LAW20060 Taxation Law of Australia Individual Assignment 2019

VerifiedAdded on 2023/01/06

|17

|4361

|22

Homework Assignment

AI Summary

This document presents a comprehensive solution to an individual assignment on Australian Taxation Law (LAW20060). The assignment addresses several key areas, including the determination of effective asset life for depreciation, tax offsets, top tax rates, capital gains tax (CGT) exemptions, CGT events, and the calculation of income tax. It also examines tax deductions, such as interest on borrowings, and the deductibility of various expenses, including mobile phone expenses, child care expenses, and losses from theft. Furthermore, the assignment explores CGT events related to leases and the application of the CGT discount, along with the treatment of capital gains and losses. The solution incorporates relevant legislation, including the ITAA 1997, and case law to support the answers. The document concludes with a detailed analysis and conclusion, providing a thorough understanding of the complex aspects of Australian Taxation Law.

Running head: TAXATION LAW OF AUSTRALIA

Taxation Law of Australia

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Taxation Law of Australia

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW OF AUSTRALIA

Table of Contents

Question 1:.................................................................................................................................3

Answer to Part a:....................................................................................................................3

Answer to Part b:....................................................................................................................3

Answer to Part c:....................................................................................................................3

Answer to Part d:....................................................................................................................3

Answer to Part e:....................................................................................................................3

Answer to Part f:....................................................................................................................4

Answer to Part g:....................................................................................................................4

Answer to Part h:....................................................................................................................4

Answer to Part i:.....................................................................................................................5

Question 2:.................................................................................................................................5

Answer to Part a:....................................................................................................................5

Answer to Part b:....................................................................................................................6

Answer to Part c:....................................................................................................................6

Answer to Part d:....................................................................................................................7

Answer to Part e:....................................................................................................................7

Question 3:.................................................................................................................................8

Answer to Part a:....................................................................................................................8

Answer to Part b:....................................................................................................................8

Answer to Part c:....................................................................................................................9

Table of Contents

Question 1:.................................................................................................................................3

Answer to Part a:....................................................................................................................3

Answer to Part b:....................................................................................................................3

Answer to Part c:....................................................................................................................3

Answer to Part d:....................................................................................................................3

Answer to Part e:....................................................................................................................3

Answer to Part f:....................................................................................................................4

Answer to Part g:....................................................................................................................4

Answer to Part h:....................................................................................................................4

Answer to Part i:.....................................................................................................................5

Question 2:.................................................................................................................................5

Answer to Part a:....................................................................................................................5

Answer to Part b:....................................................................................................................6

Answer to Part c:....................................................................................................................6

Answer to Part d:....................................................................................................................7

Answer to Part e:....................................................................................................................7

Question 3:.................................................................................................................................8

Answer to Part a:....................................................................................................................8

Answer to Part b:....................................................................................................................8

Answer to Part c:....................................................................................................................9

2TAXATION LAW OF AUSTRALIA

Answer to Part d:..................................................................................................................10

Question 4:...............................................................................................................................10

Answer to Part a:..................................................................................................................10

Answer to Part b:..................................................................................................................11

Answer to Part c:..................................................................................................................11

Answer to Part d:..................................................................................................................12

Answer to Part e:..................................................................................................................12

Question 5:...............................................................................................................................12

Issues:...................................................................................................................................12

Laws:....................................................................................................................................13

Application:..........................................................................................................................14

Conclusion:..........................................................................................................................14

References:...............................................................................................................................15

Answer to Part d:..................................................................................................................10

Question 4:...............................................................................................................................10

Answer to Part a:..................................................................................................................10

Answer to Part b:..................................................................................................................11

Answer to Part c:..................................................................................................................11

Answer to Part d:..................................................................................................................12

Answer to Part e:..................................................................................................................12

Question 5:...............................................................................................................................12

Issues:...................................................................................................................................12

Laws:....................................................................................................................................13

Application:..........................................................................................................................14

Conclusion:..........................................................................................................................14

References:...............................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW OF AUSTRALIA

Question 1:

Answer to Part a:

According to the “Taxation Ruling of TR 2018/4”, there is a clarification provided

for the methods that the Taxation Commissioner has used in order to ascertain the effective

life of assets for depreciation, in accordance with “Section 40 (100) of ITAA 1997”.

