Financial Analysis, Valuation and Capital Structure of BAE Systems

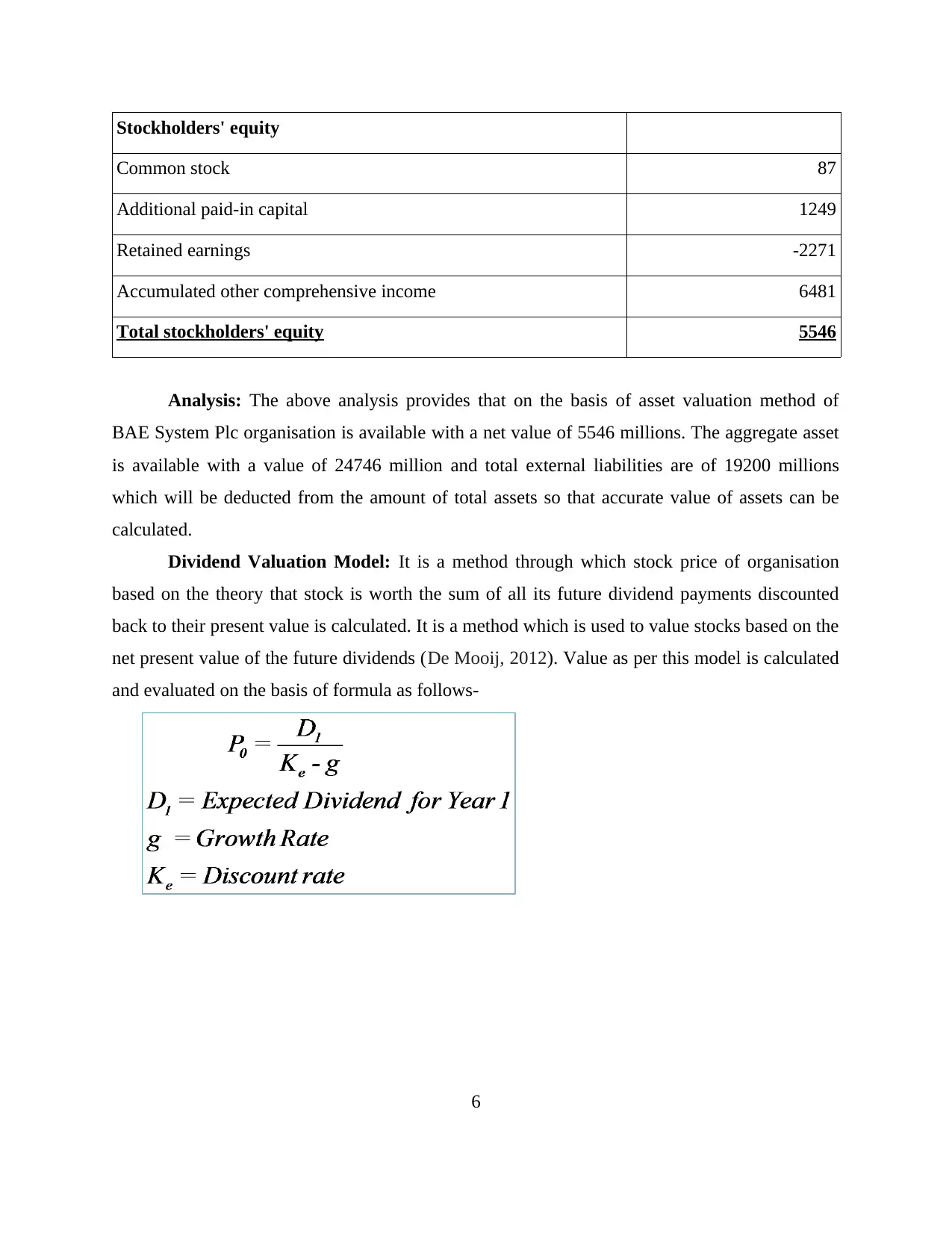

VerifiedAdded on 2023/01/16

|14

|2430

|52

Report

AI Summary

This report presents a comprehensive financial analysis of BAE Systems Plc. It begins with an introduction to financial analysis and its importance, followed by a detailed examination of various financial ratios, including net profit margin, gross profit ratio, current ratio, debt-equity ratio, and return on equity, comparing BAE Systems to General Dynamics Corp. The report then explores the limitations of ratio analysis. The core of the report focuses on company valuation, employing asset-based valuation, dividend valuation model, and price-to-earnings ratio methods. The report also delves into capital structure, calculating the cost of debt and equity, and discussing the weighted average cost of capital (WACC) along with the difficulties associated with its calculation. The analysis provides insights into BAE Systems' financial performance and valuation, offering a comprehensive overview of its financial health.

Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

2.1 ...............................................................................................................................................1

(a)Financial Analysis..................................................................................................................1

(b) Limitations on the usefulness of ratio analysis......................................................................3

2.2 Company Valuation..............................................................................................................3

2.3 Capital Structure....................................................................................................................8

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

2.1 ...............................................................................................................................................1

(a)Financial Analysis..................................................................................................................1

(b) Limitations on the usefulness of ratio analysis......................................................................3

2.2 Company Valuation..............................................................................................................3

2.3 Capital Structure....................................................................................................................8

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

Finance is termed as one of the most important element for each business organisation in

order to perform all the required activities so that operations can be conducted in well defined

manner. Financial performance of business organisation is an important tool used to access

success of business in measurable terms. Financial statements are prepared so that financial

performance can be measured and assessment for financial needs can be identified (Knorr Cetina

and Preda, 2012). This project report is based on financial analysis of BAE Systems Plc which is

listed in London stock exchange. The project report includes financial analysis, company

valuation and analysis of capital structure of business organisation so that financial calculations

can be made in appropriate manner.

MAIN BODY

2.1

(a)Financial Analysis

Financial Analysis is a process through which businesses, projects and budgets are

evaluated in order to determine performance as per set targets. In the process of Financial

Analysis number of financial documents needs to be prepared so that performance can be

analysed appropriately. Ratio analysis is one of the tool which helps in financial analysis as it is

purely based on formulas and leads to generation of best results for business organisations.

