Taxation Law Assignment: Australian Taxation Law and Case Studies

VerifiedAdded on 2022/10/12

|17

|3562

|242

Homework Assignment

AI Summary

This Taxation Law assignment provides detailed answers to several questions related to Australian income tax law. The assignment explores topics such as the definition of a small business entity, deductibility of gifts, marginal tax rates, capital gains tax, CGT events, and the tax-free threshold. It also delves into the differences between ordinary and statutory income, Medicare Levy and Medicare Levy Surcharge. The assignment further analyzes the concept of 'usual place of abode' and 'permanent place of abode' in the context of residency. Moreover, it examines the deductibility of various expenses, including HECS-HELP, travel costs, books, childcare, home repairs, clothing, and legal fees. The student provides a thorough analysis of each expense based on relevant tax laws and case precedents, offering a comprehensive understanding of the subject matter.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................3

Answer A:..............................................................................................................................3

Answer B:...............................................................................................................................3

Answer C:...............................................................................................................................3

Answer D:..............................................................................................................................3

Answer E:...............................................................................................................................4

Answer F:...............................................................................................................................4

Answer G:..............................................................................................................................4

Answer H:..............................................................................................................................4

Answer I:................................................................................................................................5

Answer to question 2:.................................................................................................................6

Answer to question 3:.................................................................................................................7

Answer to question 4:...............................................................................................................10

Answer to A:........................................................................................................................10

Answer to B:........................................................................................................................11

Answer to C:........................................................................................................................11

Answer to D:........................................................................................................................12

Answer to question 5:...............................................................................................................12

Answer A:............................................................................................................................12

Answer B:.............................................................................................................................12

Table of Contents

Answer to question 1:.................................................................................................................3

Answer A:..............................................................................................................................3

Answer B:...............................................................................................................................3

Answer C:...............................................................................................................................3

Answer D:..............................................................................................................................3

Answer E:...............................................................................................................................4

Answer F:...............................................................................................................................4

Answer G:..............................................................................................................................4

Answer H:..............................................................................................................................4

Answer I:................................................................................................................................5

Answer to question 2:.................................................................................................................6

Answer to question 3:.................................................................................................................7

Answer to question 4:...............................................................................................................10

Answer to A:........................................................................................................................10

Answer to B:........................................................................................................................11

Answer to C:........................................................................................................................11

Answer to D:........................................................................................................................12

Answer to question 5:...............................................................................................................12

Answer A:............................................................................................................................12

Answer B:.............................................................................................................................12

2TAXATION LAW

Answer to C:........................................................................................................................13

Answer to D:........................................................................................................................13

Answer to E:.........................................................................................................................14

References:...............................................................................................................................15

Answer to C:........................................................................................................................13

Answer to D:........................................................................................................................13

Answer to E:.........................................................................................................................14

References:...............................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

Answer to question 1:

Answer A:

As explained in “Taxation Ruling of TR 2009/1” it provides the tax commissioner

view on when the company carry-out the business within the meaning of small business

entity under “Sec-23 of the Income Tax Rates Act 1986” that are applicable from the year

2015-16 and 2016-17 or within “sec-328-110, ITAA 1997” (Barkoczy, 2016).

Answer B:

Deductibility of gifts or contribution is outlined in the “Division 30, ITAA 1997”.

