Comprehensive Analysis of Aveo Ltd's Capital Structure and Dividends

VerifiedAdded on 2020/03/16

|13

|2592

|269

Report

AI Summary

This report provides a comprehensive analysis of Aveo Ltd's capital structure and dividend policy over a five-year period. It examines the company's debt-to-equity ratio, evaluating its financial health and stability. The analysis delves into Aveo's dividend history, discussing arguments for and against dividend distribution and its impact on shareholders. The report also explores the concept of optimal capital structure, considering the influence of taxes and the company's overall financial attractiveness to investors. It highlights the importance of financial decisions in maximizing company value, emphasizing the interplay between capital structure, dividend policy, and investment strategies. The report references financial models and principles, such as Modigliani and Miller's theory, to provide a detailed understanding of Aveo's financial performance and its implications for investors. The report also discusses the attractiveness of Aveo to investors considering aspects such as profitability, liquidity and company stability. The report concludes by discussing the dividend payment process.

1

Name:

Course

Professor’s name

University name

City, State

Date of submission

Name:

Course

Professor’s name

University name

City, State

Date of submission

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Table of Contents

Introduction......................................................................................................................................1

Capital structure of Aveo in the past 5 years...................................................................................1

Optimum capital structure............................................................................................................3

b. Dividend history and policy.........................................................................................................4

Arguments in favor of the distribution of dividends....................................................................5

Pay-out.........................................................................................................................................5

Dividend history for the past 5 years...........................................................................................6

Conclusion.......................................................................................................................................8

References........................................................................................................................................9

Table of Contents

Introduction......................................................................................................................................1

Capital structure of Aveo in the past 5 years...................................................................................1

Optimum capital structure............................................................................................................3

b. Dividend history and policy.........................................................................................................4

Arguments in favor of the distribution of dividends....................................................................5

Pay-out.........................................................................................................................................5

Dividend history for the past 5 years...........................................................................................6

Conclusion.......................................................................................................................................8

References........................................................................................................................................9

3

Introduction

The most important decision that is made within a company in the quest to maximize its value is

usually the decision on which products to manufacture and / or which services to offer, however,

the decision on how to finance the investments in those assets that allow offering such products

and / or services (eg in machines and equipment), is often seen as a minor or secondary decision

(Miglo, n.d.). This paper intends to emphasize the importance that financing decisions can have

on the value of a company, without forgetting that the expected results will depend considerably

on the assumptions that are made about the capital markets and the agents that operate in these

markets.

The capital structure of a business is the combination of debt and capital that an organization

uses to

Capital structure of Aveo in the past 5 years

It is time to review how the capital structure of a firm behaves in the presence of taxes. To that

end, we will continue to use the theoretical framework that Modigliani and Miller developed in

his article: The Cost of Capital, Corporation Finance and the Theory of Investment published in

1958 (Bena and Hanousek, 2006).

With a very strong balance sheet, the investors look at various things in the balance sheet to

invest in the company. There are two measurements for evaluating a company’s strength. The

Introduction

The most important decision that is made within a company in the quest to maximize its value is

usually the decision on which products to manufacture and / or which services to offer, however,

the decision on how to finance the investments in those assets that allow offering such products

and / or services (eg in machines and equipment), is often seen as a minor or secondary decision

(Miglo, n.d.). This paper intends to emphasize the importance that financing decisions can have

on the value of a company, without forgetting that the expected results will depend considerably

on the assumptions that are made about the capital markets and the agents that operate in these

markets.

The capital structure of a business is the combination of debt and capital that an organization

uses to

Capital structure of Aveo in the past 5 years

It is time to review how the capital structure of a firm behaves in the presence of taxes. To that

end, we will continue to use the theoretical framework that Modigliani and Miller developed in

his article: The Cost of Capital, Corporation Finance and the Theory of Investment published in

1958 (Bena and Hanousek, 2006).

