Financial Evaluation and Sourcing Recommendation: Award Programme

VerifiedAdded on 2020/01/06

|13

|4923

|132

Report

AI Summary

This report presents a comprehensive financial analysis of a corporate award program, utilizing ratio analysis to evaluate profitability, liquidity, and gearing. The analysis includes a detailed examination of the company's financial statements from 2013 and 2014, highlighting strengths and weaknesses. The report assesses profitability ratios such as gross profit, net profit, and return on capital employed, along with liquidity ratios, including current and quick ratios. Efficiency and gearing ratios are also evaluated to provide a holistic view of the organization's financial health. Based on this analysis, the report provides a justified recommendation regarding the suitability of the organization for a sourcing exercise for facilities management services, emphasizing the importance of supplier appraisal and financial exposure limits, specifically the maximum contract value. The report concludes with recommendations for improving financial performance and optimizing capital structure.

CORPORATE

AWARD PROGRAME

1

AWARD PROGRAME

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION................................................................................................................................3

1. Evaluate the finances of this organization highlighting the strengths and weaknesses of their. .3

Position............................................................................................................................................3

2. Provide a justified recommendation as to whether you would consider this organization for a

sourcing exercise for facilities management services emphasizing any limit that should be placed

on the financial exposure (maximum contract value)......................................................................6

CONCLUSION...................................................................................................................................11

REFERENCES...................................................................................................................................12

2

INTRODUCTION................................................................................................................................3

1. Evaluate the finances of this organization highlighting the strengths and weaknesses of their. .3

Position............................................................................................................................................3

2. Provide a justified recommendation as to whether you would consider this organization for a

sourcing exercise for facilities management services emphasizing any limit that should be placed

on the financial exposure (maximum contract value)......................................................................6

CONCLUSION...................................................................................................................................11

REFERENCES...................................................................................................................................12

2

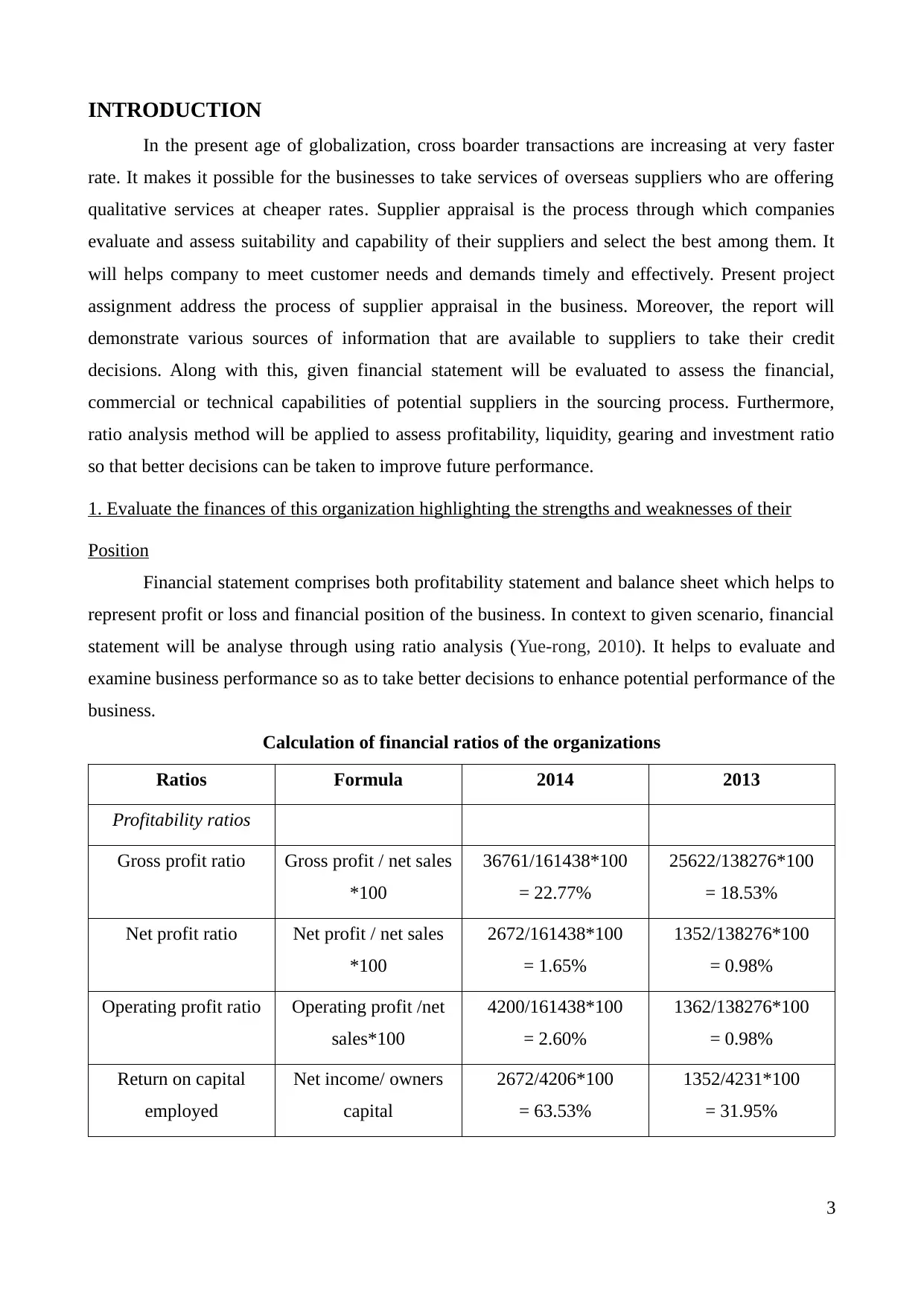

INTRODUCTION

In the present age of globalization, cross boarder transactions are increasing at very faster

rate. It makes it possible for the businesses to take services of overseas suppliers who are offering

qualitative services at cheaper rates. Supplier appraisal is the process through which companies

evaluate and assess suitability and capability of their suppliers and select the best among them. It

will helps company to meet customer needs and demands timely and effectively. Present project

assignment address the process of supplier appraisal in the business. Moreover, the report will

demonstrate various sources of information that are available to suppliers to take their credit

decisions. Along with this, given financial statement will be evaluated to assess the financial,

commercial or technical capabilities of potential suppliers in the sourcing process. Furthermore,

ratio analysis method will be applied to assess profitability, liquidity, gearing and investment ratio

so that better decisions can be taken to improve future performance.

