AYB340: Mid-Semester Exam - Company Accounting, Semester 2, 2019

VerifiedAdded on 2022/12/14

|12

|3130

|191

Quiz and Exam

AI Summary

This document presents the solutions to the AYB340 Company Accounting Mid-Semester Exam, covering key concepts from topics 1-4. The exam includes multiple-choice questions on topics like events after the reporting date, accounting policies, errors, and the presentation of financial statements, including trade receivables and inventory. It also delves into deferred tax assets and liabilities, taxable and deductible temporary differences, and the calculation of current tax liabilities. Furthermore, the solutions address business combinations, including gain on bargain purchase and the journal entries required for the acquisition of net assets. The exam assesses understanding of AASB standards and their application in practical scenarios. This resource provides a comprehensive guide for students to review and understand the concepts covered in the exam, assisting with preparation and reinforcing knowledge of financial accounting principles.

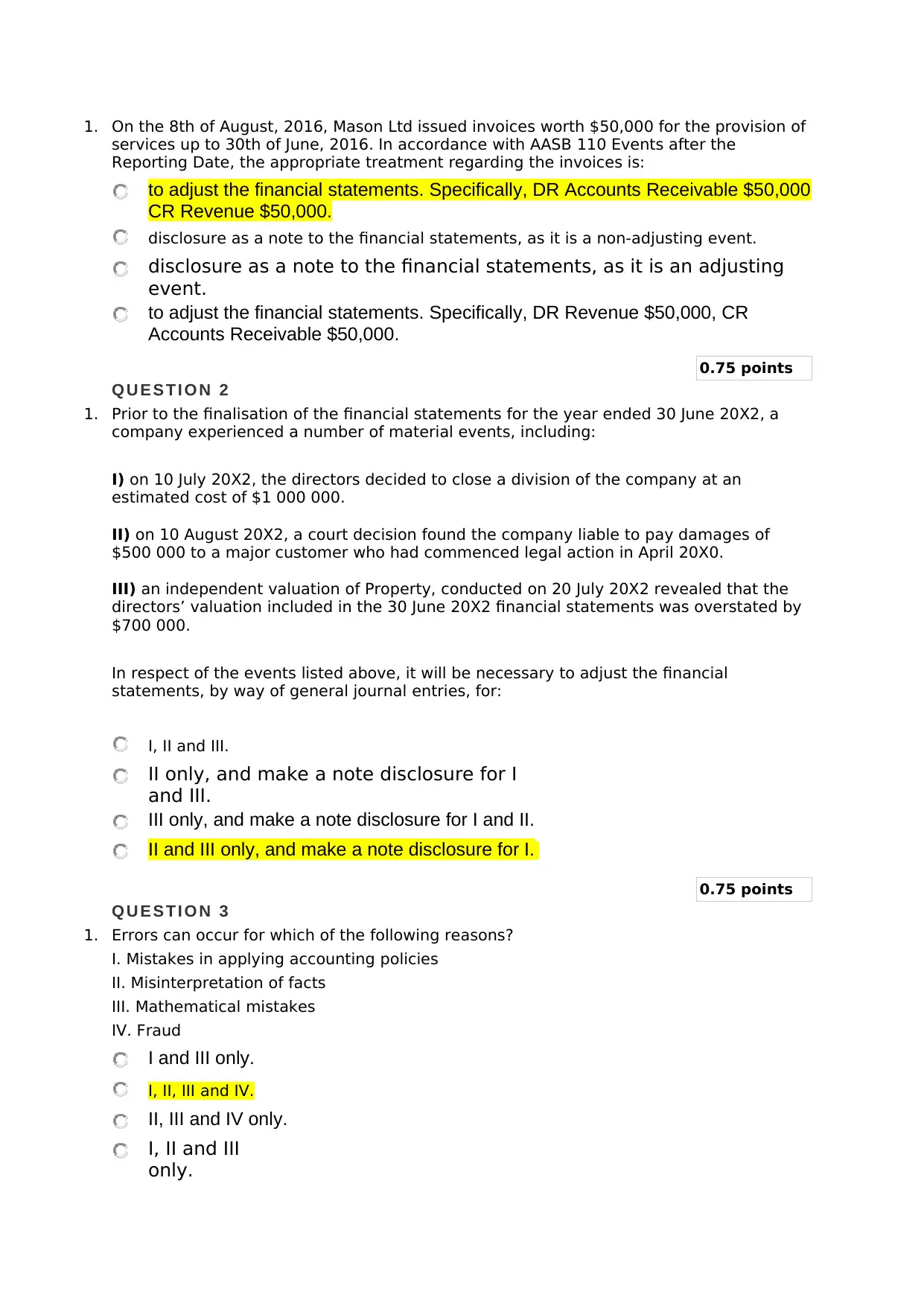

1. On the 8th of August, 2016, Mason Ltd issued invoices worth $50,000 for the provision of

services up to 30th of June, 2016. In accordance with AASB 110 Events after the

Reporting Date, the appropriate treatment regarding the invoices is:

to adjust the financial statements. Specifically, DR Accounts Receivable $50,000

CR Revenue $50,000.

disclosure as a note to the financial statements, as it is a non-adjusting event.

disclosure as a note to the financial statements, as it is an adjusting

event.

to adjust the financial statements. Specifically, DR Revenue $50,000, CR

Accounts Receivable $50,000.

0.75 points

Q U E S T I O N 2

1. Prior to the finalisation of the financial statements for the year ended 30 June 20X2, a

company experienced a number of material events, including:

I) on 10 July 20X2, the directors decided to close a division of the company at an

estimated cost of $1 000 000.

II) on 10 August 20X2, a court decision found the company liable to pay damages of

$500 000 to a major customer who had commenced legal action in April 20X0.

III) an independent valuation of Property, conducted on 20 July 20X2 revealed that the

directors’ valuation included in the 30 June 20X2 financial statements was overstated by

$700 000.

In respect of the events listed above, it will be necessary to adjust the financial

statements, by way of general journal entries, for:

I, II and III.

II only, and make a note disclosure for I

and III.

III only, and make a note disclosure for I and II.

II and III only, and make a note disclosure for I.

0.75 points

Q U E S T I O N 3

1. Errors can occur for which of the following reasons?

I. Mistakes in applying accounting policies

II. Misinterpretation of facts

III. Mathematical mistakes

IV. Fraud

I and III only.

I, II, III and IV.

II, III and IV only.

I, II and III

only.

services up to 30th of June, 2016. In accordance with AASB 110 Events after the

Reporting Date, the appropriate treatment regarding the invoices is:

to adjust the financial statements. Specifically, DR Accounts Receivable $50,000

CR Revenue $50,000.

disclosure as a note to the financial statements, as it is a non-adjusting event.

disclosure as a note to the financial statements, as it is an adjusting

event.

to adjust the financial statements. Specifically, DR Revenue $50,000, CR

Accounts Receivable $50,000.

0.75 points

Q U E S T I O N 2

1. Prior to the finalisation of the financial statements for the year ended 30 June 20X2, a

company experienced a number of material events, including:

I) on 10 July 20X2, the directors decided to close a division of the company at an

estimated cost of $1 000 000.

II) on 10 August 20X2, a court decision found the company liable to pay damages of

$500 000 to a major customer who had commenced legal action in April 20X0.

III) an independent valuation of Property, conducted on 20 July 20X2 revealed that the

directors’ valuation included in the 30 June 20X2 financial statements was overstated by

$700 000.

In respect of the events listed above, it will be necessary to adjust the financial

statements, by way of general journal entries, for:

I, II and III.