With a very strong balance sheet, the investors look at various things in the balance sheet to

invest in the company. There are two measurements for evaluating a company’s strength. The

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

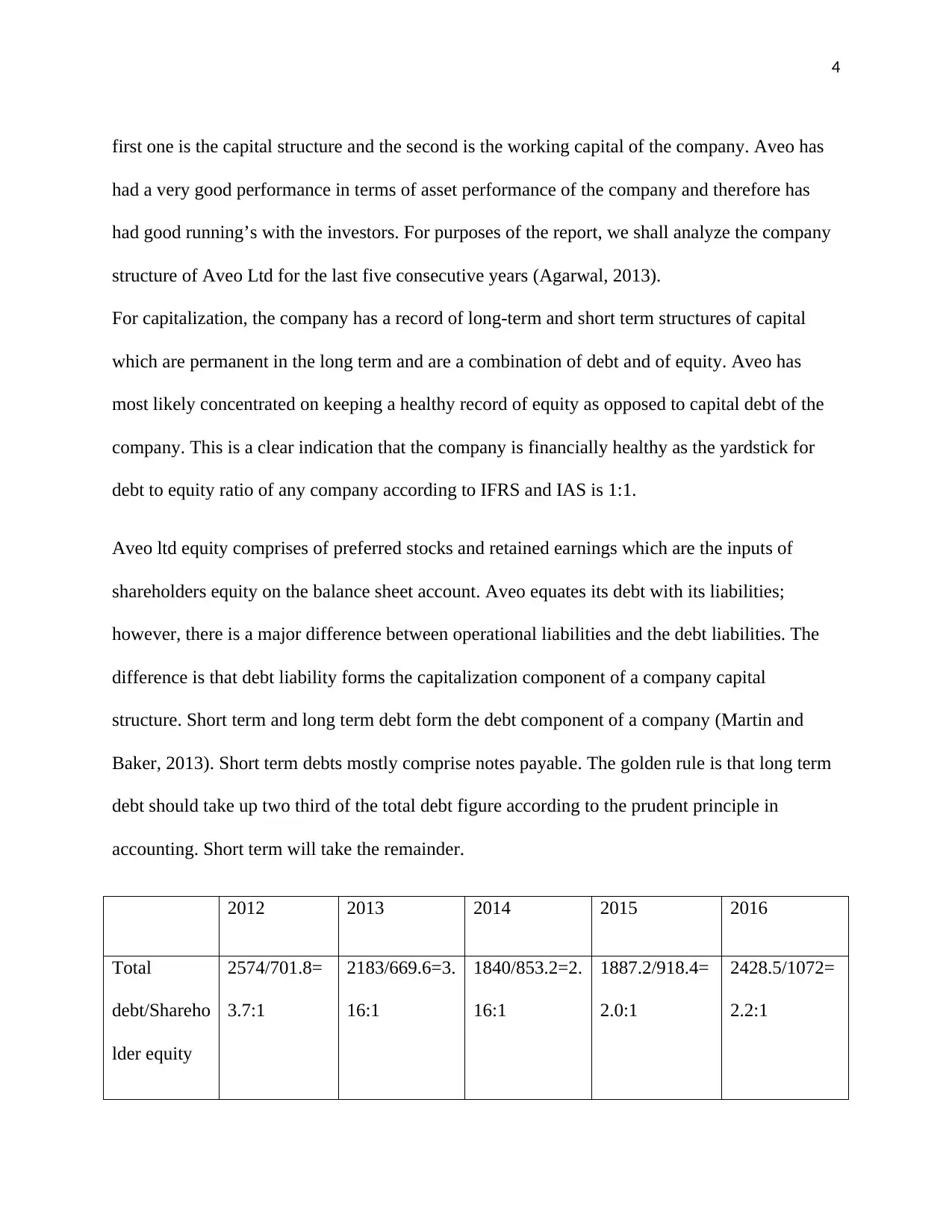

first one is the capital structure and the second is the working capital of the company. Aveo has

had a very good performance in terms of asset performance of the company and therefore has

had good running’s with the investors. For purposes of the report, we shall analyze the company

structure of Aveo Ltd for the last five consecutive years (Agarwal, 2013).

For capitalization, the company has a record of long-term and short term structures of capital

which are permanent in the long term and are a combination of debt and of equity. Aveo has

most likely concentrated on keeping a healthy record of equity as opposed to capital debt of the

company. This is a clear indication that the company is financially healthy as the yardstick for

debt to equity ratio of any company according to IFRS and IAS is 1:1.

Aveo ltd equity comprises of preferred stocks and retained earnings which are the inputs of

shareholders equity on the balance sheet account. Aveo equates its debt with its liabilities;

however, there is a major difference between operational liabilities and the debt liabilities. The

difference is that debt liability forms the capitalization component of a company capital

structure. Short term and long term debt form the debt component of a company (Martin and

Baker, 2013). Short term debts mostly comprise notes payable. The golden rule is that long term

debt should take up two third of the total debt figure according to the prudent principle in

accounting. Short term will take the remainder.