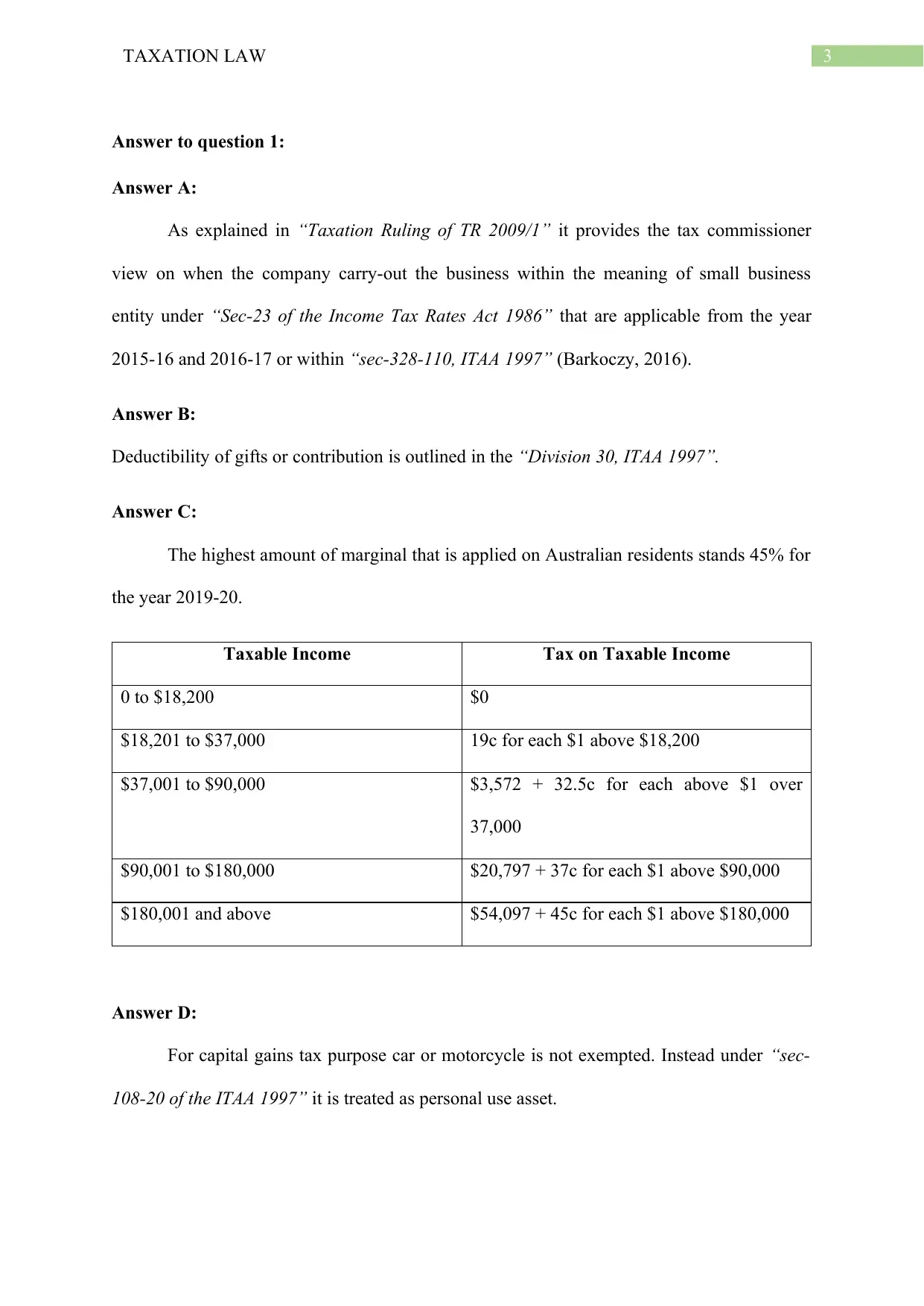

Answer C:

The highest amount of marginal that is applied on Australian residents stands 45% for

the year 2019-20.

Taxable Income Tax on Taxable Income

0 to $18,200 $0

$18,201 to $37,000 19c for each $1 above $18,200

$37,001 to $90,000 $3,572 + 32.5c for each above $1 over

37,000

$90,001 to $180,000 $20,797 + 37c for each $1 above $90,000

$180,001 and above $54,097 + 45c for each $1 above $180,000

Answer D:

For capital gains tax purpose car or motorcycle is not exempted. Instead under “sec-

108-20 of the ITAA 1997” it is treated as personal use asset.

Answer to question 1:

Answer A:

As explained in “Taxation Ruling of TR 2009/1” it provides the tax commissioner

view on when the company carry-out the business within the meaning of small business

entity under “Sec-23 of the Income Tax Rates Act 1986” that are applicable from the year

2015-16 and 2016-17 or within “sec-328-110, ITAA 1997” (Barkoczy, 2016).

Answer B:

Deductibility of gifts or contribution is outlined in the “Division 30, ITAA 1997”.

Answer C:

The highest amount of marginal that is applied on Australian residents stands 45% for

the year 2019-20.

Taxable Income Tax on Taxable Income

0 to $18,200 $0

$18,201 to $37,000 19c for each $1 above $18,200

$37,001 to $90,000 $3,572 + 32.5c for each above $1 over

37,000

$90,001 to $180,000 $20,797 + 37c for each $1 above $90,000

$180,001 and above $54,097 + 45c for each $1 above $180,000

Answer D:

For capital gains tax purpose car or motorcycle is not exempted. Instead under “sec-

108-20 of the ITAA 1997” it is treated as personal use asset.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

Answer E:

CGT event C1 under “sec-104-20 of the ITAA 1997” occurs when a taxpayer holding

a CGT asset is either lost or destroyed. CGT event C1 is applied to a portion of CGT asset

when no payment is received by taxpayer for loss or damage (Chardon, 2014).

Answer F:

Currently the tax-free threshold limit for individuals that are resident is $18,200 for

income year of 2019-20.

Answer G:

The law court in “Hayes v FCT (1956)”, held that where the accountant has received

a substantial amount of shares in the public company which was set up by a previous

employer. Unpaid advice was casually given by the accountant to previous employer and

carried out small unpaid services (Lang, 2014). The service was out of common friendship

between the parties. In the current case, the law court held that the gift was not considered as

income because there was no relation with revenue making acts and the private relation

among them was the circumstance of the gift.

