appeals tribunal was satisfied that taxpayer was

domiciled in Australia with relevant years of income as he was not Australian resident during

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

these years. Furthermore, his permanent place of abode was also outside Australia and his

income through sources of Saudi Arabian in these years was not subjected for Australian income

tax.

Application and Conclusion for Minh's residency

With context to residency status of Minh's residency after weighing the facts reflected

that Minh did not reside in Australia in income year and his permanent place of abode was also

in Malaysia. For making this decision, number of relevant authorities was considered such as

DEMPSEY v FC OF T, Administrative Appeals Tribunal of Australia, 29 May 2014.

Henceforth, it could be concluded that particular matters involved questions related to degree and

fact and various facts with outcome of various conclusion to residency.

2. Explaining Minh's residency status impact assessability of Malaysian investment income and

business.

Minh is considered as foreign resident to Australia as he is active partner in business in

Kuala Lumpur along with substantial investment. Simultaneously, in income year 2017-20.18

(from June) he was absent from Australia and even he has not stated any opinion for settling in

Austrlia. This residency status will directly impact on assessability of Malaysian investment

income and business as this will decrease tax liability (Street, Lacey and Somoray, 2019).

Generally, all resident and non-resident organizations are capable for enjoying benefits of tax

treaties so these companies are entitled for claiming relief for double taxation with its

applicability.

Further, Malaysia has formed agreements with various countries with objective of

avoiding double taxation with allocation of taxing rights over bilateral income flows among

different treaty partners. Foreign income is subjected to Malaysian tax when it is remitted or

obtained to Malaysia through resident individual. Before assessment year 1995, income derived

through overseas and remitted to Malaysia through resident company which is usually

chargeable to income tax (Residence Status of Companies and Bodies of Persons, 2019). These

type of income gained is Malaysia is now exempted through income tax until business belongs to

insurance, air transport, shipping and banking. Furthermore, with year 1998, foreign income

obtained in Malaysia through unit trust is also exempted through tax.

Australia is having DTA with Malaysia and bilateral relief is with availability to any

resident with context of paying foreign tax such as Minh is paying. The credit amount will be

3

income through sources of Saudi Arabian in these years was not subjected for Australian income

tax.

Application and Conclusion for Minh's residency

With context to residency status of Minh's residency after weighing the facts reflected

that Minh did not reside in Australia in income year and his permanent place of abode was also

in Malaysia. For making this decision, number of relevant authorities was considered such as

DEMPSEY v FC OF T, Administrative Appeals Tribunal of Australia, 29 May 2014.

Henceforth, it could be concluded that particular matters involved questions related to degree and

fact and various facts with outcome of various conclusion to residency.

2. Explaining Minh's residency status impact assessability of Malaysian investment income and

business.

Minh is considered as foreign resident to Australia as he is active partner in business in

Kuala Lumpur along with substantial investment. Simultaneously, in income year 2017-20.18

(from June) he was absent from Australia and even he has not stated any opinion for settling in

Austrlia. This residency status will directly impact on assessability of Malaysian investment

income and business as this will decrease tax liability (Street, Lacey and Somoray, 2019).

Generally, all resident and non-resident organizations are capable for enjoying benefits of tax

treaties so these companies are entitled for claiming relief for double taxation with its

applicability.

Further, Malaysia has formed agreements with various countries with objective of

avoiding double taxation with allocation of taxing rights over bilateral income flows among

different treaty partners. Foreign income is subjected to Malaysian tax when it is remitted or

obtained to Malaysia through resident individual. Before assessment year 1995, income derived

through overseas and remitted to Malaysia through resident company which is usually

chargeable to income tax (Residence Status of Companies and Bodies of Persons, 2019). These

type of income gained is Malaysia is now exempted through income tax until business belongs to

insurance, air transport, shipping and banking. Furthermore, with year 1998, foreign income

obtained in Malaysia through unit trust is also exempted through tax.

Australia is having DTA with Malaysia and bilateral relief is with availability to any

resident with context of paying foreign tax such as Minh is paying. The credit amount will be

3

provided to lower of tax suffering with context to foreign country and Malaysian tax is directly

attributable to foreign income. For example, countries with absence of DTA with Malaysia, there

is unilateral relief is provided and restricted to lower half of tax is suffered in foreign country and

further Malaysian tax is attributable with reference to foreign income. There are various DTA

which provide interests on approved and long term loans along with approved industrial royalties

which are exempted through tax in Malaysia.

