Report on Capital Gains Tax Under Australian Taxation Law: Analysis

VerifiedAdded on 2020/10/05

|7

|1200

|417

Report

AI Summary

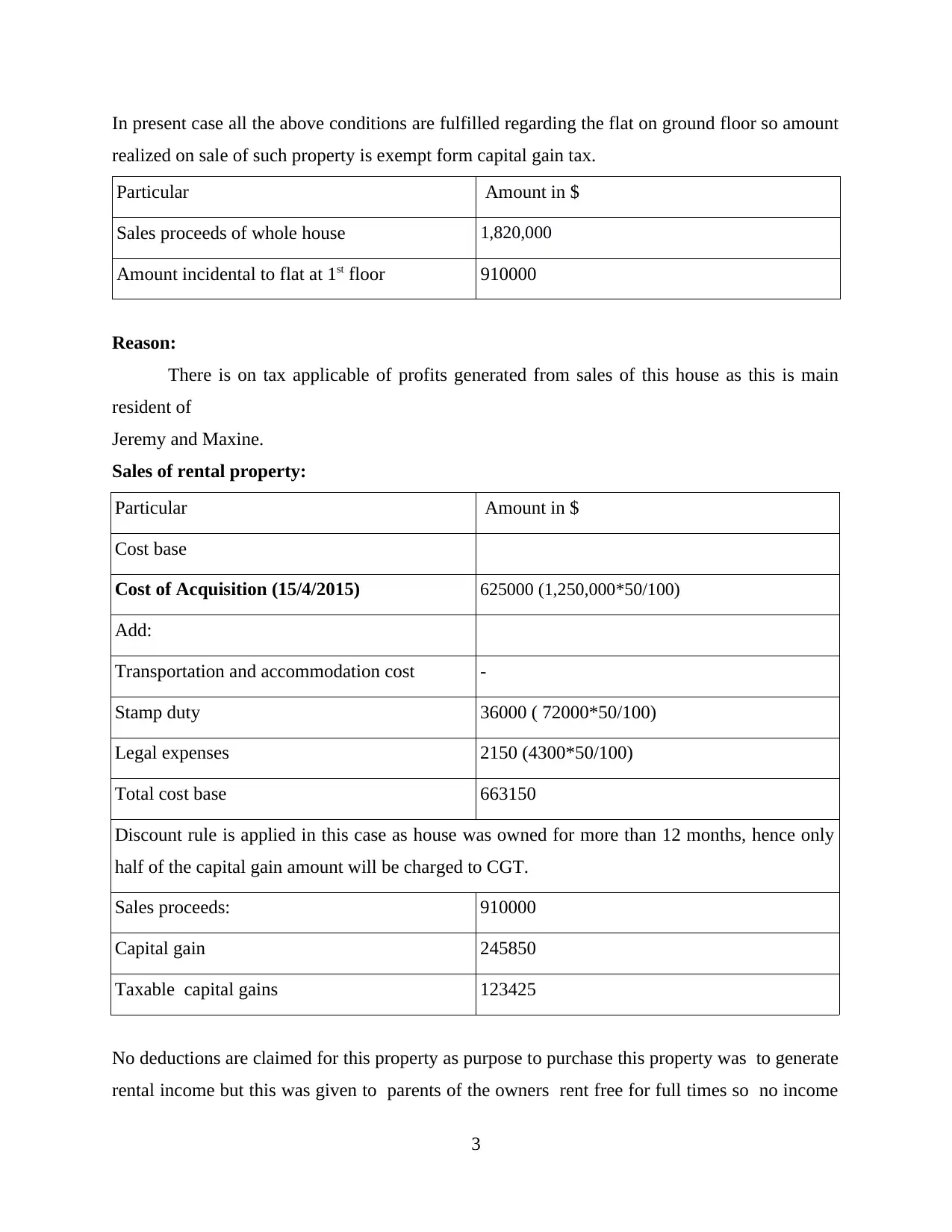

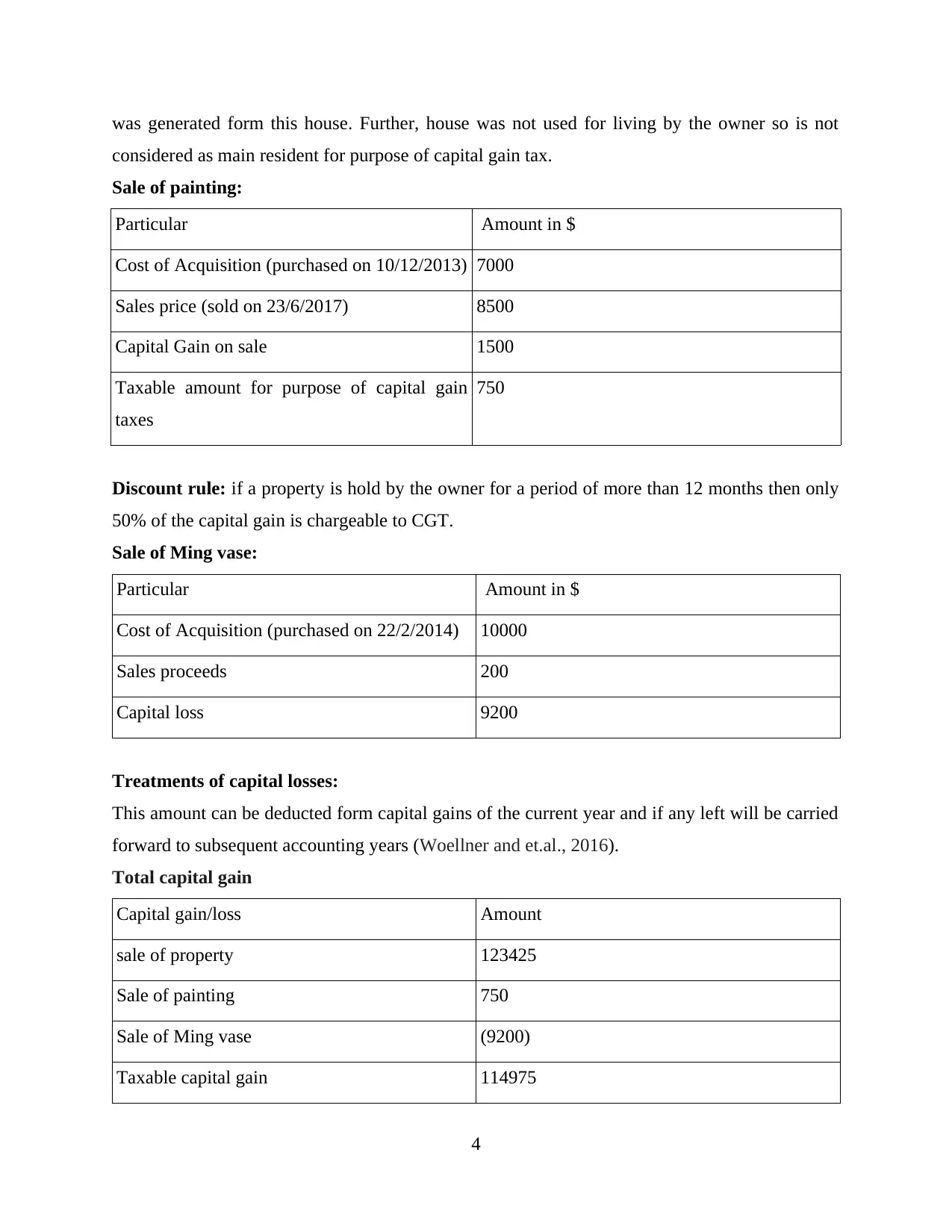

This report provides a detailed analysis of capital gains tax (CGT) within the framework of Australian taxation law. It examines the applicability of CGT to property sales, including main residences and rental properties, and other assets such as paintings and collectibles. The report outlines exemptions, cost base calculations, and the treatment of capital losses. It includes specific examples to illustrate how CGT is computed on the sale of a house (main residence and rental property) and artwork. The report also discusses the discount rule and the impact of holding periods on taxable capital gains. The document includes the computation of capital gains and losses for various scenarios, and it concludes with a summary of taxable capital gains. References to relevant sources such as the Australian Taxation Office (ATO) rulings and Australian Taxation Act, 1997, are also provided to support the analysis.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.