Taxation Law of Australia Assignment - Semester 2, 2019, University

VerifiedAdded on 2022/10/07

|20

|4272

|42

Homework Assignment

AI Summary

This document presents a comprehensive solution to a taxation law assignment focusing on the taxation laws of Australia. The assignment addresses several key areas, including small business entities and relevant tax rulings, and gift deductions. It also delves into the marginal tax rates for Australian residents, capital gains tax on personal assets, and the implications of capital event C1. The assignment further explores the tax-free threshold, the legal precedent set by the Hayes vs FCT case, and the distinction between ordinary and statutory income. It also clarifies the differences between the Medicare Levy and Medicare Levy Surcharge. Additionally, it examines the residency status of individuals under TR 98/17. The solution provides detailed analysis of HECS-HELP deductions, travel expenses, book expenses, and childcare costs, along with relevant legislation and case law such as Finn v FCT and FCT v Lodge, to support the arguments and conclusions. The assignment adheres to the Australian Guide to Legal Citation (AGLC) 4th Edition referencing method and provides an in-depth understanding of the complexities of Australian taxation law.

Running head: TAXATION LAW

Taxation Law

Name of the Student:

Name of the University:

Author Note

Taxation Law

Name of the Student:

Name of the University:

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Solution to Question 1:...............................................................................................................3

Solution to part A:..................................................................................................................3

Solution to part B:..................................................................................................................3

Solution to part C:..................................................................................................................3

Solution to part D:..................................................................................................................4

Solution to part E:..................................................................................................................4

Solution to part F:...................................................................................................................4

Solution to part G:..................................................................................................................4

Solution to part H:..................................................................................................................5

Solution to part I:...................................................................................................................6

Solution to Question 2-..............................................................................................................6

Solution to Question 3:...............................................................................................................8

Solution to Question 4:.............................................................................................................12

Solution to part A:................................................................................................................12

Solution to part B:................................................................................................................12

Solution to part C:................................................................................................................13

Solution to part D:................................................................................................................13

Solution to Question 5-............................................................................................................14

Solution to part A:................................................................................................................14

Solution to part B:................................................................................................................14

Table of Contents

Solution to Question 1:...............................................................................................................3

Solution to part A:..................................................................................................................3

Solution to part B:..................................................................................................................3

Solution to part C:..................................................................................................................3

Solution to part D:..................................................................................................................4

Solution to part E:..................................................................................................................4

Solution to part F:...................................................................................................................4

Solution to part G:..................................................................................................................4

Solution to part H:..................................................................................................................5

Solution to part I:...................................................................................................................6

Solution to Question 2-..............................................................................................................6

Solution to Question 3:...............................................................................................................8

Solution to Question 4:.............................................................................................................12

Solution to part A:................................................................................................................12

Solution to part B:................................................................................................................12

Solution to part C:................................................................................................................13

Solution to part D:................................................................................................................13

Solution to Question 5-............................................................................................................14

Solution to part A:................................................................................................................14

Solution to part B:................................................................................................................14

2TAXATION LAW

Solution to part C:................................................................................................................15

Solution to part D:................................................................................................................15

Solution to part E:................................................................................................................16

References:...............................................................................................................................17

Solution to part C:................................................................................................................15

Solution to part D:................................................................................................................15

Solution to part E:................................................................................................................16

References:...............................................................................................................................17

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

Solution to Question 1:

Solution to part A:

According to the “Taxation Ruling of TR 2009/1” when an organization continue its

business operation, which is considering a small business entity generally followed the

viewpoints of a tax commissioner under “Sec-23 of the Income Tax Rates Act 1986”, that are

applicable from the year financial year 2015-16 and 2016-17 or within “sec-328-110, ITAA

1997”1.

Solution to part B:

As per “Division 30, ITAA 1997” Gift or a contribution is allowed for deduction in

order such gift must be consider as donation2.

