Critical Analysis of B2B Customer Management: Barclay & Rufus

VerifiedAdded on 2020/01/06

|15

|3634

|18

Report

AI Summary

This report provides a critical analysis of B2B customer management practices, contrasting Barclay Bank and Rufus Leonard. It begins with an introduction to B2B models, emphasizing the importance of customer satisfaction and loyalty in a competitive landscape. The report then delves into the current performance of both companies, assessing their value propositions and customer experiences. Barclay Bank, a large financial institution, is examined as a 'bad' B2B company, while Rufus Leonard, a digital agency, is presented as a 'good' example. The analysis includes a discussion of customer experience issues within Barclay Bank, such as inadequate information and a lack of personalized relationship management, which contrasts with Rufus Leonard's customer-centric approach. The core of the report focuses on developing a customer relationship management (CRM) improvement strategy for Barclay Bank. This includes recommending the implementation of the QCI/Payne model to enhance customer engagement, and the development of a new value proposition. The report also explores other business operation concepts, such as capital management and regulatory compliance. The conclusion summarizes the key findings and recommendations for improving Barclay Bank's customer relationships and overall B2B performance.

B2B between good

company and bad

company

company and bad

company

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

1. INTRODUCTION.......................................................................................................................1

2. Critical analysis of Barclay Bank and Rufus Leonard in managing their customers..................1

2.1 Overview of current performance.........................................................................................1

2.2 The Value Proposition...........................................................................................................2

2.2.1 Value Proposition undertaken by Barclay Bank...........................................................2

2.2.2 Value proposition undertaken by Rufus Leonard Limited............................................3

2.3 The Customer Experience.....................................................................................................3

2.3.1 Customer Experience in Barclay Bank..........................................................................3

2.3.2 Customer Experience in Refuses Leonard....................................................................3

3. Developing a customer relationship management improvement strategy for Barclay Bank.......4

3.1 Introduction...........................................................................................................................4

3.2 Use of QCI/Payne model by Barclay Bank...........................................................................5

QCI-........................................................................................................................................5

Payne model-..........................................................................................................................7

3.3 Developing a new value proposition for Barclay Bank........................................................7

3.4 Other concepts of business operations of Barclay Bank.......................................................8

3.5 Customer Experience in Barclay Bank.................................................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................12

Books and Journals...................................................................................................................12

Online........................................................................................................................................13

1. INTRODUCTION.......................................................................................................................1

2. Critical analysis of Barclay Bank and Rufus Leonard in managing their customers..................1

2.1 Overview of current performance.........................................................................................1

2.2 The Value Proposition...........................................................................................................2

2.2.1 Value Proposition undertaken by Barclay Bank...........................................................2

2.2.2 Value proposition undertaken by Rufus Leonard Limited............................................3

2.3 The Customer Experience.....................................................................................................3

2.3.1 Customer Experience in Barclay Bank..........................................................................3

2.3.2 Customer Experience in Refuses Leonard....................................................................3

3. Developing a customer relationship management improvement strategy for Barclay Bank.......4

3.1 Introduction...........................................................................................................................4

3.2 Use of QCI/Payne model by Barclay Bank...........................................................................5

QCI-........................................................................................................................................5

Payne model-..........................................................................................................................7

3.3 Developing a new value proposition for Barclay Bank........................................................7

3.4 Other concepts of business operations of Barclay Bank.......................................................8

3.5 Customer Experience in Barclay Bank.................................................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................12

Books and Journals...................................................................................................................12

Online........................................................................................................................................13

1. INTRODUCTION

In the present era of globalisation and hyper competition, organisations are running on

the track of achieving the leading heights of success effectively. For this all the companies

nowadays are laying its significant concern over closely accomplishing the needs and desires of

its core consumers thereby attaining the highest level of customer satisfaction, trust and loyalty.

