Taxation Law in Australia: Comprehensive Analysis and Application

VerifiedAdded on 2021/04/24

|15

|3143

|126

Homework Assignment

AI Summary

This assignment solution delves into the intricacies of Australian taxation law, addressing key aspects such as income tax, deductions, and residency. The solution analyzes various scenarios, including the determination of taxable income, the application of progressive tax systems, and the treatment of different types of income, allowances, and deductions as per the Income Tax Assessment Act 1997 (ITAA 1997). It also explores the concept of residency and its implications, referencing relevant tax rulings and case laws. The assignment further calculates tax liabilities based on specific income levels and examines the application of capital allowances and the treatment of non-assessable non-exempt income. Finally, the solution addresses the tax implications of various income sources, including salaries, interest, winnings, and payments for restrictive covenants, providing a detailed breakdown of assessable income, allowable deductions, and the resulting tax payable. The assignment also provides a comparative analysis of depreciation methods and their impact on tax deductions.

Running head: TAXATION LAW IN AUSTRALIA

Taxation Law in Australia

Name of the Student:

Name of the University

Author’s Note:

Taxation Law in Australia

Name of the Student:

Name of the University

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

TAXATION LAW IN AUSTRALIA

Table of Contents

Question 1........................................................................................................................................2

Question 2........................................................................................................................................5

Question 3........................................................................................................................................7

Question 4........................................................................................................................................9

Question 5......................................................................................................................................10

Question 6......................................................................................................................................11

Reference.......................................................................................................................................13

TAXATION LAW IN AUSTRALIA

Table of Contents

Question 1........................................................................................................................................2

Question 2........................................................................................................................................5

Question 3........................................................................................................................................7

Question 4........................................................................................................................................9

Question 5......................................................................................................................................10

Question 6......................................................................................................................................11

Reference.......................................................................................................................................13

2

TAXATION LAW IN AUSTRALIA

Question 1

Requirement a

The major role which is played by the tax system in Australia is to maintain the revenue

administration system of the Government which is then used for running the nation as a whole.

There are a variety of taxes which are in place in Australia which relates to income tax system,

superannuation and excise which are all maintained by the taxation system incorporated by the

Government1. Therefore, in general the taxation system in Australia maintains the revenue

system and flow of cash from public to government and then back to the public in Australia.

Requirement b

The concept of equity in a tax system refers to the principle that the burden which is

related to tax liability should be imposed fairly on the society. The principle of equity is made up

of two elements which are horizontal equity and vertical equity2. The concept of horizontal

equity states that individuals should pay the same amount of taxes while the concept of vertical

equity states that individuals who are in different positions should pay different sum as taxes.

Requirement c

As per the provisions of Section 4-15 of Income Tax Assessment Act 1997 (ITTA 1997),

establishes the method in which an individual can work out taxable income for the year. The

general formula which is followed for computing the taxable income of the business is

Taxable Income=Assessable Income−Deductions

1 Winer, Stanley L., Paola Profeta, and Walter Hettich. The political economy of taxation. Oxford University Press,

2013.

2 Lindsay, Ira K. "Tax Fairness by Convention: A Defense of Horizontal Equity." Fla. Tax Rev. 19 (2016): 79.

TAXATION LAW IN AUSTRALIA

Question 1

Requirement a

The major role which is played by the tax system in Australia is to maintain the revenue

administration system of the Government which is then used for running the nation as a whole.

There are a variety of taxes which are in place in Australia which relates to income tax system,

superannuation and excise which are all maintained by the taxation system incorporated by the

Government1. Therefore, in general the taxation system in Australia maintains the revenue

system and flow of cash from public to government and then back to the public in Australia.

Requirement b

The concept of equity in a tax system refers to the principle that the burden which is

related to tax liability should be imposed fairly on the society. The principle of equity is made up

of two elements which are horizontal equity and vertical equity2. The concept of horizontal

equity states that individuals should pay the same amount of taxes while the concept of vertical

equity states that individuals who are in different positions should pay different sum as taxes.