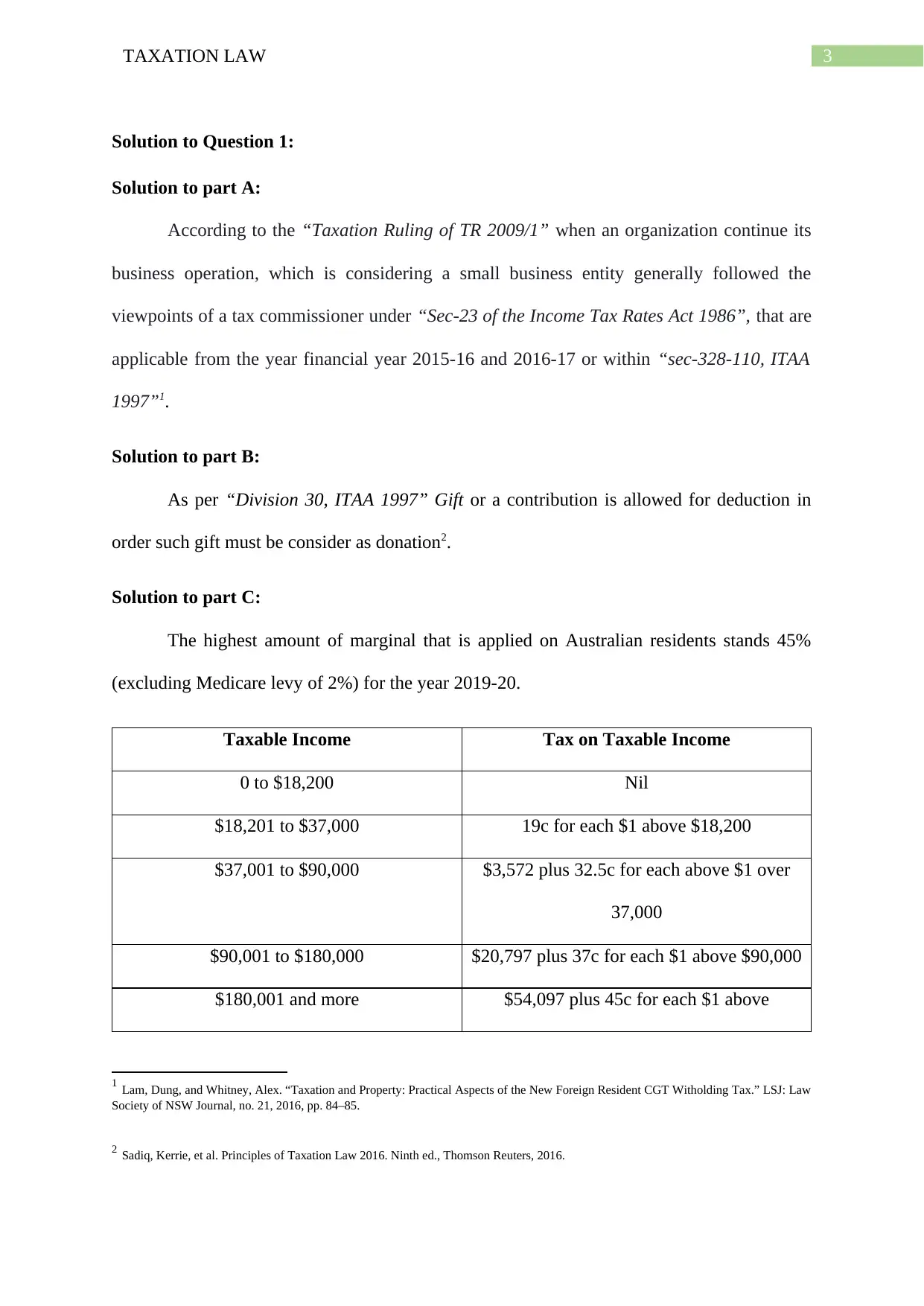

Solution to part C:

The highest amount of marginal that is applied on Australian residents stands 45%

(excluding Medicare levy of 2%) for the year 2019-20.

Taxable Income Tax on Taxable Income

0 to $18,200 Nil

$18,201 to $37,000 19c for each $1 above $18,200

$37,001 to $90,000 $3,572 plus 32.5c for each above $1 over

37,000

$90,001 to $180,000 $20,797 plus 37c for each $1 above $90,000

$180,001 and more $54,097 plus 45c for each $1 above

1 Lam, Dung, and Whitney, Alex. “Taxation and Property: Practical Aspects of the New Foreign Resident CGT Witholding Tax.” LSJ: Law

Society of NSW Journal, no. 21, 2016, pp. 84–85.

2 Sadiq, Kerrie, et al. Principles of Taxation Law 2016. Ninth ed., Thomson Reuters, 2016.

Solution to Question 1:

Solution to part A:

According to the “Taxation Ruling of TR 2009/1” when an organization continue its

business operation, which is considering a small business entity generally followed the

viewpoints of a tax commissioner under “Sec-23 of the Income Tax Rates Act 1986”, that are

applicable from the year financial year 2015-16 and 2016-17 or within “sec-328-110, ITAA

1997”1.

Solution to part B:

As per “Division 30, ITAA 1997” Gift or a contribution is allowed for deduction in

order such gift must be consider as donation2.

Solution to part C:

The highest amount of marginal that is applied on Australian residents stands 45%

(excluding Medicare levy of 2%) for the year 2019-20.

Taxable Income Tax on Taxable Income

0 to $18,200 Nil

$18,201 to $37,000 19c for each $1 above $18,200

$37,001 to $90,000 $3,572 plus 32.5c for each above $1 over

37,000

$90,001 to $180,000 $20,797 plus 37c for each $1 above $90,000

$180,001 and more $54,097 plus 45c for each $1 above

1 Lam, Dung, and Whitney, Alex. “Taxation and Property: Practical Aspects of the New Foreign Resident CGT Witholding Tax.” LSJ: Law

Society of NSW Journal, no. 21, 2016, pp. 84–85.

2 Sadiq, Kerrie, et al. Principles of Taxation Law 2016. Ninth ed., Thomson Reuters, 2016.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

