Taxation Homework Assignment

VerifiedAdded on 2019/10/30

|13

|2100

|145

Homework Assignment

AI Summary

This homework assignment presents a comprehensive solution to a taxation problem. It addresses four key questions related to Australian tax law, including the calculation of taxable income, the allowance of GST input credits for advertising expenses, the calculation of foreign tax offsets, and the determination of allowable deductions. The solution meticulously details the relevant sections of the Income Tax Assessment Act 1997 and provides step-by-step calculations, tables, and explanations to clarify the application of tax laws to specific scenarios. The assignment demonstrates a strong understanding of Australian tax principles and their practical application, making it a valuable resource for students studying taxation.

Running head: TAX

Tax

Name of the Student:

Name of the University:

Authors Note:

Tax

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAX

Table of Contents

Answer to Question 1:................................................................................................................2

Answer to Question 2:................................................................................................................3

Answer to Question 3.................................................................................................................5

Answer to Question 4...............................................................................................................11

Reference..................................................................................................................................13

Table of Contents

Answer to Question 1:................................................................................................................2

Answer to Question 2:................................................................................................................3

Answer to Question 3.................................................................................................................5

Answer to Question 4...............................................................................................................11

Reference..................................................................................................................................13

2TAX

Answer to Question 1:

The section 4-15 of the Income Tax Assessment Act states that the taxable income is

calculated by deducting allowable deductions from the assessable income. The Section 8-

1(1) of the ITAA 1997 provides that a person who pay tax have the right to claim for

deduction against the expenses which are incurred for the purpose of:

i. Producing an assessable income;

ii. For carrying on business activity.

Therefore,

1. The expenditure which is incurred for moving a machinery will not be considered as

deduction which is stated under section 8-1 of the ITAA 1997.

2. The cost of revaluation of any asset cannot be granted as a deductible expense

according to Section 8-1 of the ITAA 1997.

3. If any such expenditure occurs which is incurred in relation to legal proceedings to

compete against the company’s winding up then such expenses will be allowed as

deductible expenses as stated in section 8-1 of the Income Tax Assessment Act 1997.

4. In order to make business income, any expenditure which is experienced by lawyer

must be taken as deductible expenditure which is permissible under section 8-1 of the

Income Tax Assessment Act 19971.

1 Forsyth, Peter, Larry Dwyer, Ray Spurr, and Tien Pham. "The impacts of Australia's departure tax: Tourism

versus the economy?." Tourism Management 40 (2014): 126-136.

Answer to Question 1:

The section 4-15 of the Income Tax Assessment Act states that the taxable income is

calculated by deducting allowable deductions from the assessable income. The Section 8-

1(1) of the ITAA 1997 provides that a person who pay tax have the right to claim for

deduction against the expenses which are incurred for the purpose of:

i. Producing an assessable income;

ii. For carrying on business activity.

Therefore,

1. The expenditure which is incurred for moving a machinery will not be considered as

deduction which is stated under section 8-1 of the ITAA 1997.

2. The cost of revaluation of any asset cannot be granted as a deductible expense

according to Section 8-1 of the ITAA 1997.

3. If any such expenditure occurs which is incurred in relation to legal proceedings to

compete against the company’s winding up then such expenses will be allowed as

deductible expenses as stated in section 8-1 of the Income Tax Assessment Act 1997.

4. In order to make business income, any expenditure which is experienced by lawyer

must be taken as deductible expenditure which is permissible under section 8-1 of the

Income Tax Assessment Act 19971.

1 Forsyth, Peter, Larry Dwyer, Ray Spurr, and Tien Pham. "The impacts of Australia's departure tax: Tourism

versus the economy?." Tourism Management 40 (2014): 126-136.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAX

Answer to Question 2:

If the required proof in connection to the purchase made by the company is preserved

properly then only the GST input with respect to such purchase will be allowed. Any business

or organization which is functioning for the purpose of earing income is entitled to claim

input credit for the purchase of materials or assets in case of payments that are made

including GST.

Issue:

Big Bank limited spent an amount of $1,650,000 which is inclusive of GST for

advertisement purpose. Now the bank wants to know that whether the amount which is spent

for advertisement purpose including GST will be allowable as input credit or not.

Rules:

As Chapter 2 of the GST Act conveys that any expenses or cost incurred by the

organization or any business during the regular or normal course of business will be

permitted to take input tax credit only if such expenditure is inclusive of GST.

Application:

Big Bank Limited is a well reputed company having more than 50 branches all over

the country. The company mainly provides the people finance related services. The

headquarters of the company is situated on a 10 storey building. During the recent period, Big

Bank Limited have released some of its new products in the market which are home contents

and insurance policy apart from giving loans and deposits to the people of the country over

Answer to Question 2:

If the required proof in connection to the purchase made by the company is preserved

properly then only the GST input with respect to such purchase will be allowed. Any business

or organization which is functioning for the purpose of earing income is entitled to claim

input credit for the purchase of materials or assets in case of payments that are made

including GST.

Issue:

Big Bank limited spent an amount of $1,650,000 which is inclusive of GST for

advertisement purpose. Now the bank wants to know that whether the amount which is spent

for advertisement purpose including GST will be allowable as input credit or not.

Rules:

As Chapter 2 of the GST Act conveys that any expenses or cost incurred by the

organization or any business during the regular or normal course of business will be

permitted to take input tax credit only if such expenditure is inclusive of GST.

Application:

Big Bank Limited is a well reputed company having more than 50 branches all over

the country. The company mainly provides the people finance related services. The

headquarters of the company is situated on a 10 storey building. During the recent period, Big

Bank Limited have released some of its new products in the market which are home contents

and insurance policy apart from giving loans and deposits to the people of the country over

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAX

the years2. For the purpose of advertisement, the bank had already kept aside separately an

amount of $1,650,000. Amongst this, an amount of $550,000 was held by the company for

the purpose of advertising its home and insurance products and the rest of which was kept

separately for advertising its other products and services. All the expenses made by the

company are inclusive of GST

Hence it was found that an amount of $1,100,000 was incurred by the company for

the purpose of promoting the company’s regular and existing products and services.

Moreover the majority of the revenue of the company comes from this segment and thus it is

an essential segment for the company. Whereas on the other hand, the newly launched

segment that is insurance policy and home content is yet to contribute towards the revenue of

the company. Since this segment is yet to contribute towards company’s income generation

thus the amount of $550,000 incurred for the promotion of insurance and home content will

be considered as capital expenditure.

