BACT105 Business Accounting: Trial Balance and Adjustments Report

VerifiedAdded on 2023/06/03

|16

|2645

|489

Report

AI Summary

This business accounting report delves into the intricacies of trial balances, adjusting entries, and the preparation of financial statements. It covers key aspects such as the purpose and creation of trial balances, including identifying errors and reconciling balances. Adjusting entries, their necessity, and categories like accruals, deferrals, and estimates are explained. The report also discusses the purpose of writing an adjusted trial balance and highlights the differences between adjusting and closing journal entries, providing a comprehensive overview of essential accounting processes. The document includes numerical examples and balance sheets to illustrate the concepts. Desklib provides a platform for students to access similar solved assignments and past papers.

Running Head: BUSINESS ACCOUNTING 0

Business Accounting

Business Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BUSINESS ACCOUNTING 1

Table of Contents

Question-1..................................................................................................................................2

Question-2..................................................................................................................................3

Question-3..................................................................................................................................6

Question-4..................................................................................................................................7

Question-5..................................................................................................................................8

Question-6..................................................................................................................................9

Trial balance overview...........................................................................................................9

Purpose for Creation.............................................................................................................10

Adjusting entries...................................................................................................................11

Purpose of writing an adjusted trial balance.........................................................................11

Difference between the adjustment entries and closing journal entries...............................12

References................................................................................................................................14

Table of Contents

Question-1..................................................................................................................................2

Question-2..................................................................................................................................3

Question-3..................................................................................................................................6

Question-4..................................................................................................................................7

Question-5..................................................................................................................................8

Question-6..................................................................................................................................9

Trial balance overview...........................................................................................................9

Purpose for Creation.............................................................................................................10

Adjusting entries...................................................................................................................11

Purpose of writing an adjusted trial balance.........................................................................11

Difference between the adjustment entries and closing journal entries...............................12

References................................................................................................................................14

BUSINESS ACCOUNTING 2

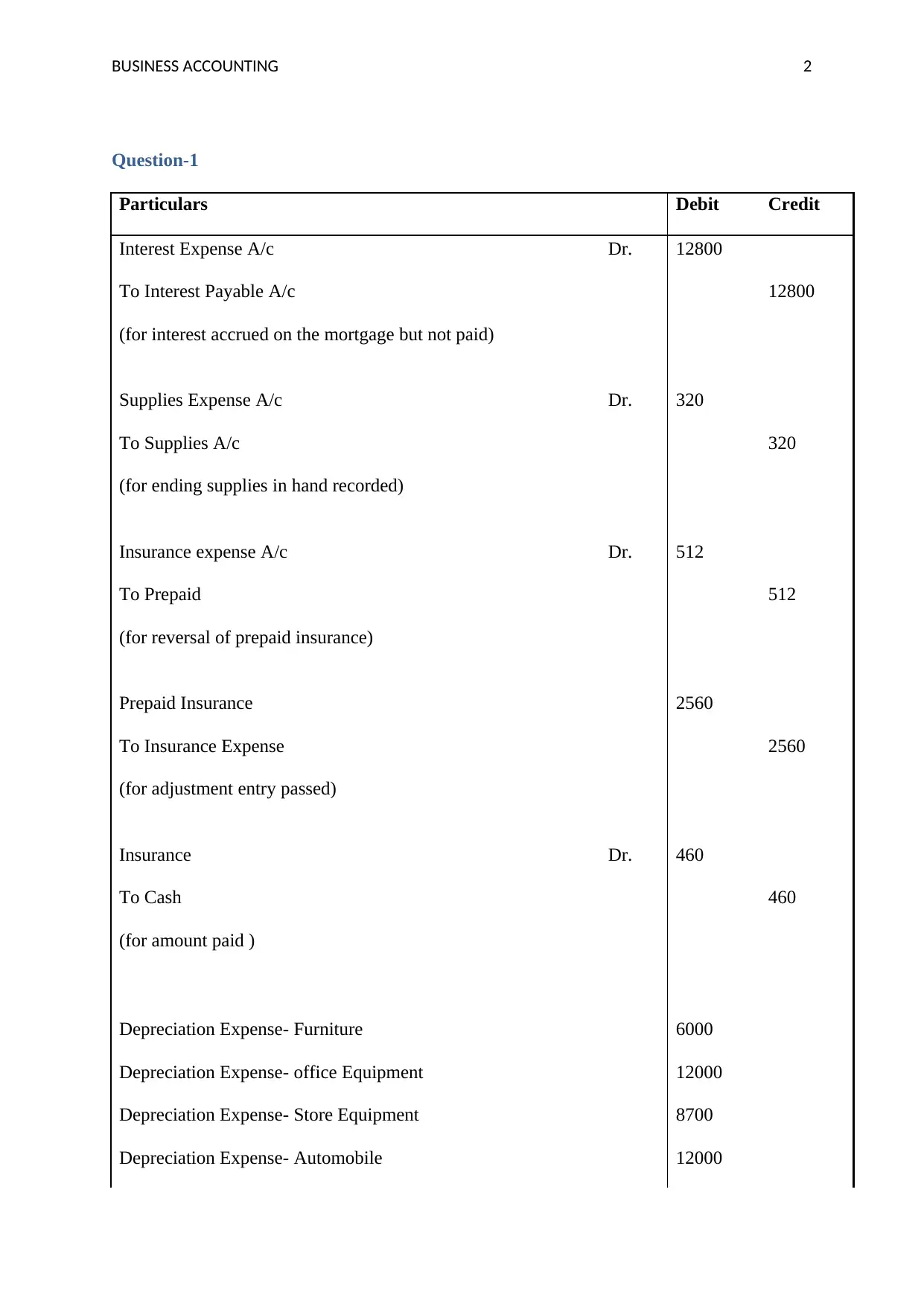

Question-1

Particulars Debit Credit

Interest Expense A/c Dr. 12800

To Interest Payable A/c 12800

(for interest accrued on the mortgage but not paid)

