Australia Taxation Law: Benefits, Income, and Deductions Analysis

VerifiedAdded on 2020/02/19

|10

|2328

|35

Homework Assignment

AI Summary

This assignment analyzes various aspects of Australian taxation law. It begins by examining the tax treatment of different scenarios, including frequent flyer benefits, damage payments for capital assets, free holiday packages, return of excess funds, payments to sports persons, expenses related to building apprentices, short course expenses, work makeup and dresses, and home-to-office and employer-to-employer expenses. Each scenario is assessed according to relevant tax rulings and legislation. The assignment then calculates the net taxable income for an individual named Manpreet for the 2016/17 financial year, including salary, income from a trust, deductions, tax payable, and low-income tax offsets. The document also includes references to relevant Australian tax legislation and rulings, as well as academic sources.

Running head: AUSTRALIA TAXATION LAW

Australia Taxation Law

Name of the University:

Name of the Student:

Authors Note:

Australia Taxation Law

Name of the University:

Name of the Student:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUSTRALIA TAXATION LAW

Table of Contents

Answer for the Question 1: Depicting the treatment for tax purposes under Australian Tax

Law.............................................................................................................................................2

Q i) Benefits provided by Airline Company to frequent flyers.................................................2

Q ii) Damage payment for Capital asset....................................................................................2

Q iii) Free holiday package........................................................................................................3

Q iv) Return of excess funds......................................................................................................4

Q v) Payment to sports person...................................................................................................4

Q vi) Expense related to building apprentices...........................................................................4

Q vii) Short course expense for becoming art director..............................................................5

Q viii) Work Makeup and dresses..............................................................................................5

Q ix) Expenses between home and office..................................................................................6

Q x) Expenses between one employer to another employer......................................................6

Answer to Question 2: Net taxable income of Manpreet for the year 2016/17 financial year. .7

Reference..................................................................................................................................10

Table of Contents

Answer for the Question 1: Depicting the treatment for tax purposes under Australian Tax

Law.............................................................................................................................................2

Q i) Benefits provided by Airline Company to frequent flyers.................................................2

Q ii) Damage payment for Capital asset....................................................................................2

Q iii) Free holiday package........................................................................................................3

Q iv) Return of excess funds......................................................................................................4

Q v) Payment to sports person...................................................................................................4

Q vi) Expense related to building apprentices...........................................................................4

Q vii) Short course expense for becoming art director..............................................................5

Q viii) Work Makeup and dresses..............................................................................................5

Q ix) Expenses between home and office..................................................................................6

Q x) Expenses between one employer to another employer......................................................6

Answer to Question 2: Net taxable income of Manpreet for the year 2016/17 financial year. .7

Reference..................................................................................................................................10

2AUSTRALIA TAXATION LAW

Answer for the Question 1: Depicting the treatment for tax purposes under Australian

Tax Law

Q i) Benefits provided by Airline Company to frequent flyers

Relevant reward points are provided to the customer on the basis of frequent flying

conducted by the business analyst. Therefore, the benefit gained from reward points cannot

be considered under taxable income or Fringe benefit tax. This is mainly because the overall

benefits provided to the business analyst is mainly due to the frequent playing that has been

conducted by the individual. According to the taxation ruling of TR 1999/6, any kind of

rewards for benefits that is received by the customer by the airline company cannot be treated

as a taxable income. However, there are some scenarios where fringe benefit tax could be

associated with the reward points are provided by the airline company. The first and foremost

point is the family relationship between employer and employee, where reward points is

provided to the employee in context with their employment. The second point mainly states

that reward points that are provided due to some particular arrangement could be considered

under fringe benefit tax1. Therefore, the scenario does not represent any kind of fringe benefit

tax or taxable income for the benefits provided by Airline Company.

