Analysis of BAE Systems Plc: Financials, Valuation & Capital

VerifiedAdded on 2023/01/16

|13

|3119

|57

Report

AI Summary

This report provides a comprehensive financial analysis of BAE Systems Plc, focusing on its financial and operating performance for the year 2018. It includes an assessment of profitability, liquidity, and efficiency ratios, alongside a discussion of the limitations of ratio analysis. The report further delves into company valuation, employing asset-based valuation, dividend discount model, and P/E ratio methods to estimate the company's worth. It also examines the capital structure of Absolute plc, calculating the cost of convertible bonds, cost of equity, and weighted average cost of capital (WACC), while acknowledging the difficulties in WACC calculation. The analysis aims to provide insights into BAE Systems' financial health and investment potential.

FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

TABLE OF CONTENTS................................................................................................................2

INTRODUCTION...........................................................................................................................1

2.1 Financial Analysis.....................................................................................................................1

a) Assessment of financial and operating performance of BAE systems plc for the year 2018..1

b) Limitations of using ratio analysis..........................................................................................4

2.2 Company Valuation...........................................................................................................5

a) Calculating the value of BAE systems using different methods.............................................5

b) Valuation methodologies.........................................................................................................7

2.3 Capital structure.........................................................................................................................8

a) Cost of convertible bonds for Absolute plc.............................................................................8

b) Cost of Equity at dividend of 0.30 per ordinary shares...........................................................8

c)Calculation of Weighed Average Cost of Capital of Aboslute plc...........................................8

d) The difficulties faced in calculating the WACC.....................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

TABLE OF CONTENTS................................................................................................................2

INTRODUCTION...........................................................................................................................1

2.1 Financial Analysis.....................................................................................................................1

a) Assessment of financial and operating performance of BAE systems plc for the year 2018..1

b) Limitations of using ratio analysis..........................................................................................4

2.2 Company Valuation...........................................................................................................5

a) Calculating the value of BAE systems using different methods.............................................5

b) Valuation methodologies.........................................................................................................7

2.3 Capital structure.........................................................................................................................8

a) Cost of convertible bonds for Absolute plc.............................................................................8

b) Cost of Equity at dividend of 0.30 per ordinary shares...........................................................8

c)Calculation of Weighed Average Cost of Capital of Aboslute plc...........................................8

d) The difficulties faced in calculating the WACC.....................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

Finance is the lifeblood for an enterprise. Finance is needed for carrying out different

activities of company. There are various sources of finance through which funds can be raised by

companies. Present report will reveal about the financial analysis of BAE Systems, valuation of

company using different methods and cost of capital using weighted average cost of capital.

