Taxation Law Assignment - Individual, LAWS20060, Term 1, 2019

VerifiedAdded on 2023/01/23

|19

|4646

|84

Homework Assignment

AI Summary

This document presents a comprehensive solution to a Taxation Law assignment, likely for an Australian university course (LAWS20060). The assignment addresses several key aspects of taxation law, including depreciation, tax offsets, assessable income calculations, and the definition of collectibles. It further explores CGT events, income tax calculations, and the deductibility of expenses under section 8-1 of the ITAA 1997. The solution analyzes various scenarios, such as interest expenses, work-related versus private expenses, and the treatment of losses. It also delves into CGT events F2 and B1, the main residence exemption, and capital gains tax calculations. The assignment utilizes relevant case law, tax rulings, and legislative provisions to support its arguments and conclusions.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................3

Answer A:..............................................................................................................................3

Answer B:...............................................................................................................................3

Answer C:...............................................................................................................................3

Answer D:..............................................................................................................................3

Answer E:...............................................................................................................................4

Answer F:...............................................................................................................................4

Answer to G:..........................................................................................................................4

Answer H:..............................................................................................................................5

Answer I:................................................................................................................................5

Answer to question 2:.................................................................................................................6

Answer A:..............................................................................................................................6

Answer B:...............................................................................................................................6

Answer C:...............................................................................................................................7

Answer D:..............................................................................................................................7

Answer E:...............................................................................................................................8

Answer to question 3:.................................................................................................................9

Answer A:..............................................................................................................................9

Answer B:...............................................................................................................................9

Answer to C:........................................................................................................................10

Table of Contents

Answer to question 1:.................................................................................................................3

Answer A:..............................................................................................................................3

Answer B:...............................................................................................................................3

Answer C:...............................................................................................................................3

Answer D:..............................................................................................................................3

Answer E:...............................................................................................................................4

Answer F:...............................................................................................................................4

Answer to G:..........................................................................................................................4

Answer H:..............................................................................................................................5

Answer I:................................................................................................................................5

Answer to question 2:.................................................................................................................6

Answer A:..............................................................................................................................6

Answer B:...............................................................................................................................6

Answer C:...............................................................................................................................7

Answer D:..............................................................................................................................7

Answer E:...............................................................................................................................8

Answer to question 3:.................................................................................................................9

Answer A:..............................................................................................................................9

Answer B:...............................................................................................................................9

Answer to C:........................................................................................................................10

2TAXATION LAW

Answer D:............................................................................................................................10

Answer to question 4:...............................................................................................................11

Answer to A:........................................................................................................................11

Answer to B:........................................................................................................................11

Answer to C:........................................................................................................................12

Answer to D:........................................................................................................................12

Answer to E:.........................................................................................................................13

Answer to question 5:...............................................................................................................13

Issue:....................................................................................................................................13

Laws:....................................................................................................................................13

Application:..........................................................................................................................14

Conclusion:..........................................................................................................................15

References:...............................................................................................................................16

Answer D:............................................................................................................................10

Answer to question 4:...............................................................................................................11

Answer to A:........................................................................................................................11

Answer to B:........................................................................................................................11

Answer to C:........................................................................................................................12

Answer to D:........................................................................................................................12

Answer to E:.........................................................................................................................13

Answer to question 5:...............................................................................................................13

Issue:....................................................................................................................................13

Laws:....................................................................................................................................13

Application:..........................................................................................................................14

Conclusion:..........................................................................................................................15

References:...............................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

Answer to question 1:

Answer A:

The ruling of TR 2018/4 is concerned with the methodology that is employed by the

taxation commissioner to make the effective determination of the useful life of depreciation

asset under the “section 40-100, ITAA 1997”. It is used to compute the decline in value of

the asset for taxation purpose.

Answer B:

An important explanation has been made under the “Division 13, ITAA 1997”. It

mainly deals with tax offsets that a taxpayer claims under this division.

