Financial Analysis: Automotive Sector Risk and Capital Structure

VerifiedAdded on 2020/06/04

|17

|5966

|76

Report

AI Summary

This report provides a comprehensive financial analysis of four automotive companies: Genuine Parts Company, Daimler, Brembo, and Continental. It begins with an assessment of each company's risk profile using beta analysis, examining factors influencing stock price fluctuations and the impact of market index returns. The report then delves into the capital structure of each company, evaluating debt-to-equity ratios, weighted average cost of capital (WACC), and whether each firm is under- or over-leveraged. Furthermore, the analysis includes an examination of dividend policies and an assessment of each firm's value using free cash flow techniques. The report aims to determine which automotive company demonstrates superior financial performance across these key metrics.

ACF

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

A) Risk profile of the firm and sources of risk.......................................................................1

B) Analysis of Capital structure.............................................................................................3

C Examining dividend policy.................................................................................................6

D) Analysing value of the firm...............................................................................................8

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

A) Risk profile of the firm and sources of risk.......................................................................1

B) Analysis of Capital structure.............................................................................................3

C Examining dividend policy.................................................................................................6

D) Analysing value of the firm...............................................................................................8

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................13

INTRODUCTION

In the present times, investors lay high level of emphasis on doing risk and return

evaluation with the motive to generate high return from funds invested. Dividend is recognized

as income which investors earn by investing money in the shares of different firms. Capital

structure of the company is highly significant which in turn renders information about the extent

to which solvency position of the company is good. In accordance with the theoretical

framework pertaining to capital structure firms need to issue 2 equities in against to 1 debt. This

in turn helps in reducing the level of fixed obligation and enables to get tax benefits. In this, four

companies have been selected from automotive sector namely Genuine Parts company, Daimler,

Brembo and Continental. Hence, this report will shed light on the capital structure of selected

business units and helps in determining whether they are under over leveraged. It also highlights

risk profile of the business unit through regression analysis. Report will also provide deeper

insight about the dividend policies of all four business units undertaken for investigation

purpose. Besides this, report also entails the value of firm by taking into account the technique of

free cash flows. Hence, it helps in assessing automotive company which is performing better

over others.

A) Risk profile of the firm and sources of risk

Beta is the most effectual measure which assists in measuring changes takes place in

stock in relation to the overall market. This value provides help in determining and evaluating

expected rate of return pertaining to stock (Damodaran, 2016). In this, for assessing and getting

information about volatility or risk level beta value is calculated. Positive beta value presents

that, stock will move in the similar direction as per stock market.

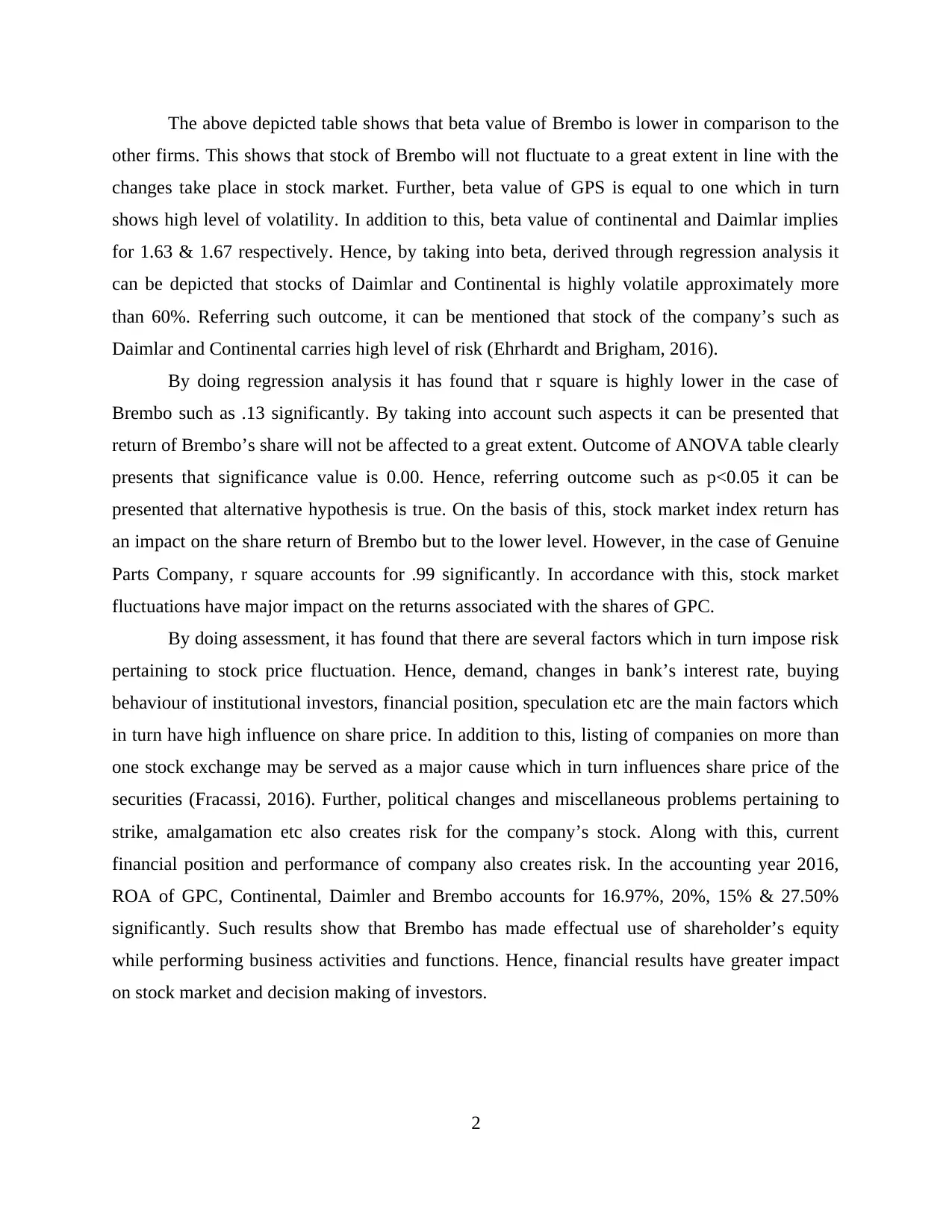

Risk profile of the selected companies belongs from automotive sector is as follows:

Name of the companies Beta

Daimlar 1.67

Continental 1.63

Brembo 0.90

Genuine Parts company 1.00

1

In the present times, investors lay high level of emphasis on doing risk and return

evaluation with the motive to generate high return from funds invested. Dividend is recognized

as income which investors earn by investing money in the shares of different firms. Capital

structure of the company is highly significant which in turn renders information about the extent

to which solvency position of the company is good. In accordance with the theoretical

framework pertaining to capital structure firms need to issue 2 equities in against to 1 debt. This

in turn helps in reducing the level of fixed obligation and enables to get tax benefits. In this, four

companies have been selected from automotive sector namely Genuine Parts company, Daimler,

Brembo and Continental. Hence, this report will shed light on the capital structure of selected

business units and helps in determining whether they are under over leveraged. It also highlights

risk profile of the business unit through regression analysis. Report will also provide deeper

insight about the dividend policies of all four business units undertaken for investigation

purpose. Besides this, report also entails the value of firm by taking into account the technique of

free cash flows. Hence, it helps in assessing automotive company which is performing better

over others.

A) Risk profile of the firm and sources of risk

Beta is the most effectual measure which assists in measuring changes takes place in

stock in relation to the overall market. This value provides help in determining and evaluating

expected rate of return pertaining to stock (Damodaran, 2016). In this, for assessing and getting

information about volatility or risk level beta value is calculated. Positive beta value presents

that, stock will move in the similar direction as per stock market.

Risk profile of the selected companies belongs from automotive sector is as follows:

Name of the companies Beta

Daimlar 1.67

Continental 1.63

Brembo 0.90

Genuine Parts company 1.00

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The above depicted table shows that beta value of Brembo is lower in comparison to the

other firms. This shows that stock of Brembo will not fluctuate to a great extent in line with the

changes take place in stock market. Further, beta value of GPS is equal to one which in turn

shows high level of volatility. In addition to this, beta value of continental and Daimlar implies

for 1.63 & 1.67 respectively. Hence, by taking into beta, derived through regression analysis it

can be depicted that stocks of Daimlar and Continental is highly volatile approximately more

than 60%. Referring such outcome, it can be mentioned that stock of the company’s such as

Daimlar and Continental carries high level of risk (Ehrhardt and Brigham, 2016).

By doing regression analysis it has found that r square is highly lower in the case of

Brembo such as .13 significantly. By taking into account such aspects it can be presented that

return of Brembo’s share will not be affected to a great extent. Outcome of ANOVA table clearly

presents that significance value is 0.00. Hence, referring outcome such as p<0.05 it can be

presented that alternative hypothesis is true. On the basis of this, stock market index return has

an impact on the share return of Brembo but to the lower level. However, in the case of Genuine

Parts Company, r square accounts for .99 significantly. In accordance with this, stock market

fluctuations have major impact on the returns associated with the shares of GPC.

By doing assessment, it has found that there are several factors which in turn impose risk

pertaining to stock price fluctuation. Hence, demand, changes in bank’s interest rate, buying

behaviour of institutional investors, financial position, speculation etc are the main factors which

in turn have high influence on share price. In addition to this, listing of companies on more than

one stock exchange may be served as a major cause which in turn influences share price of the

securities (Fracassi, 2016). Further, political changes and miscellaneous problems pertaining to

strike, amalgamation etc also creates risk for the company’s stock. Along with this, current

financial position and performance of company also creates risk. In the accounting year 2016,

ROA of GPC, Continental, Daimler and Brembo accounts for 16.97%, 20%, 15% & 27.50%

significantly. Such results show that Brembo has made effectual use of shareholder’s equity

while performing business activities and functions. Hence, financial results have greater impact

on stock market and decision making of investors.

2

other firms. This shows that stock of Brembo will not fluctuate to a great extent in line with the

changes take place in stock market. Further, beta value of GPS is equal to one which in turn

shows high level of volatility. In addition to this, beta value of continental and Daimlar implies

for 1.63 & 1.67 respectively. Hence, by taking into beta, derived through regression analysis it

can be depicted that stocks of Daimlar and Continental is highly volatile approximately more

than 60%. Referring such outcome, it can be mentioned that stock of the company’s such as

Daimlar and Continental carries high level of risk (Ehrhardt and Brigham, 2016).

By doing regression analysis it has found that r square is highly lower in the case of

Brembo such as .13 significantly. By taking into account such aspects it can be presented that

return of Brembo’s share will not be affected to a great extent. Outcome of ANOVA table clearly

presents that significance value is 0.00. Hence, referring outcome such as p<0.05 it can be

presented that alternative hypothesis is true. On the basis of this, stock market index return has

an impact on the share return of Brembo but to the lower level. However, in the case of Genuine

Parts Company, r square accounts for .99 significantly. In accordance with this, stock market

fluctuations have major impact on the returns associated with the shares of GPC.

