Tax Law Assignment: Analyzing Company and Individual Tax Obligations

VerifiedAdded on 2022/11/25

|30

|5219

|396

Homework Assignment

AI Summary

This assignment provides a detailed analysis of Australian taxation law, covering various aspects of company and individual tax liabilities. It includes calculations for taxable income, tax payable, and Medicare levy for companies and individuals, considering different income sources like professional fees, salaries, dividends, and rental income. The assignment also explores capital gains tax (CGT) calculations, including capital losses and gains from property and share transactions, as well as fringe benefits tax (FBT). It addresses partnership income, the tax implications for child partners, and trust net income distributions. Furthermore, the assignment includes working notes and calculations to illustrate the application of relevant tax laws and regulations, making it a comprehensive resource for understanding Australian taxation principles. The assignment covers a wide range of tax scenarios, from calculating individual tax liabilities to analyzing complex business transactions, providing a practical understanding of the Australian tax system.

Australian Taxation Law

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

QUESTION ONE.......................................................................................................................4

QUESTION TWO......................................................................................................................4

QUESTION THREE..................................................................................................................5

QUESTION ONE.......................................................................................................................6

QUESTION TWO......................................................................................................................7

QUESTION THREE..................................................................................................................8

SECTION A.............................................................................................................................10

QUESTION 1...........................................................................................................................10

QUIESTION 2.........................................................................................................................10

Part A..................................................................................................................................10

Part B...................................................................................................................................12

QUESTION 3...........................................................................................................................13

a)..........................................................................................................................................13

b)..........................................................................................................................................14

QUESTION 4...........................................................................................................................15

Part A..................................................................................................................................15

Part B...................................................................................................................................16

QUESTION ONE.....................................................................................................................18

QUESTION TWO....................................................................................................................19

QUESTION THREE................................................................................................................20

QUESTION ONE.....................................................................................................................21

QUESTION TWO....................................................................................................................22

QUESTION THREE................................................................................................................24

QUESTION ONE.....................................................................................................................25

QUESTION TWO....................................................................................................................26

QUESTION THREE................................................................................................................27

QUESTION ONE.......................................................................................................................4

QUESTION TWO......................................................................................................................4

QUESTION THREE..................................................................................................................5

QUESTION ONE.......................................................................................................................6

QUESTION TWO......................................................................................................................7

QUESTION THREE..................................................................................................................8

SECTION A.............................................................................................................................10

QUESTION 1...........................................................................................................................10

QUIESTION 2.........................................................................................................................10

Part A..................................................................................................................................10

Part B...................................................................................................................................12

QUESTION 3...........................................................................................................................13

a)..........................................................................................................................................13

b)..........................................................................................................................................14

QUESTION 4...........................................................................................................................15

Part A..................................................................................................................................15

Part B...................................................................................................................................16

QUESTION ONE.....................................................................................................................18

QUESTION TWO....................................................................................................................19

QUESTION THREE................................................................................................................20

QUESTION ONE.....................................................................................................................21

QUESTION TWO....................................................................................................................22

QUESTION THREE................................................................................................................24

QUESTION ONE.....................................................................................................................25

QUESTION TWO....................................................................................................................26

QUESTION THREE................................................................................................................27

REFERENCES.........................................................................................................................29

