Taxation Law Report: Australian Taxation, Capital Gains and Allowances

VerifiedAdded on 2021/02/21

|9

|2395

|113

Report

AI Summary

This report provides a comprehensive analysis of Australian taxation law, focusing on capital gains tax (CGT) and capital allowances. The report begins with an introduction to taxation law in Australia, highlighting the role of the Australian Taxation Office (ATO) and the purpose of generating revenue for public needs. It then addresses two key questions. Question 1 examines the CGT implications for an Australian resident, Jasmine, who is selling various assets upon retirement, including a family home, a car, a small cleaning business, furniture, and paintings. The analysis covers relevant exemptions and calculations for each asset. Question 2 delves into the taxation aspects of a CNC machine owned by a motor vehicle parts manufacturing company. This section focuses on calculating the cost of the asset, including purchase price, travel expenses, and installation costs, and determining the start time for capital allowances. The report concludes by summarizing key findings and emphasizing the importance of understanding taxation policies for accurate income tax return filing and claiming capital allowances. The report references various books and journals for its analysis.

Taxation Law

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

QUESTION 2...................................................................................................................................3

ISSUE..........................................................................................................................................3

LAW AND APPLICATION FOR COST...................................................................................3

LAW AND APPLICATION FOR TIME CALCULATION.......................................................4

CONCLUSION REGARDING THE EXACT START TIME OF HOLDING CNC AND

TOTAL COST OF AN ASSET...................................................................................................5

COCLUSION...................................................................................................................................5

REFERENCE...................................................................................................................................6

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

QUESTION 2...................................................................................................................................3

ISSUE..........................................................................................................................................3

LAW AND APPLICATION FOR COST...................................................................................3

LAW AND APPLICATION FOR TIME CALCULATION.......................................................4

CONCLUSION REGARDING THE EXACT START TIME OF HOLDING CNC AND

TOTAL COST OF AN ASSET...................................................................................................5

COCLUSION...................................................................................................................................5

REFERENCE...................................................................................................................................6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Taxation law is defined as rules, policies and laws that oversee the tax process while

involving the charges on estates, transactions and property income. In Australia the Australian

Taxation Office is an Australian statutory agency and the principal revenue collection body for

the government. Taxation law helps in imposing amount of tax on multi-pal transactions for sale

and purchase of goods and services (Berns, 2018). It is charged by the government on the income

of an individual, corporate, trust as well as transfer of gifts. The objective in assessing tax is to

generate revenue that will be used for public needs. In this project report imposition of capital

gain or loss will be elaborated for some capital transactions. This report also includes details

regarding rules and regulations regarding capital allowances.

QUESTION 1

Capital gain tax means the amount of tax imposed on the assets that is held other then

inventory for more then a year and selling price of which is more then purchase price. In

Australia Capital Gain Tax (CGT) was introduced on 20 September 1985. Capital gain or loss on

the assets will be applied only when the assets are acquired or owned after the date of CGT.

Capital gain or loss should be reported in the income tax return and it is an part of income tax.

The amount of capital gain is applicable on various assets that is held for long run and then sold

in some profits (Delfabbro and King, 2012).

In the present case Jasmine is an Australian resident who is 65 years old. She is selling

her Australian assets as she is retiring from business. The block of assets includes different

capital assets and application of Capital Taxation law will differ for them. Tax implication on

selling of following assets are as follows-

Capital gain in relation to family home

Jasmine's house was purchased in 1981 for $40000 and now worth $650000. this was her

main residence since she purchased the house. As per Australian capital gain taxation laws

“Main Residence” is generally exempt from imposition of taxation and to get exemption the

property must be used for living as it must not be a vacant land. An individual will be entitled for

a full main residence exemption if the residential dwelling has fulfilled the following criteria-

the property has been home for you and other dependants of yours for the whole period of

ownership.

1

Taxation law is defined as rules, policies and laws that oversee the tax process while

involving the charges on estates, transactions and property income. In Australia the Australian

Taxation Office is an Australian statutory agency and the principal revenue collection body for

the government. Taxation law helps in imposing amount of tax on multi-pal transactions for sale

and purchase of goods and services (Berns, 2018). It is charged by the government on the income

of an individual, corporate, trust as well as transfer of gifts. The objective in assessing tax is to

generate revenue that will be used for public needs. In this project report imposition of capital

gain or loss will be elaborated for some capital transactions. This report also includes details

regarding rules and regulations regarding capital allowances.