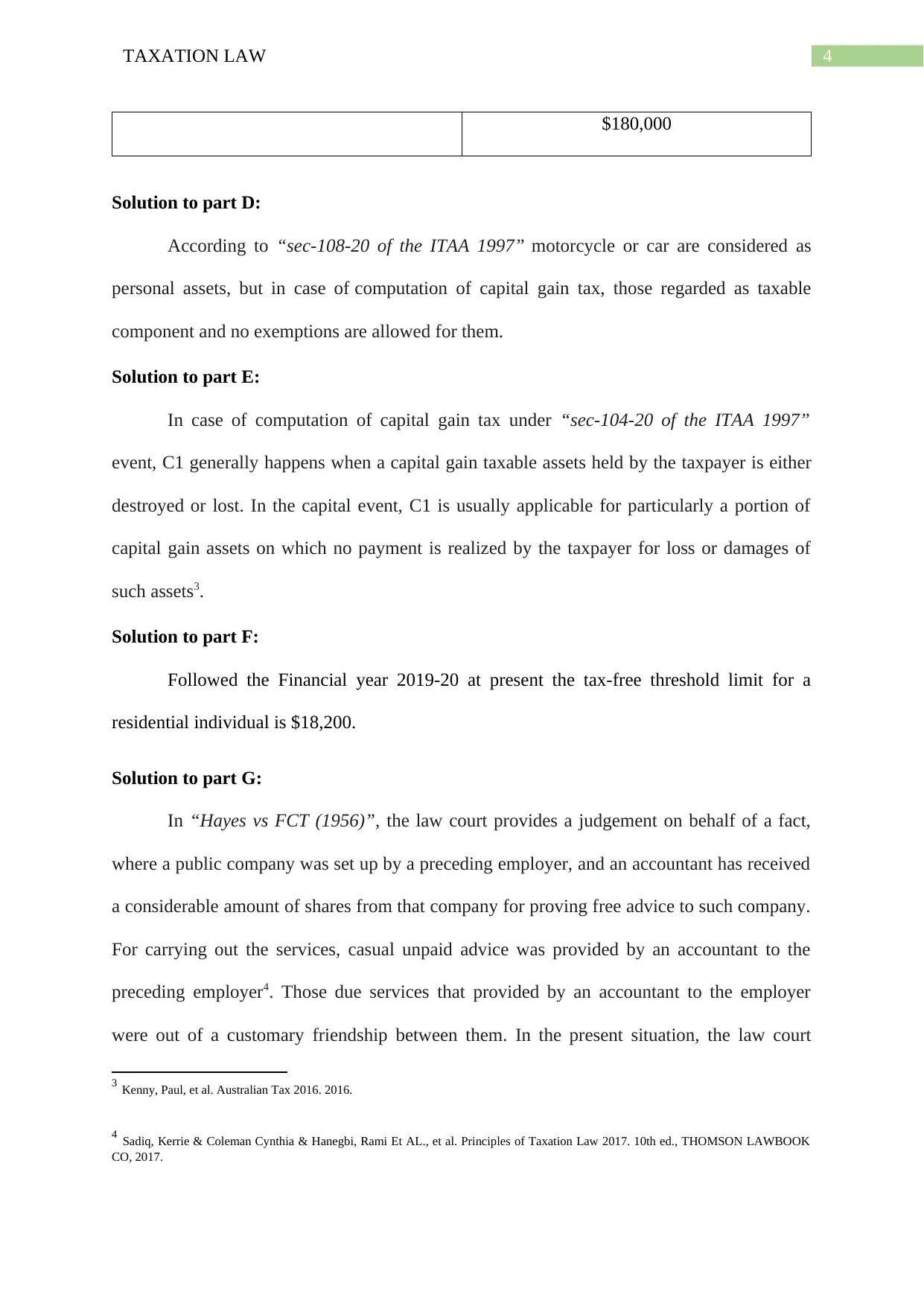

$180,000

Solution to part D:

According to “sec-108-20 of the ITAA 1997” motorcycle or car are considered as

personal assets, but in case of computation of capital gain tax, those regarded as taxable

component and no exemptions are allowed for them.

Solution to part E:

In case of computation of capital gain tax under “sec-104-20 of the ITAA 1997”

event, C1 generally happens when a capital gain taxable assets held by the taxpayer is either

destroyed or lost. In the capital event, C1 is usually applicable for particularly a portion of

capital gain assets on which no payment is realized by the taxpayer for loss or damages of

such assets3.

Solution to part F:

Followed the Financial year 2019-20 at present the tax-free threshold limit for a

residential individual is $18,200.

Solution to part G:

In “Hayes vs FCT (1956)”, the law court provides a judgement on behalf of a fact,

where a public company was set up by a preceding employer, and an accountant has received

a considerable amount of shares from that company for proving free advice to such company.

For carrying out the services, casual unpaid advice was provided by an accountant to the

preceding employer4. Those due services that provided by an accountant to the employer

were out of a customary friendship between them. In the present situation, the law court

3 Kenny, Paul, et al. Australian Tax 2016. 2016.

4 Sadiq, Kerrie & Coleman Cynthia & Hanegbi, Rami Et AL., et al. Principles of Taxation Law 2017. 10th ed., THOMSON LAWBOOK

CO, 2017.

$180,000

Solution to part D:

According to “sec-108-20 of the ITAA 1997” motorcycle or car are considered as

personal assets, but in case of computation of capital gain tax, those regarded as taxable

component and no exemptions are allowed for them.

Solution to part E:

In case of computation of capital gain tax under “sec-104-20 of the ITAA 1997”

event, C1 generally happens when a capital gain taxable assets held by the taxpayer is either

destroyed or lost. In the capital event, C1 is usually applicable for particularly a portion of

capital gain assets on which no payment is realized by the taxpayer for loss or damages of

such assets3.

Solution to part F:

Followed the Financial year 2019-20 at present the tax-free threshold limit for a

residential individual is $18,200.

Solution to part G:

In “Hayes vs FCT (1956)”, the law court provides a judgement on behalf of a fact,

where a public company was set up by a preceding employer, and an accountant has received

a considerable amount of shares from that company for proving free advice to such company.

For carrying out the services, casual unpaid advice was provided by an accountant to the

preceding employer4. Those due services that provided by an accountant to the employer

were out of a customary friendship between them. In the present situation, the law court

3 Kenny, Paul, et al. Australian Tax 2016. 2016.

4 Sadiq, Kerrie & Coleman Cynthia & Hanegbi, Rami Et AL., et al. Principles of Taxation Law 2017. 10th ed., THOMSON LAWBOOK

CO, 2017.

5TAXATION LAW

draws attention through delivering the judgement that in case of any gift derived from relative

and if there is no relation of revenues exist than such contribution will not consider as income

and chargeable to tax as per Income tax act.