2.1 Financial Analysis

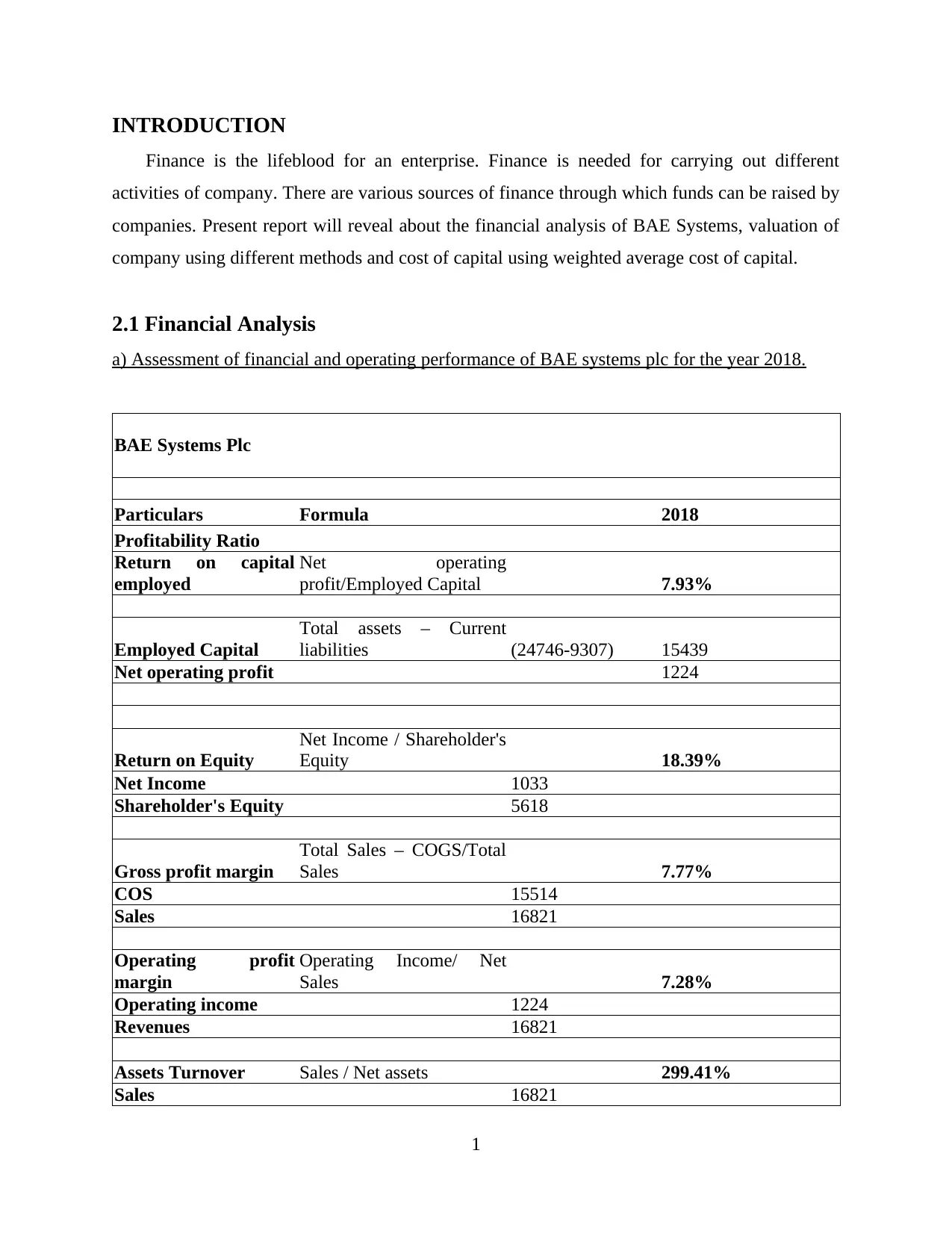

a) Assessment of financial and operating performance of BAE systems plc for the year 2018.

BAE Systems Plc

Particulars Formula 2018

Profitability Ratio

Return on capital

employed

Net operating

profit/Employed Capital 7.93%

Employed Capital

Total assets – Current

liabilities (24746-9307) 15439

Net operating profit 1224

Return on Equity

Net Income / Shareholder's

Equity 18.39%

Net Income 1033

Shareholder's Equity 5618

Gross profit margin

Total Sales – COGS/Total

Sales 7.77%

COS 15514

Sales 16821

Operating profit

margin

Operating Income/ Net

Sales 7.28%

Operating income 1224

Revenues 16821

Assets Turnover Sales / Net assets 299.41%

Sales 16821

1

Finance is the lifeblood for an enterprise. Finance is needed for carrying out different

activities of company. There are various sources of finance through which funds can be raised by

companies. Present report will reveal about the financial analysis of BAE Systems, valuation of

company using different methods and cost of capital using weighted average cost of capital.

2.1 Financial Analysis

a) Assessment of financial and operating performance of BAE systems plc for the year 2018.