Answer C:

The highest amount of tax that is applied on the Australian occupant is as follows;

Assessable Earnings Tax (in$)

$180,001 or more $54,097 + 45c for each $1 beyond $180,000

Answer D:

“Section 108-10 (2)” defines collectibles as anything that is kept mostly for personal

usage or the enjoyment. There are special rules that are applicable to collectible this includes

that acquiring collectible for less than $500 and making capital gains or loss thereon is

ignored under “section 118-10 (1), ITAA 1997”1.

1 Campbell, Sam. "Personal liability of a trustee to tax on trust income: Part 1." Taxation in

Australia 53.5 (2018): 263.

Answer to question 1:

Answer A:

The ruling of TR 2018/4 is concerned with the methodology that is employed by the

taxation commissioner to make the effective determination of the useful life of depreciation

asset under the “section 40-100, ITAA 1997”. It is used to compute the decline in value of

the asset for taxation purpose.

Answer B:

An important explanation has been made under the “Division 13, ITAA 1997”. It

mainly deals with tax offsets that a taxpayer claims under this division.

Answer C:

The highest amount of tax that is applied on the Australian occupant is as follows;

Assessable Earnings Tax (in$)

$180,001 or more $54,097 + 45c for each $1 beyond $180,000

Answer D:

“Section 108-10 (2)” defines collectibles as anything that is kept mostly for personal

usage or the enjoyment. There are special rules that are applicable to collectible this includes

that acquiring collectible for less than $500 and making capital gains or loss thereon is

ignored under “section 118-10 (1), ITAA 1997”1.

1 Campbell, Sam. "Personal liability of a trustee to tax on trust income: Part 1." Taxation in

Australia 53.5 (2018): 263.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

Answer E:

An important explanation has been made in “section 104-15, ITAA 1997” regarding

the CGT event B1 where the usage as well as enjoyment of title before it is passed. The CGT

Event B1 only happens when a taxpayer forms a contract with another company where the

right for using and enjoying the title of the asset under the ownership of the taxpayer is

passed to another entity2. The CGT event explains that title of asset may be passed to another

entity before the contract comes to an end.

Answer F:

Under this “section 4-10 (3)” a person is required to pay the income tax every

financial year. This section explains that a person should work out the amount of income tax

that is payable by using the below formula;

Income tax = (Taxable Income x Rate) – Tax offsets

Answer to G:

Under the case of “FC of T v Day 2008 ATC 20-064” the public servant officer under

the “section 8-1, ITAA 1997” applied this provision of deduction for deducting the legal

outgoings the taxpayer occurred because of the numerous cases against the taxpayer was

levied by the employer which were associated to the disciplinary charges3. The cases that

were bought against the public servant was because of his own consequences and hence the

legal outgoings that were incurred was non-deductible.

2 Jones, Daryl. "Tax and accounting income-Worlds apart?." Taxation in Australia 52.1

(2017): 14.

3 Brydges, Neil, and Kelvin Yuen. "A matter of trusts: Trusts, income tax, CGT and foreign

residents." Taxation in Australia53.2 (2018): 80.

Answer E:

An important explanation has been made in “section 104-15, ITAA 1997” regarding

the CGT event B1 where the usage as well as enjoyment of title before it is passed. The CGT

Event B1 only happens when a taxpayer forms a contract with another company where the

right for using and enjoying the title of the asset under the ownership of the taxpayer is

passed to another entity2. The CGT event explains that title of asset may be passed to another

entity before the contract comes to an end.

Answer F:

Under this “section 4-10 (3)” a person is required to pay the income tax every

financial year. This section explains that a person should work out the amount of income tax

that is payable by using the below formula;

Income tax = (Taxable Income x Rate) – Tax offsets

Answer to G:

Under the case of “FC of T v Day 2008 ATC 20-064” the public servant officer under

the “section 8-1, ITAA 1997” applied this provision of deduction for deducting the legal

outgoings the taxpayer occurred because of the numerous cases against the taxpayer was

levied by the employer which were associated to the disciplinary charges3. The cases that

were bought against the public servant was because of his own consequences and hence the

legal outgoings that were incurred was non-deductible.