Requirement c

As per the provisions of Section 4-15 of Income Tax Assessment Act 1997 (ITTA 1997),

establishes the method in which an individual can work out taxable income for the year. The

general formula which is followed for computing the taxable income of the business is

Taxable Income=Assessable Income−Deductions

1 Winer, Stanley L., Paola Profeta, and Walter Hettich. The political economy of taxation. Oxford University Press,

2013.

2 Lindsay, Ira K. "Tax Fairness by Convention: A Defense of Horizontal Equity." Fla. Tax Rev. 19 (2016): 79.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

TAXATION LAW IN AUSTRALIA

The above formula makes it clear that the taxpayer needs to sum up his assessable

income and the deductions which are applicable and finally subtract the total deductions from the

assessable income of the individual to arrive at taxable income of the individual3.

Requirement d

The main principle of progressive tax system is to increase the rate of taxation as the

income of the taxpayer increases. In this tax system, tax are charged as per tax brackets which

are set which progressively increases to a higher rate of tax as the income of the taxpayer

increases4. This sort of taxation system focuses to reduce the inequity of distribution of income

among individuals and charges more taxes from lower earning group of peoples and more from

higher earning group peoples5. Progressive taxation system aims to bring about growth and

development in areas where it is difficult to bring about intervention of government.

Requirement e

The section which includes the value of allowances into the assessable income is Section

15-2 of ITAA 1997.

Requirement f

The “taxation ruling of TR 2004/15” includes provisions which is related to the case

where a company which is not incorporated in Australia will be treated as an Australian resident

as per the second statutory test of the definition of “Resident of Australia” which is stated in

“subsection 6(1) of the ITAA 1936”.

3 Bobek, Donna D., Amy M. Hageman, and Charles F. Kelliher. "Analyzing the role of social norms in tax

compliance behavior." Journal of Business Ethics 115, no. 3 (2013): 451-468.

4 Chen, Shu-Hua, and Jang-Ting Guo. "Progressive taxation and macroeconomic (In) stability with productive

government spending." Journal of Economic Dynamics and Control 37, no. 5 (2013): 951-963.

5 Mehrotra, Ajay K. Making the Modern American Fiscal State: Law, Politics, and the Rise of Progressive Taxation,

1877-1929. Cambridge University Press, 2013.

TAXATION LAW IN AUSTRALIA

The above formula makes it clear that the taxpayer needs to sum up his assessable

income and the deductions which are applicable and finally subtract the total deductions from the

assessable income of the individual to arrive at taxable income of the individual3.

Requirement d

The main principle of progressive tax system is to increase the rate of taxation as the

income of the taxpayer increases. In this tax system, tax are charged as per tax brackets which

are set which progressively increases to a higher rate of tax as the income of the taxpayer

increases4. This sort of taxation system focuses to reduce the inequity of distribution of income

among individuals and charges more taxes from lower earning group of peoples and more from

higher earning group peoples5. Progressive taxation system aims to bring about growth and

development in areas where it is difficult to bring about intervention of government.

Requirement e

The section which includes the value of allowances into the assessable income is Section

15-2 of ITAA 1997.

Requirement f

The “taxation ruling of TR 2004/15” includes provisions which is related to the case

where a company which is not incorporated in Australia will be treated as an Australian resident

as per the second statutory test of the definition of “Resident of Australia” which is stated in

“subsection 6(1) of the ITAA 1936”.

3 Bobek, Donna D., Amy M. Hageman, and Charles F. Kelliher. "Analyzing the role of social norms in tax

compliance behavior." Journal of Business Ethics 115, no. 3 (2013): 451-468.

4 Chen, Shu-Hua, and Jang-Ting Guo. "Progressive taxation and macroeconomic (In) stability with productive

government spending." Journal of Economic Dynamics and Control 37, no. 5 (2013): 951-963.

5 Mehrotra, Ajay K. Making the Modern American Fiscal State: Law, Politics, and the Rise of Progressive Taxation,

1877-1929. Cambridge University Press, 2013.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

TAXATION LAW IN AUSTRALIA

Requirement g

The two divisions which provide for deduction for capital deductions under ITAA 1997

are listed below:

Division 40 Uniform Capital allowance

Division 43 Capital Works Allowances

Requirement h

The applicable tax rate in the case where the taxable income of the business is $ 80,000 in

2017/18 for a taxpayer is shown below:

Taxable Income = $ 80,000 (Marginal tax rate 32.5% with $ 3,572 plus 32.5 cents for

every dollar over $ 37,000).