By doing assessment, it has found that there are several factors which in turn impose risk

pertaining to stock price fluctuation. Hence, demand, changes in bank’s interest rate, buying

behaviour of institutional investors, financial position, speculation etc are the main factors which

in turn have high influence on share price. In addition to this, listing of companies on more than

one stock exchange may be served as a major cause which in turn influences share price of the

securities (Fracassi, 2016). Further, political changes and miscellaneous problems pertaining to

strike, amalgamation etc also creates risk for the company’s stock. Along with this, current

financial position and performance of company also creates risk. In the accounting year 2016,

ROA of GPC, Continental, Daimler and Brembo accounts for 16.97%, 20%, 15% & 27.50%

significantly. Such results show that Brembo has made effectual use of shareholder’s equity

while performing business activities and functions. Hence, financial results have greater impact

on stock market and decision making of investors.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

B) Analysis of Capital structure

Capital structure plays important role in financing activities of the business in effective

way. It means that organisation should have adequate mix of debt and equity so that it may be

able to finance tasks quite easily. This is important as if more of equity is used by the company

in the capital structure, shareholders will seek for higher returns and as such, more dividends will

have to paid by the company. On the other hand, if more of debt is used then, repayment

liabilities increases which is not good for the firm (Lerner and Seru, 2017). The main reason

behind is that business becomes obliged to repay the debt amount along with the interest accrued

on it. Thus, by analysing this, it is required that optimal capital structure should be implemented

to carry out activities and as such, having balanced structure of debt and equity is essentially

required for easily finance operational tasks and achieve higher value in the market.

Optimal capital structure is the one which in turn includes suitable mix of debt and

equity. Moreover, in the case of shares business unit offers dividend when it generates enough

returns. On the other side, under debt sources, company has to pay interest when it becomes due

irrespective of the aspect that profit is generated during the accounting year or not. Along with

this, high interest payment also increases the level of expenses and thereby affects profitability

aspect (Dang, Li and Yang, 2018). Hence, at the time of raising funds firm should focus on

maintaining ideal ratio such as .5:1. Trade off theory pertaining to capital structure presents that

firm should ensure proper integration between debt and equity while taking decision in relation

to raising funds. On the basis of this, optimal structure includes trade off between interest tax

shield and cost of financial distress.

Value of firm = Value if all-equity financed + PV (tax shield) – PV (cost of financial distress)

3

Capital structure plays important role in financing activities of the business in effective

way. It means that organisation should have adequate mix of debt and equity so that it may be

able to finance tasks quite easily. This is important as if more of equity is used by the company

in the capital structure, shareholders will seek for higher returns and as such, more dividends will

have to paid by the company. On the other hand, if more of debt is used then, repayment

liabilities increases which is not good for the firm (Lerner and Seru, 2017). The main reason

behind is that business becomes obliged to repay the debt amount along with the interest accrued

on it. Thus, by analysing this, it is required that optimal capital structure should be implemented

to carry out activities and as such, having balanced structure of debt and equity is essentially

required for easily finance operational tasks and achieve higher value in the market.

Optimal capital structure is the one which in turn includes suitable mix of debt and

equity. Moreover, in the case of shares business unit offers dividend when it generates enough

returns. On the other side, under debt sources, company has to pay interest when it becomes due

irrespective of the aspect that profit is generated during the accounting year or not. Along with

this, high interest payment also increases the level of expenses and thereby affects profitability

aspect (Dang, Li and Yang, 2018). Hence, at the time of raising funds firm should focus on

maintaining ideal ratio such as .5:1. Trade off theory pertaining to capital structure presents that

firm should ensure proper integration between debt and equity while taking decision in relation

to raising funds. On the basis of this, optimal structure includes trade off between interest tax

shield and cost of financial distress.

Value of firm = Value if all-equity financed + PV (tax shield) – PV (cost of financial distress)

