HA3042 Taxation Law T2 2018: Australian Taxation Case Law Analysis

VerifiedAdded on 2023/06/07

|11

|2976

|328

Case Study

AI Summary

This assignment delves into various aspects of Australian taxation law through case studies. It addresses the tax implications of lottery winnings, particularly the 'Set for Life' lottery, referencing Australian Tax Office guidelines and rulings to determine taxability. The assignment also analyzes the accrual basis of accounting in the context of Corner Pharmacy, calculating taxable income by considering cash sales, credit card sales, pharmaceutical benefits, and allowable tax deductions. Furthermore, it examines the landmark case of Inland Revenue Commissioners v. Duke of Westminster, discussing tax avoidance strategies and their impact on taxpayers and the Australian Tax Office. The analysis includes the ATO's measures to control unlawful tax avoidance, highlighting the Tax Avoidance Taskforce and Multinational anti-tax avoidance bodies.

TAXATION LAW

AUSTRALIAN TAXATION CASE LAWS AND ITS APPLICATION

Course:

Professor’s Name

Institution

City

Date

AUSTRALIAN TAXATION CASE LAWS AND ITS APPLICATION

Course:

Professor’s Name

Institution

City

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TAXATION LAW

Question 1;

According to Australian Tax Office on prizes and awards, any windfall gain that is earned

as a result of a lottery run by institutions that make money the likes of financial institutions,

building industrial societies, credit unions chambers must be declared to the tax man by

respective individuals who indeed won them for tax purposes.

These prices and gifts that appear in the form of cash, cars, holidays, credit loans and

debentures that are at low-interest levels or even interest-free loans must be declared and

reported as though it is part of their income without fail for tax purposes. In cases where gifts are

not in cash form at some point, the items are valued for computation purposes and of course by

appointed commissioners on behalf of AUSTRALIAN TAX OFFICE. Likewise the same office

of the tax man tasks both parties, i.e., the awarder and the awardee to take the initiative of

declaring the act and effort which either party has taken to ensure that the prizes and awards have

been accounted for legitimately.

However it is not all awards or prizes won that are declarable as income for tax purpose, oh

no, this is because the Australian Tax Office considers this prizes and awards won on ordinary

lotteries like raffle ticket and lotto to be out of luck and fate. Awards, therefore, succeeded in this

form of the usual or ordinary lottery are not declarable for tax purposes as income at all.

For instance this case of “Set For Life” lottery is an excellent prudent example of this

scenario of non –declarable gift simply because this was an instant lottery conducted by Lotteries

Commission that was engaging parties who were similarly not aware of whether they would win

or not since it was a trial of fate and luck. Therefore the 50000 payable for 20years in this set for

life lottery platform is not taxable at all according to Australian Tax Office.

Australian Tax Office item 2002/644 is seen to interpret a decision on what should be

termed as a gift or prize that is worn resulting from the ordinary lottery and that which is not

Question 1;

According to Australian Tax Office on prizes and awards, any windfall gain that is earned

as a result of a lottery run by institutions that make money the likes of financial institutions,

building industrial societies, credit unions chambers must be declared to the tax man by

respective individuals who indeed won them for tax purposes.

These prices and gifts that appear in the form of cash, cars, holidays, credit loans and

debentures that are at low-interest levels or even interest-free loans must be declared and

reported as though it is part of their income without fail for tax purposes. In cases where gifts are

not in cash form at some point, the items are valued for computation purposes and of course by

appointed commissioners on behalf of AUSTRALIAN TAX OFFICE. Likewise the same office

of the tax man tasks both parties, i.e., the awarder and the awardee to take the initiative of

declaring the act and effort which either party has taken to ensure that the prizes and awards have

been accounted for legitimately.

However it is not all awards or prizes won that are declarable as income for tax purpose, oh

no, this is because the Australian Tax Office considers this prizes and awards won on ordinary

lotteries like raffle ticket and lotto to be out of luck and fate. Awards, therefore, succeeded in this

form of the usual or ordinary lottery are not declarable for tax purposes as income at all.

