Financial Performance Analysis of Australian Vintage Limited (2019)

VerifiedAdded on 2022/08/23

|18

|2875

|14

Report

AI Summary

This report presents a comprehensive financial analysis of Australian Vintage Limited (AVL) for the year 2019, as required by the Accounting Essentials for Decision Making course. The analysis encompasses a detailed examination of AVL's financial performance through various financial ratios, including profitability, asset efficiency, liquidity, financial gearing, and investment ratios. The report calculates and interprets these ratios, comparing them to previous years and industry benchmarks to assess AVL's financial health and operational effectiveness. It evaluates AVL's performance, highlighting trends and providing insights into the company's strengths and weaknesses. Furthermore, the report provides recommendations based on the ratio analysis and overall financial assessment, offering a concluding perspective on AVL's financial standing and future prospects. The report is a student contribution, available on Desklib, a platform offering AI-based study tools for students.

Running head: ACCOUNTING ESSENTIALS FOR DECISION MAKING

Accounting Essentials for Decision Making

Name of the Student

Name of the University

Authors Note

Course ID

Accounting Essentials for Decision Making

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING ESSENTIALS FOR DECISION MAKING

Table of Contents

Introduction:...............................................................................................................................2

Evaluation of Performance of the Company:.............................................................................2

Profitability Ratios:....................................................................................................................2

Gross Profit Ratio:..................................................................................................................2

Net profit Ratio:.....................................................................................................................3

Return on Equity:...................................................................................................................3

Return on Assets:...................................................................................................................4

Asset efficiency ratio:................................................................................................................5

Asset Turnover Ratio:............................................................................................................5

Inventory Turnover Ratio:......................................................................................................5

Days Sales in Inventory:........................................................................................................6

Accounts Receivable Turnover Ratio:...................................................................................6

Liquidity Ratios:.........................................................................................................................7

Current Ratio:.........................................................................................................................7

Quick Ratio:...........................................................................................................................8

Cash Ratio:.............................................................................................................................8

Financial Gearing Ratio:............................................................................................................9

Times Interest Earned Ratio:..................................................................................................9

Debt to Equity Ratio:...........................................................................................................10

Debt Ratio:...........................................................................................................................10

Table of Contents

Introduction:...............................................................................................................................2

Evaluation of Performance of the Company:.............................................................................2

Profitability Ratios:....................................................................................................................2

Gross Profit Ratio:..................................................................................................................2

Net profit Ratio:.....................................................................................................................3

Return on Equity:...................................................................................................................3

Return on Assets:...................................................................................................................4

Asset efficiency ratio:................................................................................................................5

Asset Turnover Ratio:............................................................................................................5

Inventory Turnover Ratio:......................................................................................................5

Days Sales in Inventory:........................................................................................................6

Accounts Receivable Turnover Ratio:...................................................................................6

Liquidity Ratios:.........................................................................................................................7

Current Ratio:.........................................................................................................................7

Quick Ratio:...........................................................................................................................8

Cash Ratio:.............................................................................................................................8

Financial Gearing Ratio:............................................................................................................9

Times Interest Earned Ratio:..................................................................................................9

Debt to Equity Ratio:...........................................................................................................10

Debt Ratio:...........................................................................................................................10

2ACCOUNTING ESSENTIALS FOR DECISION MAKING

Equity Ratio:........................................................................................................................10

Investment Ratios:....................................................................................................................11

Price Earnings P/E:..............................................................................................................11

Earnings per share:...............................................................................................................12

Dividend Pay-out Ratio:.......................................................................................................12

Dividend Yield Ratio:..........................................................................................................12

Recommendations:...................................................................................................................13

Conclusion:..............................................................................................................................14

References:...............................................................................................................................15

Equity Ratio:........................................................................................................................10

Investment Ratios:....................................................................................................................11

Price Earnings P/E:..............................................................................................................11

Earnings per share:...............................................................................................................12

Dividend Pay-out Ratio:.......................................................................................................12

Dividend Yield Ratio:..........................................................................................................12

Recommendations:...................................................................................................................13

Conclusion:..............................................................................................................................14

References:...............................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING ESSENTIALS FOR DECISION MAKING

Introduction:

Ratio analysis can be defined as the quantitative process of obtaining an insight in the

liquidity position, operational effectiveness and profitability by examining its financial

statements. Investors normally make use of ratio analysis to examine the financial health of

the organization by scrutinizing past and present financial statements (No 2018). The current

report is based on evaluating the financial performance Australian Vintage Limited for the

year 2019.

Australian Vintage Limited is one of the world’s leading international wine producing

company one of the largest wine producers in Australia. The company is at the fore front in

Australian wine industry with approximately 7% of the yearly production in Australia

(Australian Vintage Limited 2020). Diversity in wine producing methods and regionality

enables wine producing team to be the leader in innovation and in the formation of wide

range of wine styles as well as varieties.

Evaluation of Performance of the Company:

Profitability Ratios:

The profitability ratios are useful in comparing the income statement accounts and

categories to demonstrate an organization’s ability to produce profits from its operations

(Schroeder, Clark and Cathey 2019). This ratio emphasizes on an organization’s return on

investment and other assets.