1. Evaluate the finances of this organization highlighting the strengths and weaknesses of their

Position

Financial statement comprises both profitability statement and balance sheet which helps to

represent profit or loss and financial position of the business. In context to given scenario, financial

statement will be analyse through using ratio analysis (Yue-rong, 2010). It helps to evaluate and

examine business performance so as to take better decisions to enhance potential performance of the

business.

Calculation of financial ratios of the organizations

Ratios Formula 2014 2013

Profitability ratios

Gross profit ratio Gross profit / net sales

*100

36761/161438*100

= 22.77%

25622/138276*100

= 18.53%

Net profit ratio Net profit / net sales

*100

2672/161438*100

= 1.65%

1352/138276*100

= 0.98%

Operating profit ratio Operating profit /net

sales*100

4200/161438*100

= 2.60%

1362/138276*100

= 0.98%

Return on capital

employed

Net income/ owners

capital

2672/4206*100

= 63.53%

1352/4231*100

= 31.95%

3

In the present age of globalization, cross boarder transactions are increasing at very faster

rate. It makes it possible for the businesses to take services of overseas suppliers who are offering

qualitative services at cheaper rates. Supplier appraisal is the process through which companies

evaluate and assess suitability and capability of their suppliers and select the best among them. It

will helps company to meet customer needs and demands timely and effectively. Present project

assignment address the process of supplier appraisal in the business. Moreover, the report will

demonstrate various sources of information that are available to suppliers to take their credit

decisions. Along with this, given financial statement will be evaluated to assess the financial,

commercial or technical capabilities of potential suppliers in the sourcing process. Furthermore,

ratio analysis method will be applied to assess profitability, liquidity, gearing and investment ratio

so that better decisions can be taken to improve future performance.

1. Evaluate the finances of this organization highlighting the strengths and weaknesses of their

Position

Financial statement comprises both profitability statement and balance sheet which helps to

represent profit or loss and financial position of the business. In context to given scenario, financial

statement will be analyse through using ratio analysis (Yue-rong, 2010). It helps to evaluate and

examine business performance so as to take better decisions to enhance potential performance of the

business.