3

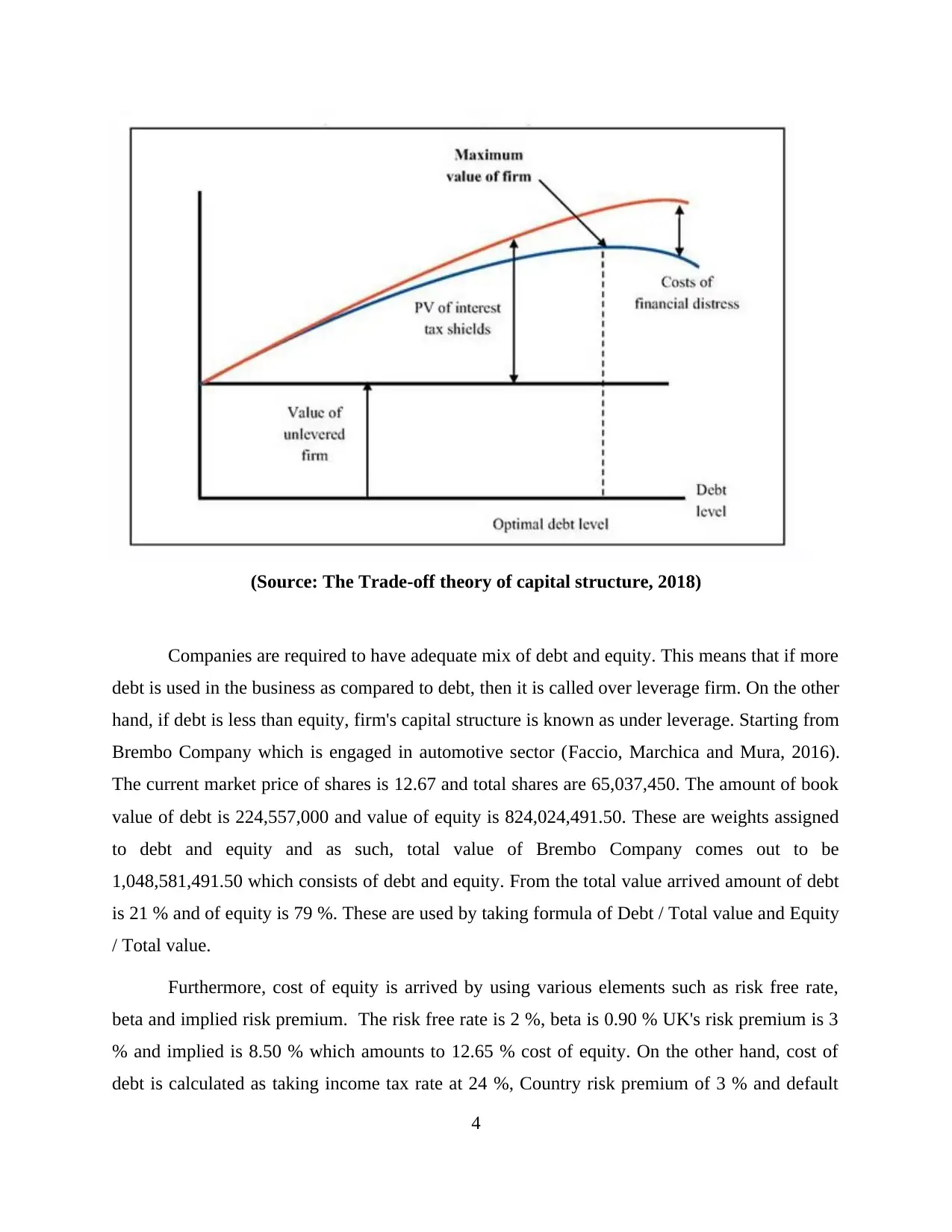

(Source: The Trade-off theory of capital structure, 2018)

Companies are required to have adequate mix of debt and equity. This means that if more

debt is used in the business as compared to debt, then it is called over leverage firm. On the other

hand, if debt is less than equity, firm's capital structure is known as under leverage. Starting from

Brembo Company which is engaged in automotive sector (Faccio, Marchica and Mura, 2016).

The current market price of shares is 12.67 and total shares are 65,037,450. The amount of book

value of debt is 224,557,000 and value of equity is 824,024,491.50. These are weights assigned

to debt and equity and as such, total value of Brembo Company comes out to be

1,048,581,491.50 which consists of debt and equity. From the total value arrived amount of debt

is 21 % and of equity is 79 %. These are used by taking formula of Debt / Total value and Equity

/ Total value.

Furthermore, cost of equity is arrived by using various elements such as risk free rate,

beta and implied risk premium. The risk free rate is 2 %, beta is 0.90 % UK's risk premium is 3

% and implied is 8.50 % which amounts to 12.65 % cost of equity. On the other hand, cost of

debt is calculated as taking income tax rate at 24 %, Country risk premium of 3 % and default

4

Companies are required to have adequate mix of debt and equity. This means that if more

debt is used in the business as compared to debt, then it is called over leverage firm. On the other

hand, if debt is less than equity, firm's capital structure is known as under leverage. Starting from

Brembo Company which is engaged in automotive sector (Faccio, Marchica and Mura, 2016).

The current market price of shares is 12.67 and total shares are 65,037,450. The amount of book

value of debt is 224,557,000 and value of equity is 824,024,491.50. These are weights assigned

to debt and equity and as such, total value of Brembo Company comes out to be

1,048,581,491.50 which consists of debt and equity. From the total value arrived amount of debt

is 21 % and of equity is 79 %. These are used by taking formula of Debt / Total value and Equity

/ Total value.

Furthermore, cost of equity is arrived by using various elements such as risk free rate,

beta and implied risk premium. The risk free rate is 2 %, beta is 0.90 % UK's risk premium is 3

% and implied is 8.50 % which amounts to 12.65 % cost of equity. On the other hand, cost of

debt is calculated as taking income tax rate at 24 %, Country risk premium of 3 % and default

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

spread 1.25 %. Thus, after tax cost of debt comes to 4.75 %. Thus, by using formula of WACC

(Weighted Average Cost of Capital), the value comes to 10.96 % by adding weights and cost of

debt and equity. D/ (D+E) ratio is 40.63 % which should be 30 %. It can be identified that there

is more equity than debt in the firm's capital structure, thus, Brembo Company is under leveraged

as debt is less in comparison to equity (Jacob, Johan, Schweizer and Zhan, 2016).

Another company is Continental Organisation engaged in automotive sector. The market

price of shares is 51.54 and outstanding shares are 200, 005,983. While book value of debt is

2,917,900,000 and current market value of equity is 10,308.31. This implies that total capital

structure consist of debt and equity comes out to be 2,917,910,308.31. Total value of equity by

multiplying outstanding shares and market price amounts to 10,308,308,563.83. On the other

hand, Continental Organisation total value by adding debt and equity is 13,226,208,563. Thus,

after arriving total firm's value, amount of debt is 22 % and of equity comes to 78 %.

On the other hand, cost of equity is arrived at taking risk free premium rate of 2.89 %,

beta is 1.63 and implied risk premium is 5.50 %. By applying the formula of Cost of equity

which implies Risk free rate + Beta * Implied risk, value arrived is 11.86 %. While, for

calculating cost of debt, there are various elements taken in this aspect. Such as income tax rate

is 35 % USA risk premium is 0, default spread is 3 %. Thus, by adding all these elements and

applicable formula, cost of debt is 3.83 %. With regards to this, adding debt and equity, WACC

comes out to be 10.09 %. D/ (D+E) ratio is 59.27 % which should be 80 %. It can be analysed

that firm is under leverage as optimum balance in capital structure is not present (Karolyi, 2016).

Daimler Group has outstanding shares of 1,069,800,000 and price of shares is 66.47.

Current market value of equity is 71,109.61 and book value of debt is 73,725. Total capital

structure turns out to be 144,834.61. It can be analysed that weight of Equity is 49 % and on the

other hand, weight of debt is 51 %. This clearly shows that firm has more debt than equity. On

the other hand, cost of equity is arrived as 12.08 % and cost of debt is 4.12 %. By summing up,

debt and equity, WACC comes out to be 8.03 % which is low as compared to other two firms

discussed in preceding paragraphs. D/ (D+E) ratio is 34.76 % which is low debt means company

is not utilising debt to finance activities. The debt is more than equity and as such, Daimler

Group has less equity. Thus, it is the over leveraged firm.