BAE Systems Plc

Particulars Formula 2018

Profitability Ratio

Return on capital

employed

Net operating

profit/Employed Capital 7.93%

Employed Capital

Total assets – Current

liabilities (24746-9307) 15439

Net operating profit 1224

Return on Equity

Net Income / Shareholder's

Equity 18.39%

Net Income 1033

Shareholder's Equity 5618

Gross profit margin

Total Sales – COGS/Total

Sales 7.77%

COS 15514

Sales 16821

Operating profit

margin

Operating Income/ Net

Sales 7.28%

Operating income 1224

Revenues 16821

Assets Turnover Sales / Net assets 299.41%

Sales 16821

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Net assets 5618

Liquidity Ratios

Current assets 9576

Current liabilities 9307

Inventory 774

Quick assets 8802

Current ratio

Current assets / current

liabilities 1.03

Quick ratio

Current assets - (stock +

prepaid expenses) 0.95

Efficiency Ratios

Inventory 774

Trade Receivables 5177

Trade Payables 7740

Days 365

COS 15514

Sales 16821

Inventory days Inventory/COS*365 18.210

Debtor days Debtor/ Sales*365 112.34

Creditor days Creditor / Sales*365 167.95

Investor Return

EPS

Total Earnings/

Outstanding shares

Total Earnings(post

tax) 1370

Outstanding Shares

(in millions) 3192

EPS 0.429

Gearing Ratio

Long-term debt 5050

Shareholder's equity 5618

Debt-equity ratio 0.90

Profitability Ratios

2

Liquidity Ratios

Current assets 9576

Current liabilities 9307

Inventory 774

Quick assets 8802

Current ratio

Current assets / current

liabilities 1.03

Quick ratio

Current assets - (stock +

prepaid expenses) 0.95

Efficiency Ratios

Inventory 774

Trade Receivables 5177

Trade Payables 7740

Days 365

COS 15514

Sales 16821

Inventory days Inventory/COS*365 18.210

Debtor days Debtor/ Sales*365 112.34

Creditor days Creditor / Sales*365 167.95

Investor Return

EPS

Total Earnings/

Outstanding shares

Total Earnings(post

tax) 1370

Outstanding Shares

(in millions) 3192

EPS 0.429

Gearing Ratio

Long-term debt 5050

Shareholder's equity 5618

Debt-equity ratio 0.90

Profitability Ratios

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

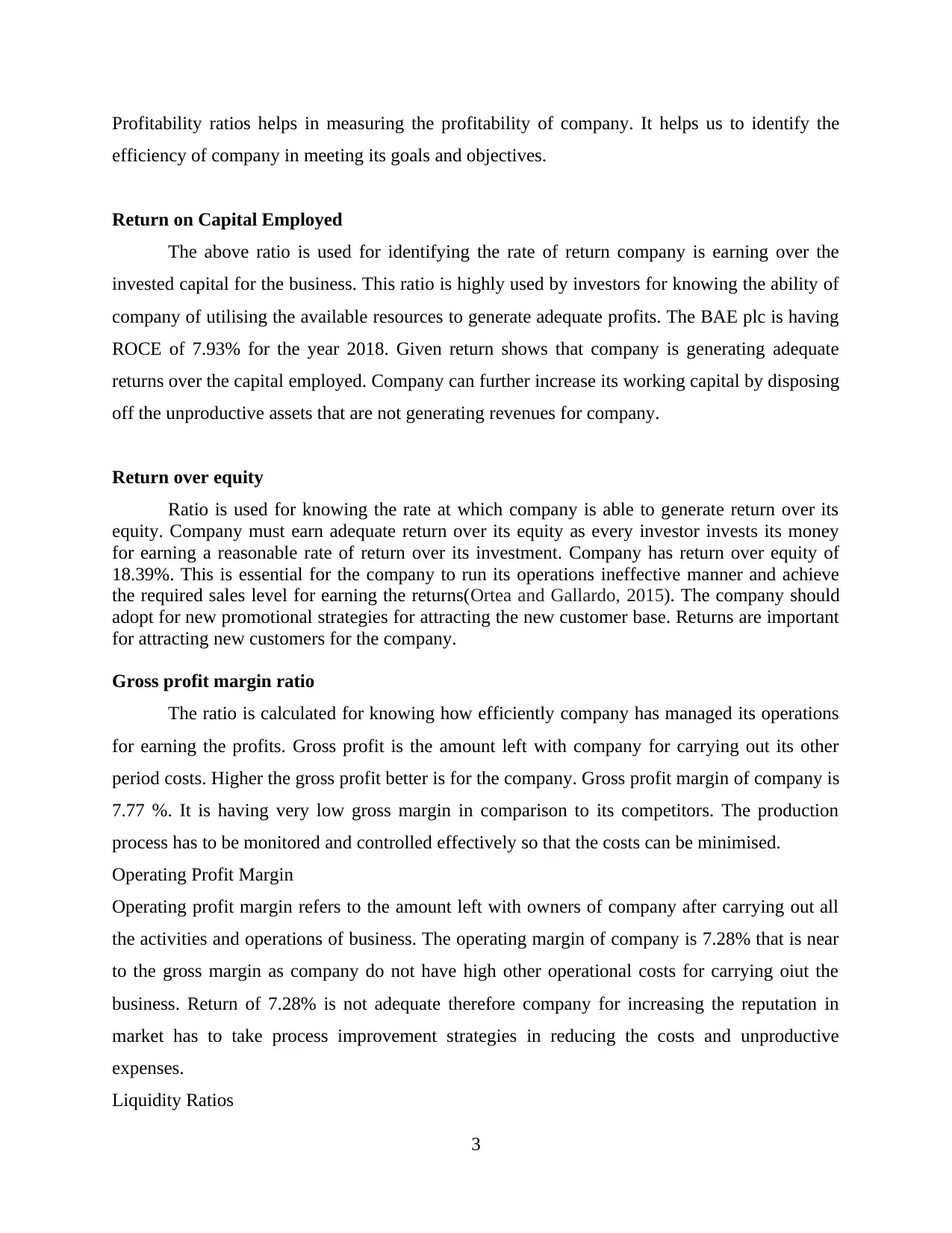

Profitability ratios helps in measuring the profitability of company. It helps us to identify the

efficiency of company in meeting its goals and objectives.

Return on Capital Employed

The above ratio is used for identifying the rate of return company is earning over the

invested capital for the business. This ratio is highly used by investors for knowing the ability of

company of utilising the available resources to generate adequate profits. The BAE plc is having

ROCE of 7.93% for the year 2018. Given return shows that company is generating adequate

returns over the capital employed. Company can further increase its working capital by disposing

off the unproductive assets that are not generating revenues for company.

Return over equity

Ratio is used for knowing the rate at which company is able to generate return over its

equity. Company must earn adequate return over its equity as every investor invests its money

for earning a reasonable rate of return over its investment. Company has return over equity of

18.39%. This is essential for the company to run its operations ineffective manner and achieve

the required sales level for earning the returns(Ortea and Gallardo, 2015). The company should

adopt for new promotional strategies for attracting the new customer base. Returns are important

for attracting new customers for the company.

Gross profit margin ratio

The ratio is calculated for knowing how efficiently company has managed its operations

for earning the profits. Gross profit is the amount left with company for carrying out its other

period costs. Higher the gross profit better is for the company. Gross profit margin of company is

7.77 %. It is having very low gross margin in comparison to its competitors. The production

process has to be monitored and controlled effectively so that the costs can be minimised.

Operating Profit Margin

Operating profit margin refers to the amount left with owners of company after carrying out all

the activities and operations of business. The operating margin of company is 7.28% that is near

to the gross margin as company do not have high other operational costs for carrying oiut the

business. Return of 7.28% is not adequate therefore company for increasing the reputation in

market has to take process improvement strategies in reducing the costs and unproductive

expenses.

Liquidity Ratios

3

efficiency of company in meeting its goals and objectives.

Return on Capital Employed

The above ratio is used for identifying the rate of return company is earning over the

invested capital for the business. This ratio is highly used by investors for knowing the ability of

company of utilising the available resources to generate adequate profits. The BAE plc is having

ROCE of 7.93% for the year 2018. Given return shows that company is generating adequate

returns over the capital employed. Company can further increase its working capital by disposing

off the unproductive assets that are not generating revenues for company.