Calculation of financial ratios of the organizations

Ratios Formula 2014 2013

Profitability ratios

Gross profit ratio Gross profit / net sales

*100

36761/161438*100

= 22.77%

25622/138276*100

= 18.53%

Net profit ratio Net profit / net sales

*100

2672/161438*100

= 1.65%

1352/138276*100

= 0.98%

Operating profit ratio Operating profit /net

sales*100

4200/161438*100

= 2.60%

1362/138276*100

= 0.98%

Return on capital

employed

Net income/ owners

capital

2672/4206*100

= 63.53%

1352/4231*100

= 31.95%

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

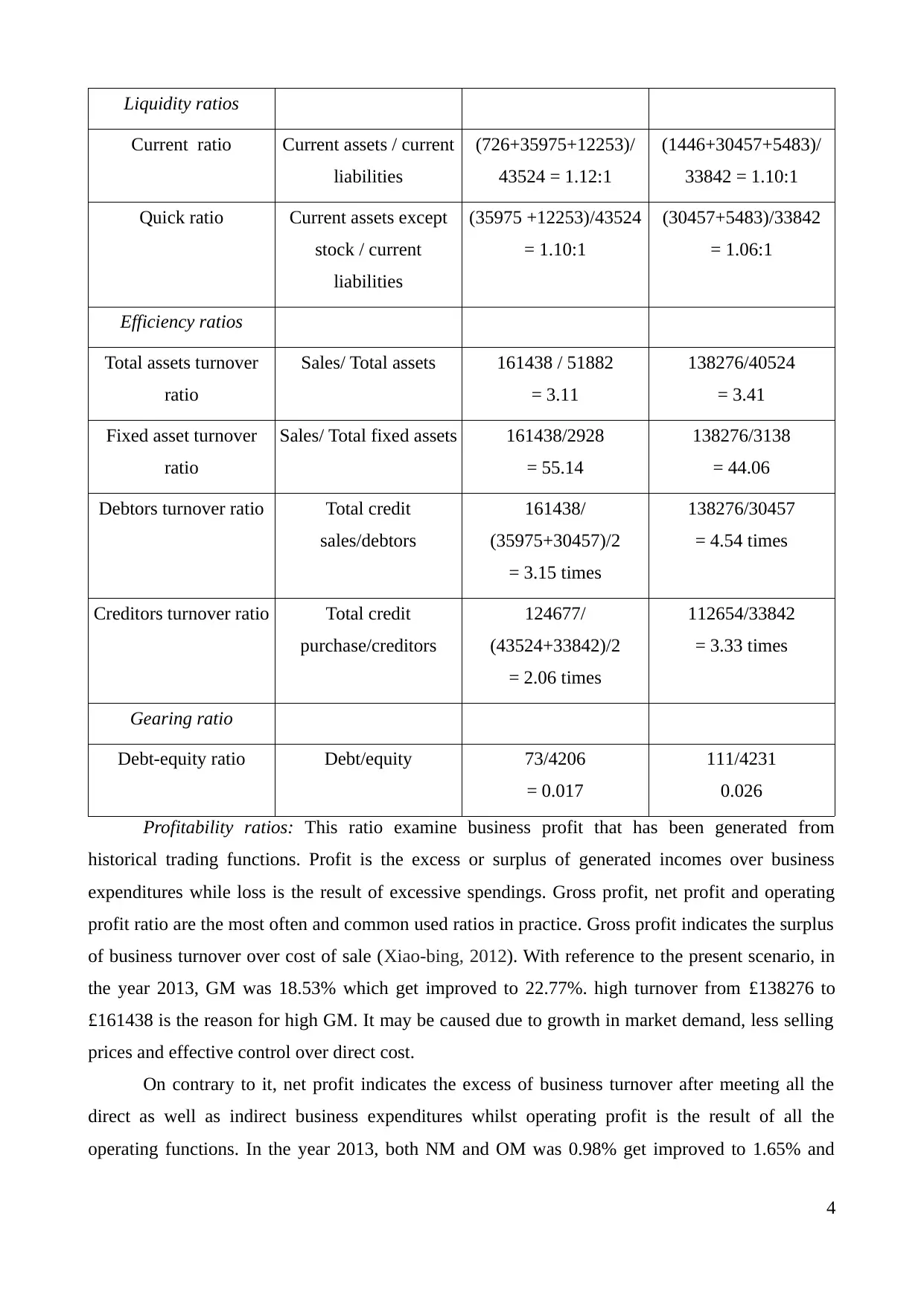

Liquidity ratios

Current ratio Current assets / current

liabilities

(726+35975+12253)/

43524 = 1.12:1

(1446+30457+5483)/

33842 = 1.10:1

Quick ratio Current assets except

stock / current

liabilities

(35975 +12253)/43524

= 1.10:1

(30457+5483)/33842

= 1.06:1

Efficiency ratios

Total assets turnover

ratio

Sales/ Total assets 161438 / 51882

= 3.11

138276/40524

= 3.41

Fixed asset turnover

ratio

Sales/ Total fixed assets 161438/2928

= 55.14

138276/3138

= 44.06

Debtors turnover ratio Total credit

sales/debtors

161438/

(35975+30457)/2

= 3.15 times

138276/30457

= 4.54 times

Creditors turnover ratio Total credit

purchase/creditors

124677/

(43524+33842)/2

= 2.06 times

112654/33842

= 3.33 times

Gearing ratio

Debt-equity ratio Debt/equity 73/4206

= 0.017

111/4231

0.026

Profitability ratios: This ratio examine business profit that has been generated from

historical trading functions. Profit is the excess or surplus of generated incomes over business

expenditures while loss is the result of excessive spendings. Gross profit, net profit and operating

profit ratio are the most often and common used ratios in practice. Gross profit indicates the surplus

of business turnover over cost of sale (Xiao-bing, 2012). With reference to the present scenario, in

the year 2013, GM was 18.53% which get improved to 22.77%. high turnover from £138276 to

£161438 is the reason for high GM. It may be caused due to growth in market demand, less selling

prices and effective control over direct cost.

On contrary to it, net profit indicates the excess of business turnover after meeting all the

direct as well as indirect business expenditures whilst operating profit is the result of all the

operating functions. In the year 2013, both NM and OM was 0.98% get improved to 1.65% and

4

Current ratio Current assets / current

liabilities

(726+35975+12253)/

43524 = 1.12:1

(1446+30457+5483)/

33842 = 1.10:1

Quick ratio Current assets except

stock / current

liabilities

(35975 +12253)/43524

= 1.10:1

(30457+5483)/33842

= 1.06:1

Efficiency ratios

Total assets turnover

ratio

Sales/ Total assets 161438 / 51882

= 3.11

138276/40524

= 3.41

Fixed asset turnover

ratio

Sales/ Total fixed assets 161438/2928

= 55.14

138276/3138

= 44.06

Debtors turnover ratio Total credit

sales/debtors

161438/

(35975+30457)/2

= 3.15 times

138276/30457

= 4.54 times

Creditors turnover ratio Total credit

purchase/creditors

124677/

(43524+33842)/2

= 2.06 times

112654/33842

= 3.33 times

Gearing ratio

Debt-equity ratio Debt/equity 73/4206

= 0.017

111/4231

0.026

Profitability ratios: This ratio examine business profit that has been generated from

historical trading functions. Profit is the excess or surplus of generated incomes over business

expenditures while loss is the result of excessive spendings. Gross profit, net profit and operating

profit ratio are the most often and common used ratios in practice. Gross profit indicates the surplus

of business turnover over cost of sale (Xiao-bing, 2012). With reference to the present scenario, in

the year 2013, GM was 18.53% which get improved to 22.77%. high turnover from £138276 to

£161438 is the reason for high GM. It may be caused due to growth in market demand, less selling

prices and effective control over direct cost.

On contrary to it, net profit indicates the excess of business turnover after meeting all the

direct as well as indirect business expenditures whilst operating profit is the result of all the

operating functions. In the year 2013, both NM and OM was 0.98% get improved to 1.65% and

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2.60% respectively (Wu, Rossetti and Tepper, 2015). Rising trend in profitability ratios from £1352

to £2672 is a good sign. It may be due to increase in consumer demand and less offering prices.

Moreover, return on capital employed measure the profit percentage on total shareholder's

investment. It has been increased from 31.95% to 63.53% due to larger the net earnings. Thus, it

can be said that company is performing well as compare to PY 2013. But still, in both the years,

there is a huge difference in GM and NM. It reflects that firm is not maintaining an effective control

over its indirect costs. In order to increase potential performance, it can be suggested that by

offering more effective services at affordable prices and control on expenditures greatly assist

users to enlarge their turnover and reduce expenses (Wang, Kayande and Jap, 2010). This in turn, it

enable firm to get larger profitability and enjoy more success.

Liquidity ratios: It measure the ability of the firm to pay their short-term liabilities

effectively. Current ratio and quick ratio are the most commonly used liquidity position of the

business (Vodova, 2011). Current ratio (CR) measure that firm has enough current assets or not to

discharge their current obligations timely. However, quick ratio measure liquidity ability except the

inventory balance. In the year 2013, CR was 1.10 which has been inclined to 1.12 in the year 2014.

Increase in debtors and cash are the reason for high CR. It reflects that business is more able to pay

off their current liabilities (not more than 12 month) more effectively.

Moreover, QR has been increased from 1.06:1 to 1.10 which indicates that company is able

to pay off their short-term obligations without having inventory in the business (Van den End and

Kruidhof, 2013). In addition to it, both the liquidity ratios are higher than idle industrial current

ratio of 1:1 and QR of 0.5:1. Thus, it can be said that liquidity position of the business is sound.

Henceforth, it will be able to take more on credit and at favourable terms.

Efficiency ratios: This ratio also called activity ratios which measure managers ability to use

business assets so as to generate larger revenues (Sherry and Teece, 2015). Total assets turnover

ratio (TATR) indicates that how effectively the assets are using by the management while fixed

assets turnover ratio (FATR) measure ability to use fixed assets. In the year 2013, TATR was 3.41

which get declined to 3.11 while FATR has been increased from 44.06 to 55.14. Thus, it can be said

that fixed assets such as plant and machinery, computer equipment and others are more effectively

utilizing so as to generate high turnover and profitability. While, on the other side, management are

using total assets less effectively (Sepúlveda and Derpich, 2014).

Accounts receivable turnover ratio indicates the relationship between net sales and debtors.

It indicates the ability to generate quicker cash inflow by selling the inventory. It has been declined

from 4.54 times to 3.15 times which is not good because it indicates slower conversion of stock into

sales as compare to PY 2013 (Saleem and Rehman, 2011). This in turn, company's sales and cash

5

to £2672 is a good sign. It may be due to increase in consumer demand and less offering prices.