II only, and make a note disclosure for I

and III.

III only, and make a note disclosure for I and II.

II and III only, and make a note disclosure for I.

0.75 points

Q U E S T I O N 3

1. Errors can occur for which of the following reasons?

I. Mistakes in applying accounting policies

II. Misinterpretation of facts

III. Mathematical mistakes

IV. Fraud

I and III only.

I, II, III and IV.

II, III and IV only.

I, II and III

only.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

0.75 points

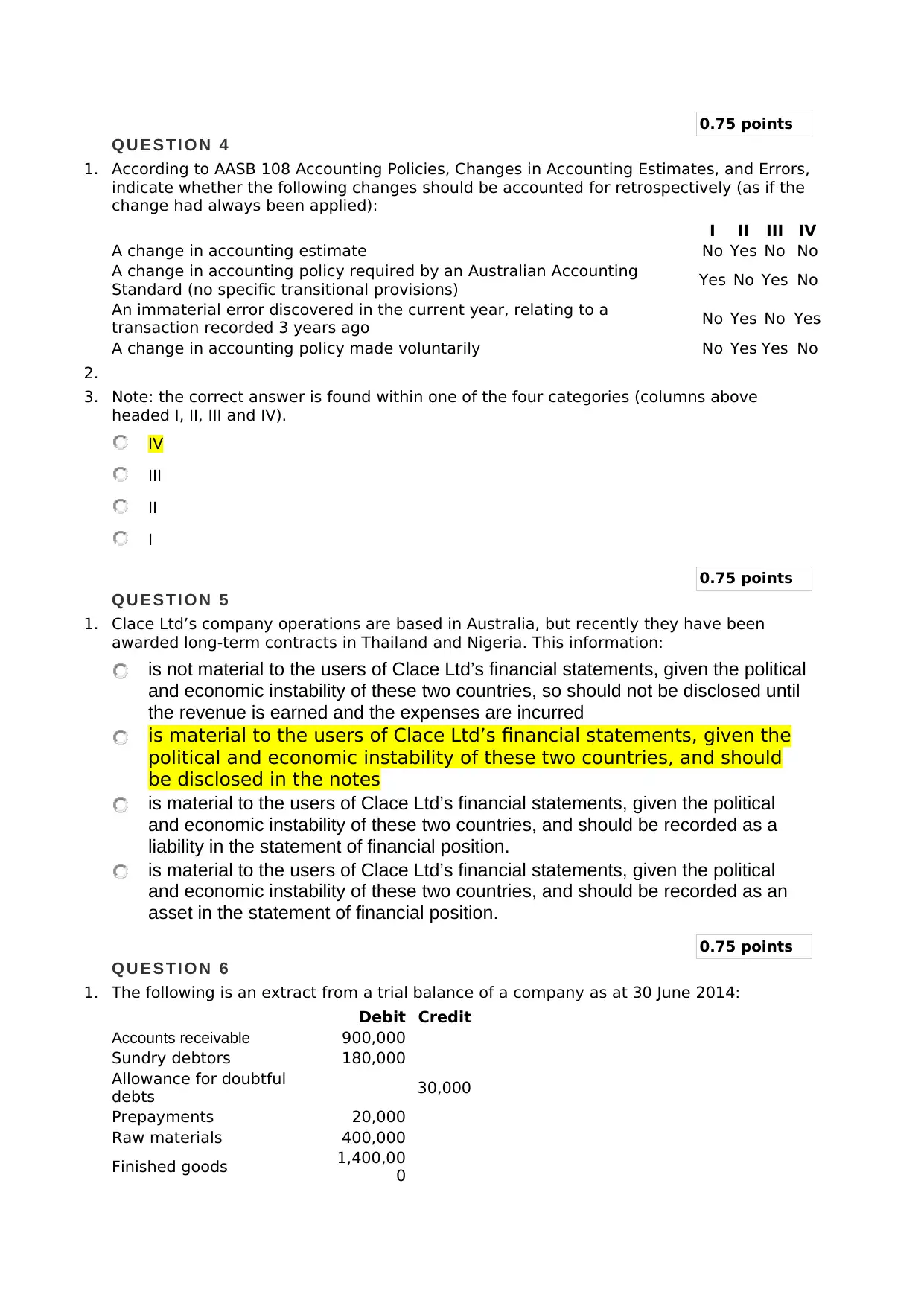

Q U E S T I O N 4

1. According to AASB 108 Accounting Policies, Changes in Accounting Estimates, and Errors,

indicate whether the following changes should be accounted for retrospectively (as if the

change had always been applied):

I II III IV

A change in accounting estimate No Yes No No

A change in accounting policy required by an Australian Accounting

Standard (no specific transitional provisions) Yes No Yes No

An immaterial error discovered in the current year, relating to a

transaction recorded 3 years ago No Yes No Yes

A change in accounting policy made voluntarily No Yes Yes No

2.

3. Note: the correct answer is found within one of the four categories (columns above

headed I, II, III and IV).

IV

III

II

I

0.75 points

Q U E S T I O N 5

1. Clace Ltd’s company operations are based in Australia, but recently they have been

awarded long-term contracts in Thailand and Nigeria. This information:

is not material to the users of Clace Ltd’s financial statements, given the political

and economic instability of these two countries, so should not be disclosed until

the revenue is earned and the expenses are incurred

is material to the users of Clace Ltd’s financial statements, given the

political and economic instability of these two countries, and should

be disclosed in the notes

is material to the users of Clace Ltd’s financial statements, given the political

and economic instability of these two countries, and should be recorded as a

liability in the statement of financial position.

is material to the users of Clace Ltd’s financial statements, given the political

and economic instability of these two countries, and should be recorded as an

asset in the statement of financial position.

0.75 points

Q U E S T I O N 6

1. The following is an extract from a trial balance of a company as at 30 June 2014:

Debit Credit

Accounts receivable 900,000

Sundry debtors 180,000

Allowance for doubtful

debts 30,000

Prepayments 20,000

Raw materials 400,000

Finished goods 1,400,00

0

Q U E S T I O N 4

1. According to AASB 108 Accounting Policies, Changes in Accounting Estimates, and Errors,

indicate whether the following changes should be accounted for retrospectively (as if the

change had always been applied):

I II III IV

A change in accounting estimate No Yes No No

A change in accounting policy required by an Australian Accounting

Standard (no specific transitional provisions) Yes No Yes No

An immaterial error discovered in the current year, relating to a

transaction recorded 3 years ago No Yes No Yes

A change in accounting policy made voluntarily No Yes Yes No

2.

3. Note: the correct answer is found within one of the four categories (columns above

headed I, II, III and IV).

IV

III

II

I

0.75 points

Q U E S T I O N 5

1. Clace Ltd’s company operations are based in Australia, but recently they have been

awarded long-term contracts in Thailand and Nigeria. This information:

is not material to the users of Clace Ltd’s financial statements, given the political

and economic instability of these two countries, so should not be disclosed until

the revenue is earned and the expenses are incurred

is material to the users of Clace Ltd’s financial statements, given the

political and economic instability of these two countries, and should

be disclosed in the notes

is material to the users of Clace Ltd’s financial statements, given the political

and economic instability of these two countries, and should be recorded as a

liability in the statement of financial position.

is material to the users of Clace Ltd’s financial statements, given the political

and economic instability of these two countries, and should be recorded as an

asset in the statement of financial position.