Supplies Expense A/c Dr. 320

To Supplies A/c 320

(for ending supplies in hand recorded)

Insurance expense A/c Dr. 512

To Prepaid 512

(for reversal of prepaid insurance)

Prepaid Insurance 2560

To Insurance Expense 2560

(for adjustment entry passed)

Insurance Dr. 460

To Cash 460

(for amount paid )

Depreciation Expense- Furniture 6000

Depreciation Expense- office Equipment 12000

Depreciation Expense- Store Equipment 8700

Depreciation Expense- Automobile 12000

Question-1

Particulars Debit Credit

Interest Expense A/c Dr. 12800

To Interest Payable A/c 12800

(for interest accrued on the mortgage but not paid)

Supplies Expense A/c Dr. 320

To Supplies A/c 320

(for ending supplies in hand recorded)

Insurance expense A/c Dr. 512

To Prepaid 512

(for reversal of prepaid insurance)

Prepaid Insurance 2560

To Insurance Expense 2560

(for adjustment entry passed)

Insurance Dr. 460

To Cash 460

(for amount paid )

Depreciation Expense- Furniture 6000

Depreciation Expense- office Equipment 12000

Depreciation Expense- Store Equipment 8700

Depreciation Expense- Automobile 12000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BUSINESS ACCOUNTING 3

To Accumulated Depreciation 38700

(for depreciation adjusted )

Cash A/c Dr. 8000

To unearned Revenue 8000

Unearned Revenue Dr. 8000

To Revenue 8000

Question-2

Paul services Trial Balance As At 30 June 2016

Accoun

t No Account Name Debit

Credi

t Adjustments

Final

Trial

Debit

Credi

t Debit Credit

101 Cash at Bank

27560.

00 8000 460

35100.

00

105 Accounts Receivable

9190.0

0

9190.0

0 0.00

115 Supplies

1280.0

0 320 960.00

120 Prepaid Insurance

2560.0

0 512

2048.0

0

135 Office Furniture

32000.

00

32000.

00 0.00

To Accumulated Depreciation 38700

(for depreciation adjusted )

Cash A/c Dr. 8000

To unearned Revenue 8000

Unearned Revenue Dr. 8000

To Revenue 8000

Question-2

Paul services Trial Balance As At 30 June 2016

Accoun

t No Account Name Debit

Credi

t Adjustments

Final

Trial

Debit

Credi

t Debit Credit

101 Cash at Bank

27560.

00 8000 460

35100.

00

105 Accounts Receivable

9190.0

0

9190.0

0 0.00

115 Supplies

1280.0

0 320 960.00

120 Prepaid Insurance

2560.0

0 512

2048.0

0

135 Office Furniture

32000.

00

32000.