Conclusion:

Thus after reviewing the above discussion it can be realised that the amount of

$1,100,000 will be permitted to receive input credit as it largely contribute toward company’s

income generation. While the rest $550,000 will not be entirely disallowed to receive input

credit due to the reason that 2% of such expense contribute towards the company’s revenue

generation.

2 McLachlan, Rosalie. "Deep and Persistent Disadvantage in Australia-Productivity Commission Staff Working

Paper." (2013).

the years2. For the purpose of advertisement, the bank had already kept aside separately an

amount of $1,650,000. Amongst this, an amount of $550,000 was held by the company for

the purpose of advertising its home and insurance products and the rest of which was kept

separately for advertising its other products and services. All the expenses made by the

company are inclusive of GST

Hence it was found that an amount of $1,100,000 was incurred by the company for

the purpose of promoting the company’s regular and existing products and services.

Moreover the majority of the revenue of the company comes from this segment and thus it is

an essential segment for the company. Whereas on the other hand, the newly launched

segment that is insurance policy and home content is yet to contribute towards the revenue of

the company. Since this segment is yet to contribute towards company’s income generation

thus the amount of $550,000 incurred for the promotion of insurance and home content will

be considered as capital expenditure.

Conclusion:

Thus after reviewing the above discussion it can be realised that the amount of

$1,100,000 will be permitted to receive input credit as it largely contribute toward company’s

income generation. While the rest $550,000 will not be entirely disallowed to receive input

credit due to the reason that 2% of such expense contribute towards the company’s revenue

generation.

2 McLachlan, Rosalie. "Deep and Persistent Disadvantage in Australia-Productivity Commission Staff Working

Paper." (2013).

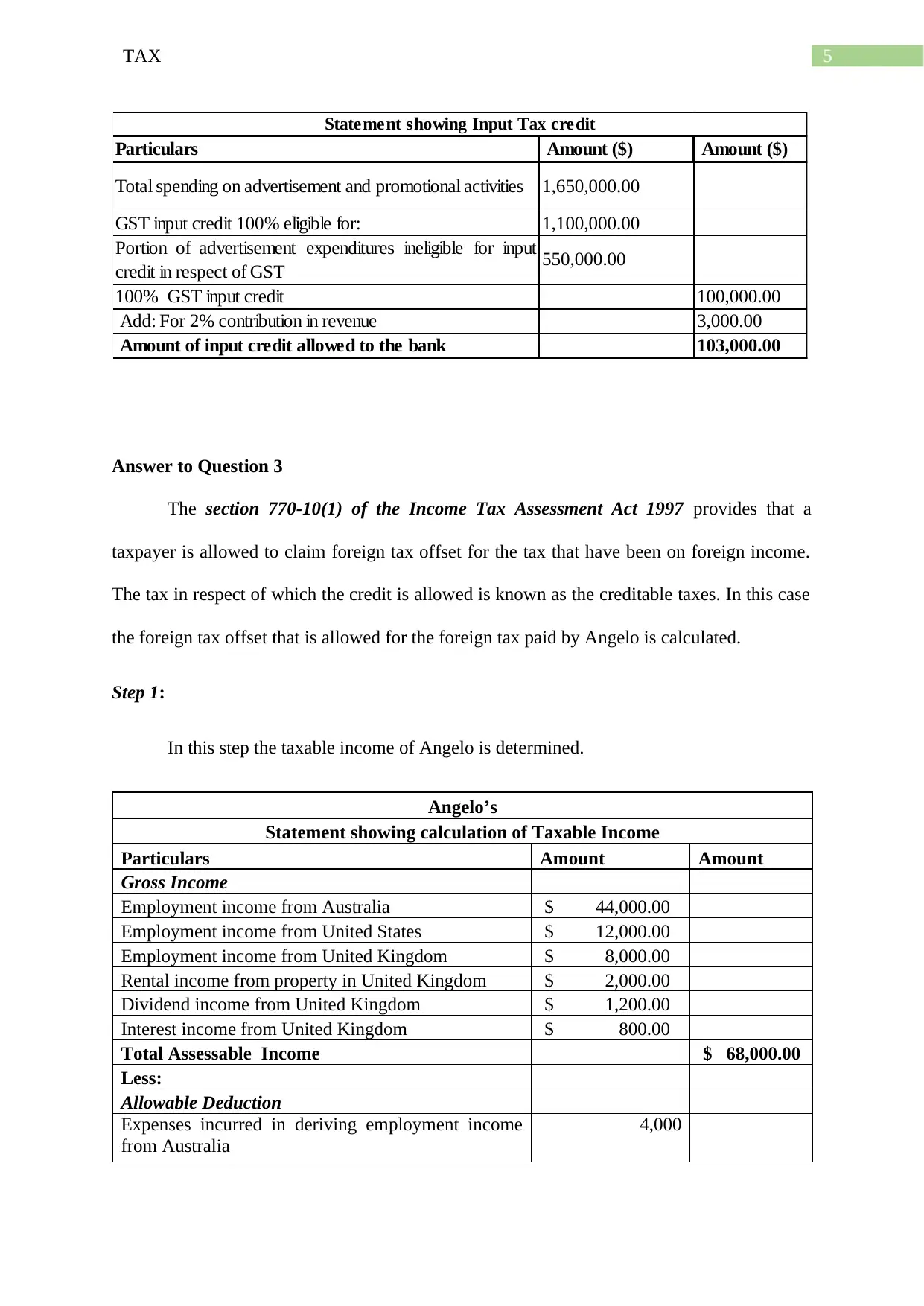

5TAX

Particulars Amount ($) Amount ($)

