B7AF111 Advanced Economic Perspectives: The Flaw Document Analysis

VerifiedAdded on 2021/11/17

|7

|2305

|60

Report

AI Summary

This document analyzes the 2008 and 1929 financial crises, attributing them primarily to increased income inequality and high household debt. It examines the deregulation of the financial sector, globalization, and the rise of subprime mortgages as contributing factors to the 2008 crisis, drawing parallels with the 1929 crisis and the role of easy credit and market manipulation. The report also explores the Keynesian response to the Great Depression, highlighting government intervention to stimulate demand and employment. It further discusses the decline of Keynesian economics in the 1970s and the subsequent shift towards less government intervention, offering a comprehensive overview of economic perspectives and historical events.

B7AF111 Advanced Economic Perspectives

‘The Flaw’ document analysis

Page 1 of 7

B7AF111 Advanced Economic Perspectives, Dermot Gallagher

‘The Flaw’

Document Analysis

Total Words 1,947

Phil Darcy 10542773

‘The Flaw’ document analysis

Page 1 of 7

B7AF111 Advanced Economic Perspectives, Dermot Gallagher

‘The Flaw’

Document Analysis

Total Words 1,947

Phil Darcy 10542773

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

B7AF111 Advanced Economic Perspectives

‘The Flaw’ document analysis

Page 2 of 7

2008 Financial Crisis

On September 15th, 2008 Lehman Brothers collapsed. For many, this marked the climax of the 2008

Financial Crisis.

There were many contributory factors which brought about the 2008 crisis. In my view, the increased

inequality in the United States, which drove high levels of debt amongst the lower and middle class was the

main cause.

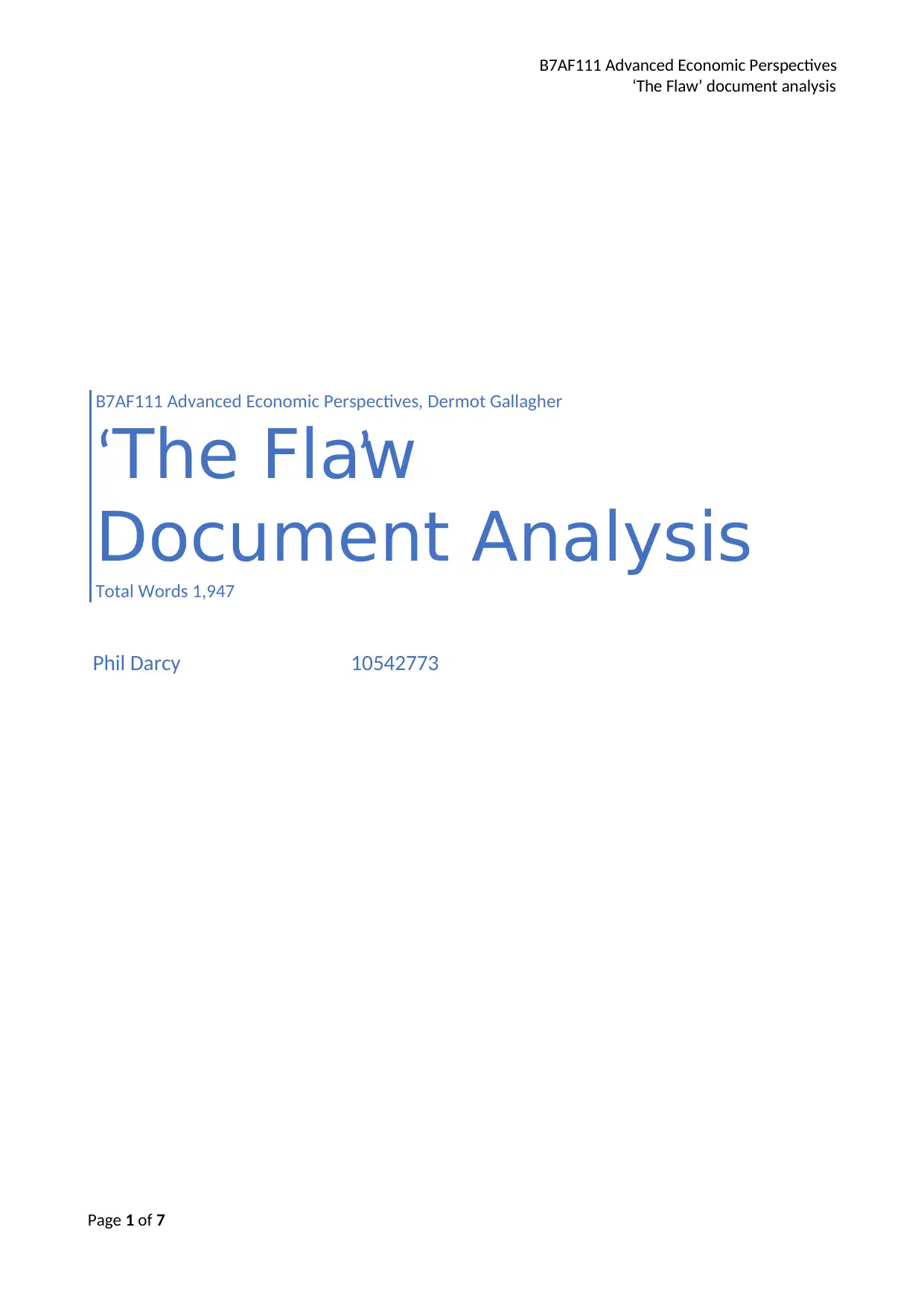

The chart below demonstrates how the ratio of household debt to personal income remained relatively

steady throughout the 60’s and 70’s but began to increase thereafter. This culminated in households taking

on more debt than they had income in the 2000’s.

To understand the cause for this we need to go back to the 1980’s.

In 1979 Margaret Thatcher was elected Prime Minister of the United Kingdom, while in 1981 Ronald Regan

was voted the 40th President of the United States. And so began a 30-year period of Financial deregulation.