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

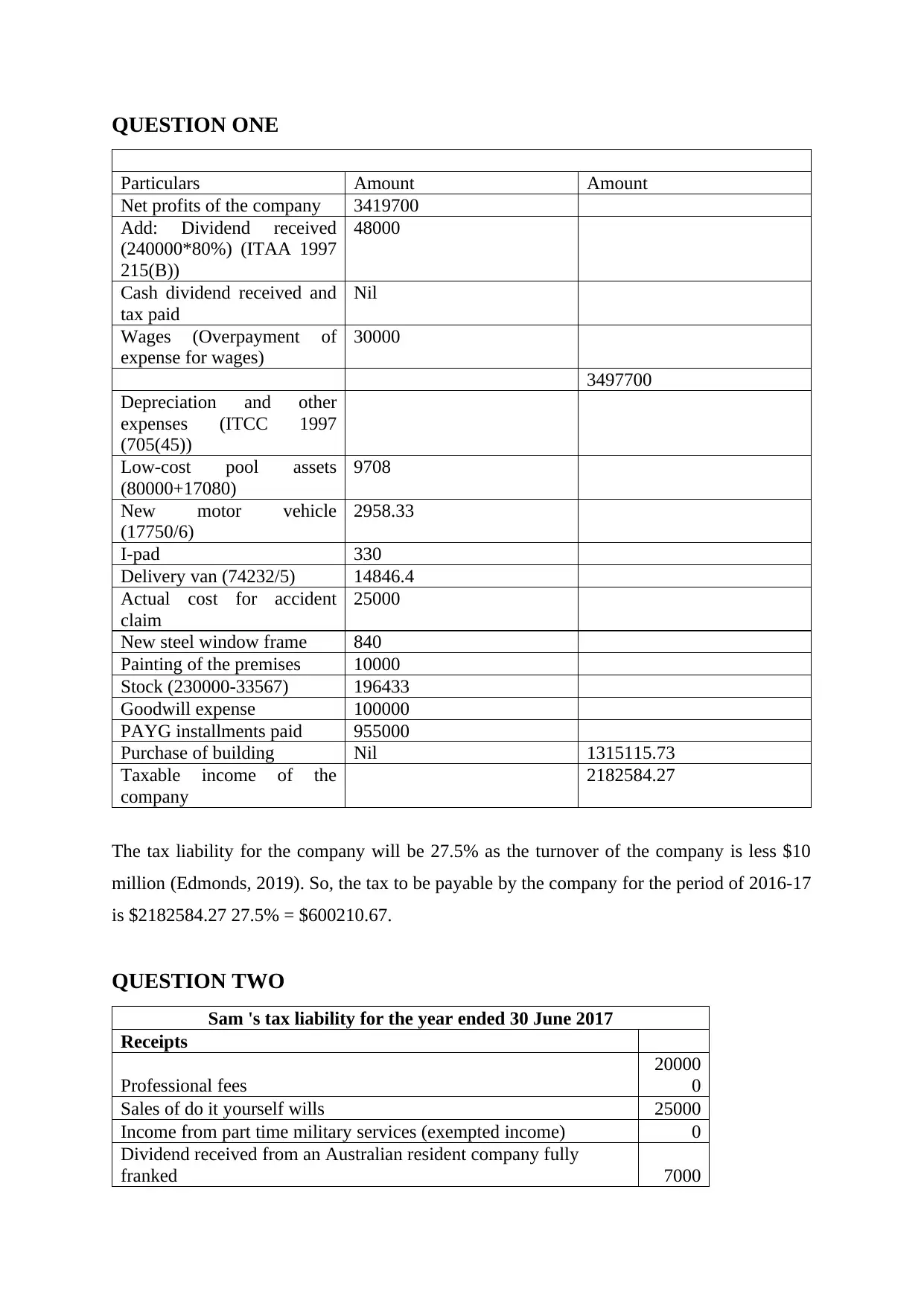

QUESTION ONE

Particulars Amount Amount

Net profits of the company 3419700

Add: Dividend received

(240000*80%) (ITAA 1997

215(B))

48000

Cash dividend received and

tax paid

Nil

Wages (Overpayment of

expense for wages)

30000

3497700

Depreciation and other

expenses (ITCC 1997

(705(45))

Low-cost pool assets

(80000+17080)

9708

New motor vehicle

(17750/6)

2958.33

I-pad 330

Delivery van (74232/5) 14846.4

Actual cost for accident

claim

25000

New steel window frame 840

Painting of the premises 10000

Stock (230000-33567) 196433

Goodwill expense 100000

PAYG installments paid 955000

Purchase of building Nil 1315115.73

Taxable income of the

company

2182584.27

The tax liability for the company will be 27.5% as the turnover of the company is less $10

million (Edmonds, 2019). So, the tax to be payable by the company for the period of 2016-17

is $2182584.27 27.5% = $600210.67.

QUESTION TWO

Sam 's tax liability for the year ended 30 June 2017

Receipts

Professional fees

20000

0

Sales of do it yourself wills 25000

Income from part time military services (exempted income) 0

Dividend received from an Australian resident company fully

franked 7000

Particulars Amount Amount

Net profits of the company 3419700

Add: Dividend received

(240000*80%) (ITAA 1997

215(B))

48000

Cash dividend received and

tax paid

Nil

Wages (Overpayment of

expense for wages)

30000

3497700

Depreciation and other

expenses (ITCC 1997

(705(45))

Low-cost pool assets

(80000+17080)

9708

New motor vehicle

(17750/6)

2958.33

I-pad 330

Delivery van (74232/5) 14846.4

Actual cost for accident

claim

25000

New steel window frame 840

Painting of the premises 10000

Stock (230000-33567) 196433

Goodwill expense 100000

PAYG installments paid 955000

Purchase of building Nil 1315115.73

Taxable income of the

company

2182584.27

The tax liability for the company will be 27.5% as the turnover of the company is less $10

million (Edmonds, 2019). So, the tax to be payable by the company for the period of 2016-17

is $2182584.27 27.5% = $600210.67.

