Investment Appraisal Report: Business Decision Making (BA4008QA)

VerifiedAdded on 2022/11/25

|8

|1473

|298

Report

AI Summary

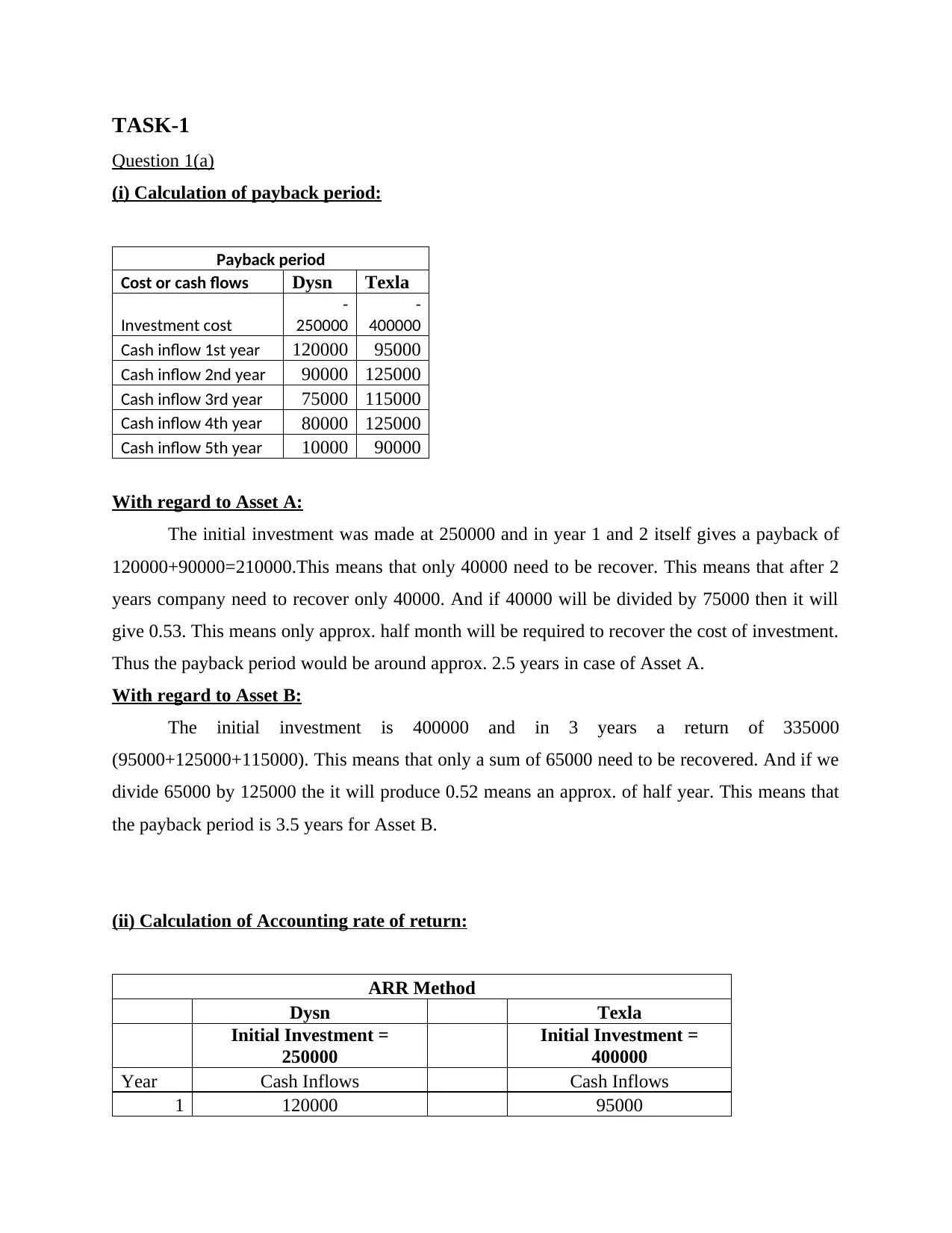

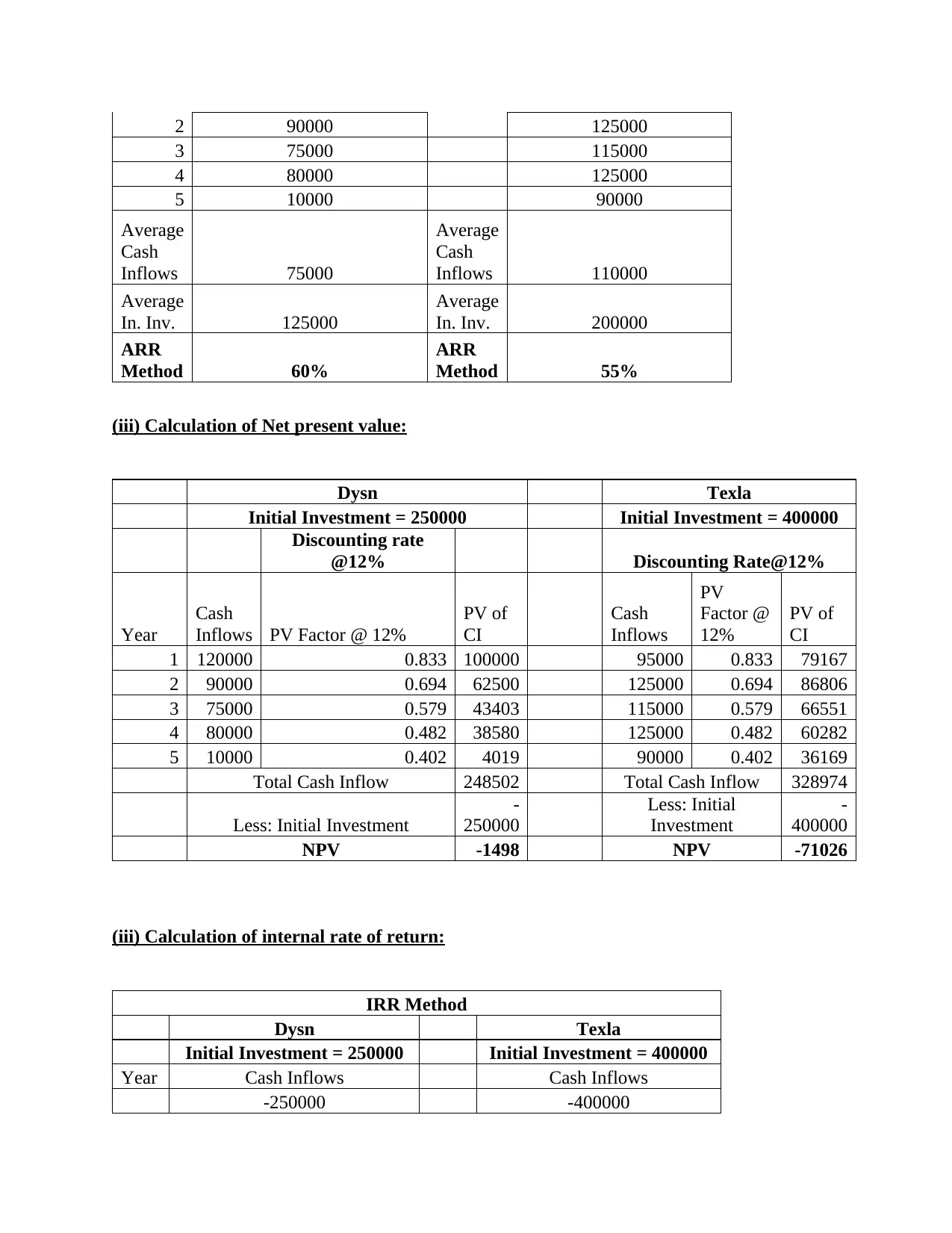

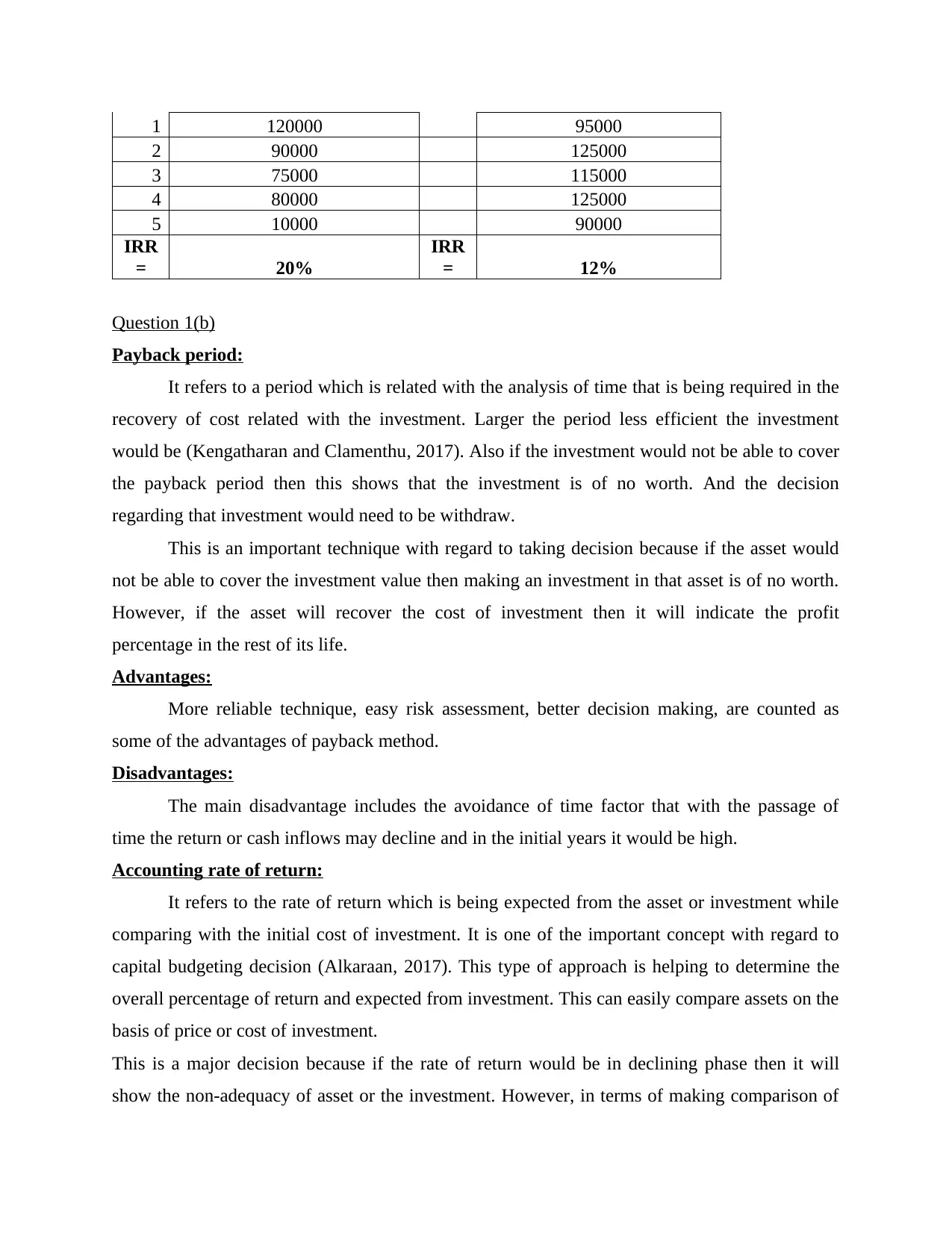

This report provides a detailed analysis of investment appraisal techniques applied to a business case involving the selection of a machine model. The report begins with the calculation of payback periods, accounting rates of return (ARR), net present values (NPV), and internal rates of return (IRR) for two machine models, Dysn and Texla. The calculations consider initial investments, cash inflows over a five-year period, and scrap values. The report then discusses the advantages and disadvantages of each appraisal method, offering insights into their practical application. The final section provides recommendations based on the analysis, suggesting the most financially viable machine model for Dolapo Plc. The report concludes by summarizing the key findings and emphasizing the importance of using various investment appraisal techniques to make informed business decisions and enhance overall business performance.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.