Comparative Financial Analysis: Australian Vanadium and Alcoa Report

VerifiedAdded on 2020/04/01

|14

|3409

|288

Report

AI Summary

This report provides a comprehensive financial analysis comparing Australian Vanadium (formerly Yellow Rock Resources Limited) and Alcoa Inc. The analysis includes a detailed examination of financial results, comparing key metrics such as revenue, net profit, operating income, and various ratios related to profitability, liquidity, resource management, and financial stability. The report also delves into additional financial issues like interest rate risk, liquidity risk, credit risk, foreign currency impacts, and commodity price fluctuations. Furthermore, it contrasts the environmental reporting practices of both companies, highlighting Alcoa's proactive approach to reducing carbon emissions and promoting sustainability, while noting the lack of such detailed reporting from Australian Vanadium. The conclusion synthesizes the findings, offering insights into the financial performance and environmental consciousness of both companies.

Accounting for Management

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction................................................................................................................................3

Comparison of financial result...................................................................................................3

Profitability:...........................................................................................................................5

Liquidity:................................................................................................................................6

Operation:...............................................................................................................................6

Resource management...........................................................................................................6

Financial Stability & Performance:........................................................................................7

Additional financial issues.....................................................................................................8

Comparison of environmental issues and reporting of the issues............................................10

Conclusion:..............................................................................................................................12

Reference..................................................................................................................................13

2

Introduction................................................................................................................................3

Comparison of financial result...................................................................................................3

Profitability:...........................................................................................................................5

Liquidity:................................................................................................................................6

Operation:...............................................................................................................................6

Resource management...........................................................................................................6

Financial Stability & Performance:........................................................................................7

Additional financial issues.....................................................................................................8

Comparison of environmental issues and reporting of the issues............................................10

Conclusion:..............................................................................................................................12

Reference..................................................................................................................................13

2

Introduction

In the current report the selected company is ‘Yellow rock resources limited’ (YRR) which

currently changed its name as ‘Australian Vanadium’. The company currently at

Meekatharra, is developing a project ‘Gabanintha Vanadium’ which would produce the

Vanadium of highest grade (Australian Vanadium, 2017). The main revenue source for this

product is the battery company who needs these high grade materials. The growth in this

sector is extremely positive because of the renewable energy popularity. The organisation

wants to develop great value for their shareholders by growing in this market. On the other

hand the benchmarking company here is Alcoa Inc. Alcoa has the bauxite miming facility

which is one of the largest in the world. The organisation comes under the list of leading

exporter of Australia with around $4 billion in export valuation (Alcoa, 2017). Considering

all of this information the following section of the report would focus on the financial and

environmental aspect of these businesses.

Comparison of financial result

Australian Vanadium limited or Yellow

Rock Resource Limited(YRR)

$ $

2016 2015

Revenue 290005 200247

net profit/loss

-

1,285,100

-

1,434,013

operating

income/loss 233663 -128237

Current asset 3,376,810 2087697

Current Liability 225,737 242750

Total asset

17,886,78

9

16,273,62

5

Share holders

equity

17,661,05

2

16,030,87

5

Profitability

Ratio

Net profit

margin(net

profit/sales

revenue)

-

4.431303

-

7.161221

3

In the current report the selected company is ‘Yellow rock resources limited’ (YRR) which

currently changed its name as ‘Australian Vanadium’. The company currently at

Meekatharra, is developing a project ‘Gabanintha Vanadium’ which would produce the

Vanadium of highest grade (Australian Vanadium, 2017). The main revenue source for this

product is the battery company who needs these high grade materials. The growth in this

sector is extremely positive because of the renewable energy popularity. The organisation

wants to develop great value for their shareholders by growing in this market. On the other

hand the benchmarking company here is Alcoa Inc. Alcoa has the bauxite miming facility

which is one of the largest in the world. The organisation comes under the list of leading

exporter of Australia with around $4 billion in export valuation (Alcoa, 2017). Considering

all of this information the following section of the report would focus on the financial and

environmental aspect of these businesses.

Comparison of financial result

Australian Vanadium limited or Yellow

Rock Resource Limited(YRR)

$ $

2016 2015

Revenue 290005 200247

net profit/loss

-

1,285,100

-

1,434,013

operating

income/loss 233663 -128237

Current asset 3,376,810 2087697

Current Liability 225,737 242750

Total asset

17,886,78

9

16,273,62

5

Share holders

equity

17,661,05

2

16,030,87

5

Profitability

Ratio

Net profit

margin(net

profit/sales

revenue)

-

4.431303

-

7.161221

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

operation related

ratios

Operating profit

margin[operating

profit or loss/net

sales]

0.805720

6

-

0.640394

Liquidity ratio

Current

Ratio[current

asset/current

liability]

14.95904

5

8.600193

6

Resource

management

Return on

asset[ROA](Net

profit/Average

total asset)

-

0.071846

-

0.088119

ROCE(Return on

capital employed)

[Net

op-profit/{TA-

CL}]

0.013230

4

-

0.007999

ROE(Return on

Equity)[net

income/share

holders equity]

-

0.072765

-

0.089453

[Source: australianvanadium.com.au, 2017]