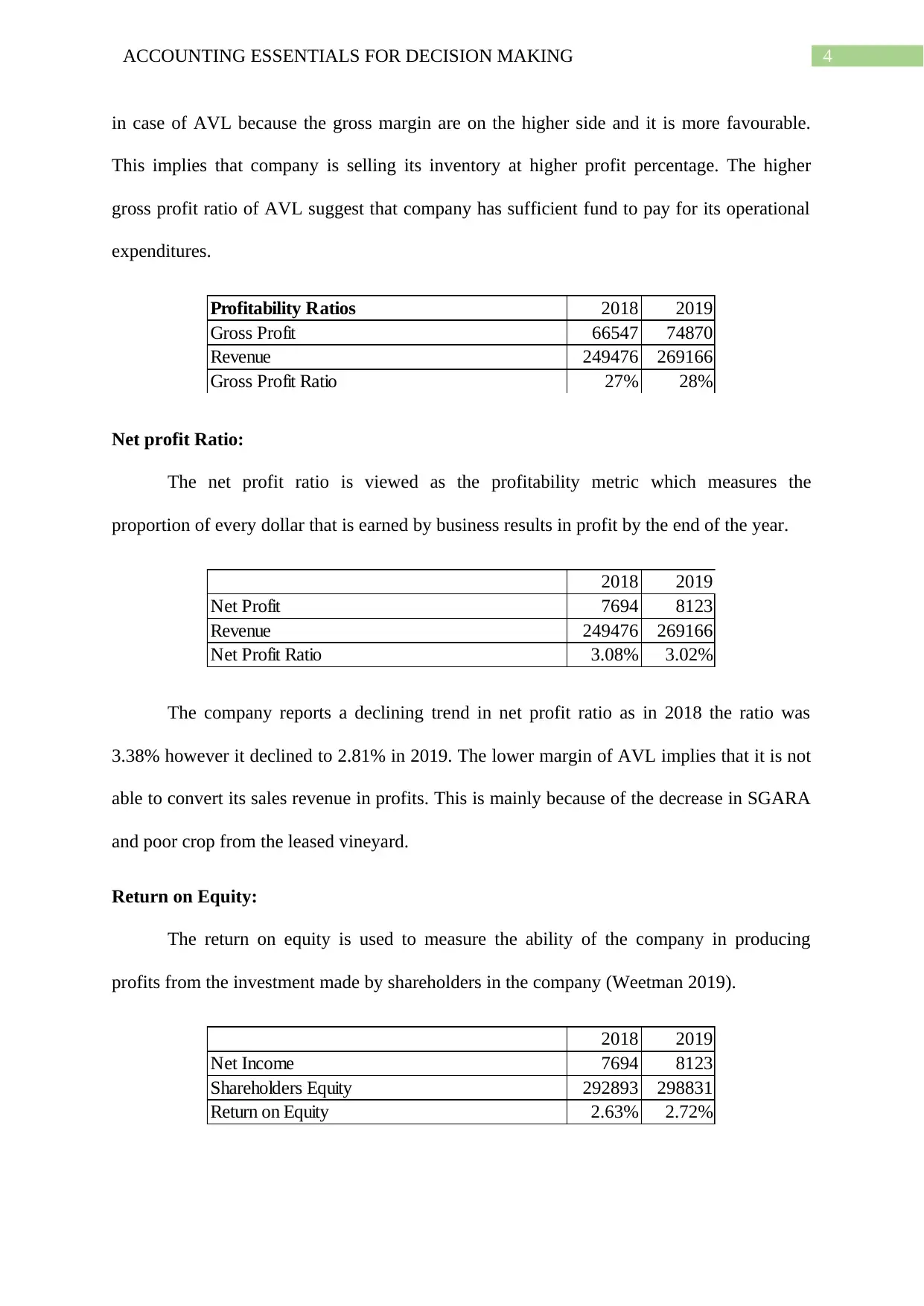

Gross Profit Ratio:

The gross profit ratio measures the amount of profit a company produces following

the deduction of its cost of revenues (Henderson et al. 2015). As evident the gross profit of

AVL in 2018 stood 27% while in 2019 it increased marginally to 28%. The ratio makes sense

Introduction:

Ratio analysis can be defined as the quantitative process of obtaining an insight in the

liquidity position, operational effectiveness and profitability by examining its financial

statements. Investors normally make use of ratio analysis to examine the financial health of

the organization by scrutinizing past and present financial statements (No 2018). The current

report is based on evaluating the financial performance Australian Vintage Limited for the

year 2019.

Australian Vintage Limited is one of the world’s leading international wine producing

company one of the largest wine producers in Australia. The company is at the fore front in

Australian wine industry with approximately 7% of the yearly production in Australia

(Australian Vintage Limited 2020). Diversity in wine producing methods and regionality

enables wine producing team to be the leader in innovation and in the formation of wide

range of wine styles as well as varieties.

Evaluation of Performance of the Company:

Profitability Ratios:

The profitability ratios are useful in comparing the income statement accounts and

categories to demonstrate an organization’s ability to produce profits from its operations

(Schroeder, Clark and Cathey 2019). This ratio emphasizes on an organization’s return on

investment and other assets.

