ACC621: Materiality Assessment and Audit Procedures for Azure Ent.

VerifiedAdded on 2023/06/07

|16

|2788

|161

Report

AI Summary

This report focuses on the audit of Azure Enterprise's income statement, establishing a materiality level and identifying material items. It details the rational for selection, relevant assertions (occurrence, accuracy, cut off and ownership), and suggested audit procedures for key accounts like sales, other income, depreciation, and wages. The report also addresses the auditor's responsibility in detecting fraud and concludes that while material items were identified through analytical review, no instances of fraud were detected. The report highlights the importance of proper audit planning, including analytical review and preliminary materiality judgments, in ensuring the accuracy and reliability of financial statements. Desklib provides similar past papers and solved assignments for students.

Running head: AUDITING ISSUES AND PRACTICE

Auditing issues and practice

Name of the student

Name of the university

Author note

Auditing issues and practice

Name of the student

Name of the university

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUDITING ISSUES AND PRACTICE 1

Executive summary

The main objective of the report is to consider the income statement of Azure Enterprise and

establishing the materiality level. Based on the materiality level the report will identify

material items from the income statement and will determine the assertion involved with

those account. Further, the report will state the audit procedure that will be carried out by the

auditor while audit will be carried out for the identified items. The report will further

determine whether any fraud risk detected from the analytical review.

Executive summary

The main objective of the report is to consider the income statement of Azure Enterprise and

establishing the materiality level. Based on the materiality level the report will identify

material items from the income statement and will determine the assertion involved with

those account. Further, the report will state the audit procedure that will be carried out by the

auditor while audit will be carried out for the identified items. The report will further

determine whether any fraud risk detected from the analytical review.

AUDITING ISSUES AND PRACTICE 2

Table of Contents

1.0 Audit planning.................................................................................................................4

1.1 Analytical review.............................................................................................................4

1.2 Preliminary judgement for materiality.............................................................................6

Accounts regarded as material...................................................................................................8

2.0 First account – Sales.........................................................................................................8

2.1 Rational for selection.......................................................................................................8

2.2 Assertion and explanation...........................................................................................8

3.0 Second account – Other income..................................................................................8

3.1 Rational for selection.......................................................................................................8

3.2 Assertion and explanation................................................................................................9

4.0 Third account – Depreciation...........................................................................................9

4.1 Rational for selection.......................................................................................................9

4.2 Assertion and explanation................................................................................................9

5.0 Fourth account – Wages............................................................................................10

5.1 Rational for selection.....................................................................................................10

5.2 Assertion and explanation..............................................................................................10

6.0 Suggested audit procedure.................................................................................................10

6.1 Audit procedure – sales..................................................................................................10

6.2 Audit procedure – other income.....................................................................................11

6.3 Audit procedure – depreciation......................................................................................11

Table of Contents

1.0 Audit planning.................................................................................................................4

1.1 Analytical review.............................................................................................................4

1.2 Preliminary judgement for materiality.............................................................................6

Accounts regarded as material...................................................................................................8

2.0 First account – Sales.........................................................................................................8

2.1 Rational for selection.......................................................................................................8

2.2 Assertion and explanation...........................................................................................8

3.0 Second account – Other income..................................................................................8

3.1 Rational for selection.......................................................................................................8

3.2 Assertion and explanation................................................................................................9

4.0 Third account – Depreciation...........................................................................................9

4.1 Rational for selection.......................................................................................................9

4.2 Assertion and explanation................................................................................................9

5.0 Fourth account – Wages............................................................................................10

5.1 Rational for selection.....................................................................................................10

5.2 Assertion and explanation..............................................................................................10

6.0 Suggested audit procedure.................................................................................................10

6.1 Audit procedure – sales..................................................................................................10

6.2 Audit procedure – other income.....................................................................................11

6.3 Audit procedure – depreciation......................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AUDITING ISSUES AND PRACTICE 3

6.4 Audit procedure – wages................................................................................................11

7.0 Fraud..................................................................................................................................11

8.0 Conclusion..........................................................................................................................12