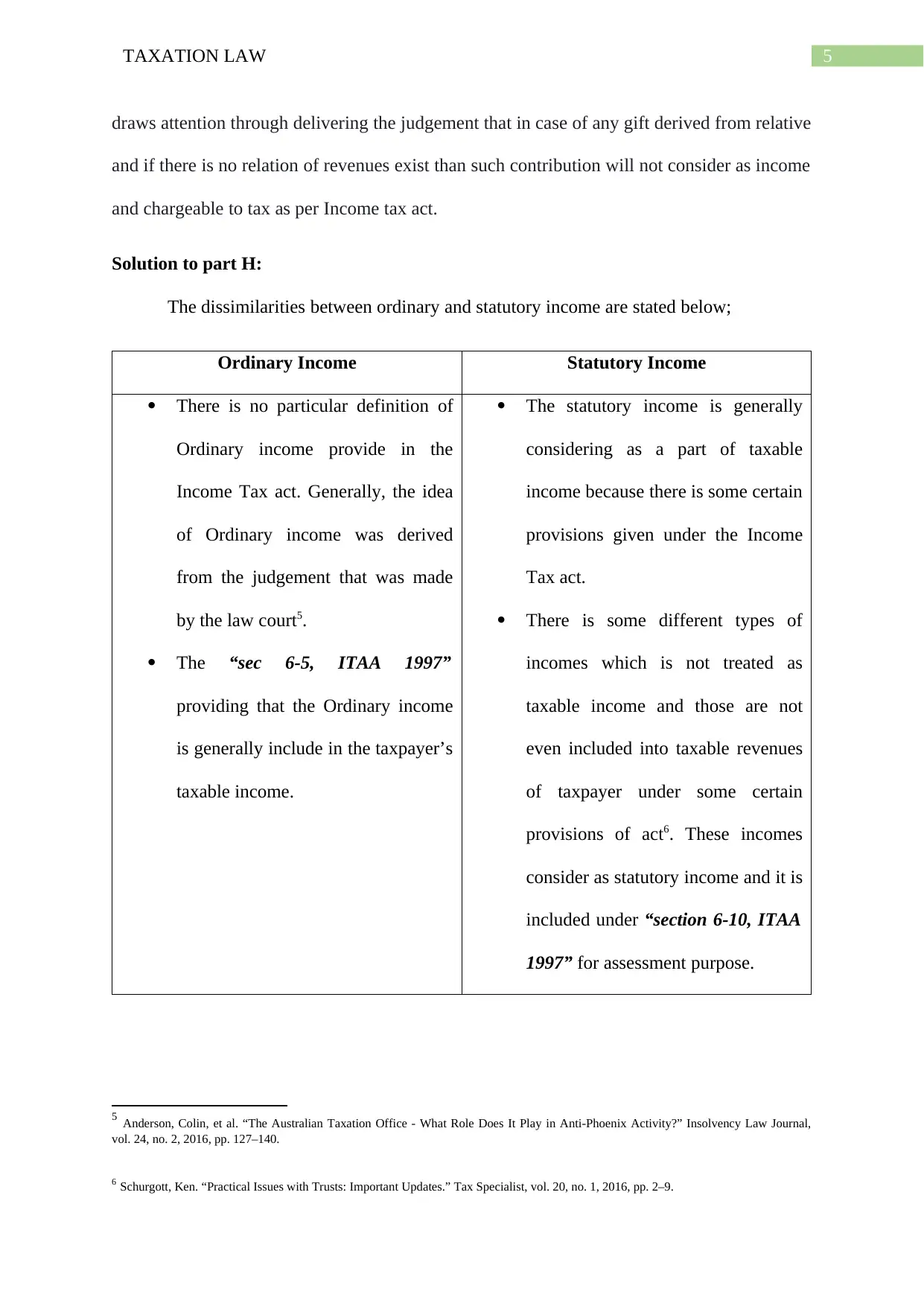

Solution to part H:

The dissimilarities between ordinary and statutory income are stated below;

Ordinary Income Statutory Income

There is no particular definition of

Ordinary income provide in the

Income Tax act. Generally, the idea

of Ordinary income was derived

from the judgement that was made

by the law court5.

The “sec 6-5, ITAA 1997”

providing that the Ordinary income

is generally include in the taxpayer’s

taxable income.

The statutory income is generally

considering as a part of taxable

income because there is some certain

provisions given under the Income

Tax act.

There is some different types of

incomes which is not treated as

taxable income and those are not

even included into taxable revenues

of taxpayer under some certain

provisions of act6. These incomes

consider as statutory income and it is

included under “section 6-10, ITAA

1997” for assessment purpose.

5 Anderson, Colin, et al. “The Australian Taxation Office - What Role Does It Play in Anti-Phoenix Activity?” Insolvency Law Journal,

vol. 24, no. 2, 2016, pp. 127–140.

6 Schurgott, Ken. “Practical Issues with Trusts: Important Updates.” Tax Specialist, vol. 20, no. 1, 2016, pp. 2–9.

draws attention through delivering the judgement that in case of any gift derived from relative

and if there is no relation of revenues exist than such contribution will not consider as income

and chargeable to tax as per Income tax act.

Solution to part H:

The dissimilarities between ordinary and statutory income are stated below;

Ordinary Income Statutory Income

There is no particular definition of

Ordinary income provide in the

Income Tax act. Generally, the idea

of Ordinary income was derived

from the judgement that was made

by the law court5.

The “sec 6-5, ITAA 1997”

providing that the Ordinary income

is generally include in the taxpayer’s

taxable income.

The statutory income is generally

considering as a part of taxable

income because there is some certain

provisions given under the Income

Tax act.

There is some different types of

incomes which is not treated as

taxable income and those are not

even included into taxable revenues

of taxpayer under some certain

provisions of act6. These incomes

consider as statutory income and it is

included under “section 6-10, ITAA

1997” for assessment purpose.

5 Anderson, Colin, et al. “The Australian Taxation Office - What Role Does It Play in Anti-Phoenix Activity?” Insolvency Law Journal,

vol. 24, no. 2, 2016, pp. 127–140.