2 Jones, Daryl. "Tax and accounting income-Worlds apart?." Taxation in Australia 52.1

(2017): 14.

3 Brydges, Neil, and Kelvin Yuen. "A matter of trusts: Trusts, income tax, CGT and foreign

residents." Taxation in Australia53.2 (2018): 80.

5TAXATION LAW

Answer H:

Marginal Tax Rate Average Tax Rate

Marginal tax is defined as the tax which a

taxpayer would pay on their next dollar of

earnings4.

The average tax rate represents the total

amount of tax that is paid by a taxpayer

divided by their total income.

Marginal tax is useful in measuring the

effect of tax on incentives for earning,

saving, investment or expenditure.

This tax is useful in measuring the taxation

weight.

This tax is useful in assessing the extent up

to which the tax impact economic incentive

of households

The average tax is useful in measuring the

burden of tax in households.

Answer I:

Tax that is imposed on the consumption expenditure of the goods and services is

known as the consumption tax5. The base of tax for this type of tax is the sum of money that

is spend on the consumption. These type of tax is usually the indirect tax. It involves the

value-added tax or the sales tax. The consumption tax is generally structured in the form of

direct or personal tax.

4 Cooper, Graeme S. "The Curious Reform of Foreign Source Income." The Tax Specialist 22

(2018): 2-14.

5 King, Alexander. "Mid market focus: The new attribution tax regime for MITs: Part

2." Taxation in Australia 51.1 (2016): 12.

Answer H:

Marginal Tax Rate Average Tax Rate

Marginal tax is defined as the tax which a

taxpayer would pay on their next dollar of

earnings4.

The average tax rate represents the total

amount of tax that is paid by a taxpayer

divided by their total income.

Marginal tax is useful in measuring the

effect of tax on incentives for earning,

saving, investment or expenditure.

This tax is useful in measuring the taxation

weight.

This tax is useful in assessing the extent up

to which the tax impact economic incentive

of households

The average tax is useful in measuring the

burden of tax in households.

Answer I:

Tax that is imposed on the consumption expenditure of the goods and services is

known as the consumption tax5. The base of tax for this type of tax is the sum of money that

is spend on the consumption. These type of tax is usually the indirect tax. It involves the

value-added tax or the sales tax. The consumption tax is generally structured in the form of

direct or personal tax.

4 Cooper, Graeme S. "The Curious Reform of Foreign Source Income." The Tax Specialist 22

(2018): 2-14.

5 King, Alexander. "Mid market focus: The new attribution tax regime for MITs: Part

2." Taxation in Australia 51.1 (2016): 12.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

Answer to question 2:

Answer A:

The deduction of expenditure that consists of the interest under the “section 8-1,

ITAA 1997” is largely reliant on meeting the words of this provision that is capable of

showing that an outgoing has been occurred by the taxpayer in gaining taxable income of

taxpayer and it is not private or domestic in nature6. The court in “FCT v Roberts and Smith

(1992)” held that interest expenses should have appropriate relation with operation or

activities that are directly related to gaining the taxable income of the taxpayer and not

private or capita in nature.

Brett occurred interest expenses on loan taken to pay the employee wages. Citing

“FCT v Roberts and Smith (1992)” the interest on loan has appropriate relation with

operation or activities that are directly related to gaining the taxable income of Brett.

Therefore, it is deductible under “section 8-1, ITAA 1997”.

Answer B:

The ATO states that while filing tax return, a taxpayer is permitted to obtain

deduction for some expenses that are directly associated to earning income7. If outgoing was

occurred for both work and private purpose, then only work purpose expenses are allowed for

6 Datt, Kalmen H., and Mark Keating. "The Commissioner’s obligation to make

compensating adjustments for income tax and GST in Australia and New

Zealand." Australian Tax Forum. Vol. 33. No. 3. 2018.

7 Kudrna, George. "Australia’s Retirement Income Policy: Means Testing and Taxation of

Pensions." CESifo DICE Report 14.1 (2016): 3-9.