One example was the deregulation of Savings & Loans companies in the United States which allowed for

risky investments to be made with customers deposits. This resulted in the failure of 100’s of Savings &

Loans companies which led to the consolidation of the financial sector to a few large powerful firms by the

late 90’s – creating an Oligopoly within the market.

Meanwhile, as the Financial sector was experiencing a period of deregulation, an economic globalization

was taking place. Trade agreements put in place across the globe prioritised corporate interests but

provided little protection against a race to the bottom for labour.

Businesses moved manufacturing to lower waged countries which boosted company profits. However,

rather than reinvest profits into production, innovation, and capital expenditure - which could stimulate job

creation in other areas to mitigate deindustrialisation - profits were invested in strategies such as share

buybacks, which ultimately increased executive pay and shareholder wealth.

Fewer workers in the union-dominated manufacturing sector also led to the decline of unions. And as a

result, we have seen a wage stagnation since the 1980’s for the average worker. This has directly led to

increased personal debt to simply maintain living standards.

‘The Flaw’ document analysis

Page 2 of 7

2008 Financial Crisis

On September 15th, 2008 Lehman Brothers collapsed. For many, this marked the climax of the 2008

Financial Crisis.

There were many contributory factors which brought about the 2008 crisis. In my view, the increased

inequality in the United States, which drove high levels of debt amongst the lower and middle class was the

main cause.

The chart below demonstrates how the ratio of household debt to personal income remained relatively

steady throughout the 60’s and 70’s but began to increase thereafter. This culminated in households taking

on more debt than they had income in the 2000’s.

To understand the cause for this we need to go back to the 1980’s.

In 1979 Margaret Thatcher was elected Prime Minister of the United Kingdom, while in 1981 Ronald Regan

was voted the 40th President of the United States. And so began a 30-year period of Financial deregulation.

One example was the deregulation of Savings & Loans companies in the United States which allowed for

risky investments to be made with customers deposits. This resulted in the failure of 100’s of Savings &

Loans companies which led to the consolidation of the financial sector to a few large powerful firms by the

late 90’s – creating an Oligopoly within the market.

Meanwhile, as the Financial sector was experiencing a period of deregulation, an economic globalization

was taking place. Trade agreements put in place across the globe prioritised corporate interests but

provided little protection against a race to the bottom for labour.

Businesses moved manufacturing to lower waged countries which boosted company profits. However,

rather than reinvest profits into production, innovation, and capital expenditure - which could stimulate job

creation in other areas to mitigate deindustrialisation - profits were invested in strategies such as share

buybacks, which ultimately increased executive pay and shareholder wealth.

Fewer workers in the union-dominated manufacturing sector also led to the decline of unions. And as a

result, we have seen a wage stagnation since the 1980’s for the average worker. This has directly led to

increased personal debt to simply maintain living standards.

B7AF111 Advanced Economic Perspectives

‘The Flaw’ document analysis

Page 3 of 7

In theory, globalised markets should be to the benefit of everyone. If low tech jobs leave the Unites States,

high tech jobs should become more widely available. Workers should have the opportunity to re-educate to

avail of these higher paid jobs. But with the increased demand to attend college, the cost of doing so has

sky-rocketed, and with it the need to take on further debt.