Comparison for financial performance is made on the basis of industrial standards so that actual

performance can be analysed and most productive results can be generated (Ayub, 2013). In

order to access financial performance of BAE Systems Plc and one of its competitor ratio

analysis needs to be performed which is as follows-

Net-profit Margin:

Year – 2018 BAE Systems General Dynamics Corp

Net Profit Margin ( % ) 5.94% 9.24%

This ratio represents the net profitability situation of business by showing proportion of

net profit and turnover. GD corporation and BAE system has net profit ratio of 5.94% and 9.24%

1

Finance is termed as one of the most important element for each business organisation in

order to perform all the required activities so that operations can be conducted in well defined

manner. Financial performance of business organisation is an important tool used to access

success of business in measurable terms. Financial statements are prepared so that financial

performance can be measured and assessment for financial needs can be identified (Knorr Cetina

and Preda, 2012). This project report is based on financial analysis of BAE Systems Plc which is

listed in London stock exchange. The project report includes financial analysis, company

valuation and analysis of capital structure of business organisation so that financial calculations

can be made in appropriate manner.

MAIN BODY

2.1

(a)Financial Analysis

Financial Analysis is a process through which businesses, projects and budgets are

evaluated in order to determine performance as per set targets. In the process of Financial

Analysis number of financial documents needs to be prepared so that performance can be

analysed appropriately. Ratio analysis is one of the tool which helps in financial analysis as it is

purely based on formulas and leads to generation of best results for business organisations.

Comparison for financial performance is made on the basis of industrial standards so that actual

performance can be analysed and most productive results can be generated (Ayub, 2013). In

order to access financial performance of BAE Systems Plc and one of its competitor ratio

analysis needs to be performed which is as follows-

Net-profit Margin:

Year – 2018 BAE Systems General Dynamics Corp

Net Profit Margin ( % ) 5.94% 9.24%

This ratio represents the net profitability situation of business by showing proportion of

net profit and turnover. GD corporation and BAE system has net profit ratio of 5.94% and 9.24%

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

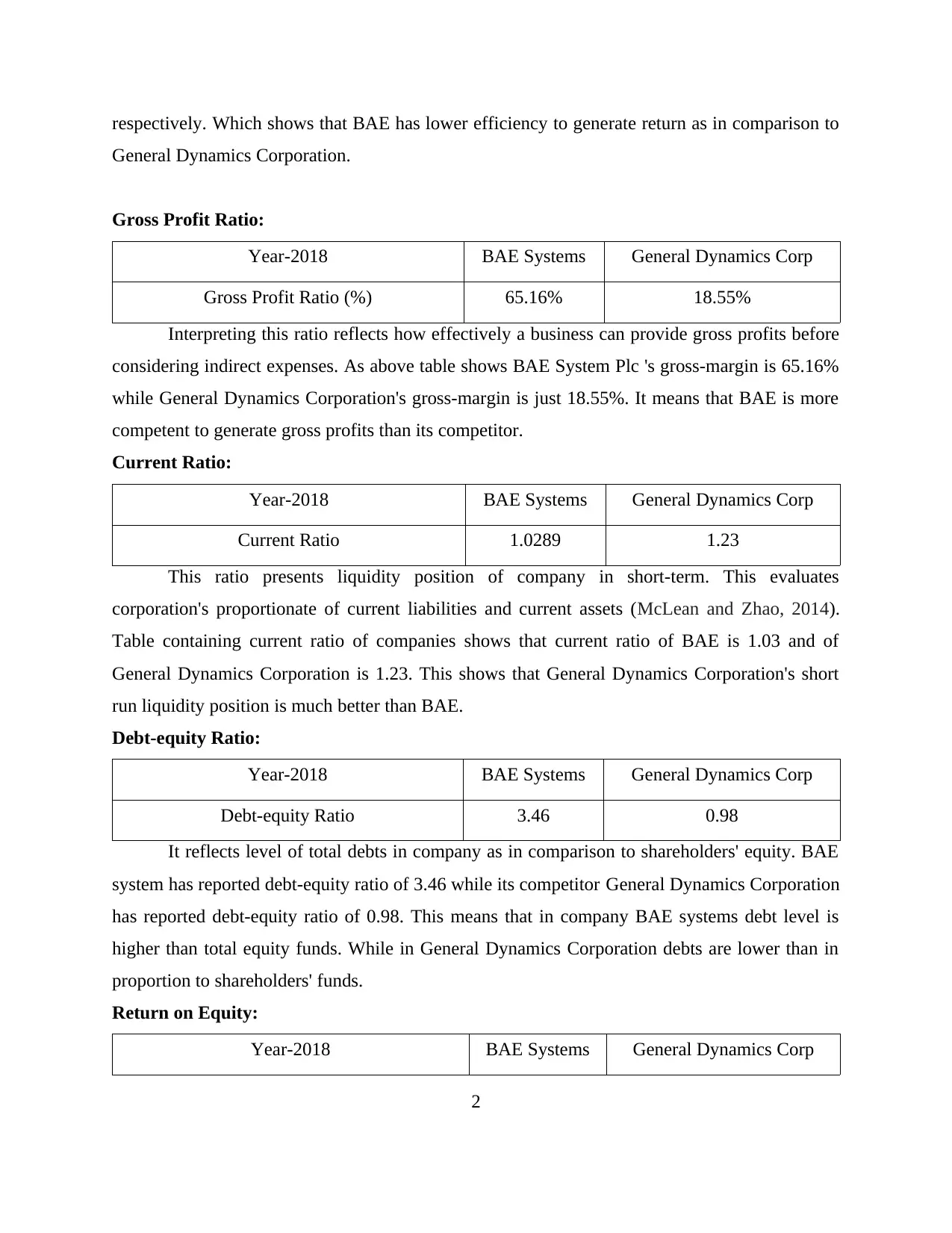

respectively. Which shows that BAE has lower efficiency to generate return as in comparison to

General Dynamics Corporation.

Gross Profit Ratio:

Year-2018 BAE Systems General Dynamics Corp

Gross Profit Ratio (%) 65.16% 18.55%

Interpreting this ratio reflects how effectively a business can provide gross profits before

considering indirect expenses. As above table shows BAE System Plc 's gross-margin is 65.16%

while General Dynamics Corporation's gross-margin is just 18.55%. It means that BAE is more

competent to generate gross profits than its competitor.

Current Ratio:

Year-2018 BAE Systems General Dynamics Corp

Current Ratio 1.0289 1.23

This ratio presents liquidity position of company in short-term. This evaluates

corporation's proportionate of current liabilities and current assets (McLean and Zhao, 2014).

Table containing current ratio of companies shows that current ratio of BAE is 1.03 and of

General Dynamics Corporation is 1.23. This shows that General Dynamics Corporation's short

run liquidity position is much better than BAE.