2012 2013 2014 2015 2016

Total

debt/Shareho

lder equity

2574/701.8=

3.7:1

2183/669.6=3.

16:1

1840/853.2=2.

16:1

1887.2/918.4=

2.0:1

2428.5/1072=

2.2:1

first one is the capital structure and the second is the working capital of the company. Aveo has

had a very good performance in terms of asset performance of the company and therefore has

had good running’s with the investors. For purposes of the report, we shall analyze the company

structure of Aveo Ltd for the last five consecutive years (Agarwal, 2013).

For capitalization, the company has a record of long-term and short term structures of capital

which are permanent in the long term and are a combination of debt and of equity. Aveo has

most likely concentrated on keeping a healthy record of equity as opposed to capital debt of the

company. This is a clear indication that the company is financially healthy as the yardstick for

debt to equity ratio of any company according to IFRS and IAS is 1:1.

Aveo ltd equity comprises of preferred stocks and retained earnings which are the inputs of

shareholders equity on the balance sheet account. Aveo equates its debt with its liabilities;

however, there is a major difference between operational liabilities and the debt liabilities. The

difference is that debt liability forms the capitalization component of a company capital

structure. Short term and long term debt form the debt component of a company (Martin and

Baker, 2013). Short term debts mostly comprise notes payable. The golden rule is that long term

debt should take up two third of the total debt figure according to the prudent principle in

accounting. Short term will take the remainder.

2012 2013 2014 2015 2016

Total

debt/Shareho

lder equity

2574/701.8=

3.7:1

2183/669.6=3.

16:1

1840/853.2=2.

16:1

1887.2/918.4=

2.0:1

2428.5/1072=

2.2:1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

The analysis in the figures above indicate that the debt to equity ratio in the five years have been

very high. While the recommended yardstick of debt to equity ratio is 1:1, Aveo ltd remains to

have a high ratio in terms of debt to equity ratio. In the year 2012, the debt to equity ratio was

3.7:1 which was 3 times higher than the recommended threshold. This is not optimal at all. In

2013, the ratio dropped albeit marginally to 3.2: 1 as well as in the year 2014. This was an

improvement in terms of financial management despite being high for the accounting standards.

In the financial year ended 2015, it dropped to 2.0:1, although not optimal, it seems the company

had put in place measures to tame the high debt to equity ratio. This shows that the liquidity of a

company is improving (Brown, Liang and Weisbenner, 2006). This is also the case in 2016

where the debt to equity ratio was 2.2: 1. This shows that in all the 5 financial years the debt to

equity ratio exceed the yardstick and this is not good for the investors in Aveo ltd.

Optimum capital structure

The assumption in prudence use of leverage or debt is that the management can earn more on

borrowed money to the amount of interest and fees expense paid on these funds.If a company in

a highly competitive environment, is hobbled by high debt , the company may find its

competitors taking advantage of the problems facing the company to grab more market share.

But if there are taxes, is the irrelevance of the capital structure maintained? To answer this

question, let us imagine that the cash flow (FC) of a company is similar to a pie. That cash flow,

brought to present value with the appropriate discount rate, will give us the value of the firm. In a

The analysis in the figures above indicate that the debt to equity ratio in the five years have been

very high. While the recommended yardstick of debt to equity ratio is 1:1, Aveo ltd remains to

have a high ratio in terms of debt to equity ratio. In the year 2012, the debt to equity ratio was

3.7:1 which was 3 times higher than the recommended threshold. This is not optimal at all. In

2013, the ratio dropped albeit marginally to 3.2: 1 as well as in the year 2014. This was an

improvement in terms of financial management despite being high for the accounting standards.

In the financial year ended 2015, it dropped to 2.0:1, although not optimal, it seems the company

had put in place measures to tame the high debt to equity ratio. This shows that the liquidity of a

company is improving (Brown, Liang and Weisbenner, 2006). This is also the case in 2016

where the debt to equity ratio was 2.2: 1. This shows that in all the 5 financial years the debt to

equity ratio exceed the yardstick and this is not good for the investors in Aveo ltd.

Optimum capital structure

The assumption in prudence use of leverage or debt is that the management can earn more on

borrowed money to the amount of interest and fees expense paid on these funds.If a company in

a highly competitive environment, is hobbled by high debt , the company may find its

competitors taking advantage of the problems facing the company to grab more market share.