Q ii) Damage payment for Capital asset

There is relevant payment for Capital Asset damage that was conducted by the

customer. According to the Australian taxation law, relevant payments for damages are not

considered under the taxation method. However, there are certain measures that need to be

1 Cheshire, Lynda, Jo-Anne Everingham, and Geoffrey Lawrence. "Governing the impacts of

mining and the impacts of mining governance: Challenges for rural and regional local

governments in Australia." Journal of Rural Studies36 (2014): 330-339.

Answer for the Question 1: Depicting the treatment for tax purposes under Australian

Tax Law

Q i) Benefits provided by Airline Company to frequent flyers

Relevant reward points are provided to the customer on the basis of frequent flying

conducted by the business analyst. Therefore, the benefit gained from reward points cannot

be considered under taxable income or Fringe benefit tax. This is mainly because the overall

benefits provided to the business analyst is mainly due to the frequent playing that has been

conducted by the individual. According to the taxation ruling of TR 1999/6, any kind of

rewards for benefits that is received by the customer by the airline company cannot be treated

as a taxable income. However, there are some scenarios where fringe benefit tax could be

associated with the reward points are provided by the airline company. The first and foremost

point is the family relationship between employer and employee, where reward points is

provided to the employee in context with their employment. The second point mainly states

that reward points that are provided due to some particular arrangement could be considered

under fringe benefit tax1. Therefore, the scenario does not represent any kind of fringe benefit

tax or taxable income for the benefits provided by Airline Company.

Q ii) Damage payment for Capital asset

There is relevant payment for Capital Asset damage that was conducted by the

customer. According to the Australian taxation law, relevant payments for damages are not

considered under the taxation method. However, there are certain measures that need to be

1 Cheshire, Lynda, Jo-Anne Everingham, and Geoffrey Lawrence. "Governing the impacts of

mining and the impacts of mining governance: Challenges for rural and regional local

governments in Australia." Journal of Rural Studies36 (2014): 330-339.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUSTRALIA TAXATION LAW

fulfilled by the compensation receiver before excluding the damage payment. Firstly, the

asset should be used adequately by the receiver, which depicts that the asset acts as a capital

in the business. The second measure includes that depreciation of the Asset needs to be

included in the accounts book and revamping of the assets needs to be conducted. Therefore,

in the scenario then money received for the damaged crane is not considered under the

taxable income, unless it violates the above-mentioned criteria’s2.

Q iii) Free holiday package

The alcohol supplier as mainly given a gift of holiday package to the nightclub

manager, which directly indicates that benefits is provided to the individual. According to the

Australian taxation method, Small gift are mainly exempted from the taxation process, where

is big and expensive are subject to tax treatment. The Australian taxation method also state

that irrelevant gift is neither considered under exemption to rule non exempted income.

However, with relevant valuation an individual could identify that whether the gift is

considered to be taxable or not. In the relevant scenario, the gift provided by the supplier to

the nightclub manager amounts is considered to be high value. Therefore, it is considered

under taxable amount of the night club manager3.

2 Davis, Angela K., David A. Guenther, Linda K. Krull, and Brian M. Williams. "Do socially

responsible firms pay more taxes?." The Accounting Review 91, no. 1 (2015): 47-68.

3 Richardson, Grant, Grantley Taylor, and Roman Lanis. "The impact of board of director

oversight characteristics on corporate tax aggressiveness: An empirical analysis." Journal of

Accounting and Public Policy 32, no. 3 (2013): 68-88.

fulfilled by the compensation receiver before excluding the damage payment. Firstly, the

asset should be used adequately by the receiver, which depicts that the asset acts as a capital

in the business. The second measure includes that depreciation of the Asset needs to be

included in the accounts book and revamping of the assets needs to be conducted. Therefore,

in the scenario then money received for the damaged crane is not considered under the

taxable income, unless it violates the above-mentioned criteria’s2.