Requirement i

The provisions of sub-division 11-B of ITAA 1997 covers the provisions of treating the

amounts of Non-Assessable Non-Exempt Income.

Requirement j

As per the provisions of Tax Determination TD 2017/4, 53 cents per kilometer is

applicable for motor vehicles which has an engine capacity of 2500 cc.

Question 2

The “taxation ruling of TR 98/17” is associated with the provisions of residency status

of a person who enters Australia. The term of residence which in ordinary meaning can be

TAXATION LAW IN AUSTRALIA

Requirement g

The two divisions which provide for deduction for capital deductions under ITAA 1997

are listed below:

Division 40 Uniform Capital allowance

Division 43 Capital Works Allowances

Requirement h

The applicable tax rate in the case where the taxable income of the business is $ 80,000 in

2017/18 for a taxpayer is shown below:

Taxable Income = $ 80,000 (Marginal tax rate 32.5% with $ 3,572 plus 32.5 cents for

every dollar over $ 37,000).

Requirement i

The provisions of sub-division 11-B of ITAA 1997 covers the provisions of treating the

amounts of Non-Assessable Non-Exempt Income.

Requirement j

As per the provisions of Tax Determination TD 2017/4, 53 cents per kilometer is

applicable for motor vehicles which has an engine capacity of 2500 cc.

Question 2

The “taxation ruling of TR 98/17” is associated with the provisions of residency status

of a person who enters Australia. The term of residence which in ordinary meaning can be

5

TAXATION LAW IN AUSTRALIA

interpreted by taxation commissioner and the same is covered in “subsection 6(1) of the ITAA

1936”. The ruling which are covered in the section generally relates to individuals who enter

Australia.

As per the case study which is shown in the question deals with Martelle who has arrived

in Australia for some work purpose even though she intends to return to her country after the

work is done. As per the provision, when a person comes into the country with no intention on

staying in the country for a permanent basis than all factors of the person’s presence should be

considered when determining the residential status of the person6. The quality and behavior of

the individual also helps in determination of the residential status of the business. The factors

which are considered by Australian Tax Office (ATO) for establishing a residency status of an

individual are listed below:

The intention and the objective for the presence of the individual

The individual relation of family, employment and business relations in the country.

Maintenance as well as location of the assets.

Individual’s social and living arrangements in Australia.

As per the provisions which are stated in Residency laws, when an individual’s behavior is

similar with those who are living in Australia, then such a person will be treated as a resident of

Australia7. The tax commissioner of Australia is of the view that a period of six months is

sufficient for determining whether the behavior of a person is consistent with the usual residents

of the country. As per the cases laws of “Reid v The commissioner of Inland Revenue (1926)”

6 "Residency - The Resides Test". 2018. Ato.Gov.Au. Accessed September 2 2018.

https://www.ato.gov.au/Individuals/International-tax-for-individuals/In-detail/Residency/Residency---the-resides-

test/.

7 Meade, James E. The Structure and Reform of Direct Taxation (Routledge Revivals). Routledge, 2013.

TAXATION LAW IN AUSTRALIA

interpreted by taxation commissioner and the same is covered in “subsection 6(1) of the ITAA

1936”. The ruling which are covered in the section generally relates to individuals who enter

Australia.

As per the case study which is shown in the question deals with Martelle who has arrived

in Australia for some work purpose even though she intends to return to her country after the

work is done. As per the provision, when a person comes into the country with no intention on

staying in the country for a permanent basis than all factors of the person’s presence should be

considered when determining the residential status of the person6. The quality and behavior of

the individual also helps in determination of the residential status of the business. The factors

which are considered by Australian Tax Office (ATO) for establishing a residency status of an

individual are listed below:

The intention and the objective for the presence of the individual

The individual relation of family, employment and business relations in the country.

Maintenance as well as location of the assets.

Individual’s social and living arrangements in Australia.