QUESTION TWO

Sam 's tax liability for the year ended 30 June 2017

Receipts

Professional fees

20000

0

Sales of do it yourself wills 25000

Income from part time military services (exempted income) 0

Dividend received from an Australian resident company fully

franked 7000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

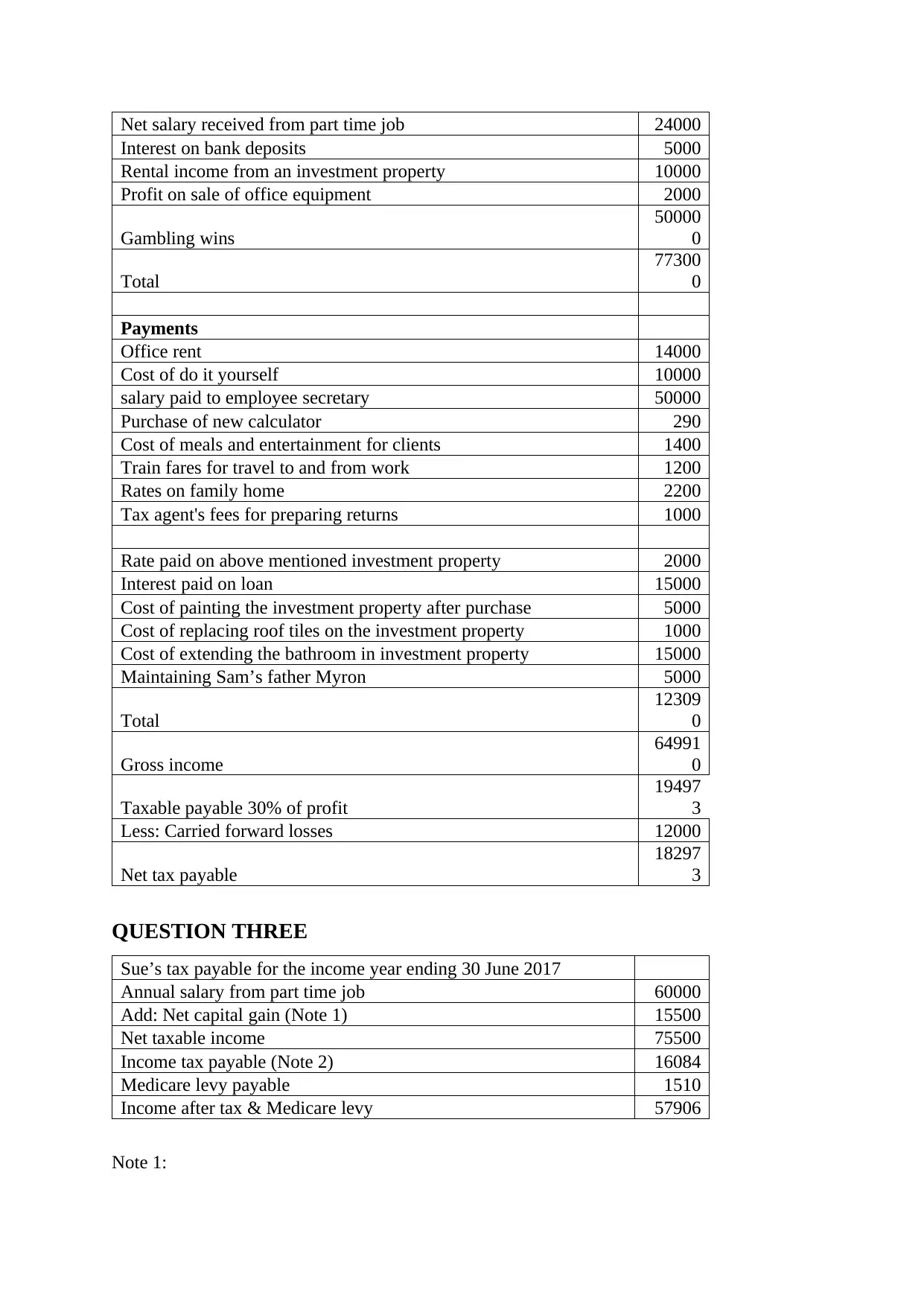

Net salary received from part time job 24000

Interest on bank deposits 5000

Rental income from an investment property 10000

Profit on sale of office equipment 2000

Gambling wins

50000

0

Total

77300

0

Payments

Office rent 14000

Cost of do it yourself 10000

salary paid to employee secretary 50000

Purchase of new calculator 290

Cost of meals and entertainment for clients 1400

Train fares for travel to and from work 1200

Rates on family home 2200

Tax agent's fees for preparing returns 1000

Rate paid on above mentioned investment property 2000

Interest paid on loan 15000

Cost of painting the investment property after purchase 5000

Cost of replacing roof tiles on the investment property 1000

Cost of extending the bathroom in investment property 15000

Maintaining Sam’s father Myron 5000

Total

12309

0

Gross income

64991

0

Taxable payable 30% of profit

19497

3

Less: Carried forward losses 12000

Net tax payable

18297

3

QUESTION THREE

Sue’s tax payable for the income year ending 30 June 2017

Annual salary from part time job 60000

Add: Net capital gain (Note 1) 15500

Net taxable income 75500

Income tax payable (Note 2) 16084

Medicare levy payable 1510

Income after tax & Medicare levy 57906

Note 1:

Interest on bank deposits 5000

Rental income from an investment property 10000

Profit on sale of office equipment 2000

Gambling wins

50000

0

Total

77300

0

Payments

Office rent 14000

Cost of do it yourself 10000

salary paid to employee secretary 50000

Purchase of new calculator 290

Cost of meals and entertainment for clients 1400

Train fares for travel to and from work 1200

Rates on family home 2200

Tax agent's fees for preparing returns 1000

Rate paid on above mentioned investment property 2000

Interest paid on loan 15000

Cost of painting the investment property after purchase 5000

Cost of replacing roof tiles on the investment property 1000

Cost of extending the bathroom in investment property 15000

Maintaining Sam’s father Myron 5000

Total

12309

0

Gross income

64991

0

Taxable payable 30% of profit

19497

3

Less: Carried forward losses 12000

Net tax payable

18297

3

QUESTION THREE

Sue’s tax payable for the income year ending 30 June 2017

Annual salary from part time job 60000

Add: Net capital gain (Note 1) 15500

Net taxable income 75500

Income tax payable (Note 2) 16084

Medicare levy payable 1510

Income after tax & Medicare levy 57906

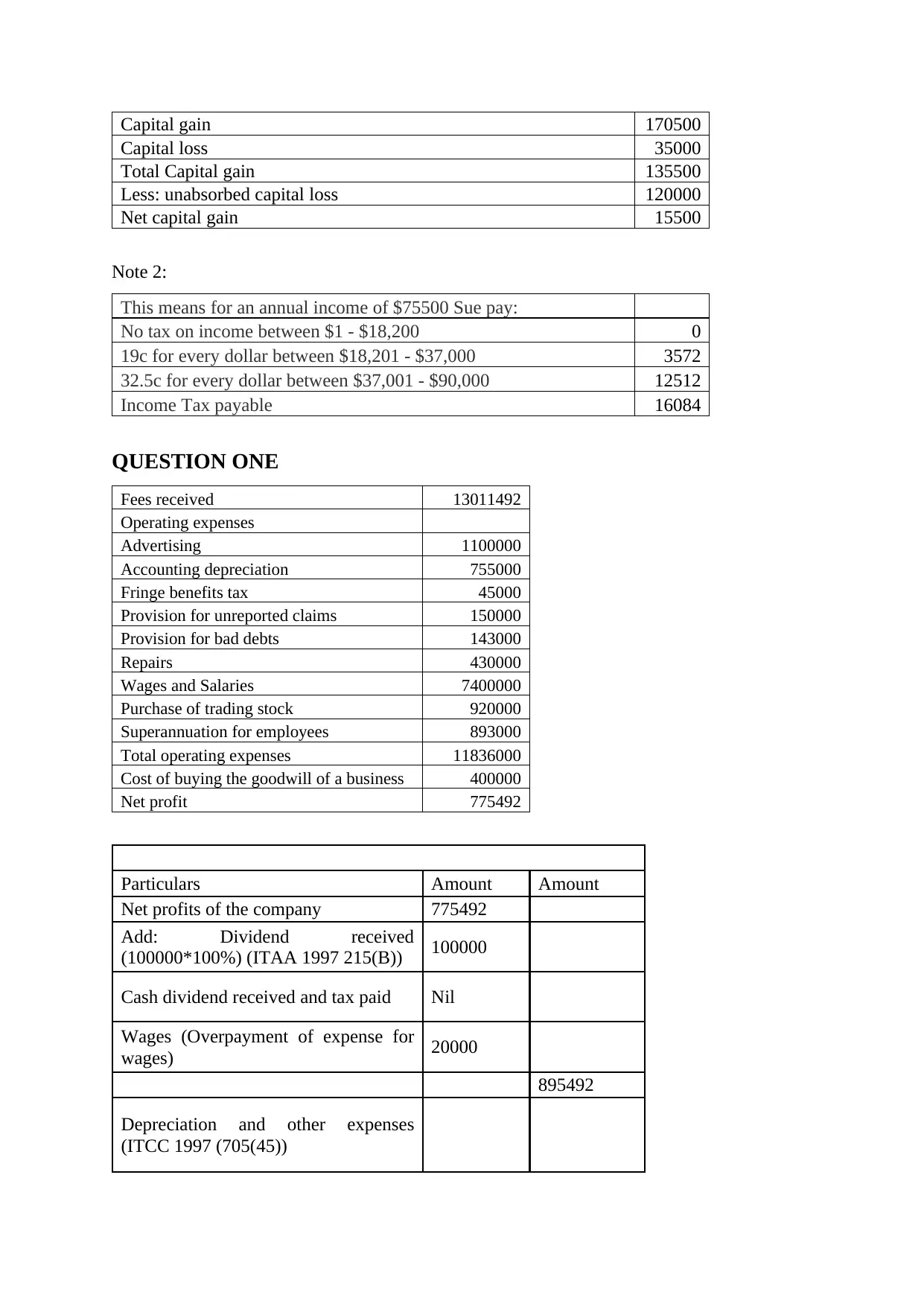

Note 1:

Capital gain 170500

Capital loss 35000

Total Capital gain 135500

Less: unabsorbed capital loss 120000

Net capital gain 15500

Note 2:

This means for an annual income of $75500 Sue pay:

No tax on income between $1 - $18,200 0

19c for every dollar between $18,201 - $37,000 3572

32.5c for every dollar between $37,001 - $90,000 12512

Income Tax payable 16084

QUESTION ONE

Fees received 13011492

Operating expenses

Advertising 1100000

Accounting depreciation 755000

Fringe benefits tax 45000

Provision for unreported claims 150000

Provision for bad debts 143000

Repairs 430000

Wages and Salaries 7400000

Purchase of trading stock 920000

Superannuation for employees 893000

Total operating expenses 11836000

Cost of buying the goodwill of a business 400000

Net profit 775492

Particulars Amount Amount

Net profits of the company 775492

Add: Dividend received

(100000*100%) (ITAA 1997 215(B)) 100000

Cash dividend received and tax paid Nil

Wages (Overpayment of expense for

wages) 20000

895492

Depreciation and other expenses

(ITCC 1997 (705(45))

Capital loss 35000

Total Capital gain 135500

Less: unabsorbed capital loss 120000

Net capital gain 15500

Note 2:

This means for an annual income of $75500 Sue pay:

No tax on income between $1 - $18,200 0

19c for every dollar between $18,201 - $37,000 3572

32.5c for every dollar between $37,001 - $90,000 12512

Income Tax payable 16084

QUESTION ONE

Fees received 13011492

Operating expenses

Advertising 1100000

Accounting depreciation 755000

Fringe benefits tax 45000

Provision for unreported claims 150000

Provision for bad debts 143000

Repairs 430000

Wages and Salaries 7400000

Purchase of trading stock 920000

Superannuation for employees 893000

Total operating expenses 11836000

Cost of buying the goodwill of a business 400000

Net profit 775492

Particulars Amount Amount

Net profits of the company 775492

Add: Dividend received

(100000*100%) (ITAA 1997 215(B)) 100000

Cash dividend received and tax paid Nil

Wages (Overpayment of expense for

wages) 20000

895492

Depreciation and other expenses

(ITCC 1997 (705(45))