Answer to question 2:

Answer A:

The deduction of expenditure that consists of the interest under the “section 8-1,

ITAA 1997” is largely reliant on meeting the words of this provision that is capable of

showing that an outgoing has been occurred by the taxpayer in gaining taxable income of

taxpayer and it is not private or domestic in nature6. The court in “FCT v Roberts and Smith

(1992)” held that interest expenses should have appropriate relation with operation or

activities that are directly related to gaining the taxable income of the taxpayer and not

private or capita in nature.

Brett occurred interest expenses on loan taken to pay the employee wages. Citing

“FCT v Roberts and Smith (1992)” the interest on loan has appropriate relation with

operation or activities that are directly related to gaining the taxable income of Brett.

Therefore, it is deductible under “section 8-1, ITAA 1997”.

Answer B:

The ATO states that while filing tax return, a taxpayer is permitted to obtain

deduction for some expenses that are directly associated to earning income7. If outgoing was

occurred for both work and private purpose, then only work purpose expenses are allowed for

6 Datt, Kalmen H., and Mark Keating. "The Commissioner’s obligation to make

compensating adjustments for income tax and GST in Australia and New

Zealand." Australian Tax Forum. Vol. 33. No. 3. 2018.

7 Kudrna, George. "Australia’s Retirement Income Policy: Means Testing and Taxation of

Pensions." CESifo DICE Report 14.1 (2016): 3-9.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

deductions. In “Ronpibon Tin NL v FC of T (1949)” the commissioner stated that the part of

expenses that were occurred in directly producing taxable income.

The mobile phone outgoing of $500 was occurred by Julie where 60% were related to

work-purpose while rest were for private purpose. Quoting “Ronpibon Tin NL v FC of T

(1949)” only work-purpose portion is deductible under “section 8-1, ITAA 1997”.

Answer C:

The expense that are private or domestic in nature is non-deductible. The high-court

in “Lodge v FC of T (1972)” held that child care outgoings were not relevant or not related in

producing the taxable earnings and not deductible under “section 8-1, ITAA 1997”8.

The baby sitter expenses paid by Sally is a private or domestic expenses. Quoting

“Lodge v FC of T (1972)” baby sitter expenses is not relevant in producing income and not

permitted for deduction under “section 8-1, ITAA 1997”.

Answer D:

Deduction for loss of financial resources of taxpayer is allowed under the “section 8-

1, ITAA 1997”. In “Charles Moore & Co (WA) Pty Ltd v FCT (1965)” deduction for theft of

money was allowed to taxpayer because it was a loss of financial resources9.

8 Yuan, Helena. "Mid market focus: The sharing economy and taxation." Taxation in

Australia 51.6 (2016): 293.

9 Burton, Mark. "A Review of Judicial References to the Dictum of Jordan CJ, Expressed in

Scott v. Commissioner of Taxation, in Elaborating the Meaning of Income for the Purposes

of the Australian Income Tax." J. Austl. Tax'n 19 (2017): 50.

deductions. In “Ronpibon Tin NL v FC of T (1949)” the commissioner stated that the part of

expenses that were occurred in directly producing taxable income.

The mobile phone outgoing of $500 was occurred by Julie where 60% were related to

work-purpose while rest were for private purpose. Quoting “Ronpibon Tin NL v FC of T

(1949)” only work-purpose portion is deductible under “section 8-1, ITAA 1997”.

Answer C:

The expense that are private or domestic in nature is non-deductible. The high-court

in “Lodge v FC of T (1972)” held that child care outgoings were not relevant or not related in

producing the taxable earnings and not deductible under “section 8-1, ITAA 1997”8.

The baby sitter expenses paid by Sally is a private or domestic expenses. Quoting

“Lodge v FC of T (1972)” baby sitter expenses is not relevant in producing income and not

permitted for deduction under “section 8-1, ITAA 1997”.