Reference..................................................................................................................................13

Appendix..................................................................................................................................15

6.4 Audit procedure – wages................................................................................................11

7.0 Fraud..................................................................................................................................11

8.0 Conclusion..........................................................................................................................12

Reference..................................................................................................................................13

Appendix..................................................................................................................................15

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUDITING ISSUES AND PRACTICE 4

1.0 Audit planning

The main objective of auditor is planning the audit to conduct is effectively. The audit

engagement partner is further responsible for engagement and performance. The auditor shall

plan the audit properly that includes the establishment of overall audit strategy for

engagement and development of the audit plan. Planning is not the discrete phase of audit

rather it is the iterative and continual procedure that are expected to start just after the

completion of last audit (Byrnes et al. 2015). Main objective of this report is to focus on

establishing the materiality level for Azure Enterprise. The report will further carry out the

analytical procedure to identify the material items from the income statement and will state

the key assertions involved with the accounts and the audit procedures required to be carried

out for each material item.

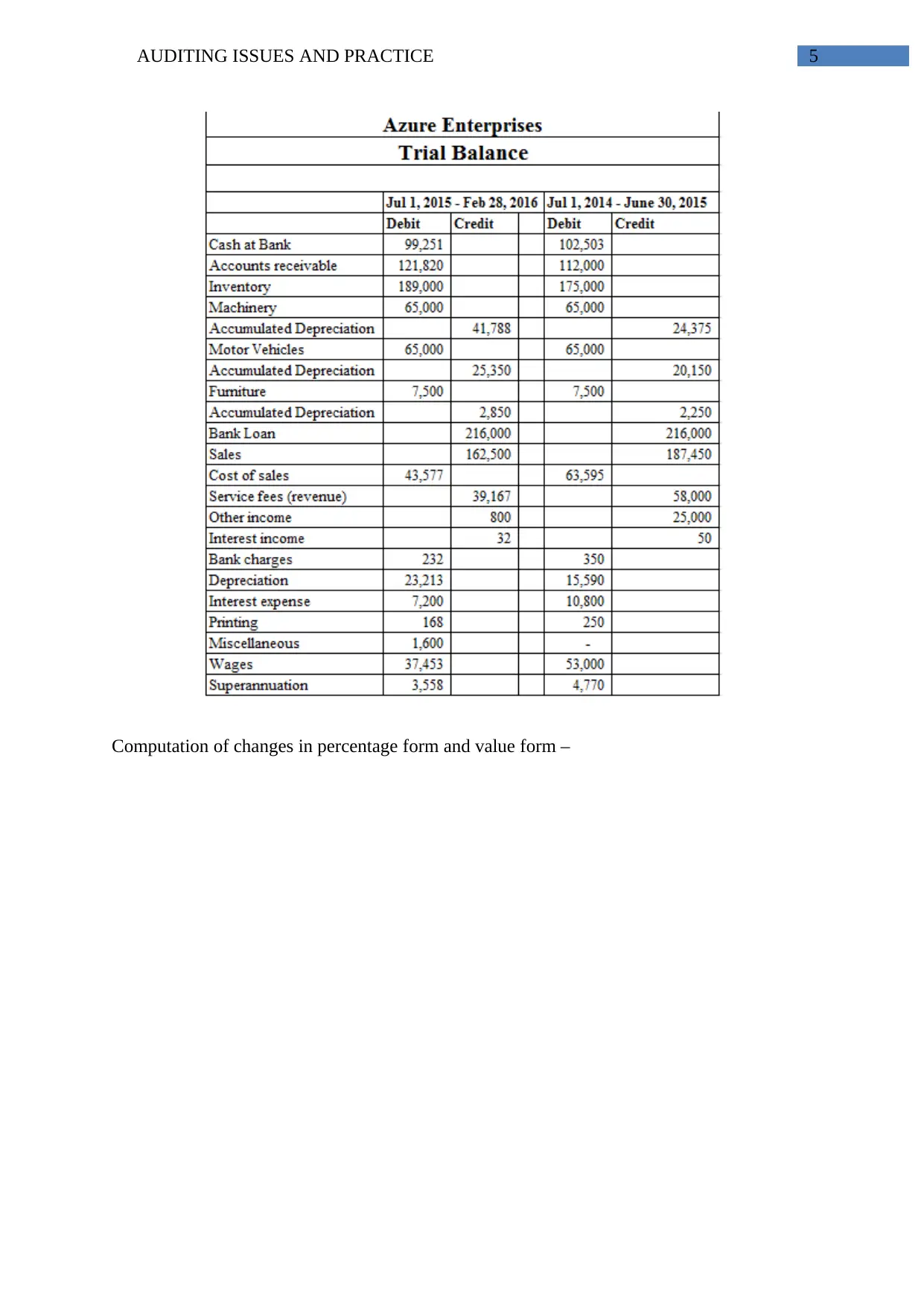

1.1 Analytical review

Analytical review is carried out to assess the reasonableness associated with the

account balance. Analytical review is carried out through ratio analysis and trend analysis and

comparing it with the company’s past performance. In case of Azure enterprise trend analysis

will be performed for the income statement for the year ended 30th June 2015 and 30th June