Q iii) Free holiday package

The alcohol supplier as mainly given a gift of holiday package to the nightclub

manager, which directly indicates that benefits is provided to the individual. According to the

Australian taxation method, Small gift are mainly exempted from the taxation process, where

is big and expensive are subject to tax treatment. The Australian taxation method also state

that irrelevant gift is neither considered under exemption to rule non exempted income.

However, with relevant valuation an individual could identify that whether the gift is

considered to be taxable or not. In the relevant scenario, the gift provided by the supplier to

the nightclub manager amounts is considered to be high value. Therefore, it is considered

under taxable amount of the night club manager3.

2 Davis, Angela K., David A. Guenther, Linda K. Krull, and Brian M. Williams. "Do socially

responsible firms pay more taxes?." The Accounting Review 91, no. 1 (2015): 47-68.

3 Richardson, Grant, Grantley Taylor, and Roman Lanis. "The impact of board of director

oversight characteristics on corporate tax aggressiveness: An empirical analysis." Journal of

Accounting and Public Policy 32, no. 3 (2013): 68-88.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUSTRALIA TAXATION LAW

Q iv) Return of excess funds

The situation mainly states that relevant fund is returned to the members due to excess

collection for purchase of additional canoes. The overall total income includes the payments

conducted to canoes, which is used in deriving the taxable income of the members.

According to the taxation law in Australia, relevant personal expenses conducted by

individual and not deductible in taxable amount. Therefore, any kind of returns conducted on

personal expenses will not be considered under taxable income, as expenses are not excluded

from the taxation process. Hence, the evaluation of the scenario mainly states that return of

the funds will not be included as taxable income.

Q v) Payment to sports person

According to the Australian taxation ruling TR 1999/17, any sports person receiving

money from different parties is considered under taxable income. Under the taxation method

relevant income that is generated by the sports person needs to be considered under taxable

income. Therefore, the event conducted by TV station to the sportsperson is directly

considered under taxable income. There is no exception of any kind for the income that is

generated by sports person, which could be considered as a deduction and the taxable

amount. The taxation rule directly specifies the adequate tax, which needs to be way to the

Australian taxation authorities.

Q vi) Expense related to building apprentices

The situation mainly states that relevant expenses are been conducted for building

apprentice due to its building qualification. This mainly states that the building apprentice is

directly involved in commencing the building work, which under the taxation ruling of TR

95/22 is considered under the reimbursement, allowance and compensation provided by the

project manager. The ruling directly states that relevant employees of the building could be

Q iv) Return of excess funds

The situation mainly states that relevant fund is returned to the members due to excess

collection for purchase of additional canoes. The overall total income includes the payments

conducted to canoes, which is used in deriving the taxable income of the members.

According to the taxation law in Australia, relevant personal expenses conducted by

individual and not deductible in taxable amount. Therefore, any kind of returns conducted on

personal expenses will not be considered under taxable income, as expenses are not excluded

from the taxation process. Hence, the evaluation of the scenario mainly states that return of

the funds will not be included as taxable income.

Q v) Payment to sports person

According to the Australian taxation ruling TR 1999/17, any sports person receiving

money from different parties is considered under taxable income. Under the taxation method

relevant income that is generated by the sports person needs to be considered under taxable

income. Therefore, the event conducted by TV station to the sportsperson is directly

considered under taxable income. There is no exception of any kind for the income that is

generated by sports person, which could be considered as a deduction and the taxable

amount. The taxation rule directly specifies the adequate tax, which needs to be way to the

Australian taxation authorities.

Q vi) Expense related to building apprentices

The situation mainly states that relevant expenses are been conducted for building

apprentice due to its building qualification. This mainly states that the building apprentice is

directly involved in commencing the building work, which under the taxation ruling of TR

95/22 is considered under the reimbursement, allowance and compensation provided by the

project manager. The ruling directly states that relevant employees of the building could be

5AUSTRALIA TAXATION LAW

identified, as leaders, trainees, apprentices, carpenters, supervisors, project managers, and

many more who are responsible for completing the building structure. Therefore, evaluation

of the situation maybe indicates that the apprentice is considered to be an employee in the

building under the taxation rule of TR 95/224.