QUESTION 1

Capital gain tax means the amount of tax imposed on the assets that is held other then

inventory for more then a year and selling price of which is more then purchase price. In

Australia Capital Gain Tax (CGT) was introduced on 20 September 1985. Capital gain or loss on

the assets will be applied only when the assets are acquired or owned after the date of CGT.

Capital gain or loss should be reported in the income tax return and it is an part of income tax.

The amount of capital gain is applicable on various assets that is held for long run and then sold

in some profits (Delfabbro and King, 2012).

In the present case Jasmine is an Australian resident who is 65 years old. She is selling

her Australian assets as she is retiring from business. The block of assets includes different

capital assets and application of Capital Taxation law will differ for them. Tax implication on

selling of following assets are as follows-

Capital gain in relation to family home

Jasmine's house was purchased in 1981 for $40000 and now worth $650000. this was her

main residence since she purchased the house. As per Australian capital gain taxation laws

“Main Residence” is generally exempt from imposition of taxation and to get exemption the

property must be used for living as it must not be a vacant land. An individual will be entitled for

a full main residence exemption if the residential dwelling has fulfilled the following criteria-

the property has been home for you and other dependants of yours for the whole period of

ownership.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Property has not been used to produce assessable income that is, not used for business

purpose or rented out (Capital gain for residential house, 2019).

Property is on land of two hectares or less.

From the above criteria of full exemption of residential dwelling it can be said that

residential property of Jasmine is not liable to capital gain.

Capital gain or loss made for the car

Jasmine purchased a car in 2011 for $31000 and now worth around $10000. Taxation law

is applied on all the capital assets otherwise they are granted exemption. As per Capital gain

taxation law cars and other small vehicles (small being carrying capacity less the 1 tonne and less

the 9 passengers) are exempt from tax implications. Car purchased by Jasmine will be assumed

to be fulfilling the criteria for exemption and no amount of tax will be imposed on sale for asset

in form of capital gain or loss (Lignier and Evans, 2012).

Capital gain in relation to sale of business

Jasmine commenced her small cleaning business and now at the time of retirement she

founds a buyer for business in $125000. The sale price includes $65000 for all the business

equipment which cost $75000 and goodwill of $60000. Capital gain tax consequences have been

available since 21 September 1999. When a small business is operated for 15 years and more and

sold due to retirement by an individual who is more then 55 years of age. This all criteria puts

Jasmine into another claim for exemption for capital gain on sale of a small house. As duration

of conducting business is not given and it will be assumed to be 15 years or more. When this

assumption is not taken then implication of capital gain tax will be of 50% active deduction. In

this capital gains are reduced by 50% for assets used actively in business. The normal 50%

deduction for assets held for at-lest one year will also be applicable. Overall 75% deduction will

be allowed on the amount of capital gain (Martin and Rice, 2012).

Capital gain in relation to selling of furniture

Jasmine is selling her furniture for $5000 and no single item offered for sale cost more

then $2000. As per capital gain taxation rules personal assets are CGT assets and mainly used for

personal purpose. Boats, furniture, electrical goods and household items are mentioned as

personal goods. Any personal assets acquired for less the $10000 will be disregarded for CGT

purposes. Main residence, car and motorbike will not be termed as personal assets. The

exemption on personal assets will be applicable only if the acquired set is for $10000 or less. It

2

purpose or rented out (Capital gain for residential house, 2019).

Property is on land of two hectares or less.

From the above criteria of full exemption of residential dwelling it can be said that

residential property of Jasmine is not liable to capital gain.

Capital gain or loss made for the car

Jasmine purchased a car in 2011 for $31000 and now worth around $10000. Taxation law

is applied on all the capital assets otherwise they are granted exemption. As per Capital gain

taxation law cars and other small vehicles (small being carrying capacity less the 1 tonne and less

the 9 passengers) are exempt from tax implications. Car purchased by Jasmine will be assumed

to be fulfilling the criteria for exemption and no amount of tax will be imposed on sale for asset

in form of capital gain or loss (Lignier and Evans, 2012).

Capital gain in relation to sale of business

Jasmine commenced her small cleaning business and now at the time of retirement she

founds a buyer for business in $125000. The sale price includes $65000 for all the business

equipment which cost $75000 and goodwill of $60000. Capital gain tax consequences have been

available since 21 September 1999. When a small business is operated for 15 years and more and

sold due to retirement by an individual who is more then 55 years of age. This all criteria puts

Jasmine into another claim for exemption for capital gain on sale of a small house. As duration

of conducting business is not given and it will be assumed to be 15 years or more. When this

assumption is not taken then implication of capital gain tax will be of 50% active deduction. In

this capital gains are reduced by 50% for assets used actively in business. The normal 50%

deduction for assets held for at-lest one year will also be applicable. Overall 75% deduction will

be allowed on the amount of capital gain (Martin and Rice, 2012).