They are constantly keeping their eyes open to gain an exotic global exposure within short span

of time. To achieve this, the corporations are focusing on engaging themselves in B2B activities

to attain the desired set of organisation's goal (Horta, Camanho and da Costa, 2012). B2B also

called as business to business model facilitates the exchange of raw materials, components and

essential parts which provides a source for additional profit through production or manufacturing

or through the final sales to its buyers. This kind of business model help the companies to

integrate their activities with other business entity to gain higher economies of scale and to beat

the tough line of core competitors in an appropriate and significant way. The recent study about

B2B marketers reveals the fact that it assist the organisation in generating lead in the vast

international economies along with developing leadership-market education in a significant way.

Also, B2B provides its customers with brand focused and premium quality products with high

profit margins to the companies (Reichheld and Markey, 2011). With this context, the present

report highlights a critical analysis of how Barclay Bank which is a bad B2B company and Rufus

Leonard, a good B2B company, have been managing their customers. Also, the report will focus

on developing an effective customer relationship management improvement strategy for the

above mentioned companies.

2. Critical analysis of Barclay Bank and Rufus Leonard in managing their

customers

2.1 Overview of current performance

Barclay Bank is a leading financial services entity headquartered in London. It is the

largest British multinational company which deals in wholesale, retail, investment banking,

wealth management, credit cards and mortgage lending. It serves approximately 48 millions

customers and has its operations in around 50 countries across the globe. The said company is

also one of the leading B2B organisation and has systematically organised its business into four

vital segments which includes Personal Banking, Wealth management, Corporate Banking and

1

In the present era of globalisation and hyper competition, organisations are running on

the track of achieving the leading heights of success effectively. For this all the companies

nowadays are laying its significant concern over closely accomplishing the needs and desires of

its core consumers thereby attaining the highest level of customer satisfaction, trust and loyalty.

They are constantly keeping their eyes open to gain an exotic global exposure within short span

of time. To achieve this, the corporations are focusing on engaging themselves in B2B activities

to attain the desired set of organisation's goal (Horta, Camanho and da Costa, 2012). B2B also

called as business to business model facilitates the exchange of raw materials, components and

essential parts which provides a source for additional profit through production or manufacturing

or through the final sales to its buyers. This kind of business model help the companies to

integrate their activities with other business entity to gain higher economies of scale and to beat

the tough line of core competitors in an appropriate and significant way. The recent study about

B2B marketers reveals the fact that it assist the organisation in generating lead in the vast

international economies along with developing leadership-market education in a significant way.

Also, B2B provides its customers with brand focused and premium quality products with high

profit margins to the companies (Reichheld and Markey, 2011). With this context, the present

report highlights a critical analysis of how Barclay Bank which is a bad B2B company and Rufus

Leonard, a good B2B company, have been managing their customers. Also, the report will focus

on developing an effective customer relationship management improvement strategy for the

above mentioned companies.

2. Critical analysis of Barclay Bank and Rufus Leonard in managing their

customers

2.1 Overview of current performance

Barclay Bank is a leading financial services entity headquartered in London. It is the

largest British multinational company which deals in wholesale, retail, investment banking,

wealth management, credit cards and mortgage lending. It serves approximately 48 millions

customers and has its operations in around 50 countries across the globe. The said company is

also one of the leading B2B organisation and has systematically organised its business into four

vital segments which includes Personal Banking, Wealth management, Corporate Banking and

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Investment Management (Svensson and et.al., 2012). Barclay has developed tremendous

corporate acquisitions which broadly includes London. Provincial and South Western Bank,

Mercantile Credit and the Woolwich. Currently, the company is listed on the London Stock

Exchange and is a significant part of FTSE 100Index.

The another B2B Company is Rufus Leonard Limited, which is a privately owned

organisation deals in hosting industry and website designing. It provides the companies with

B2B brands, energy suppliers, telecom, retail banking markets and children's charity. The said

organisation is headquartered in London and constitutes as one of the best and fast growing B2B

companies in UK. The company deals in providing the best customer services along with

impressive management of funds. It operates as a digital agency in a significant way. The

concerned innovative and positive brands renders creative and impressive communications to its

core high profile clients which broadly includes Bank of Scotland, British Gas and O2. Rufus

Leonard posses the strong ability to gain an exotic global exposure by combining its competitive

experience with its traditional brand developing skills (Kärkkäinen, Jussila and Väisänen, 2010).