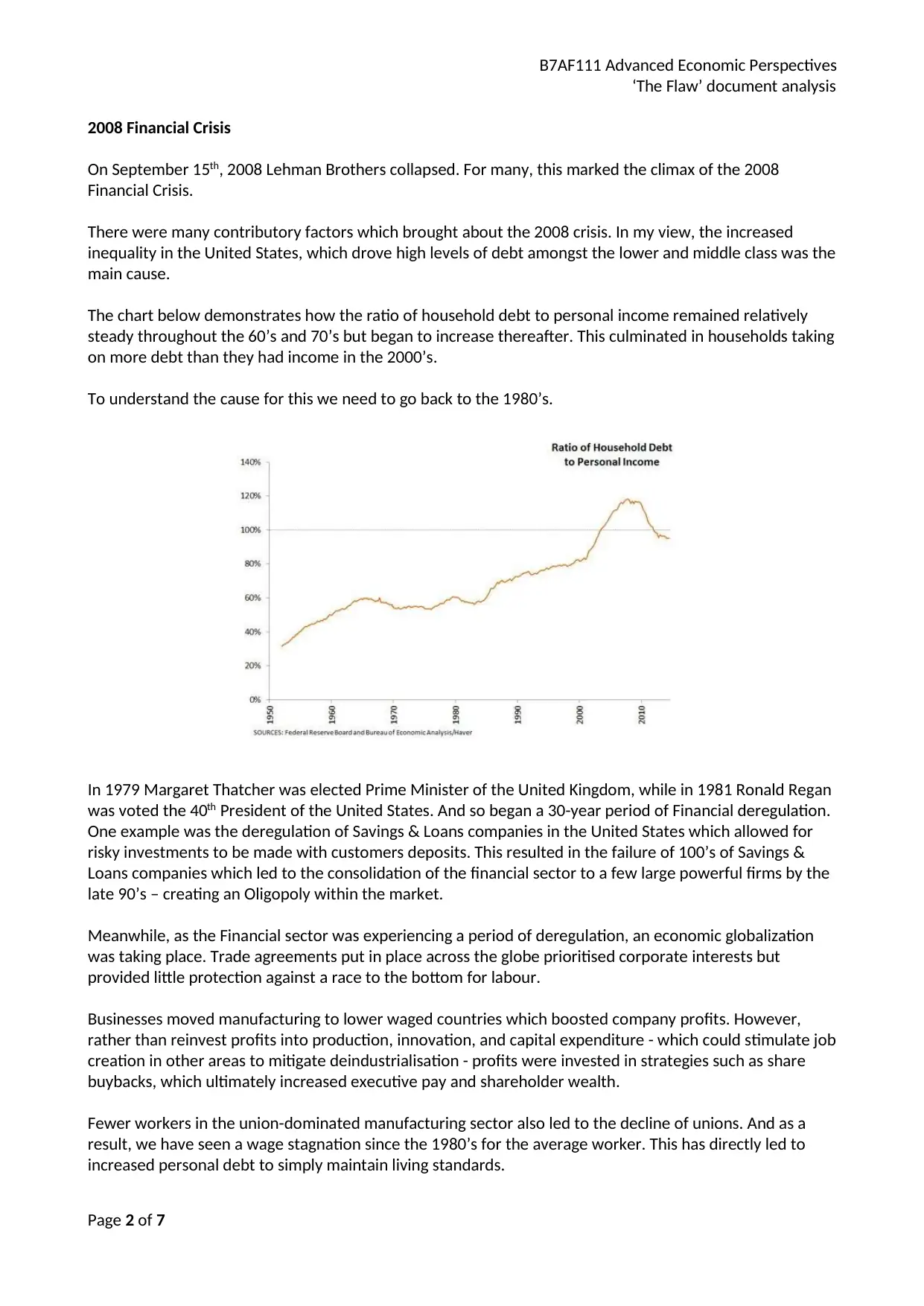

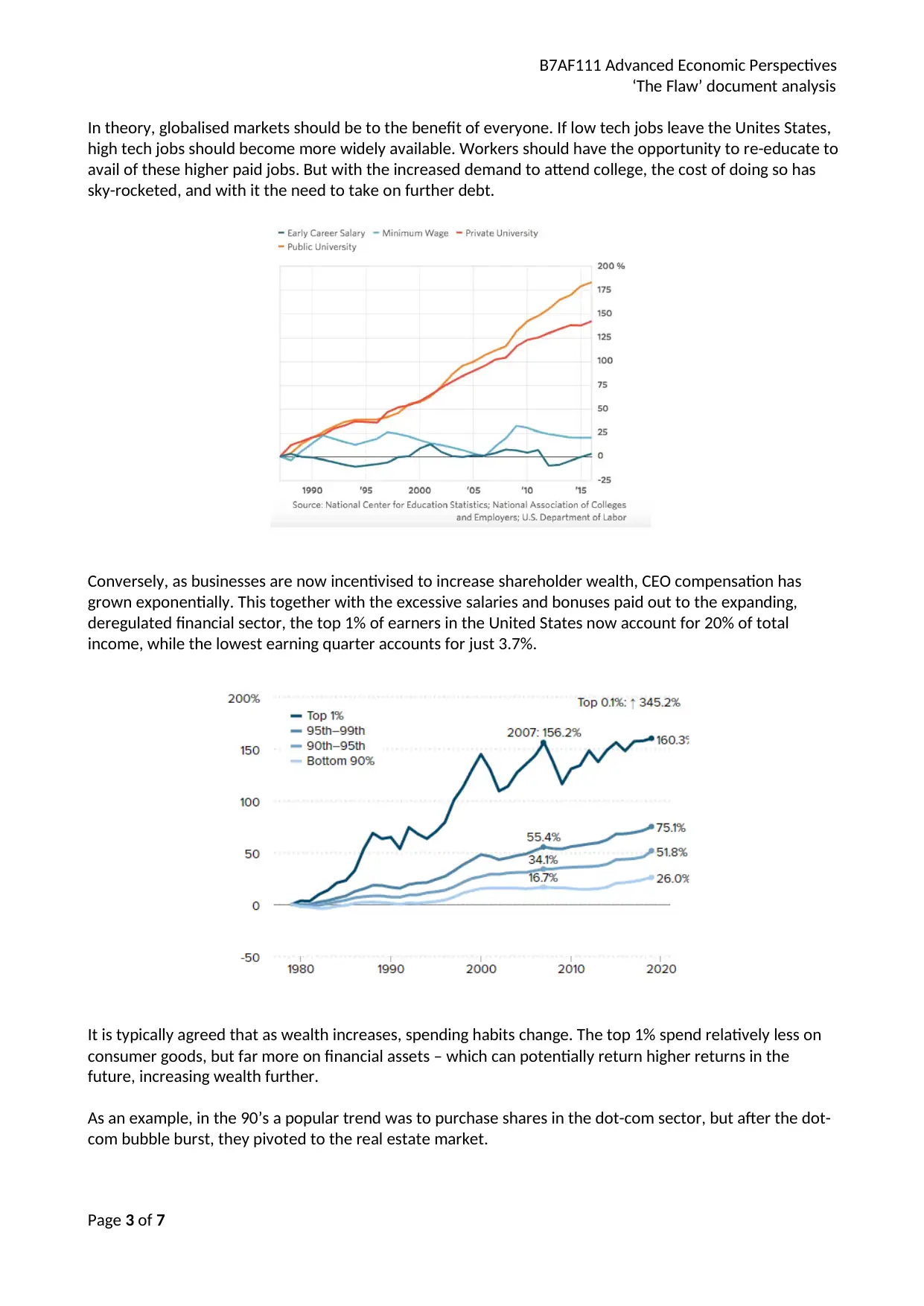

Conversely, as businesses are now incentivised to increase shareholder wealth, CEO compensation has

grown exponentially. This together with the excessive salaries and bonuses paid out to the expanding,

deregulated financial sector, the top 1% of earners in the United States now account for 20% of total

income, while the lowest earning quarter accounts for just 3.7%.

It is typically agreed that as wealth increases, spending habits change. The top 1% spend relatively less on

consumer goods, but far more on financial assets – which can potentially return higher returns in the

future, increasing wealth further.

As an example, in the 90’s a popular trend was to purchase shares in the dot-com sector, but after the dot-

com bubble burst, they pivoted to the real estate market.

‘The Flaw’ document analysis

Page 3 of 7

In theory, globalised markets should be to the benefit of everyone. If low tech jobs leave the Unites States,

high tech jobs should become more widely available. Workers should have the opportunity to re-educate to

avail of these higher paid jobs. But with the increased demand to attend college, the cost of doing so has

sky-rocketed, and with it the need to take on further debt.