As per the provisions which are stated in Residency laws, when an individual’s behavior is

similar with those who are living in Australia, then such a person will be treated as a resident of

Australia7. The tax commissioner of Australia is of the view that a period of six months is

sufficient for determining whether the behavior of a person is consistent with the usual residents

of the country. As per the cases laws of “Reid v The commissioner of Inland Revenue (1926)”

6 "Residency - The Resides Test". 2018. Ato.Gov.Au. Accessed September 2 2018.

https://www.ato.gov.au/Individuals/International-tax-for-individuals/In-detail/Residency/Residency---the-resides-

test/.

7 Meade, James E. The Structure and Reform of Direct Taxation (Routledge Revivals). Routledge, 2013.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

TAXATION LAW IN AUSTRALIA

the quality of existence and also the time which the person spends in the country or the duration

of the stay of the person decides the residence of that particular person. In addition to this, it was

the verdict given by the court in case of “Miesegaes v Commissioner of Inland Revenue

(1957)” that a person who enters the country with a view to avail employment opportunities in

the country can be held to be resident of the country if the same is consistent with the residency

laws which are in force in Australia.

In the case which is provided in the question, Martelle opened an account in bank that had

the facility of receiving her salary directly into that account and moreover she purchased a boat

for a vacation trip with her friends to an island. The behavior which is demonstrated by Martella

is consistent with that of a normal resident living in Australia8. Therefore, adhering to the case

laws and judgements which was made in “Reid v The commissioner of Inland Revenue (1926)”

Martellla will be considered to be a resident of the country which is covered in “subsection 6(1)

of the ITAA 1936”. The salary amount which Martella receives in the bank account which she

has opened will be liable for taxation as per the tax laws applicable in Australia.

Question 3

The earnings of an employee which can be through salaries, wages, bonus, fees

allowances which is received by the employee for the services which is provided by the

employee are subjected to income tax which the employee needs to pay which is stated in

“Section 6-1 of the ITAA 1936”. Section 6-5 states that most of the income which is earned by

residents forms part of the ordinary income of the resident and therefore subjected to tax.

Therefore, the amount which Ellen earns as salary during the year is to be considered for tax

8 Burkhauser, Richard V., Markus H. Hahn, and Roger Wilkins. "Measuring top incomes using tax record data: A

cautionary tale from Australia." The Journal of Economic Inequality 13, no. 2 (2015): 181-205.

TAXATION LAW IN AUSTRALIA

the quality of existence and also the time which the person spends in the country or the duration

of the stay of the person decides the residence of that particular person. In addition to this, it was

the verdict given by the court in case of “Miesegaes v Commissioner of Inland Revenue

(1957)” that a person who enters the country with a view to avail employment opportunities in

the country can be held to be resident of the country if the same is consistent with the residency

laws which are in force in Australia.

In the case which is provided in the question, Martelle opened an account in bank that had

the facility of receiving her salary directly into that account and moreover she purchased a boat

for a vacation trip with her friends to an island. The behavior which is demonstrated by Martella

is consistent with that of a normal resident living in Australia8. Therefore, adhering to the case

laws and judgements which was made in “Reid v The commissioner of Inland Revenue (1926)”

Martellla will be considered to be a resident of the country which is covered in “subsection 6(1)

of the ITAA 1936”. The salary amount which Martella receives in the bank account which she

has opened will be liable for taxation as per the tax laws applicable in Australia.

Question 3

The earnings of an employee which can be through salaries, wages, bonus, fees

allowances which is received by the employee for the services which is provided by the

employee are subjected to income tax which the employee needs to pay which is stated in

“Section 6-1 of the ITAA 1936”. Section 6-5 states that most of the income which is earned by

residents forms part of the ordinary income of the resident and therefore subjected to tax.

Therefore, the amount which Ellen earns as salary during the year is to be considered for tax

8 Burkhauser, Richard V., Markus H. Hahn, and Roger Wilkins. "Measuring top incomes using tax record data: A

cautionary tale from Australia." The Journal of Economic Inequality 13, no. 2 (2015): 181-205.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

TAXATION LAW IN AUSTRALIA

assessment. Similarly, Ellen also received $ 425 from Westpac bank and the same is also

covered in the provisions of “section 6-5 of the ITAA 1997” and therefore covered as ordinary

income which is taxable in nature.