Henceforth, in this case Minh is foreign resident to Australia and resident in Malaysia

where his all business and investment income is there. In-spite of paying tax in Australia, his all

income will be fully taxable in Malaysia with application double taxation agreements.

4

attributable to foreign income. For example, countries with absence of DTA with Malaysia, there

is unilateral relief is provided and restricted to lower half of tax is suffered in foreign country and

further Malaysian tax is attributable with reference to foreign income. There are various DTA

which provide interests on approved and long term loans along with approved industrial royalties

which are exempted through tax in Malaysia.

Henceforth, in this case Minh is foreign resident to Australia and resident in Malaysia

where his all business and investment income is there. In-spite of paying tax in Australia, his all

income will be fully taxable in Malaysia with application double taxation agreements.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

QUESTION 2

ISSUES:

What alternatives are available to Penny over the assessments of the income generated

from sales of three town houses

Calculation of assessable income

Which is the correct outcomes or alternative for Penny

RULES AND LEGISLATION

Buying and selling of residential property: On the sale of home a person lives in under

the main resident exemption of Australian taxation the individual is not required to pay capital

gain taxes (CGT). But for the same income tax deduction can also not be claimed by the person

for selling home (Faccio and Xu, 2018). A second property such as holiday house or hobby

farm is subject to CGT.

Main resident And exemption: to qualify under this property must have dwelling on it

and person must have lived in the house. The dwelling is also considered as main resident when

family of the person lives in it, personal belonging are in their, its address is on mails are

delivered on its address (Jacob, 2018) . In case a person builds a home on the land he/she owns.

They can treat the land as their main resident for up to a period of 4 years before they move in,

provided that they must move in as soon as practicable after the constructionist is finished.

Capital gain tax: in case a capital asset is sold by a taxpayer such as reals estate or share

the person generally makes capital gain or loss. This the difference between cost of acquisition

of assets and the sales proceed of the assets. The capital gains is added in the assessable income

of the taxpayer and no separate tax is charged over the capital gains (Capital gains tax, 2018). It

is applicable for the properties and assets acquired on of after 20th September 1985 and a person

becomes the owners of the same after 20th August 1991.

Capital gain assets and exemptions: All the assets which are purchase after 20th September

1985 are subject to CGT unless specifically mentioned: CGT applied to real state, share, units

and similar investments, lease, goodwill, major improvements made on the land and collectables.

Exemption from CGT includes, main resident, car and motorcycle and depreciating assest.

5

ISSUES:

What alternatives are available to Penny over the assessments of the income generated

from sales of three town houses

Calculation of assessable income

Which is the correct outcomes or alternative for Penny

RULES AND LEGISLATION

Buying and selling of residential property: On the sale of home a person lives in under

the main resident exemption of Australian taxation the individual is not required to pay capital

gain taxes (CGT). But for the same income tax deduction can also not be claimed by the person

for selling home (Faccio and Xu, 2018). A second property such as holiday house or hobby

farm is subject to CGT.

Main resident And exemption: to qualify under this property must have dwelling on it

and person must have lived in the house. The dwelling is also considered as main resident when

family of the person lives in it, personal belonging are in their, its address is on mails are

delivered on its address (Jacob, 2018) . In case a person builds a home on the land he/she owns.

They can treat the land as their main resident for up to a period of 4 years before they move in,

provided that they must move in as soon as practicable after the constructionist is finished.

Capital gain tax: in case a capital asset is sold by a taxpayer such as reals estate or share

the person generally makes capital gain or loss. This the difference between cost of acquisition

of assets and the sales proceed of the assets. The capital gains is added in the assessable income

of the taxpayer and no separate tax is charged over the capital gains (Capital gains tax, 2018). It

is applicable for the properties and assets acquired on of after 20th September 1985 and a person

becomes the owners of the same after 20th August 1991.

Capital gain assets and exemptions: All the assets which are purchase after 20th September

1985 are subject to CGT unless specifically mentioned: CGT applied to real state, share, units

and similar investments, lease, goodwill, major improvements made on the land and collectables.