Q vii) Short course expense for becoming art director

There is relevant short term course that is conducted by an individual for becoming an

art director in future. According to the Australian taxation law, educational courses that are

conducted by individuals, which do not support in enhancing their career, are not included as

deduction in taxable income. however, the Australian taxation law also states that relevant

short term Education courses that are conducted by an individual enhancing the career growth

can be taken into consideration. There are relevant computation for these expenses, which

helps in identifying the expense as a deductible or not. Educating through software and

module, short term fees for the course, involving of all the travelling cost. The above scenario

mainly states that an individual has spent for a short term course for becoming an art director,

which is deductible from its taxable income.

Q viii) Work Makeup and dresses

Expenses are been conducted on makeup and dresses, which are deemed as work

related expenses. According to the Australian taxation law, expenses made on performing

Artist are detectable in nature. However, there are certain rules that need to be maintained

while determining the performing artist. The performing artist could be considered as any one

of the performers as variety address, circus performer, singer, dancer, magician, and an actor.

The current scenario directly states that expenses are conducted on makeup and dresses,

4 Gitman, Lawrence J., Roger Juchau, and Jack Flanagan. Principles of managerial finance.

Pearson Higher Education AU, 2015.

identified, as leaders, trainees, apprentices, carpenters, supervisors, project managers, and

many more who are responsible for completing the building structure. Therefore, evaluation

of the situation maybe indicates that the apprentice is considered to be an employee in the

building under the taxation rule of TR 95/224.

Q vii) Short course expense for becoming art director

There is relevant short term course that is conducted by an individual for becoming an

art director in future. According to the Australian taxation law, educational courses that are

conducted by individuals, which do not support in enhancing their career, are not included as

deduction in taxable income. however, the Australian taxation law also states that relevant

short term Education courses that are conducted by an individual enhancing the career growth

can be taken into consideration. There are relevant computation for these expenses, which

helps in identifying the expense as a deductible or not. Educating through software and

module, short term fees for the course, involving of all the travelling cost. The above scenario

mainly states that an individual has spent for a short term course for becoming an art director,

which is deductible from its taxable income.

Q viii) Work Makeup and dresses

Expenses are been conducted on makeup and dresses, which are deemed as work

related expenses. According to the Australian taxation law, expenses made on performing

Artist are detectable in nature. However, there are certain rules that need to be maintained

while determining the performing artist. The performing artist could be considered as any one

of the performers as variety address, circus performer, singer, dancer, magician, and an actor.

The current scenario directly states that expenses are conducted on makeup and dresses,

4 Gitman, Lawrence J., Roger Juchau, and Jack Flanagan. Principles of managerial finance.

Pearson Higher Education AU, 2015.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUSTRALIA TAXATION LAW

where it could be assume that expenses are conducted on an artist. Therefore, these expenses

are deductible in nature and could be excluded from the taxable income5.

Q ix) Expenses between home and office

An expense that is related to travelling from home to work is mainly considered to be

an office activity, which is directly deducted from the taxable income. However there is not

enough evidence in determining, which type of expenses is been conducted in this scenario.

Therefore, if the expense is conducted for official purposes then it are deductible in nature

and if not it cannot be deducted from the taxable income. Nevertheless, we assume that the

overall expenses are conducted for official purposes, where it could be used for deducting

from the taxable income.

Q x) Expenses between one employer to another employer

The relevant expenses conducted while travelling from one employer to another is

mainly determined as an official expense. Therefore, these types of expenses are directly

deductible in nature, where it could be used in reducing the taxable amount of an individual.