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

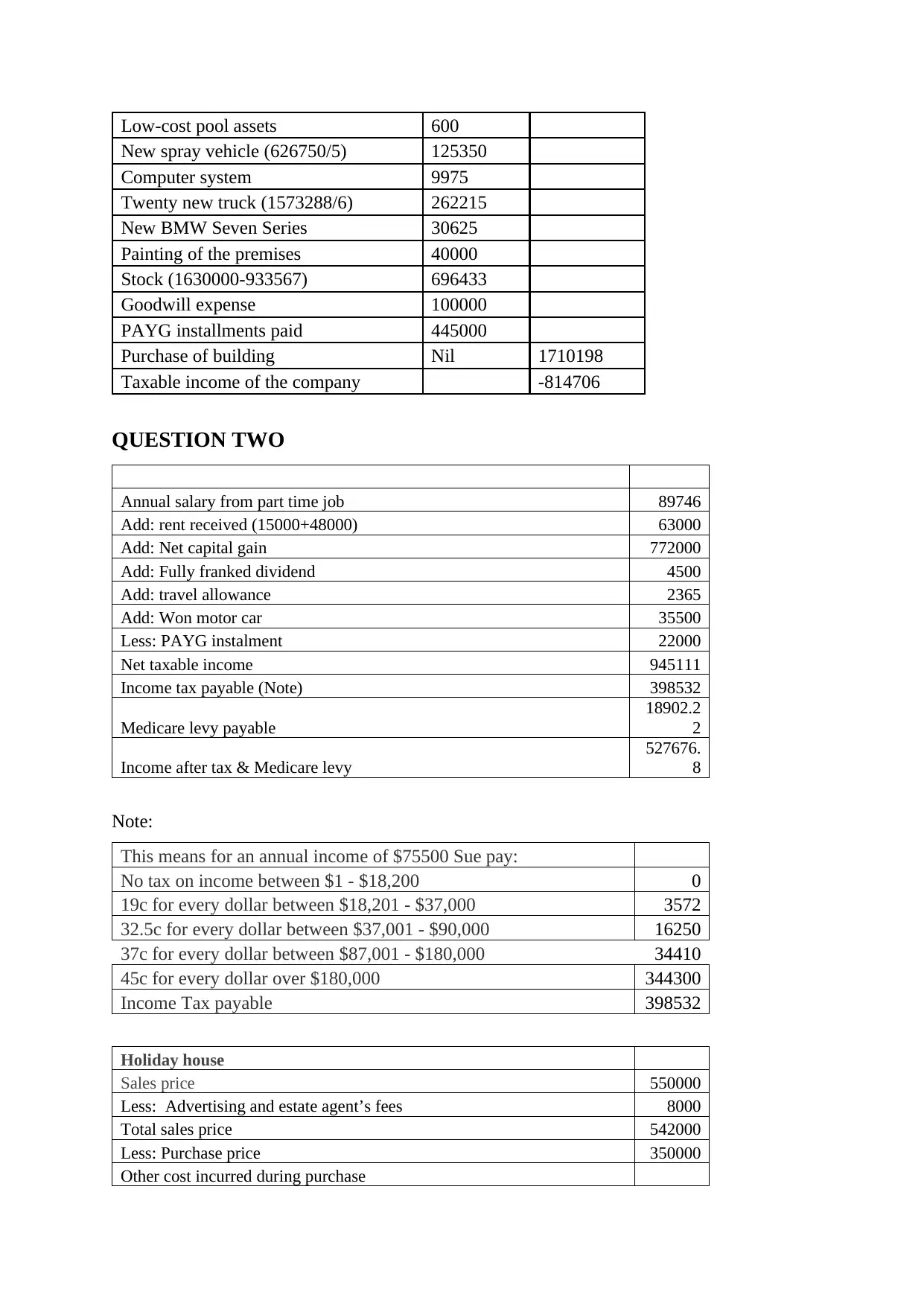

Low-cost pool assets 600

New spray vehicle (626750/5) 125350

Computer system 9975

Twenty new truck (1573288/6) 262215

New BMW Seven Series 30625

Painting of the premises 40000

Stock (1630000-933567) 696433

Goodwill expense 100000

PAYG installments paid 445000

Purchase of building Nil 1710198

Taxable income of the company -814706

QUESTION TWO

Annual salary from part time job 89746

Add: rent received (15000+48000) 63000

Add: Net capital gain 772000

Add: Fully franked dividend 4500

Add: travel allowance 2365

Add: Won motor car 35500

Less: PAYG instalment 22000

Net taxable income 945111

Income tax payable (Note) 398532

Medicare levy payable

18902.2

2

Income after tax & Medicare levy

527676.

8

Note:

This means for an annual income of $75500 Sue pay:

No tax on income between $1 - $18,200 0

19c for every dollar between $18,201 - $37,000 3572

32.5c for every dollar between $37,001 - $90,000 16250

37c for every dollar between $87,001 - $180,000 34410

45c for every dollar over $180,000 344300

Income Tax payable 398532

Holiday house

Sales price 550000

Less: Advertising and estate agent’s fees 8000

Total sales price 542000

Less: Purchase price 350000

Other cost incurred during purchase

New spray vehicle (626750/5) 125350

Computer system 9975

Twenty new truck (1573288/6) 262215

New BMW Seven Series 30625

Painting of the premises 40000

Stock (1630000-933567) 696433

Goodwill expense 100000

PAYG installments paid 445000

Purchase of building Nil 1710198

Taxable income of the company -814706

QUESTION TWO

Annual salary from part time job 89746

Add: rent received (15000+48000) 63000

Add: Net capital gain 772000

Add: Fully franked dividend 4500

Add: travel allowance 2365

Add: Won motor car 35500

Less: PAYG instalment 22000

Net taxable income 945111

Income tax payable (Note) 398532

Medicare levy payable

18902.2

2

Income after tax & Medicare levy

527676.

8

Note:

This means for an annual income of $75500 Sue pay:

No tax on income between $1 - $18,200 0

19c for every dollar between $18,201 - $37,000 3572

32.5c for every dollar between $37,001 - $90,000 16250

37c for every dollar between $87,001 - $180,000 34410

45c for every dollar over $180,000 344300

Income Tax payable 398532

Holiday house

Sales price 550000

Less: Advertising and estate agent’s fees 8000

Total sales price 542000

Less: Purchase price 350000

Other cost incurred during purchase

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

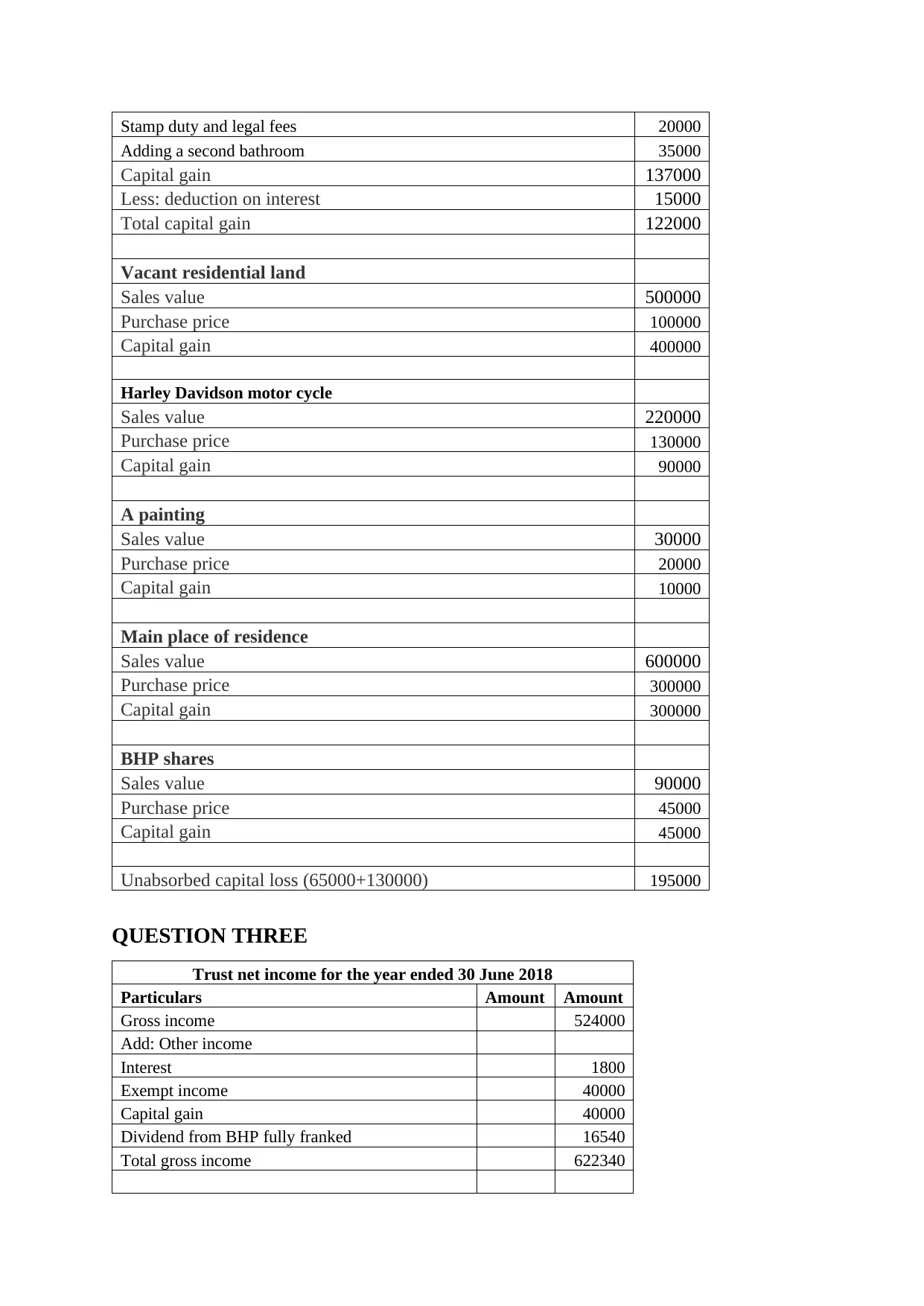

Stamp duty and legal fees 20000

Adding a second bathroom 35000

Capital gain 137000

Less: deduction on interest 15000

Total capital gain 122000

Vacant residential land

Sales value 500000

Purchase price 100000

Capital gain 400000

Harley Davidson motor cycle

Sales value 220000

Purchase price 130000

Capital gain 90000

A painting

Sales value 30000

Purchase price 20000

Capital gain 10000

Main place of residence

Sales value 600000

Purchase price 300000

Capital gain 300000

BHP shares

Sales value 90000

Purchase price 45000

Capital gain 45000

Unabsorbed capital loss (65000+130000) 195000

QUESTION THREE

Trust net income for the year ended 30 June 2018

Particulars Amount Amount

Gross income 524000

Add: Other income

Interest 1800

Exempt income 40000

Capital gain 40000

Dividend from BHP fully franked 16540

Total gross income 622340

Adding a second bathroom 35000

Capital gain 137000

Less: deduction on interest 15000

Total capital gain 122000

Vacant residential land

Sales value 500000

Purchase price 100000

Capital gain 400000

Harley Davidson motor cycle

Sales value 220000

Purchase price 130000

Capital gain 90000

A painting

Sales value 30000

Purchase price 20000

Capital gain 10000

Main place of residence

Sales value 600000

Purchase price 300000

Capital gain 300000

BHP shares

Sales value 90000

Purchase price 45000

Capital gain 45000

Unabsorbed capital loss (65000+130000) 195000

QUESTION THREE

Trust net income for the year ended 30 June 2018

Particulars Amount Amount

Gross income 524000

Add: Other income

Interest 1800

Exempt income 40000

Capital gain 40000

Dividend from BHP fully franked 16540

Total gross income 622340

Less: deductions or expenses

Rent 40000

Salaries to employees 127000

PAYG Withholding paid to ATO 18000

Salary to Jim Lee including PAYGW $23,000 72000

Salary to Mary Lee including PAYGW $15,000 35000

Salary to Mary Lee including PAYGW $15,000 1000

Superannuation contributions for employees 15674

Superannuation contributions for Jim and Mary 100000

Depreciation New computer system 4750

Depreciation New motor vehicle for Jim and Mary 10812.5

Motor vehicle expense 3500

Accounting conference 3000

Net interest 1800

Robbed 26000

Total expense

458536.

5

Net income before deduction of loss

163803.

5

Loss from the last year 120000

Net income 43803.5

Jim Lee's personal income year ended 30 June 2018

Particulars Amount

Jim Lee and Marry Lee's split equal distribution of

income total as $43803.5

21901.7

5

Add: Salary paid by trust 90000

Add: Revenue 6000

Total income

117901.

8

Less: Expenses and payments

Interest paid 8000

Medical expenses for Marry and Jim 7000

Professional membership fees 1500

Total expenses 16500

Income before loss

101401.

8

Trading loss 36000

Capital loss 12000

Net income for Jim Lee

53401.7

5

Income tax payable 8902

Medicare levy payable

1068.03

5

Note:

Rent 40000

Salaries to employees 127000

PAYG Withholding paid to ATO 18000

Salary to Jim Lee including PAYGW $23,000 72000

Salary to Mary Lee including PAYGW $15,000 35000

Salary to Mary Lee including PAYGW $15,000 1000

Superannuation contributions for employees 15674

Superannuation contributions for Jim and Mary 100000

Depreciation New computer system 4750

Depreciation New motor vehicle for Jim and Mary 10812.5

Motor vehicle expense 3500

Accounting conference 3000

Net interest 1800

Robbed 26000

Total expense

458536.

5

Net income before deduction of loss

163803.

5

Loss from the last year 120000

Net income 43803.5

Jim Lee's personal income year ended 30 June 2018

Particulars Amount

Jim Lee and Marry Lee's split equal distribution of

income total as $43803.5

21901.7

5

Add: Salary paid by trust 90000

Add: Revenue 6000

Total income

117901.

8

Less: Expenses and payments

Interest paid 8000

Medical expenses for Marry and Jim 7000

Professional membership fees 1500

Total expenses 16500

Income before loss

101401.