But if there are taxes, is the irrelevance of the capital structure maintained? To answer this

question, let us imagine that the cash flow (FC) of a company is similar to a pie. That cash flow,

brought to present value with the appropriate discount rate, will give us the value of the firm. In a

6

taxed world, a company without debt would have a CF like this: (Brown, Liang and Weisbenner,

2006)

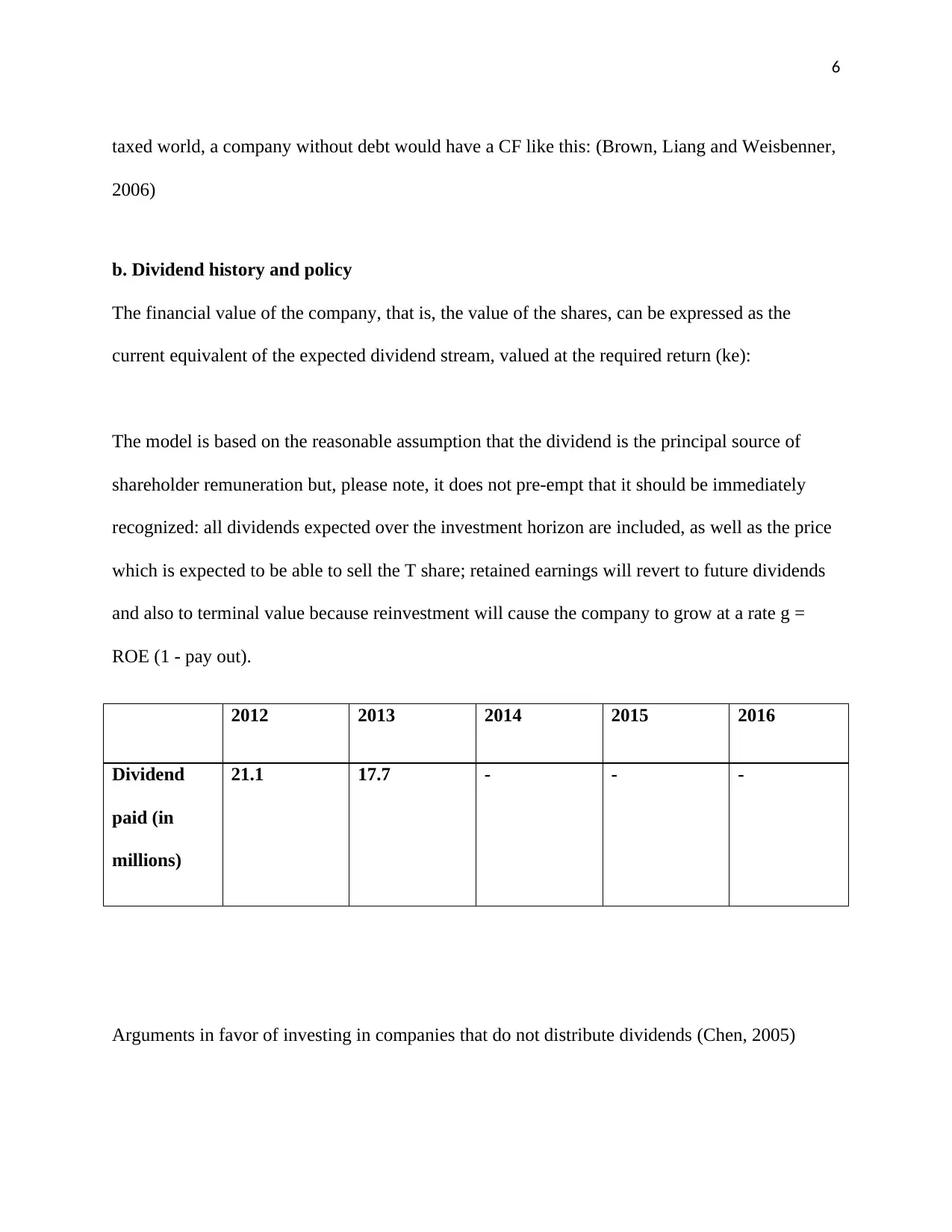

b. Dividend history and policy

The financial value of the company, that is, the value of the shares, can be expressed as the

current equivalent of the expected dividend stream, valued at the required return (ke):

The model is based on the reasonable assumption that the dividend is the principal source of

shareholder remuneration but, please note, it does not pre-empt that it should be immediately

recognized: all dividends expected over the investment horizon are included, as well as the price

which is expected to be able to sell the T share; retained earnings will revert to future dividends

and also to terminal value because reinvestment will cause the company to grow at a rate g =

ROE (1 - pay out).