For instance this case of “Set For Life” lottery is an excellent prudent example of this

scenario of non –declarable gift simply because this was an instant lottery conducted by Lotteries

Commission that was engaging parties who were similarly not aware of whether they would win

or not since it was a trial of fate and luck. Therefore the 50000 payable for 20years in this set for

life lottery platform is not taxable at all according to Australian Tax Office.

Australian Tax Office item 2002/644 is seen to interpret a decision on what should be

termed as a gift or prize that is worn resulting from the ordinary lottery and that which is not

TAXATION LAW

Woellner, Barkoczy, Murphy, Evans and Pinto(2010.Pg 34.) It was introduced to guide the

taxpayers who venture in lottery and gaming activities as to what they should declare and what

not to avoid penalty and of course prosecution. It is from this regulation that we derive the aspect

that non-payment of tax is only applicable if the payment award is done on monthly and if it is

on an annual basis no extra gain or interest is earned from it as it is in seeing ‘Set For Life’ case

whereby expected monthly payment of 20000 for 12 months is not seen to be invested. If the

same lump sum amount or monthly pay is spent to generate revenue whether as interest or bonus

it will be taxed as capital gain or as regular revenue.

Exemption of tax on prizes and awards won through lotteries is likewise illustrated and

defined in the Income Tax 2584 preamble 2 whereby it elaborates more in Part IIIA that a payer

lottery winning is deemed as an asset hence an attraction of a capital gain or loss but only upon

disposal therefore not in order for the tax man to claim tax declaration on an asset that is not

disposed. The ruling is further seen to warn on capitalization of this winning to generate revenue

by informing the tax man that as soon as the lottery winning is capitalized and invested in a

manner suggesting interest or income generation at that point capital gain or loss on tax will be

imposed. This ruling as definitely explained why the only amount on lottery winning is the single

item that enjoys tax exemption holiday icon Saad (2014.Pg 1069.).

Indeed it is now clear that the lottery payment done by Set For Life scratches as long as the

beneficiary is alive he or she will enjoy this tax holiday as that whose annual income is not

taxable at all as directed by Australian Tax Office purposely because it results from ordinary

lottery winning competition that had the option of win to loss outcome. This non-taxation

exercise of the awardee is however limited to the winning amount only hence any extra interest

value generated from the investment of the winning amount will be taxed as stipulated in the law

without a do.

Woellner, Barkoczy, Murphy, Evans and Pinto(2010.Pg 34.) It was introduced to guide the

taxpayers who venture in lottery and gaming activities as to what they should declare and what

not to avoid penalty and of course prosecution. It is from this regulation that we derive the aspect

that non-payment of tax is only applicable if the payment award is done on monthly and if it is

on an annual basis no extra gain or interest is earned from it as it is in seeing ‘Set For Life’ case

whereby expected monthly payment of 20000 for 12 months is not seen to be invested. If the

same lump sum amount or monthly pay is spent to generate revenue whether as interest or bonus

it will be taxed as capital gain or as regular revenue.

Exemption of tax on prizes and awards won through lotteries is likewise illustrated and

defined in the Income Tax 2584 preamble 2 whereby it elaborates more in Part IIIA that a payer

lottery winning is deemed as an asset hence an attraction of a capital gain or loss but only upon

disposal therefore not in order for the tax man to claim tax declaration on an asset that is not

disposed. The ruling is further seen to warn on capitalization of this winning to generate revenue

by informing the tax man that as soon as the lottery winning is capitalized and invested in a

manner suggesting interest or income generation at that point capital gain or loss on tax will be

imposed. This ruling as definitely explained why the only amount on lottery winning is the single

item that enjoys tax exemption holiday icon Saad (2014.Pg 1069.).