Alcoa -benchmark company of Aluminum

exploration Industry, Australia

$ $

2016 2015

Revenue 9,318 11,199

net profit/loss -162 -337

operating

income/loss 1028 1738

Current asset 3,181 2,566

Current Liability 2,821 2,404

Total asset 16,741 16,413

Share holders equity 5,654 9,442

Profitability Ratio

4

ratios

Operating profit

margin[operating

profit or loss/net

sales]

0.805720

6

-

0.640394

Liquidity ratio

Current

Ratio[current

asset/current

liability]

14.95904

5

8.600193

6

Resource

management

Return on

asset[ROA](Net

profit/Average

total asset)

-

0.071846

-

0.088119

ROCE(Return on

capital employed)

[Net

op-profit/{TA-

CL}]

0.013230

4

-

0.007999

ROE(Return on

Equity)[net

income/share

holders equity]

-

0.072765

-

0.089453

[Source: australianvanadium.com.au, 2017]

Alcoa -benchmark company of Aluminum

exploration Industry, Australia

$ $

2016 2015

Revenue 9,318 11,199

net profit/loss -162 -337

operating

income/loss 1028 1738

Current asset 3,181 2,566

Current Liability 2,821 2,404

Total asset 16,741 16,413

Share holders equity 5,654 9,442

Profitability Ratio

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

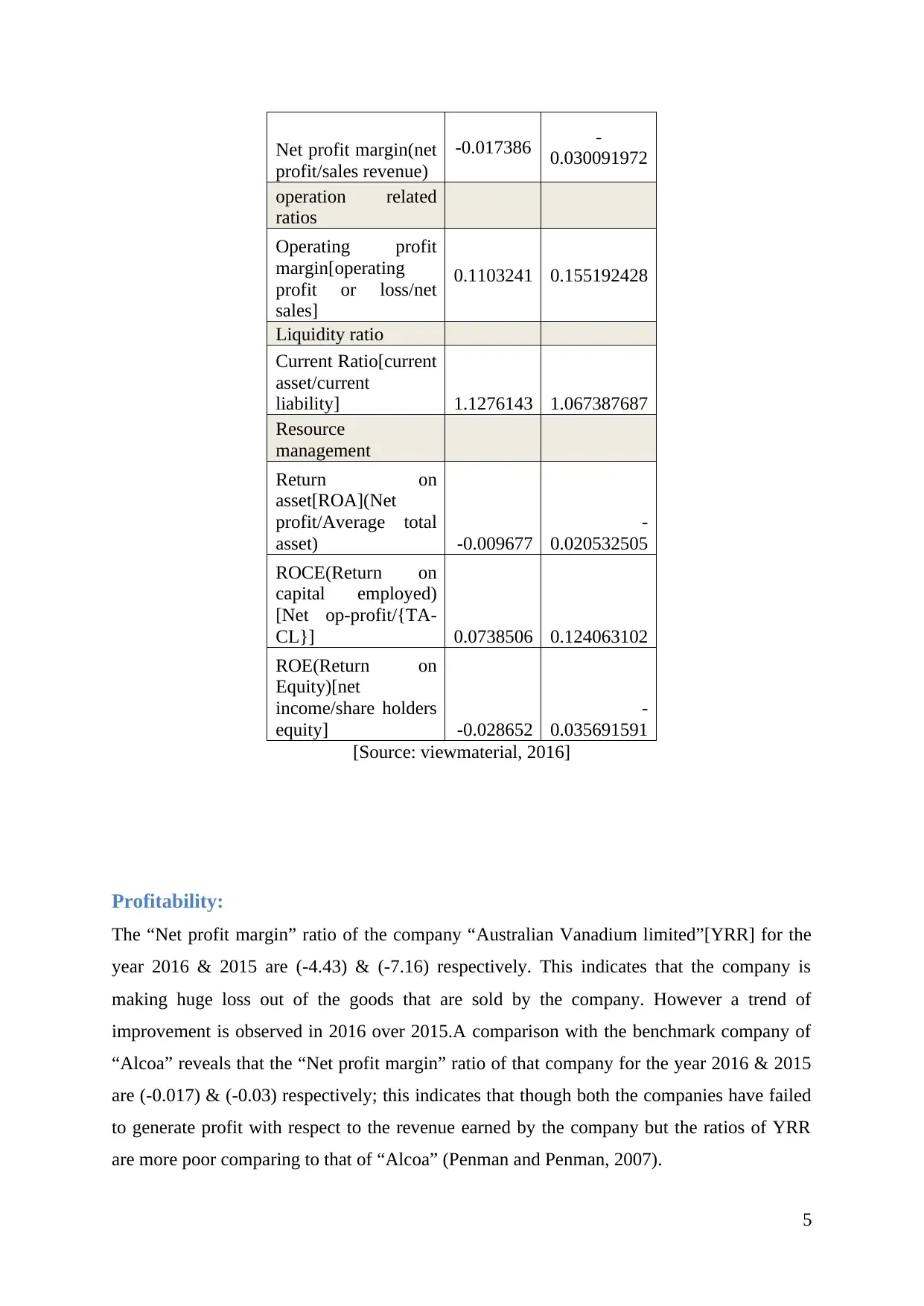

Net profit margin(net

profit/sales revenue)

-0.017386 -

0.030091972

operation related

ratios

Operating profit

margin[operating

profit or loss/net

sales]

0.1103241 0.155192428

Liquidity ratio

Current Ratio[current

asset/current

liability] 1.1276143 1.067387687

Resource

management

Return on

asset[ROA](Net

profit/Average total

asset) -0.009677

-

0.020532505

ROCE(Return on

capital employed)