Gross Profit Ratio:

The gross profit ratio measures the amount of profit a company produces following

the deduction of its cost of revenues (Henderson et al. 2015). As evident the gross profit of

AVL in 2018 stood 27% while in 2019 it increased marginally to 28%. The ratio makes sense

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING ESSENTIALS FOR DECISION MAKING

in case of AVL because the gross margin are on the higher side and it is more favourable.

This implies that company is selling its inventory at higher profit percentage. The higher

gross profit ratio of AVL suggest that company has sufficient fund to pay for its operational

expenditures.

Profitability Ratios 2018 2019

Gross Profit 66547 74870

Revenue 249476 269166

Gross Profit Ratio 27% 28%

Net profit Ratio:

The net profit ratio is viewed as the profitability metric which measures the

proportion of every dollar that is earned by business results in profit by the end of the year.

2018 2019

Net Profit 7694 8123

Revenue 249476 269166

Net Profit Ratio 3.08% 3.02%

The company reports a declining trend in net profit ratio as in 2018 the ratio was

3.38% however it declined to 2.81% in 2019. The lower margin of AVL implies that it is not

able to convert its sales revenue in profits. This is mainly because of the decrease in SGARA

and poor crop from the leased vineyard.

Return on Equity:

The return on equity is used to measure the ability of the company in producing

profits from the investment made by shareholders in the company (Weetman 2019).

2018 2019

Net Income 7694 8123

Shareholders Equity 292893 298831

Return on Equity 2.63% 2.72%

in case of AVL because the gross margin are on the higher side and it is more favourable.

This implies that company is selling its inventory at higher profit percentage. The higher

gross profit ratio of AVL suggest that company has sufficient fund to pay for its operational

expenditures.

Profitability Ratios 2018 2019

Gross Profit 66547 74870

Revenue 249476 269166

Gross Profit Ratio 27% 28%

Net profit Ratio:

The net profit ratio is viewed as the profitability metric which measures the

proportion of every dollar that is earned by business results in profit by the end of the year.

2018 2019

Net Profit 7694 8123

Revenue 249476 269166

Net Profit Ratio 3.08% 3.02%

The company reports a declining trend in net profit ratio as in 2018 the ratio was

3.38% however it declined to 2.81% in 2019. The lower margin of AVL implies that it is not

able to convert its sales revenue in profits. This is mainly because of the decrease in SGARA

and poor crop from the leased vineyard.

Return on Equity:

The return on equity is used to measure the ability of the company in producing

profits from the investment made by shareholders in the company (Weetman 2019).