Debt-equity Ratio:

Year-2018 BAE Systems General Dynamics Corp

Debt-equity Ratio 3.46 0.98

It reflects level of total debts in company as in comparison to shareholders' equity. BAE

system has reported debt-equity ratio of 3.46 while its competitor General Dynamics Corporation

has reported debt-equity ratio of 0.98. This means that in company BAE systems debt level is

higher than total equity funds. While in General Dynamics Corporation debts are lower than in

proportion to shareholders' funds.

Return on Equity:

Year-2018 BAE Systems General Dynamics Corp

2

General Dynamics Corporation.

Gross Profit Ratio:

Year-2018 BAE Systems General Dynamics Corp

Gross Profit Ratio (%) 65.16% 18.55%

Interpreting this ratio reflects how effectively a business can provide gross profits before

considering indirect expenses. As above table shows BAE System Plc 's gross-margin is 65.16%

while General Dynamics Corporation's gross-margin is just 18.55%. It means that BAE is more

competent to generate gross profits than its competitor.

Current Ratio:

Year-2018 BAE Systems General Dynamics Corp

Current Ratio 1.0289 1.23

This ratio presents liquidity position of company in short-term. This evaluates

corporation's proportionate of current liabilities and current assets (McLean and Zhao, 2014).

Table containing current ratio of companies shows that current ratio of BAE is 1.03 and of

General Dynamics Corporation is 1.23. This shows that General Dynamics Corporation's short

run liquidity position is much better than BAE.

Debt-equity Ratio:

Year-2018 BAE Systems General Dynamics Corp

Debt-equity Ratio 3.46 0.98

It reflects level of total debts in company as in comparison to shareholders' equity. BAE

system has reported debt-equity ratio of 3.46 while its competitor General Dynamics Corporation

has reported debt-equity ratio of 0.98. This means that in company BAE systems debt level is

higher than total equity funds. While in General Dynamics Corporation debts are lower than in

proportion to shareholders' funds.

Return on Equity:

Year-2018 BAE Systems General Dynamics Corp

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

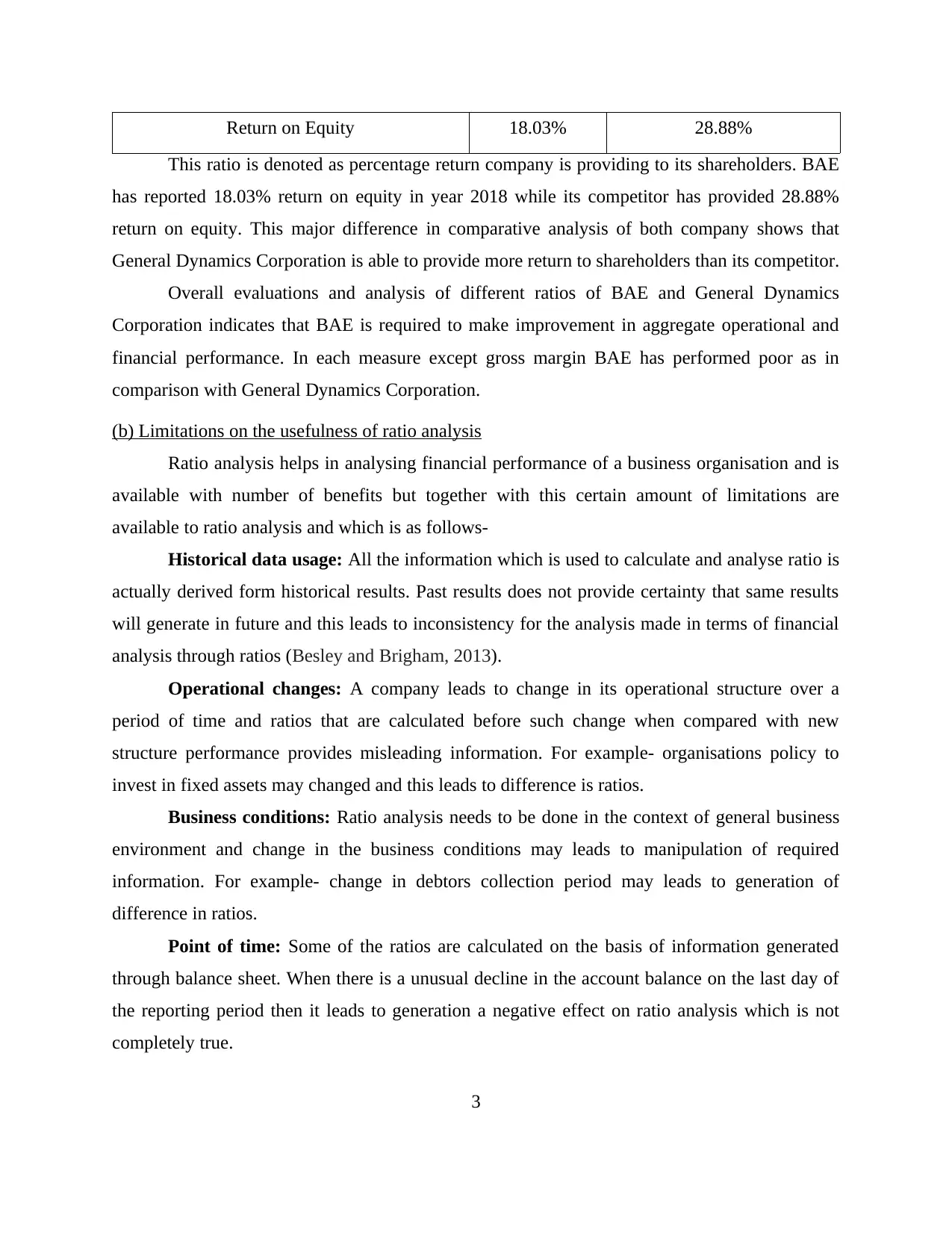

Return on Equity 18.03% 28.88%

This ratio is denoted as percentage return company is providing to its shareholders. BAE

has reported 18.03% return on equity in year 2018 while its competitor has provided 28.88%

return on equity. This major difference in comparative analysis of both company shows that

General Dynamics Corporation is able to provide more return to shareholders than its competitor.

Overall evaluations and analysis of different ratios of BAE and General Dynamics

Corporation indicates that BAE is required to make improvement in aggregate operational and

financial performance. In each measure except gross margin BAE has performed poor as in

comparison with General Dynamics Corporation.

