Preparation and Analysis of AWM Manufacturing Budget for 2019

VerifiedAdded on 2022/12/09

|7

|1544

|236

Project

AI Summary

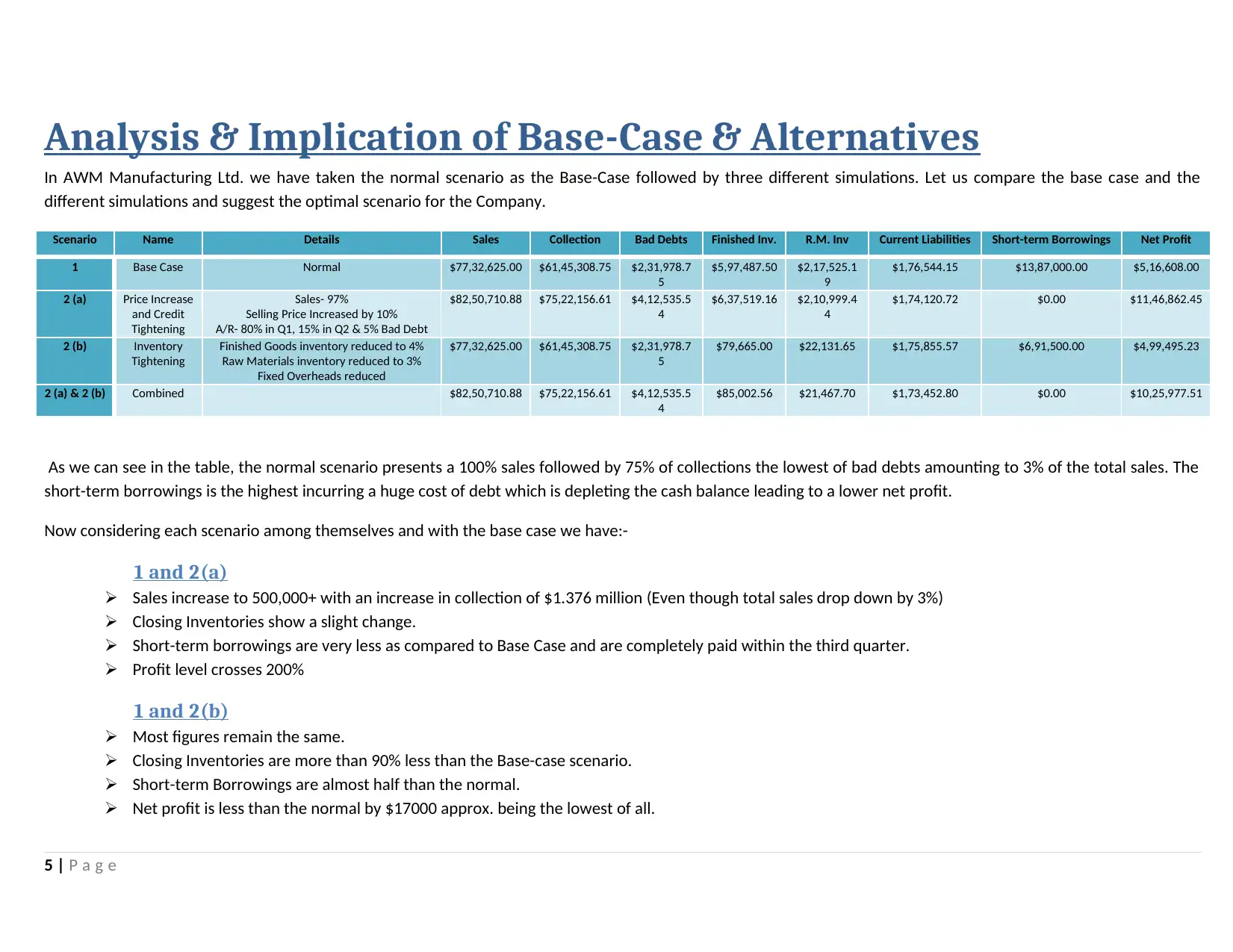

This project presents a comprehensive budget analysis for AWM Manufacturing Ltd. for the year 2019. It starts with the preparation of a base-case budget using provided accounting information and then proceeds with the analysis of this budget across various financial metrics, including net sales, collections, inventory levels, debt costs, and net profit. The project further explores multiple scenarios through simulations, considering factors like price increases, credit tightening, and inventory adjustments. These alternative scenarios are then compared against the base case to identify an optimal budget plan that maximizes the company's long-term wealth. Additionally, the analysis includes suggestions for improving budget efficiency, such as break-even analysis and working capital management, along with a brief introduction to the Balanced Scorecard as an informational reference for the management's consideration. The project concludes with recommendations regarding dividend payments, emphasizing the importance of a balanced approach to maintain shareholder trust while ensuring the company's financial stability.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.