8

Trading loss 36000

Capital loss 12000

Net income for Jim Lee

53401.7

5

Income tax payable 8902

Medicare levy payable

1068.03

5

Note:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

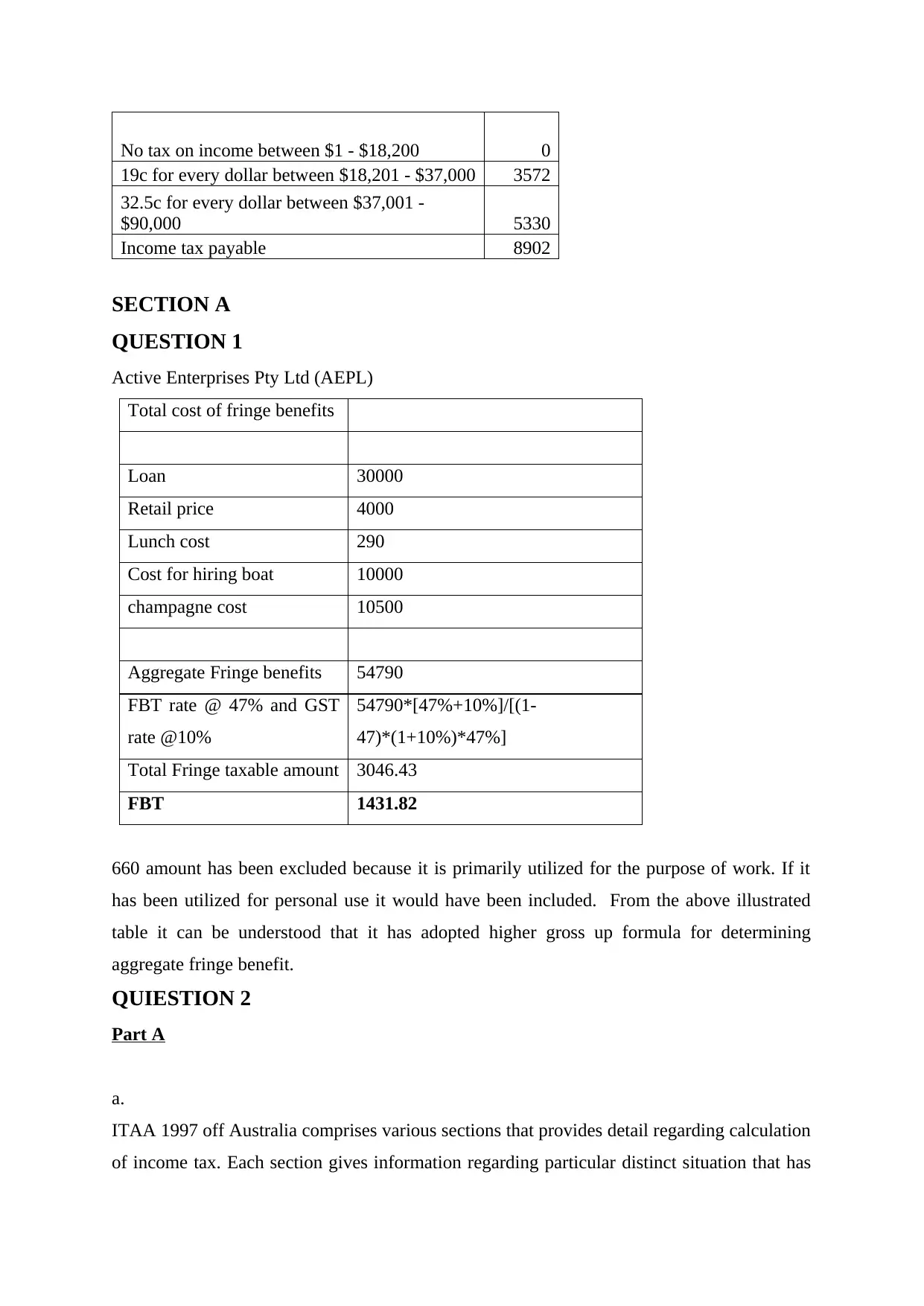

No tax on income between $1 - $18,200 0

19c for every dollar between $18,201 - $37,000 3572

32.5c for every dollar between $37,001 -

$90,000 5330

Income tax payable 8902

SECTION A

QUESTION 1

Active Enterprises Pty Ltd (AEPL)

Total cost of fringe benefits

Loan 30000

Retail price 4000

Lunch cost 290

Cost for hiring boat 10000

champagne cost 10500

Aggregate Fringe benefits 54790

FBT rate @ 47% and GST

rate @10%

54790*[47%+10%]/[(1-

47)*(1+10%)*47%]

Total Fringe taxable amount 3046.43

FBT 1431.82

660 amount has been excluded because it is primarily utilized for the purpose of work. If it

has been utilized for personal use it would have been included. From the above illustrated

table it can be understood that it has adopted higher gross up formula for determining

aggregate fringe benefit.

QUIESTION 2

Part A

a.

ITAA 1997 off Australia comprises various sections that provides detail regarding calculation

of income tax. Each section gives information regarding particular distinct situation that has

19c for every dollar between $18,201 - $37,000 3572

32.5c for every dollar between $37,001 -

$90,000 5330

Income tax payable 8902

SECTION A

QUESTION 1

Active Enterprises Pty Ltd (AEPL)

Total cost of fringe benefits

Loan 30000

Retail price 4000

Lunch cost 290

Cost for hiring boat 10000

champagne cost 10500

Aggregate Fringe benefits 54790

FBT rate @ 47% and GST

rate @10%

54790*[47%+10%]/[(1-

47)*(1+10%)*47%]

Total Fringe taxable amount 3046.43

FBT 1431.82

660 amount has been excluded because it is primarily utilized for the purpose of work. If it

has been utilized for personal use it would have been included. From the above illustrated

table it can be understood that it has adopted higher gross up formula for determining

aggregate fringe benefit.

QUIESTION 2

Part A

a.