Indeed it is now clear that the lottery payment done by Set For Life scratches as long as the

beneficiary is alive he or she will enjoy this tax holiday as that whose annual income is not

taxable at all as directed by Australian Tax Office purposely because it results from ordinary

lottery winning competition that had the option of win to loss outcome. This non-taxation

exercise of the awardee is however limited to the winning amount only hence any extra interest

value generated from the investment of the winning amount will be taxed as stipulated in the law

without a do.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TAXATION LAW

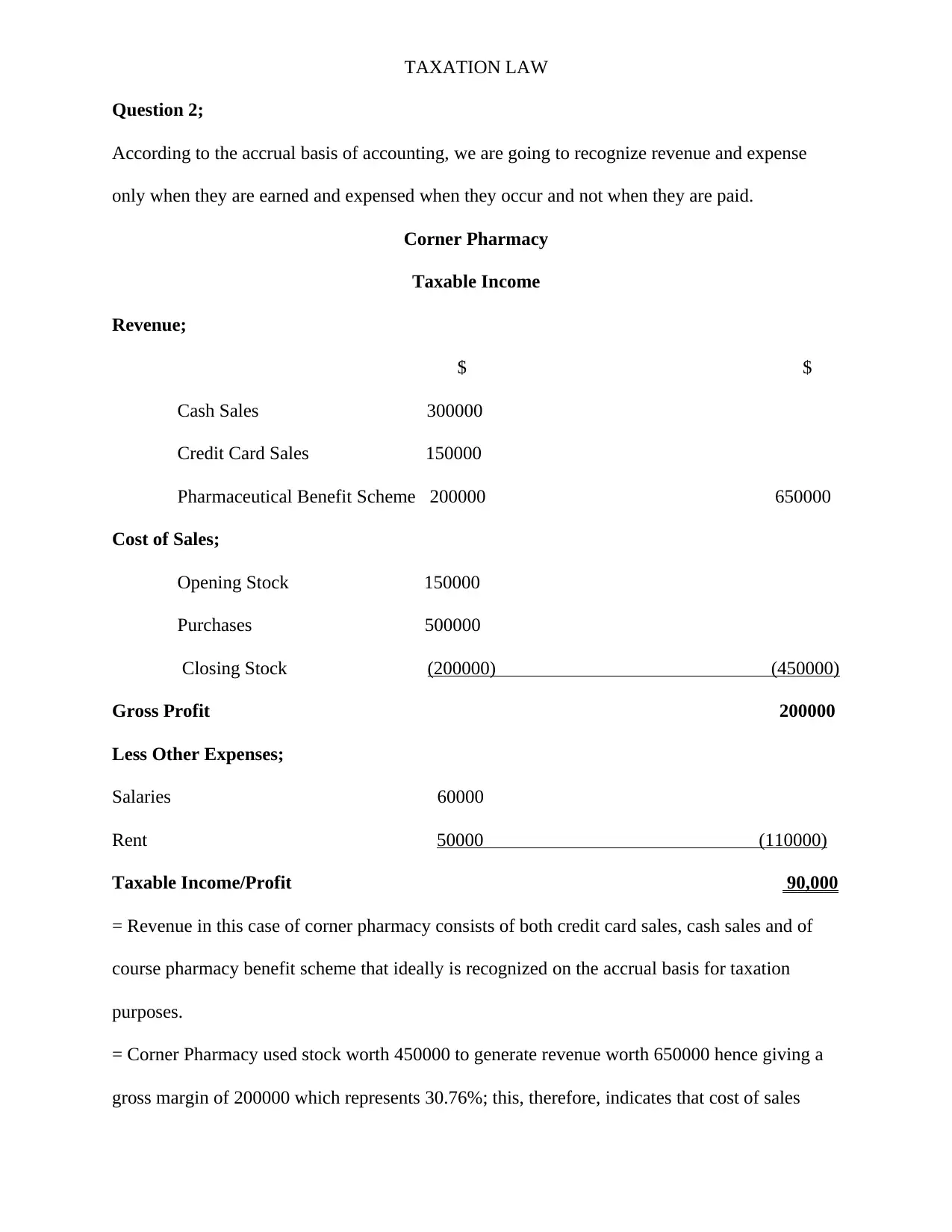

Question 2;

According to the accrual basis of accounting, we are going to recognize revenue and expense

only when they are earned and expensed when they occur and not when they are paid.