Total spending on advertisement and promotional activities 1,650,000.00

GST input credit 100% eligible for: 1,100,000.00

Portion of advertisement expenditures ineligible for input

credit in respect of GST 550,000.00

100% GST input credit 100,000.00

Add: For 2% contribution in revenue 3,000.00

Amount of input credit allowed to the bank 103,000.00

Statement showing Input Tax credit

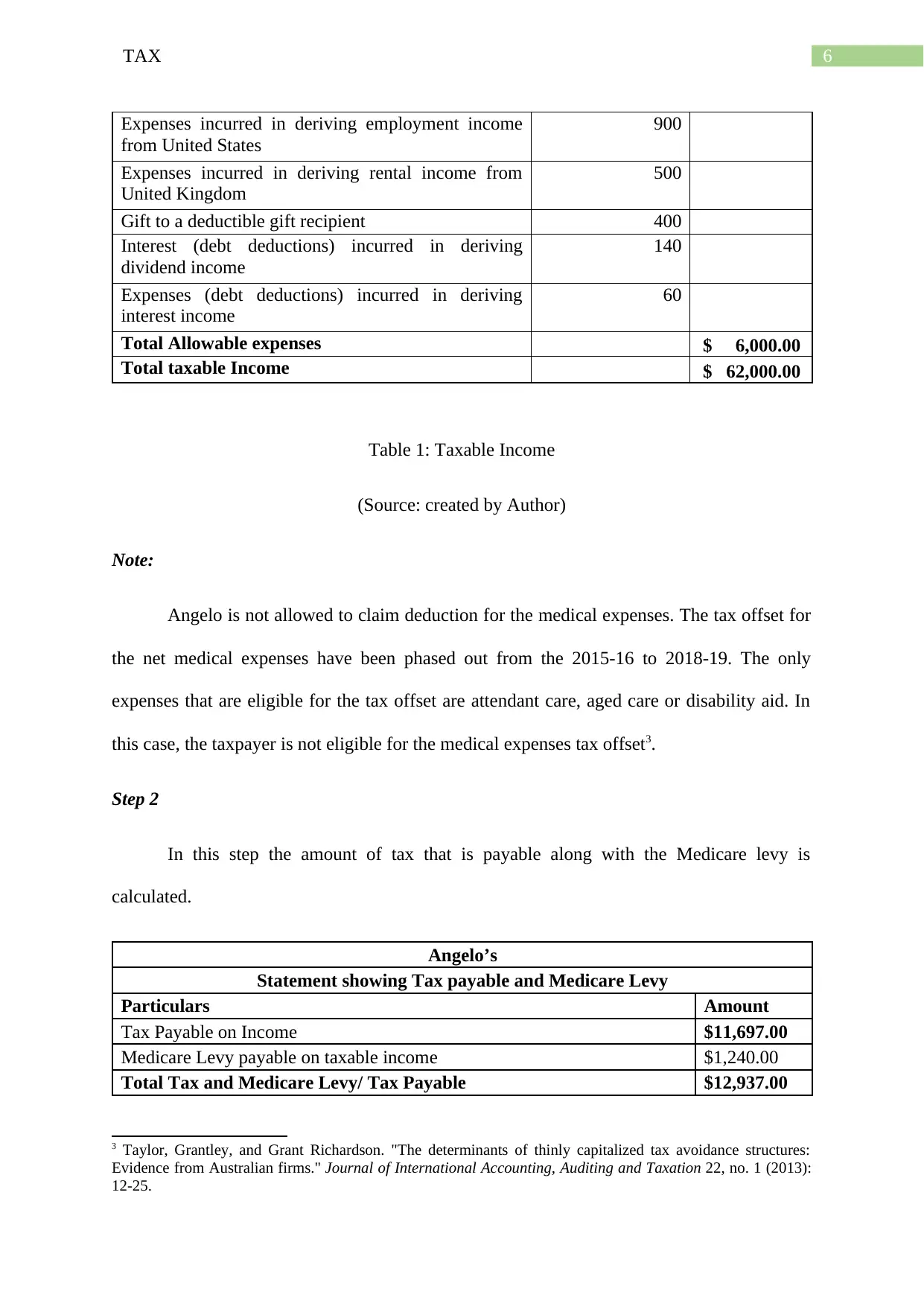

Answer to Question 3

The section 770-10(1) of the Income Tax Assessment Act 1997 provides that a

taxpayer is allowed to claim foreign tax offset for the tax that have been on foreign income.

The tax in respect of which the credit is allowed is known as the creditable taxes. In this case

the foreign tax offset that is allowed for the foreign tax paid by Angelo is calculated.

Step 1:

In this step the taxable income of Angelo is determined.

Angelo’s

Statement showing calculation of Taxable Income

Particulars Amount Amount

Gross Income

Employment income from Australia $ 44,000.00

Employment income from United States $ 12,000.00

Employment income from United Kingdom $ 8,000.00

Rental income from property in United Kingdom $ 2,000.00

Dividend income from United Kingdom $ 1,200.00

Interest income from United Kingdom $ 800.00

Total Assessable Income $ 68,000.00

Less:

Allowable Deduction

Expenses incurred in deriving employment income

from Australia

4,000

Particulars Amount ($) Amount ($)

Total spending on advertisement and promotional activities 1,650,000.00

GST input credit 100% eligible for: 1,100,000.00

Portion of advertisement expenditures ineligible for input

credit in respect of GST 550,000.00

100% GST input credit 100,000.00

Add: For 2% contribution in revenue 3,000.00

Amount of input credit allowed to the bank 103,000.00

Statement showing Input Tax credit

Answer to Question 3

The section 770-10(1) of the Income Tax Assessment Act 1997 provides that a

taxpayer is allowed to claim foreign tax offset for the tax that have been on foreign income.

The tax in respect of which the credit is allowed is known as the creditable taxes. In this case

the foreign tax offset that is allowed for the foreign tax paid by Angelo is calculated.

Step 1:

In this step the taxable income of Angelo is determined.

Angelo’s

Statement showing calculation of Taxable Income

Particulars Amount Amount

Gross Income

Employment income from Australia $ 44,000.00

Employment income from United States $ 12,000.00

Employment income from United Kingdom $ 8,000.00

Rental income from property in United Kingdom $ 2,000.00

Dividend income from United Kingdom $ 1,200.00

Interest income from United Kingdom $ 800.00

Total Assessable Income $ 68,000.00

Less:

Allowable Deduction

Expenses incurred in deriving employment income

from Australia

4,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAX

Expenses incurred in deriving employment income

from United States

900

Expenses incurred in deriving rental income from

United Kingdom

500

Gift to a deductible gift recipient 400

Interest (debt deductions) incurred in deriving

dividend income

140

Expenses (debt deductions) incurred in deriving

interest income

60

Total Allowable expenses $ 6,000.00

Total taxable Income $ 62,000.00

Table 1: Taxable Income

(Source: created by Author)

Note:

Angelo is not allowed to claim deduction for the medical expenses. The tax offset for

the net medical expenses have been phased out from the 2015-16 to 2018-19. The only

expenses that are eligible for the tax offset are attendant care, aged care or disability aid. In

this case, the taxpayer is not eligible for the medical expenses tax offset3.

Step 2

In this step the amount of tax that is payable along with the Medicare levy is

calculated.