Answer D:

Deduction for loss of financial resources of taxpayer is allowed under the “section 8-

1, ITAA 1997”. In “Charles Moore & Co (WA) Pty Ltd v FCT (1965)” deduction for theft of

money was allowed to taxpayer because it was a loss of financial resources9.

8 Yuan, Helena. "Mid market focus: The sharing economy and taxation." Taxation in

Australia 51.6 (2016): 293.

9 Burton, Mark. "A Review of Judicial References to the Dictum of Jordan CJ, Expressed in

Scott v. Commissioner of Taxation, in Elaborating the Meaning of Income for the Purposes

of the Australian Income Tax." J. Austl. Tax'n 19 (2017): 50.

8TAXATION LAW

Jerry here reported a loss of $20,000 that was stolen by the long term employee from the

business. Denoting “Charles Moore & Co (WA) Pty Ltd v FCT (1965)” the theft involves

the loss of financial resources for Jerry and it is deductible under “section 8-1, ITAA 1997”.

Answer E:

The general provision of “8-1, ITAA 1997” explains that outgoings that are

preliminary to beginning income or business activities is not regarded as in course of earning

income. In “Maddalena v FCT (1971)” no deduction was permitted under 1st positive limb

for expenses in getting contract with another club because it was occurred at a point very

soon10.

Expenses occurred in contesting the local government election and spending on the

big election party is non-deductible under general provision of “8-1, ITAA 1997”. This is

because the expenses were preliminary to income producing activities and occurred at a point

very soon11.

Answer to question 3:

Answer A:

A taxpayer is allowed to choose or apply the CGT event F2 when they grant, renew or

extend the long term lease. It can be implemented if the taxpayer is the owner of land or

provides any sub-lease. However, no CGT discount is applicable to CGT event F212.

10 Tran, Alfred. "Can taxable income be estimated from financial reports of listed companies

in Australia." Austl. Tax F. 30 (2015): 569.

11 Fisher, Donna. "Mid market focus: No joy regarding FBT on travel expenses for FIFO

arrangements." Taxation in Australia49.7 (2015): 377.

Jerry here reported a loss of $20,000 that was stolen by the long term employee from the

business. Denoting “Charles Moore & Co (WA) Pty Ltd v FCT (1965)” the theft involves

the loss of financial resources for Jerry and it is deductible under “section 8-1, ITAA 1997”.

Answer E:

The general provision of “8-1, ITAA 1997” explains that outgoings that are

preliminary to beginning income or business activities is not regarded as in course of earning

income. In “Maddalena v FCT (1971)” no deduction was permitted under 1st positive limb

for expenses in getting contract with another club because it was occurred at a point very

soon10.

Expenses occurred in contesting the local government election and spending on the

big election party is non-deductible under general provision of “8-1, ITAA 1997”. This is

because the expenses were preliminary to income producing activities and occurred at a point

very soon11.

Answer to question 3:

Answer A:

A taxpayer is allowed to choose or apply the CGT event F2 when they grant, renew or

extend the long term lease. It can be implemented if the taxpayer is the owner of land or

provides any sub-lease. However, no CGT discount is applicable to CGT event F212.

10 Tran, Alfred. "Can taxable income be estimated from financial reports of listed companies

in Australia." Austl. Tax F. 30 (2015): 569.

11 Fisher, Donna. "Mid market focus: No joy regarding FBT on travel expenses for FIFO

arrangements." Taxation in Australia49.7 (2015): 377.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

Any owned the land and provides the grants of a lease to Brian at a premium rate of

$5,000. Any can choose the application of CGT event F2 when he granted the lease for five

years. However, no CGT discount is applicable for Andy.

Answer B:

As per the “CGT event B1” if the taxpayer forms an agreement with the another

entity where the right of using the CGT asset owned by the owner is passed to another

entity13. The title would be passed to another entity either at the end or before the end of

contract under “subsection 104-15 (1), ITAA 1997”.

On 11th January 2018, an option was granted by John to Farm Ltd so that it can

purchase the 100-acre farm for $800,000. As a result, the passing of title to Farm Ltd is a

CGT event B1 under “subsection 104-15 (1), ITAA 1997”. John can obtain CGT discount for

the capital gains made from the asset.