Corner Pharmacy

Taxable Income

Revenue;

$ $

Cash Sales 300000

Credit Card Sales 150000

Pharmaceutical Benefit Scheme 200000 650000

Cost of Sales;

Opening Stock 150000

Purchases 500000

Closing Stock (200000) (450000)

Gross Profit 200000

Less Other Expenses;

Salaries 60000

Rent 50000 (110000)

Taxable Income/Profit 90,000

= Revenue in this case of corner pharmacy consists of both credit card sales, cash sales and of

course pharmacy benefit scheme that ideally is recognized on the accrual basis for taxation

purposes.

= Corner Pharmacy used stock worth 450000 to generate revenue worth 650000 hence giving a

gross margin of 200000 which represents 30.76%; this, therefore, indicates that cost of sales

Question 2;

According to the accrual basis of accounting, we are going to recognize revenue and expense

only when they are earned and expensed when they occur and not when they are paid.

Corner Pharmacy

Taxable Income

Revenue;

$ $

Cash Sales 300000

Credit Card Sales 150000

Pharmaceutical Benefit Scheme 200000 650000

Cost of Sales;

Opening Stock 150000

Purchases 500000

Closing Stock (200000) (450000)

Gross Profit 200000

Less Other Expenses;

Salaries 60000

Rent 50000 (110000)

Taxable Income/Profit 90,000

= Revenue in this case of corner pharmacy consists of both credit card sales, cash sales and of

course pharmacy benefit scheme that ideally is recognized on the accrual basis for taxation

purposes.

= Corner Pharmacy used stock worth 450000 to generate revenue worth 650000 hence giving a

gross margin of 200000 which represents 30.76%; this, therefore, indicates that cost of sales

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TAXATION LAW

control determines the taxable income of a company as well as tax liability of a company. This

indeed shows that whenever the stock levels are accurately accounted for especially the three of

them, i.e., opening stock, closing stock and purchases there exist fewer possibilities of getting tax

penalties or litigation concerning tax evasion or under-declaration of tax.

= Pharmaceutical Benefits Scheme is believed to be a plan that makes sales on behalf of the

pharmacy hence the amount billed of 200000 is actually what they did as sales on behalf of the

pharmacy. Hence = 25000 + 200000 = 195000 + 30000 meaning that analysis of what was sold

indeed corresponds to stock usage analysis defined. Likewise, if we were to test whether indeed

pharmacy benefit scheme sales compare to receipts indeed it will give us a neutral ground as

follows;

= 25000 + 200000 – 195000 – 30000 = 0, meaning that there is a neutral ground on this.

= We have only considered the credit card sales made and not reimbursement made on this

because going with accruals it is believed that revenue are reported and recognized when they

are earned and not actualized as defined in Australian Tax Office on accruals basis whereby it

depicts that “based on accrual justification the accounting information system expects that all

income earned be termed as part of assessable income for tax purpose whether it is paid or it

will, later on, be paid.’’

= Salaries and Rent according to Australian Tax Office are deemed to be allowable tax

deductions that is why it is claimed by Corner Pharmacy so as to reduce tax deduction and

liability mainly because both of them directly relate to revenue generation in the sense that rent is

a fixed expense that directly relates to business because it is indeed where every sales stock is

sheltered in. On the other hand, the salary is as well an expensive drive that directly relates to

Corner revenue because the staffs are the one who generates revenue and most probably not

machines.

control determines the taxable income of a company as well as tax liability of a company. This

indeed shows that whenever the stock levels are accurately accounted for especially the three of

them, i.e., opening stock, closing stock and purchases there exist fewer possibilities of getting tax

penalties or litigation concerning tax evasion or under-declaration of tax.