2012 2013 2014 2015 2016

Dividend

paid (in

millions)

21.1 17.7 - - -

Arguments in favor of investing in companies that do not distribute dividends (Chen, 2005)

taxed world, a company without debt would have a CF like this: (Brown, Liang and Weisbenner,

2006)

b. Dividend history and policy

The financial value of the company, that is, the value of the shares, can be expressed as the

current equivalent of the expected dividend stream, valued at the required return (ke):

The model is based on the reasonable assumption that the dividend is the principal source of

shareholder remuneration but, please note, it does not pre-empt that it should be immediately

recognized: all dividends expected over the investment horizon are included, as well as the price

which is expected to be able to sell the T share; retained earnings will revert to future dividends

and also to terminal value because reinvestment will cause the company to grow at a rate g =

ROE (1 - pay out).

2012 2013 2014 2015 2016

Dividend

paid (in

millions)

21.1 17.7 - - -

Arguments in favor of investing in companies that do not distribute dividends (Chen, 2005)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

In Aveo Ltd, the company cannot afford to be capitalized by distributing their dividends to the

shareholders because of their investment need. Reinvestment is done in bid not to fall behind

their competitors and to give the shareholders maximum value in terms of shareholders value for

the future. In many cases, the company like Aveo will sell its shares in order to have a tax

advantage where dividends are subject to the IRPF.

Arguments in favor of the distribution of dividends

This is the other side of the coin, where shareholders can sketch a smile every three months. The

perspective from this position is totally different from the previous one, where it is preferred that

the money earned with the contributions made by the shareholders be returned to them, since in a

certain way these benefits belong to them. In this way the shareholder has the freedom to choose

what to do with the liquidity obtained.

Pay-out

Another fact that we usually take into account when we intend to invest in a company that

distributes dividend is the Pay-out. This is the part of profits that the company destines to

dividends, so it will always be advisable to take it into account since, depending on the situation

in which the company is, more or less dividends will be distributed.

Where are the profits of companies that do not distribute dividends invested?

The profits that the company obtains and are not destined to the distribution of dividends do not

have a specific destiny, each company makes the most appropriate decision as to where it has to

invest this money, although usually this destination is usually the same for all the companies7.

In Aveo Ltd, the company cannot afford to be capitalized by distributing their dividends to the

shareholders because of their investment need. Reinvestment is done in bid not to fall behind

their competitors and to give the shareholders maximum value in terms of shareholders value for

the future. In many cases, the company like Aveo will sell its shares in order to have a tax

advantage where dividends are subject to the IRPF.

Arguments in favor of the distribution of dividends

This is the other side of the coin, where shareholders can sketch a smile every three months. The

perspective from this position is totally different from the previous one, where it is preferred that

the money earned with the contributions made by the shareholders be returned to them, since in a

certain way these benefits belong to them. In this way the shareholder has the freedom to choose

what to do with the liquidity obtained.

Pay-out

Another fact that we usually take into account when we intend to invest in a company that

distributes dividend is the Pay-out. This is the part of profits that the company destines to

dividends, so it will always be advisable to take it into account since, depending on the situation

in which the company is, more or less dividends will be distributed.

Where are the profits of companies that do not distribute dividends invested?

The profits that the company obtains and are not destined to the distribution of dividends do not

have a specific destiny, each company makes the most appropriate decision as to where it has to

invest this money, although usually this destination is usually the same for all the companies7.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

For example: to ensure greater liquidity, to have a working fund to help us in a difficult situation,

etc. But we must also take into account that there are shareholders who have deposited their trust

and money in the company so that it can carry out its activities, so the reward to these

shareholders has to come from a part of the profits (Graham, n.d.)

Dividend history for the past 5 years

The quality of dividends distributed is directly proportional to the quality of financial reports

produced. The dividend structure is commensurate to the profits received for the company. Aveo

ltd has not paid out dividends for the last three years. In fact the last dividend paid was in the

year 2013, the debt to equity ratio has also reduced in those years.

Aveo ltd has not paid out dividends for the last three years, and its debt equity ratio has reduced

in those three years (Vandekerckhove, 2012).