Return over equity

Ratio is used for knowing the rate at which company is able to generate return over its

equity. Company must earn adequate return over its equity as every investor invests its money

for earning a reasonable rate of return over its investment. Company has return over equity of

18.39%. This is essential for the company to run its operations ineffective manner and achieve

the required sales level for earning the returns(Ortea and Gallardo, 2015). The company should

adopt for new promotional strategies for attracting the new customer base. Returns are important

for attracting new customers for the company.

Gross profit margin ratio

The ratio is calculated for knowing how efficiently company has managed its operations

for earning the profits. Gross profit is the amount left with company for carrying out its other

period costs. Higher the gross profit better is for the company. Gross profit margin of company is

7.77 %. It is having very low gross margin in comparison to its competitors. The production

process has to be monitored and controlled effectively so that the costs can be minimised.

Operating Profit Margin

Operating profit margin refers to the amount left with owners of company after carrying out all

the activities and operations of business. The operating margin of company is 7.28% that is near

to the gross margin as company do not have high other operational costs for carrying oiut the

business. Return of 7.28% is not adequate therefore company for increasing the reputation in

market has to take process improvement strategies in reducing the costs and unproductive

expenses.

Liquidity Ratios

3

Liquidity ratios helps in measuring the liquidity position of company. Company may not rub for

long smoothly if company do not have adequate liquid assets. For measuring the liquidity

position of company current ratio and quick ratio are used.

Current ratio

Current ratio of company is 1.03 that shows liquidity position of company is below the

standard level of 2:1. The current ratio shows the ability of company to repay its short term

liabilities with the available current assets. Company can in place of raising short term can make

long term borrowings for meeting its working capital requirements (Shahrukh and et.al., 2016).

Quick ratio of company is 0.95, the ratio do not consider the inventory in measuring the

liquidity of company. Standard ratio is 1.5 and it is below standard therefore the company

should adopt for policies and procedures that will increase the current assets of company

improving its liquidity position. For strengthening the liquidity position company should focus

over the cash flows during the year. It is essential that company have a strong liquidity position

as stakeholders have significant influence over company from its liquidity concerns.

The efficiency ratio of company is used for identifying how efficiently company is

managing its operations. Company is having high cash operating cycle as the creditor days and

debtor days of company are high. High operating cycle have higher cash requirements, therefore

the cash cycle should be reduced by reducing the debtor and creditor days (Bebu and Lachin,

2015).

Debt equity ratio represents the debt of company as against its equity. Debt equity ratio of

company is 0.90. Company is having debt near to its equity. The debt position of company is

high. Company should not raise further loans as this will increase the interest expenses further

reducing the profit of company. Company for meeting the financial requirements can raise funds

through issue of equity shares and like securities that though have higher risks but do not

increase the costs of company.

b) Limitations of using ratio analysis.

Ratio analysis is very important tool for measuring the financial health and position of and

enterprise. Along with the advantages it also have certain limitations:

Companies makes changes after the year end in the financial statements for enhancing the

ratios. When the financial statements are modified ratio analysis ends with just window

dressing.

4

long smoothly if company do not have adequate liquid assets. For measuring the liquidity

position of company current ratio and quick ratio are used.

Current ratio

Current ratio of company is 1.03 that shows liquidity position of company is below the

standard level of 2:1. The current ratio shows the ability of company to repay its short term

liabilities with the available current assets. Company can in place of raising short term can make

long term borrowings for meeting its working capital requirements (Shahrukh and et.al., 2016).

Quick ratio of company is 0.95, the ratio do not consider the inventory in measuring the

liquidity of company. Standard ratio is 1.5 and it is below standard therefore the company

should adopt for policies and procedures that will increase the current assets of company

improving its liquidity position. For strengthening the liquidity position company should focus

over the cash flows during the year. It is essential that company have a strong liquidity position

as stakeholders have significant influence over company from its liquidity concerns.

The efficiency ratio of company is used for identifying how efficiently company is

managing its operations. Company is having high cash operating cycle as the creditor days and

debtor days of company are high. High operating cycle have higher cash requirements, therefore

the cash cycle should be reduced by reducing the debtor and creditor days (Bebu and Lachin,

2015).

Debt equity ratio represents the debt of company as against its equity. Debt equity ratio of

company is 0.90. Company is having debt near to its equity. The debt position of company is

high. Company should not raise further loans as this will increase the interest expenses further

reducing the profit of company. Company for meeting the financial requirements can raise funds

through issue of equity shares and like securities that though have higher risks but do not

increase the costs of company.

b) Limitations of using ratio analysis.

Ratio analysis is very important tool for measuring the financial health and position of and

enterprise. Along with the advantages it also have certain limitations:

Companies makes changes after the year end in the financial statements for enhancing the

ratios. When the financial statements are modified ratio analysis ends with just window

dressing.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Changes due to inflation in the price levels are ignored by ratio analysis. Most of the

ratios are calculated on historical costs and also the changes in price level between

periods. Correct financial situations are therefore not reflected by the ratio analysis.

Qualitative aspects also affect the operations of company affecting the financial

conditions which are ignored by ratios. Only monetary aspects are taken into

considerations by the accounting ratios.

Ratios do not provide any solutions for resolving the financial problems. It is only used

for identifying the analysis of company. They are just means to end not actual solutions

for the problem.