5

(Weighted Average Cost of Capital), the value comes to 10.96 % by adding weights and cost of

debt and equity. D/ (D+E) ratio is 40.63 % which should be 30 %. It can be identified that there

is more equity than debt in the firm's capital structure, thus, Brembo Company is under leveraged

as debt is less in comparison to equity (Jacob, Johan, Schweizer and Zhan, 2016).

Another company is Continental Organisation engaged in automotive sector. The market

price of shares is 51.54 and outstanding shares are 200, 005,983. While book value of debt is

2,917,900,000 and current market value of equity is 10,308.31. This implies that total capital

structure consist of debt and equity comes out to be 2,917,910,308.31. Total value of equity by

multiplying outstanding shares and market price amounts to 10,308,308,563.83. On the other

hand, Continental Organisation total value by adding debt and equity is 13,226,208,563. Thus,

after arriving total firm's value, amount of debt is 22 % and of equity comes to 78 %.

On the other hand, cost of equity is arrived at taking risk free premium rate of 2.89 %,

beta is 1.63 and implied risk premium is 5.50 %. By applying the formula of Cost of equity

which implies Risk free rate + Beta * Implied risk, value arrived is 11.86 %. While, for

calculating cost of debt, there are various elements taken in this aspect. Such as income tax rate

is 35 % USA risk premium is 0, default spread is 3 %. Thus, by adding all these elements and

applicable formula, cost of debt is 3.83 %. With regards to this, adding debt and equity, WACC

comes out to be 10.09 %. D/ (D+E) ratio is 59.27 % which should be 80 %. It can be analysed

that firm is under leverage as optimum balance in capital structure is not present (Karolyi, 2016).

Daimler Group has outstanding shares of 1,069,800,000 and price of shares is 66.47.

Current market value of equity is 71,109.61 and book value of debt is 73,725. Total capital

structure turns out to be 144,834.61. It can be analysed that weight of Equity is 49 % and on the

other hand, weight of debt is 51 %. This clearly shows that firm has more debt than equity. On

the other hand, cost of equity is arrived as 12.08 % and cost of debt is 4.12 %. By summing up,

debt and equity, WACC comes out to be 8.03 % which is low as compared to other two firms

discussed in preceding paragraphs. D/ (D+E) ratio is 34.76 % which is low debt means company

is not utilising debt to finance activities. The debt is more than equity and as such, Daimler

Group has less equity. Thus, it is the over leveraged firm.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Another firm is GPC (Genuine Parts Company) which has market price of shares is

149,804,000 and share price is 95.54. The current value of equity is 14,312,274,160 and on the

other hand, book value of debt is 1,018,058,000. Thus, total capital comes to 15,330,332,160.

Thus, weight of equity is 93 % and of debt is 7 %. This clearly shows that there is little part of

debt in the capital structure of GPC Company as compared to equity. Cost of equity is 8.95 %

and after tax cost of debt is 3.83 %. Thus, adding up these rates of debt and equity, WACC is

8.61 %. Furthermore, D/ (D+E) ratio is 63.80 % while it should be 50 % which means that the

ratio is high and it shows that firm may not be able to produce cash to satisfy its debt obligations.

Moreover, it can be interpreted that Daimler Group has more debt and as such, it is over leverage

firm (Frésard and Valta, 2016). While, Continental Company is under leverage firm and Brembo

Organisation is also under leveraged. On the other hand, GPC Company has very little amount of

debt and is highly under leveraged organisation.

Optimal capital structure

Companies WACC

Brembo Company 10.96%

Continental Company 10.09%

Daimler Group 8.03%

GPC Company 8.61%

6

149,804,000 and share price is 95.54. The current value of equity is 14,312,274,160 and on the

other hand, book value of debt is 1,018,058,000. Thus, total capital comes to 15,330,332,160.

Thus, weight of equity is 93 % and of debt is 7 %. This clearly shows that there is little part of

debt in the capital structure of GPC Company as compared to equity. Cost of equity is 8.95 %

and after tax cost of debt is 3.83 %. Thus, adding up these rates of debt and equity, WACC is

8.61 %. Furthermore, D/ (D+E) ratio is 63.80 % while it should be 50 % which means that the

ratio is high and it shows that firm may not be able to produce cash to satisfy its debt obligations.

Moreover, it can be interpreted that Daimler Group has more debt and as such, it is over leverage

firm (Frésard and Valta, 2016). While, Continental Company is under leverage firm and Brembo

Organisation is also under leveraged. On the other hand, GPC Company has very little amount of

debt and is highly under leveraged organisation.