As per the verdict which is given by the court in “Moore v Griffiths (1972)” wiining of

lotteries or prizes is not to be considered as an income source and therefore cannot be charged to

tax. However, such winnings can be held taxable in case there is a “nexus” with the normal

revenue generating activities of the individual. It was held in the case of “Kelly v FC of T

(1985)” where a professional footballer was awarded as the best player in football profession.

The amount which was received by the player was held taxable as the same was closely related

to the profession which required application of his skills and therefore was included in the

taxable income of the player9. Thus, relying on the judgement in the case cited above the amount

which is received by Ellen which is of $ 6,500 will be held taxable as the same is incidental to

the profession which is followed by Ellen.

As per the tax rules which are stated, payments which are received for restriction of

practice or relinquishing rights of practice is not considered to be a part of income of the

individual. Any payments which is received by an individual which restrain him from doing a

business cannot be considered to be a part of the income of the individual. It can result in CGT

event D1 where a taxpayer agrees not to carry out similar business with his competitor in

exchange for a lumpsum payment which is also not considered to be included in the taxable

income of the business. Therefore, as stated in the case of Ellen where she received $ 10,000 for

signing a restriction of operation contract cannot be held as taxable income of the taxable.

9 "Deductions You Can Claim". 2018. Ato.Gov.Au. Accessed September 2 2018.

https://www.ato.gov.au/Individuals/Income-and-deductions/Deductions-you-can-claim/.

TAXATION LAW IN AUSTRALIA

assessment. Similarly, Ellen also received $ 425 from Westpac bank and the same is also

covered in the provisions of “section 6-5 of the ITAA 1997” and therefore covered as ordinary

income which is taxable in nature.

As per the verdict which is given by the court in “Moore v Griffiths (1972)” wiining of

lotteries or prizes is not to be considered as an income source and therefore cannot be charged to

tax. However, such winnings can be held taxable in case there is a “nexus” with the normal

revenue generating activities of the individual. It was held in the case of “Kelly v FC of T

(1985)” where a professional footballer was awarded as the best player in football profession.

The amount which was received by the player was held taxable as the same was closely related

to the profession which required application of his skills and therefore was included in the

taxable income of the player9. Thus, relying on the judgement in the case cited above the amount

which is received by Ellen which is of $ 6,500 will be held taxable as the same is incidental to

the profession which is followed by Ellen.

As per the tax rules which are stated, payments which are received for restriction of

practice or relinquishing rights of practice is not considered to be a part of income of the

individual. Any payments which is received by an individual which restrain him from doing a

business cannot be considered to be a part of the income of the individual. It can result in CGT

event D1 where a taxpayer agrees not to carry out similar business with his competitor in

exchange for a lumpsum payment which is also not considered to be included in the taxable

income of the business. Therefore, as stated in the case of Ellen where she received $ 10,000 for

signing a restriction of operation contract cannot be held as taxable income of the taxable.

9 "Deductions You Can Claim". 2018. Ato.Gov.Au. Accessed September 2 2018.

https://www.ato.gov.au/Individuals/Income-and-deductions/Deductions-you-can-claim/.

8

TAXATION LAW IN AUSTRALIA

The Australian Tax Office (ATO) allows an individual to claim private health insurance

rebate which is refundable tax offset which can be acquired by filing tax returns. The sum of $

500 incurred by Ellen for private health insurance can be claimed as tax offset.