Conversely, as businesses are now incentivised to increase shareholder wealth, CEO compensation has

grown exponentially. This together with the excessive salaries and bonuses paid out to the expanding,

deregulated financial sector, the top 1% of earners in the United States now account for 20% of total

income, while the lowest earning quarter accounts for just 3.7%.

It is typically agreed that as wealth increases, spending habits change. The top 1% spend relatively less on

consumer goods, but far more on financial assets – which can potentially return higher returns in the

future, increasing wealth further.

As an example, in the 90’s a popular trend was to purchase shares in the dot-com sector, but after the dot-

com bubble burst, they pivoted to the real estate market.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

B7AF111 Advanced Economic Perspectives

‘The Flaw’ document analysis

Page 4 of 7

Consider the law of supply and demand for a moment. When the price of a good rises dramatically, the

demand for that good will decrease.

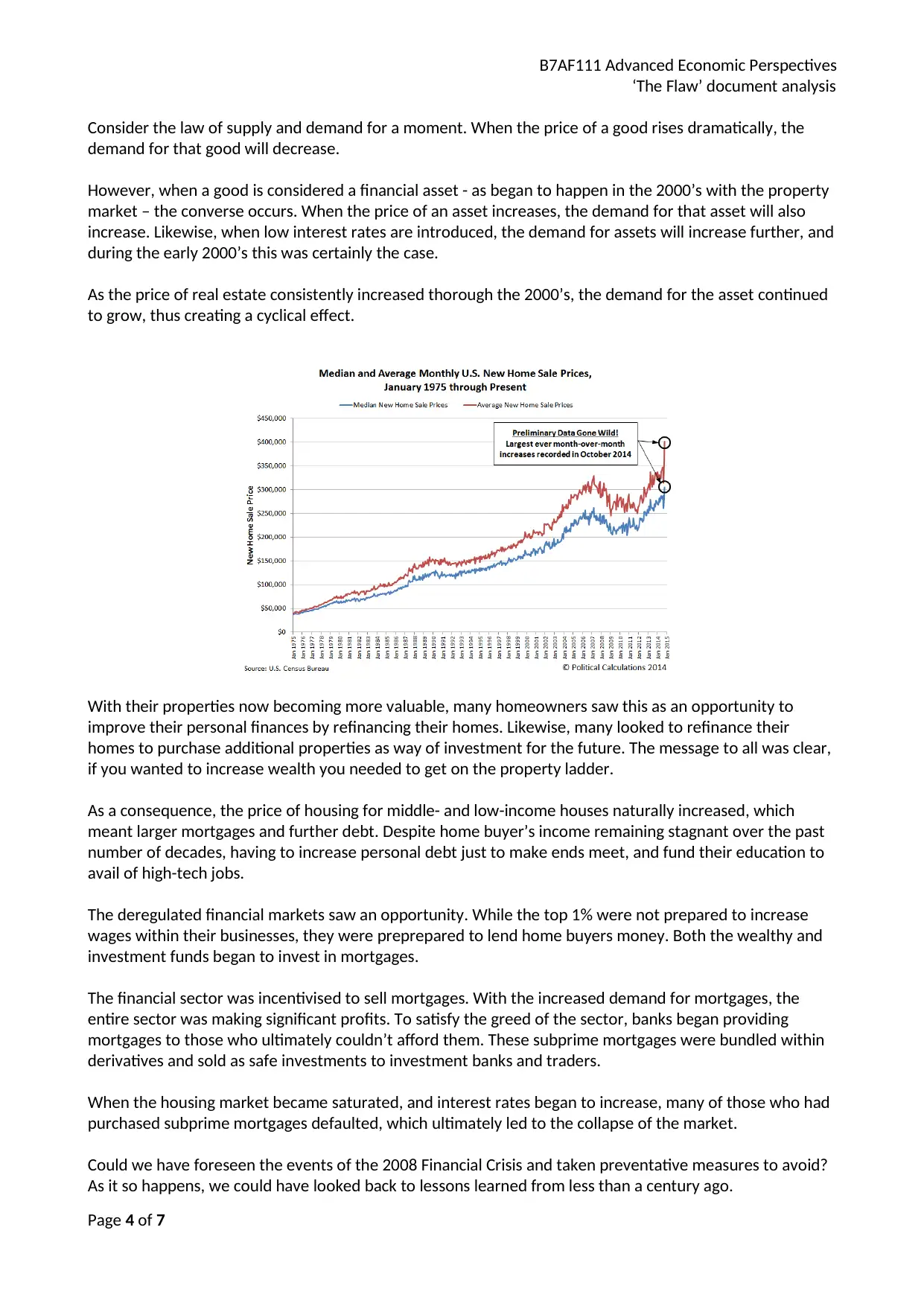

However, when a good is considered a financial asset - as began to happen in the 2000’s with the property

market – the converse occurs. When the price of an asset increases, the demand for that asset will also

increase. Likewise, when low interest rates are introduced, the demand for assets will increase further, and

during the early 2000’s this was certainly the case.

As the price of real estate consistently increased thorough the 2000’s, the demand for the asset continued

to grow, thus creating a cyclical effect.

With their properties now becoming more valuable, many homeowners saw this as an opportunity to

improve their personal finances by refinancing their homes. Likewise, many looked to refinance their

homes to purchase additional properties as way of investment for the future. The message to all was clear,

if you wanted to increase wealth you needed to get on the property ladder.

As a consequence, the price of housing for middle- and low-income houses naturally increased, which

meant larger mortgages and further debt. Despite home buyer’s income remaining stagnant over the past

number of decades, having to increase personal debt just to make ends meet, and fund their education to

avail of high-tech jobs.

The deregulated financial markets saw an opportunity. While the top 1% were not prepared to increase

wages within their businesses, they were preprepared to lend home buyers money. Both the wealthy and

investment funds began to invest in mortgages.

The financial sector was incentivised to sell mortgages. With the increased demand for mortgages, the

entire sector was making significant profits. To satisfy the greed of the sector, banks began providing

mortgages to those who ultimately couldn’t afford them. These subprime mortgages were bundled within

derivatives and sold as safe investments to investment banks and traders.