Optimal capital structure

Companies WACC

Brembo Company 10.96%

Continental Company 10.09%

Daimler Group 8.03%

GPC Company 8.61%

6

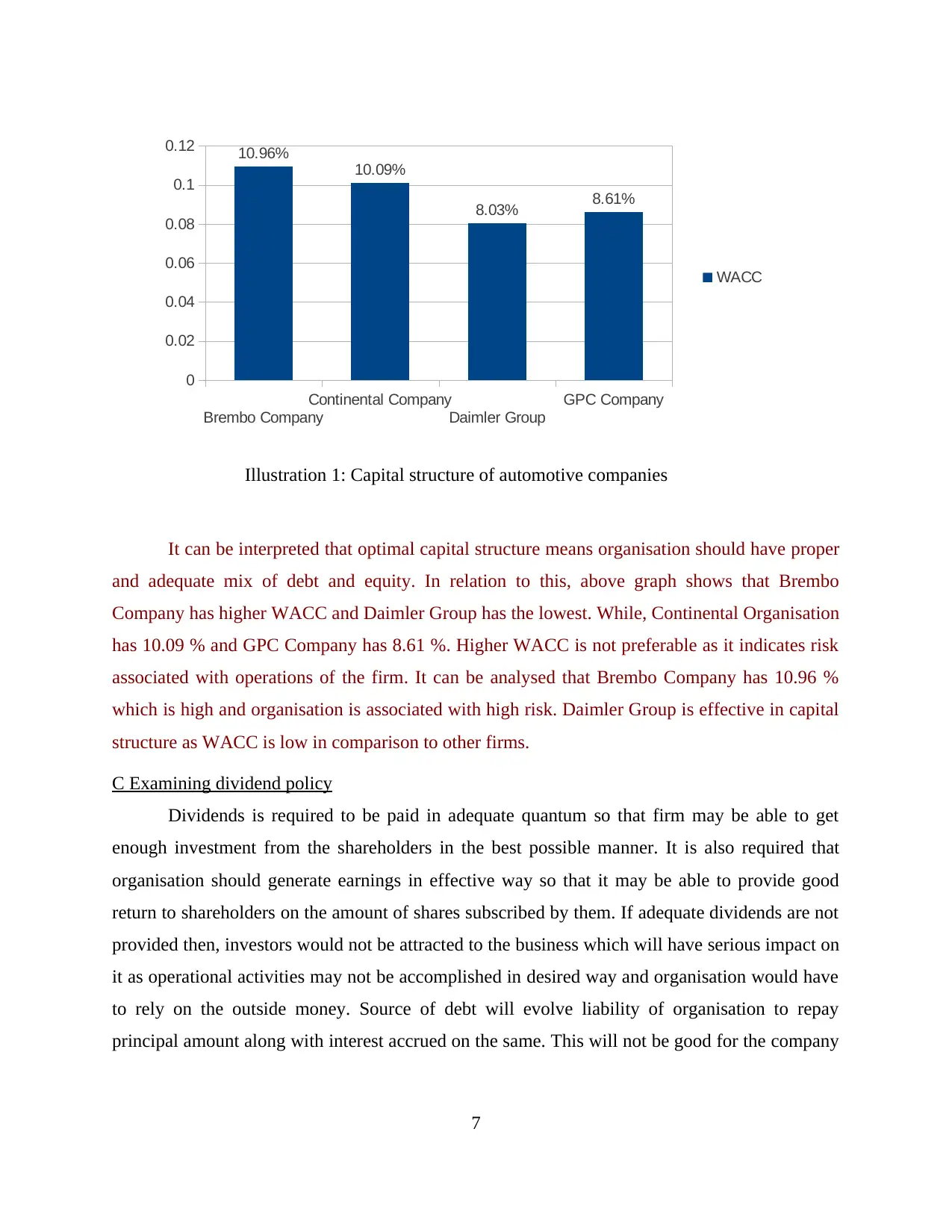

It can be interpreted that optimal capital structure means organisation should have proper

and adequate mix of debt and equity. In relation to this, above graph shows that Brembo

Company has higher WACC and Daimler Group has the lowest. While, Continental Organisation

has 10.09 % and GPC Company has 8.61 %. Higher WACC is not preferable as it indicates risk

associated with operations of the firm. It can be analysed that Brembo Company has 10.96 %

which is high and organisation is associated with high risk. Daimler Group is effective in capital

structure as WACC is low in comparison to other firms.

C Examining dividend policy

Dividends is required to be paid in adequate quantum so that firm may be able to get

enough investment from the shareholders in the best possible manner. It is also required that

organisation should generate earnings in effective way so that it may be able to provide good

return to shareholders on the amount of shares subscribed by them. If adequate dividends are not

provided then, investors would not be attracted to the business which will have serious impact on

it as operational activities may not be accomplished in desired way and organisation would have

to rely on the outside money. Source of debt will evolve liability of organisation to repay

principal amount along with interest accrued on the same. This will not be good for the company

7

Brembo Company

Continental Company

Daimler Group

GPC Company

0

0.02

0.04

0.06

0.08

0.1

0.12 10.96%

10.09%

8.03% 8.61%

WACC

Illustration 1: Capital structure of automotive companies

and adequate mix of debt and equity. In relation to this, above graph shows that Brembo

Company has higher WACC and Daimler Group has the lowest. While, Continental Organisation

has 10.09 % and GPC Company has 8.61 %. Higher WACC is not preferable as it indicates risk

associated with operations of the firm. It can be analysed that Brembo Company has 10.96 %

which is high and organisation is associated with high risk. Daimler Group is effective in capital

structure as WACC is low in comparison to other firms.

C Examining dividend policy

Dividends is required to be paid in adequate quantum so that firm may be able to get

enough investment from the shareholders in the best possible manner. It is also required that

organisation should generate earnings in effective way so that it may be able to provide good

return to shareholders on the amount of shares subscribed by them. If adequate dividends are not

provided then, investors would not be attracted to the business which will have serious impact on

it as operational activities may not be accomplished in desired way and organisation would have

to rely on the outside money. Source of debt will evolve liability of organisation to repay

principal amount along with interest accrued on the same. This will not be good for the company

7

Brembo Company

Continental Company

Daimler Group

GPC Company

0

0.02

0.04

0.06

0.08

0.1

0.12 10.96%

10.09%

8.03% 8.61%

WACC

Illustration 1: Capital structure of automotive companies

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

to rely more on debt as it increases risk to repay debt and lowers down solvency position of the

organisation.

In relation to this, Free Cash Flow to Firm (FCFF) and Free Cash Flow to Creditors

(FCFE). The company after considering FCFF and FCFE provides dividends to equity

shareholders (Ibrahim, Arif and Paino, 2017). FCFF means that total amount generated in cash

after paying out expenses, investments, taxes and as such, it measures organisation ability to

produce cash after making all such deductions in the best possible manner. Positive FCFF is

always preferable as it shows company has enough of cash for providing dividends to

shareholders. On the other hand, FCFE is the measure of financial performance of company

which shows amount left after paying expenses to creditors. From the left out amount, creditors

are paid.