According to the Australian taxation authority, expenses conducted for official purposes are

deductible in nature, which could reduce the overall taxable income. However, the scenario

states that relevant travel expenses are been conducted from travelling to one employer to

another, which is currently not deductible from the income of amount. Travelling from

employee to employer is mainly considered a personal expense, where official work is not

5 Lal, Anita, Ana Maria Mantilla-Herrera, Lennert Veerman, Kathryn Backholer, Gary Sacks,

Marjory Moodie, Mohammad Siahpush, Rob Carter, and Anna Peeters. "Modelled health

benefits of a sugar-sweetened beverage tax across different socioeconomic groups in

Australia: A cost-effectiveness and equity analysis." PLoS medicine 14, no. 6 (2017):

e1002326.

where it could be assume that expenses are conducted on an artist. Therefore, these expenses

are deductible in nature and could be excluded from the taxable income5.

Q ix) Expenses between home and office

An expense that is related to travelling from home to work is mainly considered to be

an office activity, which is directly deducted from the taxable income. However there is not

enough evidence in determining, which type of expenses is been conducted in this scenario.

Therefore, if the expense is conducted for official purposes then it are deductible in nature

and if not it cannot be deducted from the taxable income. Nevertheless, we assume that the

overall expenses are conducted for official purposes, where it could be used for deducting

from the taxable income.

Q x) Expenses between one employer to another employer

The relevant expenses conducted while travelling from one employer to another is

mainly determined as an official expense. Therefore, these types of expenses are directly

deductible in nature, where it could be used in reducing the taxable amount of an individual.

According to the Australian taxation authority, expenses conducted for official purposes are

deductible in nature, which could reduce the overall taxable income. However, the scenario

states that relevant travel expenses are been conducted from travelling to one employer to

another, which is currently not deductible from the income of amount. Travelling from

employee to employer is mainly considered a personal expense, where official work is not

5 Lal, Anita, Ana Maria Mantilla-Herrera, Lennert Veerman, Kathryn Backholer, Gary Sacks,

Marjory Moodie, Mohammad Siahpush, Rob Carter, and Anna Peeters. "Modelled health

benefits of a sugar-sweetened beverage tax across different socioeconomic groups in

Australia: A cost-effectiveness and equity analysis." PLoS medicine 14, no. 6 (2017):

e1002326.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUSTRALIA TAXATION LAW

been conducted by the individual. It is mainly assume that the individual is travelling from

employer to employer for getting a job6.