Moreover, return on capital employed measure the profit percentage on total shareholder's

investment. It has been increased from 31.95% to 63.53% due to larger the net earnings. Thus, it

can be said that company is performing well as compare to PY 2013. But still, in both the years,

there is a huge difference in GM and NM. It reflects that firm is not maintaining an effective control

over its indirect costs. In order to increase potential performance, it can be suggested that by

offering more effective services at affordable prices and control on expenditures greatly assist

users to enlarge their turnover and reduce expenses (Wang, Kayande and Jap, 2010). This in turn, it

enable firm to get larger profitability and enjoy more success.

Liquidity ratios: It measure the ability of the firm to pay their short-term liabilities

effectively. Current ratio and quick ratio are the most commonly used liquidity position of the

business (Vodova, 2011). Current ratio (CR) measure that firm has enough current assets or not to

discharge their current obligations timely. However, quick ratio measure liquidity ability except the

inventory balance. In the year 2013, CR was 1.10 which has been inclined to 1.12 in the year 2014.

Increase in debtors and cash are the reason for high CR. It reflects that business is more able to pay

off their current liabilities (not more than 12 month) more effectively.

Moreover, QR has been increased from 1.06:1 to 1.10 which indicates that company is able

to pay off their short-term obligations without having inventory in the business (Van den End and

Kruidhof, 2013). In addition to it, both the liquidity ratios are higher than idle industrial current

ratio of 1:1 and QR of 0.5:1. Thus, it can be said that liquidity position of the business is sound.

Henceforth, it will be able to take more on credit and at favourable terms.

Efficiency ratios: This ratio also called activity ratios which measure managers ability to use

business assets so as to generate larger revenues (Sherry and Teece, 2015). Total assets turnover

ratio (TATR) indicates that how effectively the assets are using by the management while fixed

assets turnover ratio (FATR) measure ability to use fixed assets. In the year 2013, TATR was 3.41

which get declined to 3.11 while FATR has been increased from 44.06 to 55.14. Thus, it can be said

that fixed assets such as plant and machinery, computer equipment and others are more effectively

utilizing so as to generate high turnover and profitability. While, on the other side, management are

using total assets less effectively (Sepúlveda and Derpich, 2014).

Accounts receivable turnover ratio indicates the relationship between net sales and debtors.

It indicates the ability to generate quicker cash inflow by selling the inventory. It has been declined

from 4.54 times to 3.15 times which is not good because it indicates slower conversion of stock into

sales as compare to PY 2013 (Saleem and Rehman, 2011). This in turn, company's sales and cash

5

flow management will be adversely affected. While, accounts payable ratio measure ability to pay

creditors by comparing net credit purchase with the average creditors. It has been reduced from 3.33

times to 2.06 times in the year 2014 which reflects that company is making delayed payment to

their suppliers.

Gearing ratios: Debt/equity ratio indicate the percentage of debt and equity funds in the total

capital employed. It has been declined from 0.026 to 0.017 due to excessive shareholders funds and

very little debt funds. Although, declined debt-equity ratio is a sign of less financial risk but still,

idle industrial ratio is 0.5:1. Thus, as per this standard, companies must use both debt and equity

capital and manage their capital risk accordingly (Paul and et.al., 2013). However, in the given case,

it is very shorter than set standard. It dilute controlling rights to the investors to a large extent.

Moreover, it makes it necessary for the company to meet shareholder expectation by providing them

consistent and increased return either in term of dividend and capital appreciation. Thus, it is clear

that gearing position of the firm is not good. Henceforth, it should take long term debts from lenders

to create an optimum capital structure so that it can pay its long term liabilities timely and

effectively (Park, Shin, Chang and Park, 2010).

Taken into account all the derived results, it can be said that operational performance of the

company has been improved due to large profitability. Moreover, firm has sound liquidity position

hence, it is able to pay timely to the suppliers. On contrary to it, management need to pay focus on

effective utilization of resources to generate larger revenue (Lartey, Antwi and Boadi, 2013). Along

with this, it has to obtain funds from debt also so that company will be more able to increase their

gearing position by enlarging the ability to pay long term liabilities more effectively. This in turn, it

can assure long run survival and high success in future period.

2. Provide a justified recommendation as to whether you would consider this organization for a

sourcing exercise for facilities management services emphasizing any limit that should be

placed on the financial exposure (maximum contract value)

Procurement and supply management process involves an assessment and evaluation of

supplier's ability to deliver goods and services on time. Manufacturing companies purchase raw

material from the outsiders on credit, called suppliers. In the present competitive age, it is essential

for the firms to assure that their suppliers deliver timely services which enable organization to

ensure production in required quantity to meet market demand (Kumbirai and Webb, 2013).

Suppliers offer their services on credit henceforth, they provide financial services to the company

also. Supplier appraisal is an crucial aspect of strategic sourcing and managing suppliers so that

corporations can attain competitive advantages. It is an pre-purchase activity that assist firm to

6

creditors by comparing net credit purchase with the average creditors. It has been reduced from 3.33

times to 2.06 times in the year 2014 which reflects that company is making delayed payment to

their suppliers.

Gearing ratios: Debt/equity ratio indicate the percentage of debt and equity funds in the total

capital employed. It has been declined from 0.026 to 0.017 due to excessive shareholders funds and

very little debt funds. Although, declined debt-equity ratio is a sign of less financial risk but still,

idle industrial ratio is 0.5:1. Thus, as per this standard, companies must use both debt and equity

capital and manage their capital risk accordingly (Paul and et.al., 2013). However, in the given case,

it is very shorter than set standard. It dilute controlling rights to the investors to a large extent.

Moreover, it makes it necessary for the company to meet shareholder expectation by providing them

consistent and increased return either in term of dividend and capital appreciation. Thus, it is clear

that gearing position of the firm is not good. Henceforth, it should take long term debts from lenders

to create an optimum capital structure so that it can pay its long term liabilities timely and

effectively (Park, Shin, Chang and Park, 2010).

Taken into account all the derived results, it can be said that operational performance of the

company has been improved due to large profitability. Moreover, firm has sound liquidity position

hence, it is able to pay timely to the suppliers. On contrary to it, management need to pay focus on

effective utilization of resources to generate larger revenue (Lartey, Antwi and Boadi, 2013). Along

with this, it has to obtain funds from debt also so that company will be more able to increase their

gearing position by enlarging the ability to pay long term liabilities more effectively. This in turn, it

can assure long run survival and high success in future period.