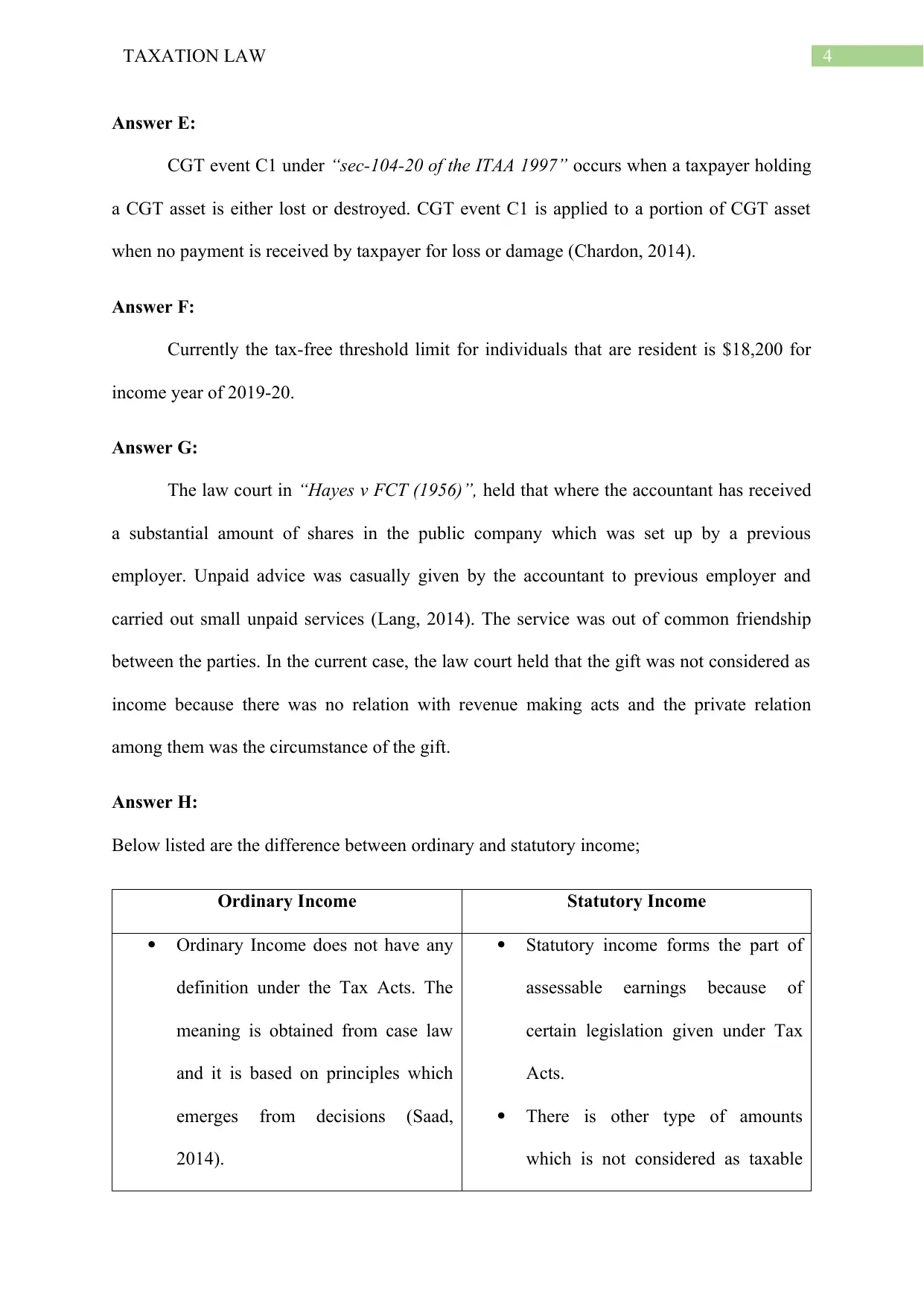

Answer H:

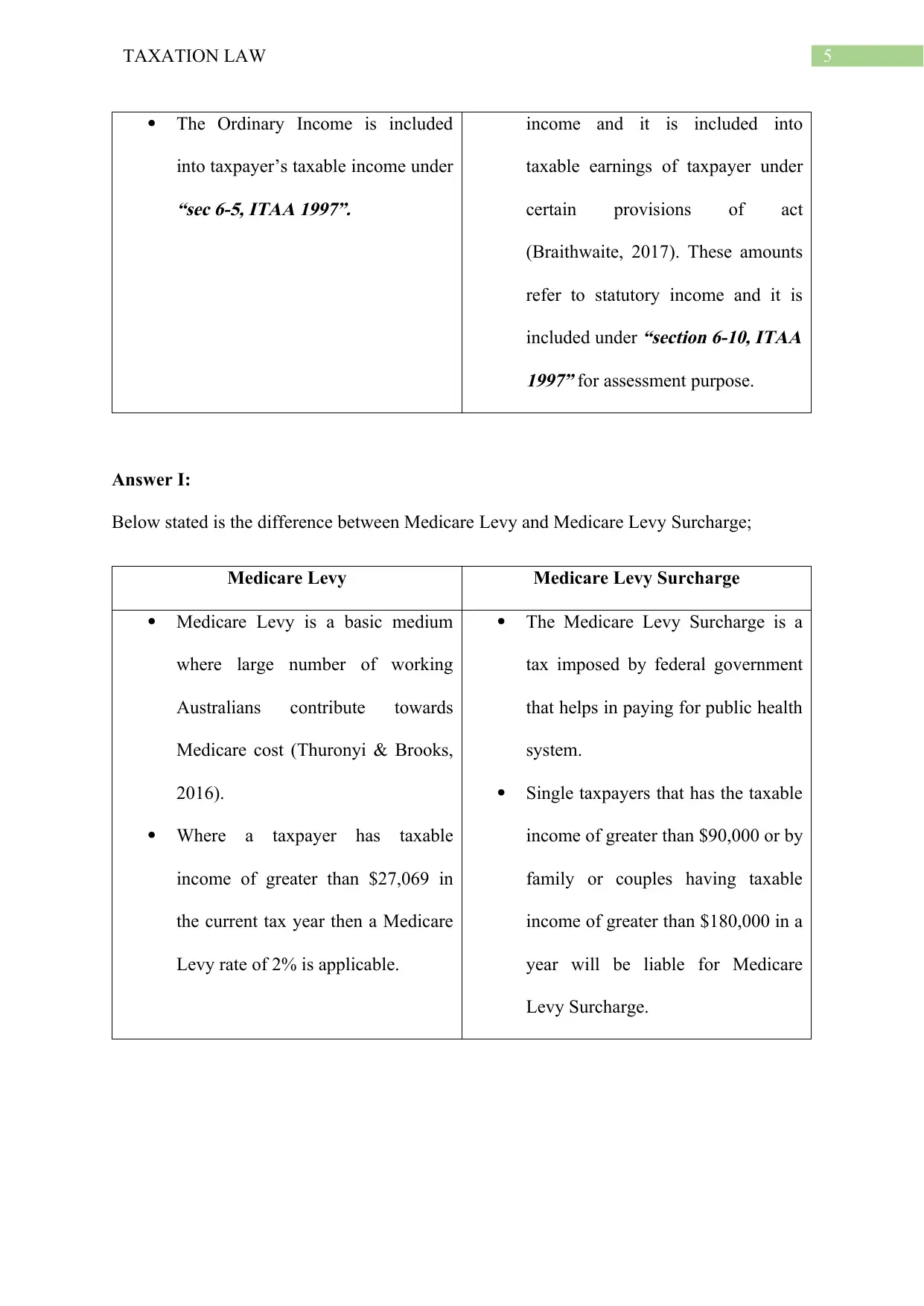

Below listed are the difference between ordinary and statutory income;

Ordinary Income Statutory Income

Ordinary Income does not have any

definition under the Tax Acts. The

meaning is obtained from case law

and it is based on principles which

emerges from decisions (Saad,

2014).

Statutory income forms the part of

assessable earnings because of

certain legislation given under Tax

Acts.

There is other type of amounts

which is not considered as taxable

Answer E:

CGT event C1 under “sec-104-20 of the ITAA 1997” occurs when a taxpayer holding

a CGT asset is either lost or destroyed. CGT event C1 is applied to a portion of CGT asset

when no payment is received by taxpayer for loss or damage (Chardon, 2014).

Answer F:

Currently the tax-free threshold limit for individuals that are resident is $18,200 for

income year of 2019-20.

Answer G:

The law court in “Hayes v FCT (1956)”, held that where the accountant has received

a substantial amount of shares in the public company which was set up by a previous

employer. Unpaid advice was casually given by the accountant to previous employer and

carried out small unpaid services (Lang, 2014). The service was out of common friendship

between the parties. In the current case, the law court held that the gift was not considered as

income because there was no relation with revenue making acts and the private relation

among them was the circumstance of the gift.

Answer H:

Below listed are the difference between ordinary and statutory income;

Ordinary Income Statutory Income

Ordinary Income does not have any

definition under the Tax Acts. The

meaning is obtained from case law

and it is based on principles which

emerges from decisions (Saad,

2014).

Statutory income forms the part of

assessable earnings because of

certain legislation given under Tax

Acts.

There is other type of amounts

which is not considered as taxable

5TAXATION LAW

The Ordinary Income is included

into taxpayer’s taxable income under“sec 6-5, ITAA 1997”.

income and it is included into

taxable earnings of taxpayer under

certain provisions of act

(Braithwaite, 2017). These amounts

refer to statutory income and it is

included under

“section 6-10, ITAA

1997” for assessment purpose.

Answer I:

Below stated is the difference between Medicare Levy and Medicare Levy Surcharge;

Medicare Levy Medicare Levy Surcharge

Medicare Levy is a basic medium

where large number of working

Australians contribute towards

Medicare cost (Thuronyi & Brooks,

2016).

Where a taxpayer has taxable

income of greater than $27,069 in

the current tax year then a Medicare

Levy rate of 2% is applicable.

The Medicare Levy Surcharge is a

tax imposed by federal government

that helps in paying for public health

system.

Single taxpayers that has the taxable

income of greater than $90,000 or by

family or couples having taxable

income of greater than $180,000 in a

year will be liable for Medicare

Levy Surcharge.

The Ordinary Income is included

into taxpayer’s taxable income under“sec 6-5, ITAA 1997”.

income and it is included into

taxable earnings of taxpayer under

certain provisions of act

(Braithwaite, 2017). These amounts

refer to statutory income and it is

included under

“section 6-10, ITAA

1997” for assessment purpose.

Answer I:

Below stated is the difference between Medicare Levy and Medicare Levy Surcharge;

Medicare Levy Medicare Levy Surcharge

Medicare Levy is a basic medium

where large number of working

Australians contribute towards

Medicare cost (Thuronyi & Brooks,

2016).