[Net op-profit/{TA-

CL}] 0.0738506 0.124063102

ROE(Return on

Equity)[net

income/share holders

equity] -0.028652

-

0.035691591

[Source: viewmaterial, 2016]

Profitability:

The “Net profit margin” ratio of the company “Australian Vanadium limited”[YRR] for the

year 2016 & 2015 are (-4.43) & (-7.16) respectively. This indicates that the company is

making huge loss out of the goods that are sold by the company. However a trend of

improvement is observed in 2016 over 2015.A comparison with the benchmark company of

“Alcoa” reveals that the “Net profit margin” ratio of that company for the year 2016 & 2015

are (-0.017) & (-0.03) respectively; this indicates that though both the companies have failed

to generate profit with respect to the revenue earned by the company but the ratios of YRR

are more poor comparing to that of “Alcoa” (Penman and Penman, 2007).

5

profit/sales revenue)

-0.017386 -

0.030091972

operation related

ratios

Operating profit

margin[operating

profit or loss/net

sales]

0.1103241 0.155192428

Liquidity ratio

Current Ratio[current

asset/current

liability] 1.1276143 1.067387687

Resource

management

Return on

asset[ROA](Net

profit/Average total

asset) -0.009677

-

0.020532505

ROCE(Return on

capital employed)

[Net op-profit/{TA-

CL}] 0.0738506 0.124063102

ROE(Return on

Equity)[net

income/share holders

equity] -0.028652

-

0.035691591

[Source: viewmaterial, 2016]

Profitability:

The “Net profit margin” ratio of the company “Australian Vanadium limited”[YRR] for the

year 2016 & 2015 are (-4.43) & (-7.16) respectively. This indicates that the company is

making huge loss out of the goods that are sold by the company. However a trend of

improvement is observed in 2016 over 2015.A comparison with the benchmark company of

“Alcoa” reveals that the “Net profit margin” ratio of that company for the year 2016 & 2015

are (-0.017) & (-0.03) respectively; this indicates that though both the companies have failed

to generate profit with respect to the revenue earned by the company but the ratios of YRR

are more poor comparing to that of “Alcoa” (Penman and Penman, 2007).

5

Liquidity:

The current ratio of 14.96 in 2016 and that of 8.60 of 2015 of the company YRR shows that

the company is having huge amount of liquid asset in hand in comparison to the current

liability of the company. More over the current ratio of 2016 is higher than that of 2015.This

indicates that the company prefers to hold huge amount of liquid cash instead of investing

them (MacQueen et al., 2016). An evaluation of the liquidity ratios with that of Alcoa shows

that ratios of that company are around 1.13 & 1.07 for 2016 & 2015 respectively. This

indicates that Alcoa is not holding good liquidity position but is also more capable to make

good utilization of their liquid cash in comparison to YRR

Operation:

The operational profit margin ratio of YRR are 0.81 & (-0.64) for 2116 & 2015 respectively.

This indicates that the operating profit generating capacity out of the sales generated by the

company is comparatively better than the net profit generation capacity of that company

(Penman and Penman, 2007). However the operating profit generation capacity of that

company is showing some degree of improvements in 2016 over that of 2015.That is the ratio

has become positive in 2015.

The operating profit ratios of Alcoa are 0.11 & 0.16 respectively and therefore it can be seen

that Alcoa is having better operational efficiency with respect to YRR.

Resource management

The resource management position of the companies would be compared through the ratios

like the return on asset, return on equity and return on capital (Griffin, 2009). Return on asset

of Alcoa is -0.0096 and -0.0205 for the year 2016 and 2015 respectively. On the other hand

the return on asset for ‘Yellow rock resources limited’ (YRR) are -0.071 and -0.088 for the

year 2016 and 2015 respectively. The ratios are both in negative as the net profit of both the

businesses are in negative. For Alcoa the ratio has improved from year 2015 to 2016. On the

other hand the ratio for YRR is more or less the same. So as a benchmark company the

utilisation of asset in the business operation is much more efficient for Alcoa in comparison

to YRR.

The ROCE ratios for RYC are 0.0132 and -0.007 for the year 2016 and 2015 respectively. On

the other hand the ratios for Alcoa are 0.073 and 0.124. In case of Alcoa as a benchmark

company the performance is better than RYC but the efficiency of capital employed has

6

The current ratio of 14.96 in 2016 and that of 8.60 of 2015 of the company YRR shows that

the company is having huge amount of liquid asset in hand in comparison to the current

liability of the company. More over the current ratio of 2016 is higher than that of 2015.This

indicates that the company prefers to hold huge amount of liquid cash instead of investing

them (MacQueen et al., 2016). An evaluation of the liquidity ratios with that of Alcoa shows

that ratios of that company are around 1.13 & 1.07 for 2016 & 2015 respectively. This

indicates that Alcoa is not holding good liquidity position but is also more capable to make

good utilization of their liquid cash in comparison to YRR

Operation:

The operational profit margin ratio of YRR are 0.81 & (-0.64) for 2116 & 2015 respectively.

This indicates that the operating profit generating capacity out of the sales generated by the

company is comparatively better than the net profit generation capacity of that company

(Penman and Penman, 2007). However the operating profit generation capacity of that

company is showing some degree of improvements in 2016 over that of 2015.That is the ratio

has become positive in 2015.