2. Provide a justified recommendation as to whether you would consider this organization for a

sourcing exercise for facilities management services emphasizing any limit that should be

placed on the financial exposure (maximum contract value)

Procurement and supply management process involves an assessment and evaluation of

supplier's ability to deliver goods and services on time. Manufacturing companies purchase raw

material from the outsiders on credit, called suppliers. In the present competitive age, it is essential

for the firms to assure that their suppliers deliver timely services which enable organization to

ensure production in required quantity to meet market demand (Kumbirai and Webb, 2013).

Suppliers offer their services on credit henceforth, they provide financial services to the company

also. Supplier appraisal is an crucial aspect of strategic sourcing and managing suppliers so that

corporations can attain competitive advantages. It is an pre-purchase activity that assist firm to

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

analyse the ability of potential creditors in terms of quality, prices, delivery, quantity and all the

other factors that to be embodied in the contract (Kiruri, 2013). It is the process through which

company will approve most appropriate suppliers by placing order to them.

Pre-qualification criteria or process for supplier appraisal in the sourcing process

Supplier appraisal process comprises mainly three elements that are strategic sourcing,

supplier management and accomplishment of competitive advantage. In such respect, strategic

sourcing can be defined as the location, evaluation and selection of the most capable supplier who

will be greatly able to meet purchase requirement and contribute competitive advantage to them

(Karande and Chakraborty, 2012). While, supplier management is a cross functional activity,

through which firms rationalize supplier base so as to purchase, coordinate, assess suppliers

performance and develop their potential as well. However, competitive advantage enable

corporations to compete more effectively with the rivalry firms. The process of supplier appraisal

has been described below:

Clarifying requirements: Initially, corporations has to clarify their requirement that “what

they want” from the suppliers. Management has to determine that what value can be added by

buying from the suppliers. For instance, supplier appraisal process can drive benefits of less prices,

costs, minimum risk, effective services, high quality, compliance with regulations etc. In the

process, firms mainly pay focus on 5 rights that are price, quality, quantity, time and place (Glass

and Knight, 2010). Corporations need to assess the priority of key internal stakeholders such as

managers, directors and staff member of various departments in terms of all the 5 rights. Business

has to identify the needs of stakeholders and make effective management strategies to meet goals by

negotiating (ZHANG ans et.al., 2010). Procurement process comprises need specification, decide

contract terms, identify potential suppliers, supplier appraisal, invite quotations or tenders, select

most suitable, negotiating, award the contract, supplier management and invoice payment (Gervais,

Levant and Ducrocq, 2010). Firms set policies and rules to regulate whole the process. In order to

implement the process more effectively, authority and responsibility must be delegated to the

accountable person in the business.

Sourcing options: There are three sourcing options available to the business, that are single

supplier, dual supplier or multiple supplier. Company need to set framework or agreement with the

supplier in which all the conditions or contractual terms must be decided. It will govern whole the

contract with the supplier, specially with regard to price and quantity (Supplier evaluation and

appraisal, n.d.). Competition based selection, fixed contract duration, economies of scale and

greater dependence are the benefits of single supplier framework. While, risk of incorrect supplier

selection may bring jeopardy to the business and create negative market image. However, multiple

7

other factors that to be embodied in the contract (Kiruri, 2013). It is the process through which

company will approve most appropriate suppliers by placing order to them.

Pre-qualification criteria or process for supplier appraisal in the sourcing process

Supplier appraisal process comprises mainly three elements that are strategic sourcing,

supplier management and accomplishment of competitive advantage. In such respect, strategic

sourcing can be defined as the location, evaluation and selection of the most capable supplier who

will be greatly able to meet purchase requirement and contribute competitive advantage to them

(Karande and Chakraborty, 2012). While, supplier management is a cross functional activity,

through which firms rationalize supplier base so as to purchase, coordinate, assess suppliers

performance and develop their potential as well. However, competitive advantage enable

corporations to compete more effectively with the rivalry firms. The process of supplier appraisal

has been described below:

Clarifying requirements: Initially, corporations has to clarify their requirement that “what

they want” from the suppliers. Management has to determine that what value can be added by

buying from the suppliers. For instance, supplier appraisal process can drive benefits of less prices,

costs, minimum risk, effective services, high quality, compliance with regulations etc. In the

process, firms mainly pay focus on 5 rights that are price, quality, quantity, time and place (Glass

and Knight, 2010). Corporations need to assess the priority of key internal stakeholders such as

managers, directors and staff member of various departments in terms of all the 5 rights. Business

has to identify the needs of stakeholders and make effective management strategies to meet goals by

negotiating (ZHANG ans et.al., 2010). Procurement process comprises need specification, decide

contract terms, identify potential suppliers, supplier appraisal, invite quotations or tenders, select

most suitable, negotiating, award the contract, supplier management and invoice payment (Gervais,

Levant and Ducrocq, 2010). Firms set policies and rules to regulate whole the process. In order to

implement the process more effectively, authority and responsibility must be delegated to the

accountable person in the business.

Sourcing options: There are three sourcing options available to the business, that are single

supplier, dual supplier or multiple supplier. Company need to set framework or agreement with the

supplier in which all the conditions or contractual terms must be decided. It will govern whole the

contract with the supplier, specially with regard to price and quantity (Supplier evaluation and

appraisal, n.d.). Competition based selection, fixed contract duration, economies of scale and

greater dependence are the benefits of single supplier framework. While, risk of incorrect supplier

selection may bring jeopardy to the business and create negative market image. However, multiple

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

supplier framework helps to mitigate the risk of wrongful supplier selection. On contrary to it, risk

of collusion between suppliers to fix agreements and difficulties to determine perfect number of

supplier are its disadvantage (Viviana and et.al., 2003).

Developing ITTs: After identifying the sourcing options, management need to develop

invitation to tenderer. Specification of the products or services, tender form, pricing schedule, KPIs,

contractual terms, plans, customer and site information all are the part of ITT.

Selection and award criteria:Company will select supplier through taking into consideration

technical capability, financial stability, reliability, environment system, product quality, availability

of resources etc. Firm will assign weight to all the factors as per their importance (Yue-rong, 2010).

There are two methods available to evaluate such criteria such as pre-qualification questionnaire

and supplier visit as well. PQQ provide huge benefits to facility management to identify

information for their current contracts, arrangement for administration, sales order processing,

managing deliveries etc. While, in award criteria, entity can make technical and commercial

evaluation of suppliers either separately or jointly (Xiao-bing, 2012).

