AYB200 Financial Accounting: Aerodrone Limited & Accounting Standards

VerifiedAdded on 2023/04/21

|7

|1454

|214

Report

AI Summary

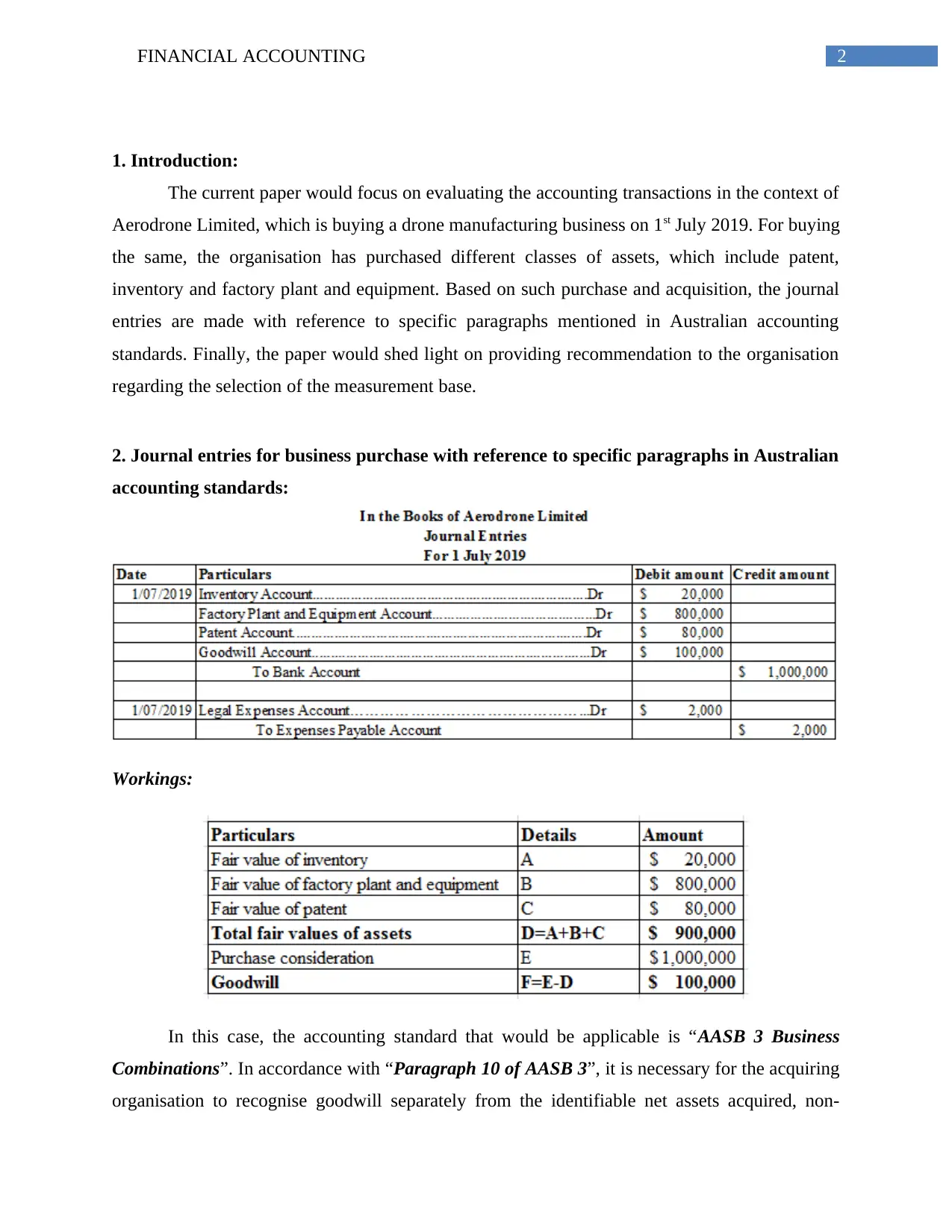

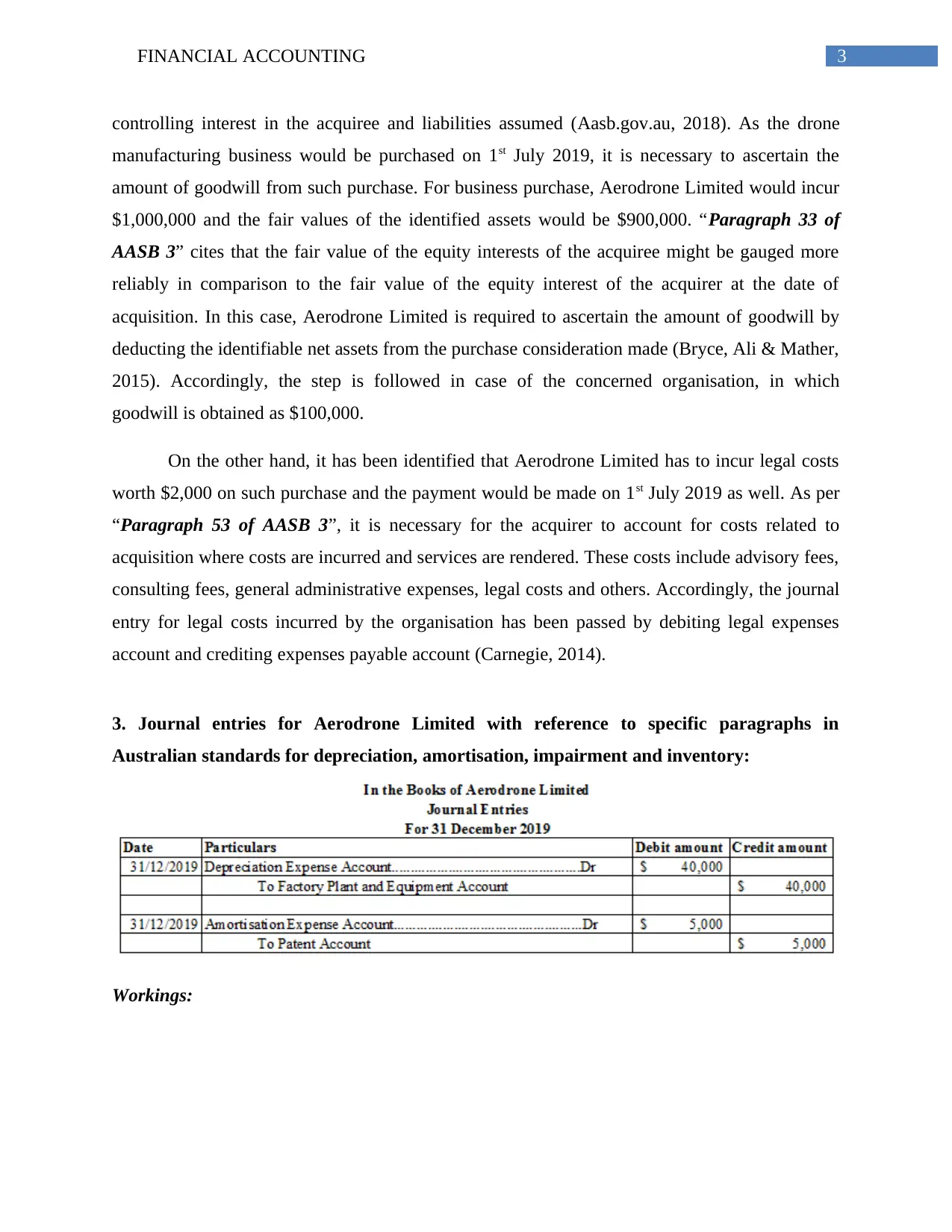

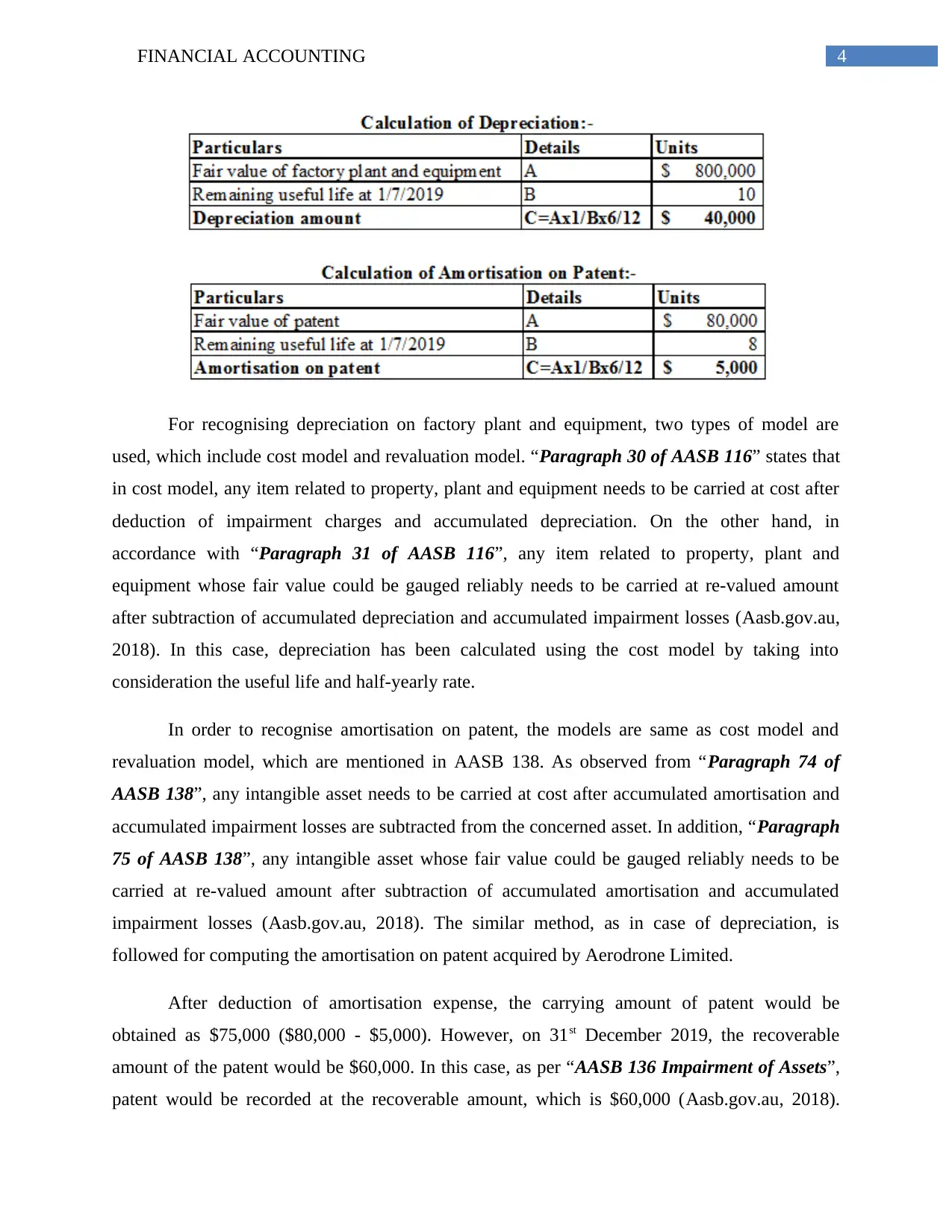

This report evaluates the accounting transactions of Aerodrone Limited, focusing on its acquisition of a drone manufacturing business. It details journal entries related to the purchase, referencing specific paragraphs in Australian Accounting Standards (AASB), particularly AASB 3 concerning business combinations and the recognition of goodwill. The report also addresses depreciation, amortization, impairment, and inventory valuation, citing AASB 116, AASB 138, and AASB 136. Furthermore, it recommends a measurement basis, contrasting fair value and value-in-use, based on Conceptual Framework guidelines. The analysis covers legal costs, asset valuation, and the impact of technological advancements on recoverable amounts, providing a comprehensive overview of financial accounting principles in the context of Aerodrone Limited's business activities. Desklib provides students with access to a wealth of resources, including past papers and solved assignments, to aid in their studies.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.