6 Schurgott, Ken. “Practical Issues with Trusts: Important Updates.” Tax Specialist, vol. 20, no. 1, 2016, pp. 2–9.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

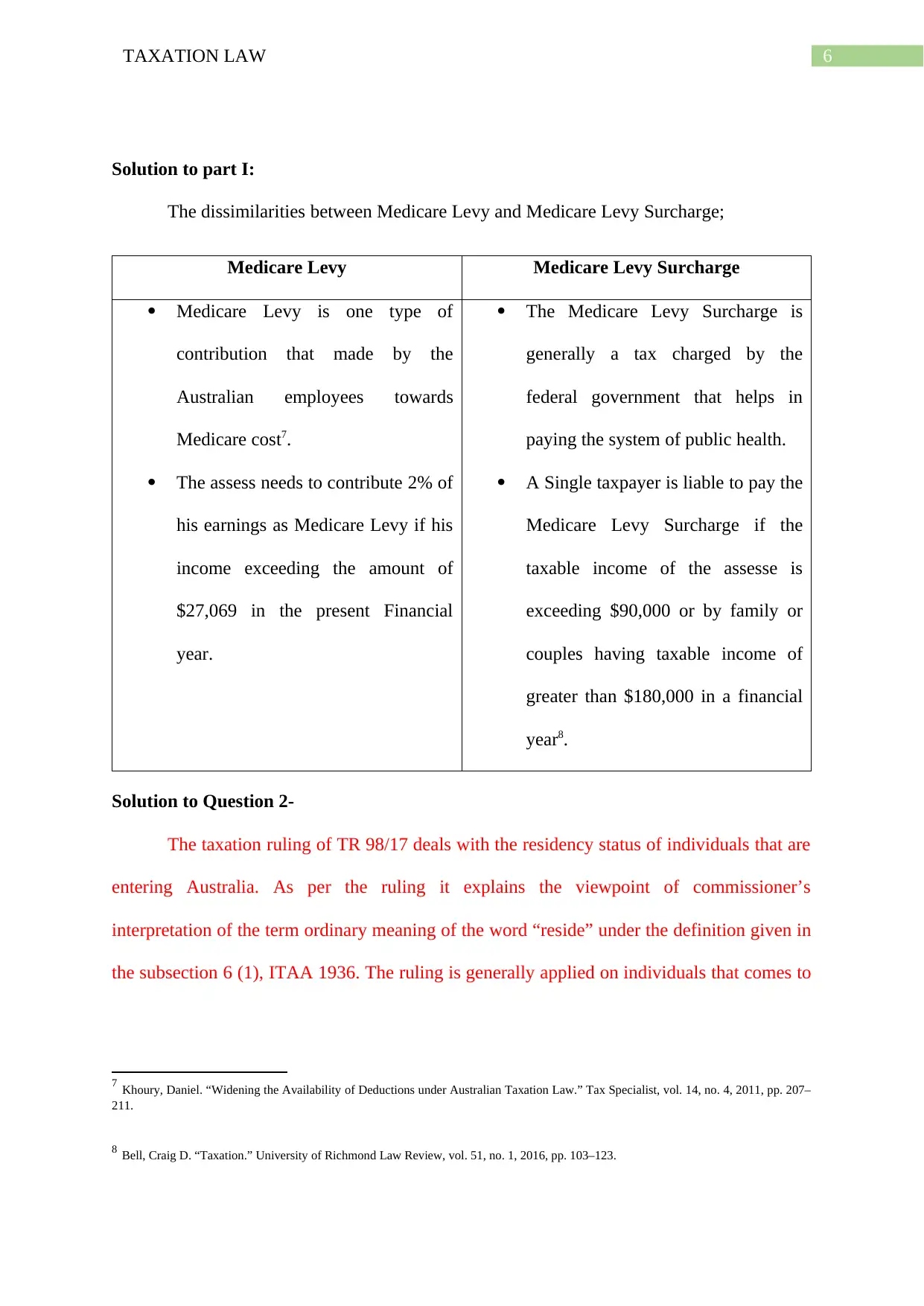

Solution to part I:

The dissimilarities between Medicare Levy and Medicare Levy Surcharge;

Medicare Levy Medicare Levy Surcharge

Medicare Levy is one type of

contribution that made by the

Australian employees towards

Medicare cost7.

The assess needs to contribute 2% of

his earnings as Medicare Levy if his

income exceeding the amount of

$27,069 in the present Financial

year.

The Medicare Levy Surcharge is

generally a tax charged by the

federal government that helps in

paying the system of public health.

A Single taxpayer is liable to pay the

Medicare Levy Surcharge if the

taxable income of the assesse is

exceeding $90,000 or by family or

couples having taxable income of

greater than $180,000 in a financial

year8.

Solution to Question 2-

The taxation ruling of TR 98/17 deals with the residency status of individuals that are

entering Australia. As per the ruling it explains the viewpoint of commissioner’s

interpretation of the term ordinary meaning of the word “reside” under the definition given in

the subsection 6 (1), ITAA 1936. The ruling is generally applied on individuals that comes to

7 Khoury, Daniel. “Widening the Availability of Deductions under Australian Taxation Law.” Tax Specialist, vol. 14, no. 4, 2011, pp. 207–

211.

8 Bell, Craig D. “Taxation.” University of Richmond Law Review, vol. 51, no. 1, 2016, pp. 103–123.

Solution to part I:

The dissimilarities between Medicare Levy and Medicare Levy Surcharge;

Medicare Levy Medicare Levy Surcharge

Medicare Levy is one type of

contribution that made by the

Australian employees towards

Medicare cost7.

The assess needs to contribute 2% of

his earnings as Medicare Levy if his

income exceeding the amount of

$27,069 in the present Financial

year.

The Medicare Levy Surcharge is

generally a tax charged by the

federal government that helps in

paying the system of public health.

