BACT105 Business Accounting: Journal Entries, Trial Balance Report

VerifiedAdded on 2023/04/21

|17

|3246

|336

Report

AI Summary

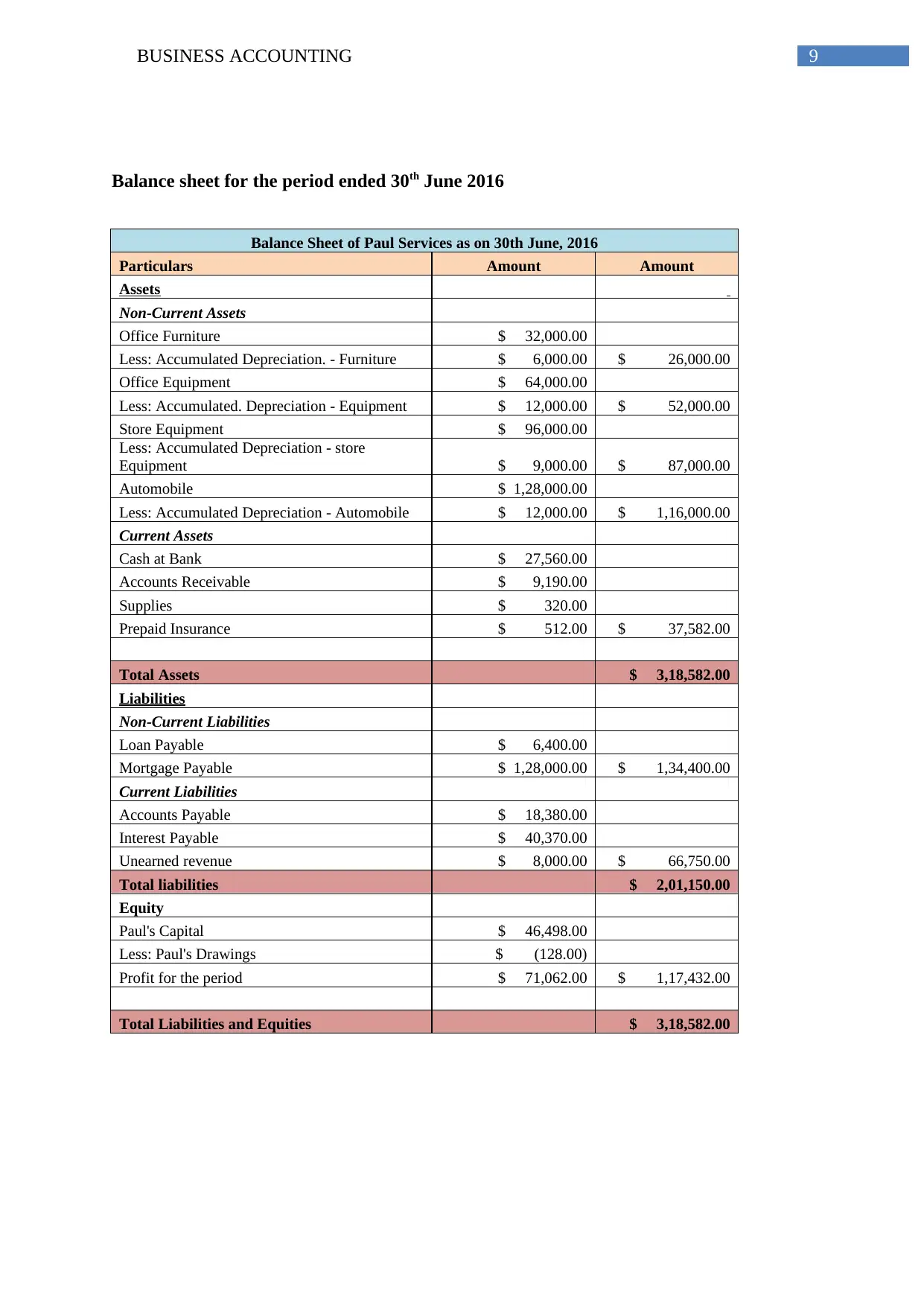

This business accounting report focuses on the significance of journal entries and trial balance preparation in creating accurate financial statements. It presents journal entries for given adjusting entries and prepares an income statement and balance sheet from the adjusted trial balance. The report explains the purpose of the trial balance in representing balances from the general ledger, ensuring that total debit amounts equal total credit amounts. Adjusting journal entries are used to correct errors before financial statements are finalized. The report details the steps involved, including journal entries for adjustments and closing, worksheet completion, and changes in equity. It further discusses the purposes of creating a trial balance, recording adjusting journal entries, and preparing an adjusted trial balance, highlighting the differences between closing and adjusting entries. This resource, available on Desklib, helps students understand these concepts and provides solved assignments for further learning.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.