Capital gain in relation to selling of furniture

Jasmine is selling her furniture for $5000 and no single item offered for sale cost more

then $2000. As per capital gain taxation rules personal assets are CGT assets and mainly used for

personal purpose. Boats, furniture, electrical goods and household items are mentioned as

personal goods. Any personal assets acquired for less the $10000 will be disregarded for CGT

purposes. Main residence, car and motorbike will not be termed as personal assets. The

exemption on personal assets will be applicable only if the acquired set is for $10000 or less. It

2

will be assumed that the value of set is as per the exemption limit and Jasmine will be liable to

get exemption on sale of furniture (Capital gain for furniture, 2019).

Capital gain in relation to selling of paintings

Jasmine has several paintings and now selling them all for $35000. All her paintings were

purchased in second hand shop or markets and no single painting cost more than $500. Among

the all one painting is purchased from artist for $1000 and sold for $5000. As per implications of

the Capital gain taxations paintings are included in collectables and certain exemption is granted

for this. When collectables (paintings) acquired for $500 or less, or worth $500 or less when

acquired then they will be exempt for capital gain.

Paintings purchased by Jasmine is not more then $500 and they all fall under the

exemption criteria. A painting that is purchased from artist for $1000 will be imposed capital

gain. The amount of capital gain will be difference in selling price and purchase price i.e. $5000

- $1000= $4000.

In the process of selling all the assets variety of exemptions will be availed by Jasmine

and tax will be applied only on $4000 for paintings. When loss incurred in the process of selling

paintings then it can be set off against profits from collectables or can be carry forward to new

year (McGregor-Lowndes, 2014).

QUESTION 2

ISSUE

John owns a motor vehicle part and accessories manufacturing company. The business

produces certified BMW parts. A computer numerical control (CNC) machine was imported by

John from Germany on November 2014 for $300000. John visited CNC factory in Germany to

inspect the machinery and this was the only reason for his visit to Germany. This visit cost him

$12000. This CNC machine was installed on 15 January at a cost of $25000. After installation it

was found that additional guiding will make it more effective. On 1 February this guiding rod

was installed for $5000. Here cost of the machinery and time from which assets will be declined

needs to be calculated as per taxation law (Mayo, 2015).

LAW AND APPLICATION FOR COST

Accounting standards applicable on property, plant and equipment specifies some

elements that forms cost of an assets. These elements includes-

3

get exemption on sale of furniture (Capital gain for furniture, 2019).

Capital gain in relation to selling of paintings

Jasmine has several paintings and now selling them all for $35000. All her paintings were

purchased in second hand shop or markets and no single painting cost more than $500. Among

the all one painting is purchased from artist for $1000 and sold for $5000. As per implications of

the Capital gain taxations paintings are included in collectables and certain exemption is granted

for this. When collectables (paintings) acquired for $500 or less, or worth $500 or less when

acquired then they will be exempt for capital gain.

Paintings purchased by Jasmine is not more then $500 and they all fall under the

exemption criteria. A painting that is purchased from artist for $1000 will be imposed capital

gain. The amount of capital gain will be difference in selling price and purchase price i.e. $5000

- $1000= $4000.

In the process of selling all the assets variety of exemptions will be availed by Jasmine

and tax will be applied only on $4000 for paintings. When loss incurred in the process of selling

paintings then it can be set off against profits from collectables or can be carry forward to new

year (McGregor-Lowndes, 2014).

QUESTION 2

ISSUE

John owns a motor vehicle part and accessories manufacturing company. The business

produces certified BMW parts. A computer numerical control (CNC) machine was imported by

John from Germany on November 2014 for $300000. John visited CNC factory in Germany to

inspect the machinery and this was the only reason for his visit to Germany. This visit cost him

$12000. This CNC machine was installed on 15 January at a cost of $25000. After installation it

was found that additional guiding will make it more effective. On 1 February this guiding rod

was installed for $5000. Here cost of the machinery and time from which assets will be declined

needs to be calculated as per taxation law (Mayo, 2015).