2.2 Company Valuation

a) Calculating the value of BAE systems using different methods.

Company is considered successful when the wealth and valuation of company is increased.

The investors invest in company for earning returns through dividend or by maximising the

wealth of shareholders. Identifying as well as maintaining the awareness of value of company is

important responsibility of financial executives. Value of company is increased when its share

prices rises in the market because of increase in return over equity or higher profitability as

compared to other players of the industry. There are different methods of valuing the company.

Asset Based Valuation

Asset Based Valuation is a business valuation approach focusing over net assets value of

company. For calculating the net assets total liabilities are subtracted from the total assets of

company. There could be difference between the assets and liabilities that are used by

organisations for valuing the enterprise. The method is used for identifying the value of

enterprise using the net assets valued over the market value of the assets & liabilities. It is

equivalent to shareholder equity or book value of company. Asset based valuations use latitude

market values rather than book values. Also the intangibles not recorded in balance sheet could

be used in this method for deriving the valuation. Challenges faced in asset based valuations are

at the time of calculating the net assets (King, 2017). This method seeks for identifying the

market value of the assets. As the fair market value of asset is different from that of its balance

sheet values. Also the adjustment are made related to the liabilities of company as the

adjustments can affect the liabilities of company.

Asset valuation

Assets 24746

Liability 19128

5

ratios are calculated on historical costs and also the changes in price level between

periods. Correct financial situations are therefore not reflected by the ratio analysis.

Qualitative aspects also affect the operations of company affecting the financial

conditions which are ignored by ratios. Only monetary aspects are taken into

considerations by the accounting ratios.

Ratios do not provide any solutions for resolving the financial problems. It is only used

for identifying the analysis of company. They are just means to end not actual solutions

for the problem.

2.2 Company Valuation

a) Calculating the value of BAE systems using different methods.

Company is considered successful when the wealth and valuation of company is increased.

The investors invest in company for earning returns through dividend or by maximising the

wealth of shareholders. Identifying as well as maintaining the awareness of value of company is

important responsibility of financial executives. Value of company is increased when its share

prices rises in the market because of increase in return over equity or higher profitability as

compared to other players of the industry. There are different methods of valuing the company.

Asset Based Valuation

Asset Based Valuation is a business valuation approach focusing over net assets value of

company. For calculating the net assets total liabilities are subtracted from the total assets of

company. There could be difference between the assets and liabilities that are used by

organisations for valuing the enterprise. The method is used for identifying the value of

enterprise using the net assets valued over the market value of the assets & liabilities. It is

equivalent to shareholder equity or book value of company. Asset based valuations use latitude

market values rather than book values. Also the intangibles not recorded in balance sheet could

be used in this method for deriving the valuation. Challenges faced in asset based valuations are

at the time of calculating the net assets (King, 2017). This method seeks for identifying the

market value of the assets. As the fair market value of asset is different from that of its balance

sheet values. Also the adjustment are made related to the liabilities of company as the

adjustments can affect the liabilities of company.

Asset valuation

Assets 24746

Liability 19128

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Shareholder equity 5618

Interpretation

The value of shareholder’s equity is 5618. Total liabilities of company are 19128 where

the total assets of company are 24746. The value of enterprise is represented by the shareholder’s

equity. In calculating the value of enterprise it has been assumed that all the assets of BAE

systems are recorded at the fair value. The wealth of shareholders is to be enhanced using

different strategies for promoting the sales of company so that the business can achieve it

targeted goals and objectives.

Dividend Valuation Model

Dividend discount model also called DDM is method for valuing stocks. This method is

based over assumption that worth of stock is discounted sums of all the future dividends. In

simple words, method is used for evaluating stocks based over net present value of the future

dividends. It is stated in the financial theory that value of stock is worth all future cash flows that

are expected to be generated by the firm discounted on risks adjusted rates.

CAPM

RFR 0.26%

Beta 0.95

Rm 13%

Cost of equity 12%

Dividend discount

model

Dividend 22.5

R 12%

G 6%

Price of equity 359

Interpretations

Under the CAPM model companies measure the value of company by identifying the

value of stocks in market. Cost of equity refers to the costs incurred by company for raising the

funds. Cost of equity is calculated in CAPM using the beta factor of company and the market

risk premium. It is calculated using the formula ; Ke = RF + (Rm – Rf)*beta. Where the Rf

stands for the risk free rate of investments, Rm represents market risk premium and beta refer to

the change in price as against market.

6

Interpretation

The value of shareholder’s equity is 5618. Total liabilities of company are 19128 where

the total assets of company are 24746. The value of enterprise is represented by the shareholder’s

equity. In calculating the value of enterprise it has been assumed that all the assets of BAE

systems are recorded at the fair value. The wealth of shareholders is to be enhanced using

different strategies for promoting the sales of company so that the business can achieve it

targeted goals and objectives.

Dividend Valuation Model

Dividend discount model also called DDM is method for valuing stocks. This method is

based over assumption that worth of stock is discounted sums of all the future dividends. In

simple words, method is used for evaluating stocks based over net present value of the future

dividends. It is stated in the financial theory that value of stock is worth all future cash flows that

are expected to be generated by the firm discounted on risks adjusted rates.