00 0.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BUSINESS ACCOUNTING 4

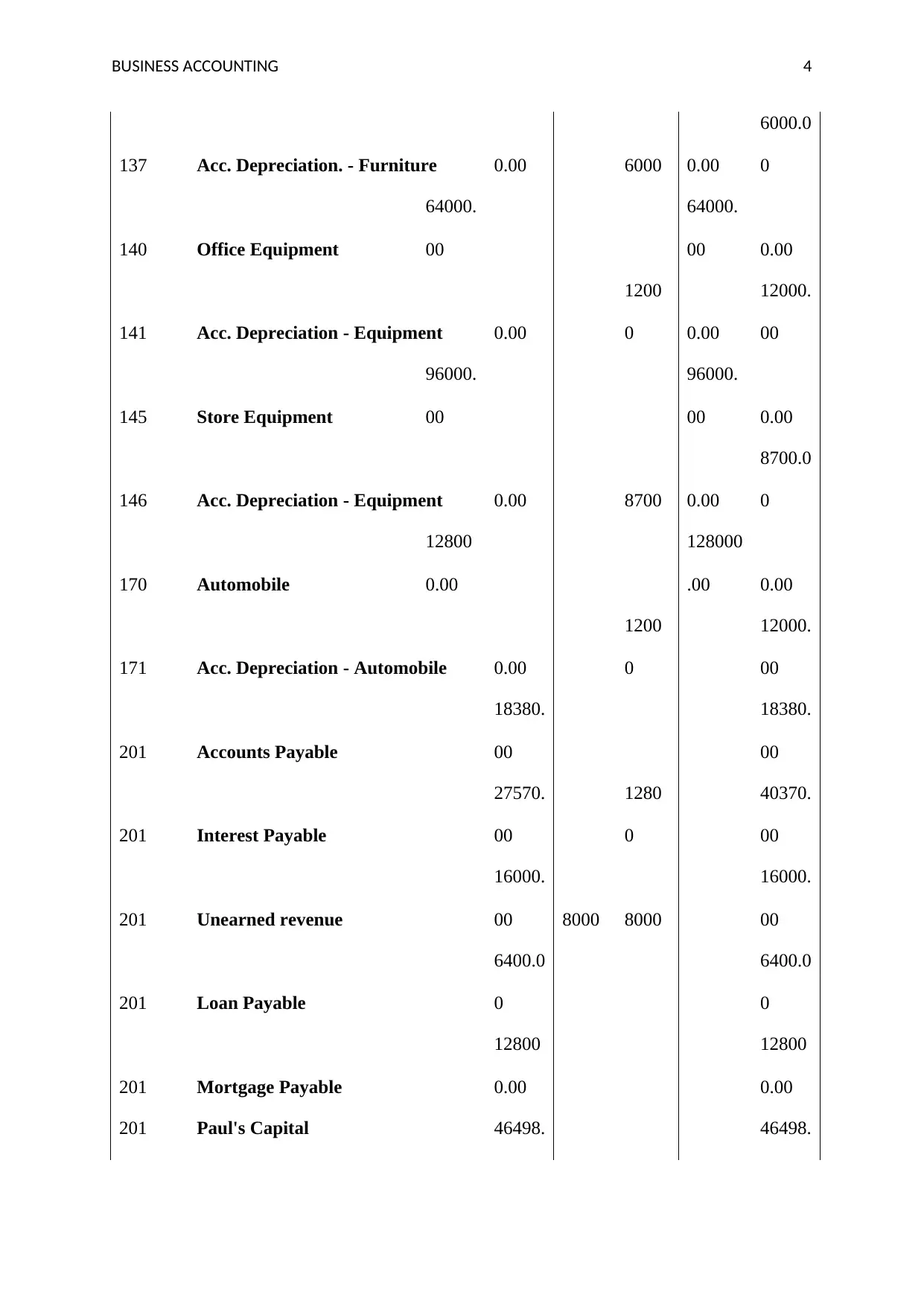

137 Acc. Depreciation. - Furniture 0.00 6000 0.00

6000.0

0

140 Office Equipment

64000.

00

64000.

00 0.00

141 Acc. Depreciation - Equipment 0.00

1200

0 0.00

12000.

00

145 Store Equipment

96000.

00

96000.

00 0.00

146 Acc. Depreciation - Equipment 0.00 8700 0.00

8700.0

0

170 Automobile

12800

0.00

128000

.00 0.00

171 Acc. Depreciation - Automobile 0.00

1200

0

12000.

00

201 Accounts Payable

18380.

00

18380.

00

201 Interest Payable

27570.

00

1280

0

40370.

00

201 Unearned revenue

16000.

00 8000 8000

16000.

00

201 Loan Payable

6400.0

0

6400.0

0

201 Mortgage Payable

12800

0.00

12800

0.00

201 Paul's Capital 46498. 46498.

137 Acc. Depreciation. - Furniture 0.00 6000 0.00

6000.0

0

140 Office Equipment

64000.

00

64000.

00 0.00

141 Acc. Depreciation - Equipment 0.00

1200

0 0.00

12000.

00

145 Store Equipment

96000.

00

96000.

00 0.00

146 Acc. Depreciation - Equipment 0.00 8700 0.00

8700.0

0

170 Automobile

12800

0.00

128000

.00 0.00

171 Acc. Depreciation - Automobile 0.00

1200

0

12000.

00

201 Accounts Payable

18380.

00

18380.

00

201 Interest Payable

27570.

00

1280

0

40370.

00

201 Unearned revenue

16000.

00 8000 8000

16000.

