Taxation Law: Analysis of Amendment in Travel Expense Deductions

VerifiedAdded on 2020/02/18

|8

|2081

|44

Report

AI Summary

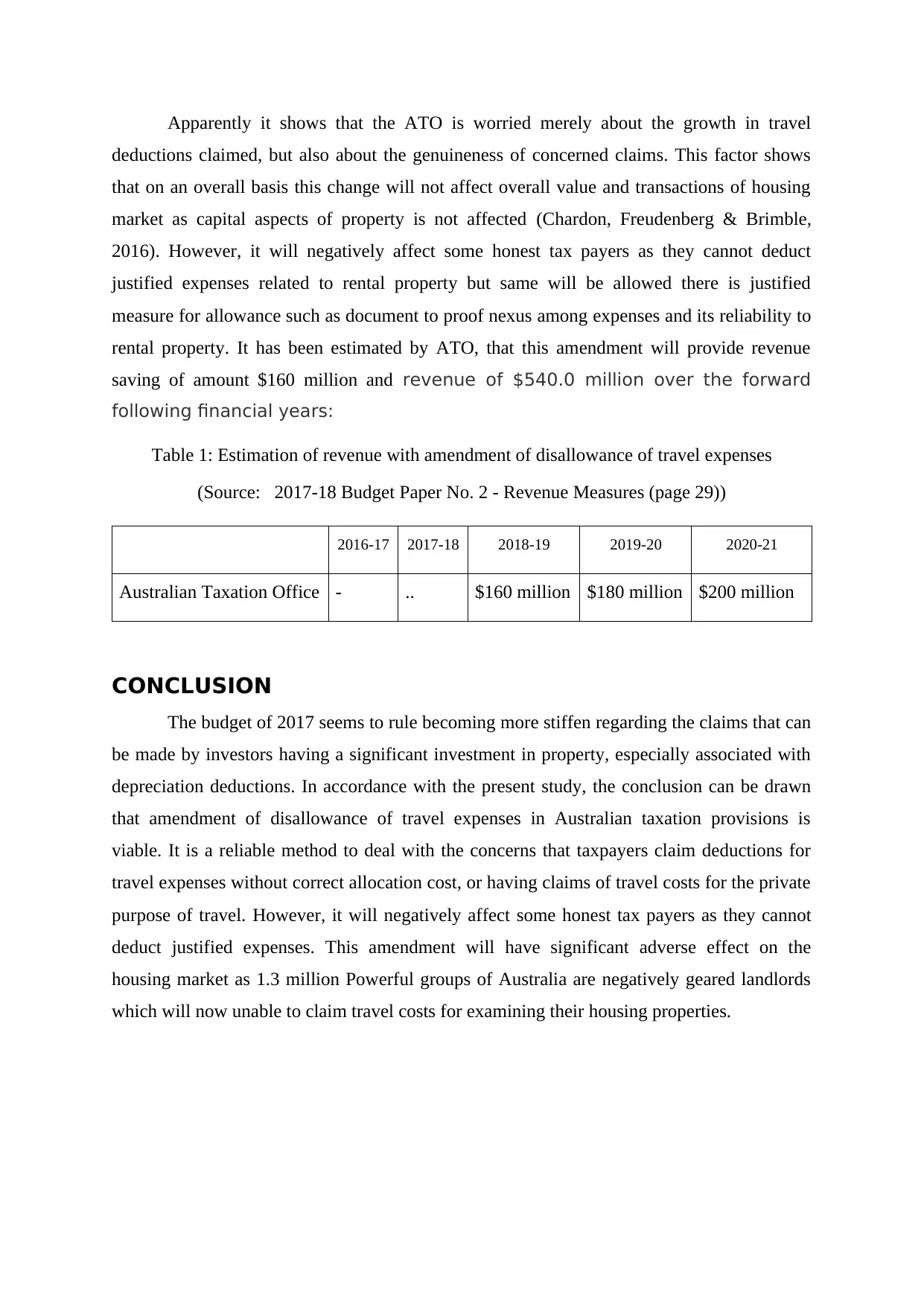

This report examines the recent amendment in Australian taxation law concerning the disallowance of travel expense deductions for rental properties. The amendment, introduced in the 2017-18 Federal Budget, restricts deductions for travel expenses related to the inspection, maintenance, and rent collection of residential rental properties. The rationale behind the amendment is to address concerns about taxpayers claiming deductions without proper cost allocation or for private purposes. The report details the amendment's impact on the housing market, including potential effects on property owners who manage their properties in remote areas. It also highlights the government's estimated revenue savings and the potential for increased scrutiny of travel expense claims. While the amendment aims to prevent tax evasion and ensure the integrity of tax measures, it may negatively affect some legitimate taxpayers. The report concludes that the amendment is a viable method to address concerns about travel expense deductions but acknowledges its potential adverse effects on some taxpayers and the housing market.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.