CAPM

RFR 0.26%

Beta 0.95

Rm 13%

Cost of equity 12%

Dividend discount

model

Dividend 22.5

R 12%

G 6%

Price of equity 359

Interpretations

Under the CAPM model companies measure the value of company by identifying the

value of stocks in market. Cost of equity refers to the costs incurred by company for raising the

funds. Cost of equity is calculated in CAPM using the beta factor of company and the market

risk premium. It is calculated using the formula ; Ke = RF + (Rm – Rf)*beta. Where the Rf

stands for the risk free rate of investments, Rm represents market risk premium and beta refer to

the change in price as against market.

6

Dividend discount model is used for calculating the share price of company. This is

calculated using the following formula; P = Do / (R-g), where D represents the dividend paid for

the year including the inflations, R represents the cost of equity and g represents the growth rate

at which the company will be growing in market. Using this formula the share price of company

comes at 359 that will be multiplied by number of shares for knowing the value of company.

P/E Ratio

P/E ratio is the price earning ratio that is used by managers and executives. Ratio is

against share price of company as against earning per share of company. It is ratio used for

measuring the value of companies. It also helps to identify whether the shares of company are

undervalued or over valued. It also used by companies for comparing itself with the historical

records.

PE ratio

Market price 570.6

EPS 31.3

PE ratio 18.23

Industry PE ratio 25

Status Undervalued

Interpretations

P/E ratio of company is calculated using the given formula.

P/E ratio = Market Value per share / Earning per share

Current market price of share is divided by the earnings per share over the stock of company.

The stocks of the company are undervalued than its actual worth. Investors should go long on the

shares of BAE as the prices of the stock may rise in future.

b) Valuation methodologies.

Asset based pricing model

The model values assets of company on the fair market value. Method is used by

investors and companies especially when facing the liquidation issues. Companies includes the

real state and financial securities for knowing the value of inventories. Drawback of this

approach is that it does not considers the earnings of company in valuation.

Dividend discount model

The dividend model is used by investors and companies for knowing the share prices. This is

calculated for knowing the value of company. Method is deeply grounded with the theoretical

aspects. It is considered reliable as dividend tends to remain constant over long period of time.

There is difficulty in making the actual projections (Bogicevic, Domanovic and Krstic, 2016).

P/E ratio

P/E ratio is highly used by investors and companies for knowing the valuation of stocks in

7

calculated using the following formula; P = Do / (R-g), where D represents the dividend paid for

the year including the inflations, R represents the cost of equity and g represents the growth rate

at which the company will be growing in market. Using this formula the share price of company

comes at 359 that will be multiplied by number of shares for knowing the value of company.

P/E Ratio

P/E ratio is the price earning ratio that is used by managers and executives. Ratio is

against share price of company as against earning per share of company. It is ratio used for

measuring the value of companies. It also helps to identify whether the shares of company are

undervalued or over valued. It also used by companies for comparing itself with the historical

records.

PE ratio

Market price 570.6

EPS 31.3

PE ratio 18.23

Industry PE ratio 25

Status Undervalued

Interpretations

P/E ratio of company is calculated using the given formula.

P/E ratio = Market Value per share / Earning per share

Current market price of share is divided by the earnings per share over the stock of company.

The stocks of the company are undervalued than its actual worth. Investors should go long on the

shares of BAE as the prices of the stock may rise in future.

b) Valuation methodologies.

Asset based pricing model

The model values assets of company on the fair market value. Method is used by

investors and companies especially when facing the liquidation issues. Companies includes the

real state and financial securities for knowing the value of inventories. Drawback of this

approach is that it does not considers the earnings of company in valuation.

Dividend discount model

The dividend model is used by investors and companies for knowing the share prices. This is

calculated for knowing the value of company. Method is deeply grounded with the theoretical

aspects. It is considered reliable as dividend tends to remain constant over long period of time.

There is difficulty in making the actual projections (Bogicevic, Domanovic and Krstic, 2016).

P/E ratio

P/E ratio is highly used by investors and companies for knowing the valuation of stocks in

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

market. Higher P/E ratio represents that stocks of company are over valued or investors may

expect high growth in the near future. P/E ratio can be calculated for only companies having

earnings.