2018 2019

Net Income 7694 8123

Shareholders Equity 292893 298831

Return on Equity 2.63% 2.72%

5ACCOUNTING ESSENTIALS FOR DECISION MAKING

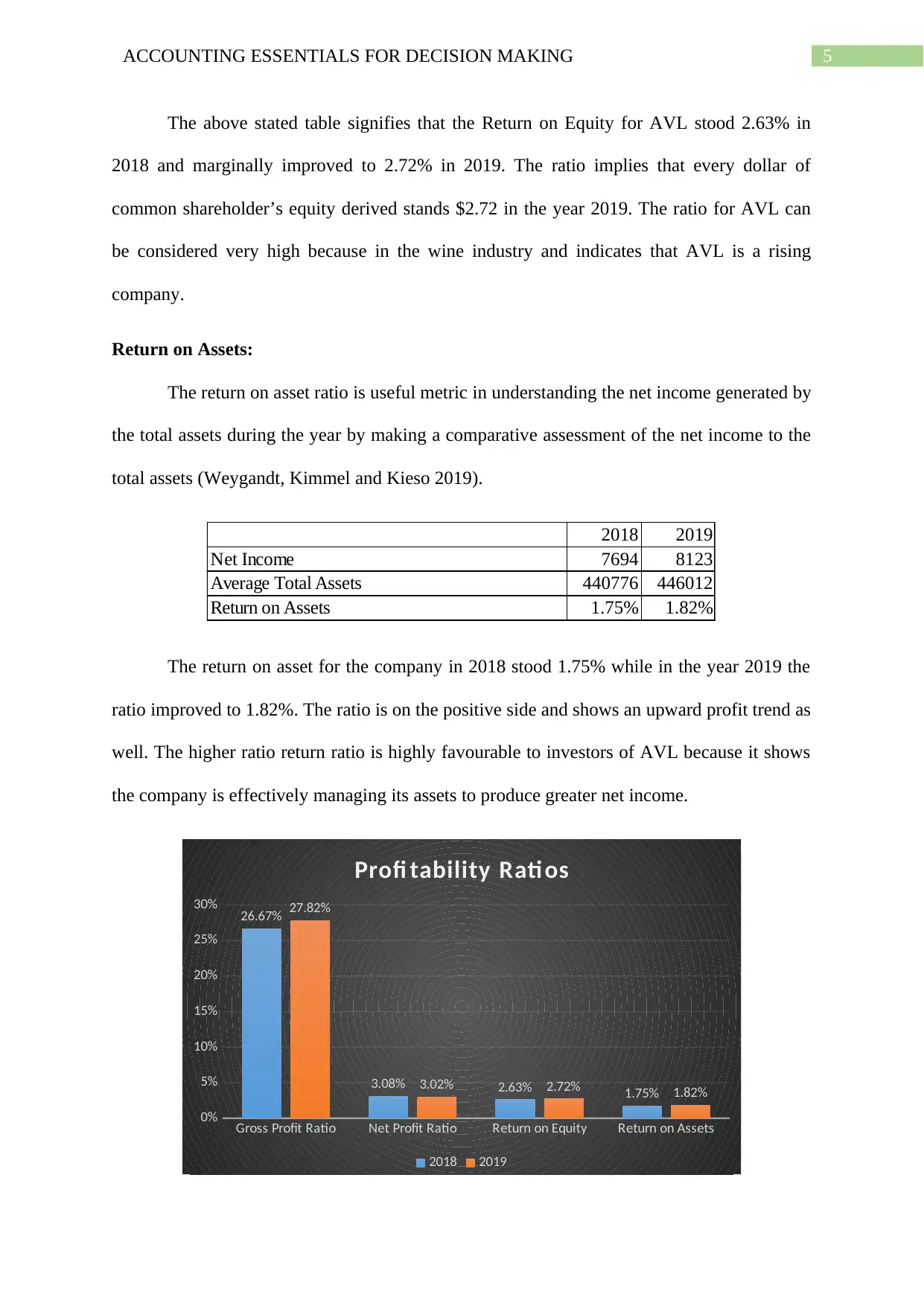

The above stated table signifies that the Return on Equity for AVL stood 2.63% in

2018 and marginally improved to 2.72% in 2019. The ratio implies that every dollar of

common shareholder’s equity derived stands $2.72 in the year 2019. The ratio for AVL can

be considered very high because in the wine industry and indicates that AVL is a rising

company.

Return on Assets:

The return on asset ratio is useful metric in understanding the net income generated by

the total assets during the year by making a comparative assessment of the net income to the

total assets (Weygandt, Kimmel and Kieso 2019).

2018 2019

Net Income 7694 8123

Average Total Assets 440776 446012

Return on Assets 1.75% 1.82%

The return on asset for the company in 2018 stood 1.75% while in the year 2019 the

ratio improved to 1.82%. The ratio is on the positive side and shows an upward profit trend as

well. The higher ratio return ratio is highly favourable to investors of AVL because it shows

the company is effectively managing its assets to produce greater net income.

Gross Profit Ratio Net Profit Ratio Return on Equity Return on Assets

0%

5%

10%

15%

20%

25%

30% 26.67%

3.08% 2.63% 1.75%

27.82%

3.02% 2.72% 1.82%

Profi tability Rati os

2018 2019

The above stated table signifies that the Return on Equity for AVL stood 2.63% in

2018 and marginally improved to 2.72% in 2019. The ratio implies that every dollar of

common shareholder’s equity derived stands $2.72 in the year 2019. The ratio for AVL can

be considered very high because in the wine industry and indicates that AVL is a rising

company.

Return on Assets:

The return on asset ratio is useful metric in understanding the net income generated by

the total assets during the year by making a comparative assessment of the net income to the

total assets (Weygandt, Kimmel and Kieso 2019).

2018 2019

Net Income 7694 8123

Average Total Assets 440776 446012

Return on Assets 1.75% 1.82%

The return on asset for the company in 2018 stood 1.75% while in the year 2019 the

ratio improved to 1.82%. The ratio is on the positive side and shows an upward profit trend as

well. The higher ratio return ratio is highly favourable to investors of AVL because it shows

the company is effectively managing its assets to produce greater net income.

Gross Profit Ratio Net Profit Ratio Return on Equity Return on Assets

0%

5%

10%

15%

20%

25%

30% 26.67%

3.08% 2.63% 1.75%

27.82%

3.02% 2.72% 1.82%

Profi tability Rati os

2018 2019

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING ESSENTIALS FOR DECISION MAKING

Asset efficiency ratio:

This efficiency ratio measures the ability of the company to produce sales from its

asset by comparing the net sales with the average total assets (Narayanaswamy 2017).

Asset Turnover Ratio:

The asset turnover ratio is useful in measuring the ability of the company in producing

sales from its asset by comparing net sales with the average total assets (Warren and Jones

2018).

Asset Efficiency Ratios 2018 2019

Net Sales 249476 269166

Average Total Assets 440776 446012

Asset Turnover Ratio 0.57 0.60

The asset turnover ratio in 2018 stood 0.57 while in 2019 it increased to 0.60. The

ratio is below the benchmark of 1 and implies that the company is not using its asset in an

effective manner (Nilsson and Stockenstrand 2015). AVL is most likely facing production

problems and the investors or creditors that company is not being managed well.

Inventory Turnover Ratio:

The inventory turnover ratio is regarded as the efficiency ratio to portray how

effectively the inventory is managed in comparison with the cost of goods sold with average

inventory for the year.

Asset efficiency ratio:

This efficiency ratio measures the ability of the company to produce sales from its

asset by comparing the net sales with the average total assets (Narayanaswamy 2017).

Asset Turnover Ratio:

The asset turnover ratio is useful in measuring the ability of the company in producing

sales from its asset by comparing net sales with the average total assets (Warren and Jones

2018).