The net amount of tax liability which needs to be incurred by Ellen for the year ended

30th June 2018 is stated below:

Particulars Amount ($) Amount ($)

Assessable Income

Income from Salaries 108000

Australian Sourced Interest Income 425

Income from Winnings 6500

Total Assessable Income 114925

Allowable Deductions Nil

Total Taxable Income 114925

Tax on Taxable Income 30154.25

Add: Medicare Levy 2298.5

Less: Private Health Insurance Offset 500

Total Tax Payable 31952.75

Question 4

As per the provisions which is stated in section 40-25 (1), an individual who is applicable

to pay taxes for the year can avail for deductions for decline in value of depreciating assets

which are used by the business for the year. The section clearly states that an individual can

claim for deductions for such depreciating assets which are used for assessable purpose10. The

assets which are used by the business or installed in the business can be held for claiming

10 Sharma, Rajeshwar, and Nisha Singh. "Use of depreciation as a tax policy device to control inflation." (2015).

TAXATION LAW IN AUSTRALIA

The Australian Tax Office (ATO) allows an individual to claim private health insurance

rebate which is refundable tax offset which can be acquired by filing tax returns. The sum of $

500 incurred by Ellen for private health insurance can be claimed as tax offset.

The net amount of tax liability which needs to be incurred by Ellen for the year ended

30th June 2018 is stated below:

Particulars Amount ($) Amount ($)

Assessable Income

Income from Salaries 108000

Australian Sourced Interest Income 425

Income from Winnings 6500

Total Assessable Income 114925

Allowable Deductions Nil

Total Taxable Income 114925

Tax on Taxable Income 30154.25

Add: Medicare Levy 2298.5

Less: Private Health Insurance Offset 500

Total Tax Payable 31952.75

Question 4

As per the provisions which is stated in section 40-25 (1), an individual who is applicable

to pay taxes for the year can avail for deductions for decline in value of depreciating assets

which are used by the business for the year. The section clearly states that an individual can

claim for deductions for such depreciating assets which are used for assessable purpose10. The

assets which are used by the business or installed in the business can be held for claiming

10 Sharma, Rajeshwar, and Nisha Singh. "Use of depreciation as a tax policy device to control inflation." (2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

TAXATION LAW IN AUSTRALIA

deduction. A taxpayer can claim deductions for decline in the value of the assets by following

the methods listed below:

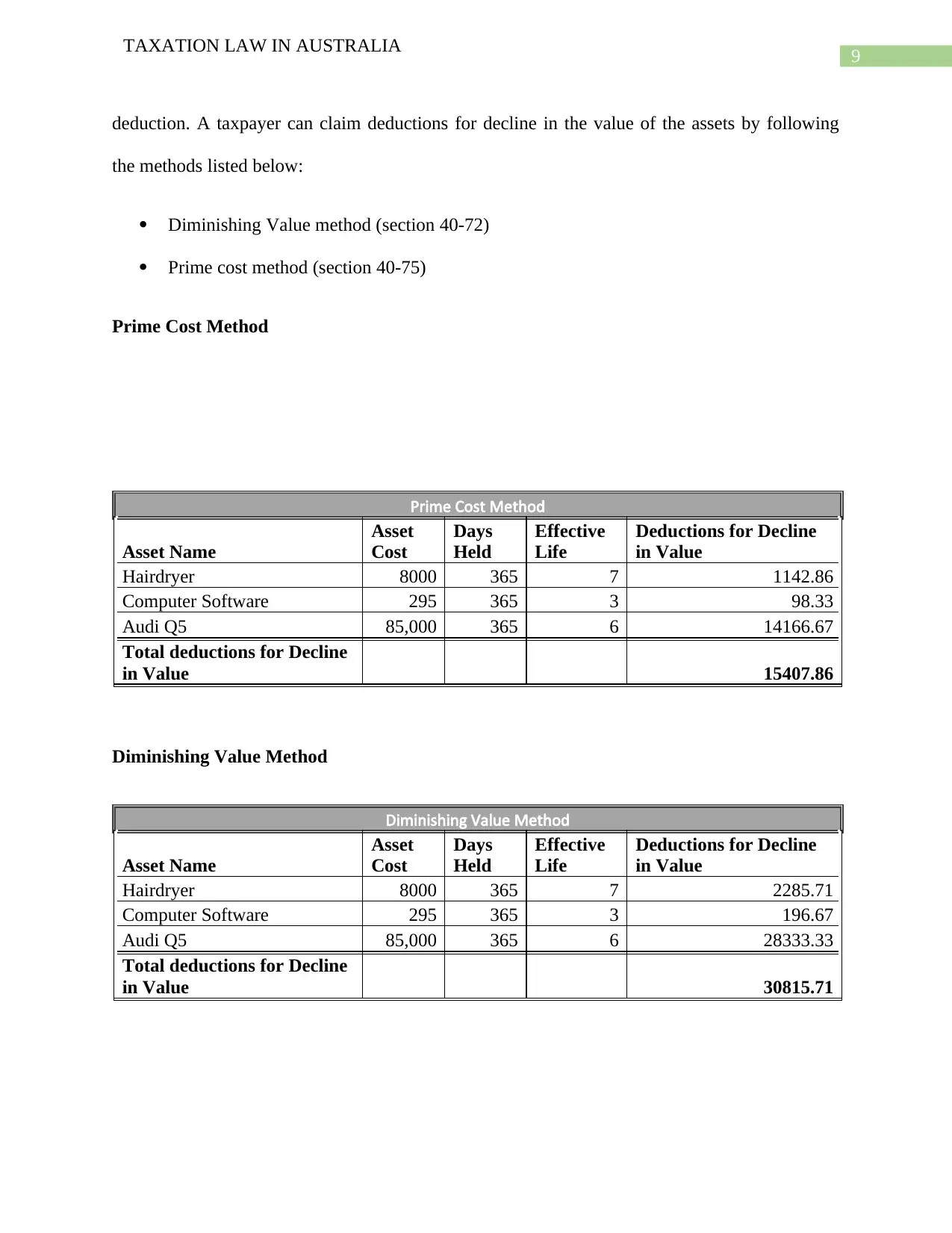

Diminishing Value method (section 40-72)

Prime cost method (section 40-75)

Prime Cost Method

Prime Cost Method

Asset Name

Asset

Cost

Days

Held

Effective

Life

Deductions for Decline

in Value

Hairdryer 8000 365 7 1142.86

Computer Software 295 365 3 98.33

Audi Q5 85,000 365 6 14166.67

Total deductions for Decline

in Value 15407.86

Diminishing Value Method

Diminishing Value Method

Asset Name

Asset

Cost

Days

Held

Effective

Life

Deductions for Decline

in Value

Hairdryer 8000 365 7 2285.71

Computer Software 295 365 3 196.67

Audi Q5 85,000 365 6 28333.33

Total deductions for Decline

in Value 30815.71

TAXATION LAW IN AUSTRALIA

deduction. A taxpayer can claim deductions for decline in the value of the assets by following

the methods listed below:

Diminishing Value method (section 40-72)

Prime cost method (section 40-75)

Prime Cost Method

Prime Cost Method

Asset Name

Asset

Cost

Days

Held

Effective

Life

Deductions for Decline

in Value

Hairdryer 8000 365 7 1142.86

Computer Software 295 365 3 98.33

Audi Q5 85,000 365 6 14166.67

Total deductions for Decline

in Value 15407.86

Diminishing Value Method

Diminishing Value Method

Asset Name

Asset

Cost

Days

Held

Effective

Life

Deductions for Decline

in Value

Hairdryer 8000 365 7 2285.71

Computer Software 295 365 3 196.67

Audi Q5 85,000 365 6 28333.33

Total deductions for Decline

in Value 30815.71

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

TAXATION LAW IN AUSTRALIA

The calculations which is shown in the above table shows deduction of $ 30815.71 under

diminishing value method and Jenifer should select this method for claiming reduction from her

assessable income.

Question 5

As per the provisions which is covered in section 6-5 states that income which are earned

during normal course of operations are covered as ordinary income. However, gains which are

earned by an individual cannot be treated as income unless other legislations provide for the

same. As per the case, Julie is a photographer by hobby and has decided to set up a business of

photography. The regulations which are set by Australian Tax Office (ATO) clarifies the

difference which exist between profession and hobby for taxation purpose. When a hobby is

turned into profession, the tax obligations for the individual commences from the same. As stated

in the case of “Stone v FC of T (2005)” the intention of generating profits from the business

must be there and also ATO considers the nature of the operations which is undertaken by the

business.