A Single taxpayer is liable to pay the

Medicare Levy Surcharge if the

taxable income of the assesse is

exceeding $90,000 or by family or

couples having taxable income of

greater than $180,000 in a financial

year8.

Solution to Question 2-

The taxation ruling of TR 98/17 deals with the residency status of individuals that are

entering Australia. As per the ruling it explains the viewpoint of commissioner’s

interpretation of the term ordinary meaning of the word “reside” under the definition given in

the subsection 6 (1), ITAA 1936. The ruling is generally applied on individuals that comes to

7 Khoury, Daniel. “Widening the Availability of Deductions under Australian Taxation Law.” Tax Specialist, vol. 14, no. 4, 2011, pp. 207–

211.

8 Bell, Craig D. “Taxation.” University of Richmond Law Review, vol. 51, no. 1, 2016, pp. 103–123.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

Australia following a temporary stay in overseas where the individuals continued to be

Australian resident when they were overseas.

The statutory definition given in “subsection 6 (1), ITAA 1936” includes the resident

of Australia as a person who has their domicile in Australia until otherwise the commissioner

is content that the place of abode is out of Australia. The expression “usual place of abode” is

not supposed to be assumed same as the expression “permanent place of abode”. The term

“usual” and “abode” shall be interpreted based on the usual meaning and organized. The

query connected to “usual place of abode” is relative to the matter of the fact. Popularly, the

expression shall be considered as usual residing place or it is popularly used at the time of

physical presence of an individual in that nation. References to the case of Harding v FCT

(2019) can be made where the federal court stated that when assessing the residency of a

person the word “permanent place of abode” must not be interpreted by reference to a

person’s specific dwelling. Rather it must be interpreted whether the person is living

permanently in a particular country or state.

An individual’s “usual place of abode” should be perpetual but it should show the

dwelling quality in comparison to monthly, weekly basis or overnight place of housing for a

traveller9. It comprises a relation, which is long-term in nature with the payer of tax having a

place of residence over those who generally have been dwelling or have their “usual place of

abode” inside Australia.

If the payer of tax has “usual place of abode” inside Australia and also includes no

fixed place of residence in a foreign country but moves from one country to another or

relocates constantly in the domestic country or has relation with particular overseas place,

then the living will not be permanent. In this case, the payer of tax will not be accepted to

9 Lee, Yooree. “Australian Practice in International Law 2016.” Australian Yearbook of International Law, vol. 35, 2017, pp. 373–508.

Australia following a temporary stay in overseas where the individuals continued to be

Australian resident when they were overseas.

The statutory definition given in “subsection 6 (1), ITAA 1936” includes the resident

of Australia as a person who has their domicile in Australia until otherwise the commissioner

is content that the place of abode is out of Australia. The expression “usual place of abode” is

not supposed to be assumed same as the expression “permanent place of abode”. The term

“usual” and “abode” shall be interpreted based on the usual meaning and organized. The

query connected to “usual place of abode” is relative to the matter of the fact. Popularly, the

expression shall be considered as usual residing place or it is popularly used at the time of

physical presence of an individual in that nation. References to the case of Harding v FCT

(2019) can be made where the federal court stated that when assessing the residency of a

person the word “permanent place of abode” must not be interpreted by reference to a

person’s specific dwelling. Rather it must be interpreted whether the person is living

permanently in a particular country or state.

An individual’s “usual place of abode” should be perpetual but it should show the

dwelling quality in comparison to monthly, weekly basis or overnight place of housing for a

traveller9. It comprises a relation, which is long-term in nature with the payer of tax having a

place of residence over those who generally have been dwelling or have their “usual place of

abode” inside Australia.

If the payer of tax has “usual place of abode” inside Australia and also includes no

fixed place of residence in a foreign country but moves from one country to another or

relocates constantly in the domestic country or has relation with particular overseas place,

then the living will not be permanent. In this case, the payer of tax will not be accepted to

9 Lee, Yooree. “Australian Practice in International Law 2016.” Australian Yearbook of International Law, vol. 35, 2017, pp. 373–508.

8TAXATION LAW

have taken other living place of their option or “permanent place of abode” external to

Australia.

The concept “permanent place of abode” means the assesse has their residence in

Australia. According to the “subparagraph (a) (i)’’, the concept of “resident” is deriving that

it needs to satisfy the tax commissioner that the assessment must have “permanent place of

abode” is within Australia10. The concept of “place of abode” means that an individual must

have a dwelling where he and his family stay together. Even in “Levene v IRC (1928)” the

law court is providing that same concept relates to the home of an assessed.

The example of leading is “FCT v Applegate (1979)” it was an Australian residence

that understood the taxpayers, as well as it travelled the New Hebrides to establish an office

branch the tax payer for that relevant year was considered non-resident as held by the

commissioner using the principle of permanent place of abode11.

Alternatively, in case of “FCT v Jenkins (1982)” the taxpayer was considered as bank

officer who shifted to New Hebrides for the duration of 3 years and he had come back to

Australia after the duration of 18 months only because of sickness. The court further

explained about the taxpayers that it was the permanent place for the abode” was not at all in

Australia all the year and he had not spent any time for living in place of New Hebrides. Both

the cases explained about permanent place of abode and it cannot be judged through

implementation of hard as well as fast rules.

The above discussion makes clear that the taxpayer should be made satisfied about

usual place of abode which is outside the place of Australia on the other hand the test makes

10 Spence, Ken. “The Evolution of Corporate Taxation - a Work in Progress.” AUSTRALIAN TAX FORUM, vol. 31, no. 3, 2016, pp. 481–

508.

11 Pert, Alison, et al. “Macoun v Commissioner of Taxation [2015] HCA 44.” Australian Year Book of International Law, vol. 34, 2016, pp.