= Pharmaceutical Benefits Scheme is believed to be a plan that makes sales on behalf of the

pharmacy hence the amount billed of 200000 is actually what they did as sales on behalf of the

pharmacy. Hence = 25000 + 200000 = 195000 + 30000 meaning that analysis of what was sold

indeed corresponds to stock usage analysis defined. Likewise, if we were to test whether indeed

pharmacy benefit scheme sales compare to receipts indeed it will give us a neutral ground as

follows;

= 25000 + 200000 – 195000 – 30000 = 0, meaning that there is a neutral ground on this.

= We have only considered the credit card sales made and not reimbursement made on this

because going with accruals it is believed that revenue are reported and recognized when they

are earned and not actualized as defined in Australian Tax Office on accruals basis whereby it

depicts that “based on accrual justification the accounting information system expects that all

income earned be termed as part of assessable income for tax purpose whether it is paid or it

will, later on, be paid.’’

= Salaries and Rent according to Australian Tax Office are deemed to be allowable tax

deductions that is why it is claimed by Corner Pharmacy so as to reduce tax deduction and

liability mainly because both of them directly relate to revenue generation in the sense that rent is

a fixed expense that directly relates to business because it is indeed where every sales stock is

sheltered in. On the other hand, the salary is as well an expensive drive that directly relates to

Corner revenue because the staffs are the one who generates revenue and most probably not

machines.

TAXATION LAW

NB; The taxable income amount of $ 90000 earned is what is to be imposed to tax either as a

corner pharmacy itself if it stands as a person, i.e., if registered for tax or as part of income for

the owner of the pharmacy if it is not registered for income tax purposes. All the same, the $

90000 is what indeed is expected to be declared for tax purposes and if possible paid to avoid

extra penalty charges or prosecution if any.

This form of accrual basis ideally leads to the tax aspect of accrual taxation whereby a

company is required to pay and declare tax as long as an invoice is raised without considering

whether the payment will be made or not. This tax accrual is mostly seen to involve the

collection of sales tax while in other scenario self-assessment is indeed conducted by the

company and declare the same to the commissioner of tax.

Question 3;

This case of Inland Revenue Commissioners v. Duke of Westminster (1936) is a platform

indeed that saw into it that taxpayers had their say while seeking the legal way of tax relief. This

case clearly illustrates how a court of the land ruled in favor of the taxpayer.

In a summary way, I wish to explain what transpired in this case of IRC V Westminster by

first stating that the subject matter of this case is the aspect of Tax Avoidance an aspect indeed

that over the years has been the only relieve option to the taxpayers. In this case Duke is seen

ceasing paying his gardeners wage from his post-tax income as he had been doing and instead

coming up with an agreement to be paying him an amount similar to the earn which he used to

earn but of course at a later period which they had agreed upon but not on monthly basis as it

was previously.

This act of treating wage as though it was salary during that year of taxi.e.1936 or instead

of having the local arrangement that led to payment being done at the end of the period gave

Duke a chance to claim the amount agreed upon as an expense that was allowable for tax

NB; The taxable income amount of $ 90000 earned is what is to be imposed to tax either as a

corner pharmacy itself if it stands as a person, i.e., if registered for tax or as part of income for

the owner of the pharmacy if it is not registered for income tax purposes. All the same, the $

90000 is what indeed is expected to be declared for tax purposes and if possible paid to avoid

extra penalty charges or prosecution if any.

This form of accrual basis ideally leads to the tax aspect of accrual taxation whereby a

company is required to pay and declare tax as long as an invoice is raised without considering

whether the payment will be made or not. This tax accrual is mostly seen to involve the

collection of sales tax while in other scenario self-assessment is indeed conducted by the

company and declare the same to the commissioner of tax.