The operating profit ratios of Alcoa are 0.11 & 0.16 respectively and therefore it can be seen

that Alcoa is having better operational efficiency with respect to YRR.

Resource management

The resource management position of the companies would be compared through the ratios

like the return on asset, return on equity and return on capital (Griffin, 2009). Return on asset

of Alcoa is -0.0096 and -0.0205 for the year 2016 and 2015 respectively. On the other hand

the return on asset for ‘Yellow rock resources limited’ (YRR) are -0.071 and -0.088 for the

year 2016 and 2015 respectively. The ratios are both in negative as the net profit of both the

businesses are in negative. For Alcoa the ratio has improved from year 2015 to 2016. On the

other hand the ratio for YRR is more or less the same. So as a benchmark company the

utilisation of asset in the business operation is much more efficient for Alcoa in comparison

to YRR.

The ROCE ratios for RYC are 0.0132 and -0.007 for the year 2016 and 2015 respectively. On

the other hand the ratios for Alcoa are 0.073 and 0.124. In case of Alcoa as a benchmark

company the performance is better than RYC but the efficiency of capital employed has

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

dropped for Alcoa from the year 2015 to 2016 (Healy and Palepu, 2012). In case of YRR the

ratio has improves over the year period.

In case of return on equity the figure for RYC are -0.072 and -0.089 for the year 2016 and

2015 respectively whereas the figure for Alcoa are -0.028 and -0.035. Both of them show

some minor improvement on this ratio (Higgins, 2012). Over all net profit of both the

business is in negative and that is why the ratio is negative but the performance of Alcoa is

better and the organisation is able to use its investment better.

Financial Stability & Performance:

From the discussion of the above ratios it can be seen that the overall financial performance

of the company is quiet poor with respect to the industry benchmark standard. It is true that

the company is operating in the heavy industry that demands a huge initial infrastructural

investment but still it is very much required that the investments are to be done in an efficient

manner so that the business can earn a good profit earning pace or momentum that can help

the business to quickly recover the initial investments made by the company (MacQueen et

al., 2016).

A deeper look at the ratios help us to identify that the operating profit margin ratio of the

company YRR is comparatively better than the net profit margin ratio. This indicates that the

business is losing out maximum of its earrings in regulating the operation expenses of the

company. Thus it can be said that YRR is badly suffering due to operational inefficiency.

The high liquidity ratios of the company are showing that the company is holding huge

amount of liquid cash instead of investments (Griffin, 2009). This indicates that the company

lacks good planning of investments

The Negative resource management ratios such as ROA & ROE are showing that the

company has failed to generate sufficient return on total asset as well as equity capital due to

inefficient management of the assets at their disposal.

However the cautious nature of the company that leads to holding of liquid cash (instead of

making unplanned expenditure that may lead to further loss) and the effort of the company to

improve their operational efficiency which leads to positive operating profit margin ratio in

2016(0.81) describes that the company is expect to sustain and to attain financial stability in

near future (Healy and Palepu, 2012).

7

ratio has improves over the year period.

In case of return on equity the figure for RYC are -0.072 and -0.089 for the year 2016 and

2015 respectively whereas the figure for Alcoa are -0.028 and -0.035. Both of them show

some minor improvement on this ratio (Higgins, 2012). Over all net profit of both the

business is in negative and that is why the ratio is negative but the performance of Alcoa is

better and the organisation is able to use its investment better.

Financial Stability & Performance:

From the discussion of the above ratios it can be seen that the overall financial performance

of the company is quiet poor with respect to the industry benchmark standard. It is true that

the company is operating in the heavy industry that demands a huge initial infrastructural

investment but still it is very much required that the investments are to be done in an efficient

manner so that the business can earn a good profit earning pace or momentum that can help

the business to quickly recover the initial investments made by the company (MacQueen et

al., 2016).

A deeper look at the ratios help us to identify that the operating profit margin ratio of the

company YRR is comparatively better than the net profit margin ratio. This indicates that the

business is losing out maximum of its earrings in regulating the operation expenses of the

company. Thus it can be said that YRR is badly suffering due to operational inefficiency.

The high liquidity ratios of the company are showing that the company is holding huge

amount of liquid cash instead of investments (Griffin, 2009). This indicates that the company

lacks good planning of investments

The Negative resource management ratios such as ROA & ROE are showing that the

company has failed to generate sufficient return on total asset as well as equity capital due to

inefficient management of the assets at their disposal.

However the cautious nature of the company that leads to holding of liquid cash (instead of

making unplanned expenditure that may lead to further loss) and the effort of the company to

improve their operational efficiency which leads to positive operating profit margin ratio in

2016(0.81) describes that the company is expect to sustain and to attain financial stability in

near future (Healy and Palepu, 2012).

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Additional financial issues

The financial risk factors of the business need to be under considered properly and those are

given below.