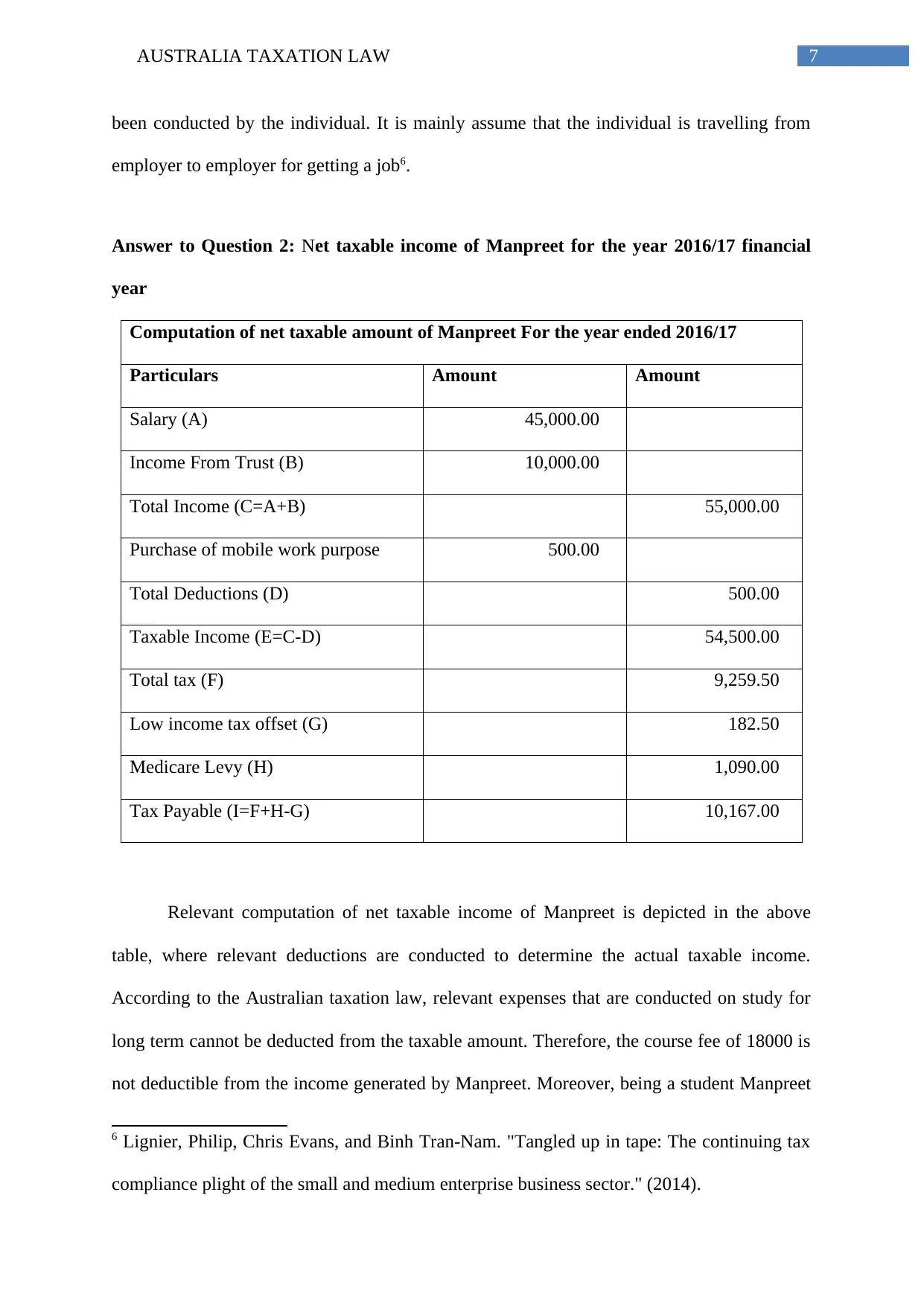

Answer to Question 2: Net taxable income of Manpreet for the year 2016/17 financial

year

Computation of net taxable amount of Manpreet For the year ended 2016/17

Particulars Amount Amount

Salary (A) 45,000.00

Income From Trust (B) 10,000.00

Total Income (C=A+B) 55,000.00

Purchase of mobile work purpose 500.00

Total Deductions (D) 500.00

Taxable Income (E=C-D) 54,500.00

Total tax (F) 9,259.50

Low income tax offset (G) 182.50

Medicare Levy (H) 1,090.00

Tax Payable (I=F+H-G) 10,167.00

Relevant computation of net taxable income of Manpreet is depicted in the above

table, where relevant deductions are conducted to determine the actual taxable income.

According to the Australian taxation law, relevant expenses that are conducted on study for

long term cannot be deducted from the taxable amount. Therefore, the course fee of 18000 is

not deductible from the income generated by Manpreet. Moreover, being a student Manpreet

6 Lignier, Philip, Chris Evans, and Binh Tran-Nam. "Tangled up in tape: The continuing tax

compliance plight of the small and medium enterprise business sector." (2014).

been conducted by the individual. It is mainly assume that the individual is travelling from

employer to employer for getting a job6.