00

201 Loan Payable

6400.0

0

6400.0

0

201 Mortgage Payable

12800

0.00

12800

0.00

201 Paul's Capital 46498. 46498.

BUSINESS ACCOUNTING 5

00 00

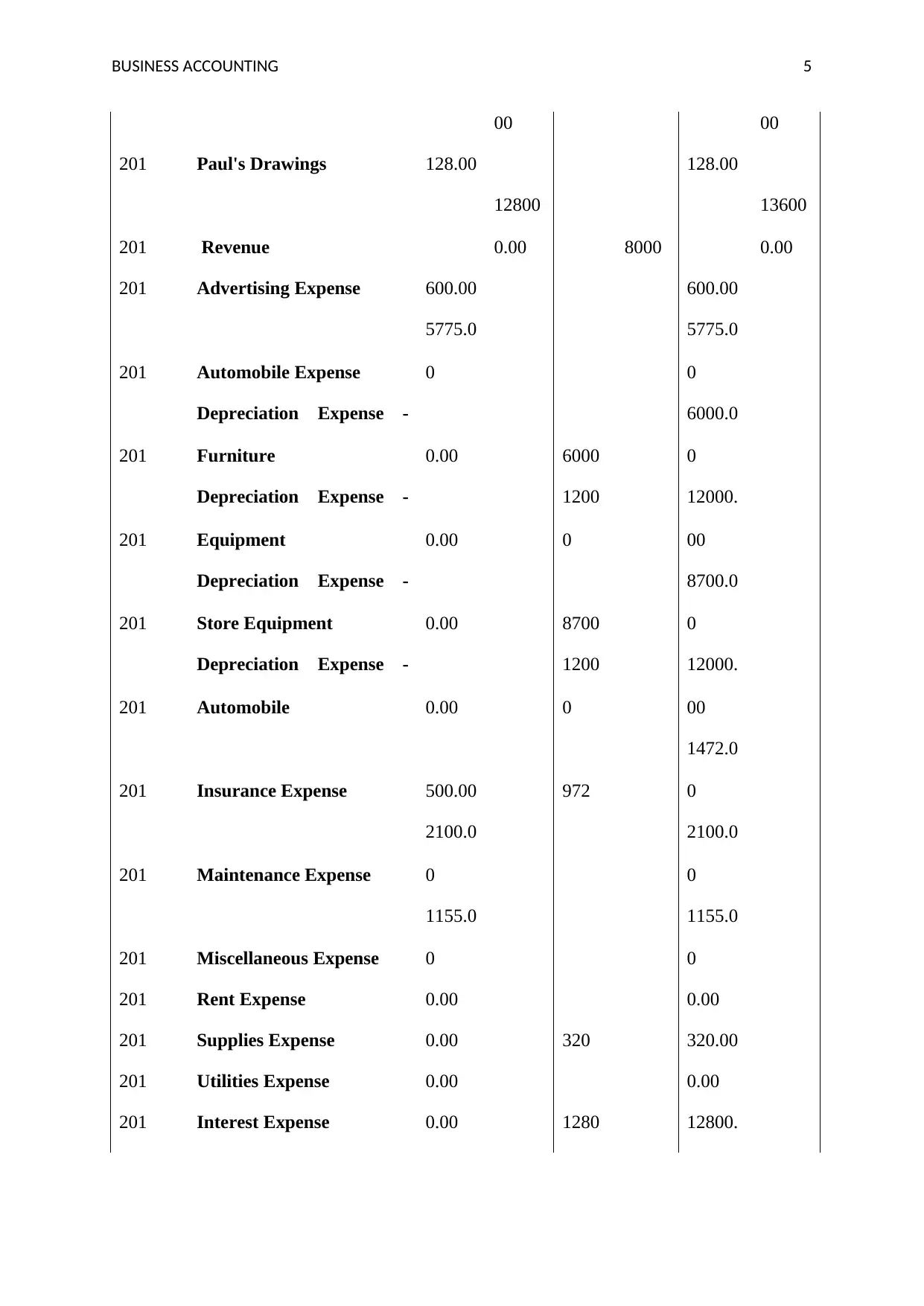

201 Paul's Drawings 128.00 128.00

201 Revenue

12800

0.00 8000

13600

0.00

201 Advertising Expense 600.00 600.00

201 Automobile Expense

5775.0

0

5775.0

0

201

Depreciation Expense -

Furniture 0.00 6000

6000.0

0

201

Depreciation Expense -

Equipment 0.00

1200

0

12000.

00

201

Depreciation Expense -

Store Equipment 0.00 8700

8700.0

0

201

Depreciation Expense -

Automobile 0.00

1200

0

12000.

00

201 Insurance Expense 500.00 972

1472.0

0

201 Maintenance Expense

2100.0

0

2100.0

0

201 Miscellaneous Expense

1155.0

0

1155.0

0

201 Rent Expense 0.00 0.00

201 Supplies Expense 0.00 320 320.00

201 Utilities Expense 0.00 0.00

201 Interest Expense 0.00 1280 12800.

00 00

201 Paul's Drawings 128.00 128.00

201 Revenue

12800

0.00 8000

13600

0.00

201 Advertising Expense 600.00 600.00

201 Automobile Expense

5775.0

0

5775.0

0

201

Depreciation Expense -

Furniture 0.00 6000

6000.0

0

201

Depreciation Expense -

Equipment 0.00

1200

0

12000.

00

201

Depreciation Expense -

Store Equipment 0.00 8700

8700.0

0

201

Depreciation Expense -

Automobile 0.00

1200

0

12000.