Angelo’s

Statement showing Tax payable and Medicare Levy

Particulars Amount

Tax Payable on Income $11,697.00

Medicare Levy payable on taxable income $1,240.00

Total Tax and Medicare Levy/ Tax Payable $12,937.00

3 Taylor, Grantley, and Grant Richardson. "The determinants of thinly capitalized tax avoidance structures:

Evidence from Australian firms." Journal of International Accounting, Auditing and Taxation 22, no. 1 (2013):

12-25.

Expenses incurred in deriving employment income

from United States

900

Expenses incurred in deriving rental income from

United Kingdom

500

Gift to a deductible gift recipient 400

Interest (debt deductions) incurred in deriving

dividend income

140

Expenses (debt deductions) incurred in deriving

interest income

60

Total Allowable expenses $ 6,000.00

Total taxable Income $ 62,000.00

Table 1: Taxable Income

(Source: created by Author)

Note:

Angelo is not allowed to claim deduction for the medical expenses. The tax offset for

the net medical expenses have been phased out from the 2015-16 to 2018-19. The only

expenses that are eligible for the tax offset are attendant care, aged care or disability aid. In

this case, the taxpayer is not eligible for the medical expenses tax offset3.

Step 2

In this step the amount of tax that is payable along with the Medicare levy is

calculated.

Angelo’s

Statement showing Tax payable and Medicare Levy

Particulars Amount

Tax Payable on Income $11,697.00

Medicare Levy payable on taxable income $1,240.00

Total Tax and Medicare Levy/ Tax Payable $12,937.00

3 Taylor, Grantley, and Grant Richardson. "The determinants of thinly capitalized tax avoidance structures:

Evidence from Australian firms." Journal of International Accounting, Auditing and Taxation 22, no. 1 (2013):

12-25.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAX

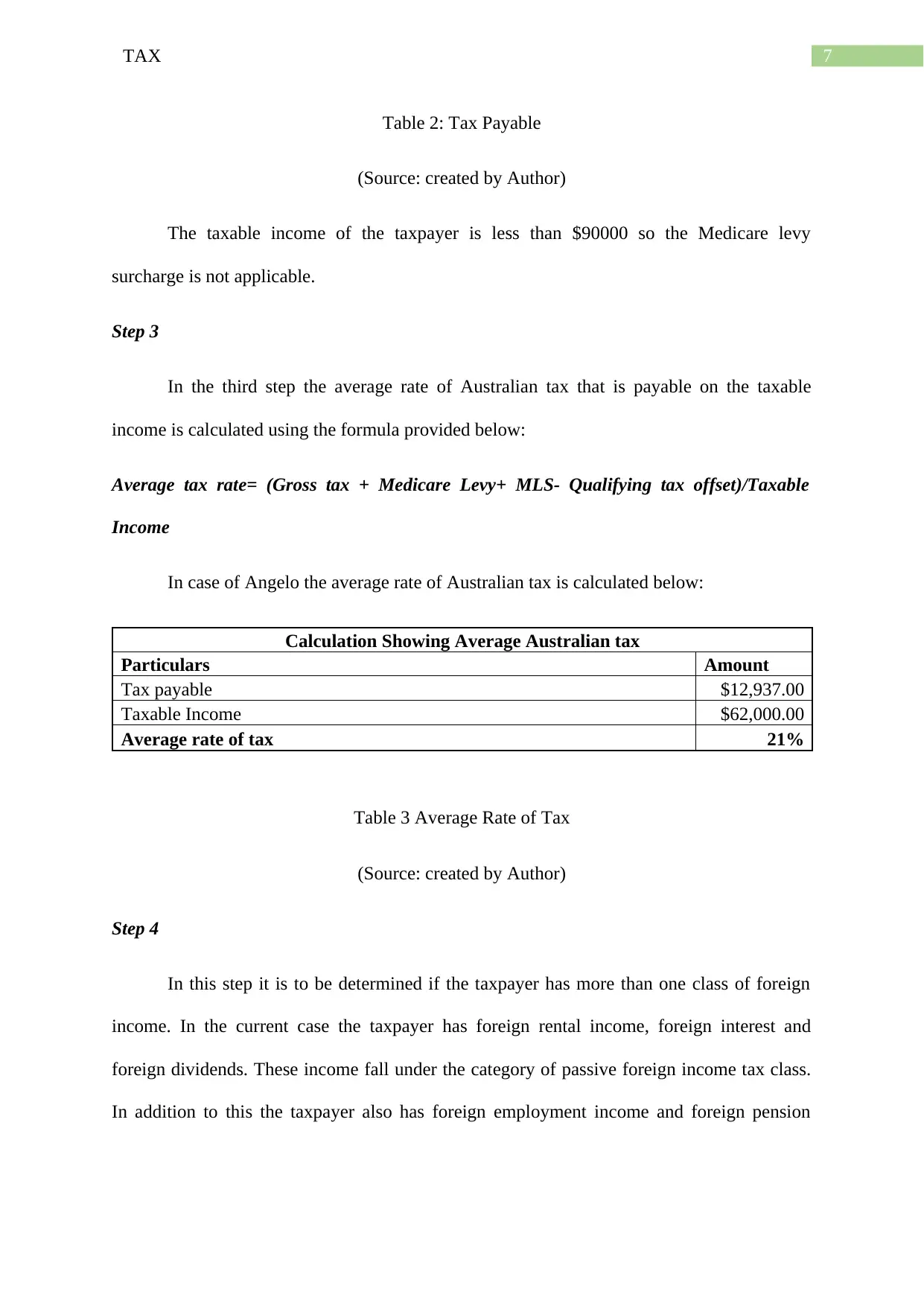

Table 2: Tax Payable

(Source: created by Author)

The taxable income of the taxpayer is less than $90000 so the Medicare levy

surcharge is not applicable.

Step 3

In the third step the average rate of Australian tax that is payable on the taxable

income is calculated using the formula provided below:

Average tax rate= (Gross tax + Medicare Levy+ MLS- Qualifying tax offset)/Taxable

Income

In case of Angelo the average rate of Australian tax is calculated below:

Calculation Showing Average Australian tax

Particulars Amount

Tax payable $12,937.00

Taxable Income $62,000.00

Average rate of tax 21%

Table 3 Average Rate of Tax

(Source: created by Author)

Step 4

In this step it is to be determined if the taxpayer has more than one class of foreign

income. In the current case the taxpayer has foreign rental income, foreign interest and

foreign dividends. These income fall under the category of passive foreign income tax class.