Answer to Question 2: Net taxable income of Manpreet for the year 2016/17 financial

year

Computation of net taxable amount of Manpreet For the year ended 2016/17

Particulars Amount Amount

Salary (A) 45,000.00

Income From Trust (B) 10,000.00

Total Income (C=A+B) 55,000.00

Purchase of mobile work purpose 500.00

Total Deductions (D) 500.00

Taxable Income (E=C-D) 54,500.00

Total tax (F) 9,259.50

Low income tax offset (G) 182.50

Medicare Levy (H) 1,090.00

Tax Payable (I=F+H-G) 10,167.00

Relevant computation of net taxable income of Manpreet is depicted in the above

table, where relevant deductions are conducted to determine the actual taxable income.

According to the Australian taxation law, relevant expenses that are conducted on study for

long term cannot be deducted from the taxable amount. Therefore, the course fee of 18000 is

not deductible from the income generated by Manpreet. Moreover, being a student Manpreet

6 Lignier, Philip, Chris Evans, and Binh Tran-Nam. "Tangled up in tape: The continuing tax

compliance plight of the small and medium enterprise business sector." (2014).

8AUSTRALIA TAXATION LAW

also earned $45,000 in 2016-17 fiscal years7. From the evaluation of the oral scenario

Manpreet has stayed in Australia for more than 6 months, which directly states that she

becomes an Australian resident for tax purposes. Manpreet also collects relevant funds from

Charitable Trust, which is considered as a taxable income according to the Australian

taxation law. Nevertheless, Manpreet paid $1,000 in tax in India for the charitable amount

provided to her. The tax deduction will not include tax paid in India, as there is no relevant

treaty between Australia and India regarding individual taxation.

According to the Australian taxation rule, any kind of expenses that is conducted on

educational purposes, which does not increase the expectancy of income from the job is not

considered as deductible expenses. Therefore, the expenses conducted by Manpreet for

educational purpose of computer course is not deductible under the Australian taxation law,

as it did not help in any kind of in criminal income8. The relevant cases that could be

evaluated to understand the restrictions that are imposed by the Australian tax organisation

(ATO) are depicted as follows.

Ronpibon Tin NL v. FC of T (1949)

Lunney v. FC of T; Hayley v. FC of T (1958) 100 CLR 478; (1958)

FC of T v. M I Roberts 92 ATC 4787

The above depicted cases mainly represent view all deductions that would be conducted

on taxable income.

7 Current Australian Incometax Rates - Resident And Non-Resident | Exfin - The Australian

Expatriate's Gateway (2017) Exfin.com <https://www.exfin.com/australian-tax-rates>

8 Low Income Earners (2017) Ato.gov.au https://www.ato.gov.au/Individuals/Income-and-

deductions/Offsets-and-rebates/Low-income-earners/

also earned $45,000 in 2016-17 fiscal years7. From the evaluation of the oral scenario

Manpreet has stayed in Australia for more than 6 months, which directly states that she

becomes an Australian resident for tax purposes. Manpreet also collects relevant funds from

Charitable Trust, which is considered as a taxable income according to the Australian

taxation law. Nevertheless, Manpreet paid $1,000 in tax in India for the charitable amount

provided to her. The tax deduction will not include tax paid in India, as there is no relevant

treaty between Australia and India regarding individual taxation.

According to the Australian taxation rule, any kind of expenses that is conducted on

educational purposes, which does not increase the expectancy of income from the job is not

considered as deductible expenses. Therefore, the expenses conducted by Manpreet for

educational purpose of computer course is not deductible under the Australian taxation law,

as it did not help in any kind of in criminal income8. The relevant cases that could be

evaluated to understand the restrictions that are imposed by the Australian tax organisation

(ATO) are depicted as follows.

Ronpibon Tin NL v. FC of T (1949)

Lunney v. FC of T; Hayley v. FC of T (1958) 100 CLR 478; (1958)

FC of T v. M I Roberts 92 ATC 4787

The above depicted cases mainly represent view all deductions that would be conducted

on taxable income.