2.2 The Value Proposition

Value Proposition refers to an innovation, feature or services which an organisation

incorporates to make its product or service attractive to its target customers. It reflects a promise

of value to be acknowledged and delivered by the companies in an appropriate and systematic

way. Considering this fact, the present report will discuss the crucial aspects of proposition

mirror adopted by Barclay Bank and Rufus Leonard Limited.

2.2.1 Value Proposition undertaken by Barclay Bank

In order to gain an understanding about what are the expectations of the customers from

the company and what are the promises being made by the Barclay Bank to attract the customers,

the company lays its significant concern over proposing an innovative and differentiated

products to attract the eyes of its potential customers thereby retaining its existing clients in a

significant and impressive way (Schakett, Gao and El-Ansary, 2011). But in the present case

scenario, Barclay bank fails to adopt such proposition which results in significant downturn of

the overall business operations. The concerned entity does not focus its attention over the capital

requirements and fails to adopt the optimal mix of capital as well as financial resources

2

corporate acquisitions which broadly includes London. Provincial and South Western Bank,

Mercantile Credit and the Woolwich. Currently, the company is listed on the London Stock

Exchange and is a significant part of FTSE 100Index.

The another B2B Company is Rufus Leonard Limited, which is a privately owned

organisation deals in hosting industry and website designing. It provides the companies with

B2B brands, energy suppliers, telecom, retail banking markets and children's charity. The said

organisation is headquartered in London and constitutes as one of the best and fast growing B2B

companies in UK. The company deals in providing the best customer services along with

impressive management of funds. It operates as a digital agency in a significant way. The

concerned innovative and positive brands renders creative and impressive communications to its

core high profile clients which broadly includes Bank of Scotland, British Gas and O2. Rufus

Leonard posses the strong ability to gain an exotic global exposure by combining its competitive

experience with its traditional brand developing skills (Kärkkäinen, Jussila and Väisänen, 2010).

2.2 The Value Proposition

Value Proposition refers to an innovation, feature or services which an organisation

incorporates to make its product or service attractive to its target customers. It reflects a promise

of value to be acknowledged and delivered by the companies in an appropriate and systematic

way. Considering this fact, the present report will discuss the crucial aspects of proposition

mirror adopted by Barclay Bank and Rufus Leonard Limited.

2.2.1 Value Proposition undertaken by Barclay Bank

In order to gain an understanding about what are the expectations of the customers from

the company and what are the promises being made by the Barclay Bank to attract the customers,

the company lays its significant concern over proposing an innovative and differentiated

products to attract the eyes of its potential customers thereby retaining its existing clients in a

significant and impressive way (Schakett, Gao and El-Ansary, 2011). But in the present case

scenario, Barclay bank fails to adopt such proposition which results in significant downturn of

the overall business operations. The concerned entity does not focus its attention over the capital

requirements and fails to adopt the optimal mix of capital as well as financial resources

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2.2.2 Value proposition undertaken by Rufus Leonard Limited

The concerned B2B company focuses its attention over the following value proposition

techniques-

Getting in total compliance with the minimum regulatory capital requirements as set by

the UK FSA.

To maintain enough capital and financial resources in order to successfully overcome the

risk appetite.

Supporting the credit rating criteria of UK banks.

2.3 The Customer Experience

Customer experience reflects a strong interaction between a company and its consumer in

a significant way. The concerned interaction encompasses customer's awareness, attraction,

cultivation, discovery, advocacy, use and purchase of a particular service (Tools, 2016). It is a

systematic and revolutionary process that companies seeks to adopt in order to gain the highest

level of consumer's trust, loyalty, commitment and confidence towards their brand. With this

regard, the customer experiences of Barclay Bank and Refuses Leonard Limited is explained as

follows-

2.3.1 Customer Experience in Barclay Bank

Barclay Bank does not reach in attaining the level of customer satisfaction. This is due to

the fact that the company does not provide its customers with effective and knowledgable

information in an appropriate way. This results in sudden downfall of its overall business

activities (Ewing, Windisch and Newton, 2010.). Also, the company does not posses a

customized range of relationship management which negatively affects the business unit to gain

the customers' trust and loyalty. Furthermore, the wealth managers appointed in Barclay Bank

fails to give proper and appropriate information to its customers which in turn results in reducing

its clients in a significant way. All such factors makes the concerned financial entity a bad B2B

company.