0.75 points

Q U E S T I O N 6

1. The following is an extract from a trial balance of a company as at 30 June 2014:

Debit Credit

Accounts receivable 900,000

Sundry debtors 180,000

Allowance for doubtful

debts 30,000

Prepayments 20,000

Raw materials 400,000

Finished goods 1,400,00

0

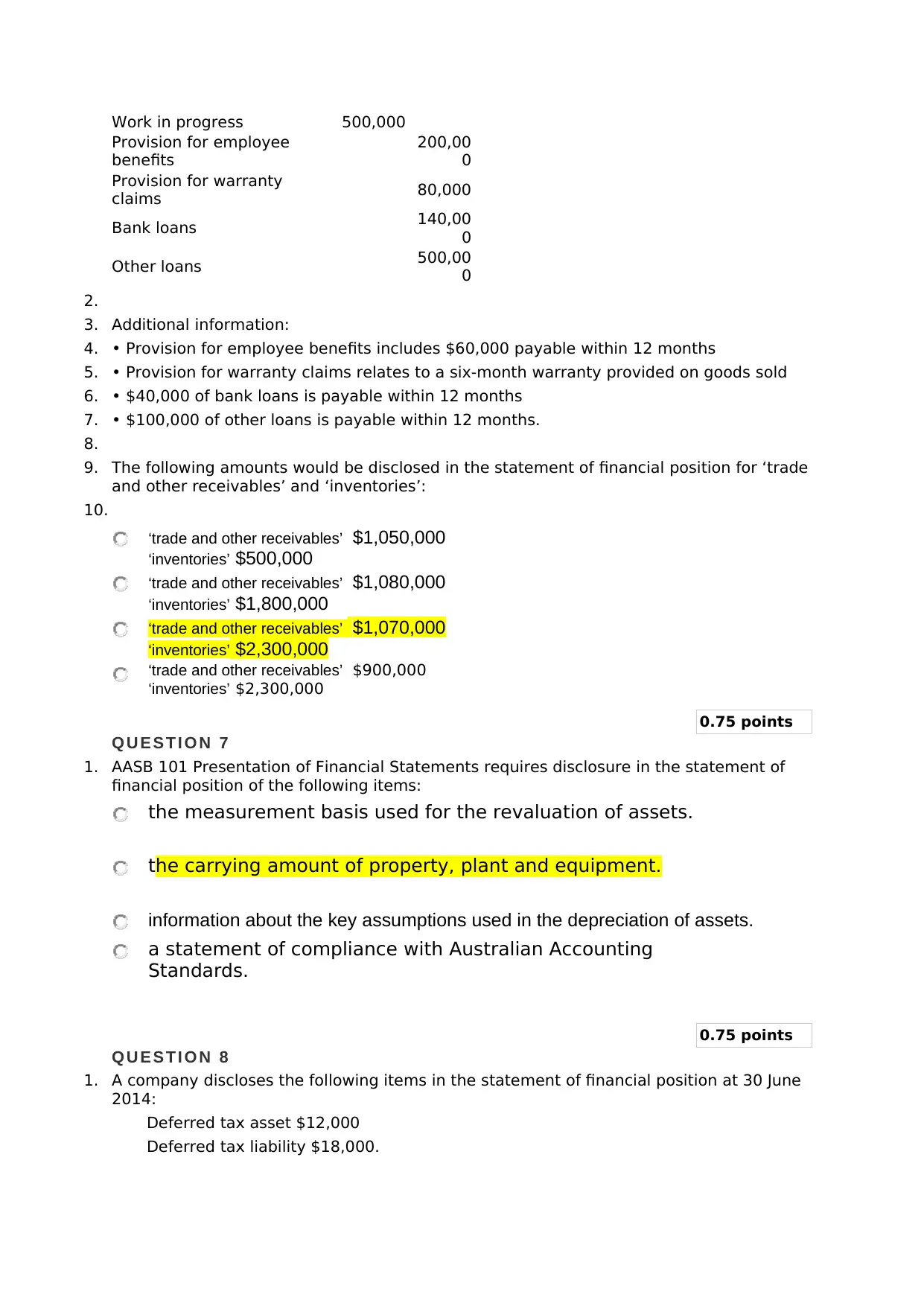

Work in progress 500,000

Provision for employee

benefits

200,00

0

Provision for warranty

claims 80,000

Bank loans 140,00

0

Other loans 500,00

0

2.

3. Additional information:

4. • Provision for employee benefits includes $60,000 payable within 12 months

5. • Provision for warranty claims relates to a six-month warranty provided on goods sold

6. • $40,000 of bank loans is payable within 12 months

7. • $100,000 of other loans is payable within 12 months.

8.

9. The following amounts would be disclosed in the statement of financial position for ‘trade

and other receivables’ and ‘inventories’:

10.

‘trade and other receivables’ $1,050,000

‘inventories’ $500,000

‘trade and other receivables’ $1,080,000

‘inventories’ $1,800,000

‘trade and other receivables’ $1,070,000

‘inventories’ $2,300,000

‘trade and other receivables’ $900,000

‘inventories’ $2,300,000

0.75 points

Q U E S T I O N 7

1. AASB 101 Presentation of Financial Statements requires disclosure in the statement of

financial position of the following items:

the measurement basis used for the revaluation of assets.

the carrying amount of property, plant and equipment.

information about the key assumptions used in the depreciation of assets.

a statement of compliance with Australian Accounting

Standards.

0.75 points

Q U E S T I O N 8

1. A company discloses the following items in the statement of financial position at 30 June

2014:

Deferred tax asset $12,000

Deferred tax liability $18,000.

Provision for employee

benefits

200,00

0

Provision for warranty

claims 80,000

Bank loans 140,00

0

Other loans 500,00

0

2.

3. Additional information:

4. • Provision for employee benefits includes $60,000 payable within 12 months

5. • Provision for warranty claims relates to a six-month warranty provided on goods sold

6. • $40,000 of bank loans is payable within 12 months

7. • $100,000 of other loans is payable within 12 months.

8.

9. The following amounts would be disclosed in the statement of financial position for ‘trade

and other receivables’ and ‘inventories’:

10.

‘trade and other receivables’ $1,050,000

‘inventories’ $500,000

‘trade and other receivables’ $1,080,000

‘inventories’ $1,800,000

‘trade and other receivables’ $1,070,000

‘inventories’ $2,300,000

‘trade and other receivables’ $900,000

‘inventories’ $2,300,000

0.75 points

Q U E S T I O N 7

1. AASB 101 Presentation of Financial Statements requires disclosure in the statement of

financial position of the following items:

the measurement basis used for the revaluation of assets.

the carrying amount of property, plant and equipment.

information about the key assumptions used in the depreciation of assets.

a statement of compliance with Australian Accounting

Standards.