When the housing market became saturated, and interest rates began to increase, many of those who had

purchased subprime mortgages defaulted, which ultimately led to the collapse of the market.

Could we have foreseen the events of the 2008 Financial Crisis and taken preventative measures to avoid?

As it so happens, we could have looked back to lessons learned from less than a century ago.

‘The Flaw’ document analysis

Page 4 of 7

Consider the law of supply and demand for a moment. When the price of a good rises dramatically, the

demand for that good will decrease.

However, when a good is considered a financial asset - as began to happen in the 2000’s with the property

market – the converse occurs. When the price of an asset increases, the demand for that asset will also

increase. Likewise, when low interest rates are introduced, the demand for assets will increase further, and

during the early 2000’s this was certainly the case.

As the price of real estate consistently increased thorough the 2000’s, the demand for the asset continued

to grow, thus creating a cyclical effect.

With their properties now becoming more valuable, many homeowners saw this as an opportunity to

improve their personal finances by refinancing their homes. Likewise, many looked to refinance their

homes to purchase additional properties as way of investment for the future. The message to all was clear,

if you wanted to increase wealth you needed to get on the property ladder.

As a consequence, the price of housing for middle- and low-income houses naturally increased, which

meant larger mortgages and further debt. Despite home buyer’s income remaining stagnant over the past

number of decades, having to increase personal debt just to make ends meet, and fund their education to

avail of high-tech jobs.

The deregulated financial markets saw an opportunity. While the top 1% were not prepared to increase

wages within their businesses, they were preprepared to lend home buyers money. Both the wealthy and

investment funds began to invest in mortgages.

The financial sector was incentivised to sell mortgages. With the increased demand for mortgages, the

entire sector was making significant profits. To satisfy the greed of the sector, banks began providing

mortgages to those who ultimately couldn’t afford them. These subprime mortgages were bundled within

derivatives and sold as safe investments to investment banks and traders.

When the housing market became saturated, and interest rates began to increase, many of those who had

purchased subprime mortgages defaulted, which ultimately led to the collapse of the market.

Could we have foreseen the events of the 2008 Financial Crisis and taken preventative measures to avoid?

As it so happens, we could have looked back to lessons learned from less than a century ago.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

B7AF111 Advanced Economic Perspectives

‘The Flaw’ document analysis

Page 5 of 7

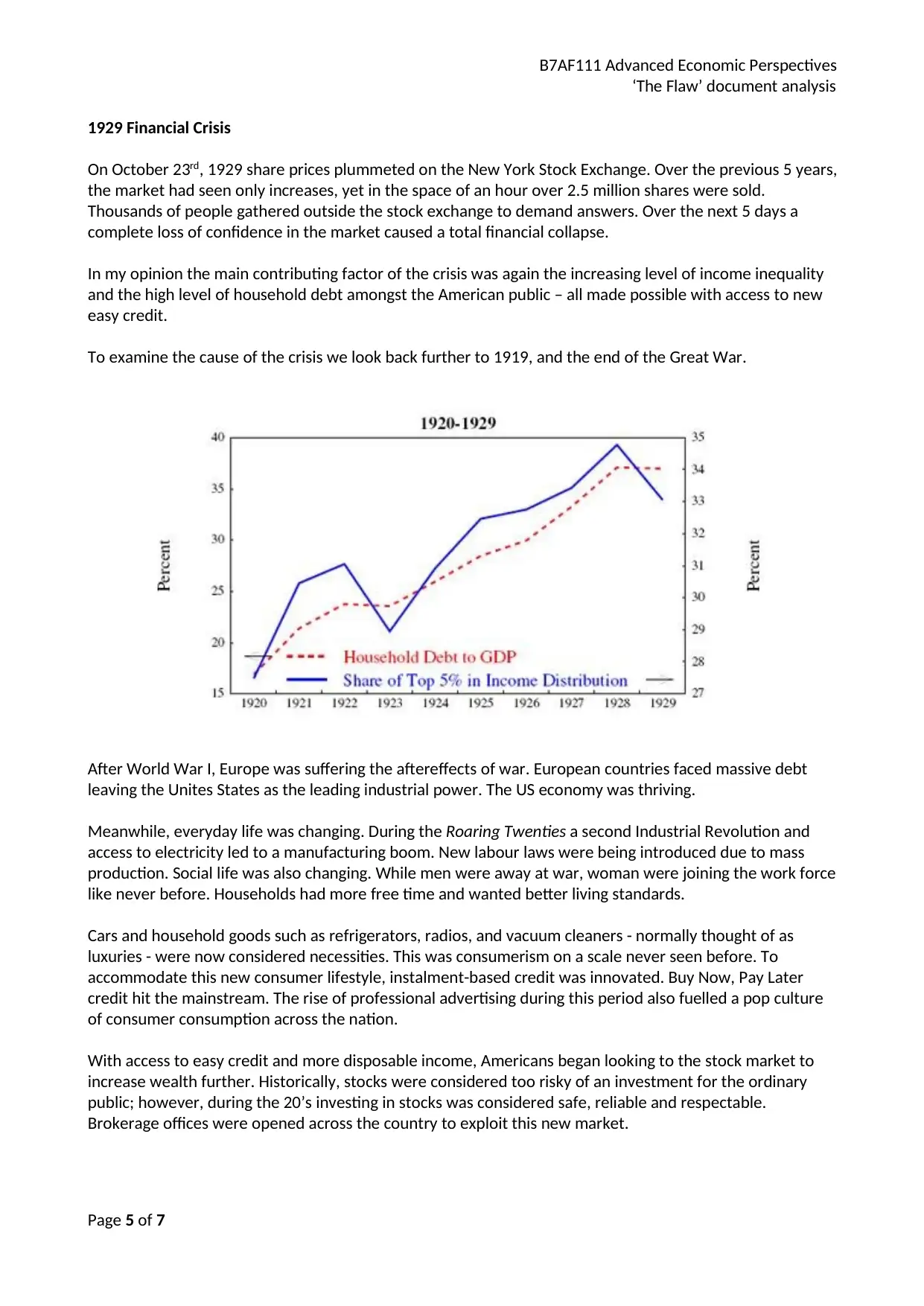

1929 Financial Crisis

On October 23rd, 1929 share prices plummeted on the New York Stock Exchange. Over the previous 5 years,

the market had seen only increases, yet in the space of an hour over 2.5 million shares were sold.