00

201 Insurance Expense 500.00 972

1472.0

0

201 Maintenance Expense

2100.0

0

2100.0

0

201 Miscellaneous Expense

1155.0

0

1155.0

0

201 Rent Expense 0.00 0.00

201 Supplies Expense 0.00 320 320.00

201 Utilities Expense 0.00 0.00

201 Interest Expense 0.00 1280 12800.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BUSINESS ACCOUNTING 6

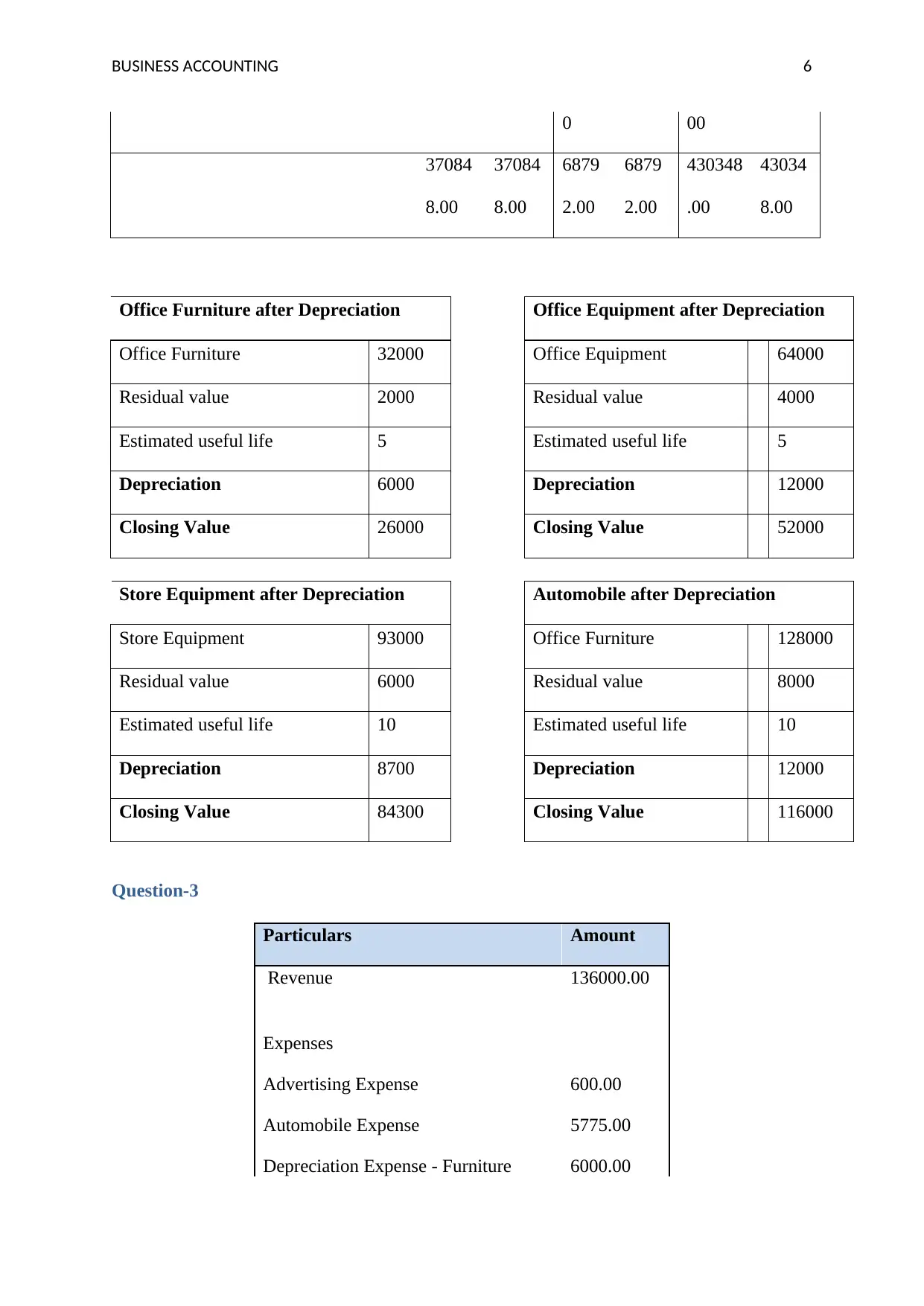

0 00

37084

8.00

37084

8.00

6879

2.00

6879

2.00

430348

.00

43034

8.00

Office Furniture after Depreciation Office Equipment after Depreciation

Office Furniture 32000 Office Equipment 64000

Residual value 2000 Residual value 4000

Estimated useful life 5 Estimated useful life 5

Depreciation 6000 Depreciation 12000

Closing Value 26000 Closing Value 52000

Store Equipment after Depreciation Automobile after Depreciation

Store Equipment 93000 Office Furniture 128000

Residual value 6000 Residual value 8000

Estimated useful life 10 Estimated useful life 10

Depreciation 8700 Depreciation 12000

Closing Value 84300 Closing Value 116000

Question-3

Particulars Amount

Revenue 136000.00

Expenses

Advertising Expense 600.00

Automobile Expense 5775.00

Depreciation Expense - Furniture 6000.00

0 00

37084

8.00

37084

8.00

6879

2.00

6879

2.00

430348

.00

43034

8.00

Office Furniture after Depreciation Office Equipment after Depreciation

Office Furniture 32000 Office Equipment 64000

Residual value 2000 Residual value 4000

Estimated useful life 5 Estimated useful life 5

Depreciation 6000 Depreciation 12000

Closing Value 26000 Closing Value 52000

Store Equipment after Depreciation Automobile after Depreciation

Store Equipment 93000 Office Furniture 128000

Residual value 6000 Residual value 8000

Estimated useful life 10 Estimated useful life 10

Depreciation 8700 Depreciation 12000

Closing Value 84300 Closing Value 116000

Question-3

Particulars Amount

Revenue 136000.00

Expenses

Advertising Expense 600.00

Automobile Expense 5775.00

Depreciation Expense - Furniture 6000.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BUSINESS ACCOUNTING 7