Answer to Part b:

The details in relation to the available tax offsets could be obtained from “Division 13

of ITAA 1997”.

Answer to Part c:

The top tax rate, which is applicable to an Australian resident taxpayer during the

2018/19 tax year, is $54,097 plus 45 cents for each $1 above $180,000 for income equal to

$180,001 and above1.

Answer to Part d:

Certain exemptions are provided to a taxpayer, in which there has been minimisation,

disregard or deferral of capital gains or losses. In accordance with the provision of “Section

118 (10-1) of ITAA 1997”, assets like collectibles purchased for or below $500 are exempted

from CGT.

Answer to Part e:

“CGT event B1 Section 104 (15) of ITAA 1997” is related to the enjoyment and use

before passing the title. This event occurs when an individual enters into a contract with an

1 Ragnar, Arnason, and Hannes H. Gissurarson. Individual transferable quotas in theory and

practice. Vol. 4. Almennabókafélagið, 2017.

Question 1:

Answer to Part a:

According to the “Taxation Ruling of TR 2018/4”, there is a clarification provided

for the methods that the Taxation Commissioner has used in order to ascertain the effective

life of assets for depreciation, in accordance with “Section 40 (100) of ITAA 1997”.

Answer to Part b:

The details in relation to the available tax offsets could be obtained from “Division 13

of ITAA 1997”.

Answer to Part c:

The top tax rate, which is applicable to an Australian resident taxpayer during the

2018/19 tax year, is $54,097 plus 45 cents for each $1 above $180,000 for income equal to

$180,001 and above1.

Answer to Part d:

Certain exemptions are provided to a taxpayer, in which there has been minimisation,

disregard or deferral of capital gains or losses. In accordance with the provision of “Section

118 (10-1) of ITAA 1997”, assets like collectibles purchased for or below $500 are exempted

from CGT.

Answer to Part e:

“CGT event B1 Section 104 (15) of ITAA 1997” is related to the enjoyment and use

before passing the title. This event occurs when an individual enters into a contract with an

1 Ragnar, Arnason, and Hannes H. Gissurarson. Individual transferable quotas in theory and

practice. Vol. 4. Almennabókafélagið, 2017.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW OF AUSTRALIA

organisation, in which the enjoyment and right-of-use CGT assets owned by the individual is

passed to the organisation. Moreover, according to this event, the asset titles might be

transferred to the organisation at or before the contract conclusion2.

Answer to Part f:

According to “Section 4-10 (3) of ITAA 1997”, the following formula is contained:

Income Tax = (Taxable Income * Rate) – Tax Offsets

Answer to Part g:

According to the High Court Case of “FC of T v Day 2008 ATC 20-064”, legal

outgoings were highlighted that the taxpayer incurred in order to generate chargeable

earnings and the simultaneous net conditions mentioned in “Paragraph 8-1(1)(a) of ITAA

1997”. This case carries immense significance associated with the tax deduction of legal

outgoings in relation to a public servant that paid charges in order to defend the conduct

arising out of day-to-day activities3. Legal expenditure deduction was provided to the

taxpayer, in accordance with the provision mentioned under “Section 8-1 of ITAA 1997”

incurred in the year 2002 so that the disciplinary actions could be defended imposed upon the

taxpayer by the employer.

Answer to Part h:

The average tax rate analyses the tax burden and the marginal tax rate evaluates the

impact of tax on incentive savings, earnings, spending or investment. The average tax rate

2 Joseph, Bankman, et al. Federal Income Taxation. Aspen Casebook, 2018.

3 Stephen, Barkoczy, "Foundations of taxation law 2016." OUP Catalogue (2016).

organisation, in which the enjoyment and right-of-use CGT assets owned by the individual is

passed to the organisation. Moreover, according to this event, the asset titles might be

transferred to the organisation at or before the contract conclusion2.