Where a taxpayer has taxable

income of greater than $27,069 in

the current tax year then a Medicare

Levy rate of 2% is applicable.

The Medicare Levy Surcharge is a

tax imposed by federal government

that helps in paying for public health

system.

Single taxpayers that has the taxable

income of greater than $90,000 or by

family or couples having taxable

income of greater than $180,000 in a

year will be liable for Medicare

Levy Surcharge.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

Answer to question 2:

The term “usual place of abode” should not be presumed as having similar sense as

the term “permanent place of abode”. The expression “usual” and “abode” should be

understood on the basis of systematic and usual meaning (Miller & Oats, 2016). The question

relating to “usual place of abode” is dependent on the matter of fact. Commonly, the term

should be treated as normal place of residence or it is commonly used when an individual is

physically present in that nation. A person’s “usual place of abode” must be permanent but it

must demonstrate the quality of dwelling in contrary to weekly basis, overnight or monthly

housing of a traveller. It includes a long-term relation with a taxpayer’s certain dwelling

place than those individuals that have usually been the dweller or having their “usual place

of abode” in Australia.

If a taxpayer has “usual place of abode” in Australia and has no fixed dwelling in

foreign country but travels country to country or relocating on constantly inside the domestic

territory or has the relation with specific place in overseas, they the dwelling will be

temporary (Freudenberg et al., 2017). The taxpayer in such situation would not be considered

to have adopted alternative dwelling of their own choice or “permanent place of abode”

outside Australia.

On the contrary, the expression “permanent place of abode” implies that a taxpayer

has their own dwelling in Australia. Accordingly, under

“subparagraph (a)(i)”, the meaning

of “resident” necessitates the tax commissioner to be satisfied that the taxpayer’s “permanent

place of abode” is within Australia (Sadiq, 2019). The expression

“place of abode” refers to

an individual having a residence where he and his family sleeps at night. The law court in

“Levene v IRC (1928)” explained that a person’s

“place of abode” constitutes a dwelling or

the physical surroundings where he or she resides in.

Answer to question 2:

The term “usual place of abode” should not be presumed as having similar sense as

the term “permanent place of abode”. The expression “usual” and “abode” should be

understood on the basis of systematic and usual meaning (Miller & Oats, 2016). The question

relating to “usual place of abode” is dependent on the matter of fact. Commonly, the term

should be treated as normal place of residence or it is commonly used when an individual is

physically present in that nation. A person’s “usual place of abode” must be permanent but it

must demonstrate the quality of dwelling in contrary to weekly basis, overnight or monthly

housing of a traveller. It includes a long-term relation with a taxpayer’s certain dwelling

place than those individuals that have usually been the dweller or having their “usual place

of abode” in Australia.

If a taxpayer has “usual place of abode” in Australia and has no fixed dwelling in

foreign country but travels country to country or relocating on constantly inside the domestic

territory or has the relation with specific place in overseas, they the dwelling will be

temporary (Freudenberg et al., 2017). The taxpayer in such situation would not be considered

to have adopted alternative dwelling of their own choice or “permanent place of abode”

outside Australia.

On the contrary, the expression “permanent place of abode” implies that a taxpayer

has their own dwelling in Australia. Accordingly, under

“subparagraph (a)(i)”, the meaning

of “resident” necessitates the tax commissioner to be satisfied that the taxpayer’s “permanent

place of abode” is within Australia (Sadiq, 2019). The expression

“place of abode” refers to

an individual having a residence where he and his family sleeps at night. The law court in

“Levene v IRC (1928)” explained that a person’s

“place of abode” constitutes a dwelling or

the physical surroundings where he or she resides in.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

In another leading example of

“FCT v Applegate (1979)” it was understood that the

taxpayer had the Australian residence, travelled to New Hebrides to establish an office branch

(Butler, 2019). The commissioner held that the “permanent place of abode” for the taxpayer

was not in Australia and was considered non-resident for the relevant income year.

In an alternative case of

“FCT v Jenkins (1982)” the taxpayer was bank officer who

moved to New Hebrides for 3 years and came back to Australia after 18 months because of

bad health (Murray et al., 2018). The court elucidated that the taxpayers “permanent place of

abode” was not in Australia all through the year despite he did not spend any physical time to

reside in New Hebrides. Both aforementioned cases explain that “permanent place of abode”

cannot be ascertained by implementing any hard and fast rules.

The explanation above clarifies that a taxpayer should be satisfied given their “usual

place of abode” is outside Australia, whereas the statutory test necessitates a person to be

satisfied that their “permanent place of abode” is not in Australia.

Answer to question 3:

HECS-HELP: $850:

As explained by ATO, permissible income tax deduction is permitted to taxpayer for

certain types of outgoings that is related to self-education provided that the expenses are

occurred in relevant assessable earnings of taxpayer. As per the ATO, if an individual

taxpayer incurs expenses on self-education and satisfies the eligibility criteria then particular

outgoings namely Fee-Help, VET or the student loan that is paid inside the HECS-HELP is

not allowed for deduction. Similarly, the expenses of $850 occurred for HECS-HELP is non-

deductible expenditure.