0.75 points

Q U E S T I O N 8

1. A company discloses the following items in the statement of financial position at 30 June

2014:

Deferred tax asset $12,000

Deferred tax liability $18,000.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

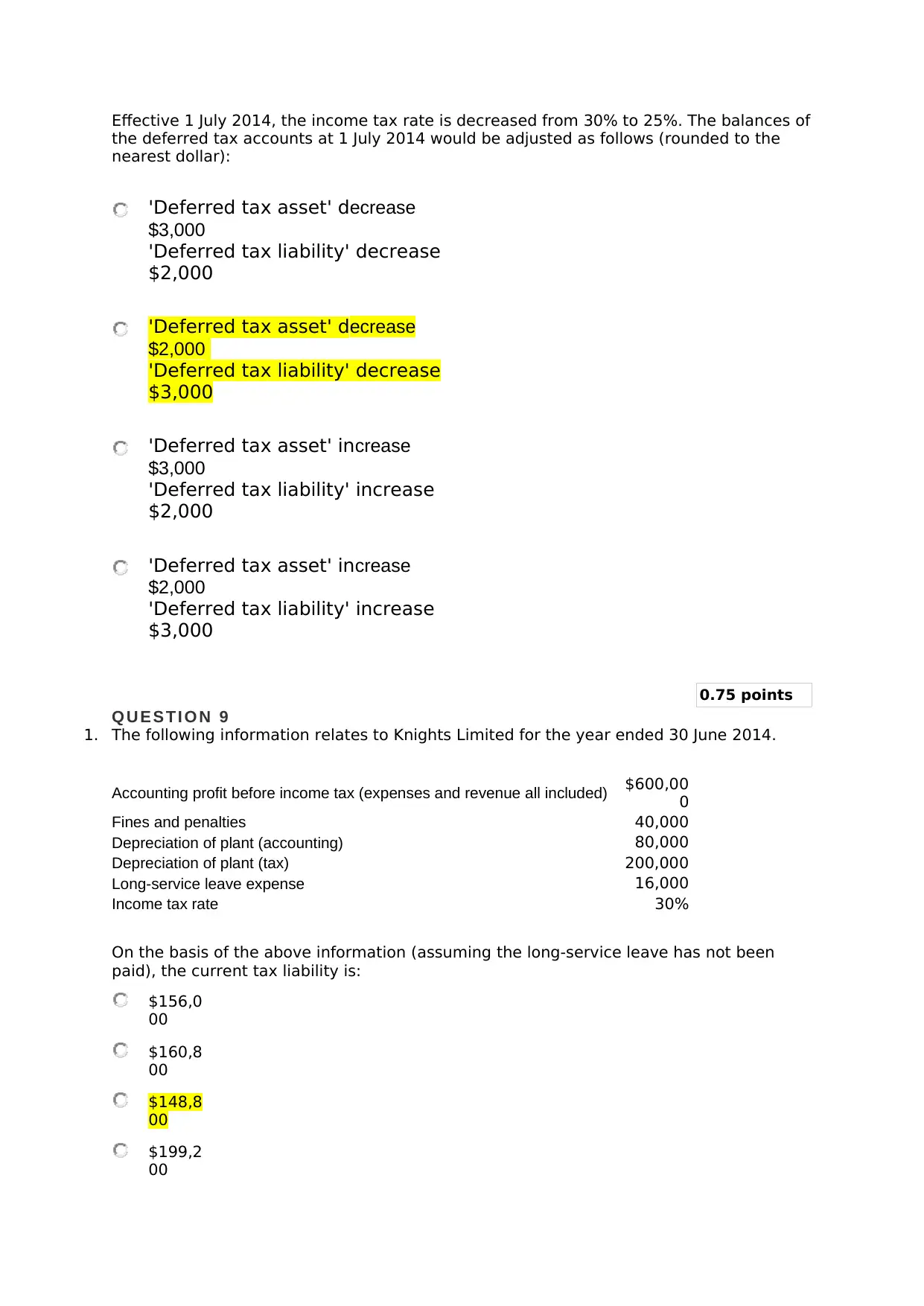

Effective 1 July 2014, the income tax rate is decreased from 30% to 25%. The balances of

the deferred tax accounts at 1 July 2014 would be adjusted as follows (rounded to the

nearest dollar):

'Deferred tax asset' decrease

$3,000

'Deferred tax liability' decrease

$2,000

'Deferred tax asset' decrease

$2,000

'Deferred tax liability' decrease

$3,000

'Deferred tax asset' increase

$3,000

'Deferred tax liability' increase

$2,000

'Deferred tax asset' increase

$2,000

'Deferred tax liability' increase

$3,000

0.75 points

Q U E S T I O N 9

1. The following information relates to Knights Limited for the year ended 30 June 2014.

Accounting profit before income tax (expenses and revenue all included) $600,00

0

Fines and penalties 40,000

Depreciation of plant (accounting) 80,000

Depreciation of plant (tax) 200,000

Long-service leave expense 16,000

Income tax rate 30%

On the basis of the above information (assuming the long-service leave has not been

paid), the current tax liability is:

$156,0

00

$160,8

00

$148,8

00

$199,2

00

the deferred tax accounts at 1 July 2014 would be adjusted as follows (rounded to the

nearest dollar):

'Deferred tax asset' decrease

$3,000

'Deferred tax liability' decrease

$2,000

'Deferred tax asset' decrease

$2,000

'Deferred tax liability' decrease

$3,000

'Deferred tax asset' increase

$3,000

'Deferred tax liability' increase

$2,000

'Deferred tax asset' increase

$2,000

'Deferred tax liability' increase

$3,000

0.75 points

Q U E S T I O N 9

1. The following information relates to Knights Limited for the year ended 30 June 2014.

Accounting profit before income tax (expenses and revenue all included) $600,00

0

Fines and penalties 40,000

Depreciation of plant (accounting) 80,000

Depreciation of plant (tax) 200,000

Long-service leave expense 16,000

Income tax rate 30%

On the basis of the above information (assuming the long-service leave has not been

paid), the current tax liability is:

$156,0

00

$160,8

00

$148,8

00

$199,2

00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

0.75 points

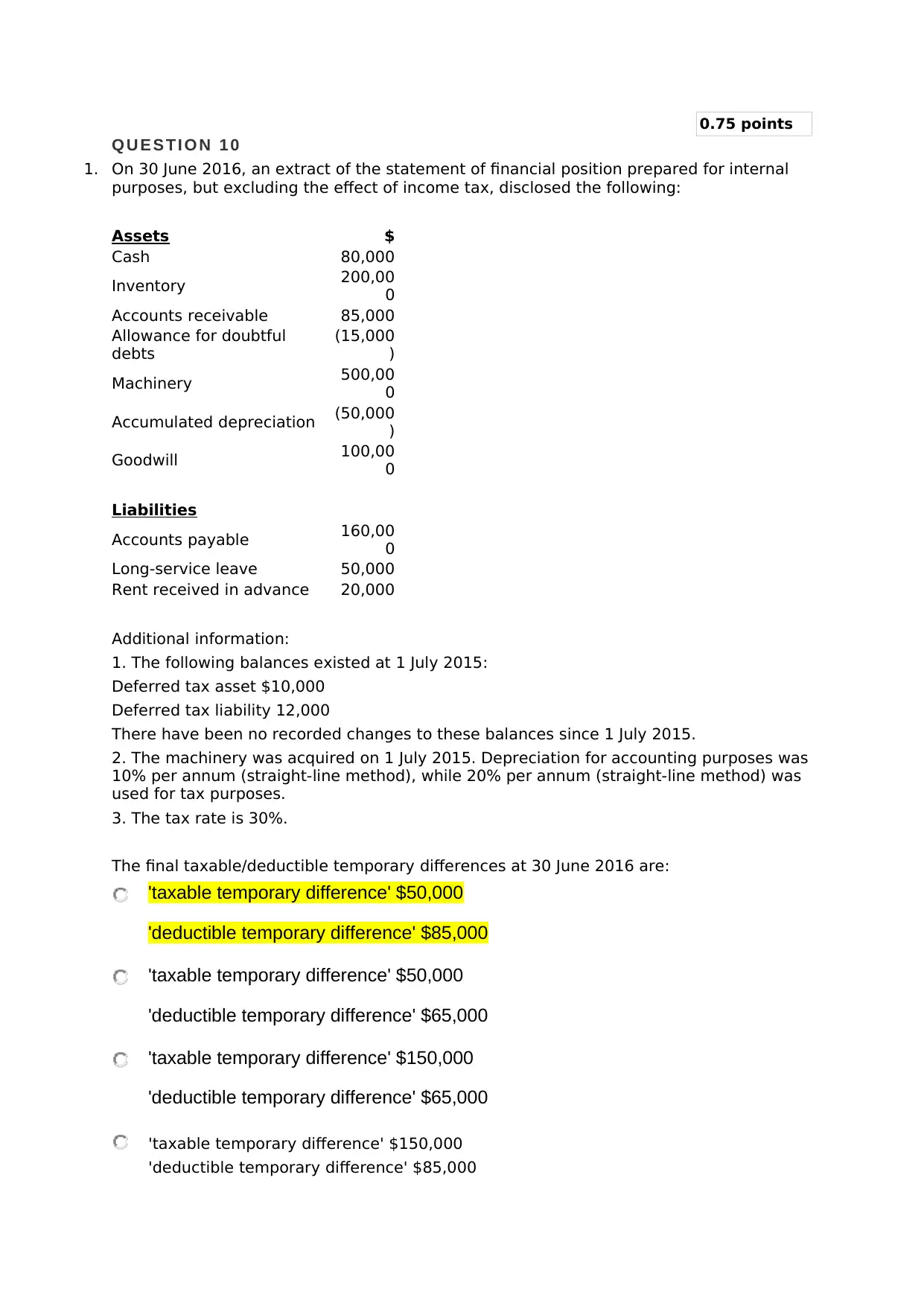

Q U E S T I O N 1 0

1. On 30 June 2016, an extract of the statement of financial position prepared for internal

purposes, but excluding the effect of income tax, disclosed the following:

Assets $

Cash 80,000

Inventory 200,00

0

Accounts receivable 85,000

Allowance for doubtful

debts

(15,000

)

Machinery 500,00

0

Accumulated depreciation (50,000

)

Goodwill 100,00

0

Liabilities

Accounts payable 160,00

0

Long-service leave 50,000

Rent received in advance 20,000

Additional information:

1. The following balances existed at 1 July 2015:

Deferred tax asset $10,000

Deferred tax liability 12,000

There have been no recorded changes to these balances since 1 July 2015.

2. The machinery was acquired on 1 July 2015. Depreciation for accounting purposes was

10% per annum (straight-line method), while 20% per annum (straight-line method) was

used for tax purposes.

3. The tax rate is 30%.

The final taxable/deductible temporary differences at 30 June 2016 are:

'taxable temporary difference' $50,000

'deductible temporary difference' $85,000

'taxable temporary difference' $50,000

'deductible temporary difference' $65,000

'taxable temporary difference' $150,000

'deductible temporary difference' $65,000

'taxable temporary difference' $150,000

'deductible temporary difference' $85,000

Q U E S T I O N 1 0

1. On 30 June 2016, an extract of the statement of financial position prepared for internal

purposes, but excluding the effect of income tax, disclosed the following:

Assets $

Cash 80,000

Inventory 200,00

0

Accounts receivable 85,000

Allowance for doubtful

debts

(15,000

)

Machinery 500,00

0

Accumulated depreciation (50,000

)

Goodwill 100,00

0

Liabilities

Accounts payable 160,00

0

Long-service leave 50,000

Rent received in advance 20,000

Additional information:

1. The following balances existed at 1 July 2015:

Deferred tax asset $10,000

Deferred tax liability 12,000

There have been no recorded changes to these balances since 1 July 2015.

2. The machinery was acquired on 1 July 2015. Depreciation for accounting purposes was

10% per annum (straight-line method), while 20% per annum (straight-line method) was

used for tax purposes.

3. The tax rate is 30%.

The final taxable/deductible temporary differences at 30 June 2016 are:

'taxable temporary difference' $50,000

'deductible temporary difference' $85,000

'taxable temporary difference' $50,000

'deductible temporary difference' $65,000

'taxable temporary difference' $150,000

'deductible temporary difference' $65,000

'taxable temporary difference' $150,000

'deductible temporary difference' $85,000

0.75 points

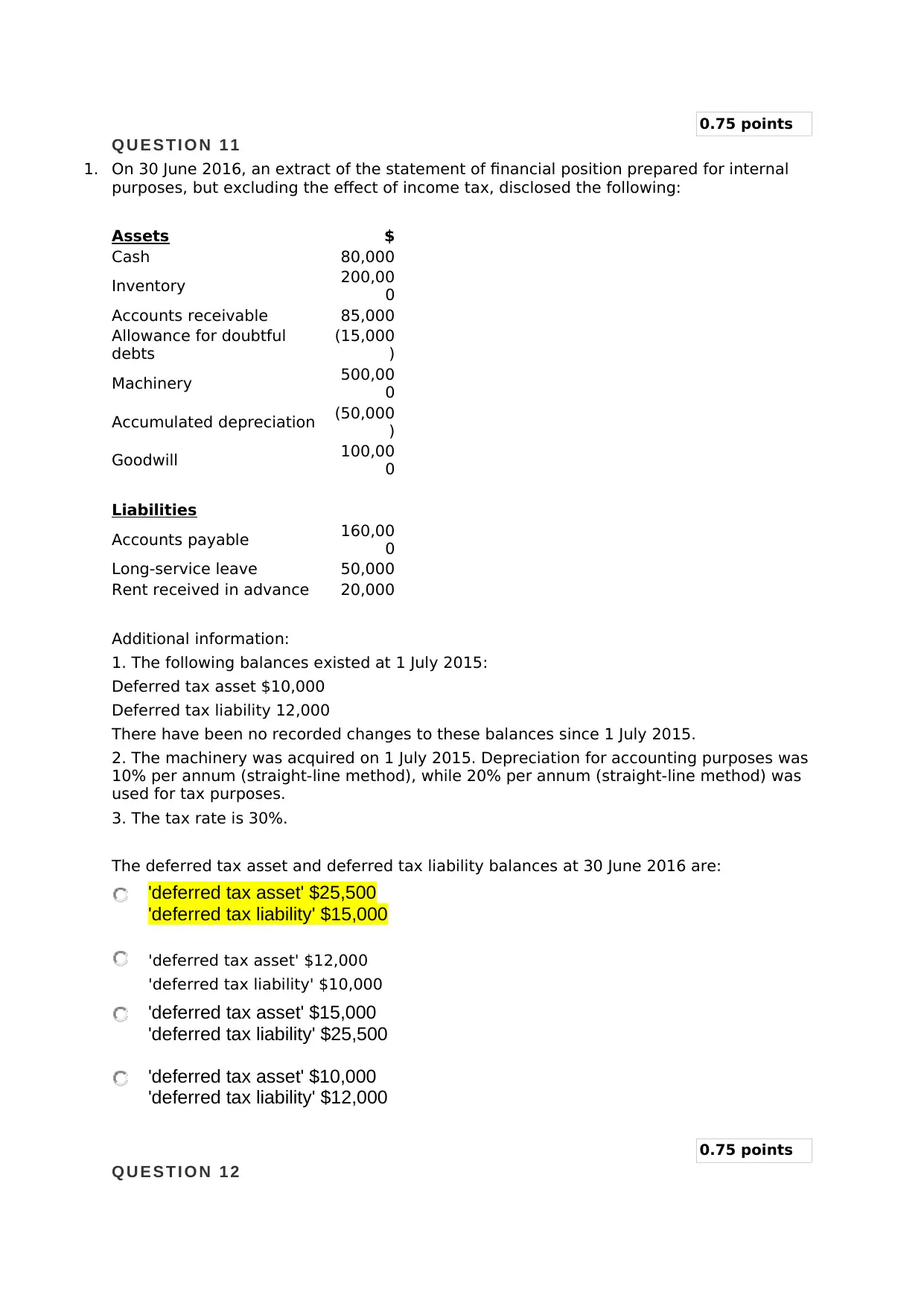

Q U E S T I O N 1 1

1. On 30 June 2016, an extract of the statement of financial position prepared for internal

purposes, but excluding the effect of income tax, disclosed the following:

Assets $

Cash 80,000

Inventory 200,00

0

Accounts receivable 85,000

Allowance for doubtful

debts

(15,000

)

Machinery 500,00

0

Accumulated depreciation (50,000

)

Goodwill 100,00

0

Liabilities

Accounts payable 160,00

0

Long-service leave 50,000

Rent received in advance 20,000

Additional information:

1. The following balances existed at 1 July 2015:

Deferred tax asset $10,000

Deferred tax liability 12,000

There have been no recorded changes to these balances since 1 July 2015.