Answer to Part f:

According to “Section 4-10 (3) of ITAA 1997”, the following formula is contained:

Income Tax = (Taxable Income * Rate) – Tax Offsets

Answer to Part g:

According to the High Court Case of “FC of T v Day 2008 ATC 20-064”, legal

outgoings were highlighted that the taxpayer incurred in order to generate chargeable

earnings and the simultaneous net conditions mentioned in “Paragraph 8-1(1)(a) of ITAA

1997”. This case carries immense significance associated with the tax deduction of legal

outgoings in relation to a public servant that paid charges in order to defend the conduct

arising out of day-to-day activities3. Legal expenditure deduction was provided to the

taxpayer, in accordance with the provision mentioned under “Section 8-1 of ITAA 1997”

incurred in the year 2002 so that the disciplinary actions could be defended imposed upon the

taxpayer by the employer.

Answer to Part h:

The average tax rate analyses the tax burden and the marginal tax rate evaluates the

impact of tax on incentive savings, earnings, spending or investment. The average tax rate

2 Joseph, Bankman, et al. Federal Income Taxation. Aspen Casebook, 2018.

3 Stephen, Barkoczy, "Foundations of taxation law 2016." OUP Catalogue (2016).

5TAXATION LAW OF AUSTRALIA

denotes the total tax divided by the overall income. On the other hand, the marginal tax rate

signifies the incremental tax incurred on increased income.

Answer to Part i:

A consumption tax could be defined as expenditure tax imposed on the purchase of

products and services. It could be referred as the taxation system, in which the individuals are

imposed taxes based on their level of consumption rather than the amount contributed by

them to the economy4.

Question 2:

Answer to Part a:

The Australian Taxation Office (ATO) allows a taxpayer for claiming deduction in

relation to expenses paid for interest on borrowings at the time of producing assessable

income. According to “Section 8 (1) of ITAA 1997”, interest on loan paid for business

purpose is adjudged in the form of allowable deduction.

Brent has incurred interest on loan in order to settle the wages of the staffs. By

referring to the case of “Amalgamated Zinc Limited v FC of T (1935)”, Brent has incurred

interest on land so that the taxable earnings could be generated or gained accordingly. Hence,

based on the positive limbs related to “Section 8 (1) of ITAA 1997”, there would be an

allowable deduction to Brent for interest on borrowings5.

4 Duncan, Bentley, "Does A Capital Gains Tax Work? The Australian Experience Eleven

Years On." Journal of Malaysian and Comparative Law 23 (2019): 13-36.

5 John D., Buenker, The Income Tax and the Progressive Era. Routledge, 2018.

denotes the total tax divided by the overall income. On the other hand, the marginal tax rate

signifies the incremental tax incurred on increased income.

Answer to Part i:

A consumption tax could be defined as expenditure tax imposed on the purchase of

products and services. It could be referred as the taxation system, in which the individuals are

imposed taxes based on their level of consumption rather than the amount contributed by

them to the economy4.

Question 2:

Answer to Part a:

The Australian Taxation Office (ATO) allows a taxpayer for claiming deduction in

relation to expenses paid for interest on borrowings at the time of producing assessable

income. According to “Section 8 (1) of ITAA 1997”, interest on loan paid for business

purpose is adjudged in the form of allowable deduction.

Brent has incurred interest on loan in order to settle the wages of the staffs. By

referring to the case of “Amalgamated Zinc Limited v FC of T (1935)”, Brent has incurred

interest on land so that the taxable earnings could be generated or gained accordingly. Hence,

based on the positive limbs related to “Section 8 (1) of ITAA 1997”, there would be an

allowable deduction to Brent for interest on borrowings5.

4 Duncan, Bentley, "Does A Capital Gains Tax Work? The Australian Experience Eleven

Years On." Journal of Malaysian and Comparative Law 23 (2019): 13-36.

5 John D., Buenker, The Income Tax and the Progressive Era. Routledge, 2018.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW OF AUSTRALIA

Answer to Part b:

On certain occasions, it is necessary to assign outgoings or losses or they are

deductible partially. According to the court case of “Ronpiban Tin FL v FC of T (1949)”, it

is necessary for the Commissioner in order to ascertain the part of expenses incurred to

produce assessable income6. Although expenses are incurred for work and private purposes,

deduction could be claimed by a taxpayer only for work purpose.