Thousands of people gathered outside the stock exchange to demand answers. Over the next 5 days a

complete loss of confidence in the market caused a total financial collapse.

In my opinion the main contributing factor of the crisis was again the increasing level of income inequality

and the high level of household debt amongst the American public – all made possible with access to new

easy credit.

To examine the cause of the crisis we look back further to 1919, and the end of the Great War.

After World War I, Europe was suffering the aftereffects of war. European countries faced massive debt

leaving the Unites States as the leading industrial power. The US economy was thriving.

Meanwhile, everyday life was changing. During the Roaring Twenties a second Industrial Revolution and

access to electricity led to a manufacturing boom. New labour laws were being introduced due to mass

production. Social life was also changing. While men were away at war, woman were joining the work force

like never before. Households had more free time and wanted better living standards.

Cars and household goods such as refrigerators, radios, and vacuum cleaners - normally thought of as

luxuries - were now considered necessities. This was consumerism on a scale never seen before. To

accommodate this new consumer lifestyle, instalment-based credit was innovated. Buy Now, Pay Later

credit hit the mainstream. The rise of professional advertising during this period also fuelled a pop culture

of consumer consumption across the nation.

With access to easy credit and more disposable income, Americans began looking to the stock market to

increase wealth further. Historically, stocks were considered too risky of an investment for the ordinary

public; however, during the 20’s investing in stocks was considered safe, reliable and respectable.

Brokerage offices were opened across the country to exploit this new market.

‘The Flaw’ document analysis

Page 5 of 7

1929 Financial Crisis

On October 23rd, 1929 share prices plummeted on the New York Stock Exchange. Over the previous 5 years,

the market had seen only increases, yet in the space of an hour over 2.5 million shares were sold.

Thousands of people gathered outside the stock exchange to demand answers. Over the next 5 days a

complete loss of confidence in the market caused a total financial collapse.

In my opinion the main contributing factor of the crisis was again the increasing level of income inequality

and the high level of household debt amongst the American public – all made possible with access to new

easy credit.

To examine the cause of the crisis we look back further to 1919, and the end of the Great War.

After World War I, Europe was suffering the aftereffects of war. European countries faced massive debt

leaving the Unites States as the leading industrial power. The US economy was thriving.

Meanwhile, everyday life was changing. During the Roaring Twenties a second Industrial Revolution and

access to electricity led to a manufacturing boom. New labour laws were being introduced due to mass

production. Social life was also changing. While men were away at war, woman were joining the work force

like never before. Households had more free time and wanted better living standards.

Cars and household goods such as refrigerators, radios, and vacuum cleaners - normally thought of as

luxuries - were now considered necessities. This was consumerism on a scale never seen before. To

accommodate this new consumer lifestyle, instalment-based credit was innovated. Buy Now, Pay Later

credit hit the mainstream. The rise of professional advertising during this period also fuelled a pop culture

of consumer consumption across the nation.

With access to easy credit and more disposable income, Americans began looking to the stock market to

increase wealth further. Historically, stocks were considered too risky of an investment for the ordinary

public; however, during the 20’s investing in stocks was considered safe, reliable and respectable.

Brokerage offices were opened across the country to exploit this new market.