Question 3;

This case of Inland Revenue Commissioners v. Duke of Westminster (1936) is a platform

indeed that saw into it that taxpayers had their say while seeking the legal way of tax relief. This

case clearly illustrates how a court of the land ruled in favor of the taxpayer.

In a summary way, I wish to explain what transpired in this case of IRC V Westminster by

first stating that the subject matter of this case is the aspect of Tax Avoidance an aspect indeed

that over the years has been the only relieve option to the taxpayers. In this case Duke is seen

ceasing paying his gardeners wage from his post-tax income as he had been doing and instead

coming up with an agreement to be paying him an amount similar to the earn which he used to

earn but of course at a later period which they had agreed upon but not on monthly basis as it

was previously.

This act of treating wage as though it was salary during that year of taxi.e.1936 or instead

of having the local arrangement that led to payment being done at the end of the period gave

Duke a chance to claim the amount agreed upon as an expense that was allowable for tax

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TAXATION LAW

deduction during that year of tax. An action that indeed made Duke reduces his taxable liability

through minimization of his income tax and of course the apparent surtax.

The Inland Revenue Commission did not agree with this arrangement since they viewed it

as a plan by Duke to evade paying tax and hence forced to seek justice on this by suing Duke

Westminster on claims that they were deliberately avoiding paying tax thus denying government

from earning its income.

This case was heard and a ruling was made in favor of Duke by judge Lord Tomlin who

ruled that “as long as a man of the land under his efforts can manage his affairs in a manner that

is applicable in the law or preferably under the legal umbrella of local arrangement so as to

loosen the strings attached to tax burden or even disconnect the ties at all, he is protected by the

law not to pay any suggested increased income tax if any, whether the commissioner for inland

revenue is willing or not.

This case indeed opened ways for many Australian taxpayers who used and until today

continue to use the philosophy of tax avoidance to relieve themselves from tax burden via the

introduction of multiple means of reducing them the weight. Although Inland Revenue

Commissioners V Duke Westminster case on tax avoidance over the years have been weakened

and diluted by facts that were brought forward, Australian Tax Office did not hesitate

introduction and application of regulation that saw into it that tax avoidance applies hence

allowing most multination companies and small and medium enterprise companies using this to

relieve themselves tax -burden.

Over the years Australian Tax Office has been losing money out of this act of tax

avoidance since some of the taxpayers never used complex legal structured means of avoiding

tax instead others did it unlawfully to the extent of arguing their case and win while others lost

deduction during that year of tax. An action that indeed made Duke reduces his taxable liability

through minimization of his income tax and of course the apparent surtax.

The Inland Revenue Commission did not agree with this arrangement since they viewed it

as a plan by Duke to evade paying tax and hence forced to seek justice on this by suing Duke

Westminster on claims that they were deliberately avoiding paying tax thus denying government

from earning its income.

This case was heard and a ruling was made in favor of Duke by judge Lord Tomlin who

ruled that “as long as a man of the land under his efforts can manage his affairs in a manner that

is applicable in the law or preferably under the legal umbrella of local arrangement so as to

loosen the strings attached to tax burden or even disconnect the ties at all, he is protected by the

law not to pay any suggested increased income tax if any, whether the commissioner for inland

revenue is willing or not.

This case indeed opened ways for many Australian taxpayers who used and until today

continue to use the philosophy of tax avoidance to relieve themselves from tax burden via the

introduction of multiple means of reducing them the weight. Although Inland Revenue

Commissioners V Duke Westminster case on tax avoidance over the years have been weakened

and diluted by facts that were brought forward, Australian Tax Office did not hesitate

introduction and application of regulation that saw into it that tax avoidance applies hence

allowing most multination companies and small and medium enterprise companies using this to

relieve themselves tax -burden.

Over the years Australian Tax Office has been losing money out of this act of tax

avoidance since some of the taxpayers never used complex legal structured means of avoiding

tax instead others did it unlawfully to the extent of arguing their case and win while others lost

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TAXATION LAW

thus forcing Australian Tax Office to come up with agencies under the law that ensured that this

crisis of unlawful tax avoidance was controlled.