P2P, E tendering, E-auction: P2P stands for purchase to pay in which information will be

provided by E-procurement, E-auction and E-tendering to save business cost. For instance, supplier

will exhibit their products and services in E-catalogues and information will be share on supplier

portals. E-auction will be conduct through using websites of buyers, sellers and third party (Wu,

Rossetti and Tepper, 2015). While, in E-tendering, business will use E-RFQ and posted information

by using web facility such as e-mail. ITT will be published on buyer's E-tender web portal and

suppliers will send bids using secure emails such as electronic vault in E-Tender system.

Furthermore, it helps to generate automatic scores, specifically for PQQ. E-Catalogues will provide

information regarding product content to all the organizations who intends to buy material from the

suppliers (Wang, Kayande and Jap, 2010). E-Auction provide benefits to administrate and reduce

acquisition lead time more efficiently. It provide quick access to buyers as they can gain knowledge

of wide range of suppliers in less time and select most suitable among these. Thus, it helps to

improve value for the buyers and provide competitive advantage to him.

Sources of information on suppliers to select the most appropriate supplier

There are different types of sources available to an organization to generate information

about the potential suppliers (Vodova, 2011). Obtaining authentic and prominent information is

necessary so as to select most appropriate supplier which will provide more effective services at

cost effective prices to the business. Some of the information sources of suppliers are given below: Financial reports: Every business prepare financial statements so as to obtain information

about their performance and financial status at the end of the financial year. Balance sheet is

8

of collusion between suppliers to fix agreements and difficulties to determine perfect number of

supplier are its disadvantage (Viviana and et.al., 2003).

Developing ITTs: After identifying the sourcing options, management need to develop

invitation to tenderer. Specification of the products or services, tender form, pricing schedule, KPIs,

contractual terms, plans, customer and site information all are the part of ITT.

Selection and award criteria:Company will select supplier through taking into consideration

technical capability, financial stability, reliability, environment system, product quality, availability

of resources etc. Firm will assign weight to all the factors as per their importance (Yue-rong, 2010).

There are two methods available to evaluate such criteria such as pre-qualification questionnaire

and supplier visit as well. PQQ provide huge benefits to facility management to identify

information for their current contracts, arrangement for administration, sales order processing,

managing deliveries etc. While, in award criteria, entity can make technical and commercial

evaluation of suppliers either separately or jointly (Xiao-bing, 2012).

P2P, E tendering, E-auction: P2P stands for purchase to pay in which information will be

provided by E-procurement, E-auction and E-tendering to save business cost. For instance, supplier

will exhibit their products and services in E-catalogues and information will be share on supplier

portals. E-auction will be conduct through using websites of buyers, sellers and third party (Wu,

Rossetti and Tepper, 2015). While, in E-tendering, business will use E-RFQ and posted information

by using web facility such as e-mail. ITT will be published on buyer's E-tender web portal and

suppliers will send bids using secure emails such as electronic vault in E-Tender system.

Furthermore, it helps to generate automatic scores, specifically for PQQ. E-Catalogues will provide

information regarding product content to all the organizations who intends to buy material from the

suppliers (Wang, Kayande and Jap, 2010). E-Auction provide benefits to administrate and reduce

acquisition lead time more efficiently. It provide quick access to buyers as they can gain knowledge

of wide range of suppliers in less time and select most suitable among these. Thus, it helps to

improve value for the buyers and provide competitive advantage to him.

Sources of information on suppliers to select the most appropriate supplier

There are different types of sources available to an organization to generate information

about the potential suppliers (Vodova, 2011). Obtaining authentic and prominent information is

necessary so as to select most appropriate supplier which will provide more effective services at

cost effective prices to the business. Some of the information sources of suppliers are given below: Financial reports: Every business prepare financial statements so as to obtain information

about their performance and financial status at the end of the financial year. Balance sheet is

8

a statement of financial position which is a snapshot of all the fixed as well as current assets

and current as well as non-current liabilities. In such respect, all the business liabilities

which will be paid within the time period of one year, is called current or short-term

liabilities. Suppliers are the part of current liabilities as they supply material for credit of less

than 12 months (Van den End and Kruidhof, 2013). Thus, company can acquire information

from the financial statement by subtracting long term liabilities such as debt from the total

liabilities. Credit rating agencies: CRA is a company that assign credit ratings by analysing the ability

of the debtors to pay back their debt inclusion of timely interest payment. They also provide

information about the potential suppliers to the organizations at some charges (Sepúlveda

and Derpich, 2014). Social media: Looking at the present market, social media also has been using to keep in

touch with the suppliers regularly. Video sharing, blogs, social networking, microblogs etc.

are some of the ways available to the firms to regularly interact with the suppliers. Use of

social media is very effective, simple and quick to engage with the current and potential

suppliers and take competitive advantage through this (Sherry and Teece, 2015). Supplier

relationship management (SRM) is an very effective tool using by the organizations to

manage their supply chain and procurement process. Supplier websites: Present age is the age of technology in which transactions are settled by

using e-facility. As said earlier, that E-auction, E-tendering, E-catalogue and E-RFQ are

some of the examples of internet use in supplier appraisal process. In such respect,

information can be obtained from supplier's web portal, websites in which information is

already published and updated regularly (Saleem and Rehman, 2011). Through getting

access of the sites, business can know information about suppliers products, quality, prices,

policies and delivery time. Moreover, Supplibase is also an effective, dynamic and engaging

platform which is using by most of the organization to manage supply chain finance process.

This platform approve the invoices and settle payment on maturity date automatically and

transfer it into the account of the supplier (Paul and et.al., 2013). Along with this, in case,

when supplier need earlier payment before maturity date than it can discount invoices at

very less discount and transfer payment electronically. It is a connecting enterprise which

connect both suppliers and buyers for their objectives. Corporations can also see buyers

reviews about the quality of offered products and services by the suppliers. It will greatly

helps entities in finding the suppliers who offer best quality material, affordable costs,

timely deliveries and favourable credit terms as well (Park, Shin, Chang and Park, 2010).