In addition to this the taxpayer also has foreign employment income and foreign pension

Table 2: Tax Payable

(Source: created by Author)

The taxable income of the taxpayer is less than $90000 so the Medicare levy

surcharge is not applicable.

Step 3

In the third step the average rate of Australian tax that is payable on the taxable

income is calculated using the formula provided below:

Average tax rate= (Gross tax + Medicare Levy+ MLS- Qualifying tax offset)/Taxable

Income

In case of Angelo the average rate of Australian tax is calculated below:

Calculation Showing Average Australian tax

Particulars Amount

Tax payable $12,937.00

Taxable Income $62,000.00

Average rate of tax 21%

Table 3 Average Rate of Tax

(Source: created by Author)

Step 4

In this step it is to be determined if the taxpayer has more than one class of foreign

income. In the current case the taxpayer has foreign rental income, foreign interest and

foreign dividends. These income fall under the category of passive foreign income tax class.

In addition to this the taxpayer also has foreign employment income and foreign pension

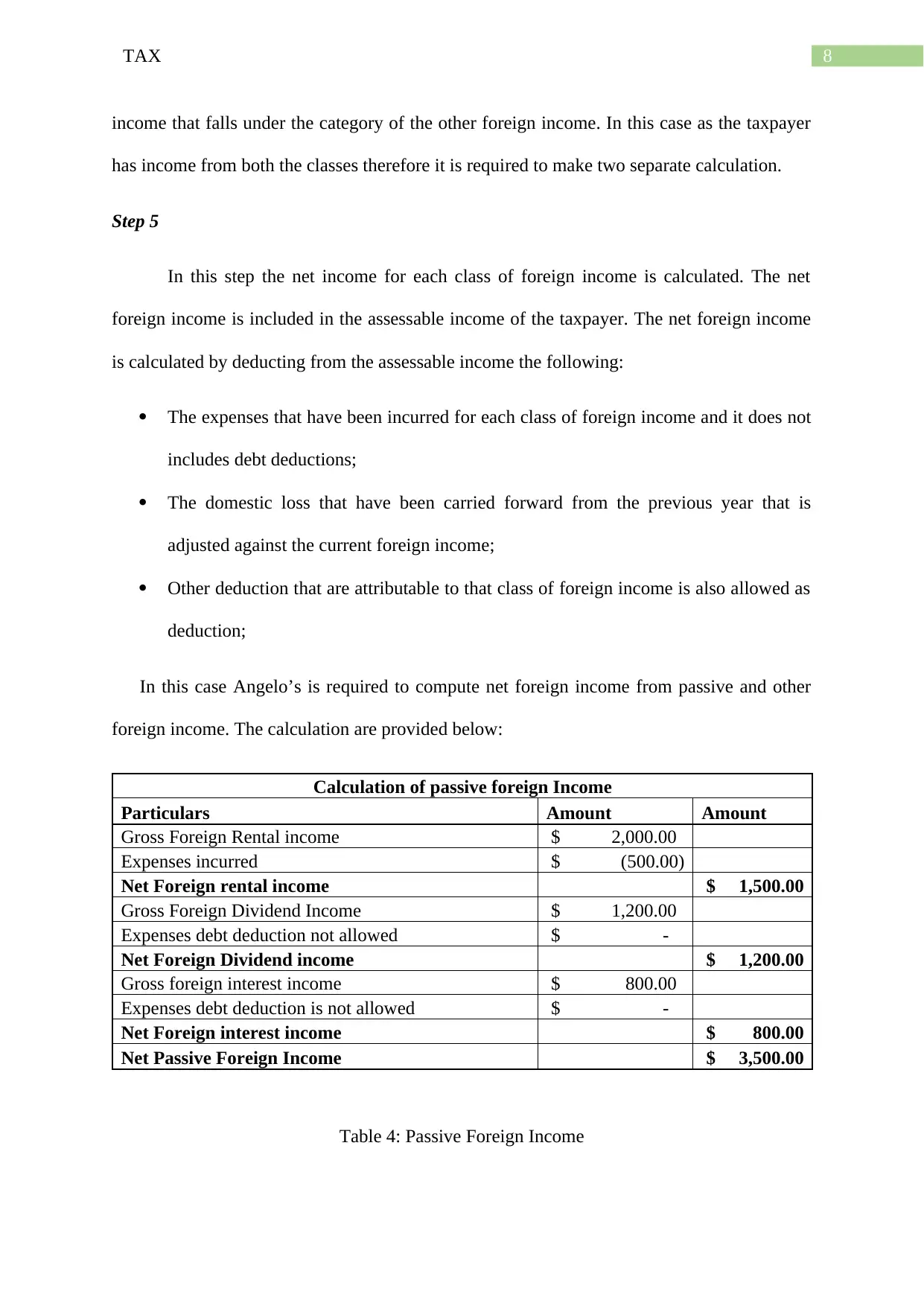

8TAX

income that falls under the category of the other foreign income. In this case as the taxpayer

has income from both the classes therefore it is required to make two separate calculation.

Step 5

In this step the net income for each class of foreign income is calculated. The net

foreign income is included in the assessable income of the taxpayer. The net foreign income

is calculated by deducting from the assessable income the following:

The expenses that have been incurred for each class of foreign income and it does not

includes debt deductions;

The domestic loss that have been carried forward from the previous year that is

adjusted against the current foreign income;

Other deduction that are attributable to that class of foreign income is also allowed as

deduction;

In this case Angelo’s is required to compute net foreign income from passive and other

foreign income. The calculation are provided below:

Calculation of passive foreign Income

Particulars Amount Amount

Gross Foreign Rental income $ 2,000.00

Expenses incurred $ (500.00)

Net Foreign rental income $ 1,500.00

Gross Foreign Dividend Income $ 1,200.00

Expenses debt deduction not allowed $ -

Net Foreign Dividend income $ 1,200.00

Gross foreign interest income $ 800.00

Expenses debt deduction is not allowed $ -

Net Foreign interest income $ 800.00

Net Passive Foreign Income $ 3,500.00

Table 4: Passive Foreign Income

income that falls under the category of the other foreign income. In this case as the taxpayer

has income from both the classes therefore it is required to make two separate calculation.