$500 was incurred in the form of mobile phone expense by Julie, 60% of which is

work-related phone calls. By referring to the case of “Ronpiban Tin FL v FC of T (1949)”,

deduction could be claimed by Julie up to 60% of the overall phone expense in accordance

with “Section 8 (1) of ITAA 1997”7. However, the remaining part of expense is private in

nature, which could not be claimed for deduction, as per the negative limbs mentioned in

“Section 8-1 (2) of ITAA 1997”.

Answer to Part c:

Child care expense is restricted by “Section 8 (1) of ITAA 1997” for deduction. In the

case of “Ledge v FC of T (1972)”, the taxpayer was not allowed any deduction for child care

expense at the time of attending work, since the outgoings were not incidental or pertinent to

produce taxable income8.

6 Irina V., Gashenko, Yuliya S. Zima, and Armenak V. Davidyan. "Principles and Methods of

Taxation." Optimization of the Taxation System: Preconditions, Tendencies and Perspectives.

Springer, Cham, 2019. 33-39.

7 Leonard E., Burman, et al. "Financial transaction taxes in theory and practice." National Tax

Journal 69.1 (2016): 171.

8 Chris, Evans, John Minas, and Youngdeok Lim. "Taxing personal capital gains in Australia:

an alternative way forward." Austl. Tax F. 30 (2015): 735.

Answer to Part b:

On certain occasions, it is necessary to assign outgoings or losses or they are

deductible partially. According to the court case of “Ronpiban Tin FL v FC of T (1949)”, it

is necessary for the Commissioner in order to ascertain the part of expenses incurred to

produce assessable income6. Although expenses are incurred for work and private purposes,

deduction could be claimed by a taxpayer only for work purpose.

$500 was incurred in the form of mobile phone expense by Julie, 60% of which is

work-related phone calls. By referring to the case of “Ronpiban Tin FL v FC of T (1949)”,

deduction could be claimed by Julie up to 60% of the overall phone expense in accordance

with “Section 8 (1) of ITAA 1997”7. However, the remaining part of expense is private in

nature, which could not be claimed for deduction, as per the negative limbs mentioned in

“Section 8-1 (2) of ITAA 1997”.

Answer to Part c:

Child care expense is restricted by “Section 8 (1) of ITAA 1997” for deduction. In the

case of “Ledge v FC of T (1972)”, the taxpayer was not allowed any deduction for child care

expense at the time of attending work, since the outgoings were not incidental or pertinent to

produce taxable income8.

6 Irina V., Gashenko, Yuliya S. Zima, and Armenak V. Davidyan. "Principles and Methods of

Taxation." Optimization of the Taxation System: Preconditions, Tendencies and Perspectives.

Springer, Cham, 2019. 33-39.

7 Leonard E., Burman, et al. "Financial transaction taxes in theory and practice." National Tax

Journal 69.1 (2016): 171.

8 Chris, Evans, John Minas, and Youngdeok Lim. "Taxing personal capital gains in Australia:

an alternative way forward." Austl. Tax F. 30 (2015): 735.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW OF AUSTRALIA

Sally incurred babysitting expense in order to look after her child, which is a non-

deductible expense owing to the fact that it is domestic or private in nature. This type of

expense fails to meet either the positive limb or negative limb mentioned in “Section 8-1 (2)

(b) of ITAA 1997”.

Answer to Part d:

The application of “Section 8 (1) of ITAA 1997” is possible for both outgoings and

losses incurred by the taxpayer. In the case of “Charles Moore & Co (WA) Private Limited v

FC of T (1956)”, the court permitted deduction to the taxpayer owing to the loss occurring

from the theft of the earnings at the time of going to the bank.

According to the positive limbs of “Section 8 (1) of ITAA 1997”, it is possible for

Jerry to claim deduction for the goods stolen by his long-term staff9. The loss has been

incurred at the time of conduction of business operations, as the goods were supposed to

generate earnings for Jerry.

Answer to Part e:

The preliminary losses or outgoings at the start of revenue generation acts are treated

as such that they did not happen in the course of such activity and thus, general deductions

are allowed in compliance with “Section 8 (1) of ITAA 1997”. In the case of “Maddalena v

FCT (1971)”, the outgoings incurred in obtaining new job were not in the course of

generating taxable income, as the outgoings happened at a point sooner and thus, they are not

allowed for deduction, as per “Section 8 (1) of ITAA 1997”.