Asset Efficiency Ratios 2018 2019

Net Sales 249476 269166

Average Total Assets 440776 446012

Asset Turnover Ratio 0.57 0.60

The asset turnover ratio in 2018 stood 0.57 while in 2019 it increased to 0.60. The

ratio is below the benchmark of 1 and implies that the company is not using its asset in an

effective manner (Nilsson and Stockenstrand 2015). AVL is most likely facing production

problems and the investors or creditors that company is not being managed well.

Inventory Turnover Ratio:

The inventory turnover ratio is regarded as the efficiency ratio to portray how

effectively the inventory is managed in comparison with the cost of goods sold with average

inventory for the year.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING ESSENTIALS FOR DECISION MAKING

2018 2019

Cost of Goods Sold 182929 194296

Average Inventory 139882 156346

Inventory Turnover Ratio 1.31 1.24

The inventory turnover in 2018 of AVL stood 1.31 times while in 2019 it stood 1.24

times. The ratio shows that AVL is not overspending to purchase larger amount of inventory

and wastes resources by storing the non-saleable inventory. AVL is effectively selling its

inventory which it buys and completes the entire inventory in one turn.

Days Sales in Inventory:

This ratio measures the number of days a company would take to sell all its inventory.

The ratio shows the number of days an organization’s current stock would last.

2018 2019

Closing Inventory 139882 156346

Cost of Goods Sold 182929 194296

Total Days in a Year 365 365

Days Sales in Inventory 279.11 293.71

The calculation done above shows that in 2018 AVL took approximately 279 days to

sell all of its inventory while in 2019 it marginally increased to 293 days. As evident the ratio

in 2019 is 293 days this implies that AVL has satisfactory inventories to turn its inventory in

cash.

Accounts Receivable Turnover Ratio:

The accounts receivable turnover ratio is regarded as an efficiency ratio which

assesses the number of times an organization can turn its cash during the year (Trucco 2016).

2018 2019

Sales 249476 269166

Accounts Receivables 47546 49357

Accounts Receivables Turnover Ratio 5.25 5.45

2018 2019

Cost of Goods Sold 182929 194296

Average Inventory 139882 156346

Inventory Turnover Ratio 1.31 1.24

The inventory turnover in 2018 of AVL stood 1.31 times while in 2019 it stood 1.24

times. The ratio shows that AVL is not overspending to purchase larger amount of inventory

and wastes resources by storing the non-saleable inventory. AVL is effectively selling its

inventory which it buys and completes the entire inventory in one turn.

Days Sales in Inventory:

This ratio measures the number of days a company would take to sell all its inventory.

The ratio shows the number of days an organization’s current stock would last.

2018 2019

Closing Inventory 139882 156346

Cost of Goods Sold 182929 194296

Total Days in a Year 365 365

Days Sales in Inventory 279.11 293.71

The calculation done above shows that in 2018 AVL took approximately 279 days to

sell all of its inventory while in 2019 it marginally increased to 293 days. As evident the ratio

in 2019 is 293 days this implies that AVL has satisfactory inventories to turn its inventory in

cash.

Accounts Receivable Turnover Ratio:

The accounts receivable turnover ratio is regarded as an efficiency ratio which

assesses the number of times an organization can turn its cash during the year (Trucco 2016).

2018 2019

Sales 249476 269166

Accounts Receivables 47546 49357

Accounts Receivables Turnover Ratio 5.25 5.45

8ACCOUNTING ESSENTIALS FOR DECISION MAKING

The above stated computation shows that AVL in 2018 reported the accounts

receivable ratio of 5.25 times while in 2019 it increased marginally to stand at 5.45 times. As

evident from the turnover AVL collects its receivables about 5.45 times in a year or once in

66 days to collect the cash from its sale.

Asset Efficiency

Ratios Asset Turnover

Ratio Inventory

Turnover Ratio Days Sales in

Inventory Accounts

Receivables

Turnover Ratio

2018.00

0.57 1.31

279.11

5.25

2019.00

0.60 1.24

293.71

5.45

Asset Efficiency Ratio

Series1 Series2

Figure 2: Figure Showing Asset Efficiency Ratios

(Source: As Created by Author)