As evident in the case of Julie, as the individual converts his hobby to form a business,

Julie needs to register the business along with the official name of the business and also obtain

appropriate ABN number for conducting the business. The other factors which the individual

needs to consider are keeping tracks of recording requirements, setting up of bank accounts. The

income which is generated by Julie from the Photography business will be considered to be

ordinary income in the normal course of business as per the provision of Australian Tax laws.

TAXATION LAW IN AUSTRALIA

The calculations which is shown in the above table shows deduction of $ 30815.71 under

diminishing value method and Jenifer should select this method for claiming reduction from her

assessable income.

Question 5

As per the provisions which is covered in section 6-5 states that income which are earned

during normal course of operations are covered as ordinary income. However, gains which are

earned by an individual cannot be treated as income unless other legislations provide for the

same. As per the case, Julie is a photographer by hobby and has decided to set up a business of

photography. The regulations which are set by Australian Tax Office (ATO) clarifies the

difference which exist between profession and hobby for taxation purpose. When a hobby is

turned into profession, the tax obligations for the individual commences from the same. As stated

in the case of “Stone v FC of T (2005)” the intention of generating profits from the business

must be there and also ATO considers the nature of the operations which is undertaken by the

business.

As evident in the case of Julie, as the individual converts his hobby to form a business,

Julie needs to register the business along with the official name of the business and also obtain

appropriate ABN number for conducting the business. The other factors which the individual

needs to consider are keeping tracks of recording requirements, setting up of bank accounts. The

income which is generated by Julie from the Photography business will be considered to be

ordinary income in the normal course of business as per the provision of Australian Tax laws.

11

TAXATION LAW IN AUSTRALIA

Question 6

As per section 8-1 of ITTA 1997 an individual is entitled to claim deductions for any

expenses which is incurred by the business during the normal course of operations of the

business. As per the case study which is shown in the question, Chang is a business owner which

operates a marketing business for which different costs are incurred by the business. Chang

incurs a salary costs which costs up to $ 300,000 and also reports a cost of $ 4,000 that Chang

pays to his son for designing of graphics. The salaries costs which are incurred by Chang during

the year will be considered to be a part of the deductions which is allowable to Chang during the

year. The deduction is allowable under general provision of section 8-1.

Chang has incurred $ 900 in local bowls club for entertainment of his clients. The

provisions of Australian Tax Office provide that deduction can be claimed for recreational

activities and therefore such an expense which is undertaken by Chang is allowable as deduction

during the year.

Chang incurred expenses which is regarding purchase of clothing materials such as suits

for portraying correct image in front of clients. This expense which is incurred by the taxpayer

will not be allowed as deductions under section 8-1. Therefore, the expenses on smart clothing

will not be allowed as deduction for Chang during the year.

The expenses which is incurred by Chang on providing meals to the clients will be

allowed as deductions during the year as the same are covered in general provisions of ATO

relating to deductions which will be allowed to taxpayers for incurring on clients for food, drink

and recreational activities.

TAXATION LAW IN AUSTRALIA

Question 6

As per section 8-1 of ITTA 1997 an individual is entitled to claim deductions for any

expenses which is incurred by the business during the normal course of operations of the

business. As per the case study which is shown in the question, Chang is a business owner which

operates a marketing business for which different costs are incurred by the business. Chang

incurs a salary costs which costs up to $ 300,000 and also reports a cost of $ 4,000 that Chang

pays to his son for designing of graphics. The salaries costs which are incurred by Chang during

the year will be considered to be a part of the deductions which is allowable to Chang during the

year. The deduction is allowable under general provision of section 8-1.

Chang has incurred $ 900 in local bowls club for entertainment of his clients. The

provisions of Australian Tax Office provide that deduction can be claimed for recreational

activities and therefore such an expense which is undertaken by Chang is allowable as deduction

during the year.

Chang incurred expenses which is regarding purchase of clothing materials such as suits

for portraying correct image in front of clients. This expense which is incurred by the taxpayer

will not be allowed as deductions under section 8-1. Therefore, the expenses on smart clothing

will not be allowed as deduction for Chang during the year.

The expenses which is incurred by Chang on providing meals to the clients will be

allowed as deductions during the year as the same are covered in general provisions of ATO

relating to deductions which will be allowed to taxpayers for incurring on clients for food, drink

and recreational activities.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.