Exemption from CGT includes, main resident, car and motorcycle and depreciating assest.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cost base: this is the total sum of the original purchase price plus the incidental,

ownership and title cost. From which deductions are made for any government grants and

depreciable items. Incidental cost includes- stamp duty, legal fees marketing expenses etc. the

ownership cost consist of rate, land tax, maintenance, interest on home loan. Title cost is related

with expenses incurred on legal fees for defending the title on the property.

Alternative 1: House is held by her for less than a person for 12 months.

Calculation of cost base for Capital gain:

Cost base = Cost of owing+ All costs - FHOG & claimed depreciation

(rates, insurance, land tax, maintenance cost, interest on the money borrowed)

Calculation of capital gain or loss

Capital gain or loss = Sale price - cost base

Deduction from capital gains: A person can not claim deduction from the cost if the

property have not been used to produce assessable income.

Alternative 2: House is held by Penny for more than 12 months.

In case the property is held by the taxpayer for a person of more than 12 months than

that person get eligible under the discounting method of capital gain taxation in accordance with

ATO (Calculating the cost base for real estate, 2018). Under this method the taxpayer is entitled

to get a 50% discount off on the capital gain liability for individuals and 33.3% on for super

funds.

Calculation of capital gain tax liability:

= (capital proceeds – cost base) * 0.5

APPLICATION OF LAWS AND FACTS

Alternative 1: Property is sold be Penny immediately after completion of the homes:

Sale process of the old house: the sales process of $1 million is not liable for capital

gain taxes as this are generated from selling of the residential houses of Penny. The house is

determined as main resident of Penny for taxation purposes she and her family lived in the house

(Selling an asset and other CGT events, 2018). Here, penny must take the possession of the

house she has build for her family and she will be liable to capital gain tax exemption of the sales

proceed of the old residential house.

Sales proceed of old house, $1 million- capital gain tax exemption.

6

ownership and title cost. From which deductions are made for any government grants and

depreciable items. Incidental cost includes- stamp duty, legal fees marketing expenses etc. the

ownership cost consist of rate, land tax, maintenance, interest on home loan. Title cost is related

with expenses incurred on legal fees for defending the title on the property.

Alternative 1: House is held by her for less than a person for 12 months.

Calculation of cost base for Capital gain:

Cost base = Cost of owing+ All costs - FHOG & claimed depreciation

(rates, insurance, land tax, maintenance cost, interest on the money borrowed)

Calculation of capital gain or loss

Capital gain or loss = Sale price - cost base

Deduction from capital gains: A person can not claim deduction from the cost if the

property have not been used to produce assessable income.

Alternative 2: House is held by Penny for more than 12 months.

In case the property is held by the taxpayer for a person of more than 12 months than

that person get eligible under the discounting method of capital gain taxation in accordance with

ATO (Calculating the cost base for real estate, 2018). Under this method the taxpayer is entitled

to get a 50% discount off on the capital gain liability for individuals and 33.3% on for super

funds.

Calculation of capital gain tax liability:

= (capital proceeds – cost base) * 0.5

APPLICATION OF LAWS AND FACTS

Alternative 1: Property is sold be Penny immediately after completion of the homes:

Sale process of the old house: the sales process of $1 million is not liable for capital

gain taxes as this are generated from selling of the residential houses of Penny. The house is

determined as main resident of Penny for taxation purposes she and her family lived in the house

(Selling an asset and other CGT events, 2018). Here, penny must take the possession of the

house she has build for her family and she will be liable to capital gain tax exemption of the sales

proceed of the old residential house.

Sales proceed of old house, $1 million- capital gain tax exemption.