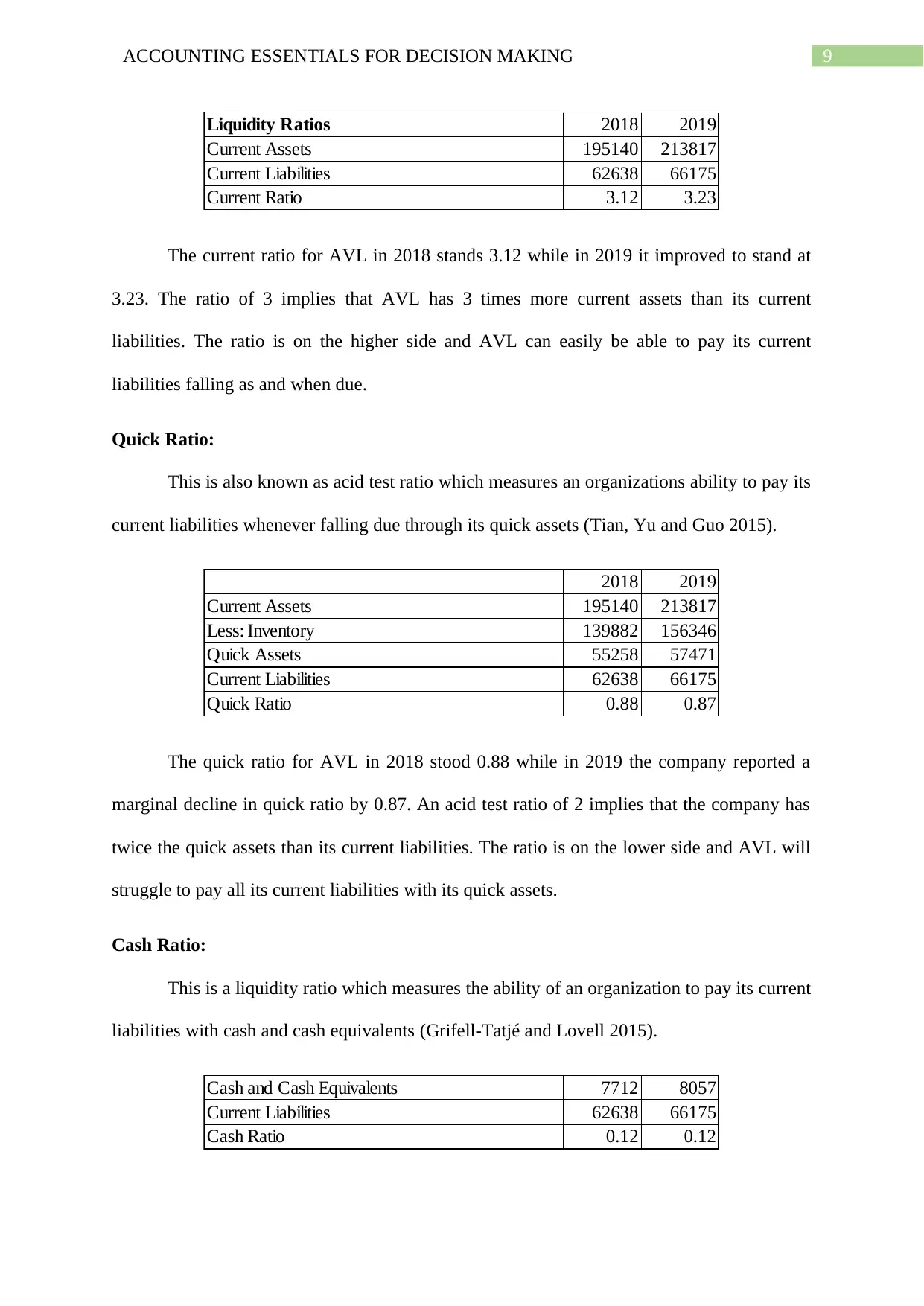

Liquidity Ratios:

This ratio is regarded as the noteworthy class of ratio which assesses the ability of the

debtor to pay its current obligations relating to debts without raising any external capital

(Liang et al. 2016).

Current Ratio:

This ratio is useful in assessing an organizations ability to pay its short-term debt

obligations through its current assets.

The above stated computation shows that AVL in 2018 reported the accounts

receivable ratio of 5.25 times while in 2019 it increased marginally to stand at 5.45 times. As

evident from the turnover AVL collects its receivables about 5.45 times in a year or once in

66 days to collect the cash from its sale.

Asset Efficiency

Ratios Asset Turnover

Ratio Inventory

Turnover Ratio Days Sales in

Inventory Accounts

Receivables

Turnover Ratio

2018.00

0.57 1.31

279.11

5.25

2019.00

0.60 1.24

293.71

5.45

Asset Efficiency Ratio

Series1 Series2

Figure 2: Figure Showing Asset Efficiency Ratios

(Source: As Created by Author)

Liquidity Ratios:

This ratio is regarded as the noteworthy class of ratio which assesses the ability of the

debtor to pay its current obligations relating to debts without raising any external capital

(Liang et al. 2016).

Current Ratio:

This ratio is useful in assessing an organizations ability to pay its short-term debt

obligations through its current assets.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING ESSENTIALS FOR DECISION MAKING

