B124 Fundamentals of Accounting: Management Accounting TMA 02

VerifiedAdded on 2023/04/26

|21

|3220

|416

Homework Assignment

AI Summary

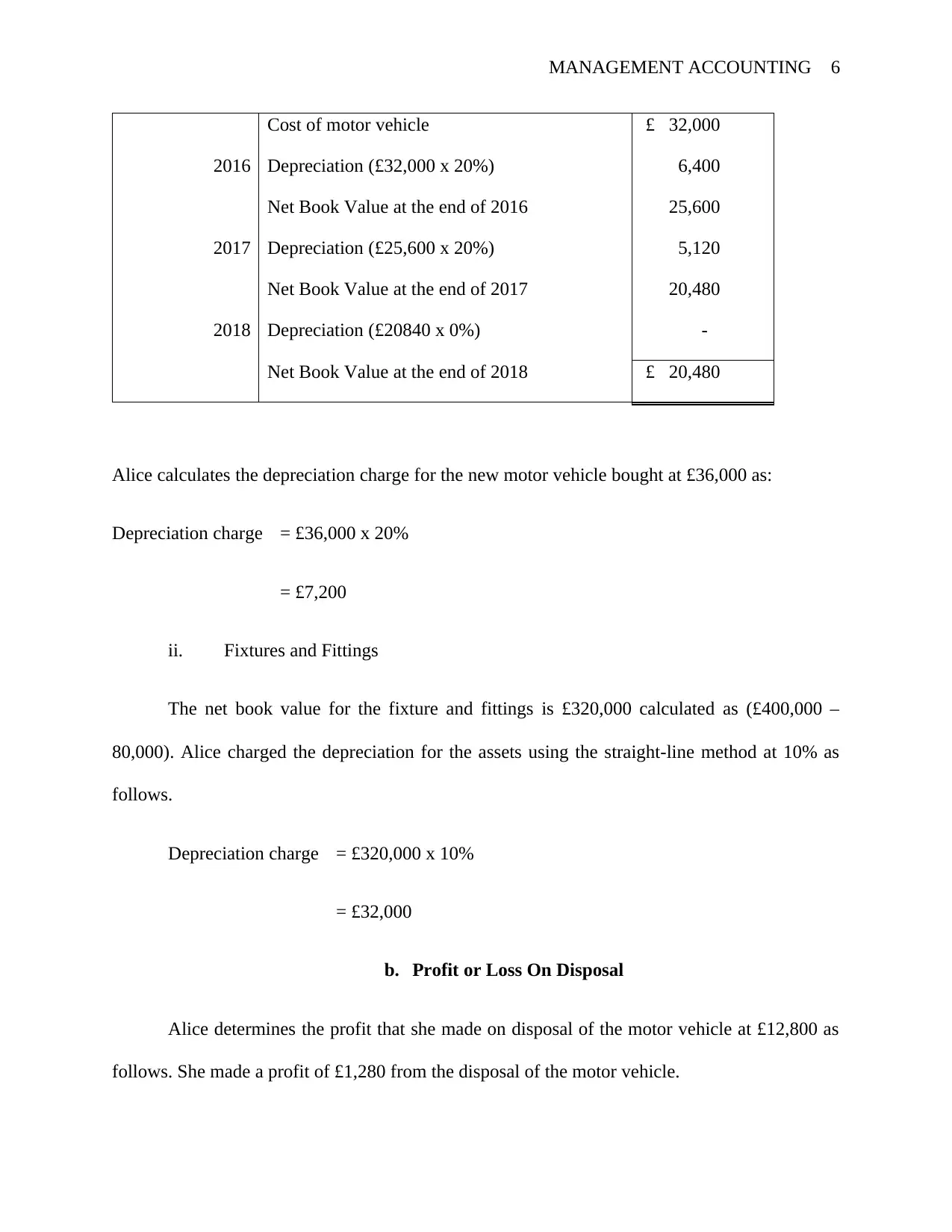

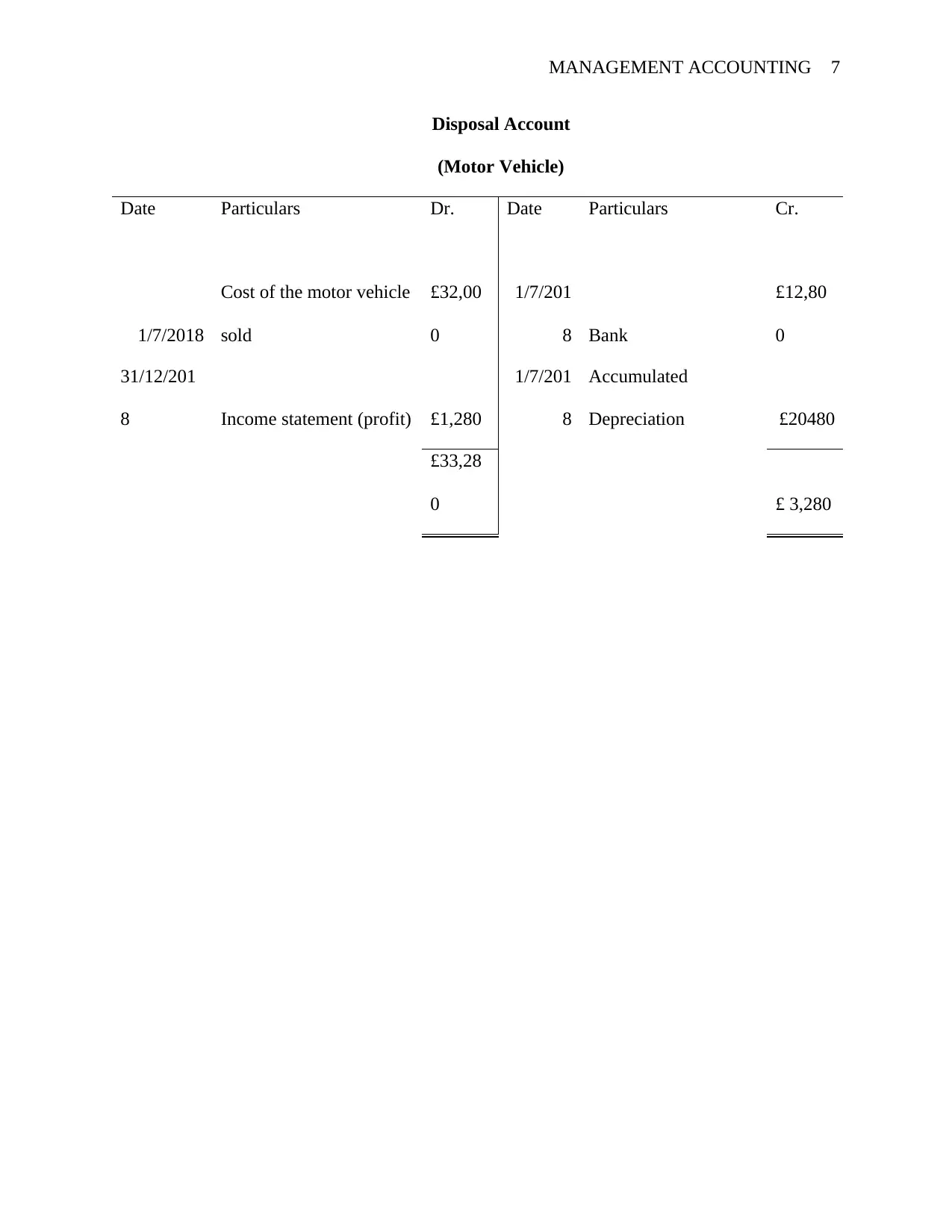