They enhance this control by the introduction of Tax Avoidance Taskforce and

Multinational anti-tax avoidance bodies that ensure that entities involved pay and declare the

right amount of tax as required by the law. It has greatly achieved this by investigating,

analyzing, scrutinizing most of the worst tax avoidance set up the likes of profit shifting with one

core sole purpose which is the need to ensure all taxpayers in Australia trust their tax system and

more so get educated that by paying the correct expected tax of the land one is doing justice to

his nation since the state relies on this tax.

Tax Avoidance indeed has been a challenge in Australia since the users, and appliers of

this legal means of minimizing tax liability went an astray and above what the law expected on

this thus shifting from tax avoidance to now evasion thus affecting the tax man revenue Saad

(2014.Pg 1070.) I therefore wish to say that Tax Avoidance in Australia only favored and until

today just those who apply it as per regulation while those who use it to evade tax are doing it at

their own risk since the task force introduced is always on toes to ensure that the taxman or

rather the government gets its portion of the cake without ado.

Therefore the case of IRC v Duke on tax avoidance has helped those taxpayers who were

legally able to utilize it lawfully and of course denied the tax man portion of its right since some

of the rogue taxpayers went an extra mile and misused the application of the law and instead did

tax evasion an act that is illegal in the eyes of the law.

Question 4;

Australian Tax Office has special consideration and treatment of regular losses resulting

from a business operation and that which result from disposal of the capital investment, i.e.,

capital loss. This same office explains instance in which a business loss occurs to be when total

thus forcing Australian Tax Office to come up with agencies under the law that ensured that this

crisis of unlawful tax avoidance was controlled.

They enhance this control by the introduction of Tax Avoidance Taskforce and

Multinational anti-tax avoidance bodies that ensure that entities involved pay and declare the

right amount of tax as required by the law. It has greatly achieved this by investigating,

analyzing, scrutinizing most of the worst tax avoidance set up the likes of profit shifting with one

core sole purpose which is the need to ensure all taxpayers in Australia trust their tax system and

more so get educated that by paying the correct expected tax of the land one is doing justice to

his nation since the state relies on this tax.

Tax Avoidance indeed has been a challenge in Australia since the users, and appliers of

this legal means of minimizing tax liability went an astray and above what the law expected on

this thus shifting from tax avoidance to now evasion thus affecting the tax man revenue Saad

(2014.Pg 1070.) I therefore wish to say that Tax Avoidance in Australia only favored and until

today just those who apply it as per regulation while those who use it to evade tax are doing it at

their own risk since the task force introduced is always on toes to ensure that the taxman or

rather the government gets its portion of the cake without ado.

Therefore the case of IRC v Duke on tax avoidance has helped those taxpayers who were

legally able to utilize it lawfully and of course denied the tax man portion of its right since some

of the rogue taxpayers went an extra mile and misused the application of the law and instead did

tax evasion an act that is illegal in the eyes of the law.

Question 4;

Australian Tax Office has special consideration and treatment of regular losses resulting

from a business operation and that which result from disposal of the capital investment, i.e.,

capital loss. This same office explains instance in which a business loss occurs to be when total

TAXATION LAW

expenses claimed is more than the revenue generated in that financial year and that capital loss

occurs when the cost of purchasing an asset exceeds the sales residual.

This first scenario of Joseph and Jane is a business loss since they invested in a rental that

they were expecting income only to realize that expenses are more than the rental income it

earned them. From the agreement these two partners are in regarding the business I wish to state

that to me this sounds like a partnership hence an aspect that makes each of them report revenue

and losses as sole individuals and not as a partnership.

Therefore if it is profit/income they earn from the rental Joseph is expected to report 20%

together with his salary as an accountant for tax purpose as Jane says 80% of the same as hers if

she is registered and if not and arm strength exists for Joseph the law allows them to combine the

two cases as income for wife and this precisely what is to take place in case of loss on

apportionment basis only that the whole portion as stipulated in the agreement is to be incurred

by Joseph.