Step 5

In this step the net income for each class of foreign income is calculated. The net

foreign income is included in the assessable income of the taxpayer. The net foreign income

is calculated by deducting from the assessable income the following:

The expenses that have been incurred for each class of foreign income and it does not

includes debt deductions;

The domestic loss that have been carried forward from the previous year that is

adjusted against the current foreign income;

Other deduction that are attributable to that class of foreign income is also allowed as

deduction;

In this case Angelo’s is required to compute net foreign income from passive and other

foreign income. The calculation are provided below:

Calculation of passive foreign Income

Particulars Amount Amount

Gross Foreign Rental income $ 2,000.00

Expenses incurred $ (500.00)

Net Foreign rental income $ 1,500.00

Gross Foreign Dividend Income $ 1,200.00

Expenses debt deduction not allowed $ -

Net Foreign Dividend income $ 1,200.00

Gross foreign interest income $ 800.00

Expenses debt deduction is not allowed $ -

Net Foreign interest income $ 800.00

Net Passive Foreign Income $ 3,500.00

Table 4: Passive Foreign Income

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAX

(Source: created by Author)

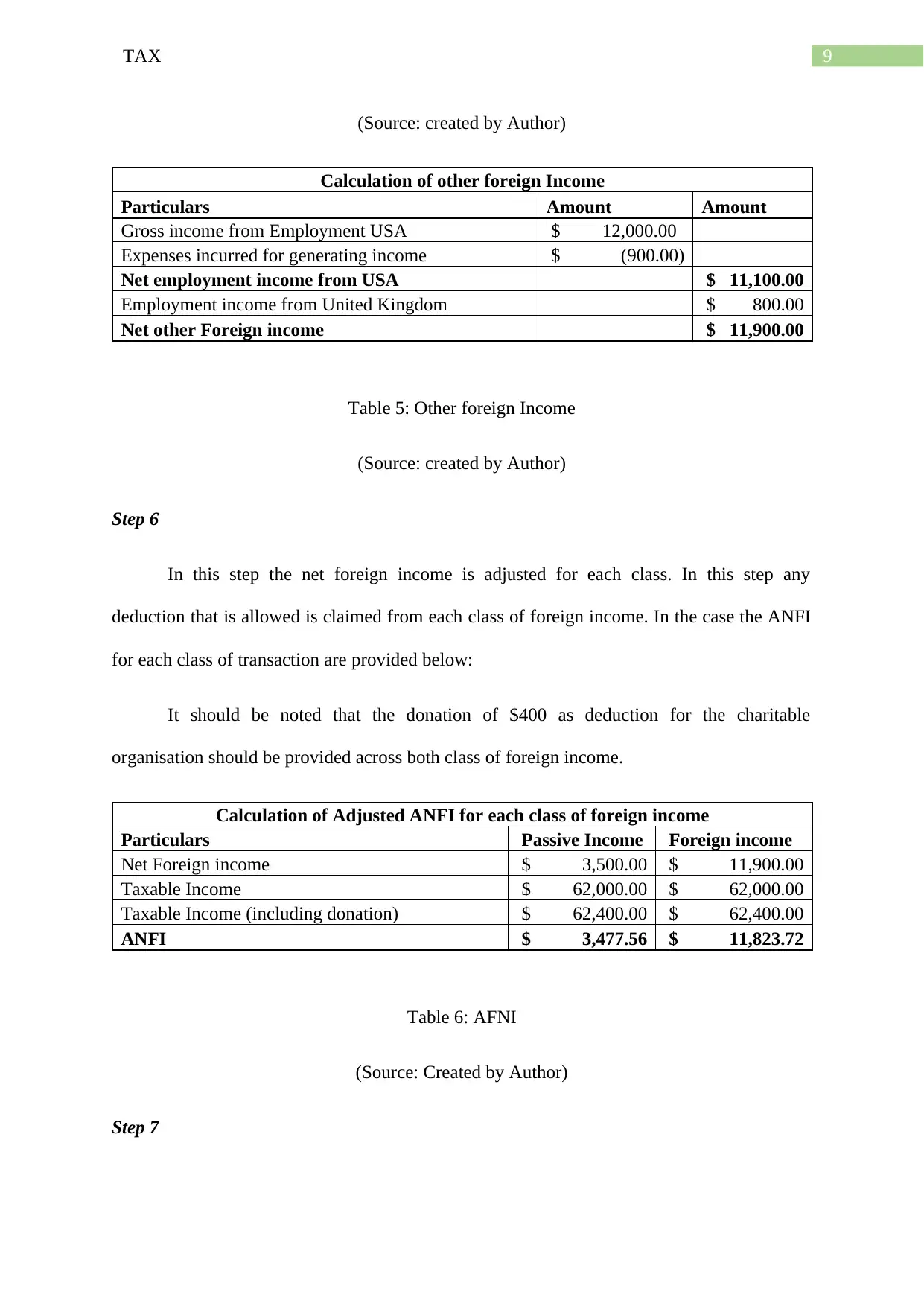

Calculation of other foreign Income

Particulars Amount Amount

Gross income from Employment USA $ 12,000.00

Expenses incurred for generating income $ (900.00)

Net employment income from USA $ 11,100.00

Employment income from United Kingdom $ 800.00

Net other Foreign income $ 11,900.00

Table 5: Other foreign Income

(Source: created by Author)

Step 6

In this step the net foreign income is adjusted for each class. In this step any

deduction that is allowed is claimed from each class of foreign income. In the case the ANFI

for each class of transaction are provided below:

It should be noted that the donation of $400 as deduction for the charitable

organisation should be provided across both class of foreign income.

Calculation of Adjusted ANFI for each class of foreign income

Particulars Passive Income Foreign income

Net Foreign income $ 3,500.00 $ 11,900.00

Taxable Income $ 62,000.00 $ 62,000.00

Taxable Income (including donation) $ 62,400.00 $ 62,400.00

ANFI $ 3,477.56 $ 11,823.72

Table 6: AFNI

(Source: Created by Author)

Step 7

(Source: created by Author)

Calculation of other foreign Income

Particulars Amount Amount

Gross income from Employment USA $ 12,000.00

Expenses incurred for generating income $ (900.00)

Net employment income from USA $ 11,100.00

Employment income from United Kingdom $ 800.00

Net other Foreign income $ 11,900.00

Table 5: Other foreign Income

(Source: created by Author)

Step 6

In this step the net foreign income is adjusted for each class. In this step any

deduction that is allowed is claimed from each class of foreign income. In the case the ANFI

for each class of transaction are provided below:

It should be noted that the donation of $400 as deduction for the charitable

organisation should be provided across both class of foreign income.