2.3.2 Customer Experience in Refuses Leonard

The major reasons for being a good and one of the leading B2B company in UK is that,

Refuses Leonard lays its significant concern over providing its clients with what they want and

3

The concerned B2B company focuses its attention over the following value proposition

techniques-

Getting in total compliance with the minimum regulatory capital requirements as set by

the UK FSA.

To maintain enough capital and financial resources in order to successfully overcome the

risk appetite.

Supporting the credit rating criteria of UK banks.

2.3 The Customer Experience

Customer experience reflects a strong interaction between a company and its consumer in

a significant way. The concerned interaction encompasses customer's awareness, attraction,

cultivation, discovery, advocacy, use and purchase of a particular service (Tools, 2016). It is a

systematic and revolutionary process that companies seeks to adopt in order to gain the highest

level of consumer's trust, loyalty, commitment and confidence towards their brand. With this

regard, the customer experiences of Barclay Bank and Refuses Leonard Limited is explained as

follows-

2.3.1 Customer Experience in Barclay Bank

Barclay Bank does not reach in attaining the level of customer satisfaction. This is due to

the fact that the company does not provide its customers with effective and knowledgable

information in an appropriate way. This results in sudden downfall of its overall business

activities (Ewing, Windisch and Newton, 2010.). Also, the company does not posses a

customized range of relationship management which negatively affects the business unit to gain

the customers' trust and loyalty. Furthermore, the wealth managers appointed in Barclay Bank

fails to give proper and appropriate information to its customers which in turn results in reducing

its clients in a significant way. All such factors makes the concerned financial entity a bad B2B

company.

2.3.2 Customer Experience in Refuses Leonard

The major reasons for being a good and one of the leading B2B company in UK is that,

Refuses Leonard lays its significant concern over providing its clients with what they want and

3

not what the company have for them. It emphasises on considering the needs and requirements of

its customers and thereafter proposes a suitable investment product for them which helps them to

manage their funds. The vital activities of Refuses Leonard to gain and attract huge crowd of

audience involves the following-

Customized focused products.

Introducing free internet services in banking halls.

Providing adequate and essential information to its clients in an appropriate way.

Establishing smarter human banking services.

3. Developing a customer relationship management improvement strategy for

Barclay Bank

3.1 Introduction

With a view to develop a strong and positive customer relationship improvement

strategy, Barclay Bank is highly recommended providing its customers with suitable information

regarding to their investment decisions. It should focus on incorporating a strong customer

relationship management strategy in its workforce to overcome the major challenges which it is

facing in the vast hyper competitive environment (Kotler, 2011). Customer relationship

management (CRM), in simple terms reflects the practices, techniques, technologies and the

strategies that the organisation use in order to manage and examine the customer interactions in a

significant and appropriate way. It is considered as one of the most important tool to achieve the

organisation's success thereby building a strong and positive relationship with its target audience.

In order to incorporate a CRM improvement strategy, Barclay Bank is advised to lay its

significant concern over the following issues-

To effectively identify the profitable prospects and customers of the company.

To devote its maximum time in expanding the corporate relationship with its target

customers by focusing on customized service, individualised marketing, discretionary

decision making, repricing etc.

Making friendly and positive interactions with its customers through individualization.

To follow up in order to make sure that the customers are satisfied with the services they

availed from such company (Gligorijević and Janičić, 2011).

To resolve the grievances of its customers in an effective and impressive way.

4

its customers and thereafter proposes a suitable investment product for them which helps them to

manage their funds. The vital activities of Refuses Leonard to gain and attract huge crowd of

audience involves the following-

Customized focused products.

Introducing free internet services in banking halls.

Providing adequate and essential information to its clients in an appropriate way.

Establishing smarter human banking services.