(b) Limitations on the usefulness of ratio analysis

Ratio analysis helps in analysing financial performance of a business organisation and is

available with number of benefits but together with this certain amount of limitations are

available to ratio analysis and which is as follows-

Historical data usage: All the information which is used to calculate and analyse ratio is

actually derived form historical results. Past results does not provide certainty that same results

will generate in future and this leads to inconsistency for the analysis made in terms of financial

analysis through ratios (Besley and Brigham, 2013).

Operational changes: A company leads to change in its operational structure over a

period of time and ratios that are calculated before such change when compared with new

structure performance provides misleading information. For example- organisations policy to

invest in fixed assets may changed and this leads to difference is ratios.

Business conditions: Ratio analysis needs to be done in the context of general business

environment and change in the business conditions may leads to manipulation of required

information. For example- change in debtors collection period may leads to generation of

difference in ratios.

Point of time: Some of the ratios are calculated on the basis of information generated

through balance sheet. When there is a unusual decline in the account balance on the last day of

the reporting period then it leads to generation a negative effect on ratio analysis which is not

completely true.

3

This ratio is denoted as percentage return company is providing to its shareholders. BAE

has reported 18.03% return on equity in year 2018 while its competitor has provided 28.88%

return on equity. This major difference in comparative analysis of both company shows that

General Dynamics Corporation is able to provide more return to shareholders than its competitor.

Overall evaluations and analysis of different ratios of BAE and General Dynamics

Corporation indicates that BAE is required to make improvement in aggregate operational and

financial performance. In each measure except gross margin BAE has performed poor as in

comparison with General Dynamics Corporation.

(b) Limitations on the usefulness of ratio analysis

Ratio analysis helps in analysing financial performance of a business organisation and is

available with number of benefits but together with this certain amount of limitations are

available to ratio analysis and which is as follows-

Historical data usage: All the information which is used to calculate and analyse ratio is

actually derived form historical results. Past results does not provide certainty that same results

will generate in future and this leads to inconsistency for the analysis made in terms of financial

analysis through ratios (Besley and Brigham, 2013).

Operational changes: A company leads to change in its operational structure over a

period of time and ratios that are calculated before such change when compared with new

structure performance provides misleading information. For example- organisations policy to

invest in fixed assets may changed and this leads to difference is ratios.

Business conditions: Ratio analysis needs to be done in the context of general business

environment and change in the business conditions may leads to manipulation of required

information. For example- change in debtors collection period may leads to generation of

difference in ratios.

Point of time: Some of the ratios are calculated on the basis of information generated

through balance sheet. When there is a unusual decline in the account balance on the last day of

the reporting period then it leads to generation a negative effect on ratio analysis which is not

completely true.

3

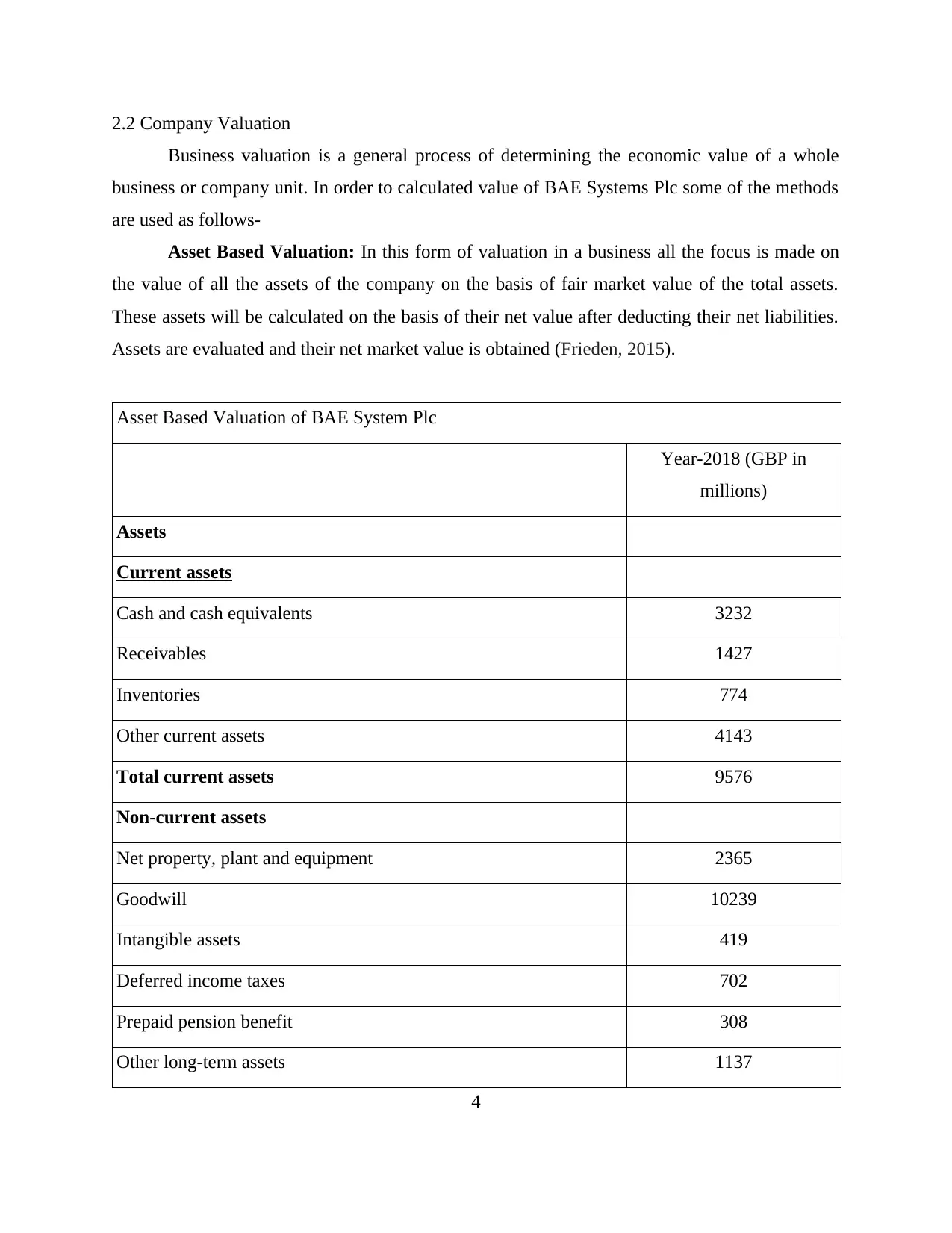

2.2 Company Valuation

Business valuation is a general process of determining the economic value of a whole

business or company unit. In order to calculated value of BAE Systems Plc some of the methods

are used as follows-

Asset Based Valuation: In this form of valuation in a business all the focus is made on

the value of all the assets of the company on the basis of fair market value of the total assets.