Answer to C:

Basic exemption is permitted to a capital gains or loss that arises from CGT event

where the CGT asset is dwelling and under “section 118-110 (1), ITAA 1997” taxpayer used

the dwelling as the main residence for the ownership period14. Partial main residence is

12 Pinto, Dale, and Michelle Evans. "Returning income taxation revenue to the states: back to

the future." (2018).

13 Long, Brendan, Jon Campbell, and Carolyn Kelshaw. "The justice lens on taxation policy

in Australia." St Mark's Review235 (2016): 94.

14 Peiros, Katerina, and Christine Smyth. "Successful succession: Tax treatment of executor's

commission." Taxation in Australia 51.7 (2017): 394.

Any owned the land and provides the grants of a lease to Brian at a premium rate of

$5,000. Any can choose the application of CGT event F2 when he granted the lease for five

years. However, no CGT discount is applicable for Andy.

Answer B:

As per the “CGT event B1” if the taxpayer forms an agreement with the another

entity where the right of using the CGT asset owned by the owner is passed to another

entity13. The title would be passed to another entity either at the end or before the end of

contract under “subsection 104-15 (1), ITAA 1997”.

On 11th January 2018, an option was granted by John to Farm Ltd so that it can

purchase the 100-acre farm for $800,000. As a result, the passing of title to Farm Ltd is a

CGT event B1 under “subsection 104-15 (1), ITAA 1997”. John can obtain CGT discount for

the capital gains made from the asset.

Answer to C:

Basic exemption is permitted to a capital gains or loss that arises from CGT event

where the CGT asset is dwelling and under “section 118-110 (1), ITAA 1997” taxpayer used

the dwelling as the main residence for the ownership period14. Partial main residence is

12 Pinto, Dale, and Michelle Evans. "Returning income taxation revenue to the states: back to

the future." (2018).

13 Long, Brendan, Jon Campbell, and Carolyn Kelshaw. "The justice lens on taxation policy

in Australia." St Mark's Review235 (2016): 94.

14 Peiros, Katerina, and Christine Smyth. "Successful succession: Tax treatment of executor's

commission." Taxation in Australia 51.7 (2017): 394.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

applied on dwelling used for generating taxable income. Jamie and Olivia bought a house in

January 2006 and soon it was let out for 2 years. They re-occupied the house to use as main

residence before selling in 2018 to make a capital gain of $300,000. A partial main residence

is permitted to Jamie and Olivia because the house was used for income producing purpose.

As the 12-month ownership rule is satisfied a 50% CGT discount can be applied on capital

gains.