3. Developing a customer relationship management improvement strategy for

Barclay Bank

3.1 Introduction

With a view to develop a strong and positive customer relationship improvement

strategy, Barclay Bank is highly recommended providing its customers with suitable information

regarding to their investment decisions. It should focus on incorporating a strong customer

relationship management strategy in its workforce to overcome the major challenges which it is

facing in the vast hyper competitive environment (Kotler, 2011). Customer relationship

management (CRM), in simple terms reflects the practices, techniques, technologies and the

strategies that the organisation use in order to manage and examine the customer interactions in a

significant and appropriate way. It is considered as one of the most important tool to achieve the

organisation's success thereby building a strong and positive relationship with its target audience.

In order to incorporate a CRM improvement strategy, Barclay Bank is advised to lay its

significant concern over the following issues-

To effectively identify the profitable prospects and customers of the company.

To devote its maximum time in expanding the corporate relationship with its target

customers by focusing on customized service, individualised marketing, discretionary

decision making, repricing etc.

Making friendly and positive interactions with its customers through individualization.

To follow up in order to make sure that the customers are satisfied with the services they

availed from such company (Gligorijević and Janičić, 2011).

To resolve the grievances of its customers in an effective and impressive way.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Apart from this, the cited entity is also recommended to use Qci/Payne model and to

develop a new value proposition to attract huge mass of audience towards its brand.