207–210.

have taken other living place of their option or “permanent place of abode” external to

Australia.

The concept “permanent place of abode” means the assesse has their residence in

Australia. According to the “subparagraph (a) (i)’’, the concept of “resident” is deriving that

it needs to satisfy the tax commissioner that the assessment must have “permanent place of

abode” is within Australia10. The concept of “place of abode” means that an individual must

have a dwelling where he and his family stay together. Even in “Levene v IRC (1928)” the

law court is providing that same concept relates to the home of an assessed.

The example of leading is “FCT v Applegate (1979)” it was an Australian residence

that understood the taxpayers, as well as it travelled the New Hebrides to establish an office

branch the tax payer for that relevant year was considered non-resident as held by the

commissioner using the principle of permanent place of abode11.

Alternatively, in case of “FCT v Jenkins (1982)” the taxpayer was considered as bank

officer who shifted to New Hebrides for the duration of 3 years and he had come back to

Australia after the duration of 18 months only because of sickness. The court further

explained about the taxpayers that it was the permanent place for the abode” was not at all in

Australia all the year and he had not spent any time for living in place of New Hebrides. Both

the cases explained about permanent place of abode and it cannot be judged through

implementation of hard as well as fast rules.

The above discussion makes clear that the taxpayer should be made satisfied about

usual place of abode which is outside the place of Australia on the other hand the test makes

10 Spence, Ken. “The Evolution of Corporate Taxation - a Work in Progress.” AUSTRALIAN TAX FORUM, vol. 31, no. 3, 2016, pp. 481–

508.

11 Pert, Alison, et al. “Macoun v Commissioner of Taxation [2015] HCA 44.” Australian Year Book of International Law, vol. 34, 2016, pp.

207–210.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

necessary for a person to get satisfied about permanent place for abode which is not existed in

place of Australia.

Solution to Question 3:

HECS HELP: $850

As per ATO, taxpayer is permitted for deduction of permissible income tax with

respect to certain outgoings for self-education such that all the expenses are as per taxpayer’s

assessable earnings. As per ATO, if the expenses are incurred by individual in respect to self-

education and if the eligibility criteria get satisfied then Free-Help or VET or even loan

provided to the student as per HECS-HELP will not be considered for further deduction12. On

the other hand, inside the HECS-HELP the expenses amounting to $850 is considered to be

as expenditure which is non-deductible.

Travel-work for university $110:

Generally, expenditure which are considered to be as deductible involves the

maintenance as well as increase of taxpayer’s skills in case of service being presently

engaged specially in case of outgoings for improvement in the income for future for

providing possibility to the taxpayer.

As per “Finn v FCT (1961)” permissible income tax deduction is allowed to the

architect who has been employed by the Government of WA for expenditure related to

travelling reacted to overseas travelling in a particular year in order to study about

architecture13. As per the court tour was quite associated in nature and closely connected for

taxpayer’s employment.

12 Tully, Stephen. “Taxation: Interpreting Bilateral Tax Treaties.” LSJ: Law Society of NSW Journal, no. 28, 2016, pp. 76–77.

13 Margarita A. Vakhtina. “Progressive Taxation as a Tool for Providing the Budget System Stability.” Aktualʹnye Problemy Èkonomiki i

Prava, vol. 10, no. 2, 2016, pp. 68–79.

necessary for a person to get satisfied about permanent place for abode which is not existed in

place of Australia.

Solution to Question 3:

HECS HELP: $850

As per ATO, taxpayer is permitted for deduction of permissible income tax with

respect to certain outgoings for self-education such that all the expenses are as per taxpayer’s

assessable earnings. As per ATO, if the expenses are incurred by individual in respect to self-

education and if the eligibility criteria get satisfied then Free-Help or VET or even loan

provided to the student as per HECS-HELP will not be considered for further deduction12. On

the other hand, inside the HECS-HELP the expenses amounting to $850 is considered to be

as expenditure which is non-deductible.

Travel-work for university $110:

Generally, expenditure which are considered to be as deductible involves the

maintenance as well as increase of taxpayer’s skills in case of service being presently

engaged specially in case of outgoings for improvement in the income for future for

providing possibility to the taxpayer.

As per “Finn v FCT (1961)” permissible income tax deduction is allowed to the

architect who has been employed by the Government of WA for expenditure related to

travelling reacted to overseas travelling in a particular year in order to study about

architecture13. As per the court tour was quite associated in nature and closely connected for

taxpayer’s employment.

12 Tully, Stephen. “Taxation: Interpreting Bilateral Tax Treaties.” LSJ: Law Society of NSW Journal, no. 28, 2016, pp. 76–77.

13 Margarita A. Vakhtina. “Progressive Taxation as a Tool for Providing the Budget System Stability.” Aktualʹnye Problemy Èkonomiki i

Prava, vol. 10, no. 2, 2016, pp. 68–79.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

With respect to the current case travel that is related to the work from University will

be accepted for being considered for deduction as per “section 8-1, ITTA 1997” as

expenditure related to travel was quite happening in nature as well closely connected to the

taxpayer’s employment14.

Books $200:

Expenditure related to self-education in cost that is related for study-materials like-

calculators, textbooks as well as stationery in order to improve the promotion as well as

earning capacities of the taxpayers is considered for deduction under “section 8-1, ITAA

1997”. As per “FCT v Highfield (1982)” general practice that has been carried by dentist

was considered for permissible deduction in case of any outgoings that would be closely

connected to fees as well as for accommodation in case of self-education expenses

undertaking15.

As per the current case expenses related to books will be considered to be acceptable

for deduction as per “section 8-1, ITAA 1997” as expenses were considered for bringing

improvement in the promotion for future as well as capacities of earning of the taxpayer.