B7AF111 Advanced Economic Perspectives

‘The Flaw’ document analysis

Page 6 of 7

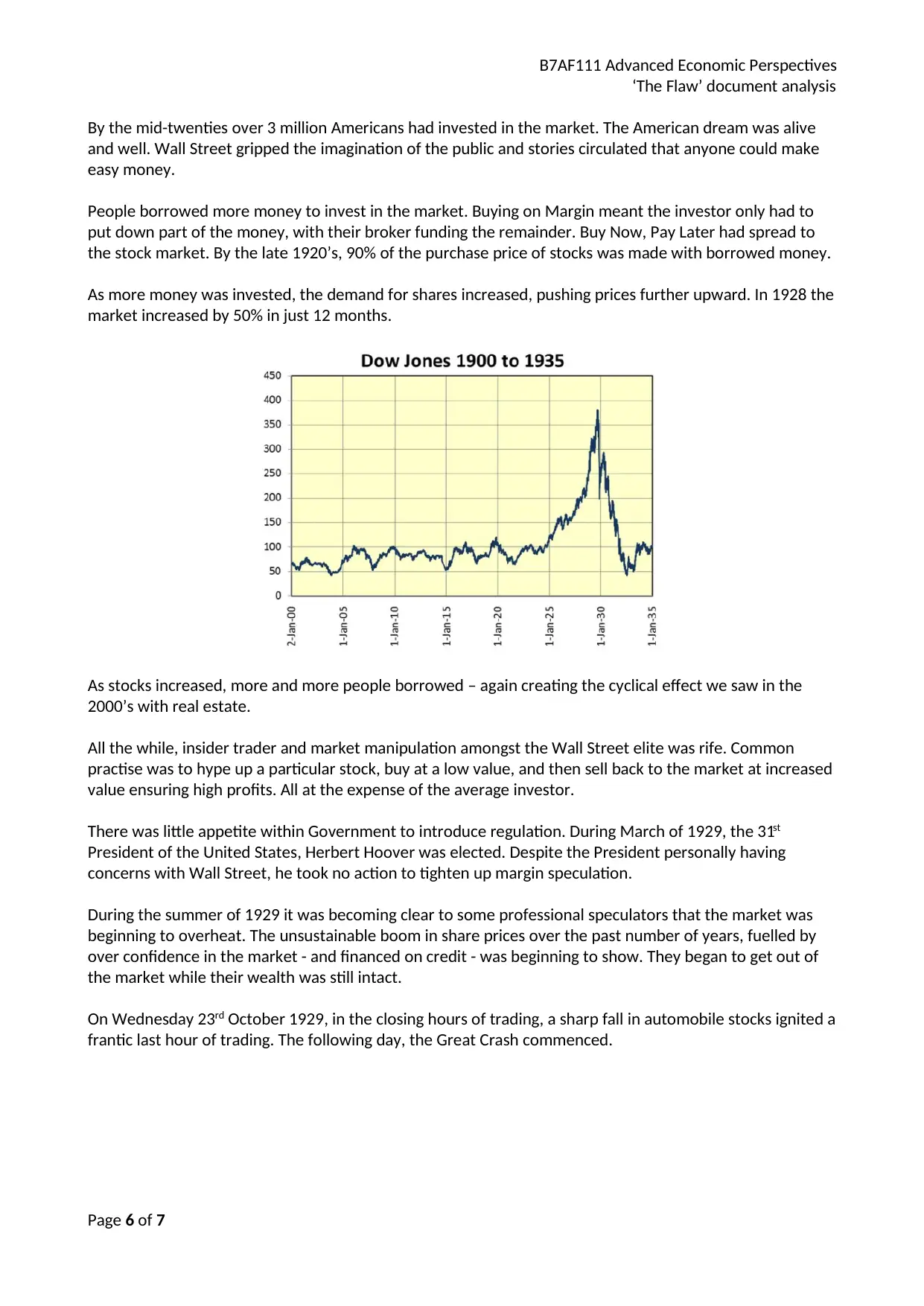

By the mid-twenties over 3 million Americans had invested in the market. The American dream was alive

and well. Wall Street gripped the imagination of the public and stories circulated that anyone could make

easy money.

People borrowed more money to invest in the market. Buying on Margin meant the investor only had to

put down part of the money, with their broker funding the remainder. Buy Now, Pay Later had spread to

the stock market. By the late 1920’s, 90% of the purchase price of stocks was made with borrowed money.

As more money was invested, the demand for shares increased, pushing prices further upward. In 1928 the

market increased by 50% in just 12 months.

As stocks increased, more and more people borrowed – again creating the cyclical effect we saw in the

2000’s with real estate.

All the while, insider trader and market manipulation amongst the Wall Street elite was rife. Common

practise was to hype up a particular stock, buy at a low value, and then sell back to the market at increased

value ensuring high profits. All at the expense of the average investor.

There was little appetite within Government to introduce regulation. During March of 1929, the 31st

President of the United States, Herbert Hoover was elected. Despite the President personally having

concerns with Wall Street, he took no action to tighten up margin speculation.

During the summer of 1929 it was becoming clear to some professional speculators that the market was

beginning to overheat. The unsustainable boom in share prices over the past number of years, fuelled by

over confidence in the market - and financed on credit - was beginning to show. They began to get out of

the market while their wealth was still intact.

On Wednesday 23rd October 1929, in the closing hours of trading, a sharp fall in automobile stocks ignited a

frantic last hour of trading. The following day, the Great Crash commenced.

‘The Flaw’ document analysis

Page 6 of 7

By the mid-twenties over 3 million Americans had invested in the market. The American dream was alive

and well. Wall Street gripped the imagination of the public and stories circulated that anyone could make

easy money.

People borrowed more money to invest in the market. Buying on Margin meant the investor only had to

put down part of the money, with their broker funding the remainder. Buy Now, Pay Later had spread to

the stock market. By the late 1920’s, 90% of the purchase price of stocks was made with borrowed money.

As more money was invested, the demand for shares increased, pushing prices further upward. In 1928 the

market increased by 50% in just 12 months.

As stocks increased, more and more people borrowed – again creating the cyclical effect we saw in the

2000’s with real estate.

All the while, insider trader and market manipulation amongst the Wall Street elite was rife. Common

practise was to hype up a particular stock, buy at a low value, and then sell back to the market at increased

value ensuring high profits. All at the expense of the average investor.

There was little appetite within Government to introduce regulation. During March of 1929, the 31st

President of the United States, Herbert Hoover was elected. Despite the President personally having

concerns with Wall Street, he took no action to tighten up margin speculation.

During the summer of 1929 it was becoming clear to some professional speculators that the market was

beginning to overheat. The unsustainable boom in share prices over the past number of years, fuelled by

over confidence in the market - and financed on credit - was beginning to show. They began to get out of

the market while their wealth was still intact.

On Wednesday 23rd October 1929, in the closing hours of trading, a sharp fall in automobile stocks ignited a

frantic last hour of trading. The following day, the Great Crash commenced.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