9 Toni, Chardon, Brett Freudenberg, and Mark Brimble. "Tax literacy in Australia: not

knowing your deduction from your offset." Austl. Tax F. 31 (2016): 321.

Sally incurred babysitting expense in order to look after her child, which is a non-

deductible expense owing to the fact that it is domestic or private in nature. This type of

expense fails to meet either the positive limb or negative limb mentioned in “Section 8-1 (2)

(b) of ITAA 1997”.

Answer to Part d:

The application of “Section 8 (1) of ITAA 1997” is possible for both outgoings and

losses incurred by the taxpayer. In the case of “Charles Moore & Co (WA) Private Limited v

FC of T (1956)”, the court permitted deduction to the taxpayer owing to the loss occurring

from the theft of the earnings at the time of going to the bank.

According to the positive limbs of “Section 8 (1) of ITAA 1997”, it is possible for

Jerry to claim deduction for the goods stolen by his long-term staff9. The loss has been

incurred at the time of conduction of business operations, as the goods were supposed to

generate earnings for Jerry.

Answer to Part e:

The preliminary losses or outgoings at the start of revenue generation acts are treated

as such that they did not happen in the course of such activity and thus, general deductions

are allowed in compliance with “Section 8 (1) of ITAA 1997”. In the case of “Maddalena v

FCT (1971)”, the outgoings incurred in obtaining new job were not in the course of

generating taxable income, as the outgoings happened at a point sooner and thus, they are not

allowed for deduction, as per “Section 8 (1) of ITAA 1997”.

9 Toni, Chardon, Brett Freudenberg, and Mark Brimble. "Tax literacy in Australia: not

knowing your deduction from your offset." Austl. Tax F. 31 (2016): 321.

8TAXATION LAW OF AUSTRALIA

The outgoings that were incurred in order to contest in the election of the local

government were preliminary to the start of revenue generation acts, as it is not taking place

in due course gaining or generating assessable income and thus, they are not permitted for

deduction in accordance with “Section 8 (1) of ITAA 1997”.

Question 3:

Answer to Part a:

“CGT event F2” could be applied, in which it is possible for an individual taxpayer in

extending, renewing or granting long-term lease. It is applicable to the underlying land owner

or the taxpayer that has obtained grant with sub-lease10. It is apparent that Andy is the owner

of land and the individual has granted five-year lease term to Brian at $5,000 premium. As a

result, “CGT event F2” has taken place. Therefore, it is not possible for Andy to obtain CGT

discount of 50%, as it could not be applied to the “CGT event F2”.

Answer to Part b:

ATO states that there is occurrence of “CGT event B1”, in which the new owner

acquires the use of land. From the actual perspective, the enjoyment and rise of land occurs at

the time land ownership is taken over by the new owner and the date on which the new holder

is permitted to rents and profits. In lieu of $40,000, Farm Limited has the alternative to buy

the 100-acre firm for $00,000. This leads to the occurrence of “CGT event B1” for John.

Therefore, it is possible to apply the CGT discount of 50% on the above transaction of John.

Answer to Part c:

According to the ATO, if the dwelling of the taxpayer is not the main residence for

the entre ownership period and it is used to produce income, in such case, a partial main

10 Mark, Davison, Ann Monotti, and Leanne Wiseman. Australian intellectual property law.

Cambridge University Press, 2015.

The outgoings that were incurred in order to contest in the election of the local

government were preliminary to the start of revenue generation acts, as it is not taking place

in due course gaining or generating assessable income and thus, they are not permitted for

deduction in accordance with “Section 8 (1) of ITAA 1997”.

Question 3:

Answer to Part a:

“CGT event F2” could be applied, in which it is possible for an individual taxpayer in

extending, renewing or granting long-term lease. It is applicable to the underlying land owner

or the taxpayer that has obtained grant with sub-lease10. It is apparent that Andy is the owner

of land and the individual has granted five-year lease term to Brian at $5,000 premium. As a

result, “CGT event F2” has taken place. Therefore, it is not possible for Andy to obtain CGT

discount of 50%, as it could not be applied to the “CGT event F2”.