Childcare for her evening classes $80:

According to “section 8-1(2)(b), ITAA 1997” expenses that are considered to be

domestic as well as private in the nature is not considered for further deduction as criterion

does not meet under positivity and on the other hand is non-deductible as per negativity

norms. As per “FCT v Lodge(1972)” the court did not give permission for the deduction for

taxpayer in case of expenses for the child care for getting her child being minded as well as

14 Hopkins, Bruce R. The Law of Tax-Exempt Organizations. 11th ed., 2016.

15 Diederichs A, et al. “ANALYSIS OF THE GUIDELINES FOR CLASSIFICATION OFADVERTISING COSTS IN TAXATION.”

International Journal of Economics and Finance Studies, vol. 8, no. 2, 2016, pp. 147–158.

With respect to the current case travel that is related to the work from University will

be accepted for being considered for deduction as per “section 8-1, ITTA 1997” as

expenditure related to travel was quite happening in nature as well closely connected to the

taxpayer’s employment14.

Books $200:

Expenditure related to self-education in cost that is related for study-materials like-

calculators, textbooks as well as stationery in order to improve the promotion as well as

earning capacities of the taxpayers is considered for deduction under “section 8-1, ITAA

1997”. As per “FCT v Highfield (1982)” general practice that has been carried by dentist

was considered for permissible deduction in case of any outgoings that would be closely

connected to fees as well as for accommodation in case of self-education expenses

undertaking15.

As per the current case expenses related to books will be considered to be acceptable

for deduction as per “section 8-1, ITAA 1997” as expenses were considered for bringing

improvement in the promotion for future as well as capacities of earning of the taxpayer.

Childcare for her evening classes $80:

According to “section 8-1(2)(b), ITAA 1997” expenses that are considered to be

domestic as well as private in the nature is not considered for further deduction as criterion

does not meet under positivity and on the other hand is non-deductible as per negativity

norms. As per “FCT v Lodge(1972)” the court did not give permission for the deduction for

taxpayer in case of expenses for the child care for getting her child being minded as well as

14 Hopkins, Bruce R. The Law of Tax-Exempt Organizations. 11th ed., 2016.

15 Diederichs A, et al. “ANALYSIS OF THE GUIDELINES FOR CLASSIFICATION OFADVERTISING COSTS IN TAXATION.”

International Journal of Economics and Finance Studies, vol. 8, no. 2, 2016, pp. 147–158.

11TAXATION LAW

she also remains present to her work16. As per the court expenses could not remain closely

connected to income producing activities of taxpayer.

On the other hand, in current situation the expenses related to childcare amounting to

$80 paid by the taxpayer for being present in the evening classes were not connected to

income producing activities of the taxpayer.

Repair of her fridge at home for $250:

An individual as a taxpayer is not permitted for claiming deduction as per “section 8-

1(2)(b), ITAA 1997” to that extent that outgoings are considered to be private as well as

domestic in their nature. As per court in “Lunney v FCT (1958)” it is made essential to

determine the loss as well as outgoings to be considered as significant prerequisite in terms of

taxable returns sourcing17. Similarly, repairs for fringe at the home for approximately $250

cannot be considered for further deduction as per “section 8-1(2)(b), ITAA 1997” as expenses

are considered to be as private and domestic in the nature and on the other hand it cannot be

as such significant prerequisite in case of taxable earnings sourcing.

Black trousers as well as shirt is necessary to be worn at office at approximately $145:

Cost for purchasing ordinary items of clothing in case of suit is not considered for

further deduction as per “section 8-1, ITAA 1997”. As per law court “Mansfield v FCT

(1996)” general expenses in case of ordinary articles of apparel could not be accepted as

deductions in spite of fact that expenses would be essential for suitable existence for

maintenance of specific job.

16 Graetz, M., Schenk, D., Freeland, J., Lathrope, D., Lind, S., Stephens, R., ... & Keyes, K. (2015). Federal Income Taxation, Principles

and Policies (University Casebook Series). Foundation Press/West Academic.

17 Bankman, Joseph, et al. Federal Income Taxation. Aspen Publishers, 2018.

she also remains present to her work16. As per the court expenses could not remain closely

connected to income producing activities of taxpayer.

On the other hand, in current situation the expenses related to childcare amounting to

$80 paid by the taxpayer for being present in the evening classes were not connected to

income producing activities of the taxpayer.

Repair of her fridge at home for $250:

An individual as a taxpayer is not permitted for claiming deduction as per “section 8-

1(2)(b), ITAA 1997” to that extent that outgoings are considered to be private as well as

domestic in their nature. As per court in “Lunney v FCT (1958)” it is made essential to

determine the loss as well as outgoings to be considered as significant prerequisite in terms of

taxable returns sourcing17. Similarly, repairs for fringe at the home for approximately $250

cannot be considered for further deduction as per “section 8-1(2)(b), ITAA 1997” as expenses

are considered to be as private and domestic in the nature and on the other hand it cannot be

as such significant prerequisite in case of taxable earnings sourcing.

Black trousers as well as shirt is necessary to be worn at office at approximately $145:

Cost for purchasing ordinary items of clothing in case of suit is not considered for

further deduction as per “section 8-1, ITAA 1997”. As per law court “Mansfield v FCT

(1996)” general expenses in case of ordinary articles of apparel could not be accepted as

deductions in spite of fact that expenses would be essential for suitable existence for

maintenance of specific job.

16 Graetz, M., Schenk, D., Freeland, J., Lathrope, D., Lind, S., Stephens, R., ... & Keyes, K. (2015). Federal Income Taxation, Principles

and Policies (University Casebook Series). Foundation Press/West Academic.

17 Bankman, Joseph, et al. Federal Income Taxation. Aspen Publishers, 2018.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.