In another leading example of

“FCT v Applegate (1979)” it was understood that the

taxpayer had the Australian residence, travelled to New Hebrides to establish an office branch

(Butler, 2019). The commissioner held that the “permanent place of abode” for the taxpayer

was not in Australia and was considered non-resident for the relevant income year.

In an alternative case of

“FCT v Jenkins (1982)” the taxpayer was bank officer who

moved to New Hebrides for 3 years and came back to Australia after 18 months because of

bad health (Murray et al., 2018). The court elucidated that the taxpayers “permanent place of

abode” was not in Australia all through the year despite he did not spend any physical time to

reside in New Hebrides. Both aforementioned cases explain that “permanent place of abode”

cannot be ascertained by implementing any hard and fast rules.

The explanation above clarifies that a taxpayer should be satisfied given their “usual

place of abode” is outside Australia, whereas the statutory test necessitates a person to be

satisfied that their “permanent place of abode” is not in Australia.

Answer to question 3:

HECS-HELP: $850:

As explained by ATO, permissible income tax deduction is permitted to taxpayer for

certain types of outgoings that is related to self-education provided that the expenses are

occurred in relevant assessable earnings of taxpayer. As per the ATO, if an individual

taxpayer incurs expenses on self-education and satisfies the eligibility criteria then particular

outgoings namely Fee-Help, VET or the student loan that is paid inside the HECS-HELP is

not allowed for deduction. Similarly, the expenses of $850 occurred for HECS-HELP is non-

deductible expenditure.

8TAXATION LAW

Travel – work to university $110:

Accordingly, self-education expenditure that are occurred is generally considered

deductible where the expenditure is occurred in maintaining or increasing the skills of the

taxpayer in the occupation in which they are present engaged, particularly where the

outgoings are occurred in improving the future income producing prospect of the taxpayer.

As held in

“Finn v FCT (1961)” the architect employed by the WA Government was

permitted allowable income tax deduction for travelling expenditure that are occurred in

travelling overseas for a year to study architecture (Morgan et al., 2018). The court held that

the tour was very much related in nature and relevant to the employment of taxpayer.

As evident in the current case travel from work to University will be considered as

allowable deduction under

“section 8-1, ITAA 1997” since the travel expenditure was very

much incidental in nature and relevant to the employment of taxpayer.

Books $200:

Self-education expenditure occurred for cost relating to study-materials such as

calculators, textbooks, stationary related to improving the future promotion and earning

capacities of the taxpayer is allowed for deduction under

“section 8-1, ITAA 1997” (Morgan

& Castelyn, 2018). As held in

“FCT v Highfield (1982)” a dentist that carried on the general

practice was permitted deduction for outgoings relating to fees and accommodation for

undertaking self-education expenses.

As evident in the current case of the accountant the expenses occurred for books will

be allowed as permissible deduction under

“section 8-1, ITAA 1997” because the expenses

were related to improving the future promotion and earning capacities of the taxpayer.

Travel – work to university $110:

Accordingly, self-education expenditure that are occurred is generally considered

deductible where the expenditure is occurred in maintaining or increasing the skills of the

taxpayer in the occupation in which they are present engaged, particularly where the

outgoings are occurred in improving the future income producing prospect of the taxpayer.

As held in

“Finn v FCT (1961)” the architect employed by the WA Government was

permitted allowable income tax deduction for travelling expenditure that are occurred in

travelling overseas for a year to study architecture (Morgan et al., 2018). The court held that

the tour was very much related in nature and relevant to the employment of taxpayer.

As evident in the current case travel from work to University will be considered as

allowable deduction under

“section 8-1, ITAA 1997” since the travel expenditure was very

much incidental in nature and relevant to the employment of taxpayer.

Books $200:

Self-education expenditure occurred for cost relating to study-materials such as

calculators, textbooks, stationary related to improving the future promotion and earning

capacities of the taxpayer is allowed for deduction under

“section 8-1, ITAA 1997” (Morgan

& Castelyn, 2018). As held in

“FCT v Highfield (1982)” a dentist that carried on the general

practice was permitted deduction for outgoings relating to fees and accommodation for

undertaking self-education expenses.

As evident in the current case of the accountant the expenses occurred for books will

be allowed as permissible deduction under

“section 8-1, ITAA 1997” because the expenses

were related to improving the future promotion and earning capacities of the taxpayer.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

Childcare during her evening classes $80:

As per

“section 8-1 (2)(b), ITAA 1997” expenses that are domestic or private in

nature is not allowed for deduction because it does not meet the criterion given under the

positive limbs and non-deductible under negative limbs. In

“FCT v Lodge (1972)” the court

did not permitted deduction to taxpayer for expenses occurred for child care in order to have

her child minded while she attends her work (Robin & Barkoczy, 2019). The court stated that

the expenses were not related to the income generating activities of taxpayer.

Similarly, in current case the childcare expenses of $80 incurred by taxpayer for

attending the evening classes is non-deductible under

“section 8-1 (2)(b), ITAA 1997”

because the expenses were not related to the income generating activities of taxpayer.