These assets will be calculated on the basis of their net value after deducting their net liabilities.

Assets are evaluated and their net market value is obtained (Frieden, 2015).

Asset Based Valuation of BAE System Plc

Year-2018 (GBP in

millions)

Assets

Current assets

Cash and cash equivalents 3232

Receivables 1427

Inventories 774

Other current assets 4143

Total current assets 9576

Non-current assets

Net property, plant and equipment 2365

Goodwill 10239

Intangible assets 419

Deferred income taxes 702

Prepaid pension benefit 308

Other long-term assets 1137

4

Business valuation is a general process of determining the economic value of a whole

business or company unit. In order to calculated value of BAE Systems Plc some of the methods

are used as follows-

Asset Based Valuation: In this form of valuation in a business all the focus is made on

the value of all the assets of the company on the basis of fair market value of the total assets.

These assets will be calculated on the basis of their net value after deducting their net liabilities.

Assets are evaluated and their net market value is obtained (Frieden, 2015).

Asset Based Valuation of BAE System Plc

Year-2018 (GBP in

millions)

Assets

Current assets

Cash and cash equivalents 3232

Receivables 1427

Inventories 774

Other current assets 4143

Total current assets 9576

Non-current assets

Net property, plant and equipment 2365

Goodwill 10239

Intangible assets 419

Deferred income taxes 702

Prepaid pension benefit 308

Other long-term assets 1137

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

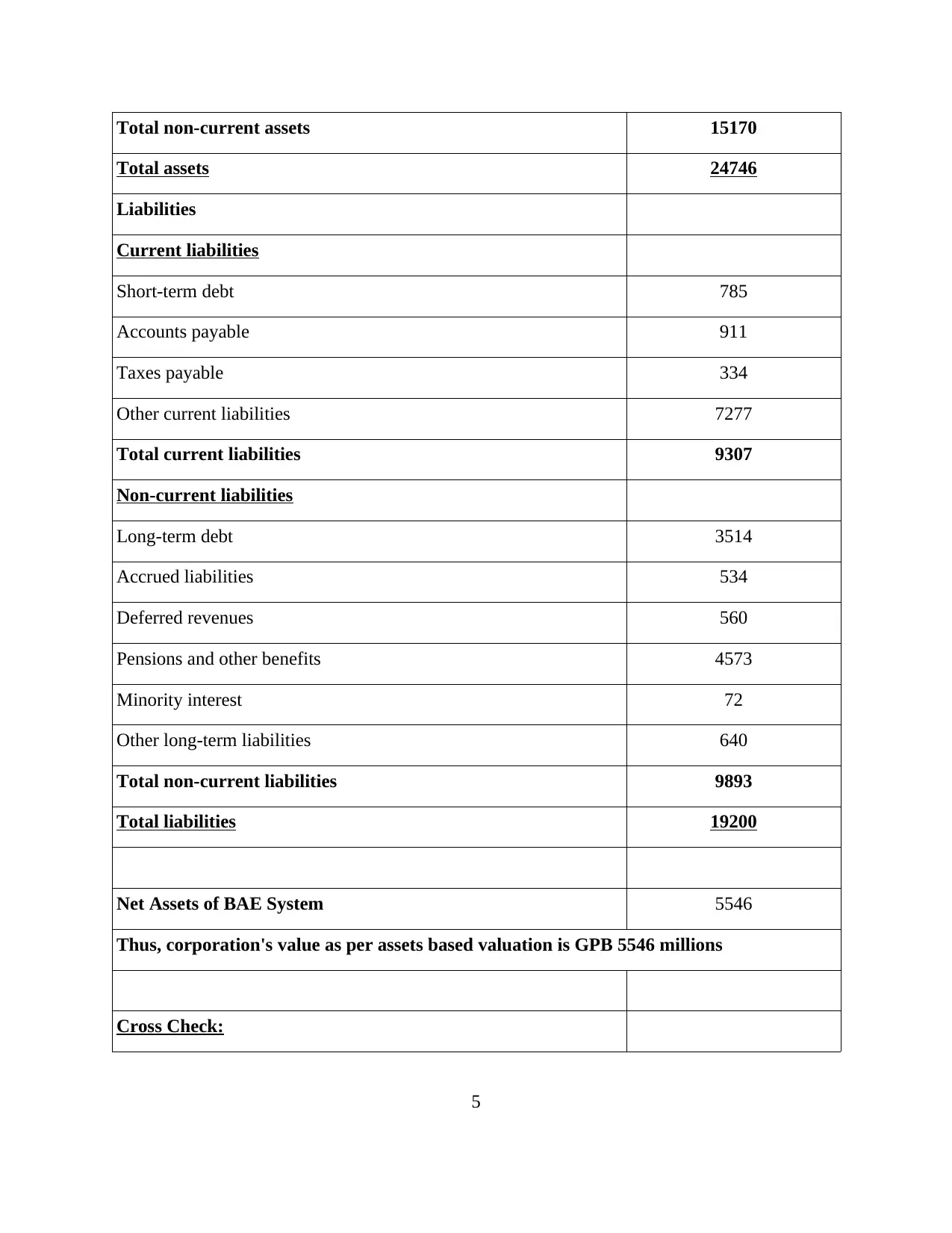

Total non-current assets 15170

Total assets 24746

Liabilities

Current liabilities

Short-term debt 785

Accounts payable 911

Taxes payable 334

Other current liabilities 7277

Total current liabilities 9307

Non-current liabilities

Long-term debt 3514

Accrued liabilities 534

Deferred revenues 560

Pensions and other benefits 4573

Minority interest 72

Other long-term liabilities 640

Total non-current liabilities 9893

Total liabilities 19200

Net Assets of BAE System 5546

Thus, corporation's value as per assets based valuation is GPB 5546 millions

Cross Check:

5

Total assets 24746

Liabilities

Current liabilities

Short-term debt 785

Accounts payable 911

Taxes payable 334

Other current liabilities 7277

Total current liabilities 9307

Non-current liabilities

Long-term debt 3514

Accrued liabilities 534

Deferred revenues 560

Pensions and other benefits 4573

Minority interest 72

Other long-term liabilities 640

Total non-current liabilities 9893

Total liabilities 19200

Net Assets of BAE System 5546

Thus, corporation's value as per assets based valuation is GPB 5546 millions

Cross Check:

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Stockholders' equity

Common stock 87

Additional paid-in capital 1249

Retained earnings -2271

Accumulated other comprehensive income 6481

Total stockholders' equity 5546

Analysis: The above analysis provides that on the basis of asset valuation method of

BAE System Plc organisation is available with a net value of 5546 millions. The aggregate asset

is available with a value of 24746 million and total external liabilities are of 19200 millions

which will be deducted from the amount of total assets so that accurate value of assets can be

calculated.