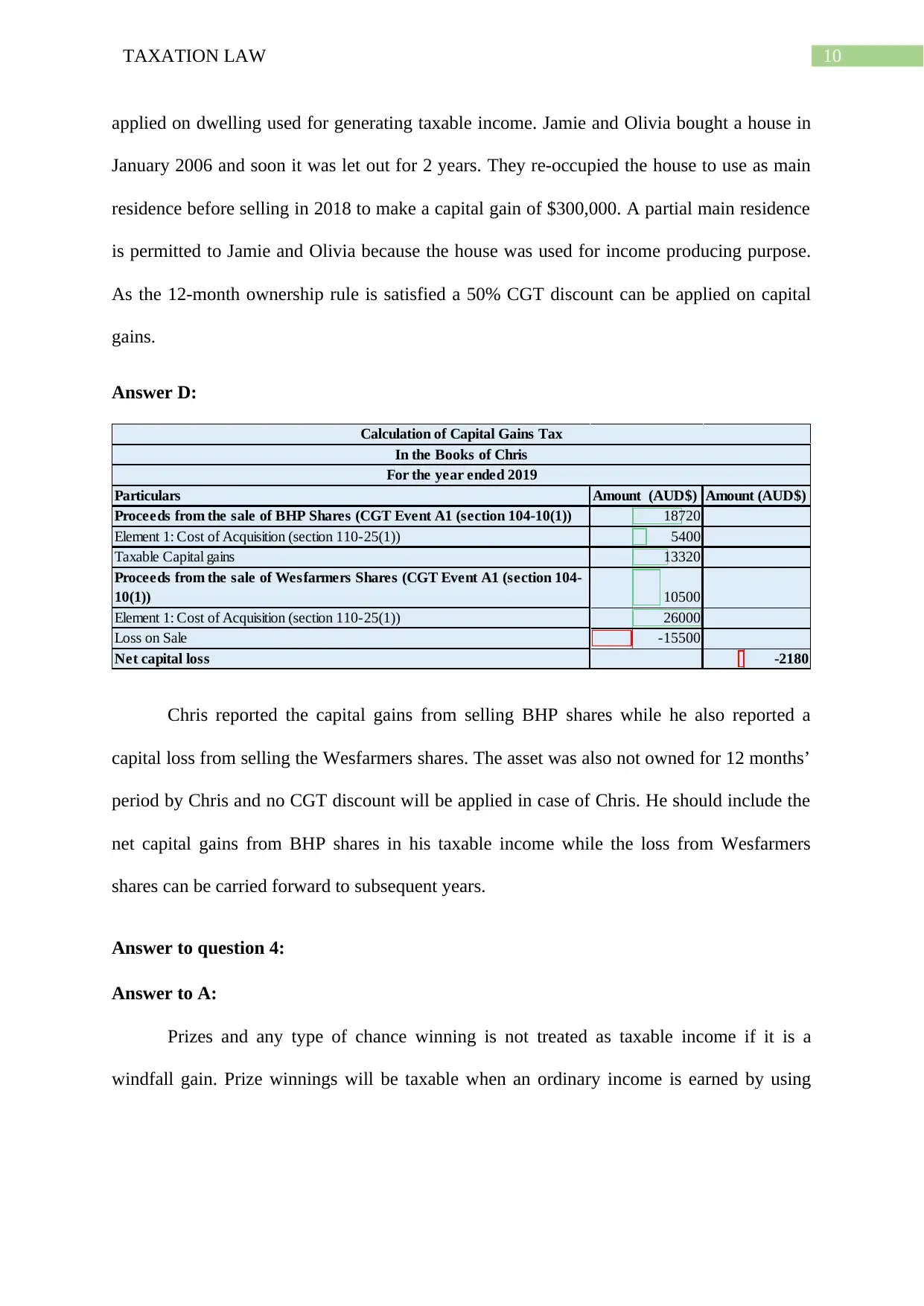

Answer D:

Particulars Amount (AUD$) Amount (AUD$)

Proceeds from the sale of BHP Shares (CGT Event A1 (section 104-10(1)) 18720

Element 1: Cost of Acquisition (section 110-25(1)) 5400

Taxable Capital gains 13320

Proceeds from the sale of Wesfarmers Shares (CGT Event A1 (section 104-

10(1)) 10500

Element 1: Cost of Acquisition (section 110-25(1)) 26000

Loss on Sale -15500

Net capital loss -2180

Calculation of Capital Gains Tax

In the Books of Chris

For the year ended 2019

Chris reported the capital gains from selling BHP shares while he also reported a

capital loss from selling the Wesfarmers shares. The asset was also not owned for 12 months’

period by Chris and no CGT discount will be applied in case of Chris. He should include the

net capital gains from BHP shares in his taxable income while the loss from Wesfarmers

shares can be carried forward to subsequent years.

Answer to question 4:

Answer to A:

Prizes and any type of chance winning is not treated as taxable income if it is a

windfall gain. Prize winnings will be taxable when an ordinary income is earned by using

applied on dwelling used for generating taxable income. Jamie and Olivia bought a house in

January 2006 and soon it was let out for 2 years. They re-occupied the house to use as main

residence before selling in 2018 to make a capital gain of $300,000. A partial main residence

is permitted to Jamie and Olivia because the house was used for income producing purpose.