Repair to her fridge at home $250:

An individual taxpayer is not allowed to claim deduction under

“section 8-1 (2)(b),

ITAA 1997” up the extent that the outgoings are private or domestic in nature. The court in

“Lunney v FCT (1958)” held that it is necessary to determine whether the loss or outgoings

are important prerequisite in the sourcing of taxable returns (Bankman et al., 2018). In the

same way, repairs to fringe at home for $250 will not be allowed for deduction under

“section 8-1 (2)(b), ITAA 1997” because the expenses are private or domestic in nature and

it is not an important prerequisite in the sourcing of taxable earnings.

Black trousers and shirt required to be worn at office $145:

Cost incurred in purchasing the ordinary items of clothing such as suit is usually not

permitted for deduction under the

“section 8-1, ITAA 1997”. The law court in

“Mansfield v

FCT (1996)” held that usually the general expenses incurred on the ordinary articles of

apparel would not be treated as deductible, irrespective of the fact that such expenses are

Childcare during her evening classes $80:

As per

“section 8-1 (2)(b), ITAA 1997” expenses that are domestic or private in

nature is not allowed for deduction because it does not meet the criterion given under the

positive limbs and non-deductible under negative limbs. In

“FCT v Lodge (1972)” the court

did not permitted deduction to taxpayer for expenses occurred for child care in order to have

her child minded while she attends her work (Robin & Barkoczy, 2019). The court stated that

the expenses were not related to the income generating activities of taxpayer.

Similarly, in current case the childcare expenses of $80 incurred by taxpayer for

attending the evening classes is non-deductible under

“section 8-1 (2)(b), ITAA 1997”

because the expenses were not related to the income generating activities of taxpayer.

Repair to her fridge at home $250:

An individual taxpayer is not allowed to claim deduction under

“section 8-1 (2)(b),

ITAA 1997” up the extent that the outgoings are private or domestic in nature. The court in

“Lunney v FCT (1958)” held that it is necessary to determine whether the loss or outgoings

are important prerequisite in the sourcing of taxable returns (Bankman et al., 2018). In the

same way, repairs to fringe at home for $250 will not be allowed for deduction under

“section 8-1 (2)(b), ITAA 1997” because the expenses are private or domestic in nature and

it is not an important prerequisite in the sourcing of taxable earnings.

Black trousers and shirt required to be worn at office $145:

Cost incurred in purchasing the ordinary items of clothing such as suit is usually not

permitted for deduction under the

“section 8-1, ITAA 1997”. The law court in

“Mansfield v

FCT (1996)” held that usually the general expenses incurred on the ordinary articles of

apparel would not be treated as deductible, irrespective of the fact that such expenses are

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

necessary to make sure that a suitable appearance is required to be maintained in a particular

job or profession.

As evident in the current case the expenses occurred for Black trousers and shirt

required to be worn at office is an ordinary items of clothing which is not permitted for

deduction under the

“section 8-1, ITAA 1997”. The expenses are non-allowable for

deduction irrespective of the fact that such expenses are necessary to make sure that a

suitable appearance is required to be maintained in office.

Legal expenses occurred in writing up a new employment with a new employer $300:

Expenses that are occurred in getting the new employment is not considered in the

course of producing taxable income. As held in

“Maddalena v FCT (1971)” expenses

incurred in getting the new employment was non-deductible as it occurred point too soon

(Siebert, 2019). Similarly, the legal outgoings for writing up new employment with new

employee is non-deductible expenditure since it occurred at point too soon.

Answer to question 4:

Answer to A:

A CGT event F1 takes place when a taxpayer grants a lease to another party or

extends or renews the lease which was previously owned by the taxpayer. No 50% CGT

discount is allowed under CGT event F1. When John leased his land at a premium of $7,000

for seven years then a CGT event F1 occurred. John however, cannot obtain 50% CGT

discount from the CGT event.

necessary to make sure that a suitable appearance is required to be maintained in a particular

job or profession.

As evident in the current case the expenses occurred for Black trousers and shirt

required to be worn at office is an ordinary items of clothing which is not permitted for

deduction under the

“section 8-1, ITAA 1997”. The expenses are non-allowable for

deduction irrespective of the fact that such expenses are necessary to make sure that a

suitable appearance is required to be maintained in office.

Legal expenses occurred in writing up a new employment with a new employer $300:

Expenses that are occurred in getting the new employment is not considered in the

course of producing taxable income. As held in

“Maddalena v FCT (1971)” expenses

incurred in getting the new employment was non-deductible as it occurred point too soon

(Siebert, 2019). Similarly, the legal outgoings for writing up new employment with new

employee is non-deductible expenditure since it occurred at point too soon.

Answer to question 4:

Answer to A:

A CGT event F1 takes place when a taxpayer grants a lease to another party or

extends or renews the lease which was previously owned by the taxpayer. No 50% CGT

discount is allowed under CGT event F1. When John leased his land at a premium of $7,000

for seven years then a CGT event F1 occurred. John however, cannot obtain 50% CGT

discount from the CGT event.