6

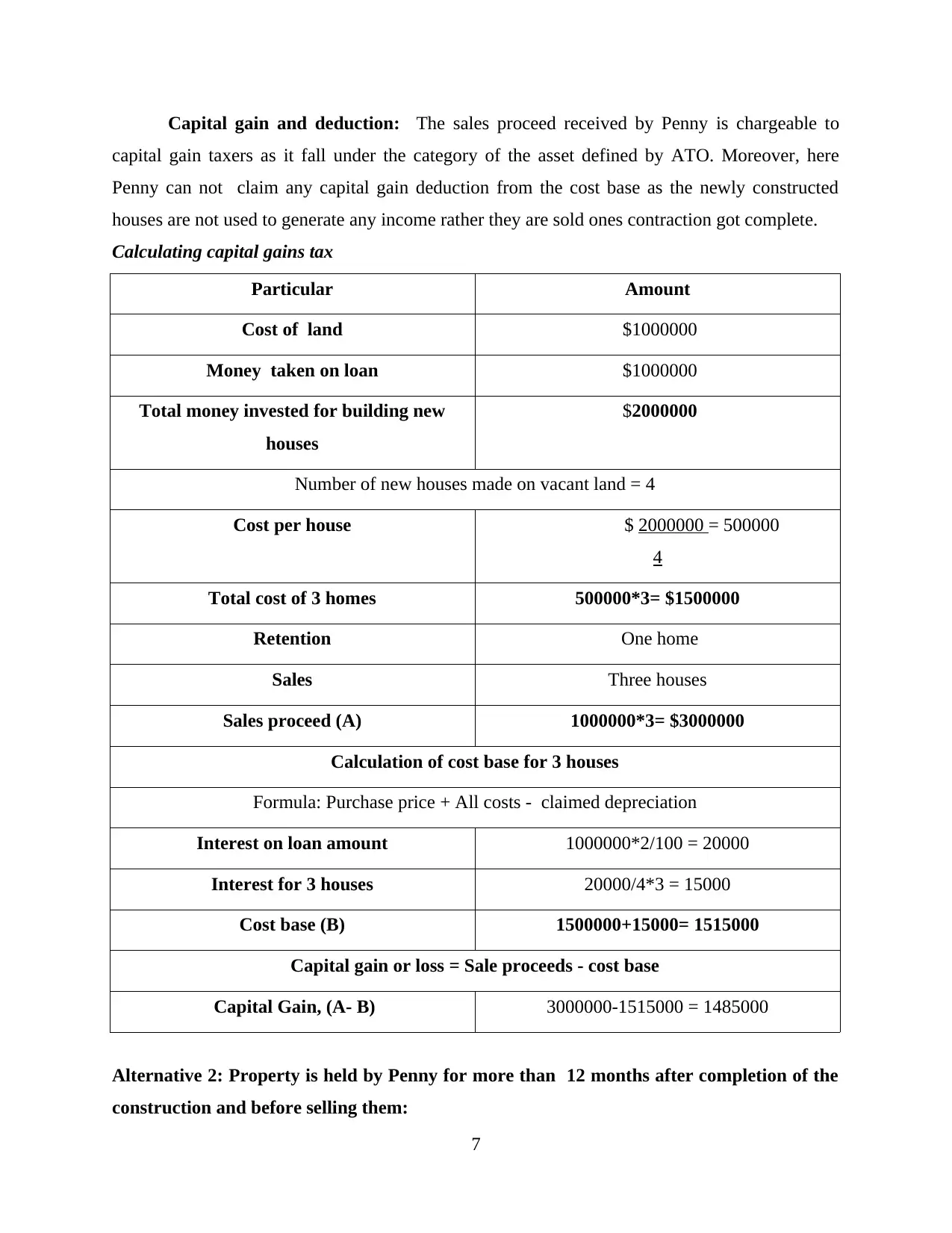

Capital gain and deduction: The sales proceed received by Penny is chargeable to

capital gain taxers as it fall under the category of the asset defined by ATO. Moreover, here

Penny can not claim any capital gain deduction from the cost base as the newly constructed

houses are not used to generate any income rather they are sold ones contraction got complete.

Calculating capital gains tax

Particular Amount

Cost of land $1000000

Money taken on loan $1000000

Total money invested for building new

houses

$2000000

Number of new houses made on vacant land = 4

Cost per house $ 2000000 = 500000

4

Total cost of 3 homes 500000*3= $1500000

Retention One home

Sales Three houses

Sales proceed (A) 1000000*3= $3000000

Calculation of cost base for 3 houses

Formula: Purchase price + All costs - claimed depreciation

Interest on loan amount 1000000*2/100 = 20000

Interest for 3 houses 20000/4*3 = 15000

Cost base (B) 1500000+15000= 1515000

Capital gain or loss = Sale proceeds - cost base

Capital Gain, (A- B) 3000000-1515000 = 1485000

Alternative 2: Property is held by Penny for more than 12 months after completion of the

construction and before selling them:

7

capital gain taxers as it fall under the category of the asset defined by ATO. Moreover, here

Penny can not claim any capital gain deduction from the cost base as the newly constructed

houses are not used to generate any income rather they are sold ones contraction got complete.