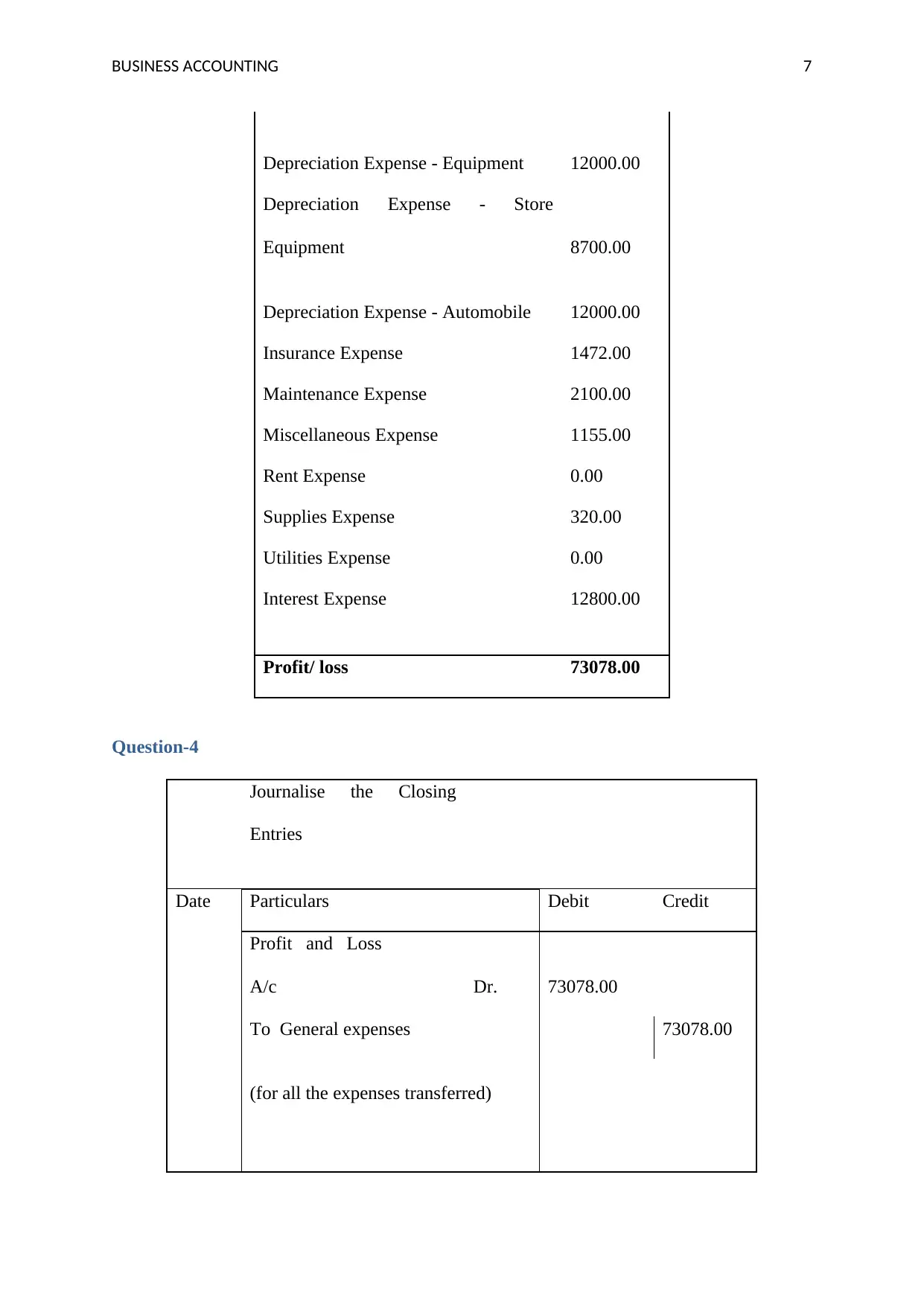

Depreciation Expense - Equipment 12000.00

Depreciation Expense - Store

Equipment 8700.00

Depreciation Expense - Automobile 12000.00

Insurance Expense 1472.00

Maintenance Expense 2100.00

Miscellaneous Expense 1155.00

Rent Expense 0.00

Supplies Expense 320.00

Utilities Expense 0.00

Interest Expense 12800.00

Profit/ loss 73078.00

Question-4

Journalise the Closing

Entries

Date Particulars Debit Credit

Profit and Loss

A/c Dr. 73078.00

To General expenses 73078.00

(for all the expenses transferred)

Depreciation Expense - Equipment 12000.00

Depreciation Expense - Store

Equipment 8700.00

Depreciation Expense - Automobile 12000.00

Insurance Expense 1472.00

Maintenance Expense 2100.00

Miscellaneous Expense 1155.00

Rent Expense 0.00

Supplies Expense 320.00

Utilities Expense 0.00

Interest Expense 12800.00

Profit/ loss 73078.00

Question-4

Journalise the Closing

Entries

Date Particulars Debit Credit

Profit and Loss

A/c Dr. 73078.00

To General expenses 73078.00

(for all the expenses transferred)