2016. Once the concerned areas are recognized through analytical review further plan will be

made for the purpose of investigation (Christensen, Glover and Wood 2013). It helps the

auditor to set the timing, nature and extent of audit procedure to be carried out. Further, it is

used as the substantive procedure as detailed tests are time consuming and less efficient. The

analysis for Azure Enterprise will be carried out through horizontal trend analysis as follows

–

1.0 Audit planning

The main objective of auditor is planning the audit to conduct is effectively. The audit

engagement partner is further responsible for engagement and performance. The auditor shall

plan the audit properly that includes the establishment of overall audit strategy for

engagement and development of the audit plan. Planning is not the discrete phase of audit

rather it is the iterative and continual procedure that are expected to start just after the

completion of last audit (Byrnes et al. 2015). Main objective of this report is to focus on

establishing the materiality level for Azure Enterprise. The report will further carry out the

analytical procedure to identify the material items from the income statement and will state

the key assertions involved with the accounts and the audit procedures required to be carried

out for each material item.

1.1 Analytical review

Analytical review is carried out to assess the reasonableness associated with the

account balance. Analytical review is carried out through ratio analysis and trend analysis and

comparing it with the company’s past performance. In case of Azure enterprise trend analysis

will be performed for the income statement for the year ended 30th June 2015 and 30th June

2016. Once the concerned areas are recognized through analytical review further plan will be

made for the purpose of investigation (Christensen, Glover and Wood 2013). It helps the

auditor to set the timing, nature and extent of audit procedure to be carried out. Further, it is

used as the substantive procedure as detailed tests are time consuming and less efficient. The

analysis for Azure Enterprise will be carried out through horizontal trend analysis as follows

–

AUDITING ISSUES AND PRACTICE 5

Computation of changes in percentage form and value form –

Computation of changes in percentage form and value form –

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AUDITING ISSUES AND PRACTICE 6