9

and current as well as non-current liabilities. In such respect, all the business liabilities

which will be paid within the time period of one year, is called current or short-term

liabilities. Suppliers are the part of current liabilities as they supply material for credit of less

than 12 months (Van den End and Kruidhof, 2013). Thus, company can acquire information

from the financial statement by subtracting long term liabilities such as debt from the total

liabilities. Credit rating agencies: CRA is a company that assign credit ratings by analysing the ability

of the debtors to pay back their debt inclusion of timely interest payment. They also provide

information about the potential suppliers to the organizations at some charges (Sepúlveda

and Derpich, 2014). Social media: Looking at the present market, social media also has been using to keep in

touch with the suppliers regularly. Video sharing, blogs, social networking, microblogs etc.

are some of the ways available to the firms to regularly interact with the suppliers. Use of

social media is very effective, simple and quick to engage with the current and potential

suppliers and take competitive advantage through this (Sherry and Teece, 2015). Supplier

relationship management (SRM) is an very effective tool using by the organizations to

manage their supply chain and procurement process. Supplier websites: Present age is the age of technology in which transactions are settled by

using e-facility. As said earlier, that E-auction, E-tendering, E-catalogue and E-RFQ are

some of the examples of internet use in supplier appraisal process. In such respect,

information can be obtained from supplier's web portal, websites in which information is

already published and updated regularly (Saleem and Rehman, 2011). Through getting

access of the sites, business can know information about suppliers products, quality, prices,

policies and delivery time. Moreover, Supplibase is also an effective, dynamic and engaging

platform which is using by most of the organization to manage supply chain finance process.

This platform approve the invoices and settle payment on maturity date automatically and

transfer it into the account of the supplier (Paul and et.al., 2013). Along with this, in case,

when supplier need earlier payment before maturity date than it can discount invoices at

very less discount and transfer payment electronically. It is a connecting enterprise which

connect both suppliers and buyers for their objectives. Corporations can also see buyers

reviews about the quality of offered products and services by the suppliers. It will greatly

helps entities in finding the suppliers who offer best quality material, affordable costs,

timely deliveries and favourable credit terms as well (Park, Shin, Chang and Park, 2010).

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

This in turn, firm will be able to satisfy global demand of the consumers on timely manner. Other appropriate publications: Trade associations of each and every industry also provide

huge assistance to match most suitable supplier as per corporation need. Moreover, business

advisers such as chamber of commerce also can provide directions to acquire information

about potential suppliers. Trade magazines and global source exhibitions are also the sources

available to an entity to assess suppliers available in the business (Lartey, Antwi and Boadi,

2013). Furthermore, directories such as yellow pages also helps to have a look for the

suppliers in local business area. In such context, Global Source Online is a comprehensive

set of online directory that give a detail list of all the verified and unverified suppliers.

Through verified suppliers, businesses can ensure that each supplier is an authentic company

who is legally registered in the market.

Assessment of financial statements to evaluate financial, commercial and technical capabilities

of potential suppliers in the sourcing process

Companies has to evaluate the ability of supplier in financial, commercial and technical

context to assess most appropriate supplier.

Financial capability: As already said, that financial statements are the source of financial

information of the business. Thus, business can determine financial capability of the suppliers by

evaluating their financial accounts (Kumbirai and Webb, 2013). Through this, buyers can assess

profitability, liquidity, solvency and cash flow position of the suppliers and select supplier who is

financial stable. For this, ratio analysis has been conducted which emphasized that profitability

performance and liquidity position of the supplier is good. While, gearing position of the supplier is

not very good because it use only the equity capital in its capital structure (Karande and

Chakraborty, 2012).

Technical capability refers to the ability of supplier to offer technological equipments and

services to meet corporation demand (Kiruri, 2013). On the basis of such factors, it can be

recommended that company has to chose supplier who have huge ability to offer new, innovative

and technological products and services. So that, companies can attract more and more customers

by providing qualitative services. It provide advantage of enlarge turnover, sales, customer base and

market share as well (Gervais, Levant and Ducrocq, 2010).

Commercial ability: It comprises willingness or ability to share market risk, location,

operating management system, product prices, service quality, environmental policy etc. Supplier

who provide quality services at cheaper prices, deliver goods on time and fulfil environmental laws

and regulations is often gains preference over others.

After evaluating financial performance and determining supplier appraisal process, it can be

10

huge assistance to match most suitable supplier as per corporation need. Moreover, business

advisers such as chamber of commerce also can provide directions to acquire information

about potential suppliers. Trade magazines and global source exhibitions are also the sources

available to an entity to assess suppliers available in the business (Lartey, Antwi and Boadi,

2013). Furthermore, directories such as yellow pages also helps to have a look for the

suppliers in local business area. In such context, Global Source Online is a comprehensive

set of online directory that give a detail list of all the verified and unverified suppliers.

Through verified suppliers, businesses can ensure that each supplier is an authentic company

who is legally registered in the market.

Assessment of financial statements to evaluate financial, commercial and technical capabilities

of potential suppliers in the sourcing process

Companies has to evaluate the ability of supplier in financial, commercial and technical

context to assess most appropriate supplier.

Financial capability: As already said, that financial statements are the source of financial

information of the business. Thus, business can determine financial capability of the suppliers by

evaluating their financial accounts (Kumbirai and Webb, 2013). Through this, buyers can assess

profitability, liquidity, solvency and cash flow position of the suppliers and select supplier who is

financial stable. For this, ratio analysis has been conducted which emphasized that profitability

performance and liquidity position of the supplier is good. While, gearing position of the supplier is

not very good because it use only the equity capital in its capital structure (Karande and

Chakraborty, 2012).

Technical capability refers to the ability of supplier to offer technological equipments and

services to meet corporation demand (Kiruri, 2013). On the basis of such factors, it can be

recommended that company has to chose supplier who have huge ability to offer new, innovative

and technological products and services. So that, companies can attract more and more customers

by providing qualitative services. It provide advantage of enlarge turnover, sales, customer base and

market share as well (Gervais, Levant and Ducrocq, 2010).

Commercial ability: It comprises willingness or ability to share market risk, location,

operating management system, product prices, service quality, environmental policy etc. Supplier

who provide quality services at cheaper prices, deliver goods on time and fulfil environmental laws

and regulations is often gains preference over others.

After evaluating financial performance and determining supplier appraisal process, it can be

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

recommended that companies should identify information about potential suppliers Global Online

Source and Supplibase web portal. So that, it can determine prominent and authentic supplier in the

form of verified suppliers. Supplibase information also provide assistance to company to settle

transactions automatically. Moreover, in the souring option, it has to select multiple supplier so that

risk of selecting wrong supplier can be eliminated. After this, company has to set some criteria in

relation to price, quality, quantity, timely delivery, environment responsibility etc. At the end, firms

has to compare actual performance of the supplier against the set standards for the corporate award

program.

CONCLUSION

The report concluded that supplier appraisal process will make an significant contribution to

assess financial stability, performance, commercial ability, technical capability so that organization

can determine most suitable supplier. It will ultimately help firm to gain quicker and timely receipts

of quality products at affordable prices. Through this, company will be able to meet customer

demand timely. This in turn, it can enlarge its market share, manage their suppliers, turnover,

profitability and take benefits of competitive advantages as well.