Risk due to interest rate-

[Source: australianvanadium.com.au, 2017]

The above interest bearing account is having huge sum of money which have increase by

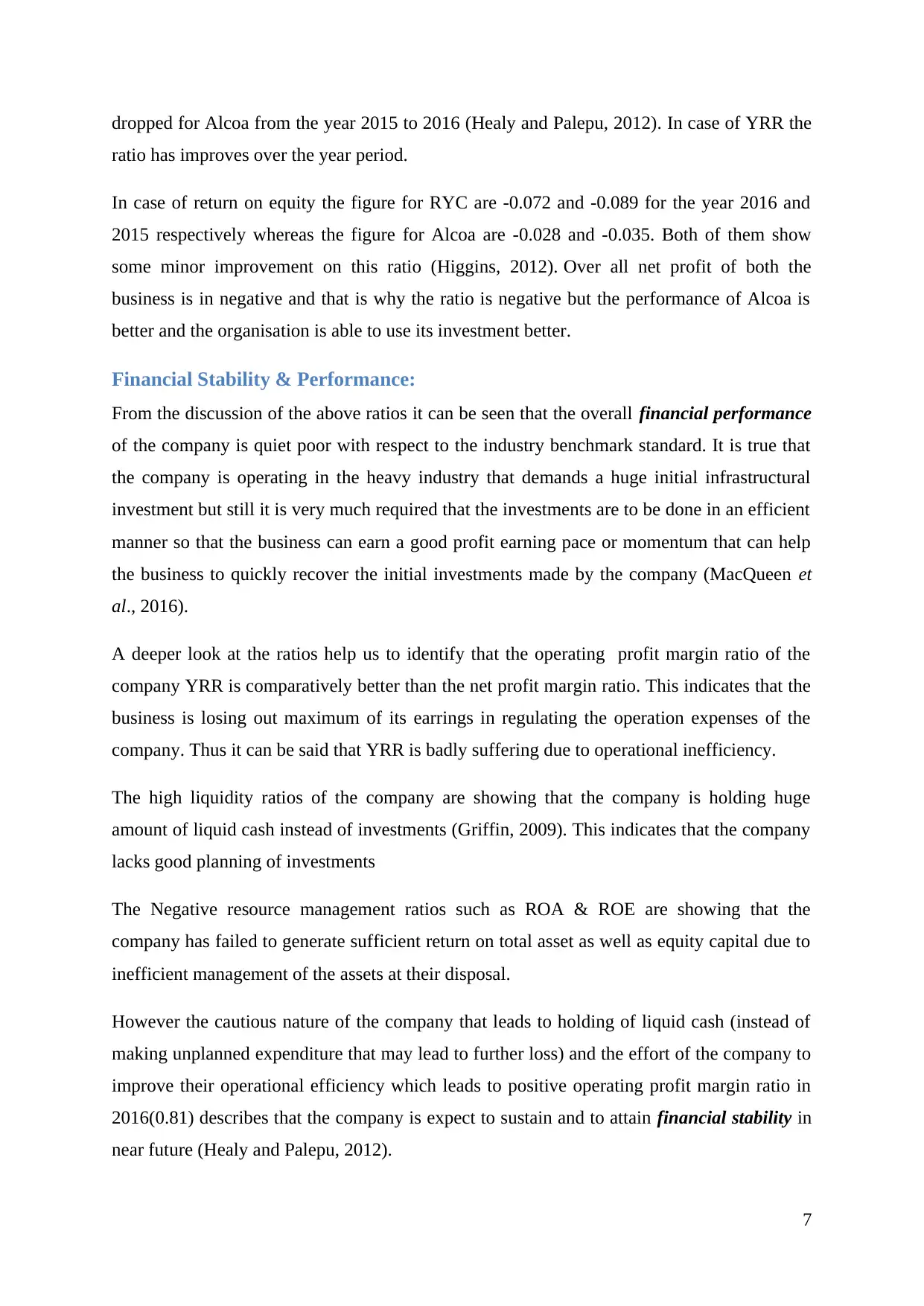

76% from the year 2015 to 2016. The increase in interest rate could create risk for this (Van

Deventer et al., 2013). The below interest rate pattern for the economy is showing a

downward pattern. So this risk is on the lower side for the company.

[Source: Tradingeconomics, 2017]

Risk of liquidity

The debt level in the YRR does not have any significant exposure in the current business

situation and because of that this risk is very low for the company (Van Deventer et al.,

2013).

8

The financial risk factors of the business need to be under considered properly and those are

given below.

Risk due to interest rate-

[Source: australianvanadium.com.au, 2017]

The above interest bearing account is having huge sum of money which have increase by

76% from the year 2015 to 2016. The increase in interest rate could create risk for this (Van

Deventer et al., 2013). The below interest rate pattern for the economy is showing a

downward pattern. So this risk is on the lower side for the company.

[Source: Tradingeconomics, 2017]

Risk of liquidity

The debt level in the YRR does not have any significant exposure in the current business

situation and because of that this risk is very low for the company (Van Deventer et al.,

2013).

8

Risk from credit

The third parties are trustworthy as stated in the annual report of YRR 2016. In that context

the risk from the bad debt are low in the company (Christoffersen, 2012). So the from the

annual report any significant risk of credit is not visible.