2. The machinery was acquired on 1 July 2015. Depreciation for accounting purposes was

10% per annum (straight-line method), while 20% per annum (straight-line method) was

used for tax purposes.

3. The tax rate is 30%.

The deferred tax asset and deferred tax liability balances at 30 June 2016 are:

'deferred tax asset' $25,500

'deferred tax liability' $15,000

'deferred tax asset' $12,000

'deferred tax liability' $10,000

'deferred tax asset' $15,000

'deferred tax liability' $25,500

'deferred tax asset' $10,000

'deferred tax liability' $12,000

0.75 points

Q U E S T I O N 1 2

Q U E S T I O N 1 1

1. On 30 June 2016, an extract of the statement of financial position prepared for internal

purposes, but excluding the effect of income tax, disclosed the following:

Assets $

Cash 80,000

Inventory 200,00

0

Accounts receivable 85,000

Allowance for doubtful

debts

(15,000

)

Machinery 500,00

0

Accumulated depreciation (50,000

)

Goodwill 100,00

0

Liabilities

Accounts payable 160,00

0

Long-service leave 50,000

Rent received in advance 20,000

Additional information:

1. The following balances existed at 1 July 2015:

Deferred tax asset $10,000

Deferred tax liability 12,000

There have been no recorded changes to these balances since 1 July 2015.

2. The machinery was acquired on 1 July 2015. Depreciation for accounting purposes was

10% per annum (straight-line method), while 20% per annum (straight-line method) was

used for tax purposes.

3. The tax rate is 30%.

The deferred tax asset and deferred tax liability balances at 30 June 2016 are:

'deferred tax asset' $25,500

'deferred tax liability' $15,000

'deferred tax asset' $12,000

'deferred tax liability' $10,000

'deferred tax asset' $15,000

'deferred tax liability' $25,500

'deferred tax asset' $10,000

'deferred tax liability' $12,000

0.75 points

Q U E S T I O N 1 2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1. On 30 June 2016, an extract of the statement of financial position prepared for internal

purposes, but excluding the effect of income tax, disclosed the following:

Assets $

Cash 80,000

Inventory 200,00

0

Accounts receivable 85,000

Allowance for doubtful

debts

(15,000

)

Machinery 500,00

0

Accumulated depreciation (50,000

)

Goodwill 100,00

0

Liabilities

Accounts payable 160,00

0

Long-service leave 50,000

Rent received in advance 20,000

Additional information:

1. The following balances existed at 1 July 2015:

Deferred tax asset $10,000

Deferred tax liability 12,000

There have been no recorded changes to these balances since 1 July 2015.

2. The machinery was acquired on 1 July 2015. Depreciation for accounting purposes was

10% per annum (straight-line method), while 20% per annum (straight-line method) was

used for tax purposes.

3. The tax rate is 30%.

The adjustments to deferred tax asset and deferred tax liability at 30 June 2016 are:

'deferred tax asset' decrease $15,500

'deferred tax liability' increase $3,000

'deferred tax asset' decrease $10,000

'deferred tax liability' increase $12,000

'deferred tax asset' increase $15,500

'deferred tax liability' increase $3,000

'deferred tax asset' increase $10,000

'deferred tax liability' decrease $12,000

0.75 points

Q U E S T I O N 1 3

1. On 30 June 2016, an extract of the statement of financial position prepared for internal

purposes, but excluding the effect of income tax, disclosed the following:

purposes, but excluding the effect of income tax, disclosed the following:

Assets $

Cash 80,000

Inventory 200,00

0

Accounts receivable 85,000

Allowance for doubtful

debts

(15,000

)

Machinery 500,00

0

Accumulated depreciation (50,000

)

Goodwill 100,00

0

Liabilities

Accounts payable 160,00

0

Long-service leave 50,000

Rent received in advance 20,000

Additional information:

1. The following balances existed at 1 July 2015:

Deferred tax asset $10,000

Deferred tax liability 12,000

There have been no recorded changes to these balances since 1 July 2015.

2. The machinery was acquired on 1 July 2015. Depreciation for accounting purposes was

10% per annum (straight-line method), while 20% per annum (straight-line method) was

used for tax purposes.

3. The tax rate is 30%.

The adjustments to deferred tax asset and deferred tax liability at 30 June 2016 are:

'deferred tax asset' decrease $15,500

'deferred tax liability' increase $3,000

'deferred tax asset' decrease $10,000

'deferred tax liability' increase $12,000

'deferred tax asset' increase $15,500

'deferred tax liability' increase $3,000

'deferred tax asset' increase $10,000

'deferred tax liability' decrease $12,000

0.75 points

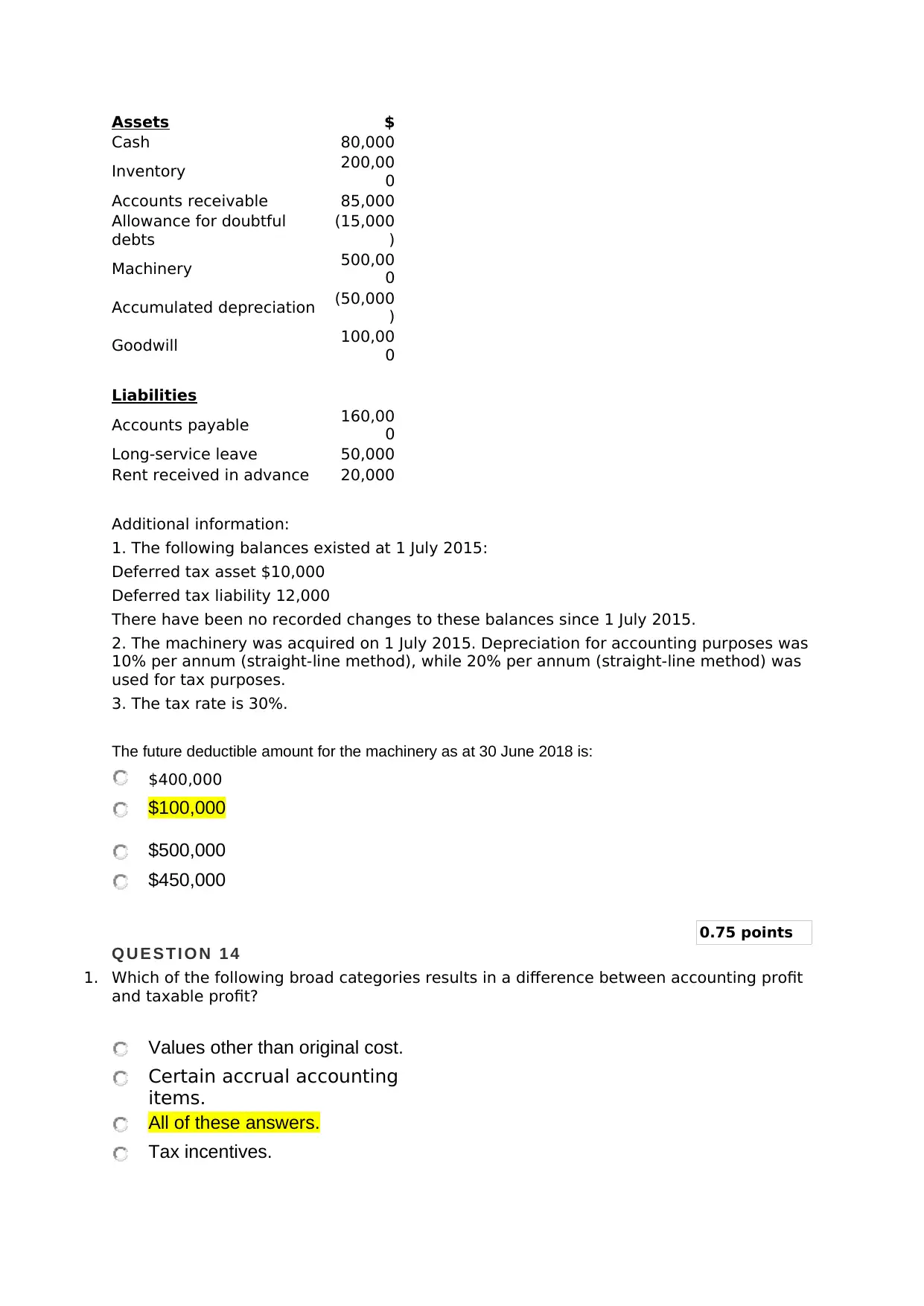

Q U E S T I O N 1 3

1. On 30 June 2016, an extract of the statement of financial position prepared for internal

purposes, but excluding the effect of income tax, disclosed the following:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Assets $

Cash 80,000

Inventory 200,00

0

Accounts receivable 85,000

Allowance for doubtful

debts

(15,000

)

Machinery 500,00

0

Accumulated depreciation (50,000

)

Goodwill 100,00

0

Liabilities

Accounts payable 160,00

0

Long-service leave 50,000

Rent received in advance 20,000

Additional information:

1. The following balances existed at 1 July 2015:

Deferred tax asset $10,000

Deferred tax liability 12,000

There have been no recorded changes to these balances since 1 July 2015.

2. The machinery was acquired on 1 July 2015. Depreciation for accounting purposes was

10% per annum (straight-line method), while 20% per annum (straight-line method) was

used for tax purposes.

3. The tax rate is 30%.

The future deductible amount for the machinery as at 30 June 2018 is:

$400,000

$100,000

$500,000

$450,000

0.75 points

Q U E S T I O N 1 4

1. Which of the following broad categories results in a difference between accounting profit

and taxable profit?

Values other than original cost.

Certain accrual accounting

items.

All of these answers.

Tax incentives.

Cash 80,000

Inventory 200,00

0

Accounts receivable 85,000

Allowance for doubtful

debts

(15,000

)

Machinery 500,00

0

Accumulated depreciation (50,000

)

Goodwill 100,00

0

Liabilities

Accounts payable 160,00

0

Long-service leave 50,000

Rent received in advance 20,000

Additional information:

1. The following balances existed at 1 July 2015:

Deferred tax asset $10,000

Deferred tax liability 12,000

There have been no recorded changes to these balances since 1 July 2015.

2. The machinery was acquired on 1 July 2015. Depreciation for accounting purposes was

10% per annum (straight-line method), while 20% per annum (straight-line method) was

used for tax purposes.

3. The tax rate is 30%.

The future deductible amount for the machinery as at 30 June 2018 is:

$400,000

$100,000

$500,000

$450,000

0.75 points

Q U E S T I O N 1 4

1. Which of the following broad categories results in a difference between accounting profit

and taxable profit?

Values other than original cost.

Certain accrual accounting

items.

All of these answers.

Tax incentives.

0.75 points

Q U E S T I O N 1 5

1. Ying Limited acquires the net assets of Yang Limited for a cash consideration of $50 000.

One half is to be paid on acquisition date and one half is payable in one year’s time. The

appropriate discount rate is 5% p.a. The present value of the cash outflow in one year’s

time is:

$47,619

$25,00

0

$23,810

$26,190

0.75 points

Q U E S T I O N 1 6

1. According to AASB 3 Business Combinations, ‘a gain on bargain purchase’ arises in a

business combination when the consideration transferred:

is less than the carrying amount of the identifiable assets and liabilities.

is less than the net fair value of the acquiree’s identifiable assets and

liabilities.

is more than the book values of the identifiable assets acquired.

is greater than the net fair value of the acquiree’s identifiable assets and

liabilities.

0.75 points

Q U E S T I O N 1 7

1. A Ltd acquires all the net assets of B Ltd and applies the requirements of AASB 3

Business Combinations. Details regarding the net assets of B Ltd are as follows:

Carrying

amount

Fair

value

$ $

Assets

Cash 50,000 50,000

Furniture 20,000 15,000

Fittings 40,000 20,000

Accounts

receivable 25,000 20,000

Goodwill 10,000 10,000

Liabilities

Accounts

payable 20,000 20,000

2.

3. Using the information above, the journal entry by A Ltd to record the acquisition of the

net assets of B Ltd would include:

Dr Furniture $20,000, Dr Fittings $20,000 and Dr Cash $50,000.

Dr Furniture $15,000, Dr Fittings $20,000 and Cr Accounts Payable $20,000.

Dr Furniture $20,000, Dr Fittings $20,000 and Cr Accounts Payable

$20,000.

Q U E S T I O N 1 5

1. Ying Limited acquires the net assets of Yang Limited for a cash consideration of $50 000.

One half is to be paid on acquisition date and one half is payable in one year’s time. The

appropriate discount rate is 5% p.a. The present value of the cash outflow in one year’s

time is:

$47,619

$25,00

0

$23,810

$26,190

0.75 points

Q U E S T I O N 1 6

1. According to AASB 3 Business Combinations, ‘a gain on bargain purchase’ arises in a

business combination when the consideration transferred:

is less than the carrying amount of the identifiable assets and liabilities.

is less than the net fair value of the acquiree’s identifiable assets and

liabilities.

is more than the book values of the identifiable assets acquired.

is greater than the net fair value of the acquiree’s identifiable assets and

liabilities.

0.75 points

Q U E S T I O N 1 7

1. A Ltd acquires all the net assets of B Ltd and applies the requirements of AASB 3

Business Combinations. Details regarding the net assets of B Ltd are as follows:

Carrying

amount

Fair

value

$ $

Assets

Cash 50,000 50,000

Furniture 20,000 15,000

Fittings 40,000 20,000

Accounts

receivable 25,000 20,000

Goodwill 10,000 10,000

Liabilities

Accounts

payable 20,000 20,000

2.

3. Using the information above, the journal entry by A Ltd to record the acquisition of the

net assets of B Ltd would include:

Dr Furniture $20,000, Dr Fittings $20,000 and Dr Cash $50,000.

Dr Furniture $15,000, Dr Fittings $20,000 and Cr Accounts Payable $20,000.