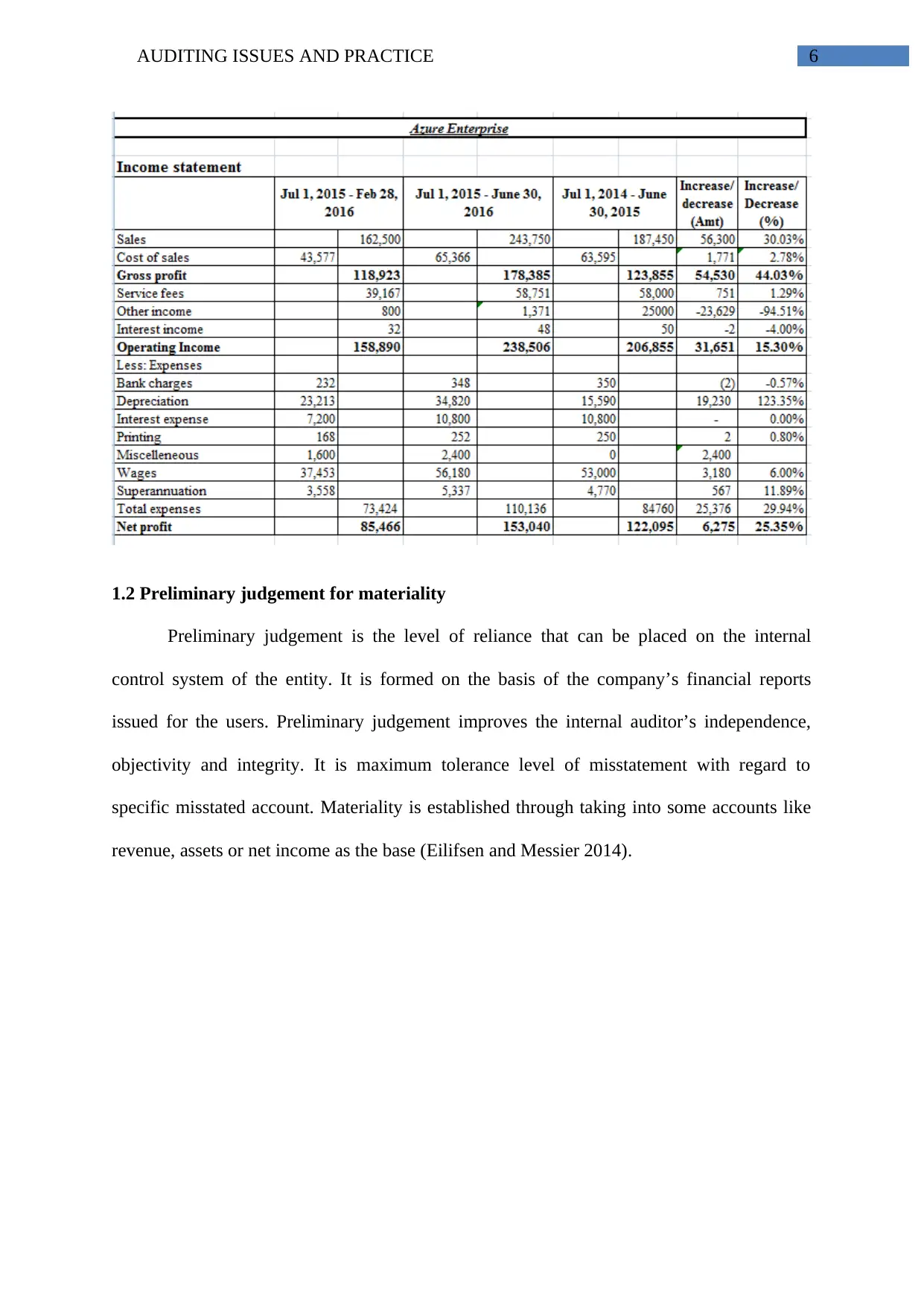

1.2 Preliminary judgement for materiality

Preliminary judgement is the level of reliance that can be placed on the internal

control system of the entity. It is formed on the basis of the company’s financial reports

issued for the users. Preliminary judgement improves the internal auditor’s independence,

objectivity and integrity. It is maximum tolerance level of misstatement with regard to

specific misstated account. Materiality is established through taking into some accounts like

revenue, assets or net income as the base (Eilifsen and Messier 2014).

1.2 Preliminary judgement for materiality

Preliminary judgement is the level of reliance that can be placed on the internal

control system of the entity. It is formed on the basis of the company’s financial reports

issued for the users. Preliminary judgement improves the internal auditor’s independence,

objectivity and integrity. It is maximum tolerance level of misstatement with regard to

specific misstated account. Materiality is established through taking into some accounts like

revenue, assets or net income as the base (Eilifsen and Messier 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUDITING ISSUES AND PRACTICE 7