BUSINESS ACCOUNTING 8

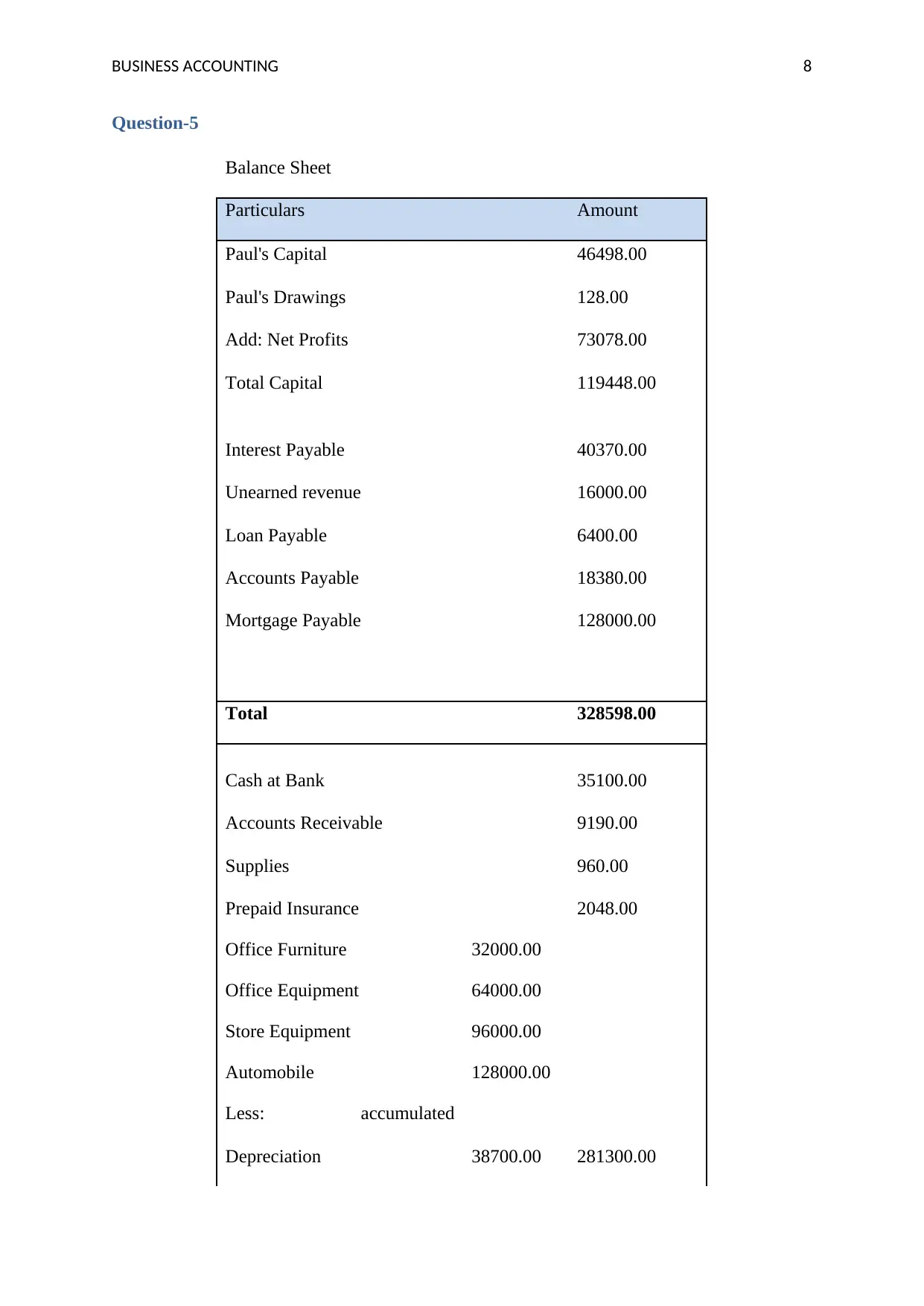

Question-5

Balance Sheet

Particulars Amount

Paul's Capital 46498.00

Paul's Drawings 128.00

Add: Net Profits 73078.00

Total Capital 119448.00

Interest Payable 40370.00

Unearned revenue 16000.00

Loan Payable 6400.00

Accounts Payable 18380.00

Mortgage Payable 128000.00

Total 328598.00

Cash at Bank 35100.00

Accounts Receivable 9190.00

Supplies 960.00

Prepaid Insurance 2048.00

Office Furniture 32000.00

Office Equipment 64000.00

Store Equipment 96000.00

Automobile 128000.00

Less: accumulated

Depreciation 38700.00 281300.00

Question-5

Balance Sheet

Particulars Amount

Paul's Capital 46498.00

Paul's Drawings 128.00

Add: Net Profits 73078.00

Total Capital 119448.00

Interest Payable 40370.00

Unearned revenue 16000.00

Loan Payable 6400.00

Accounts Payable 18380.00

Mortgage Payable 128000.00

Total 328598.00

Cash at Bank 35100.00

Accounts Receivable 9190.00

Supplies 960.00

Prepaid Insurance 2048.00

Office Furniture 32000.00

Office Equipment 64000.00

Store Equipment 96000.00

Automobile 128000.00

Less: accumulated

Depreciation 38700.00 281300.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BUSINESS ACCOUNTING 9

Total 328598.00

Question-6

Trial balance overview

A trial balance is an accounting book which helps in maintaining the organisations general

and ledger accounts. In this book of accounts all the debit balances are maintained in the

debit column of the book and the credit balances are maintained in the credit column of the

book. The balance of both the columns should be identical in nature. Such book of

accounting helps in finding errors in the financial statements of the organisation. Such a

statement is useful for the auditors in order to identify the errors of the company to audit the

accounts. Such errors are resolved by the auditors and an audit report is made on the basis of

such financial statements (Baxter and Davidson, 2014).

Under the traditional system the preparation of the trial balance was initially started by the

accountant. However under the current system of the accounting the accounting software has

been installed in the organisation in order to create more accuracy and the transparency

among the organisation. The manual system is a conventional system and it is time

consuming on the other hand the computerised system is the key component which follows

the double entry system and the system of accounting as well (Carey, Knowles and Towers-

Clark, 2017).

Purpose for Creation

The purpose for which the trial balance is created is similar for any kind of the organisation

and therefore the reasons are specifically presented below. The reason for creation of trail

balance is to identify all the errors that have been made while recording the transactions of

Total 328598.00

Question-6

Trial balance overview

A trial balance is an accounting book which helps in maintaining the organisations general

and ledger accounts. In this book of accounts all the debit balances are maintained in the

debit column of the book and the credit balances are maintained in the credit column of the

book. The balance of both the columns should be identical in nature. Such book of

accounting helps in finding errors in the financial statements of the organisation. Such a

statement is useful for the auditors in order to identify the errors of the company to audit the

accounts. Such errors are resolved by the auditors and an audit report is made on the basis of

such financial statements (Baxter and Davidson, 2014).

Under the traditional system the preparation of the trial balance was initially started by the

accountant. However under the current system of the accounting the accounting software has

been installed in the organisation in order to create more accuracy and the transparency

among the organisation. The manual system is a conventional system and it is time

consuming on the other hand the computerised system is the key component which follows

the double entry system and the system of accounting as well (Carey, Knowles and Towers-

Clark, 2017).

Purpose for Creation

The purpose for which the trial balance is created is similar for any kind of the organisation

and therefore the reasons are specifically presented below. The reason for creation of trail

balance is to identify all the errors that have been made while recording the transactions of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BUSINESS ACCOUNTING 10

the organisation. The purpose for the creation of trail balance is proved when all the credit

balances of the statement matches with all the debit balances of the statement. Such error

helps in rectification of entries and helps in preparing the profit and loss statement of the

organisation. Such a statement is prepared by the book keeper of the accounts who maintains

the daily record of transactions in the books of accounts (Kuter, Gurskaya, Andreenkova and

Musaelyan, 2017).

The Trial Balance helps in identifying all the errors which are in the form of omission, error

of commission, error in original journal entry, error of principle, compensating errors and the

error of reversal. Such errors help in preparation of financial statements. The purpose of

creation of trial balance is to help the organisation in reconciliation of the balances. The trail

balance also ensures that every entry is recorded in the financial statements. In case of any

error the trail balance helps in rectifying those entries (Ellerman, 2014).