Dr Furniture $20,000, Dr Fittings $20,000 and Cr Accounts Payable

$20,000.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Dr Furniture $20,000, Dr Fittings $40,000 and Dr Cash $50,000.

0.75 points

Q U E S T I O N 1 8

1. A Ltd acquires all the net assets of B Ltd and applies the requirements of AASB 3

Business Combinations. Details regarding the net assets of B Ltd are as follows:

Carrying

amount

Fair

value

$ $

Assets

Cash 50,000 50,000

Furniture 20,000 15,000

Fittings 40,000 20,000

Accounts

receivable 25,000 20,000

Goodwill 10,000 10,000

Liabilities

Accounts

payable 20,000 20,000

2.

3. Assume A Ltd issues 100,000 shares at a fair value of $1 each to acquire the net assets

of B Ltd. The journal entry by A Ltd to record the acquisition of the net assets of B Ltd

would include:

gain on bargain purchase of

$15,000.

gain on bargain purchase of $5,000.

goodwill of $5,000.

goodwill of $15,000.

0.75 points

Q U E S T I O N 1 9

1. A Ltd acquires all the net assets of B Ltd and applies the requirements of AASB 3

Business Combinations. Details regarding the net assets of B Ltd are as follows:

Carrying

amount

Fair

value

$ $

Assets

Cash 50,000 50,000

Furniture 20,000 15,000

Fittings 40,000 20,000

Accounts

receivable 25,000 20,000

Goodwill 10,000 10,000

Liabilities

Accounts

payable 20,000 20,000

2.

0.75 points

Q U E S T I O N 1 8

1. A Ltd acquires all the net assets of B Ltd and applies the requirements of AASB 3

Business Combinations. Details regarding the net assets of B Ltd are as follows:

Carrying

amount

Fair

value

$ $

Assets

Cash 50,000 50,000

Furniture 20,000 15,000

Fittings 40,000 20,000

Accounts

receivable 25,000 20,000

Goodwill 10,000 10,000

Liabilities

Accounts

payable 20,000 20,000

2.

3. Assume A Ltd issues 100,000 shares at a fair value of $1 each to acquire the net assets

of B Ltd. The journal entry by A Ltd to record the acquisition of the net assets of B Ltd

would include:

gain on bargain purchase of

$15,000.

gain on bargain purchase of $5,000.

goodwill of $5,000.

goodwill of $15,000.

0.75 points

Q U E S T I O N 1 9

1. A Ltd acquires all the net assets of B Ltd and applies the requirements of AASB 3

Business Combinations. Details regarding the net assets of B Ltd are as follows:

Carrying

amount

Fair

value

$ $

Assets

Cash 50,000 50,000

Furniture 20,000 15,000

Fittings 40,000 20,000

Accounts

receivable 25,000 20,000

Goodwill 10,000 10,000

Liabilities

Accounts

payable 20,000 20,000

2.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3. Assume A Ltd issues 100,000 shares at $1.50 each to acquire the net assets of B Ltd. The

acquisition analysis would disclose the fair value of the identifiable net assets of B Ltd

and the consideration transferred as:

'Fair value of identifiable net assets' $95,000

'Consideration transferred' $150,000

'Fair value of identifiable net assets' $85,000

'Consideration transferred' $150,000

'Fair value of identifiable net assets' $125,000

'Consideration transferred' $100,000

'Fair value of identifiable net assets' $85,000

'Consideration transferred' $100,000

0.75 points

Q U E S T I O N 2 0

1. A Ltd acquires all the net assets of B Ltd and applies the requirements of AASB 3

Business Combinations. Details regarding the net assets of B Ltd are as follows:

Carrying

amount

Fair

value

$ $

Assets

Cash 50,000 50,000

Furniture 20,000 15,000

Fittings 40,000 20,000

Accounts

receivable 25,000 20,000

Goodwill 10,000 10,000

Liabilities

Accounts

payable 20,000 20,000

2.

3. Assume A Ltd acquires all the net assets of B Ltd by issuing 100,000 shares at a fair

value of 80 cents each. The journal entry by A Ltd to record the acquisition of the net

assets of B Ltd would include:

gain on bargain purchase of

$15,000.

gain on bargain purchase of

$5,000.

gain on bargain purchase of

$25,000.

goodwill of $15,000.

0.75 points

Q U E S T I O N 2 1

1. In the case study on Centro Property Group, eight directors and executives were

prosecuted for failing to exercise due care. In particular, ASIC alleged Centro wrongly

classified $2.6 billion of debt as non-current (rather than current) in its 2007 financial

report.

acquisition analysis would disclose the fair value of the identifiable net assets of B Ltd

and the consideration transferred as:

'Fair value of identifiable net assets' $95,000

'Consideration transferred' $150,000

'Fair value of identifiable net assets' $85,000

'Consideration transferred' $150,000

'Fair value of identifiable net assets' $125,000

'Consideration transferred' $100,000

'Fair value of identifiable net assets' $85,000

'Consideration transferred' $100,000

0.75 points

Q U E S T I O N 2 0

1. A Ltd acquires all the net assets of B Ltd and applies the requirements of AASB 3

Business Combinations. Details regarding the net assets of B Ltd are as follows:

Carrying

amount

Fair

value

$ $

Assets

Cash 50,000 50,000

Furniture 20,000 15,000

Fittings 40,000 20,000

Accounts

receivable 25,000 20,000

Goodwill 10,000 10,000

Liabilities

Accounts

payable 20,000 20,000

2.

3. Assume A Ltd acquires all the net assets of B Ltd by issuing 100,000 shares at a fair

value of 80 cents each. The journal entry by A Ltd to record the acquisition of the net

assets of B Ltd would include:

gain on bargain purchase of

$15,000.

gain on bargain purchase of

$5,000.

gain on bargain purchase of

$25,000.

goodwill of $15,000.

0.75 points

Q U E S T I O N 2 1

1. In the case study on Centro Property Group, eight directors and executives were

prosecuted for failing to exercise due care. In particular, ASIC alleged Centro wrongly

classified $2.6 billion of debt as non-current (rather than current) in its 2007 financial

report.

Who is responsible for ensuring the financial statements are correct? Is this solely the

responsibility of directors? What are the implications for stakeholders when financial

information is wrongly reported?

The directors are responsible for ensuring that the financial statements are correct. This

is evident from the fact that s. 295 Corporations Act 2001 intends that the directors must

sign off on the financial statements. However, it would be incorrect to assume that this is

solely the responsibility of the directors. The financial managers who are involved in the

preparation of financial statements must also be careful and must not indulge in any

wrongdoing (intentional or unintentional). A host of external users such as investors,

lenders, suppliers tend to rely on the financial statements in order to take prudent

economic decisions with regards to engagement with the company. As a result, wrongly

reported financial information can lead to incorrect decision making by these

stakeholders which can potentially lead to losses and loss of confidence in the financial

markets.

responsibility of directors? What are the implications for stakeholders when financial

information is wrongly reported?

The directors are responsible for ensuring that the financial statements are correct. This

is evident from the fact that s. 295 Corporations Act 2001 intends that the directors must

sign off on the financial statements. However, it would be incorrect to assume that this is

solely the responsibility of the directors. The financial managers who are involved in the

preparation of financial statements must also be careful and must not indulge in any

wrongdoing (intentional or unintentional). A host of external users such as investors,

lenders, suppliers tend to rely on the financial statements in order to take prudent

economic decisions with regards to engagement with the company. As a result, wrongly

reported financial information can lead to incorrect decision making by these

stakeholders which can potentially lead to losses and loss of confidence in the financial

markets.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.