Dividend Valuation Model: It is a method through which stock price of organisation

based on the theory that stock is worth the sum of all its future dividend payments discounted

back to their present value is calculated. It is a method which is used to value stocks based on the

net present value of the future dividends (De Mooij, 2012). Value as per this model is calculated

and evaluated on the basis of formula as follows-

6

Common stock 87

Additional paid-in capital 1249

Retained earnings -2271

Accumulated other comprehensive income 6481

Total stockholders' equity 5546

Analysis: The above analysis provides that on the basis of asset valuation method of

BAE System Plc organisation is available with a net value of 5546 millions. The aggregate asset

is available with a value of 24746 million and total external liabilities are of 19200 millions

which will be deducted from the amount of total assets so that accurate value of assets can be

calculated.

Dividend Valuation Model: It is a method through which stock price of organisation

based on the theory that stock is worth the sum of all its future dividend payments discounted

back to their present value is calculated. It is a method which is used to value stocks based on the

net present value of the future dividends (De Mooij, 2012). Value as per this model is calculated

and evaluated on the basis of formula as follows-

6

Analysis: On the above method of calculation it has been analysed that value of stocks

possessed by BAE System Plc organisation is 24814.9071 millions. This specifies that amount of

stock is quite good and represents fair market conditions.

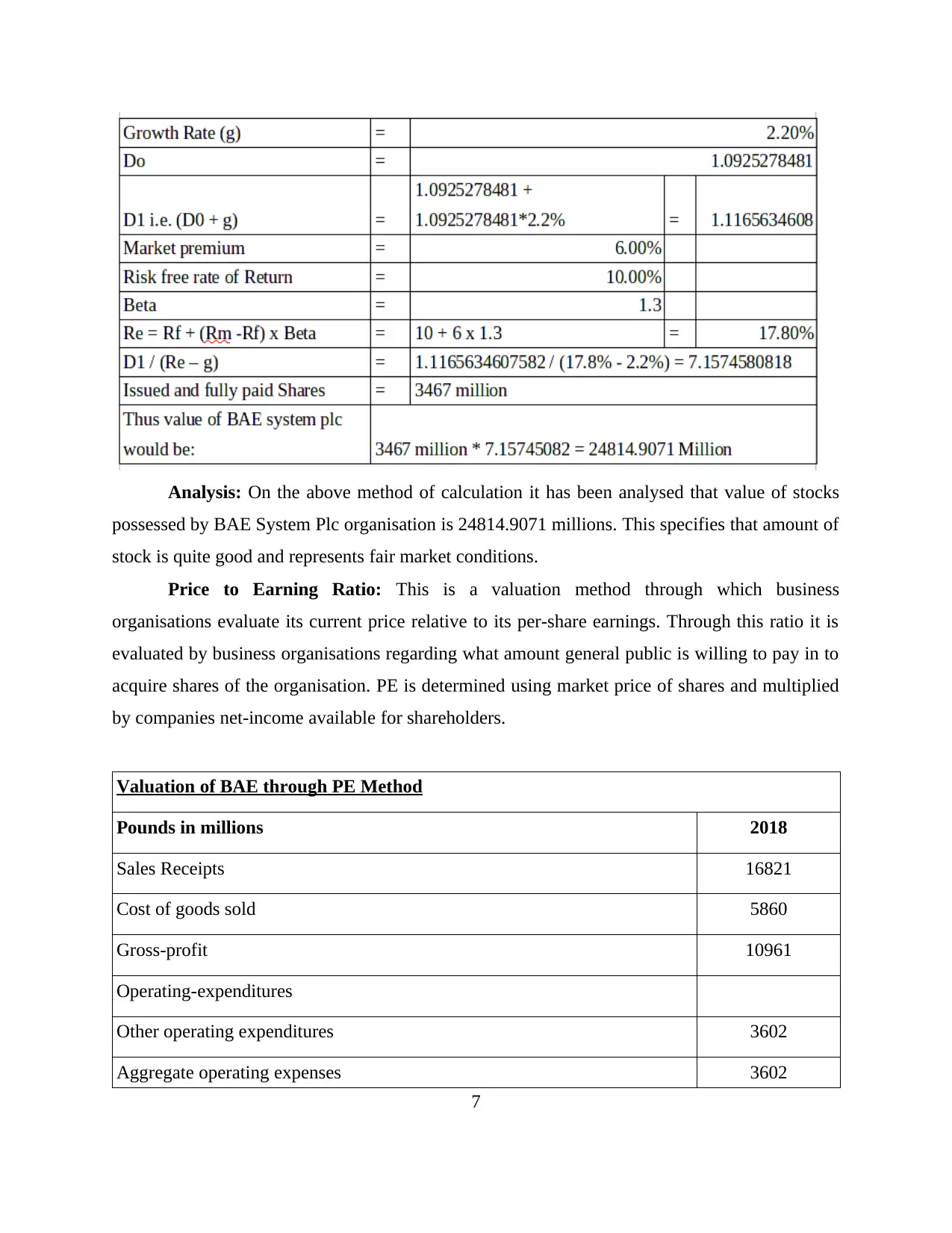

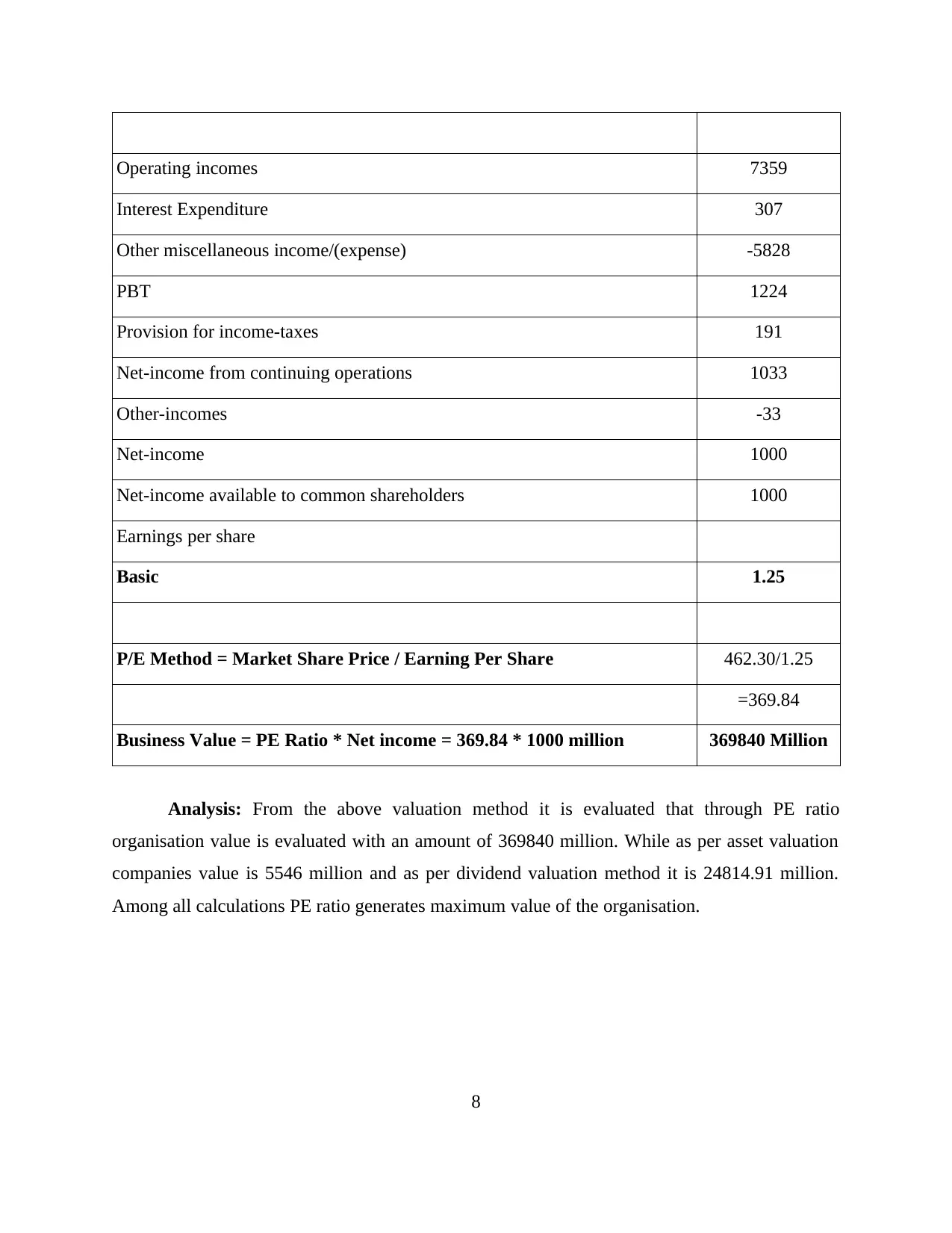

Price to Earning Ratio: This is a valuation method through which business

organisations evaluate its current price relative to its per-share earnings. Through this ratio it is

evaluated by business organisations regarding what amount general public is willing to pay in to

acquire shares of the organisation. PE is determined using market price of shares and multiplied

by companies net-income available for shareholders.

Valuation of BAE through PE Method

Pounds in millions 2018

Sales Receipts 16821

Cost of goods sold 5860

Gross-profit 10961

Operating-expenditures

Other operating expenditures 3602

Aggregate operating expenses 3602