FCFE (Free Cash Flow to Equity) is the difference between FCFF and FCFE. This is the

amount which is available to be paid to equity shareholders after paying money to creditors,

investments, taxes and expenditures. This is required cash flow which is to be paid to

shareholders on the shares subscribed by them (McCahery, Sautner and Starks, 2016). Starting

from Brembo Company which has good operating income in all the years and as such, FCFF is

quite effective in the years and are in positive. However, in 2011, FCFF is negative. The figures

are 0, -11818.40, 77826.16, 87043.52, 22316, 114564.44, 129969.64 from the years 2010 to

2016. It can be noted that FCFC is also arrived in the following years. After that, FCFE is

calculated by deducting the amount of expenses and as such, positive FCFE is generated in 2016

year amounts to 170354.12 in Euros.

It can be interpreted that from the total amount of 170354.12 of FCFE, dividends are paid

to shareholders of 52,030 and as such, cash surplus made is 118324.12. The dividend payout

ratio is 16 %. The company should pay more dividends by reducing the surplus amount so that

more stockholders may be attracted to the firm. Furthermore, it should initiate control on its

expenses so that enough of cash flows are generated to pay-off liabilities and as such, more

dividends may be paid.

Continental Company has generated operating income which are bit fluctuating in the

past. This means that organisation is unable to produce more profits and as a result, expenditures

needs to be controlled in a better way (Almamy, Aston and Ngwa, 2016). Furthermore, it is

required that firm should effectively utilise investments received from shareholders so that

8

organisation.

In relation to this, Free Cash Flow to Firm (FCFF) and Free Cash Flow to Creditors

(FCFE). The company after considering FCFF and FCFE provides dividends to equity

shareholders (Ibrahim, Arif and Paino, 2017). FCFF means that total amount generated in cash

after paying out expenses, investments, taxes and as such, it measures organisation ability to

produce cash after making all such deductions in the best possible manner. Positive FCFF is

always preferable as it shows company has enough of cash for providing dividends to

shareholders. On the other hand, FCFE is the measure of financial performance of company

which shows amount left after paying expenses to creditors. From the left out amount, creditors

are paid.

FCFE (Free Cash Flow to Equity) is the difference between FCFF and FCFE. This is the

amount which is available to be paid to equity shareholders after paying money to creditors,

investments, taxes and expenditures. This is required cash flow which is to be paid to

shareholders on the shares subscribed by them (McCahery, Sautner and Starks, 2016). Starting

from Brembo Company which has good operating income in all the years and as such, FCFF is

quite effective in the years and are in positive. However, in 2011, FCFF is negative. The figures

are 0, -11818.40, 77826.16, 87043.52, 22316, 114564.44, 129969.64 from the years 2010 to

2016. It can be noted that FCFC is also arrived in the following years. After that, FCFE is

calculated by deducting the amount of expenses and as such, positive FCFE is generated in 2016

year amounts to 170354.12 in Euros.

It can be interpreted that from the total amount of 170354.12 of FCFE, dividends are paid

to shareholders of 52,030 and as such, cash surplus made is 118324.12. The dividend payout

ratio is 16 %. The company should pay more dividends by reducing the surplus amount so that

more stockholders may be attracted to the firm. Furthermore, it should initiate control on its

expenses so that enough of cash flows are generated to pay-off liabilities and as such, more

dividends may be paid.

Continental Company has generated operating income which are bit fluctuating in the

past. This means that organisation is unable to produce more profits and as a result, expenditures

needs to be controlled in a better way (Almamy, Aston and Ngwa, 2016). Furthermore, it is

required that firm should effectively utilise investments received from shareholders so that

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

adequate income may be generated and company may earn desired profits with much ease.

Moreover, operating income is less and as such, FCFF is affected but the cash flows are positive

in the year 2016 and past years as well.

Moreover, FCFC is also calculated and after that FCFE is computed and value in 2016 is

3875.12. Thus, in relation to this, dividends paid are 755.6 in the financial year 2016. The cash

surplus comes out to be 3119.52 and common stock on per dividend paid is 4.25. Thus, dividend

paid out ratio is 26 %. Continental Company should pay fewer dividends to shareholders as there

is less operating income earned and as such, more cash can be utilised in the future course of

action. Thus, it should pay amount to creditors which are the main priorities to company.

Another company is GPC has operating income good operating income and as such,

FCFF is quite of the organisation. In this relation, FCFF in 2011 to 2016 are good of the firm.

Moreover, it can be said that firm is able to generate positive cash after paying out expenditures

with much ease. Furthermore, it implies that GPC Organisation has initiated overall control over

its expenses which has benefited firm in the best possible manner. After calculating FCFF and

FCFC, cash flows available to equity shareholders are computed. Furthermore, it can be analysed

that firm has good FCFE which are made available to equity shareholders of the company

(Dhaene, Hulle, Wuyts, Schoubben and Schoutens, 2017).

In relation to this, dividends are paid to stockholders which amounts to 386,863.

Moreover, dividend paid rate per common stock is 2.63. Thus, dividend paid out in the financial

year is 56 % which is more in comparison to other firms in the automotive sector. Furthermore, it

can be analysed that organisation has paid more dividends and as such, shareholders are

benefited as they have provided with more returns. However, GPC Company should pay fewer

dividends and use the remaining amount for financing future activities.

Next organisation is Daimler Group which has less operating income in the past years.

This is the main reason by which cash flows available to firm are low but they are positive. It is

required that company should control its expenditures and as such, income may be enhanced and

FCFF can be improved up to higher extent. It can be interpreted that organisation is able to have

positive cash flows but the position can be improved in the near future.