Calculation of Adjusted ANFI for each class of foreign income

Particulars Passive Income Foreign income

Net Foreign income $ 3,500.00 $ 11,900.00

Taxable Income $ 62,000.00 $ 62,000.00

Taxable Income (including donation) $ 62,400.00 $ 62,400.00

ANFI $ 3,477.56 $ 11,823.72

Table 6: AFNI

(Source: Created by Author)

Step 7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAX

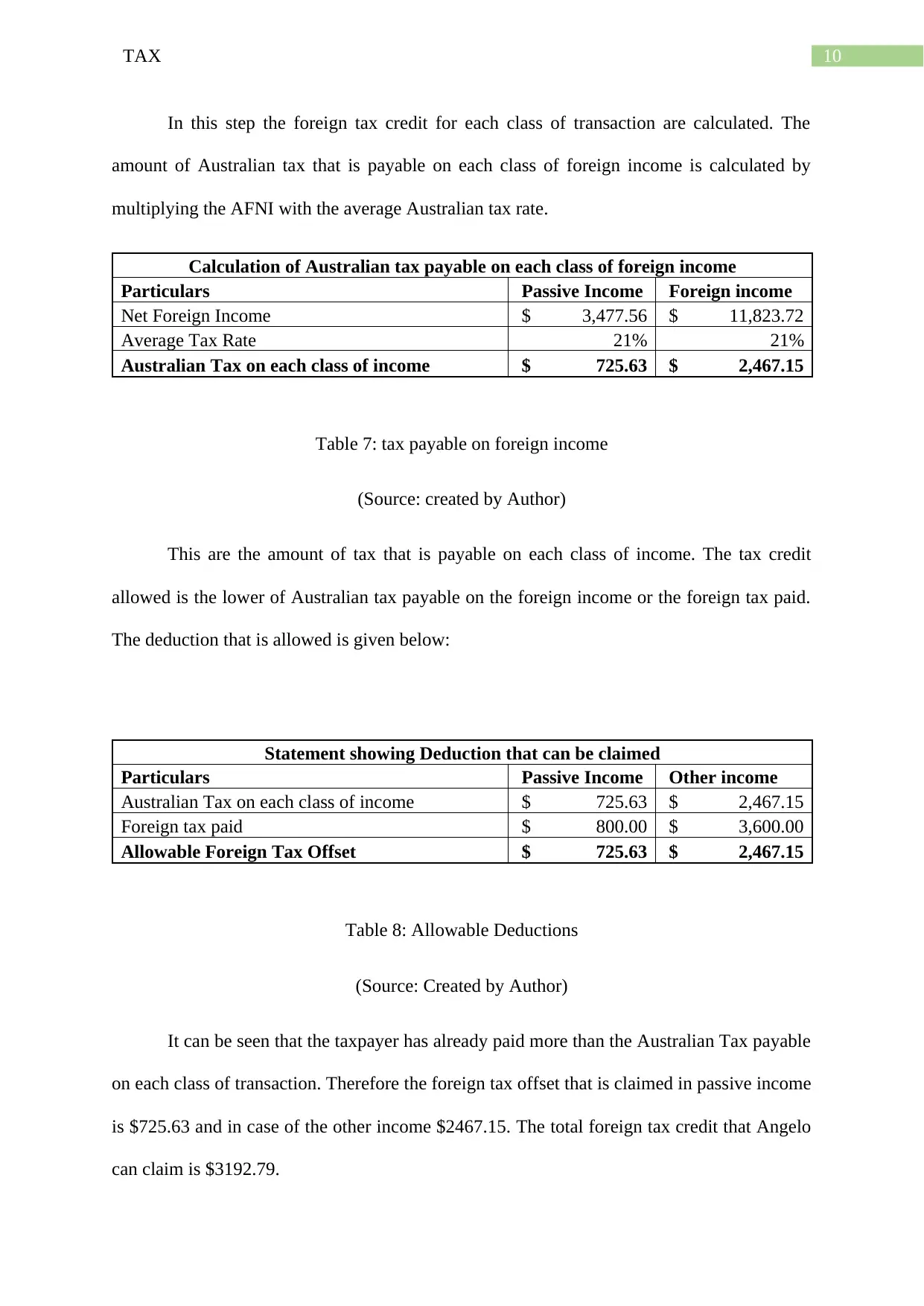

In this step the foreign tax credit for each class of transaction are calculated. The

amount of Australian tax that is payable on each class of foreign income is calculated by

multiplying the AFNI with the average Australian tax rate.

Calculation of Australian tax payable on each class of foreign income

Particulars Passive Income Foreign income

Net Foreign Income $ 3,477.56 $ 11,823.72

Average Tax Rate 21% 21%

Australian Tax on each class of income $ 725.63 $ 2,467.15

Table 7: tax payable on foreign income

(Source: created by Author)

This are the amount of tax that is payable on each class of income. The tax credit

allowed is the lower of Australian tax payable on the foreign income or the foreign tax paid.

The deduction that is allowed is given below:

Statement showing Deduction that can be claimed

Particulars Passive Income Other income

Australian Tax on each class of income $ 725.63 $ 2,467.15

Foreign tax paid $ 800.00 $ 3,600.00

Allowable Foreign Tax Offset $ 725.63 $ 2,467.15

Table 8: Allowable Deductions

(Source: Created by Author)

It can be seen that the taxpayer has already paid more than the Australian Tax payable

on each class of transaction. Therefore the foreign tax offset that is claimed in passive income

is $725.63 and in case of the other income $2467.15. The total foreign tax credit that Angelo

can claim is $3192.79.

In this step the foreign tax credit for each class of transaction are calculated. The

amount of Australian tax that is payable on each class of foreign income is calculated by

multiplying the AFNI with the average Australian tax rate.

Calculation of Australian tax payable on each class of foreign income

Particulars Passive Income Foreign income

Net Foreign Income $ 3,477.56 $ 11,823.72

Average Tax Rate 21% 21%

Australian Tax on each class of income $ 725.63 $ 2,467.15

Table 7: tax payable on foreign income

(Source: created by Author)

This are the amount of tax that is payable on each class of income. The tax credit

allowed is the lower of Australian tax payable on the foreign income or the foreign tax paid.

The deduction that is allowed is given below:

Statement showing Deduction that can be claimed

Particulars Passive Income Other income

Australian Tax on each class of income $ 725.63 $ 2,467.15

Foreign tax paid $ 800.00 $ 3,600.00

Allowable Foreign Tax Offset $ 725.63 $ 2,467.15

Table 8: Allowable Deductions

(Source: Created by Author)

It can be seen that the taxpayer has already paid more than the Australian Tax payable

on each class of transaction. Therefore the foreign tax offset that is claimed in passive income

is $725.63 and in case of the other income $2467.15. The total foreign tax credit that Angelo

can claim is $3192.79.

