Taxation Law Assignment on Residential Status and Partnership Income

VerifiedAdded on 2021/01/01

|7

|1443

|382

Homework Assignment

AI Summary

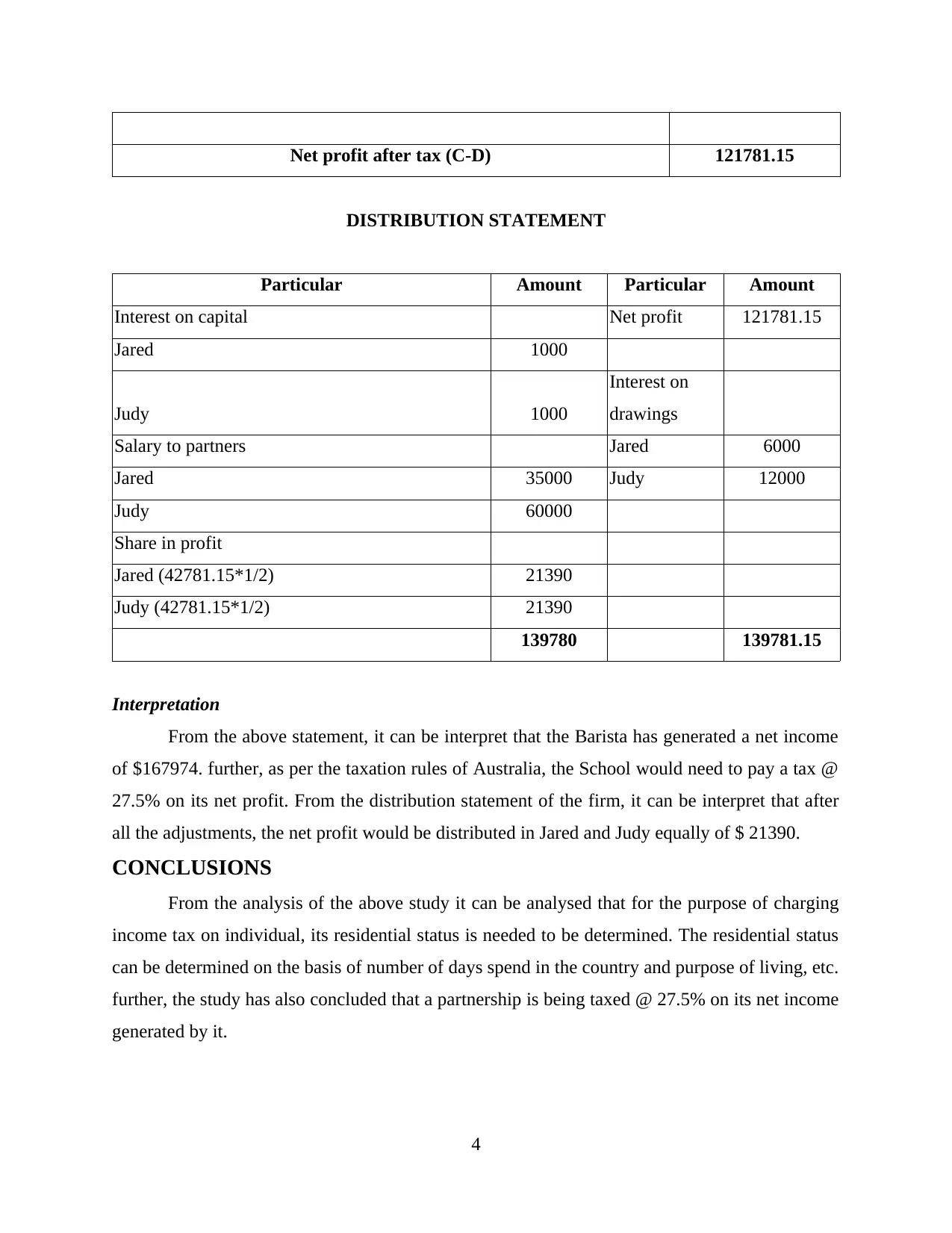

This assignment solution delves into Australian taxation law, specifically focusing on determining an individual's residential status for tax purposes and calculating the net income of a partnership. Part A analyzes the residential status of an individual, Jack, for the year ending June 30, 2018, considering various residency tests such as the resides test, domicile test, 183-day test, and superannuation test. It concludes that Jack is a non-resident based on his circumstances. Part B calculates the net income of the Barista School partnership, including revenue, expenses, and profit distribution among partners, Jared and Judy, demonstrating the application of taxation rules to partnership income. The solution also includes an income statement, distribution statement, and a conclusion summarizing the key findings of the analysis, as well as a list of references.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.