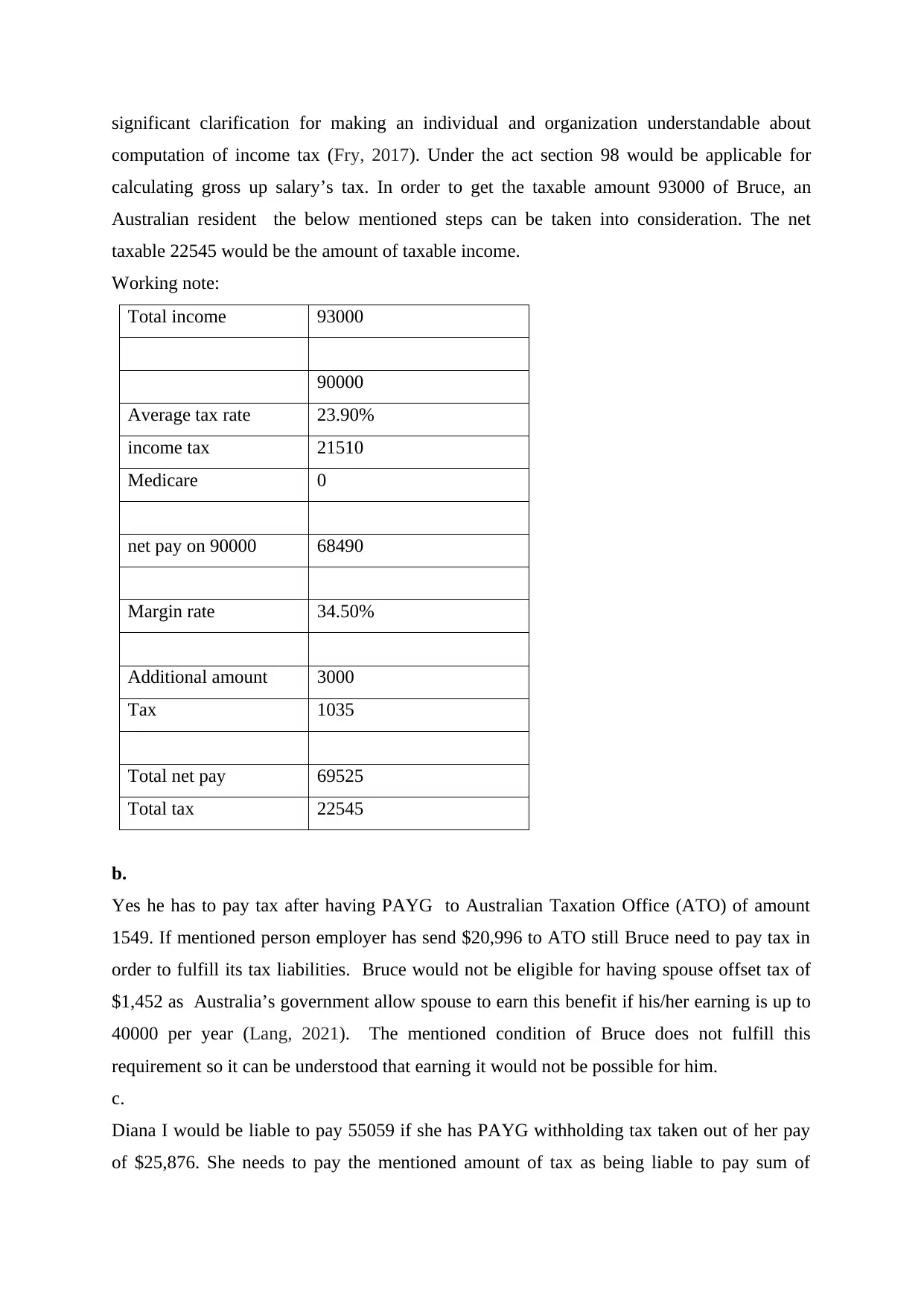

ITAA 1997 off Australia comprises various sections that provides detail regarding calculation

of income tax. Each section gives information regarding particular distinct situation that has

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

significant clarification for making an individual and organization understandable about

computation of income tax (Fry, 2017). Under the act section 98 would be applicable for

calculating gross up salary’s tax. In order to get the taxable amount 93000 of Bruce, an

Australian resident the below mentioned steps can be taken into consideration. The net

taxable 22545 would be the amount of taxable income.

Working note:

Total income 93000

90000

Average tax rate 23.90%

income tax 21510

Medicare 0

net pay on 90000 68490

Margin rate 34.50%

Additional amount 3000

Tax 1035

Total net pay 69525

Total tax 22545

b.

Yes he has to pay tax after having PAYG to Australian Taxation Office (ATO) of amount

1549. If mentioned person employer has send $20,996 to ATO still Bruce need to pay tax in

order to fulfill its tax liabilities. Bruce would not be eligible for having spouse offset tax of

$1,452 as Australia’s government allow spouse to earn this benefit if his/her earning is up to

40000 per year (Lang, 2021). The mentioned condition of Bruce does not fulfill this

requirement so it can be understood that earning it would not be possible for him.

c.

Diana I would be liable to pay 55059 if she has PAYG withholding tax taken out of her pay

of $25,876. She needs to pay the mentioned amount of tax as being liable to pay sum of

computation of income tax (Fry, 2017). Under the act section 98 would be applicable for

calculating gross up salary’s tax. In order to get the taxable amount 93000 of Bruce, an

Australian resident the below mentioned steps can be taken into consideration. The net

taxable 22545 would be the amount of taxable income.

Working note:

Total income 93000

90000

Average tax rate 23.90%

income tax 21510

Medicare 0

net pay on 90000 68490

Margin rate 34.50%

Additional amount 3000

Tax 1035

Total net pay 69525

Total tax 22545

b.

Yes he has to pay tax after having PAYG to Australian Taxation Office (ATO) of amount

1549. If mentioned person employer has send $20,996 to ATO still Bruce need to pay tax in

order to fulfill its tax liabilities. Bruce would not be eligible for having spouse offset tax of

$1,452 as Australia’s government allow spouse to earn this benefit if his/her earning is up to

40000 per year (Lang, 2021). The mentioned condition of Bruce does not fulfill this

requirement so it can be understood that earning it would not be possible for him.

c.

Diana I would be liable to pay 55059 if she has PAYG withholding tax taken out of her pay

of $25,876. She needs to pay the mentioned amount of tax as being liable to pay sum of

specified liability from the table. She would not be eligible to receive tax offset as her annual

salary is more than 40000.

Working note:

Total income 109000

90000

Average tax rate 23.90%

income tax 21510

Medicare 0

income tax

Net pay of 90000 68490

Margin rate 34.50%

Additional amount 19000

Tax 6555

Total tax 28065

Net income 80935

From the above mentioned calculation it can be understood that margin rate is

applied on amount above than 90000.

Part B

a.

Partnership income = $520,000

Expenses = $240,000

Salary of a partner = $40000

Income – expenses = taxable amount

Taxable amount = 240000

Tax= taxable figure* tax rate (45%)

Tax = 108000

Net income = Total income- tax

Net income = 132000

From the above computation it can be identified that Tito, Vic and Joey (TVJ) for 2014-15

will be liable for 108000 in order to earn 132000 net income. This specified earning after tax

salary is more than 40000.

Working note:

Total income 109000

90000

Average tax rate 23.90%

income tax 21510

Medicare 0

income tax

Net pay of 90000 68490

Margin rate 34.50%

Additional amount 19000

Tax 6555

Total tax 28065

Net income 80935

From the above mentioned calculation it can be understood that margin rate is

applied on amount above than 90000.

Part B

a.

Partnership income = $520,000

Expenses = $240,000

Salary of a partner = $40000

Income – expenses = taxable amount

Taxable amount = 240000

Tax= taxable figure* tax rate (45%)

Tax = 108000

Net income = Total income- tax

Net income = 132000

From the above computation it can be identified that Tito, Vic and Joey (TVJ) for 2014-15

will be liable for 108000 in order to earn 132000 net income. This specified earning after tax

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 30

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.