2.3 Capital structure

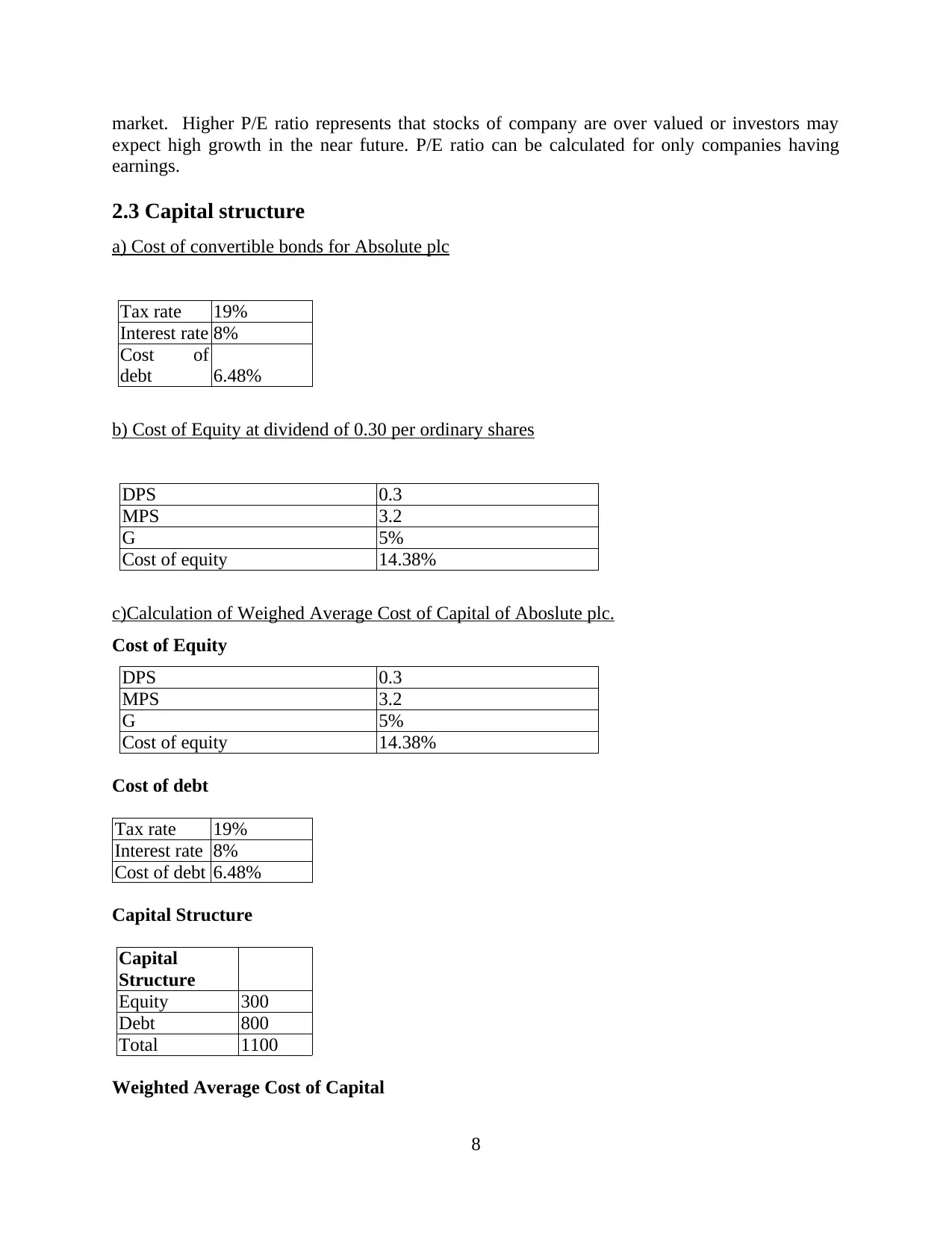

a) Cost of convertible bonds for Absolute plc

Tax rate 19%

Interest rate 8%

Cost of

debt 6.48%

b) Cost of Equity at dividend of 0.30 per ordinary shares

DPS 0.3

MPS 3.2

G 5%

Cost of equity 14.38%

c)Calculation of Weighed Average Cost of Capital of Aboslute plc.

Cost of Equity

DPS 0.3

MPS 3.2

G 5%

Cost of equity 14.38%

Cost of debt

Tax rate 19%

Interest rate 8%

Cost of debt 6.48%

Capital Structure

Capital

Structure

Equity 300

Debt 800

Total 1100

Weighted Average Cost of Capital

8

expect high growth in the near future. P/E ratio can be calculated for only companies having

earnings.

2.3 Capital structure

a) Cost of convertible bonds for Absolute plc

Tax rate 19%

Interest rate 8%

Cost of

debt 6.48%

b) Cost of Equity at dividend of 0.30 per ordinary shares

DPS 0.3

MPS 3.2

G 5%

Cost of equity 14.38%

c)Calculation of Weighed Average Cost of Capital of Aboslute plc.