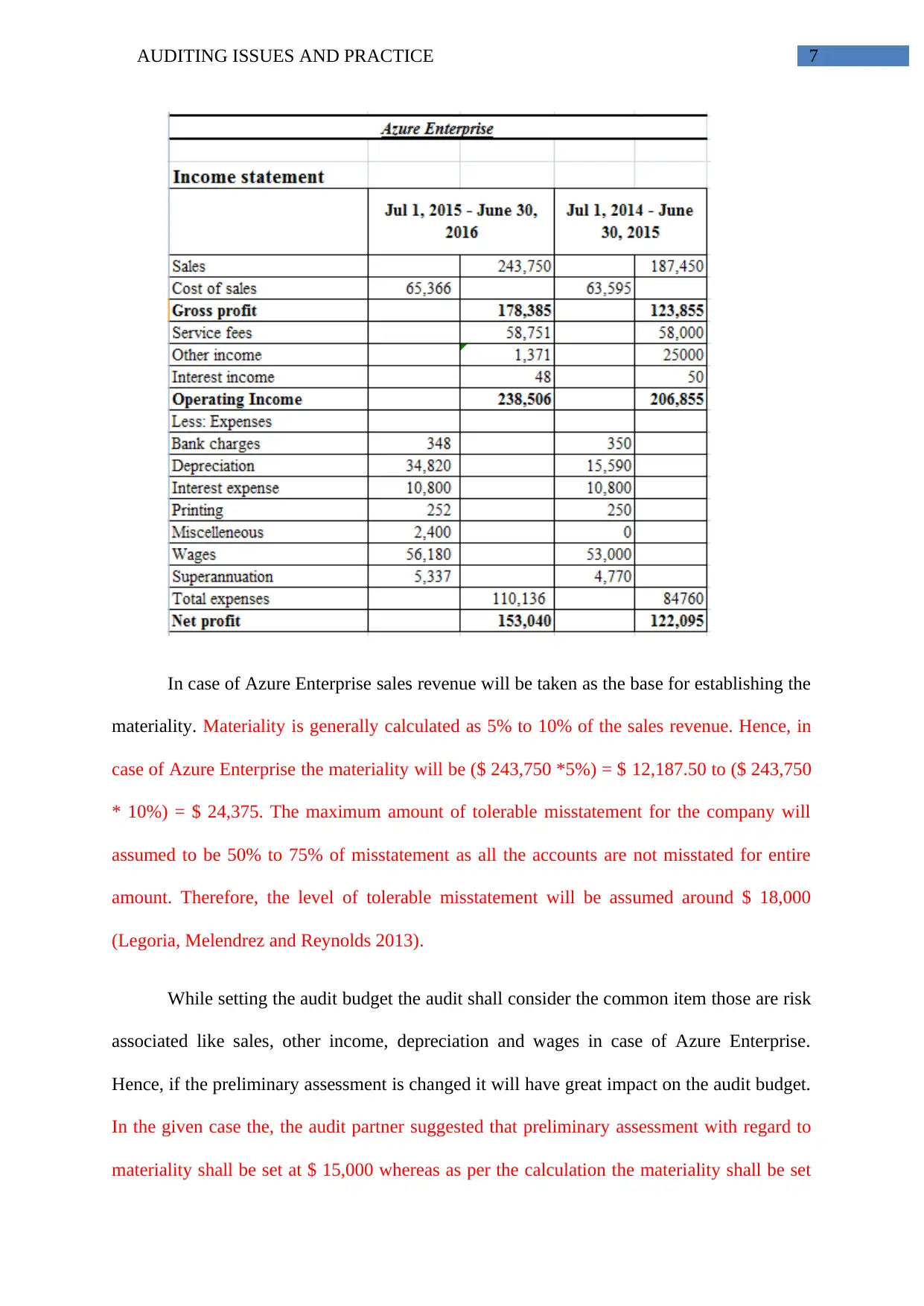

In case of Azure Enterprise sales revenue will be taken as the base for establishing the

materiality. Materiality is generally calculated as 5% to 10% of the sales revenue. Hence, in

case of Azure Enterprise the materiality will be ($ 243,750 *5%) = $ 12,187.50 to ($ 243,750

* 10%) = $ 24,375. The maximum amount of tolerable misstatement for the company will

assumed to be 50% to 75% of misstatement as all the accounts are not misstated for entire

amount. Therefore, the level of tolerable misstatement will be assumed around $ 18,000

(Legoria, Melendrez and Reynolds 2013).