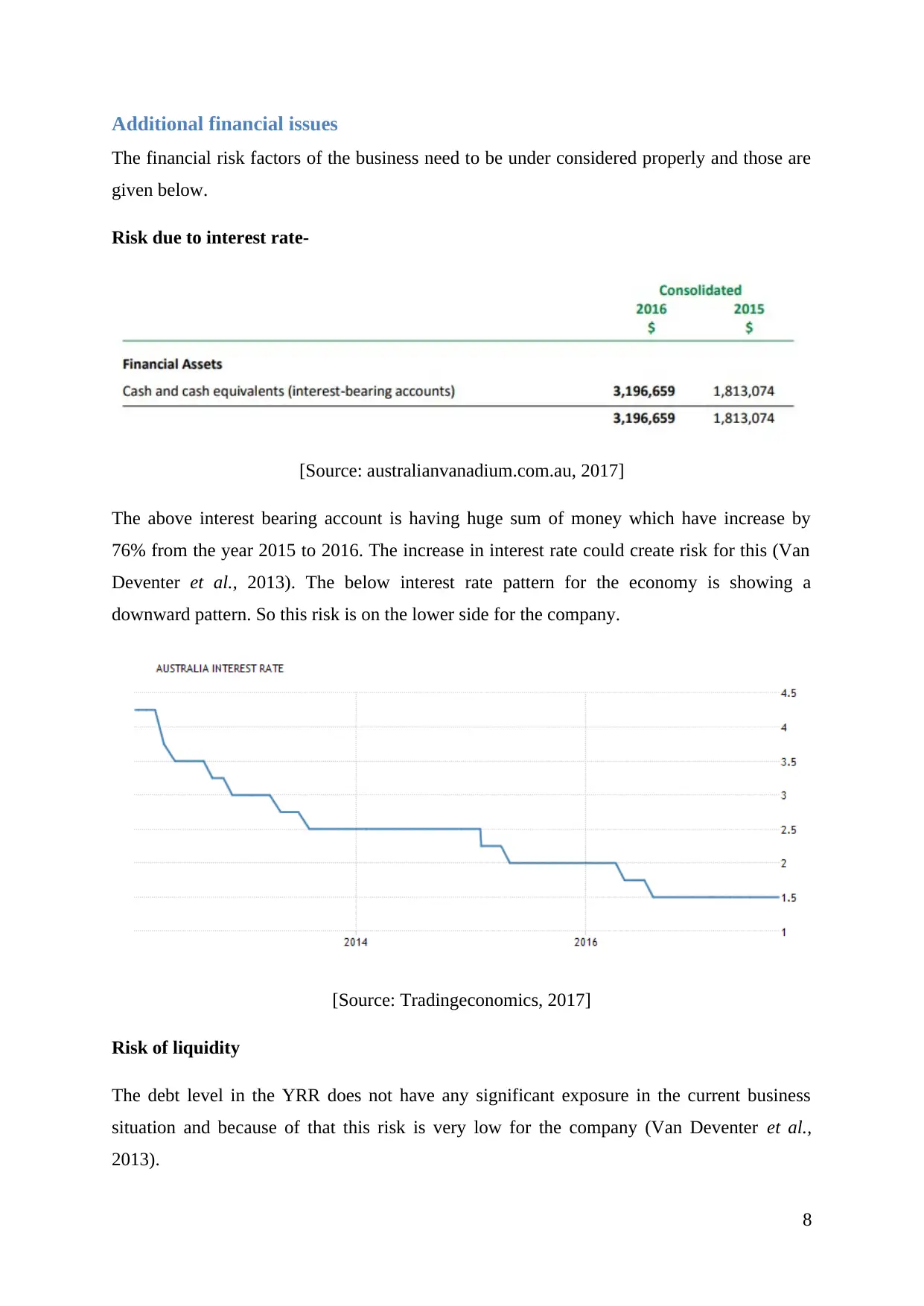

Foreign currency

From the 2014 onward the USD/AUD value is in increasing mode. That means the AUD

value is getting down against the USD. YRR is expected to gain from its export related

activates (Higgins, 2012). Considering this the export opportunity is looking bright for the

company.

[Source: Xe, 2017]

Commodity price

YRR is mainly dealing with the Vanadium. The price change in the international market

shows a downward trend up to 2016 and after that it is showing a strong upward trend. So

9

The third parties are trustworthy as stated in the annual report of YRR 2016. In that context

the risk from the bad debt are low in the company (Christoffersen, 2012). So the from the

annual report any significant risk of credit is not visible.

Foreign currency

From the 2014 onward the USD/AUD value is in increasing mode. That means the AUD

value is getting down against the USD. YRR is expected to gain from its export related

activates (Higgins, 2012). Considering this the export opportunity is looking bright for the

company.

[Source: Xe, 2017]

Commodity price

YRR is mainly dealing with the Vanadium. The price change in the international market

shows a downward trend up to 2016 and after that it is showing a strong upward trend. So