LAW AND APPLICATION FOR COST

Accounting standards applicable on property, plant and equipment specifies some

elements that forms cost of an assets. These elements includes-

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

purchase price, including import duties and non-refundable purchase taxes after

deducting trade discount this is termed as first element of the assets cost.

Any cost that is incurred and attributable to the asset for bringing it to the location and

required condition necessary for installation. All the other expenses then purchase price

of an asset will form part of second element of assets cost (Thuronyi and Brooks, 2016).

Initial cost of dismantling and removing the item and restoring the site which is located.

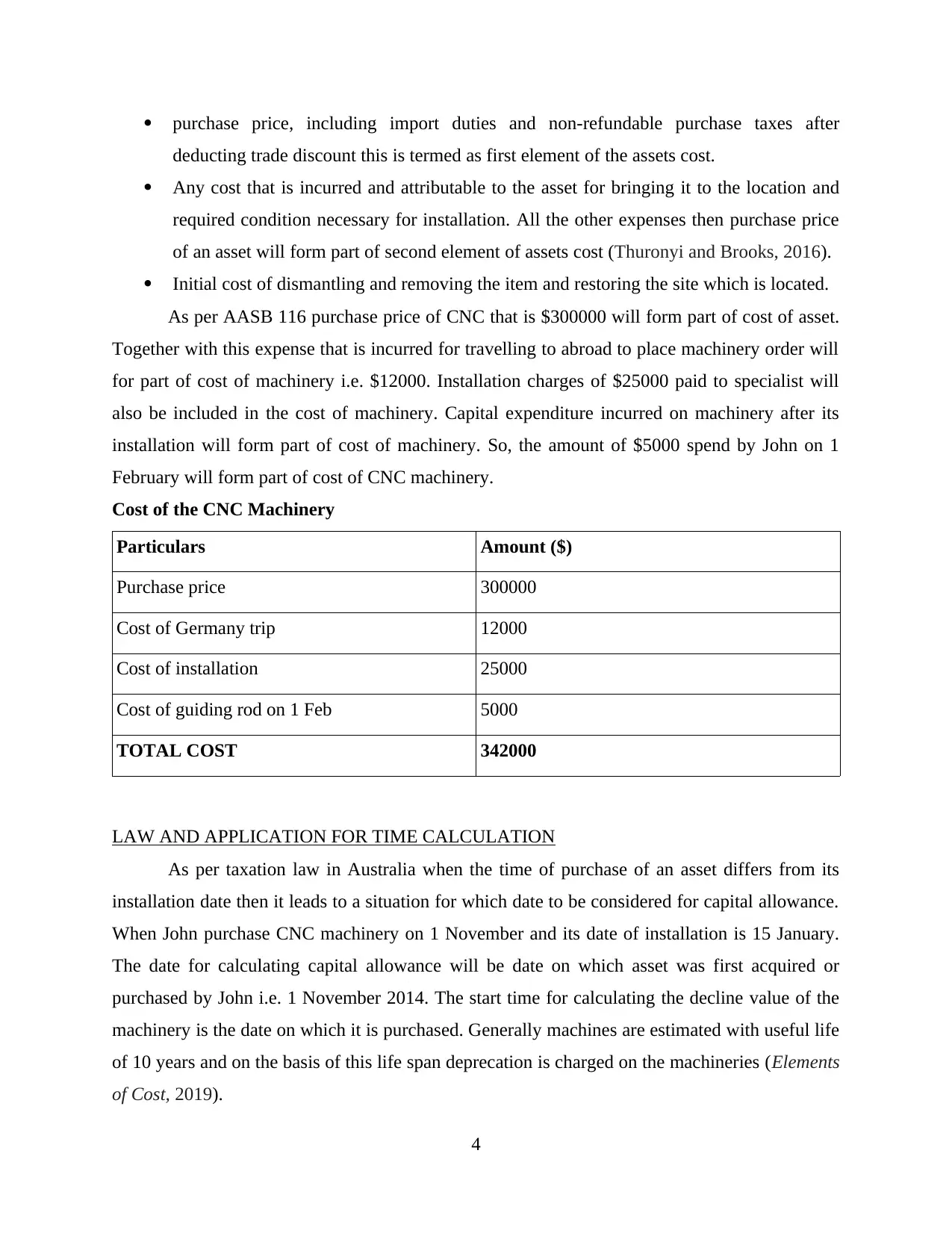

As per AASB 116 purchase price of CNC that is $300000 will form part of cost of asset.

