BACC212 - Management Accounting: Costing and Profit Improvement

VerifiedAdded on 2023/06/14

|8

|1118

|292

Report

AI Summary

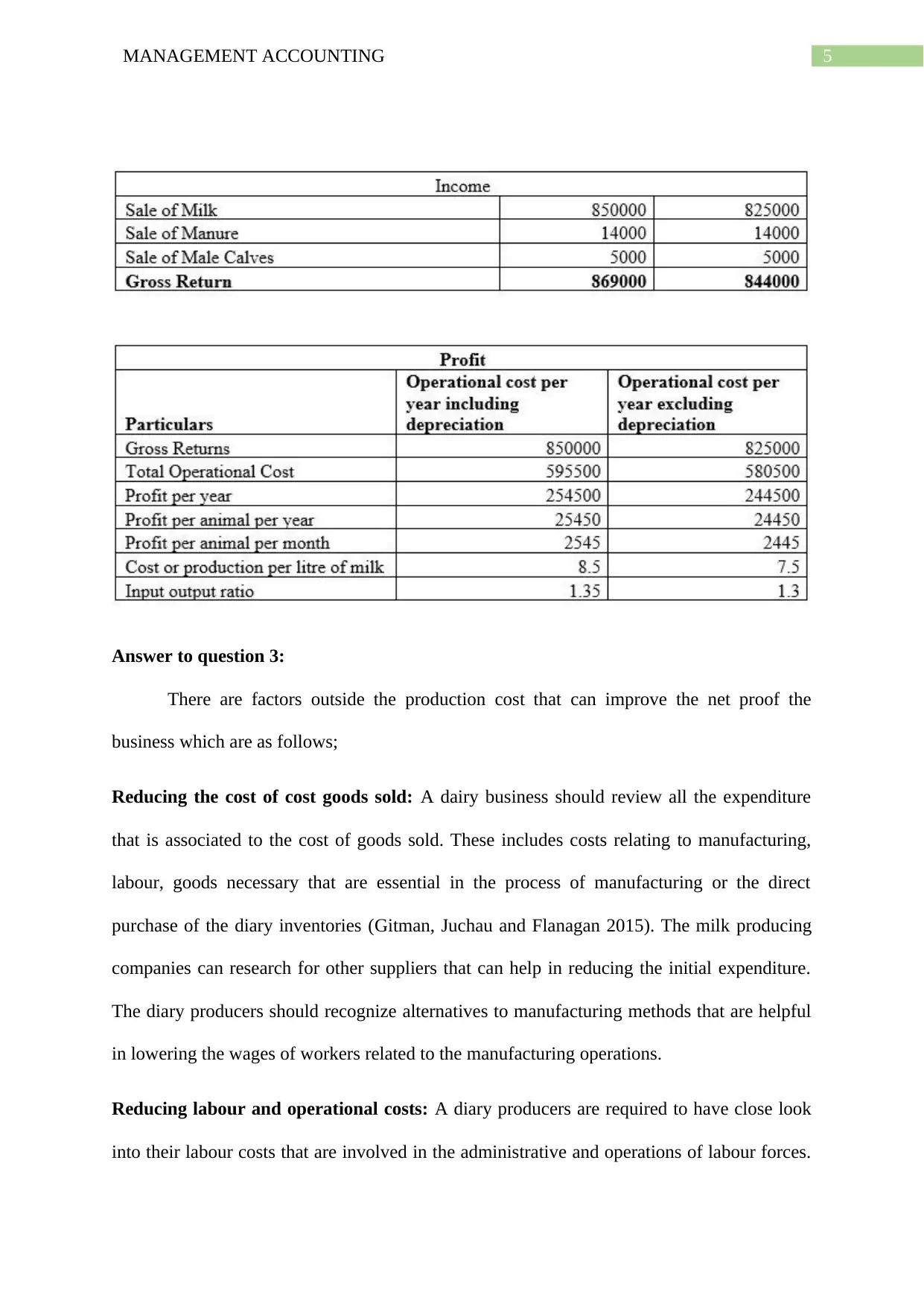

This report provides an overview of management accounting principles, focusing on costing methods and strategies for profit improvement, particularly within the context of the Australian dairy industry. It discusses the application of process costing in mass production environments, emphasizing its role in determining product costs and informing decisions related to cost control. The report also explores factors beyond production costs that can enhance a business's net profit, such as reducing the cost of goods sold, managing labor and operational expenses, and streamlining overheads through effective stock control. The content aligns with course BACC212/MPA703 and offers insights relevant to students studying management accounting. Desklib provides access to similar assignments and study tools for students.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.