7 Current Australian Incometax Rates - Resident And Non-Resident | Exfin - The Australian

Expatriate's Gateway (2017) Exfin.com <https://www.exfin.com/australian-tax-rates>

8 Low Income Earners (2017) Ato.gov.au https://www.ato.gov.au/Individuals/Income-and-

deductions/Offsets-and-rebates/Low-income-earners/

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUSTRALIA TAXATION LAW

Reference

Cheshire, Lynda, Jo-Anne Everingham, and Geoffrey Lawrence. "Governing the impacts of

mining and the impacts of mining governance: Challenges for rural and regional local

governments in Australia." Journal of Rural Studies36 (2014): 330-339.

Current Australian Incometax Rates - Resident And Non-Resident | Exfin - The Australian

Expatriate's Gateway (2017) Exfin.com <https://www.exfin.com/australian-tax-rates>

Davis, Angela K., David A. Guenther, Linda K. Krull, and Brian M. Williams. "Do socially

responsible firms pay more taxes?." The Accounting Review 91, no. 1 (2015): 47-68.

Gitman, Lawrence J., Roger Juchau, and Jack Flanagan. Principles of managerial finance.

Pearson Higher Education AU, 2015.

Lal, Anita, Ana Maria Mantilla-Herrera, Lennert Veerman, Kathryn Backholer, Gary Sacks,

Marjory Moodie, Mohammad Siahpush, Rob Carter, and Anna Peeters. "Modelled health

benefits of a sugar-sweetened beverage tax across different socioeconomic groups in

Australia: A cost-effectiveness and equity analysis." PLoS medicine 14, no. 6 (2017):

e1002326.

Lignier, Philip, Chris Evans, and Binh Tran-Nam. "Tangled up in tape: The continuing tax

compliance plight of the small and medium enterprise business sector." (2014).

Low Income Earners (2017) Ato.gov.au https://www.ato.gov.au/Individuals/Income-and-

deductions/Offsets-and-rebates/Low-income-earners/

Richardson, Grant, Grantley Taylor, and Roman Lanis. "The impact of board of director

oversight characteristics on corporate tax aggressiveness: An empirical analysis." Journal of

Accounting and Public Policy 32, no. 3 (2013): 68-88.

Reference

Cheshire, Lynda, Jo-Anne Everingham, and Geoffrey Lawrence. "Governing the impacts of

mining and the impacts of mining governance: Challenges for rural and regional local

governments in Australia." Journal of Rural Studies36 (2014): 330-339.

Current Australian Incometax Rates - Resident And Non-Resident | Exfin - The Australian

Expatriate's Gateway (2017) Exfin.com <https://www.exfin.com/australian-tax-rates>

Davis, Angela K., David A. Guenther, Linda K. Krull, and Brian M. Williams. "Do socially

responsible firms pay more taxes?." The Accounting Review 91, no. 1 (2015): 47-68.

Gitman, Lawrence J., Roger Juchau, and Jack Flanagan. Principles of managerial finance.

Pearson Higher Education AU, 2015.

Lal, Anita, Ana Maria Mantilla-Herrera, Lennert Veerman, Kathryn Backholer, Gary Sacks,

Marjory Moodie, Mohammad Siahpush, Rob Carter, and Anna Peeters. "Modelled health

benefits of a sugar-sweetened beverage tax across different socioeconomic groups in

Australia: A cost-effectiveness and equity analysis." PLoS medicine 14, no. 6 (2017):

e1002326.

Lignier, Philip, Chris Evans, and Binh Tran-Nam. "Tangled up in tape: The continuing tax

compliance plight of the small and medium enterprise business sector." (2014).

Low Income Earners (2017) Ato.gov.au https://www.ato.gov.au/Individuals/Income-and-

deductions/Offsets-and-rebates/Low-income-earners/

Richardson, Grant, Grantley Taylor, and Roman Lanis. "The impact of board of director

oversight characteristics on corporate tax aggressiveness: An empirical analysis." Journal of

Accounting and Public Policy 32, no. 3 (2013): 68-88.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.