Cost of Equity

DPS 0.3

MPS 3.2

G 5%

Cost of equity 14.38%

Cost of debt

Tax rate 19%

Interest rate 8%

Cost of debt 6.48%

Capital Structure

Capital

Structure

Equity 300

Debt 800

Total 1100

Weighted Average Cost of Capital

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

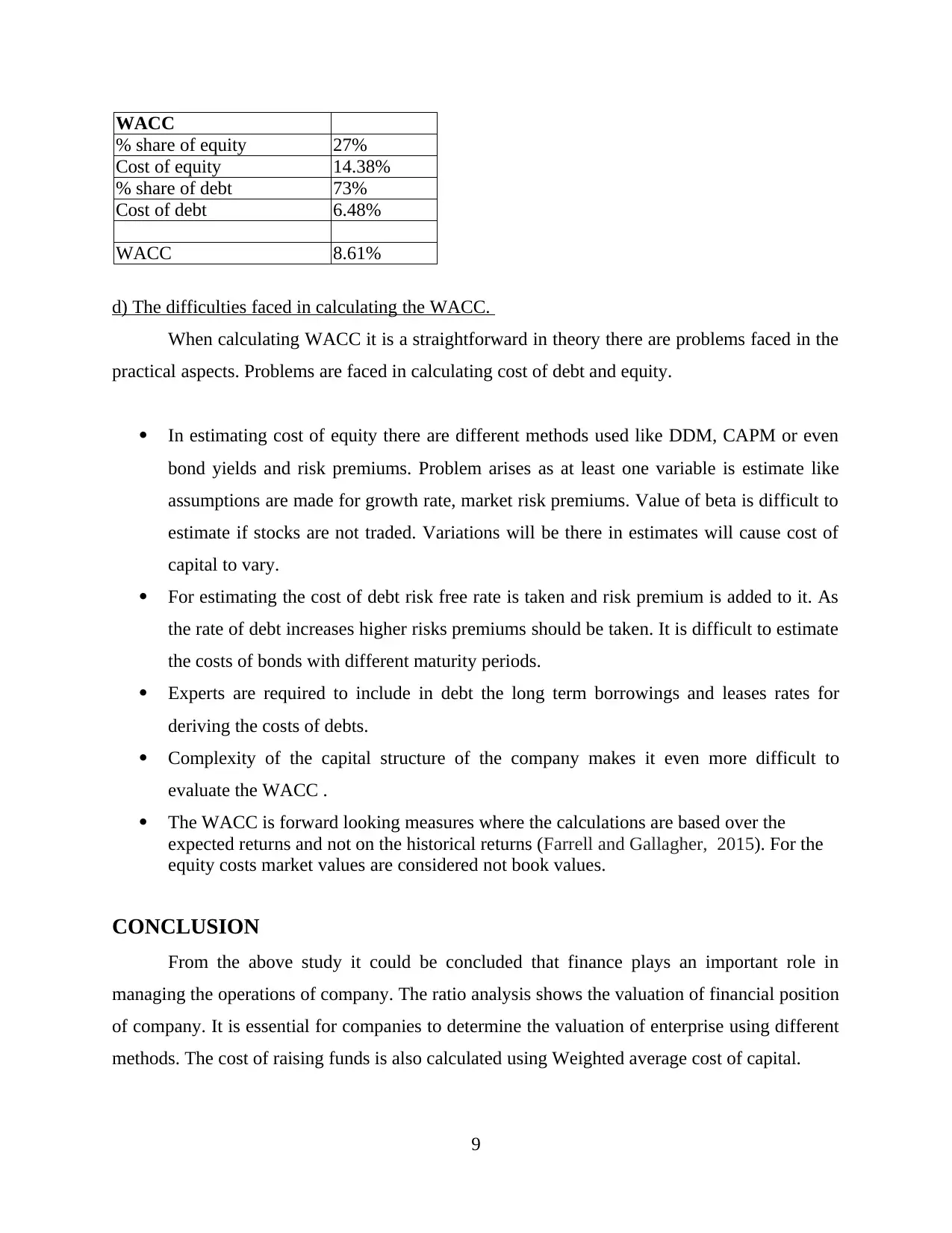

WACC

% share of equity 27%

Cost of equity 14.38%

% share of debt 73%

Cost of debt 6.48%

WACC 8.61%

d) The difficulties faced in calculating the WACC.

When calculating WACC it is a straightforward in theory there are problems faced in the

practical aspects. Problems are faced in calculating cost of debt and equity.

In estimating cost of equity there are different methods used like DDM, CAPM or even

bond yields and risk premiums. Problem arises as at least one variable is estimate like

assumptions are made for growth rate, market risk premiums. Value of beta is difficult to

estimate if stocks are not traded. Variations will be there in estimates will cause cost of

capital to vary.

For estimating the cost of debt risk free rate is taken and risk premium is added to it. As

the rate of debt increases higher risks premiums should be taken. It is difficult to estimate

the costs of bonds with different maturity periods.

Experts are required to include in debt the long term borrowings and leases rates for

deriving the costs of debts.

Complexity of the capital structure of the company makes it even more difficult to

evaluate the WACC .

The WACC is forward looking measures where the calculations are based over the

expected returns and not on the historical returns (Farrell and Gallagher, 2015). For the

equity costs market values are considered not book values.

CONCLUSION

From the above study it could be concluded that finance plays an important role in

managing the operations of company. The ratio analysis shows the valuation of financial position

of company. It is essential for companies to determine the valuation of enterprise using different

methods. The cost of raising funds is also calculated using Weighted average cost of capital.

9

% share of equity 27%

Cost of equity 14.38%

% share of debt 73%

Cost of debt 6.48%

WACC 8.61%

d) The difficulties faced in calculating the WACC.

When calculating WACC it is a straightforward in theory there are problems faced in the

practical aspects. Problems are faced in calculating cost of debt and equity.

In estimating cost of equity there are different methods used like DDM, CAPM or even

bond yields and risk premiums. Problem arises as at least one variable is estimate like

assumptions are made for growth rate, market risk premiums. Value of beta is difficult to

estimate if stocks are not traded. Variations will be there in estimates will cause cost of

capital to vary.

For estimating the cost of debt risk free rate is taken and risk premium is added to it. As

the rate of debt increases higher risks premiums should be taken. It is difficult to estimate

the costs of bonds with different maturity periods.

Experts are required to include in debt the long term borrowings and leases rates for

deriving the costs of debts.

Complexity of the capital structure of the company makes it even more difficult to

evaluate the WACC .

The WACC is forward looking measures where the calculations are based over the

expected returns and not on the historical returns (Farrell and Gallagher, 2015). For the

equity costs market values are considered not book values.

CONCLUSION

From the above study it could be concluded that finance plays an important role in

managing the operations of company. The ratio analysis shows the valuation of financial position

of company. It is essential for companies to determine the valuation of enterprise using different

methods. The cost of raising funds is also calculated using Weighted average cost of capital.

9

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.