7

possessed by BAE System Plc organisation is 24814.9071 millions. This specifies that amount of

stock is quite good and represents fair market conditions.

Price to Earning Ratio: This is a valuation method through which business

organisations evaluate its current price relative to its per-share earnings. Through this ratio it is

evaluated by business organisations regarding what amount general public is willing to pay in to

acquire shares of the organisation. PE is determined using market price of shares and multiplied

by companies net-income available for shareholders.

Valuation of BAE through PE Method

Pounds in millions 2018

Sales Receipts 16821

Cost of goods sold 5860

Gross-profit 10961

Operating-expenditures

Other operating expenditures 3602

Aggregate operating expenses 3602

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Operating incomes 7359

Interest Expenditure 307

Other miscellaneous income/(expense) -5828

PBT 1224

Provision for income-taxes 191

Net-income from continuing operations 1033

Other-incomes -33

Net-income 1000

Net-income available to common shareholders 1000

Earnings per share

Basic 1.25

P/E Method = Market Share Price / Earning Per Share 462.30/1.25

=369.84

Business Value = PE Ratio * Net income = 369.84 * 1000 million 369840 Million

Analysis: From the above valuation method it is evaluated that through PE ratio

organisation value is evaluated with an amount of 369840 million. While as per asset valuation

companies value is 5546 million and as per dividend valuation method it is 24814.91 million.

Among all calculations PE ratio generates maximum value of the organisation.

8

Interest Expenditure 307

Other miscellaneous income/(expense) -5828

PBT 1224

Provision for income-taxes 191

Net-income from continuing operations 1033

Other-incomes -33

Net-income 1000

Net-income available to common shareholders 1000

Earnings per share

Basic 1.25

P/E Method = Market Share Price / Earning Per Share 462.30/1.25

=369.84

Business Value = PE Ratio * Net income = 369.84 * 1000 million 369840 Million

Analysis: From the above valuation method it is evaluated that through PE ratio

organisation value is evaluated with an amount of 369840 million. While as per asset valuation

companies value is 5546 million and as per dividend valuation method it is 24814.91 million.