11TAX

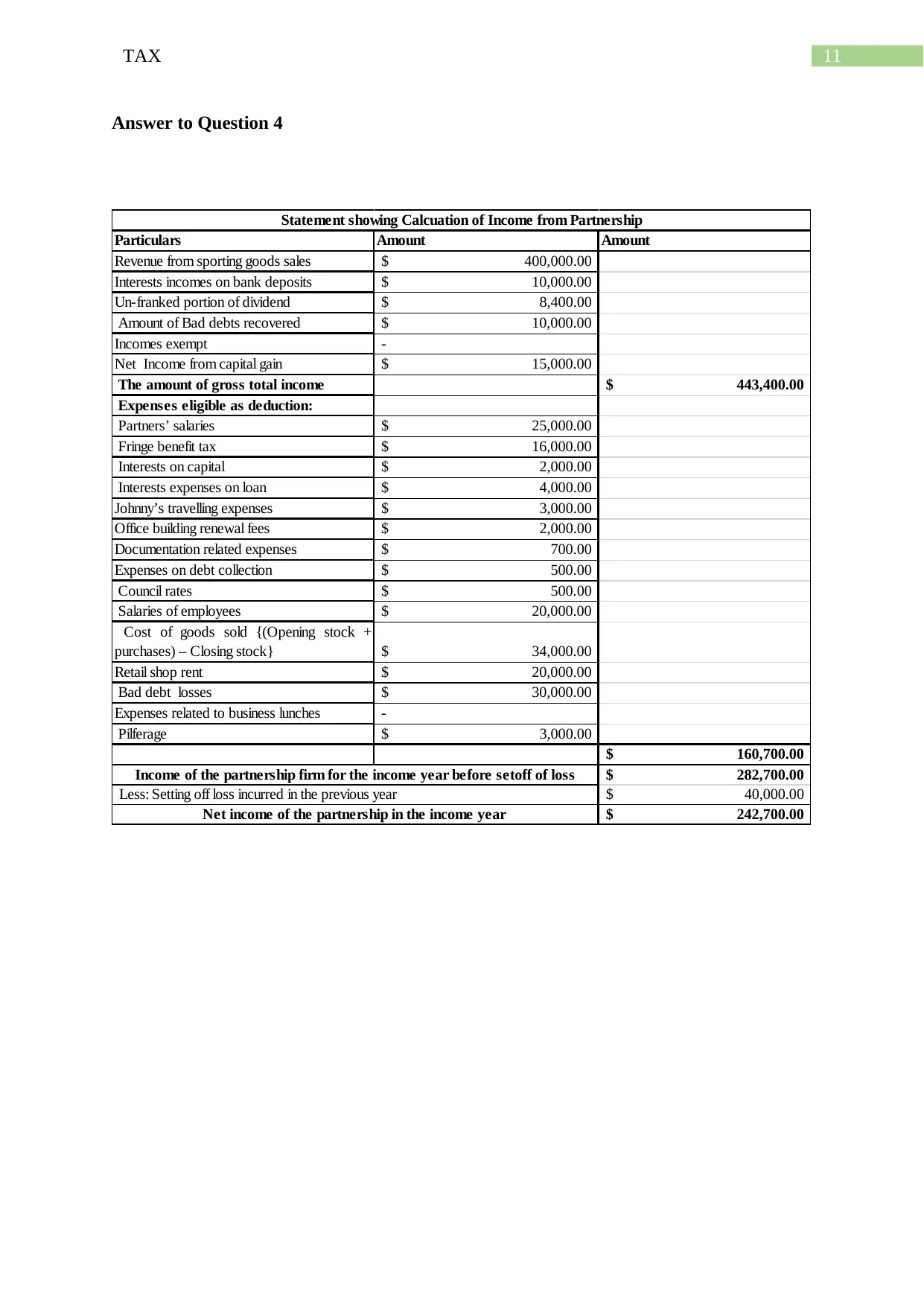

Answer to Question 4

Particulars Amount Amount

Revenue from sporting goods sales 400,000.00$

Interests incomes on bank deposits 10,000.00$

Un-franked portion of dividend 8,400.00$

Amount of Bad debts recovered 10,000.00$

Incomes exempt -

Net Income from capital gain 15,000.00$

The amount of gross total income 443,400.00$

Expenses eligible as deduction:

Partners’ salaries 25,000.00$

Fringe benefit tax 16,000.00$

Interests on capital 2,000.00$

Interests expenses on loan 4,000.00$

Johnny’s travelling expenses 3,000.00$

Office building renewal fees 2,000.00$

Documentation related expenses 700.00$

Expenses on debt collection 500.00$

Council rates 500.00$

Salaries of employees 20,000.00$

Cost of goods sold {(Opening stock +

purchases) – Closing stock} 34,000.00$

Retail shop rent 20,000.00$

Bad debt losses 30,000.00$

Expenses related to business lunches -

Pilferage 3,000.00$

160,700.00$

282,700.00$

40,000.00$

242,700.00$

Statement showing Calcuation of Income from Partnership

Income of the partnership firm for the income year before setoff of loss

Less: Setting off loss incurred in the previous year

Net income of the partnership in the income year

Answer to Question 4

Particulars Amount Amount

Revenue from sporting goods sales 400,000.00$

Interests incomes on bank deposits 10,000.00$

Un-franked portion of dividend 8,400.00$

Amount of Bad debts recovered 10,000.00$

Incomes exempt -

Net Income from capital gain 15,000.00$

The amount of gross total income 443,400.00$

Expenses eligible as deduction:

Partners’ salaries 25,000.00$

Fringe benefit tax 16,000.00$

Interests on capital 2,000.00$

Interests expenses on loan 4,000.00$

Johnny’s travelling expenses 3,000.00$

Office building renewal fees 2,000.00$

Documentation related expenses 700.00$

Expenses on debt collection 500.00$

Council rates 500.00$

Salaries of employees 20,000.00$

Cost of goods sold {(Opening stock +

purchases) – Closing stock} 34,000.00$

Retail shop rent 20,000.00$

Bad debt losses 30,000.00$

Expenses related to business lunches -

Pilferage 3,000.00$

160,700.00$

282,700.00$

40,000.00$

242,700.00$

Statement showing Calcuation of Income from Partnership

Income of the partnership firm for the income year before setoff of loss

Less: Setting off loss incurred in the previous year

Net income of the partnership in the income year

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.