Answer to Part b:

ATO states that there is occurrence of “CGT event B1”, in which the new owner

acquires the use of land. From the actual perspective, the enjoyment and rise of land occurs at

the time land ownership is taken over by the new owner and the date on which the new holder

is permitted to rents and profits. In lieu of $40,000, Farm Limited has the alternative to buy

the 100-acre firm for $00,000. This leads to the occurrence of “CGT event B1” for John.

Therefore, it is possible to apply the CGT discount of 50% on the above transaction of John.

Answer to Part c:

According to the ATO, if the dwelling of the taxpayer is not the main residence for

the entre ownership period and it is used to produce income, in such case, a partial main

10 Mark, Davison, Ann Monotti, and Leanne Wiseman. Australian intellectual property law.

Cambridge University Press, 2015.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW OF AUSTRALIA

residence exemption is allowed to the taxpayer11. Olivia and Jamie have purchased a

property, which they have rented for two years. After the occupation of property, the same

was let out for earning income and it was utilised as the main residence before sale in 2018.

As a result, Jamie and Olivia are eligible for partial main residence exemption after the

property disposal. Hence, the method of 50% CGT discount is possible to be used by Olivia

and Jamie so that they could ascertain the net capital gains tax effectively12.

Answer to Part d:

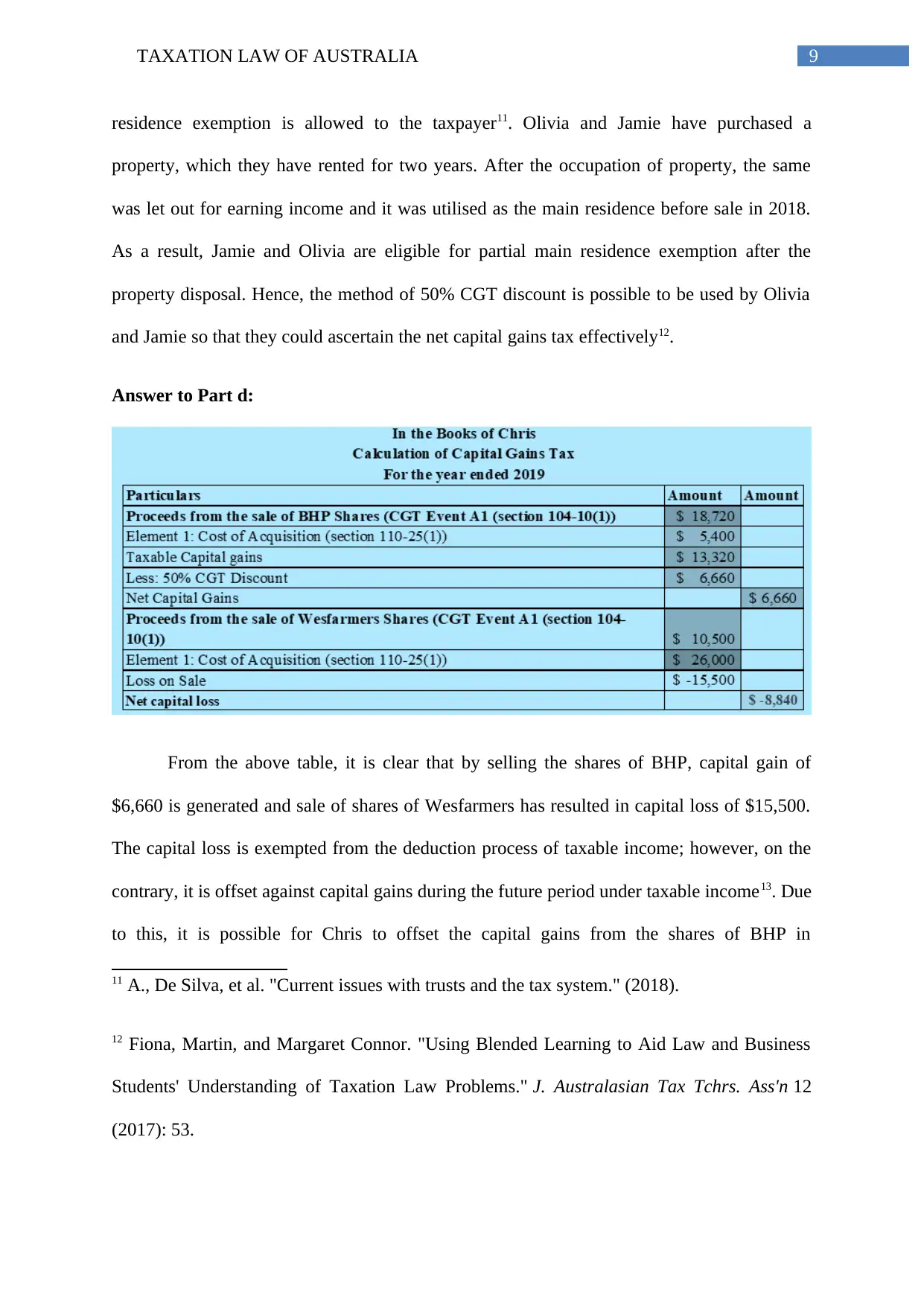

From the above table, it is clear that by selling the shares of BHP, capital gain of

$6,660 is generated and sale of shares of Wesfarmers has resulted in capital loss of $15,500.

The capital loss is exempted from the deduction process of taxable income; however, on the

contrary, it is offset against capital gains during the future period under taxable income13. Due

to this, it is possible for Chris to offset the capital gains from the shares of BHP in

11 A., De Silva, et al. "Current issues with trusts and the tax system." (2018).

12 Fiona, Martin, and Margaret Connor. "Using Blended Learning to Aid Law and Business

Students' Understanding of Taxation Law Problems." J. Australasian Tax Tchrs. Ass'n 12

(2017): 53.

residence exemption is allowed to the taxpayer11. Olivia and Jamie have purchased a

property, which they have rented for two years. After the occupation of property, the same

was let out for earning income and it was utilised as the main residence before sale in 2018.

As a result, Jamie and Olivia are eligible for partial main residence exemption after the