Furthermore, after calculating FCFF and FCFC, remaining is provided to equity

shareholders (Adhikari and Agrawal, 2016). FCFE taken out to be 2992.60 in the financial year

2016. This shows that company has less cash generated in 2016. Furthermore, there are no

9

Moreover, operating income is less and as such, FCFF is affected but the cash flows are positive

in the year 2016 and past years as well.

Moreover, FCFC is also calculated and after that FCFE is computed and value in 2016 is

3875.12. Thus, in relation to this, dividends paid are 755.6 in the financial year 2016. The cash

surplus comes out to be 3119.52 and common stock on per dividend paid is 4.25. Thus, dividend

paid out ratio is 26 %. Continental Company should pay fewer dividends to shareholders as there

is less operating income earned and as such, more cash can be utilised in the future course of

action. Thus, it should pay amount to creditors which are the main priorities to company.

Another company is GPC has operating income good operating income and as such,

FCFF is quite of the organisation. In this relation, FCFF in 2011 to 2016 are good of the firm.

Moreover, it can be said that firm is able to generate positive cash after paying out expenditures

with much ease. Furthermore, it implies that GPC Organisation has initiated overall control over

its expenses which has benefited firm in the best possible manner. After calculating FCFF and

FCFC, cash flows available to equity shareholders are computed. Furthermore, it can be analysed

that firm has good FCFE which are made available to equity shareholders of the company

(Dhaene, Hulle, Wuyts, Schoubben and Schoutens, 2017).

In relation to this, dividends are paid to stockholders which amounts to 386,863.

Moreover, dividend paid rate per common stock is 2.63. Thus, dividend paid out in the financial

year is 56 % which is more in comparison to other firms in the automotive sector. Furthermore, it

can be analysed that organisation has paid more dividends and as such, shareholders are

benefited as they have provided with more returns. However, GPC Company should pay fewer

dividends and use the remaining amount for financing future activities.

Next organisation is Daimler Group which has less operating income in the past years.

This is the main reason by which cash flows available to firm are low but they are positive. It is

required that company should control its expenditures and as such, income may be enhanced and

FCFF can be improved up to higher extent. It can be interpreted that organisation is able to have

positive cash flows but the position can be improved in the near future.

Furthermore, after calculating FCFF and FCFC, remaining is provided to equity

shareholders (Adhikari and Agrawal, 2016). FCFE taken out to be 2992.60 in the financial year

2016. This shows that company has less cash generated in 2016. Furthermore, there are no

9

dividends paid in the year which is because of less amount available in FCFE. Thus, there no

dividends available to be paid to shareholders. Moreover, it can be said that firm is required to

control upon its expenses by which organisation can earn revenue in the best possible manner.

D) Analysing value of the firm

Automotive Companies Total Value (Debt + Equity)

Brembo Company 1048581491.5

Continental Company 13226208563.83

Daimler Group 144834.61

GPC Organisation 15330332160

The above table shows value of all firms consisting of mix of debt and equity. It means

that value of firms are required to be ascertain so that investors may be able to take enhanced

decision whether to provide funds to the company or should invest in the same. Furthermore,

valuation help organisation to ascertain whether present value is good in the market or certain

improvements are required to be made. This will help organisation to evaluate and assess

valuation in the best possible manner. Furthermore, it is essential to value company as

stakeholders requires making effective and enhanced decisions with much ease (Huang, Tan and

Faff, 2016).

The valuation is important from the point of creditors as they assess whether funds should

be provided to the company or not. By having increased value of the firm, market value of shares

are injected and as a result, it is a good sign for the organisation as enhancement in market share

is maximised. Moreover, if organisation has more valuation, it indicates that company has

enough funds to finance activities in the best possible manner. This shows about good financial

performance of the company and as such, growth is achieved in effective way.

Furthermore, valuation of firm is needed for many other purposes such as investment

analysis, capital budgeting and financial reporting as well. Tax authorities also require valuation

of the firm so that proper tax filing can be made and organisation pay-off its tax liability with

much ease. Furthermore, valuing of firm is essentially required in order to ascertain that

company may analyse whether it should rely more on debt or equity. Moreover, proper mix of

10

dividends available to be paid to shareholders. Moreover, it can be said that firm is required to

control upon its expenses by which organisation can earn revenue in the best possible manner.

D) Analysing value of the firm

Automotive Companies Total Value (Debt + Equity)

Brembo Company 1048581491.5

Continental Company 13226208563.83

Daimler Group 144834.61

GPC Organisation 15330332160

The above table shows value of all firms consisting of mix of debt and equity. It means

that value of firms are required to be ascertain so that investors may be able to take enhanced

decision whether to provide funds to the company or should invest in the same. Furthermore,

valuation help organisation to ascertain whether present value is good in the market or certain

improvements are required to be made. This will help organisation to evaluate and assess

valuation in the best possible manner. Furthermore, it is essential to value company as

stakeholders requires making effective and enhanced decisions with much ease (Huang, Tan and

Faff, 2016).

The valuation is important from the point of creditors as they assess whether funds should

be provided to the company or not. By having increased value of the firm, market value of shares

are injected and as a result, it is a good sign for the organisation as enhancement in market share

is maximised. Moreover, if organisation has more valuation, it indicates that company has

enough funds to finance activities in the best possible manner. This shows about good financial

performance of the company and as such, growth is achieved in effective way.

Furthermore, valuation of firm is needed for many other purposes such as investment

analysis, capital budgeting and financial reporting as well. Tax authorities also require valuation

of the firm so that proper tax filing can be made and organisation pay-off its tax liability with

much ease. Furthermore, valuing of firm is essentially required in order to ascertain that

company may analyse whether it should rely more on debt or equity. Moreover, proper mix of

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.