This report discusses the impact of dividend payments on company value, whose maximization,

remember, is the financial objective. Modigliani and Miller demonstrated that, under certain

conditions, shareholders should be indifferent between the payment of dividends and the

capitalization of results; however, some companies have turned this pay into an essential element

of their relationship with investors. Others, on the other hand, maintain a systematic policy of

reinvestment, without their actions being penalized by investors.

For example: to ensure greater liquidity, to have a working fund to help us in a difficult situation,

etc. But we must also take into account that there are shareholders who have deposited their trust

and money in the company so that it can carry out its activities, so the reward to these

shareholders has to come from a part of the profits (Graham, n.d.)

Dividend history for the past 5 years

The quality of dividends distributed is directly proportional to the quality of financial reports

produced. The dividend structure is commensurate to the profits received for the company. Aveo

ltd has not paid out dividends for the last three years. In fact the last dividend paid was in the

year 2013, the debt to equity ratio has also reduced in those years.

Aveo ltd has not paid out dividends for the last three years, and its debt equity ratio has reduced

in those three years (Vandekerckhove, 2012).

This report discusses the impact of dividend payments on company value, whose maximization,

remember, is the financial objective. Modigliani and Miller demonstrated that, under certain

conditions, shareholders should be indifferent between the payment of dividends and the

capitalization of results; however, some companies have turned this pay into an essential element

of their relationship with investors. Others, on the other hand, maintain a systematic policy of

reinvestment, without their actions being penalized by investors.

9

Know the complete process that must be followed to make successful decisions in Financial

Investments.

Dividend distribution

Problems in individual decision-making are mainly due to two causes of fear of decision making

and thoughtless decision-making (Vandekerckhove, 2012).

C) Attractiveness of Aveo Australia ltd to an investor

Aveo is a very attractive company to invest in. it has had its fair share of troubles especially in

dividend payout but remains a very attractive company for investors nonetheless. The dividend

policy, and its broader expression as a self-financing policy, is closely related to both the

financial structure and the investment decisions. Retained earnings are a source of financing that,

depending on the preferences of the company and its owners, can make growth possible by

supplementing or supplementing debt or other sources of self-financing, such as capital

increases. Self-financing is, in fact, the preferred source for many R & D-intensive companies,

and / or latent opportunities (Graham, n.d.).

Regarding how dividends are canceled Brealey and Myers point out: The dividend is fixed by the

company's board of directors. The announcement states that payment will be made to all

shareholders who are registered on a certain closing date. Later, about two weeks later, dividend

checks are sent to shareholders. Dividends can only be declared by the board of directors, which

then has the authority to order the payment of a dividend. If the directors or board of directors

decide to declare a dividend, they must take appropriate measures to pay the members at a

certain date (Vandekerckhove, 2012).

Know the complete process that must be followed to make successful decisions in Financial

Investments.

Dividend distribution

Problems in individual decision-making are mainly due to two causes of fear of decision making

and thoughtless decision-making (Vandekerckhove, 2012).

C) Attractiveness of Aveo Australia ltd to an investor

Aveo is a very attractive company to invest in. it has had its fair share of troubles especially in

dividend payout but remains a very attractive company for investors nonetheless. The dividend

policy, and its broader expression as a self-financing policy, is closely related to both the

financial structure and the investment decisions. Retained earnings are a source of financing that,

depending on the preferences of the company and its owners, can make growth possible by

supplementing or supplementing debt or other sources of self-financing, such as capital

increases. Self-financing is, in fact, the preferred source for many R & D-intensive companies,

and / or latent opportunities (Graham, n.d.).

Regarding how dividends are canceled Brealey and Myers point out: The dividend is fixed by the

company's board of directors. The announcement states that payment will be made to all

shareholders who are registered on a certain closing date. Later, about two weeks later, dividend

checks are sent to shareholders. Dividends can only be declared by the board of directors, which

then has the authority to order the payment of a dividend. If the directors or board of directors

decide to declare a dividend, they must take appropriate measures to pay the members at a

certain date (Vandekerckhove, 2012).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

Aveo ltd profitability levels are high showing that investors can be attracted by the levels of

profit that the company is having. Although attractiveness of a company can be measured using

different yardsticks, profitability, liquidity and the company’s general stability remains the key

areas of focus for the investors outlook (Graham, n.d.).