11

Source and Supplibase web portal. So that, it can determine prominent and authentic supplier in the

form of verified suppliers. Supplibase information also provide assistance to company to settle

transactions automatically. Moreover, in the souring option, it has to select multiple supplier so that

risk of selecting wrong supplier can be eliminated. After this, company has to set some criteria in

relation to price, quality, quantity, timely delivery, environment responsibility etc. At the end, firms

has to compare actual performance of the supplier against the set standards for the corporate award

program.

CONCLUSION

The report concluded that supplier appraisal process will make an significant contribution to

assess financial stability, performance, commercial ability, technical capability so that organization

can determine most suitable supplier. It will ultimately help firm to gain quicker and timely receipts

of quality products at affordable prices. Through this, company will be able to meet customer

demand timely. This in turn, it can enlarge its market share, manage their suppliers, turnover,

profitability and take benefits of competitive advantages as well.

11

REFERENCES

Books and Journals

Gervais, M., Levant, Y. and Ducrocq, C., 2010. Time-driven activity-based costing (TDABC): An

initial appraisal through a longitudinal case study.Journal of Applied Management Accounting

Research. 8(2), pp.1

Glass, C.A. and Knight, R.A., 2010. The nurse rostering problem: A critical appraisal of the

problem structure. European Journal of Operational Research. 202(2). pp.379-389.

Karande, P. and Chakraborty, S., 2012. Application of multi-objective optimization on the basis of

ratio analysis (MOORA) method for materials selection. Materials & Design. 37, pp.317-324.

Kiruri, S.N., 2013. Role of supplier appraisal on management of public procurement at Rift Valley

Water Services Board, Nakuru. International Journal of Social Sciences and

Entrepreneurship. 1(5). pp.384-414.

Kumbirai, M. and Webb, R., 2013. A financial ratio analysis of commercial bank performance in

South Africa. African Review of Economics and Finance. 2(1), pp.30-53.

Lartey, V.C., Antwi, S. and Boadi, E.K., 2013. The relationship between liquidity and profitability

of listed banks in Ghana. International Journal of Business and Social Science. 4(3).

Park, J., Shin, K., Chang, T. W. and Park, J., 2010. An integrative framework for supplier

relationship management. Industrial Management & Data Systems. 110(4). pp.495-515.

Paul, M.C. and et.al., 2013. Analytical models for delivery performance of a supplier or a service

provider. American Journal of Industrial and Business Management. 3(06). pp.39.

Saleem, Q. and Rehman, R.U., 2011. Impact of Liquidity Ratios on Profitability. Interdisciplinary

Journal of Research in Business. 1(7), pp.95-98.

Sepúlveda, J. M. and Derpich, I. S., 2014. Automated Reasoning for Supplier Performance

Appraisal in Supply Chains. Procedia Computer Science. 31. pp.966-975.

Sherry, E.F. and Teece, D., 2015. Patent Thickets: An Economic Appraisal.Tusher Center for the

Management of Intellectual Capital, Working Paper Series, (1).

van den End, J.W. and Kruidhof, M., 2013. Modelling the liquidity ratio as macroprudential

instrument. Journal of Banking Regulation. 14(2). pp.91-106.

Vodova, P., 2011. Liquidity of Czech commercial banks and its determinants.International Journal

of Mathematical Models and Methods in Applied Sciences. 5(6). pp.1060-1067.

Wang, Q., Kayande, U. and Jap, S., 2010. The seeds of dissolution: discrepancy and incoherence in

buyer-supplier exchange. Marketing Science. 29(6). pp.1109-1124.

Wu, D., Rossetti, M. D. and Tepper, J. E., 2015. Possibility of Inventory Pooling in China’s public

12

Books and Journals

Gervais, M., Levant, Y. and Ducrocq, C., 2010. Time-driven activity-based costing (TDABC): An

initial appraisal through a longitudinal case study.Journal of Applied Management Accounting

Research. 8(2), pp.1

Glass, C.A. and Knight, R.A., 2010. The nurse rostering problem: A critical appraisal of the

problem structure. European Journal of Operational Research. 202(2). pp.379-389.

Karande, P. and Chakraborty, S., 2012. Application of multi-objective optimization on the basis of

ratio analysis (MOORA) method for materials selection. Materials & Design. 37, pp.317-324.

Kiruri, S.N., 2013. Role of supplier appraisal on management of public procurement at Rift Valley

Water Services Board, Nakuru. International Journal of Social Sciences and

Entrepreneurship. 1(5). pp.384-414.

Kumbirai, M. and Webb, R., 2013. A financial ratio analysis of commercial bank performance in

South Africa. African Review of Economics and Finance. 2(1), pp.30-53.

Lartey, V.C., Antwi, S. and Boadi, E.K., 2013. The relationship between liquidity and profitability

of listed banks in Ghana. International Journal of Business and Social Science. 4(3).

Park, J., Shin, K., Chang, T. W. and Park, J., 2010. An integrative framework for supplier

relationship management. Industrial Management & Data Systems. 110(4). pp.495-515.

Paul, M.C. and et.al., 2013. Analytical models for delivery performance of a supplier or a service

provider. American Journal of Industrial and Business Management. 3(06). pp.39.

Saleem, Q. and Rehman, R.U., 2011. Impact of Liquidity Ratios on Profitability. Interdisciplinary

Journal of Research in Business. 1(7), pp.95-98.

Sepúlveda, J. M. and Derpich, I. S., 2014. Automated Reasoning for Supplier Performance

Appraisal in Supply Chains. Procedia Computer Science. 31. pp.966-975.

Sherry, E.F. and Teece, D., 2015. Patent Thickets: An Economic Appraisal.Tusher Center for the

Management of Intellectual Capital, Working Paper Series, (1).

van den End, J.W. and Kruidhof, M., 2013. Modelling the liquidity ratio as macroprudential

instrument. Journal of Banking Regulation. 14(2). pp.91-106.

Vodova, P., 2011. Liquidity of Czech commercial banks and its determinants.International Journal

of Mathematical Models and Methods in Applied Sciences. 5(6). pp.1060-1067.

Wang, Q., Kayande, U. and Jap, S., 2010. The seeds of dissolution: discrepancy and incoherence in

buyer-supplier exchange. Marketing Science. 29(6). pp.1109-1124.

Wu, D., Rossetti, M. D. and Tepper, J. E., 2015. Possibility of Inventory Pooling in China’s public

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.