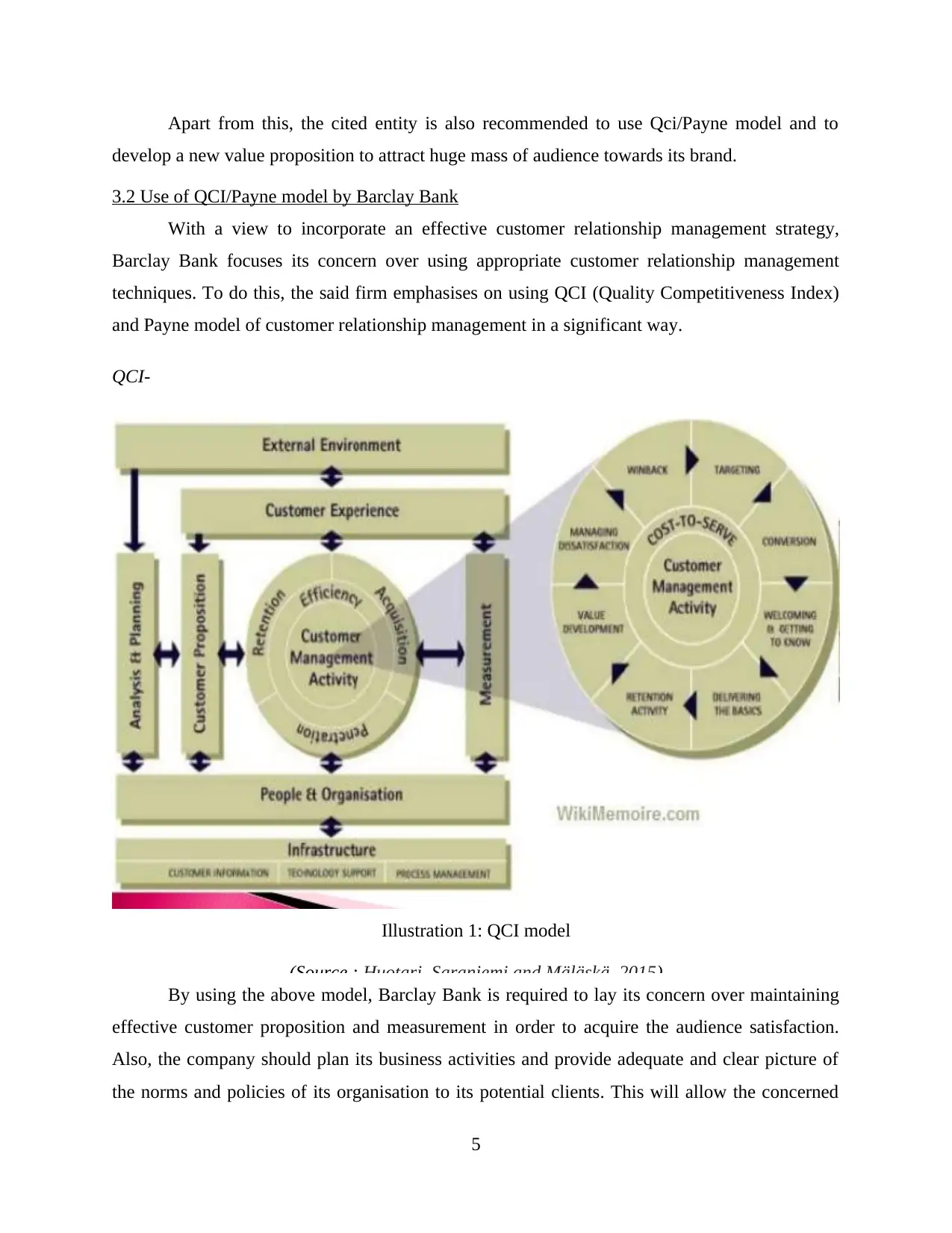

3.2 Use of QCI/Payne model by Barclay Bank

With a view to incorporate an effective customer relationship management strategy,

Barclay Bank focuses its concern over using appropriate customer relationship management

techniques. To do this, the said firm emphasises on using QCI (Quality Competitiveness Index)

and Payne model of customer relationship management in a significant way.

QCI-

Illustration 1: QCI model

(Source : Huotari, Saraniemi and Mäläskä, 2015)

By using the above model, Barclay Bank is required to lay its concern over maintaining

effective customer proposition and measurement in order to acquire the audience satisfaction.

Also, the company should plan its business activities and provide adequate and clear picture of

the norms and policies of its organisation to its potential clients. This will allow the concerned

5

develop a new value proposition to attract huge mass of audience towards its brand.

3.2 Use of QCI/Payne model by Barclay Bank

With a view to incorporate an effective customer relationship management strategy,

Barclay Bank focuses its concern over using appropriate customer relationship management

techniques. To do this, the said firm emphasises on using QCI (Quality Competitiveness Index)

and Payne model of customer relationship management in a significant way.

QCI-

Illustration 1: QCI model

(Source : Huotari, Saraniemi and Mäläskä, 2015)

By using the above model, Barclay Bank is required to lay its concern over maintaining

effective customer proposition and measurement in order to acquire the audience satisfaction.

Also, the company should plan its business activities and provide adequate and clear picture of

the norms and policies of its organisation to its potential clients. This will allow the concerned

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

entity to gain the highest level of customers trust and commitment towards its brand. By

implementing the concerned customer relationship management technique, the said firm should

focus on building such strategic measures which helps it to retain its existing customers and

attract the eyes of its new and prospective audience in an impressive way (Keshvari and et.al.,

2012). This model also assist the Barclay Bank to utilize the technologies for the overall

upliftment of its business activities.

Payne model-

This model identifies the five major process in managing customer relationship within the

workforce. By adopting this model, Barclay Bank is advised to lay its prior concern over

developing appropriate strategies along with effective value proposition. Furthermore, the said

6

Illustration 2: Payne model

(Source : Hornik, J., and et.al., 2015)

implementing the concerned customer relationship management technique, the said firm should

focus on building such strategic measures which helps it to retain its existing customers and

attract the eyes of its new and prospective audience in an impressive way (Keshvari and et.al.,

2012). This model also assist the Barclay Bank to utilize the technologies for the overall

upliftment of its business activities.

Payne model-

This model identifies the five major process in managing customer relationship within the

workforce. By adopting this model, Barclay Bank is advised to lay its prior concern over

developing appropriate strategies along with effective value proposition. Furthermore, the said

6

Illustration 2: Payne model

(Source : Hornik, J., and et.al., 2015)

financial entity is required to focus on the multichannel integration process and the performance

assessment process to gain the understanding about its customer services in a systematic and

suitable way.