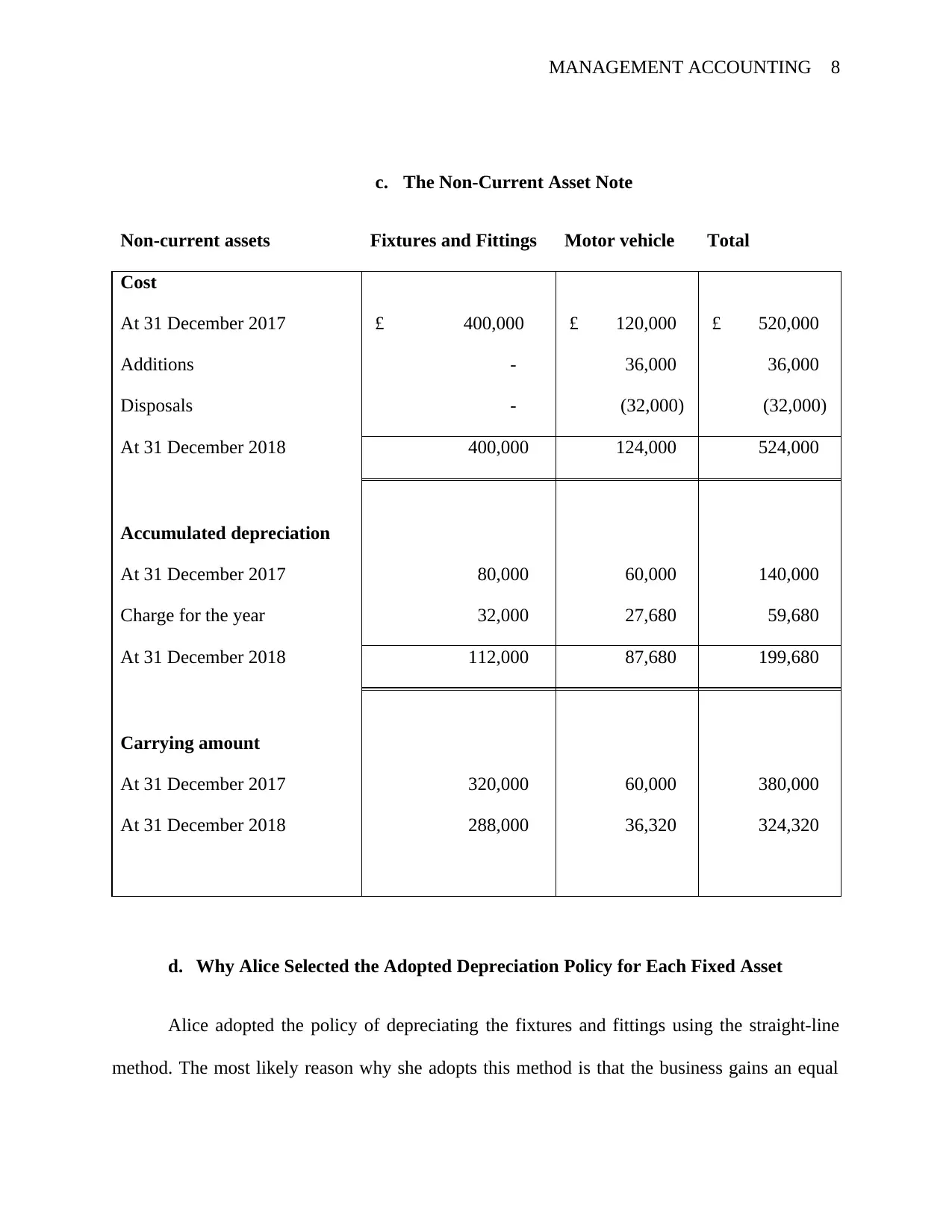

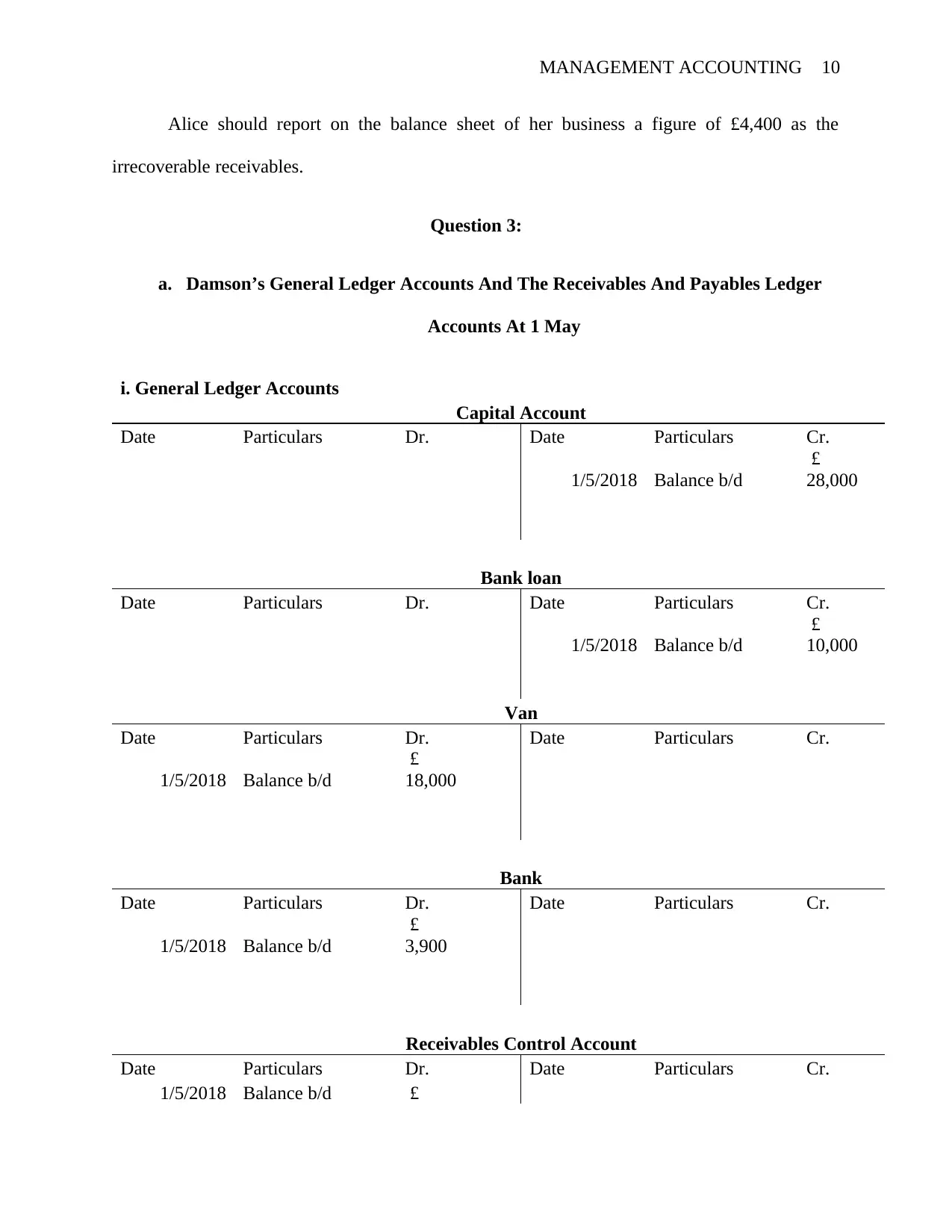

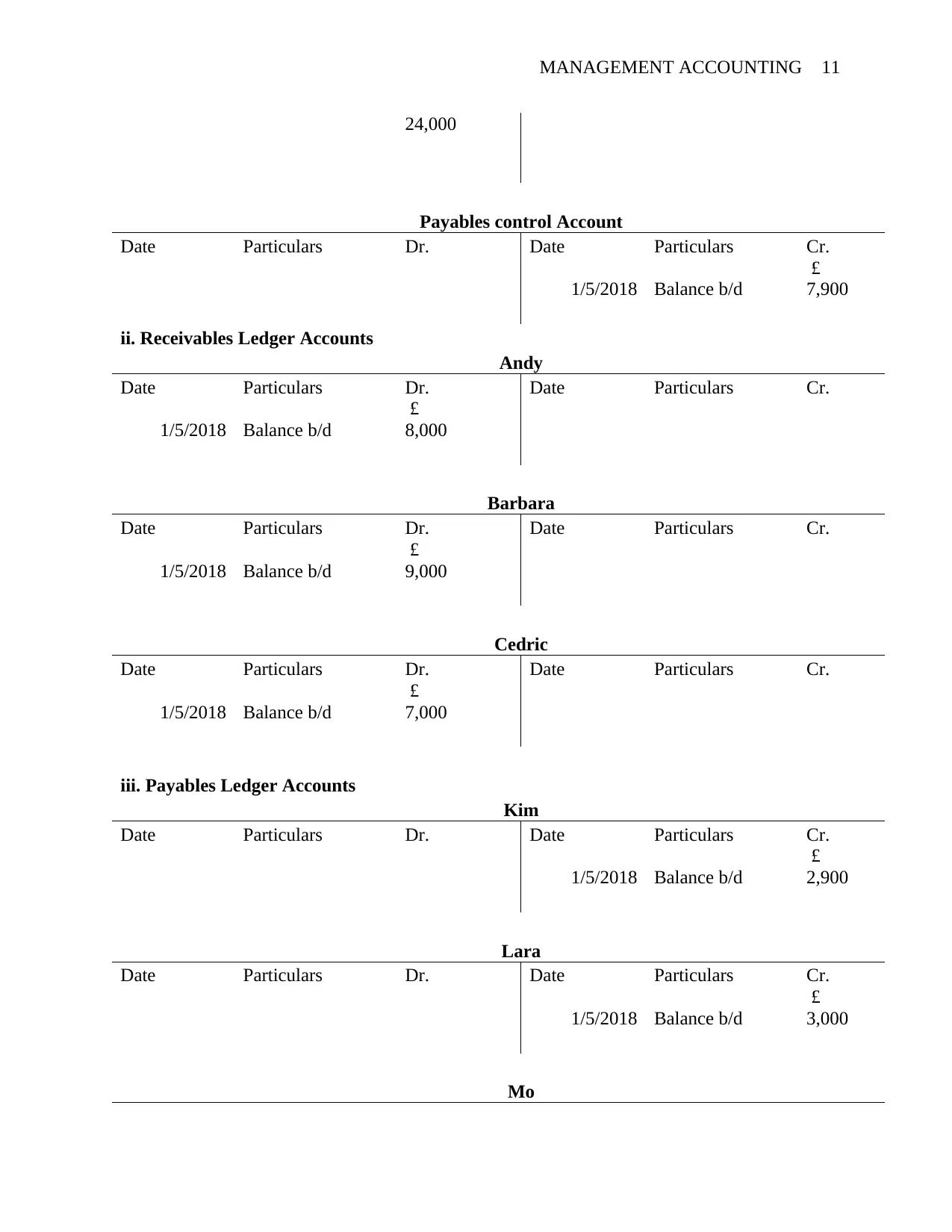

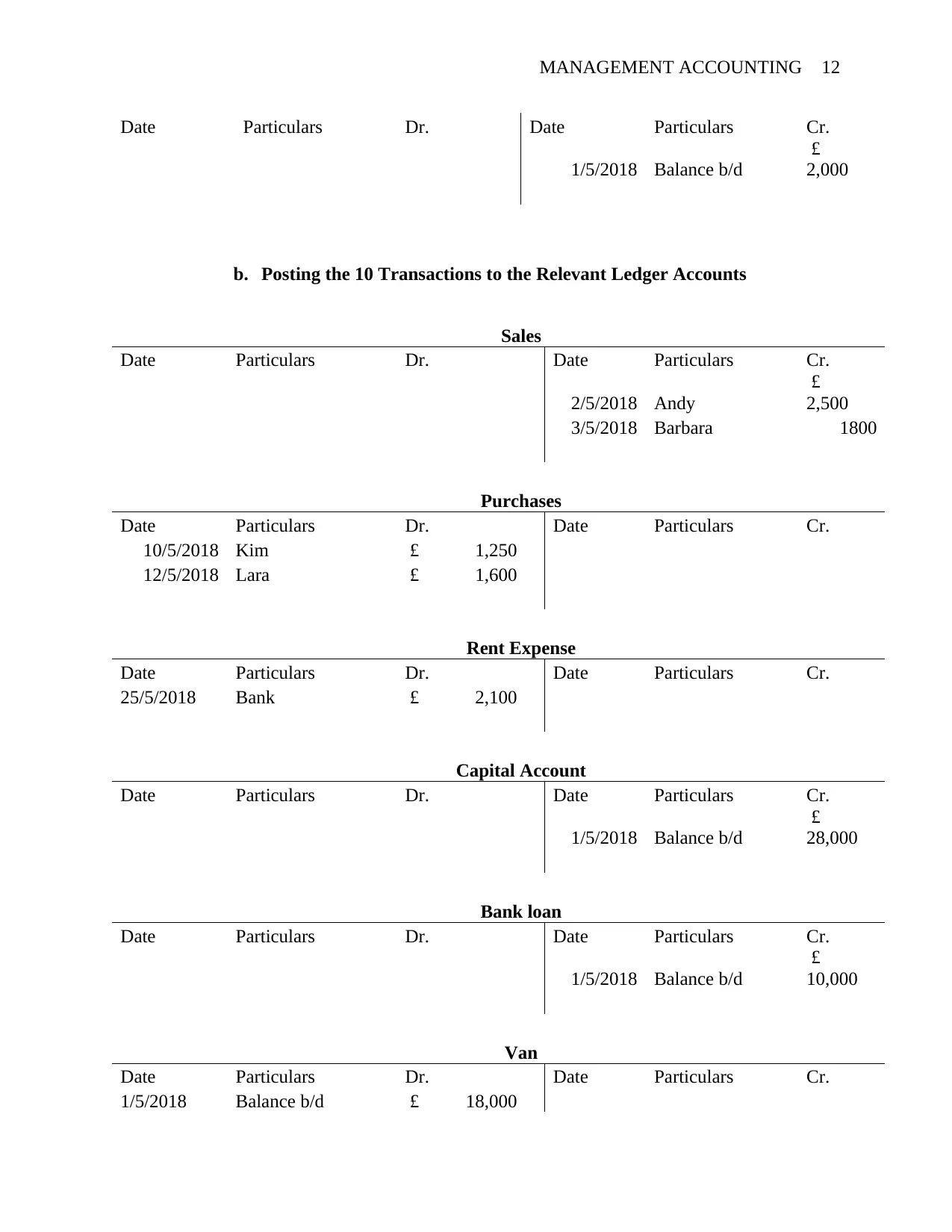

This assignment solution covers key concepts in management accounting, including accrual accounting, depreciation methods, and ledger account adjustments. It addresses the recording of subscription sales, accounting adjustments for income received in advance, and the implications of accrual versus cash-based accounting. The solution also details the calculation of depreciation charges for motor vehicles and fixtures using both straight-line and reducing balance methods, along with profit/loss on disposal of assets and the presentation of non-current asset notes. Furthermore, it includes an analysis of allowance for irrecoverable receivables and the appropriate balance sheet reporting. Finally, the assignment provides a comprehensive demonstration of posting transactions to general and subsidiary ledgers, balancing off accounts, and preparing receivables and payables ledgers, offering a thorough understanding of fundamental accounting principles. Desklib provides this assignment and more to aid students in their studies.

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.