According to this approach, the shareholder's profitability in any period t is the sum of the

dividend yield and the profitability accrued by the change in the value of the shares:

so that the model does not establish any express priority between dividends and retention. This

result has some logic, because the value of the company's asset is the current equivalent of free

cash flow, discounted to the weighted average cost of capital, and neither of these two variables

depends on the distribution policy (maintaining the presumption that the decision involves a

trade-off between paid dividends and new capital)

Nor does it pre-judge that both profits (dividends and capital gains) are strictly equivalent: in fact

they are not, because the latter are subject to risk, hence a financial valuation and a discount rate

with risk. Accordingly, in a first approximation the effect of the dividend policy on the value of

the enterprise will depend on the future impact of the retained earnings: to the extent that the

incremental result provided by the domestic reinvestment offsets the risk and the time

(preference for liquidity), shareholders will be willing to waive their current dividends in

exchange for future (incremental) dividends.

Aveo ltd profitability levels are high showing that investors can be attracted by the levels of

profit that the company is having. Although attractiveness of a company can be measured using

different yardsticks, profitability, liquidity and the company’s general stability remains the key

areas of focus for the investors outlook (Graham, n.d.).

According to this approach, the shareholder's profitability in any period t is the sum of the

dividend yield and the profitability accrued by the change in the value of the shares:

so that the model does not establish any express priority between dividends and retention. This

result has some logic, because the value of the company's asset is the current equivalent of free

cash flow, discounted to the weighted average cost of capital, and neither of these two variables

depends on the distribution policy (maintaining the presumption that the decision involves a

trade-off between paid dividends and new capital)

Nor does it pre-judge that both profits (dividends and capital gains) are strictly equivalent: in fact

they are not, because the latter are subject to risk, hence a financial valuation and a discount rate

with risk. Accordingly, in a first approximation the effect of the dividend policy on the value of

the enterprise will depend on the future impact of the retained earnings: to the extent that the

incremental result provided by the domestic reinvestment offsets the risk and the time

(preference for liquidity), shareholders will be willing to waive their current dividends in

exchange for future (incremental) dividends.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

Conclusion

Aveo is a good company to invest in. It is clear, that the cash flow of the business, will be shared

by the shareholders and the State. Then, the present value of what is left to the shareholder,

would be the value of the company, or otherwise seen, Vu = E, where Vu is the value of a

deleveraged company and E is the equity (Vandekerckhove, 2012).

Conclusion

Aveo is a good company to invest in. It is clear, that the cash flow of the business, will be shared

by the shareholders and the State. Then, the present value of what is left to the shareholder,

would be the value of the company, or otherwise seen, Vu = E, where Vu is the value of a

deleveraged company and E is the equity (Vandekerckhove, 2012).

12

References

Agarwal, Y. (2013). Capital Structure Decisions. Hoboken: Wiley.

Bena, J. and Hanousek, J. (2006). Rent extraction by large shareholders: evidence using

dividend policy in the Czech Republic. Prague: CERGE-EI.

Brown, J., Liang, J. and Weisbenner, S. (2006). Executive financial incentives and payout policy.

Washington, D.C.: Divisions of Research & Statistics and Monetary Affairs, Federal Reserve

Board.

Brown, J., Liang, J. and Weisbenner, S. (2006). Executive financial incentives and payout policy.

Washington, D.C.: Divisions of Research & Statistics and Monetary Affairs, Federal Reserve

Board.

Chen, A. (2005). Research in finance. Amsterdam: Elsevier JAI, .

Graham, B. (n.d.). The intelligent investor. New York: Collins.

References

Agarwal, Y. (2013). Capital Structure Decisions. Hoboken: Wiley.

Bena, J. and Hanousek, J. (2006). Rent extraction by large shareholders: evidence using

dividend policy in the Czech Republic. Prague: CERGE-EI.

Brown, J., Liang, J. and Weisbenner, S. (2006). Executive financial incentives and payout policy.

Washington, D.C.: Divisions of Research & Statistics and Monetary Affairs, Federal Reserve

Board.

Brown, J., Liang, J. and Weisbenner, S. (2006). Executive financial incentives and payout policy.

Washington, D.C.: Divisions of Research & Statistics and Monetary Affairs, Federal Reserve

Board.

Chen, A. (2005). Research in finance. Amsterdam: Elsevier JAI, .

Graham, B. (n.d.). The intelligent investor. New York: Collins.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.