3.3 Developing a new value proposition for Barclay Bank

In order to gain huge market share along with relative market growth across the globe,

the cited financial firm is highly required to propose its new value proposition in order to launch

an innovative and differentiated products to gain the customers' satisfaction. Considering this

fact, the capital management strategy of Barclay will seek to increase the value of its

shareholders by optimizing the overall mix and the level of its capital and financial resources in a

significant way (Steenkamp and Fang, 2011). The company's ability to conduct its business

operations as a financial service corporation is strongly conditional upon the adequate and

appropriate maintenance of its capital resources. Furthermore, Barclay Bank should operate its

financial activities in accordance with centralized capital management model and should lay its

significant concern over the economic and regulatory capital. Also, the said entity should

communicate to its customers the relevant information regarding their investments in an

appropriate way. This will allow the company to retain its existing clients thereby attracting new

clients towards its brans, Barclay Bank should provide its core clients with effective wealth

managers who can solve the grievances of its customers in an effective and appropriate way. All

such measures, will no doubt, help the said financial service company to make a competitive and

winning edge in the vast international economies thereby attaining a strong brand recognition in

the eyes of its core customers (Girard, 2012).

3.4 Other concepts of business operations of Barclay Bank

Besides laying its concern over developing an effective CRM and proposing a new value

proposition, Barclay Bank is also required to consider other business operations in a significant

way. The other business concepts broadly includes the following- Effective leadership- This is one of the most important aspects of conducting an effective

and successful business activities. Effective leadership acts as a backbone to the overall

organisation's activities. Failure of this, would lead the company in sudden downturn

thereby resulting its failure in the tough trading competitive environment. Therefore,

Barclay Bank should implement an effective leadership within its workforce to enhance

its productivity and performance in the vast international economies (Spicka, 2013).

7

assessment process to gain the understanding about its customer services in a systematic and

suitable way.

3.3 Developing a new value proposition for Barclay Bank

In order to gain huge market share along with relative market growth across the globe,

the cited financial firm is highly required to propose its new value proposition in order to launch

an innovative and differentiated products to gain the customers' satisfaction. Considering this

fact, the capital management strategy of Barclay will seek to increase the value of its

shareholders by optimizing the overall mix and the level of its capital and financial resources in a

significant way (Steenkamp and Fang, 2011). The company's ability to conduct its business

operations as a financial service corporation is strongly conditional upon the adequate and

appropriate maintenance of its capital resources. Furthermore, Barclay Bank should operate its

financial activities in accordance with centralized capital management model and should lay its

significant concern over the economic and regulatory capital. Also, the said entity should

communicate to its customers the relevant information regarding their investments in an

appropriate way. This will allow the company to retain its existing clients thereby attracting new

clients towards its brans, Barclay Bank should provide its core clients with effective wealth

managers who can solve the grievances of its customers in an effective and appropriate way. All

such measures, will no doubt, help the said financial service company to make a competitive and

winning edge in the vast international economies thereby attaining a strong brand recognition in

the eyes of its core customers (Girard, 2012).

3.4 Other concepts of business operations of Barclay Bank

Besides laying its concern over developing an effective CRM and proposing a new value

proposition, Barclay Bank is also required to consider other business operations in a significant

way. The other business concepts broadly includes the following- Effective leadership- This is one of the most important aspects of conducting an effective

and successful business activities. Effective leadership acts as a backbone to the overall

organisation's activities. Failure of this, would lead the company in sudden downturn

thereby resulting its failure in the tough trading competitive environment. Therefore,

Barclay Bank should implement an effective leadership within its workforce to enhance

its productivity and performance in the vast international economies (Spicka, 2013).

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Employment engagement techniques- Employees of the organisation plays a vital role in

achieving organisation's success. They contribute highly in the firm's profitability and

performance in the global corporate environment. It therefore, becomes mandatory for

every organisation to treat its employees as an asset for the company rather than cost.

Considering this fact, Barclay Bank should lay its significant concern over implementing

fascinating employee engagement techniques such as providing them with attractive

incentives, monetary rewards, recognition and appraisals (Kim and Baik, 2013). This will

help the firm to reduce its staff turnover and become a good B2B company in an

impressive manner.