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

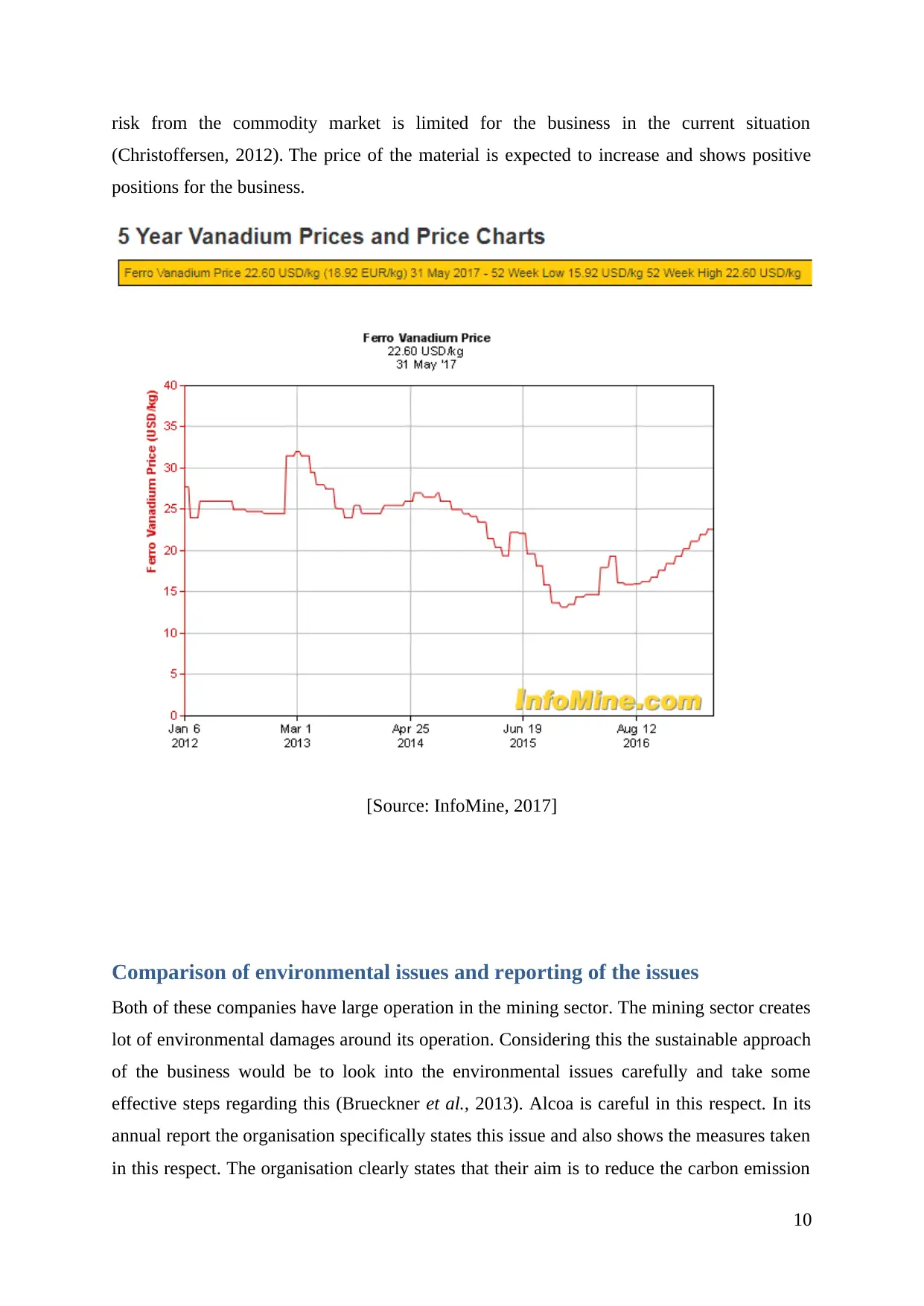

risk from the commodity market is limited for the business in the current situation

(Christoffersen, 2012). The price of the material is expected to increase and shows positive

positions for the business.

[Source: InfoMine, 2017]

Comparison of environmental issues and reporting of the issues

Both of these companies have large operation in the mining sector. The mining sector creates

lot of environmental damages around its operation. Considering this the sustainable approach

of the business would be to look into the environmental issues carefully and take some

effective steps regarding this (Brueckner et al., 2013). Alcoa is careful in this respect. In its

annual report the organisation specifically states this issue and also shows the measures taken

in this respect. The organisation clearly states that their aim is to reduce the carbon emission

10

(Christoffersen, 2012). The price of the material is expected to increase and shows positive

positions for the business.

[Source: InfoMine, 2017]

Comparison of environmental issues and reporting of the issues

Both of these companies have large operation in the mining sector. The mining sector creates

lot of environmental damages around its operation. Considering this the sustainable approach

of the business would be to look into the environmental issues carefully and take some

effective steps regarding this (Brueckner et al., 2013). Alcoa is careful in this respect. In its

annual report the organisation specifically states this issue and also shows the measures taken

in this respect. The organisation clearly states that their aim is to reduce the carbon emission

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

from the business for the environmental benefit. 5.5 million mt tons of carbon were reduced

from its operation in the year 2015 (asx.com.au, 2015). The organisation got into the

‘Aluminium stewardship initiative’ for the sustainable standard for the aluminium sector in

the world. In the annual report of 2016 the organisation mentions the reduction level of

carbon emission by 6 million mt tons. So it is clear that the business is continuously putting

effort in this context. This report further mentions the reduction of energy intensity by 1%,

consumption of water by around nineteen million m3 and landfill related waste by 86.5k mt

tons (viewmaterial, 2016). The organisation also develops product line called SUSTANA

which are basically based on the recycled material and low carbon emitting process. The

website of the company shows the target for the company in this regard. The organisation

target is to reduce the carbon emission by 30% within 2020 and 35% within completion of

2030, reduce the energy intensity by 10 and 15% within the year 2020 and 2030 respectively,

reduce the landfills by 75 and 100% within the 2020 and 2030 respectively, reduce the fresh

water use by 25% and 30% within the 2020 and 2030 respectively (Alcoa, 2017). All of these

approaches from the Alcoa side show that the company is serious about the environmental

issues and takes effective steps to reduce the impact.