B7AF111 Advanced Economic Perspectives

‘The Flaw’ document analysis

Page 7 of 7

Keynesian Era

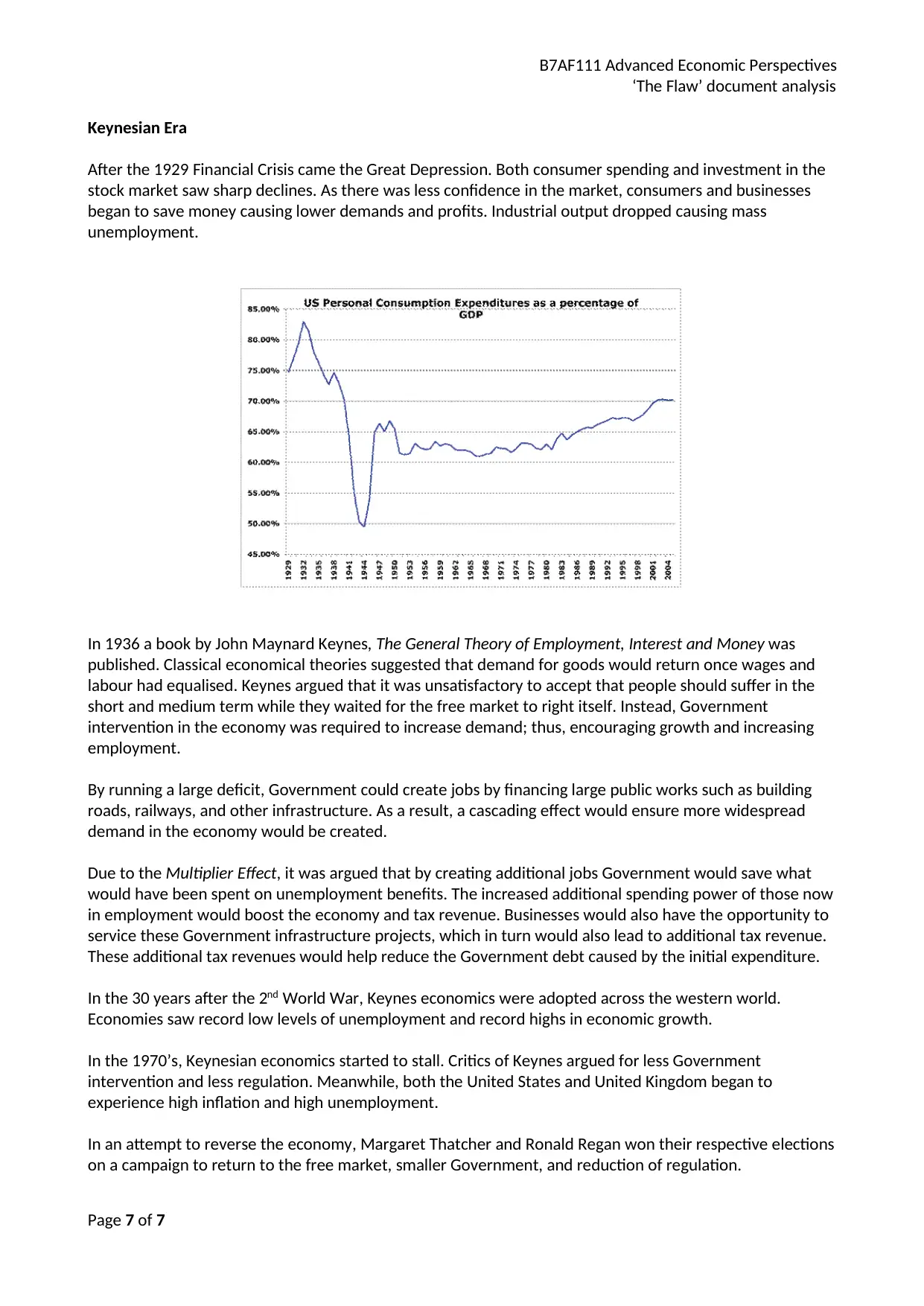

After the 1929 Financial Crisis came the Great Depression. Both consumer spending and investment in the

stock market saw sharp declines. As there was less confidence in the market, consumers and businesses

began to save money causing lower demands and profits. Industrial output dropped causing mass

unemployment.

In 1936 a book by John Maynard Keynes, The General Theory of Employment, Interest and Money was

published. Classical economical theories suggested that demand for goods would return once wages and

labour had equalised. Keynes argued that it was unsatisfactory to accept that people should suffer in the

short and medium term while they waited for the free market to right itself. Instead, Government

intervention in the economy was required to increase demand; thus, encouraging growth and increasing

employment.

By running a large deficit, Government could create jobs by financing large public works such as building

roads, railways, and other infrastructure. As a result, a cascading effect would ensure more widespread

demand in the economy would be created.

Due to the Multiplier Effect, it was argued that by creating additional jobs Government would save what

would have been spent on unemployment benefits. The increased additional spending power of those now

in employment would boost the economy and tax revenue. Businesses would also have the opportunity to

service these Government infrastructure projects, which in turn would also lead to additional tax revenue.

These additional tax revenues would help reduce the Government debt caused by the initial expenditure.

In the 30 years after the 2nd World War, Keynes economics were adopted across the western world.

Economies saw record low levels of unemployment and record highs in economic growth.

In the 1970’s, Keynesian economics started to stall. Critics of Keynes argued for less Government

intervention and less regulation. Meanwhile, both the United States and United Kingdom began to

experience high inflation and high unemployment.

In an attempt to reverse the economy, Margaret Thatcher and Ronald Regan won their respective elections

on a campaign to return to the free market, smaller Government, and reduction of regulation.

‘The Flaw’ document analysis

Page 7 of 7

Keynesian Era

After the 1929 Financial Crisis came the Great Depression. Both consumer spending and investment in the

stock market saw sharp declines. As there was less confidence in the market, consumers and businesses

began to save money causing lower demands and profits. Industrial output dropped causing mass

unemployment.

In 1936 a book by John Maynard Keynes, The General Theory of Employment, Interest and Money was

published. Classical economical theories suggested that demand for goods would return once wages and

labour had equalised. Keynes argued that it was unsatisfactory to accept that people should suffer in the

short and medium term while they waited for the free market to right itself. Instead, Government

intervention in the economy was required to increase demand; thus, encouraging growth and increasing

employment.

By running a large deficit, Government could create jobs by financing large public works such as building

roads, railways, and other infrastructure. As a result, a cascading effect would ensure more widespread

demand in the economy would be created.

Due to the Multiplier Effect, it was argued that by creating additional jobs Government would save what

would have been spent on unemployment benefits. The increased additional spending power of those now

in employment would boost the economy and tax revenue. Businesses would also have the opportunity to

service these Government infrastructure projects, which in turn would also lead to additional tax revenue.

These additional tax revenues would help reduce the Government debt caused by the initial expenditure.

In the 30 years after the 2nd World War, Keynes economics were adopted across the western world.

Economies saw record low levels of unemployment and record highs in economic growth.

In the 1970’s, Keynesian economics started to stall. Critics of Keynes argued for less Government

intervention and less regulation. Meanwhile, both the United States and United Kingdom began to

experience high inflation and high unemployment.

In an attempt to reverse the economy, Margaret Thatcher and Ronald Regan won their respective elections

on a campaign to return to the free market, smaller Government, and reduction of regulation.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.