property disposal. Hence, the method of 50% CGT discount is possible to be used by Olivia

and Jamie so that they could ascertain the net capital gains tax effectively12.

Answer to Part d:

From the above table, it is clear that by selling the shares of BHP, capital gain of

$6,660 is generated and sale of shares of Wesfarmers has resulted in capital loss of $15,500.

The capital loss is exempted from the deduction process of taxable income; however, on the

contrary, it is offset against capital gains during the future period under taxable income13. Due

to this, it is possible for Chris to offset the capital gains from the shares of BHP in

11 A., De Silva, et al. "Current issues with trusts and the tax system." (2018).

12 Fiona, Martin, and Margaret Connor. "Using Blended Learning to Aid Law and Business

Students' Understanding of Taxation Law Problems." J. Australasian Tax Tchrs. Ass'n 12

(2017): 53.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW OF AUSTRALIA

comparison to the capital loss incurred from the sale of the shares of Wesfarmers. Hence, the

net capital loss of $8,840 could be brought forward in future years.

Question 4:

Answer to Part a:

It is not possible to hold a taxpayer for assessment in case of simple prize winnings.

However, prize winnings could be treated in the form of assessable income; in case, there is

sufficient relation with the income generation acts of the taxpayer. In the case of “FCT v

Kelly (1985)”, the award that Channel 7 has provided to the footballer for best and fairest

player was treated in the form of ordinary income, since it was related to the usage of skill

and employment of the taxpayer14.

The receipt of prize money of $2,000 by the taxpayer for making the best year

advertisement includes an ordinary income, as per “Section 6 (5) of ITAA 1997”. This is a

taxable amount, since it is associated with income generation activities, which is incidental to

the work of the taxpayer15.

Answer to Part b:

According to “Section 6 (1) of ITAA 1936”, the personal exertion income constitutes

of wages, allowances, earnings, remunerations, gratuities and others that the employee has

13 Angharad, Miller, and Lynne Oats. Principles of international taxation. Bloomsbury

Publishing, 2016.

14 Michael J., Graetz, "Foundations of international income taxation." (2013).

15 Paul, Kenny, Michael Blissenden, and Sylvia Villios. Australian Tax 2018. 2018.

comparison to the capital loss incurred from the sale of the shares of Wesfarmers. Hence, the

net capital loss of $8,840 could be brought forward in future years.

Question 4:

Answer to Part a:

It is not possible to hold a taxpayer for assessment in case of simple prize winnings.