Calculating capital gains tax

Particular Amount

Cost of land $1000000

Money taken on loan $1000000

Total money invested for building new

houses

$2000000

Number of new houses made on vacant land = 4

Cost per house $ 2000000 = 500000

4

Total cost of 3 homes 500000*3= $1500000

Retention One home

Sales Three houses

Sales proceed (A) 1000000*3= $3000000

Calculation of cost base for 3 houses

Formula: Purchase price + All costs - claimed depreciation

Interest on loan amount 1000000*2/100 = 20000

Interest for 3 houses 20000/4*3 = 15000

Cost base (B) 1500000+15000= 1515000

Capital gain or loss = Sale proceeds - cost base

Capital Gain, (A- B) 3000000-1515000 = 1485000

Alternative 2: Property is held by Penny for more than 12 months after completion of the

construction and before selling them:

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

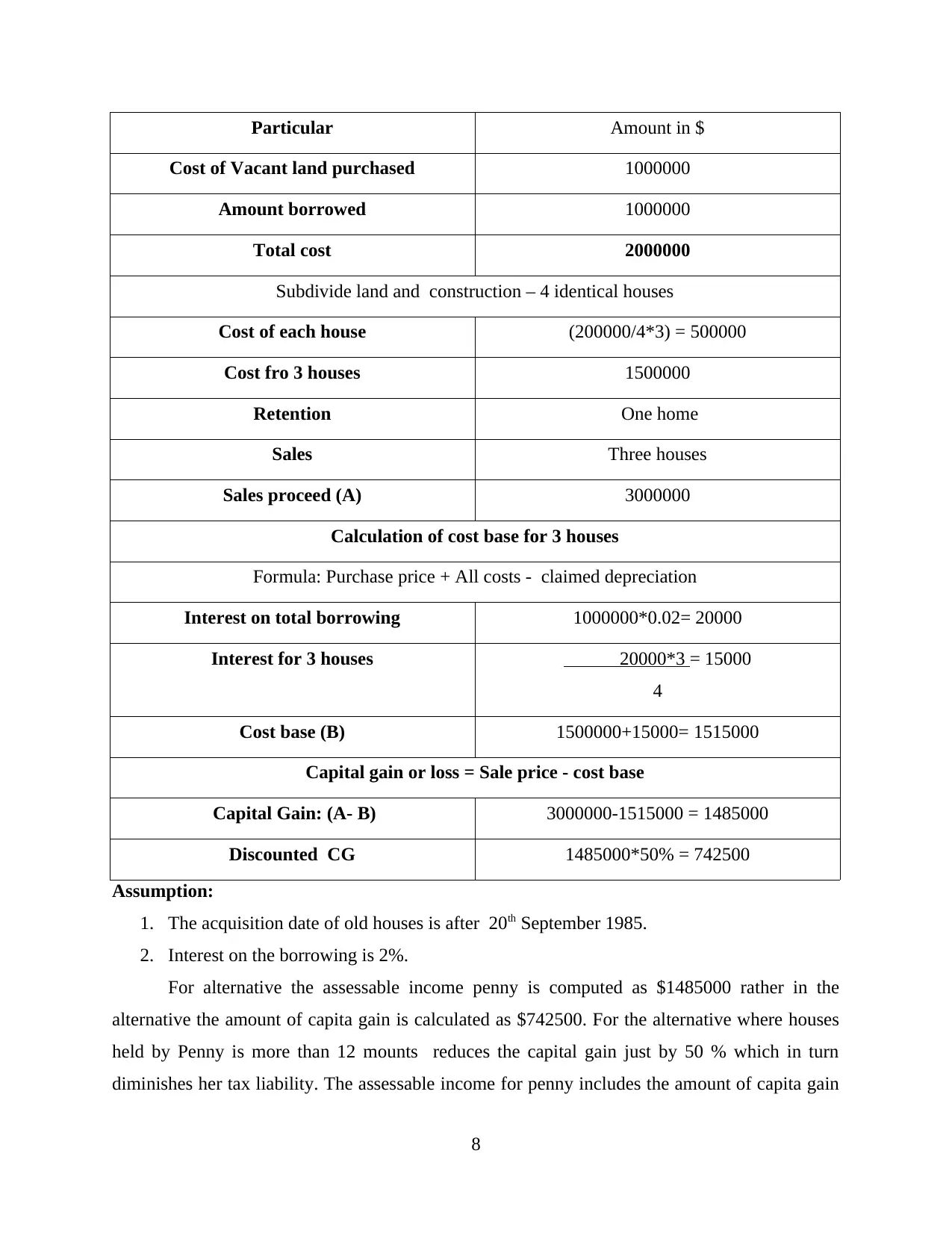

Particular Amount in $

Cost of Vacant land purchased 1000000

Amount borrowed 1000000

Total cost 2000000

Subdivide land and construction – 4 identical houses

Cost of each house (200000/4*3) = 500000

Cost fro 3 houses 1500000

Retention One home

Sales Three houses

Sales proceed (A) 3000000

Calculation of cost base for 3 houses

Formula: Purchase price + All costs - claimed depreciation

Interest on total borrowing 1000000*0.02= 20000

Interest for 3 houses 20000*3 = 15000

4

Cost base (B) 1500000+15000= 1515000

Capital gain or loss = Sale price - cost base

Capital Gain: (A- B) 3000000-1515000 = 1485000

Discounted CG 1485000*50% = 742500

Assumption:

1. The acquisition date of old houses is after 20th September 1985.

2. Interest on the borrowing is 2%.

For alternative the assessable income penny is computed as $1485000 rather in the

alternative the amount of capita gain is calculated as $742500. For the alternative where houses

held by Penny is more than 12 mounts reduces the capital gain just by 50 % which in turn

diminishes her tax liability. The assessable income for penny includes the amount of capita gain

8

Cost of Vacant land purchased 1000000

Amount borrowed 1000000

Total cost 2000000

Subdivide land and construction – 4 identical houses

Cost of each house (200000/4*3) = 500000

Cost fro 3 houses 1500000

Retention One home

Sales Three houses

Sales proceed (A) 3000000

Calculation of cost base for 3 houses