KAM (Key Account Management)- It is also one of the important business concept

which Barclay Bank is required to consider in its course of business operations. As per

this concept, the said entity is highly required to focus on managing its internal account

system in an effective and systematic way. This will allow the company to refer to the

issues and grievances which it is facing in the external environment and will also assist

the firm to adopt suitable techniques to overcome such problems in an appropriate and

suitable way.

3.5 Customer Experience in Barclay Bank

After implementing an effective CRM strategy and incorporating an attractive value

proposition along with considering other significant business concepts, Barclay Bank is now

recommended analysing the experiences of its core customers in a significant and appropriate

way. This reflects in analysing and examining the satisfaction level of its clients with the services

rendered by the said entity (Lord and Gupta, 2010). By monitoring the customer experience, the

company is able to gain deep knowledge and understanding about the needs and requirements of

its clients. It also assists Barclay Bank to render customized services in order to gain the highest

level of customer satisfaction thereby attaining huge market share across the globe (Model for

Customer Experience Management Strategy, 2016).

CONCLUSION

From the above report it can be concluded that, Barclay Bank is on the track of removing

its tag of bad B2B company in a significant way. The company is using tremendous approaches

to gain an exotic global exposure across the world (Hörndahl and Dervisevic, 2015). The report

8

achieving organisation's success. They contribute highly in the firm's profitability and

performance in the global corporate environment. It therefore, becomes mandatory for

every organisation to treat its employees as an asset for the company rather than cost.

Considering this fact, Barclay Bank should lay its significant concern over implementing

fascinating employee engagement techniques such as providing them with attractive

incentives, monetary rewards, recognition and appraisals (Kim and Baik, 2013). This will

help the firm to reduce its staff turnover and become a good B2B company in an

impressive manner.

KAM (Key Account Management)- It is also one of the important business concept

which Barclay Bank is required to consider in its course of business operations. As per

this concept, the said entity is highly required to focus on managing its internal account

system in an effective and systematic way. This will allow the company to refer to the

issues and grievances which it is facing in the external environment and will also assist

the firm to adopt suitable techniques to overcome such problems in an appropriate and

suitable way.

3.5 Customer Experience in Barclay Bank

After implementing an effective CRM strategy and incorporating an attractive value

proposition along with considering other significant business concepts, Barclay Bank is now

recommended analysing the experiences of its core customers in a significant and appropriate

way. This reflects in analysing and examining the satisfaction level of its clients with the services

rendered by the said entity (Lord and Gupta, 2010). By monitoring the customer experience, the

company is able to gain deep knowledge and understanding about the needs and requirements of

its clients. It also assists Barclay Bank to render customized services in order to gain the highest

level of customer satisfaction thereby attaining huge market share across the globe (Model for

Customer Experience Management Strategy, 2016).

CONCLUSION

From the above report it can be concluded that, Barclay Bank is on the track of removing

its tag of bad B2B company in a significant way. The company is using tremendous approaches

to gain an exotic global exposure across the world (Hörndahl and Dervisevic, 2015). The report

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

helped to gain in depth understanding about the crucial aspects of B2B industries in the present

competitive environment along with its increasing importance in the current scenario. The report

has effectively analyses the current performance of Barclay Bank and Refuses Leonardo Limited

(a good B2B company) and have suggested measures for Barclay Bank to develop an effective

customer relationship management strategy within its workforce. Furthermore, the report has

helped to gain deep learning about the concept of value proposition and has developed

impressive value proposition strategy for Barclay Bank to become a good B2B company and to

achieve the leading heights of organisation's success in an effective and impressive way.

9

competitive environment along with its increasing importance in the current scenario. The report

has effectively analyses the current performance of Barclay Bank and Refuses Leonardo Limited

(a good B2B company) and have suggested measures for Barclay Bank to develop an effective

customer relationship management strategy within its workforce. Furthermore, the report has

helped to gain deep learning about the concept of value proposition and has developed

impressive value proposition strategy for Barclay Bank to become a good B2B company and to

achieve the leading heights of organisation's success in an effective and impressive way.

9

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.