While setting the audit budget the audit shall consider the common item those are risk

associated like sales, other income, depreciation and wages in case of Azure Enterprise.

Hence, if the preliminary assessment is changed it will have great impact on the audit budget.

In the given case the, the audit partner suggested that preliminary assessment with regard to

materiality shall be set at $ 15,000 whereas as per the calculation the materiality shall be set

In case of Azure Enterprise sales revenue will be taken as the base for establishing the

materiality. Materiality is generally calculated as 5% to 10% of the sales revenue. Hence, in

case of Azure Enterprise the materiality will be ($ 243,750 *5%) = $ 12,187.50 to ($ 243,750

* 10%) = $ 24,375. The maximum amount of tolerable misstatement for the company will

assumed to be 50% to 75% of misstatement as all the accounts are not misstated for entire

amount. Therefore, the level of tolerable misstatement will be assumed around $ 18,000

(Legoria, Melendrez and Reynolds 2013).

While setting the audit budget the audit shall consider the common item those are risk

associated like sales, other income, depreciation and wages in case of Azure Enterprise.

Hence, if the preliminary assessment is changed it will have great impact on the audit budget.

In the given case the, the audit partner suggested that preliminary assessment with regard to

materiality shall be set at $ 15,000 whereas as per the calculation the materiality shall be set

AUDITING ISSUES AND PRACTICE 8

at $ 18,000. Hence, with increase of materiality level the audit budget will be reduced and the

auditor will require checking less number of items while performing the audit (Legoria,

Melendrez and Reynolds 2013).

Accounts regarded as material

2.0 First account – Sales

2.1 Rational for selection

Sales being an important item are always susceptible to misstatement, fraud or

intentional error. It is found that the sales revenue of Azure Enterprise has been increased by

$ 56,300 that is by 30.03% as compared to the previous year. Irrespective of the amounts

involved sales is considered material item by its nature.

2.2 Assertion and explanation

Sales are generally misstated through – (i) recording sales for fictitious customers (ii)

misstating the amount of invoice while recording (iii) not raising invoice for the sales made

and goods delivered or (iv) recognising revenue for the sales not yet made and goods not

despatched. Therefore, the assertions pertain to sales are – (i) occurrence that the sales

transactions recorded by the company have been taken place and related to the company (ii)

accuracy – amounts related to sales transactions have been recorded at proper amount and

under proper account (Glover and Prawitt 2014).

3.0 Second account – Other income

3.1 Rational for selection

It is recognized that the income from other sources was one of the biggest source of of

the company’s revenue in previous year. However the receipt has been reduced by a

significant amount that is by $ 23,629 or 94.51%. Therefore, the item will be considered as

at $ 18,000. Hence, with increase of materiality level the audit budget will be reduced and the

auditor will require checking less number of items while performing the audit (Legoria,

Melendrez and Reynolds 2013).

Accounts regarded as material

2.0 First account – Sales

2.1 Rational for selection

Sales being an important item are always susceptible to misstatement, fraud or

intentional error. It is found that the sales revenue of Azure Enterprise has been increased by

$ 56,300 that is by 30.03% as compared to the previous year. Irrespective of the amounts

involved sales is considered material item by its nature.

2.2 Assertion and explanation

Sales are generally misstated through – (i) recording sales for fictitious customers (ii)

misstating the amount of invoice while recording (iii) not raising invoice for the sales made

and goods delivered or (iv) recognising revenue for the sales not yet made and goods not

despatched. Therefore, the assertions pertain to sales are – (i) occurrence that the sales

transactions recorded by the company have been taken place and related to the company (ii)

accuracy – amounts related to sales transactions have been recorded at proper amount and

under proper account (Glover and Prawitt 2014).