Formula: Purchase price + All costs - claimed depreciation

Interest on total borrowing 1000000*0.02= 20000

Interest for 3 houses 20000*3 = 15000

4

Cost base (B) 1500000+15000= 1515000

Capital gain or loss = Sale price - cost base

Capital Gain: (A- B) 3000000-1515000 = 1485000

Discounted CG 1485000*50% = 742500

Assumption:

1. The acquisition date of old houses is after 20th September 1985.

2. Interest on the borrowing is 2%.

For alternative the assessable income penny is computed as $1485000 rather in the

alternative the amount of capita gain is calculated as $742500. For the alternative where houses

held by Penny is more than 12 mounts reduces the capital gain just by 50 % which in turn

diminishes her tax liability. The assessable income for penny includes the amount of capita gain

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

in the incomes and on the total amount tax will be charged as per the income tax slab of the

relevant time.

CONCLUSION

From the above calculation of two alternatives presented for calculation of capital gain

taxes on the sales proceeds of 4 different houses it is assessed that sales proceeds received from

the sales of the house is not taxable under CGT when the home is acquired after 20th September

2014. Out of the two alternative 2nd one is more preferable as under this the assessable incomes is

less than it is calculated in alternative one. With a less assessable income the tax liability of

Penny automatically gets reduced. Under the alternative two 50% of discount in the CGT

liability s available taxpayer which is more beneficial to Penny.

9

relevant time.

CONCLUSION

From the above calculation of two alternatives presented for calculation of capital gain

taxes on the sales proceeds of 4 different houses it is assessed that sales proceeds received from

the sales of the house is not taxable under CGT when the home is acquired after 20th September

2014. Out of the two alternative 2nd one is more preferable as under this the assessable incomes is

less than it is calculated in alternative one. With a less assessable income the tax liability of

Penny automatically gets reduced. Under the alternative two 50% of discount in the CGT

liability s available taxpayer which is more beneficial to Penny.

9

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.