Together with this expense that is incurred for travelling to abroad to place machinery order will

for part of cost of machinery i.e. $12000. Installation charges of $25000 paid to specialist will

also be included in the cost of machinery. Capital expenditure incurred on machinery after its

installation will form part of cost of machinery. So, the amount of $5000 spend by John on 1

February will form part of cost of CNC machinery.

Cost of the CNC Machinery

Particulars Amount ($)

Purchase price 300000

Cost of Germany trip 12000

Cost of installation 25000

Cost of guiding rod on 1 Feb 5000

TOTAL COST 342000

LAW AND APPLICATION FOR TIME CALCULATION

As per taxation law in Australia when the time of purchase of an asset differs from its

installation date then it leads to a situation for which date to be considered for capital allowance.

When John purchase CNC machinery on 1 November and its date of installation is 15 January.

The date for calculating capital allowance will be date on which asset was first acquired or

purchased by John i.e. 1 November 2014. The start time for calculating the decline value of the

machinery is the date on which it is purchased. Generally machines are estimated with useful life

of 10 years and on the basis of this life span deprecation is charged on the machineries (Elements

of Cost, 2019).

4

deducting trade discount this is termed as first element of the assets cost.

Any cost that is incurred and attributable to the asset for bringing it to the location and

required condition necessary for installation. All the other expenses then purchase price

of an asset will form part of second element of assets cost (Thuronyi and Brooks, 2016).

Initial cost of dismantling and removing the item and restoring the site which is located.

As per AASB 116 purchase price of CNC that is $300000 will form part of cost of asset.

Together with this expense that is incurred for travelling to abroad to place machinery order will

for part of cost of machinery i.e. $12000. Installation charges of $25000 paid to specialist will

also be included in the cost of machinery. Capital expenditure incurred on machinery after its

installation will form part of cost of machinery. So, the amount of $5000 spend by John on 1

February will form part of cost of CNC machinery.

Cost of the CNC Machinery

Particulars Amount ($)

Purchase price 300000

Cost of Germany trip 12000

Cost of installation 25000

Cost of guiding rod on 1 Feb 5000

TOTAL COST 342000

LAW AND APPLICATION FOR TIME CALCULATION

As per taxation law in Australia when the time of purchase of an asset differs from its

installation date then it leads to a situation for which date to be considered for capital allowance.

When John purchase CNC machinery on 1 November and its date of installation is 15 January.

The date for calculating capital allowance will be date on which asset was first acquired or

purchased by John i.e. 1 November 2014. The start time for calculating the decline value of the

machinery is the date on which it is purchased. Generally machines are estimated with useful life

of 10 years and on the basis of this life span deprecation is charged on the machineries (Elements

of Cost, 2019).

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONCLUSION REGARDING THE EXACT START TIME OF HOLDING CNC AND

TOTAL COST OF AN ASSET

The exact time for calculating period of holding the CNC machinery is the first day when

asset was acquired. This will be calculated from the first day when asset was first held and

capital allowance for the year 2014 and 2015 will be granted for 5 months from November to

march in that financial year. The total cost that will be taken for capital allowance will be

$337000 at initial stage. After incurring expense of $5000 for enhancing productivity this will

also be added to the cost of CNC and capital allowance will be allowed on the remaining life of

the asset (Wilkins, 2015).

To claim for capital allowance the asset must be owned by individual or business

claiming that allowances. Only the legal owner of asset will be entitled for capital allowance and

deprecation. When the asset is used partially in business or partially in some other activities then

business will be entitled to claim only partial deduction as depreciation.

COCLUSION

From the above project report it has been concluded that government of the country

imposes different taxation policies that helps in generating taxes. Capital tax taxation is one of

the primary source that is used to collect amount of tax from sale and purchase of capital assets.

All the transactions for capital assets must be done with implications of rules and policies of

capital gain taxation. Cost of an asset and time of its acquisition is important for claiming capital

allowances. For calculating cost of asset elements of cost defined by Australian Taxation

Officers must be considered. Estimation of capital gain or loss amount is important for filling

income tax return in correct and fair manner.

5

TOTAL COST OF AN ASSET

The exact time for calculating period of holding the CNC machinery is the first day when

asset was acquired. This will be calculated from the first day when asset was first held and

capital allowance for the year 2014 and 2015 will be granted for 5 months from November to

march in that financial year. The total cost that will be taken for capital allowance will be

$337000 at initial stage. After incurring expense of $5000 for enhancing productivity this will

also be added to the cost of CNC and capital allowance will be allowed on the remaining life of

the asset (Wilkins, 2015).