Adjusting entries

When a transaction starts in one accounting period and ends in the different accounting

period than the adjusting entry is required definitely. In simpler terms the adjusting entry can

also be known as the reporting entries that are used to rectify and reconcile the mistakes

attempted in the past years. The adjusting entry is also termed as the balance day adjustment.

The accounts that are involved with the adjusting entries are the income statement and the

balance sheet and this type of entry is typically relatable to the accrued expense, accrued

revenue, prepaid expenses and unearned revenue (Fanning and Grant, 2017). The entries are

also passed keeping in mind the matching principle concept in order to match the revenue and

the expenses and these kind of the adjustments are also carried forward to the account ledgers

and the worksheet of the accounting in the next accounting cycle step. The common

characteristics of an adjusting entry are that it will involve the incomes and expenses and the

the organisation. The purpose for the creation of trail balance is proved when all the credit

balances of the statement matches with all the debit balances of the statement. Such error

helps in rectification of entries and helps in preparing the profit and loss statement of the

organisation. Such a statement is prepared by the book keeper of the accounts who maintains

the daily record of transactions in the books of accounts (Kuter, Gurskaya, Andreenkova and

Musaelyan, 2017).

The Trial Balance helps in identifying all the errors which are in the form of omission, error

of commission, error in original journal entry, error of principle, compensating errors and the

error of reversal. Such errors help in preparation of financial statements. The purpose of

creation of trial balance is to help the organisation in reconciliation of the balances. The trail

balance also ensures that every entry is recorded in the financial statements. In case of any

error the trail balance helps in rectifying those entries (Ellerman, 2014).

Adjusting entries

When a transaction starts in one accounting period and ends in the different accounting

period than the adjusting entry is required definitely. In simpler terms the adjusting entry can

also be known as the reporting entries that are used to rectify and reconcile the mistakes

attempted in the past years. The adjusting entry is also termed as the balance day adjustment.

The accounts that are involved with the adjusting entries are the income statement and the

balance sheet and this type of entry is typically relatable to the accrued expense, accrued

revenue, prepaid expenses and unearned revenue (Fanning and Grant, 2017). The entries are

also passed keeping in mind the matching principle concept in order to match the revenue and

the expenses and these kind of the adjustments are also carried forward to the account ledgers

and the worksheet of the accounting in the next accounting cycle step. The common

characteristics of an adjusting entry are that it will involve the incomes and expenses and the

BUSINESS ACCOUNTING 11

assets and the liabilities. In summary the adjusting journal entries are basically of the three

categories namely the accruals, deferrals and estimates (Shanklin and Ehlen, 2017).

Purpose of writing an adjusted trial balance

Normally the trial balance reflects all the accounts that are recorded in the ledgers and from

the ledgers the trial balance is prepared subject to certain changes. Once the financial

statements are prepared they are prepared using the help from the trial balance. That’s when

the adjusted trial balance came into existence. The adjusted trial balance is made with the

adjustments given apart from the trial balance. The process if the adjusted trial balance is

identical just likes the normal one. The simple reason is to match the revenues with the

expenses and the monitor the performances of the company which will be beneficial from the

point of view of the shareholders (Kramer, 2017).

The cycle of the financial statements is totally dependent on the books of accounts and the

financial statements so that the shareholders can take the decisions of the company wisely

(Harris and Dilling, 2017). The trial balance is never a part of the financial statement rather it

is a document to be used internally which has basically two purposes.

To verify that the balance of the debit side and the credit side is equal to each other and to for

the purpose of the construction of the ultimate report that is circulated among the

shareholders and the investors (Gurskaya, Kuter and Andreenkova, 2017). The second

implication of the adjusted trial balance has fallen into the vain since the computerised

accounting system has been in motion for the production of the financial statements. The trial

balance is set up before the adjusting entries and after the adjusting entries the trial balance is

the adjusted and the complete trial balance. The balances of the trial changes immediately

once the entries are adjusted. In order to be sure of the data relevancy the Trial balance is to

be 100% correct (Fang and Slavin, 2018).

assets and the liabilities. In summary the adjusting journal entries are basically of the three

categories namely the accruals, deferrals and estimates (Shanklin and Ehlen, 2017).

Purpose of writing an adjusted trial balance

Normally the trial balance reflects all the accounts that are recorded in the ledgers and from

the ledgers the trial balance is prepared subject to certain changes. Once the financial

statements are prepared they are prepared using the help from the trial balance. That’s when

the adjusted trial balance came into existence. The adjusted trial balance is made with the

adjustments given apart from the trial balance. The process if the adjusted trial balance is

identical just likes the normal one. The simple reason is to match the revenues with the

expenses and the monitor the performances of the company which will be beneficial from the

point of view of the shareholders (Kramer, 2017).

The cycle of the financial statements is totally dependent on the books of accounts and the

financial statements so that the shareholders can take the decisions of the company wisely

(Harris and Dilling, 2017). The trial balance is never a part of the financial statement rather it

is a document to be used internally which has basically two purposes.

To verify that the balance of the debit side and the credit side is equal to each other and to for

the purpose of the construction of the ultimate report that is circulated among the

shareholders and the investors (Gurskaya, Kuter and Andreenkova, 2017). The second

implication of the adjusted trial balance has fallen into the vain since the computerised

accounting system has been in motion for the production of the financial statements. The trial

balance is set up before the adjusting entries and after the adjusting entries the trial balance is

the adjusted and the complete trial balance. The balances of the trial changes immediately

once the entries are adjusted. In order to be sure of the data relevancy the Trial balance is to

be 100% correct (Fang and Slavin, 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.