Among all calculations PE ratio generates maximum value of the organisation.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

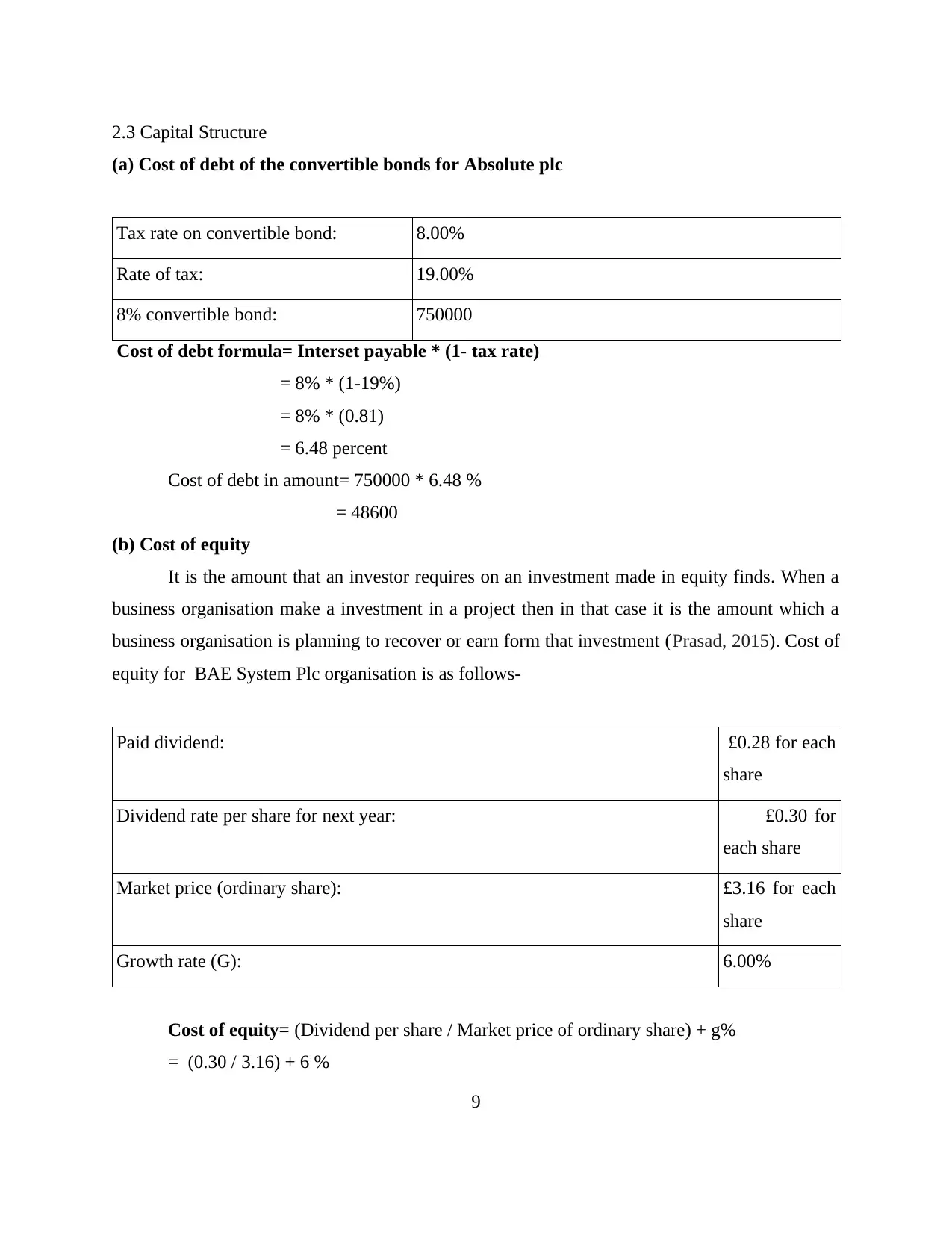

2.3 Capital Structure

(a) Cost of debt of the convertible bonds for Absolute plc

Tax rate on convertible bond: 8.00%

Rate of tax: 19.00%

8% convertible bond: 750000

Cost of debt formula= Interset payable * (1- tax rate)

= 8% * (1-19%)

= 8% * (0.81)

= 6.48 percent

Cost of debt in amount= 750000 * 6.48 %

= 48600

(b) Cost of equity

It is the amount that an investor requires on an investment made in equity finds. When a

business organisation make a investment in a project then in that case it is the amount which a

business organisation is planning to recover or earn form that investment (Prasad, 2015). Cost of

equity for BAE System Plc organisation is as follows-

Paid dividend: £0.28 for each

share

Dividend rate per share for next year: £0.30 for

each share

Market price (ordinary share): £3.16 for each

share

Growth rate (G): 6.00%

Cost of equity= (Dividend per share / Market price of ordinary share) + g%

= (0.30 / 3.16) + 6 %

9

(a) Cost of debt of the convertible bonds for Absolute plc

Tax rate on convertible bond: 8.00%

Rate of tax: 19.00%

8% convertible bond: 750000

Cost of debt formula= Interset payable * (1- tax rate)

= 8% * (1-19%)

= 8% * (0.81)

= 6.48 percent

Cost of debt in amount= 750000 * 6.48 %

= 48600

(b) Cost of equity

It is the amount that an investor requires on an investment made in equity finds. When a

business organisation make a investment in a project then in that case it is the amount which a

business organisation is planning to recover or earn form that investment (Prasad, 2015). Cost of

equity for BAE System Plc organisation is as follows-

Paid dividend: £0.28 for each

share

Dividend rate per share for next year: £0.30 for

each share

Market price (ordinary share): £3.16 for each

share

Growth rate (G): 6.00%

Cost of equity= (Dividend per share / Market price of ordinary share) + g%

= (0.30 / 3.16) + 6 %

9

= 9.49 + 6 %

= 15.49 %

(c)Weighted average cost of capital

It is the rate that a company is expected to pay on an average to all its security holders to

finance its assets. It is referred as the cost of capital that an organisation needs to pay in order to

generate and employ required finances in the business organisation. The cost incurred for the

capital is dictated by the external environment and not on the basis of management of business

organisation (Richards, 2012).

(d)Difficulties in calculating WACC

Estimation of cost of equity is performed through different methods and models and in

each model different issues are involved in relation to estimation. Difference in the rate

of assumption leads to generation of difficulties in the process of calculating WACC.

10

= 15.49 %

(c)Weighted average cost of capital

It is the rate that a company is expected to pay on an average to all its security holders to

finance its assets. It is referred as the cost of capital that an organisation needs to pay in order to

generate and employ required finances in the business organisation. The cost incurred for the

capital is dictated by the external environment and not on the basis of management of business

organisation (Richards, 2012).

(d)Difficulties in calculating WACC

Estimation of cost of equity is performed through different methods and models and in

each model different issues are involved in relation to estimation. Difference in the rate

of assumption leads to generation of difficulties in the process of calculating WACC.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.