However, prize winnings could be treated in the form of assessable income; in case, there is

sufficient relation with the income generation acts of the taxpayer. In the case of “FCT v

Kelly (1985)”, the award that Channel 7 has provided to the footballer for best and fairest

player was treated in the form of ordinary income, since it was related to the usage of skill

and employment of the taxpayer14.

The receipt of prize money of $2,000 by the taxpayer for making the best year

advertisement includes an ordinary income, as per “Section 6 (5) of ITAA 1997”. This is a

taxable amount, since it is associated with income generation activities, which is incidental to

the work of the taxpayer15.

Answer to Part b:

According to “Section 6 (1) of ITAA 1936”, the personal exertion income constitutes

of wages, allowances, earnings, remunerations, gratuities and others that the employee has

13 Angharad, Miller, and Lynne Oats. Principles of international taxation. Bloomsbury

Publishing, 2016.

14 Michael J., Graetz, "Foundations of international income taxation." (2013).

15 Paul, Kenny, Michael Blissenden, and Sylvia Villios. Australian Tax 2018. 2018.

11TAXATION LAW OF AUSTRALIA

obtained for the services provided or proceeds from conducting business activities. In this

case, the employee has received $500 from the employer associated with the expenses

incurred at the time of going to workplace from Sydney. The amount would be treated in the

form of income, since it includes allowance obtained for employment by working as a staff.

Answer to Part c:

A gain is deemed to be a simple gift, if it does not have the nature of income. In the

case of “FCT v Scott (1966)”, the client has obtained gifts amounting to £10,000 from his

wife from the personal estate, which was not deemed to be income. Therefore, the iphone

amounting to $1,000 obtained by the taxpayer is a gift from the client not having the nature of

income.

Answer to Part d:

“Paragraph 118-37 (1) (b) of ITAA 1997” states that an individual needs to disregard

receipts for the purpose of capital gains, in which the amount is associated with damages or

compensation for personal illness, wrong or injuries. The taxpayer obtained an amount of

$10,000 as damages owing to the personal injury from car accident. Thus, the amount of

compensation does not qualify as income and it is deemed to be exempted from tax16.

Answer to Part e:

Any kind of taxable earnings obtained or estimated to be obtained in future owing to

the reason of present entitlement of income for the future period is considered to be too

remote in forming a link with the existing income year. The taxpayer has bought shares

amounting to $5 per share; however, in the current year, the market value of shares was $7.50

per share. This rise in value could not be viewed as income, since the taxpayer has not made

16 Janet E., Milne, and Mikael Skou Andersen, eds. Handbook of research on environmental

taxation. Edward Elgar Publishing, 2014.

obtained for the services provided or proceeds from conducting business activities. In this

case, the employee has received $500 from the employer associated with the expenses

incurred at the time of going to workplace from Sydney. The amount would be treated in the

form of income, since it includes allowance obtained for employment by working as a staff.

Answer to Part c:

A gain is deemed to be a simple gift, if it does not have the nature of income. In the

case of “FCT v Scott (1966)”, the client has obtained gifts amounting to £10,000 from his

wife from the personal estate, which was not deemed to be income. Therefore, the iphone

amounting to $1,000 obtained by the taxpayer is a gift from the client not having the nature of

income.

Answer to Part d:

“Paragraph 118-37 (1) (b) of ITAA 1997” states that an individual needs to disregard

receipts for the purpose of capital gains, in which the amount is associated with damages or

compensation for personal illness, wrong or injuries. The taxpayer obtained an amount of

$10,000 as damages owing to the personal injury from car accident. Thus, the amount of

compensation does not qualify as income and it is deemed to be exempted from tax16.

Answer to Part e:

Any kind of taxable earnings obtained or estimated to be obtained in future owing to

the reason of present entitlement of income for the future period is considered to be too

remote in forming a link with the existing income year. The taxpayer has bought shares

amounting to $5 per share; however, in the current year, the market value of shares was $7.50

per share. This rise in value could not be viewed as income, since the taxpayer has not made

16 Janet E., Milne, and Mikael Skou Andersen, eds. Handbook of research on environmental

taxation. Edward Elgar Publishing, 2014.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.