‘Yellow rock resources limited’ do not produce any of such information. In the annual report

of 2015 the organisation says that currently the organisation does not come under any such

regulations. But the long time sustainability of the business is one important thing (Brueckner

et al., 2013). The benchmarking organisation takes a long term position in the business and

its operation. Considering this ‘Yellow rock resources limited’ must also follow those

approaches of environmental measures. Currently this mining sector is having some problems

and there is serious profitability pressure on the organisations. Alcoa is also having problem

in the profitability matter of the business operation but they are following the environmental

responsibility of the business for the long term sustainability. The profitability position of

‘Yellow rock resources limited’ is much worse than Alcoa. Currently the organisation is not

coming under any direction legislative obligation of the environmental matters

(australianvanadium.com.au, 2017). Considering this the business must take effective steps

for the improvement of the profitability position of the business. At the same time the

business must also make a long term commitment for the environmental matters. A diligent

effort in this context from now would help the business to keep low environmental impact in

the long run (Fonseca, 2010). Alcoa is trying to reverse the process by reducing the

environmental impacts whereas ‘Yellow rock resources limited’ can take effective step to

11

from its operation in the year 2015 (asx.com.au, 2015). The organisation got into the

‘Aluminium stewardship initiative’ for the sustainable standard for the aluminium sector in

the world. In the annual report of 2016 the organisation mentions the reduction level of

carbon emission by 6 million mt tons. So it is clear that the business is continuously putting

effort in this context. This report further mentions the reduction of energy intensity by 1%,

consumption of water by around nineteen million m3 and landfill related waste by 86.5k mt

tons (viewmaterial, 2016). The organisation also develops product line called SUSTANA

which are basically based on the recycled material and low carbon emitting process. The

website of the company shows the target for the company in this regard. The organisation

target is to reduce the carbon emission by 30% within 2020 and 35% within completion of

2030, reduce the energy intensity by 10 and 15% within the year 2020 and 2030 respectively,

reduce the landfills by 75 and 100% within the 2020 and 2030 respectively, reduce the fresh

water use by 25% and 30% within the 2020 and 2030 respectively (Alcoa, 2017). All of these

approaches from the Alcoa side show that the company is serious about the environmental

issues and takes effective steps to reduce the impact.

‘Yellow rock resources limited’ do not produce any of such information. In the annual report

of 2015 the organisation says that currently the organisation does not come under any such

regulations. But the long time sustainability of the business is one important thing (Brueckner

et al., 2013). The benchmarking organisation takes a long term position in the business and

its operation. Considering this ‘Yellow rock resources limited’ must also follow those

approaches of environmental measures. Currently this mining sector is having some problems

and there is serious profitability pressure on the organisations. Alcoa is also having problem

in the profitability matter of the business operation but they are following the environmental

responsibility of the business for the long term sustainability. The profitability position of

‘Yellow rock resources limited’ is much worse than Alcoa. Currently the organisation is not

coming under any direction legislative obligation of the environmental matters

(australianvanadium.com.au, 2017). Considering this the business must take effective steps

for the improvement of the profitability position of the business. At the same time the

business must also make a long term commitment for the environmental matters. A diligent

effort in this context from now would help the business to keep low environmental impact in

the long run (Fonseca, 2010). Alcoa is trying to reverse the process by reducing the

environmental impacts whereas ‘Yellow rock resources limited’ can take effective step to

11

keep those environmental impacts at minimum level from now. This would reduce the

requirement of large investment for the organisation to control the standards. Environment is

one of the main challenges that the businesses worldwide are facing and that is why the

businesses need to make long term strategy in this context.

Conclusion:

The study of the financial statements of the company YRR via ratio analysis and the

comparison of those ratios with that of Alcoa reveals the fact that the company is not only

failed to generate any net profit over the investments made by the company, but the

performance of the company is much behind compared to the benchmark standards of the

Aluminium exploration industry in which it is operating (Beck et al., 2008). The main reason

behind this poor performance can be identified (as revealed by the application of the tools of

ratio analysis) as the operational inefficiency of the company.

To improve the financial performance of the company the following recommendations can be

made:

The company should identify each department and operations that are absorbing the

maximum cash expenditure out of the total expenditure of the company

The company should judge the rationality of that expenditure to promote control &

savings of resources (Brigham and Ehrhardt, 2013).

The company should develop and intelligent framework of investment so that it can

invest the liquid assets in hand for earning good profit.

12

requirement of large investment for the organisation to control the standards. Environment is

one of the main challenges that the businesses worldwide are facing and that is why the

businesses need to make long term strategy in this context.

Conclusion:

The study of the financial statements of the company YRR via ratio analysis and the

comparison of those ratios with that of Alcoa reveals the fact that the company is not only

failed to generate any net profit over the investments made by the company, but the

performance of the company is much behind compared to the benchmark standards of the

Aluminium exploration industry in which it is operating (Beck et al., 2008). The main reason

behind this poor performance can be identified (as revealed by the application of the tools of

ratio analysis) as the operational inefficiency of the company.

To improve the financial performance of the company the following recommendations can be

made:

The company should identify each department and operations that are absorbing the

maximum cash expenditure out of the total expenditure of the company

The company should judge the rationality of that expenditure to promote control &

savings of resources (Brigham and Ehrhardt, 2013).

The company should develop and intelligent framework of investment so that it can

invest the liquid assets in hand for earning good profit.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.