11TAXATION LAW

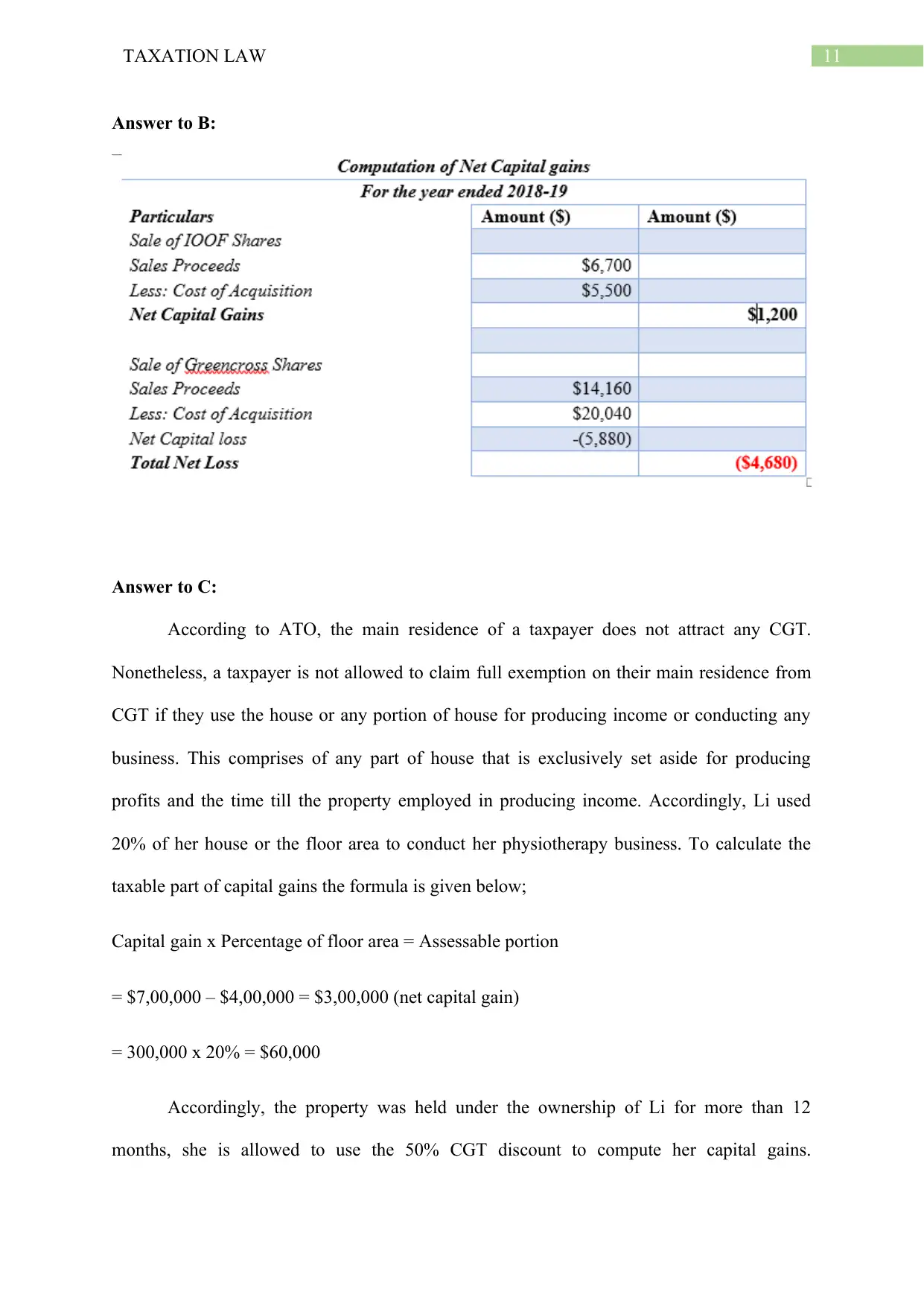

Answer to B:

Answer to C:

According to ATO, the main residence of a taxpayer does not attract any CGT.

Nonetheless, a taxpayer is not allowed to claim full exemption on their main residence from

CGT if they use the house or any portion of house for producing income or conducting any

business. This comprises of any part of house that is exclusively set aside for producing

profits and the time till the property employed in producing income. Accordingly, Li used

20% of her house or the floor area to conduct her physiotherapy business. To calculate the

taxable part of capital gains the formula is given below;

Capital gain x Percentage of floor area = Assessable portion

= $7,00,000 – $4,00,000 = $3,00,000 (net capital gain)

= 300,000 x 20% = $60,000

Accordingly, the property was held under the ownership of Li for more than 12

months, she is allowed to use the 50% CGT discount to compute her capital gains.

Answer to B:

Answer to C:

According to ATO, the main residence of a taxpayer does not attract any CGT.

Nonetheless, a taxpayer is not allowed to claim full exemption on their main residence from

CGT if they use the house or any portion of house for producing income or conducting any

business. This comprises of any part of house that is exclusively set aside for producing

profits and the time till the property employed in producing income. Accordingly, Li used

20% of her house or the floor area to conduct her physiotherapy business. To calculate the

taxable part of capital gains the formula is given below;

Capital gain x Percentage of floor area = Assessable portion

= $7,00,000 – $4,00,000 = $3,00,000 (net capital gain)

= 300,000 x 20% = $60,000

Accordingly, the property was held under the ownership of Li for more than 12

months, she is allowed to use the 50% CGT discount to compute her capital gains.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.