3.0 Second account – Other income

3.1 Rational for selection

It is recognized that the income from other sources was one of the biggest source of of

the company’s revenue in previous year. However the receipt has been reduced by a

significant amount that is by $ 23,629 or 94.51%. Therefore, the item will be considered as

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AUDITING ISSUES AND PRACTICE 9

material by amount as well as nature both. Further, as the income from other sources

generally includes incomes from various sources, it is susceptible to misstatement. Further,

irrespective of the source the managements and employee’s remuneration or bonus are

dependent on the income of the company. Therefore, any source of income is always

considered as material (Ruhnke, Pronobis and Michel 2014).

3.2 Assertion and explanation

Receipts from other sources are generally involved with the assertion that all the

transactions related to income from other sources might have been recorded wrongly by

mistake or intentionally. Further, another misstatement may be that the receipts are not

recorded under proper period. Therefore the assertions are - (i) Accuracy that the transaction

related to income from other sources have not been recorded under proper head and related

disclosures have not been made (ii) cut off that is the transaction related to income from other

sources for another period have been recorded under current period.

4.0 Third account – Depreciation

4.1 Rational for selection

Depreciation for Azure Enterprise has been increased from $ 15,590 to $ 34,280 that

is by $ 19,230 or 123.35%. Therefore, depreciation will be considered as material by amount.

Generally, depreciation goes up when the method of charging depreciation is changed by the

company or there is purchase of any new asset. However, it is found that the company has not

purchased any new fixed asset during the year (Louwers et al. 2015).

4.2 Assertion and explanation

Various assertions associated with the depreciation account is – (i) occurrence that is

transactions related to fixed assets actually taken place during the accounting period (ii)

material by amount as well as nature both. Further, as the income from other sources

generally includes incomes from various sources, it is susceptible to misstatement. Further,

irrespective of the source the managements and employee’s remuneration or bonus are

dependent on the income of the company. Therefore, any source of income is always

considered as material (Ruhnke, Pronobis and Michel 2014).

3.2 Assertion and explanation

Receipts from other sources are generally involved with the assertion that all the

transactions related to income from other sources might have been recorded wrongly by

mistake or intentionally. Further, another misstatement may be that the receipts are not

recorded under proper period. Therefore the assertions are - (i) Accuracy that the transaction

related to income from other sources have not been recorded under proper head and related

disclosures have not been made (ii) cut off that is the transaction related to income from other

sources for another period have been recorded under current period.

4.0 Third account – Depreciation

4.1 Rational for selection

Depreciation for Azure Enterprise has been increased from $ 15,590 to $ 34,280 that

is by $ 19,230 or 123.35%. Therefore, depreciation will be considered as material by amount.

Generally, depreciation goes up when the method of charging depreciation is changed by the

company or there is purchase of any new asset. However, it is found that the company has not

purchased any new fixed asset during the year (Louwers et al. 2015).

4.2 Assertion and explanation

Various assertions associated with the depreciation account is – (i) occurrence that is

transactions related to fixed assets actually taken place during the accounting period (ii)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUDITING ISSUES AND PRACTICE 10

ownership that is the company has lawful claim on the assets those are recorded under

balance sheet.

5.0 Fourth account – Wages

5.1 Rational for selection

Wages expenses shall be considered as material item as a major proportion of

revenues are consumed by this and it is an important expense for normal daily operation of

the company. Therefore wage expense is material by its nature. It can be identified that the

wage expenses of Azure Enterprise has been increased by $ 3,180 or by 6%.

5.2 Assertion and explanation

While auditing for wage expense the auditor is mainly concerned regarding (i) the

wage payment made to fictitious employees (ii) expenses has been recognised without

making the payment (iii) payment has been made but the expenses has not been recorded.

Therefore, the assertions pertain to wages are – (i) occurrence that the wages expenses

recorded by the company have been actually for the payment made during the accounting

period (ii) accuracy – amounts related to wage expenses have been recorded at proper amount

and under proper account (Kharisova and Kozlova 2014).