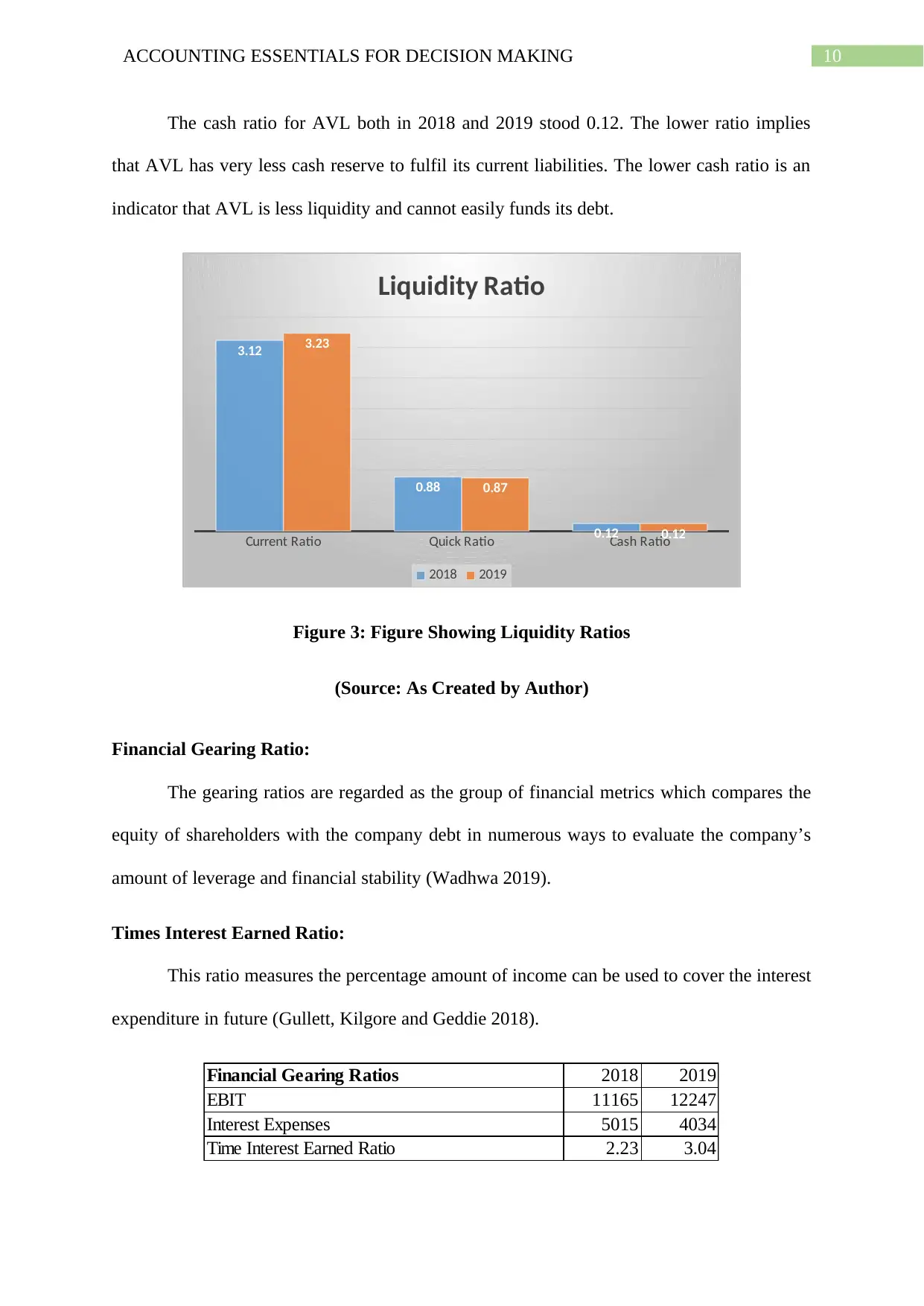

Liquidity Ratios 2018 2019

Current Assets 195140 213817

Current Liabilities 62638 66175

Current Ratio 3.12 3.23

The current ratio for AVL in 2018 stands 3.12 while in 2019 it improved to stand at

3.23. The ratio of 3 implies that AVL has 3 times more current assets than its current

liabilities. The ratio is on the higher side and AVL can easily be able to pay its current

liabilities falling as and when due.

Quick Ratio:

This is also known as acid test ratio which measures an organizations ability to pay its

current liabilities whenever falling due through its quick assets (Tian, Yu and Guo 2015).

2018 2019

Current Assets 195140 213817

Less: Inventory 139882 156346

Quick Assets 55258 57471

Current Liabilities 62638 66175

Quick Ratio 0.88 0.87

The quick ratio for AVL in 2018 stood 0.88 while in 2019 the company reported a

marginal decline in quick ratio by 0.87. An acid test ratio of 2 implies that the company has

twice the quick assets than its current liabilities. The ratio is on the lower side and AVL will

struggle to pay all its current liabilities with its quick assets.

Cash Ratio:

This is a liquidity ratio which measures the ability of an organization to pay its current

liabilities with cash and cash equivalents (Grifell-Tatjé and Lovell 2015).

Cash and Cash Equivalents 7712 8057

Current Liabilities 62638 66175

Cash Ratio 0.12 0.12

Liquidity Ratios 2018 2019

Current Assets 195140 213817

Current Liabilities 62638 66175

Current Ratio 3.12 3.23

The current ratio for AVL in 2018 stands 3.12 while in 2019 it improved to stand at

3.23. The ratio of 3 implies that AVL has 3 times more current assets than its current

liabilities. The ratio is on the higher side and AVL can easily be able to pay its current

liabilities falling as and when due.

Quick Ratio:

This is also known as acid test ratio which measures an organizations ability to pay its

current liabilities whenever falling due through its quick assets (Tian, Yu and Guo 2015).

2018 2019

Current Assets 195140 213817

Less: Inventory 139882 156346

Quick Assets 55258 57471

Current Liabilities 62638 66175

Quick Ratio 0.88 0.87

The quick ratio for AVL in 2018 stood 0.88 while in 2019 the company reported a

marginal decline in quick ratio by 0.87. An acid test ratio of 2 implies that the company has

twice the quick assets than its current liabilities. The ratio is on the lower side and AVL will

struggle to pay all its current liabilities with its quick assets.