Going with the 100% share of loss Joseph is expected to bear I wish to state that

Australian Tax Office on losses for business allows Joseph to carry forward the $40000 loss as a

set off deduction for the future income that will be earned by the rental facility for tax purposes.

Thus it is expected that in future when the rental income will have a tax to be paid part of this is

to be used to relieve the burden Woellner, Barkoczy, Murphy, Evans and Pinto (2010.Pg 14.)

If Joseph and Jane decide to dispose this asset any capital gain or loss that result from this

disposal is similarly expected to be treated similar to the injuries or gain earned but this time

around as capital gain tax. The capital gain is added to each of the individual income as per the

apportionment agreement made similarly to the loss whereby according to Australian Tax Office

the capital loss incurred should be carried forward until when they will be a capital gain to set off

these.

expenses claimed is more than the revenue generated in that financial year and that capital loss

occurs when the cost of purchasing an asset exceeds the sales residual.

This first scenario of Joseph and Jane is a business loss since they invested in a rental that

they were expecting income only to realize that expenses are more than the rental income it

earned them. From the agreement these two partners are in regarding the business I wish to state

that to me this sounds like a partnership hence an aspect that makes each of them report revenue

and losses as sole individuals and not as a partnership.

Therefore if it is profit/income they earn from the rental Joseph is expected to report 20%

together with his salary as an accountant for tax purpose as Jane says 80% of the same as hers if

she is registered and if not and arm strength exists for Joseph the law allows them to combine the

two cases as income for wife and this precisely what is to take place in case of loss on

apportionment basis only that the whole portion as stipulated in the agreement is to be incurred

by Joseph.

Going with the 100% share of loss Joseph is expected to bear I wish to state that

Australian Tax Office on losses for business allows Joseph to carry forward the $40000 loss as a

set off deduction for the future income that will be earned by the rental facility for tax purposes.

Thus it is expected that in future when the rental income will have a tax to be paid part of this is

to be used to relieve the burden Woellner, Barkoczy, Murphy, Evans and Pinto (2010.Pg 14.)

If Joseph and Jane decide to dispose this asset any capital gain or loss that result from this

disposal is similarly expected to be treated similar to the injuries or gain earned but this time

around as capital gain tax. The capital gain is added to each of the individual income as per the

apportionment agreement made similarly to the loss whereby according to Australian Tax Office

the capital loss incurred should be carried forward until when they will be a capital gain to set off

these.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TAXATION LAW

However, all the above losses whether business loss or capital loss it is expected to be

declared in that year of tax by Joseph and Jane tax agent in a loss schedule document introduced

under the instruction of losses schedule 2018 for accountability, traceability, documentation,

transparency and of course for Australian Tax Office books and system formality. This schedule

is the only document that will support any claim of future loss set off when they are deemed

redeemable merely because they take place on next date.

However, all the above losses whether business loss or capital loss it is expected to be

declared in that year of tax by Joseph and Jane tax agent in a loss schedule document introduced

under the instruction of losses schedule 2018 for accountability, traceability, documentation,

transparency and of course for Australian Tax Office books and system formality. This schedule

is the only document that will support any claim of future loss set off when they are deemed

redeemable merely because they take place on next date.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TAXATION LAW

References;

Saad, N., 2014. Tax knowledge, tax complexity and tax compliance: Taxpayers’ view. Procedia-

Social and Behavioral Sciences, 109, pp.1069-1075.

Woellner, R.H., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2010. Australian taxation

law. CCH Australia.

References;

Saad, N., 2014. Tax knowledge, tax complexity and tax compliance: Taxpayers’ view. Procedia-

Social and Behavioral Sciences, 109, pp.1069-1075.

Woellner, R.H., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2010. Australian taxation

law. CCH Australia.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.