6.0 Suggested audit procedure

6.1 Audit procedure – sales

While performing the audit for sales revenue the auditor shall verify the recognition

method for sales used by the company and shall check that the company is using the method

on consistent basis. Further, sales transaction with big amount shall be checked with the

customer name, bill raised to the customer, quantity and the price shall be verified with the

ownership that is the company has lawful claim on the assets those are recorded under

balance sheet.

5.0 Fourth account – Wages

5.1 Rational for selection

Wages expenses shall be considered as material item as a major proportion of

revenues are consumed by this and it is an important expense for normal daily operation of

the company. Therefore wage expense is material by its nature. It can be identified that the

wage expenses of Azure Enterprise has been increased by $ 3,180 or by 6%.

5.2 Assertion and explanation

While auditing for wage expense the auditor is mainly concerned regarding (i) the

wage payment made to fictitious employees (ii) expenses has been recognised without

making the payment (iii) payment has been made but the expenses has not been recorded.

Therefore, the assertions pertain to wages are – (i) occurrence that the wages expenses

recorded by the company have been actually for the payment made during the accounting

period (ii) accuracy – amounts related to wage expenses have been recorded at proper amount

and under proper account (Kharisova and Kozlova 2014).

6.0 Suggested audit procedure

6.1 Audit procedure – sales

While performing the audit for sales revenue the auditor shall verify the recognition

method for sales used by the company and shall check that the company is using the method

on consistent basis. Further, sales transaction with big amount shall be checked with the

customer name, bill raised to the customer, quantity and the price shall be verified with the

AUDITING ISSUES AND PRACTICE 11

approved price list. Sales receipt shall be further segregated as sales made on cash basis and

sales made on credit basis (Leung et al. 2015).

6.2 Audit procedure – other income

While performing the audit procedure for income from other sources the auditor shall

verify the sources from where these incomes are received. Further, the income from various

sources shall be compared with the previous year’s receipt (Coetzee and Lubbe 2014). For

significant difference found the auditor shall ask the management for justification or can even

contact the third party for confirming the reason.

6.3 Audit procedure – depreciation

The auditor shall confirm the amount of fixed asset and purchase or sales of fixed

asset through the asset register. Auditor shall further verify the method used for charging

depreciation, rate of depreciation for particular asset and shall be matched with the amount

recorded as depreciation in the accounts (Wali 2015).

6.4 Audit procedure – wages

Wage payment made to the employees under the accounting period shall be verified

with the employee register with the details like name of the employees, number of

employees, number of days worked by each employee, amount of wage entitlement for each

employee, arrear of wages for any employee and advance payment, if any paid to any

employee (Arens et al. 2016). Further, the employee register shall be verified for engagement

and retirement of any employee during the year and wage payment pertains to them.

7.0 Fraud

Fraud is the intentional error committed by any employee or management to fulfil

own objectives. Auditors while carrying out the audit procedure is responsible for identifying

approved price list. Sales receipt shall be further segregated as sales made on cash basis and

sales made on credit basis (Leung et al. 2015).

6.2 Audit procedure – other income

While performing the audit procedure for income from other sources the auditor shall

verify the sources from where these incomes are received. Further, the income from various

sources shall be compared with the previous year’s receipt (Coetzee and Lubbe 2014). For

significant difference found the auditor shall ask the management for justification or can even

contact the third party for confirming the reason.

6.3 Audit procedure – depreciation

The auditor shall confirm the amount of fixed asset and purchase or sales of fixed

asset through the asset register. Auditor shall further verify the method used for charging

depreciation, rate of depreciation for particular asset and shall be matched with the amount

recorded as depreciation in the accounts (Wali 2015).

6.4 Audit procedure – wages

Wage payment made to the employees under the accounting period shall be verified

with the employee register with the details like name of the employees, number of

employees, number of days worked by each employee, amount of wage entitlement for each

employee, arrear of wages for any employee and advance payment, if any paid to any

employee (Arens et al. 2016). Further, the employee register shall be verified for engagement

and retirement of any employee during the year and wage payment pertains to them.

7.0 Fraud

Fraud is the intentional error committed by any employee or management to fulfil

own objectives. Auditors while carrying out the audit procedure is responsible for identifying

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.