Cash Ratio:

This is a liquidity ratio which measures the ability of an organization to pay its current

liabilities with cash and cash equivalents (Grifell-Tatjé and Lovell 2015).

Cash and Cash Equivalents 7712 8057

Current Liabilities 62638 66175

Cash Ratio 0.12 0.12

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING ESSENTIALS FOR DECISION MAKING

The cash ratio for AVL both in 2018 and 2019 stood 0.12. The lower ratio implies

that AVL has very less cash reserve to fulfil its current liabilities. The lower cash ratio is an

indicator that AVL is less liquidity and cannot easily funds its debt.

Current Ratio Quick Ratio Cash Ratio

3.12

0.88

0.12

3.23

0.87

0.12

Liquidity Ratio

2018 2019

Figure 3: Figure Showing Liquidity Ratios

(Source: As Created by Author)

Financial Gearing Ratio:

The gearing ratios are regarded as the group of financial metrics which compares the

equity of shareholders with the company debt in numerous ways to evaluate the company’s

amount of leverage and financial stability (Wadhwa 2019).

Times Interest Earned Ratio:

This ratio measures the percentage amount of income can be used to cover the interest

expenditure in future (Gullett, Kilgore and Geddie 2018).

Financial Gearing Ratios 2018 2019

EBIT 11165 12247

Interest Expenses 5015 4034

Time Interest Earned Ratio 2.23 3.04

The cash ratio for AVL both in 2018 and 2019 stood 0.12. The lower ratio implies

that AVL has very less cash reserve to fulfil its current liabilities. The lower cash ratio is an

indicator that AVL is less liquidity and cannot easily funds its debt.

Current Ratio Quick Ratio Cash Ratio

3.12

0.88

0.12

3.23

0.87

0.12

Liquidity Ratio

2018 2019

Figure 3: Figure Showing Liquidity Ratios

(Source: As Created by Author)

Financial Gearing Ratio:

The gearing ratios are regarded as the group of financial metrics which compares the

equity of shareholders with the company debt in numerous ways to evaluate the company’s

amount of leverage and financial stability (Wadhwa 2019).

Times Interest Earned Ratio:

This ratio measures the percentage amount of income can be used to cover the interest

expenditure in future (Gullett, Kilgore and Geddie 2018).

Financial Gearing Ratios 2018 2019

EBIT 11165 12247

Interest Expenses 5015 4034

Time Interest Earned Ratio 2.23 3.04

11ACCOUNTING ESSENTIALS FOR DECISION MAKING

AVL reported times interest ratio of 2.23 in 2018 while in 2019 it increased to 3.04.

As evident the business as a ratio of 3.04 times in 2019 which means that its income is 3

times greater than its yearly interest expenditure. AVL can afford to pay the additional

interest expenses. The business of AVL is moderately risky.

Debt to Equity Ratio:

This ratio compares the company’s total debt to its total equity.

Total Debt 77226 72378

Total Equity 292893 298831

Debt To Equity Ratio 0.26 0.24

The debt ratio f AVL is less than 1 which means that the company is financially a

stable business. The ratio of 0.24 in 2019 implies that the investors owns 76 cents of each

dollar of AVL assets while creditors only 24 cents on the its assets.

Debt Ratio:

This ratio measures a company’s total liabilities as the percentage of its total assets.

2018 2019

Total Liabilities 147883 147181

Total Asset 440776 446012

Debt Ratio 0.34 0.33

The debt ratio for AVL is low and this means that AVL is more stable business that has the

potential of longevity since the lower ratio suggest a lower overall burden of debt on the

AVL.

Equity Ratio:

The ratio is useful in measuring the total amount of asset which is financed by the

investment of owners by comparing the total equity in an organization to its total assets

(Trucco 2016).

AVL reported times interest ratio of 2.23 in 2018 while in 2019 it increased to 3.04.

As evident the business as a ratio of 3.04 times in 2019 which means that its income is 3

times greater than its yearly interest expenditure. AVL can afford to pay the additional

interest expenses. The business of AVL is moderately risky.

Debt to Equity Ratio:

This ratio compares the company’s total debt to its total equity.

Total Debt 77226 72378

Total Equity 292893 298831

Debt To Equity Ratio 0.26 0.24

The debt ratio f AVL is less than 1 which means that the company is financially a

stable business. The ratio of 0.24 in 2019 implies that the investors owns 76 cents of each

dollar of AVL assets while creditors only 24 cents on the its assets.

Debt Ratio:

This ratio measures a company’s total liabilities as the percentage of its total assets.

2018 2019

Total Liabilities 147883 147181

Total Asset 440776 446012

Debt Ratio 0.34 0.33

The debt ratio for AVL is low and this means that AVL is more stable business that has the

potential of longevity since the lower ratio suggest a lower overall burden of debt on the

AVL.

Equity Ratio:

The ratio is useful in measuring the total amount of asset which is financed by the

investment of owners by comparing the total equity in an organization to its total assets

(Trucco 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.