As the 12-month ownership rule is satisfied a 50% CGT discount can be applied on capital

gains.

Answer D:

Particulars Amount (AUD$) Amount (AUD$)

Proceeds from the sale of BHP Shares (CGT Event A1 (section 104-10(1)) 18720

Element 1: Cost of Acquisition (section 110-25(1)) 5400

Taxable Capital gains 13320

Proceeds from the sale of Wesfarmers Shares (CGT Event A1 (section 104-

10(1)) 10500

Element 1: Cost of Acquisition (section 110-25(1)) 26000

Loss on Sale -15500

Net capital loss -2180

Calculation of Capital Gains Tax

In the Books of Chris

For the year ended 2019

Chris reported the capital gains from selling BHP shares while he also reported a

capital loss from selling the Wesfarmers shares. The asset was also not owned for 12 months’

period by Chris and no CGT discount will be applied in case of Chris. He should include the

net capital gains from BHP shares in his taxable income while the loss from Wesfarmers

shares can be carried forward to subsequent years.

Answer to question 4:

Answer to A:

Prizes and any type of chance winning is not treated as taxable income if it is a

windfall gain. Prize winnings will be taxable when an ordinary income is earned by using

11TAXATION LAW

skill that adequately outweighs windfall gain. In “Kelly v FCT (1985)” the prize money was

held income because it was derived by exercising degree of skill15.

The prize winning from best TV advertisement is assumed to be related to taxpayer

skill and professional. Citing “Kelly v FCT (1985)” the prize money is gained by taxpayer in

ordinary business course and will be taxable as ordinary income under “section 6-5, ITAA

1997”.

Answer to B:

The ATO states that reimbursements are regarded as payments which is made to the

worker for actual expenditure occurred already. In the current case the employee received a

reimbursement of $500 for the cost incurred in traveling for work purpose16. However, the

employee bought a return ticket on sale for only $120. Therefore, it can be interpreted by

stating that remaining amount constitute gain for the employee. The amount will be included

for assessment purpose in accordance with the ordinary concept of “section 6-5, ITAA

1997”.

Answer to C:

Receiving gifts for the personal qualities are not treated as income. As held in the

event of “Scott v FCT (1966)” the solicitor received the 10,000 pound as the gift from the

15 Edmonds, Mark, Christian Holle, and Wendy Hartanti. "Alternative assets insights: Super

funds-tax impediments to going global." Taxation in Australia 49.7 (2015): 413.

16 Butler, Daniel. "Superannuation: Transferring foreign super fund amounts to an Australian

resident." Taxation in Australia50.8 (2016): 481.

skill that adequately outweighs windfall gain. In “Kelly v FCT (1985)” the prize money was

held income because it was derived by exercising degree of skill15.

The prize winning from best TV advertisement is assumed to be related to taxpayer

skill and professional. Citing “Kelly v FCT (1985)” the prize money is gained by taxpayer in

ordinary business course and will be taxable as ordinary income under “section 6-5, ITAA

1997”.

Answer to B:

The ATO states that reimbursements are regarded as payments which is made to the

worker for actual expenditure occurred already. In the current case the employee received a

reimbursement of $500 for the cost incurred in traveling for work purpose16. However, the

employee bought a return ticket on sale for only $120. Therefore, it can be interpreted by

stating that remaining amount constitute gain for the employee. The amount will be included

for assessment purpose in accordance with the ordinary concept of “section 6-5, ITAA

1997”.

Answer to C:

Receiving gifts for the personal qualities are not treated as income. As held in the

event of “Scott v FCT (1966)” the solicitor received the 10,000 pound as the gift from the

15 Edmonds, Mark, Christian Holle, and Wendy Hartanti. "Alternative assets insights: Super

funds-tax impediments to going global." Taxation in Australia 49.7 (2015): 413.

16 Butler, Daniel. "Superannuation: Transferring foreign super fund amounts to an Australian

resident." Taxation in Australia50.8 (2016): 481.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.