To claim for capital allowance the asset must be owned by individual or business

claiming that allowances. Only the legal owner of asset will be entitled for capital allowance and

deprecation. When the asset is used partially in business or partially in some other activities then

business will be entitled to claim only partial deduction as depreciation.

COCLUSION

From the above project report it has been concluded that government of the country

imposes different taxation policies that helps in generating taxes. Capital tax taxation is one of

the primary source that is used to collect amount of tax from sale and purchase of capital assets.

All the transactions for capital assets must be done with implications of rules and policies of

capital gain taxation. Cost of an asset and time of its acquisition is important for claiming capital

allowances. For calculating cost of asset elements of cost defined by Australian Taxation

Officers must be considered. Estimation of capital gain or loss amount is important for filling

income tax return in correct and fair manner.

5

REFERENCE

Books and Journal

Berns, S., 2018. Women Going Backwards: Law and change in a family unfriendly society.

Routledge.

Delfabbro, P. and King, D., 2012. Gambling in Australia: Experiences, problems, research and

policy. Addiction. 107(9). pp.1556-1561.

Lignier, P. and Evans, C., 2012, August. The rise and rise of tax compliance costs for the small

business sector in Australia. In Australian Tax Forum (Vol. 27, No. 3, pp. 615-672).

Martin, N. J. and Rice, J. L., 2012. Developing renewable energy supply in Queensland,

Australia: A study of the barriers, targets, policies and actions. Renewable Energy. 44.

pp.119-127.

Mayo, W., 2015. Policy Forum: Resource Rent Taxation--Experiences from Australia. Canadian

Tax Journal/Revue Fiscale Canadienne. 63(2).

McGregor-Lowndes, M., 2014. The not for profit sector in Australia: Fact sheet. ACPNS Current

Issues Information Sheet 2014/4.

Thuronyi, V. and Brooks, K., 2016. Comparative tax law. Kluwer Law International BV.

Wilkins, R., 2015. Measuring income inequality in Australia. Australian Economic Review.

48(1). pp.93-102.

Online

Capital gain for residential house. 2019. [Online]. Available through:

<https://www.ato.gov.au/General/Capital-gains-tax/Your-home-and-other-real-estate/>

Capital gain for furniture. 2019. [Online]. Available through:

<https://www.ato.gov.au/general/capital-gains-tax/cgt-assets-and-exemptions/>

Elements of Cost. 2019. [Online]. Available through:

<https://www.ato.gov.au/General/Capital-gains-tax/Working-out-your-capital-gain-or-

loss/Cost-base/Elements-of-the-cost-base-and-reduced-cost-base/>

6

Books and Journal

Berns, S., 2018. Women Going Backwards: Law and change in a family unfriendly society.

Routledge.

Delfabbro, P. and King, D., 2012. Gambling in Australia: Experiences, problems, research and

policy. Addiction. 107(9). pp.1556-1561.

Lignier, P. and Evans, C., 2012, August. The rise and rise of tax compliance costs for the small

business sector in Australia. In Australian Tax Forum (Vol. 27, No. 3, pp. 615-672).

Martin, N. J. and Rice, J. L., 2012. Developing renewable energy supply in Queensland,

Australia: A study of the barriers, targets, policies and actions. Renewable Energy. 44.

pp.119-127.

Mayo, W., 2015. Policy Forum: Resource Rent Taxation--Experiences from Australia. Canadian

Tax Journal/Revue Fiscale Canadienne. 63(2).

McGregor-Lowndes, M., 2014. The not for profit sector in Australia: Fact sheet. ACPNS Current

Issues Information Sheet 2014/4.

Thuronyi, V. and Brooks, K., 2016. Comparative tax law. Kluwer Law International BV.

Wilkins, R., 2015. Measuring income inequality in Australia. Australian Economic Review.

48(1). pp.93-102.

Online

Capital gain for residential house. 2019. [Online]. Available through:

<https://www.ato.gov.au/General/Capital-gains-tax/Your-home-and-other-real-estate/>

Capital gain for furniture. 2019. [Online]. Available through:

<https://www.ato.gov.au/general/capital-gains-tax/cgt-assets-and-exemptions/>

Elements of Cost. 2019. [Online]. Available through:

<https://www.ato.gov.au/General/Capital-gains-tax/Working-out-your-capital-gain-or-

loss/Cost-base/Elements-of-the-cost-base-and-reduced-cost-base/>

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.