BAFN307 Financial Risk Management: Interest Rate Risk Case Study 2018

VerifiedAdded on 2023/06/03

|5

|645

|209

Case Study

AI Summary

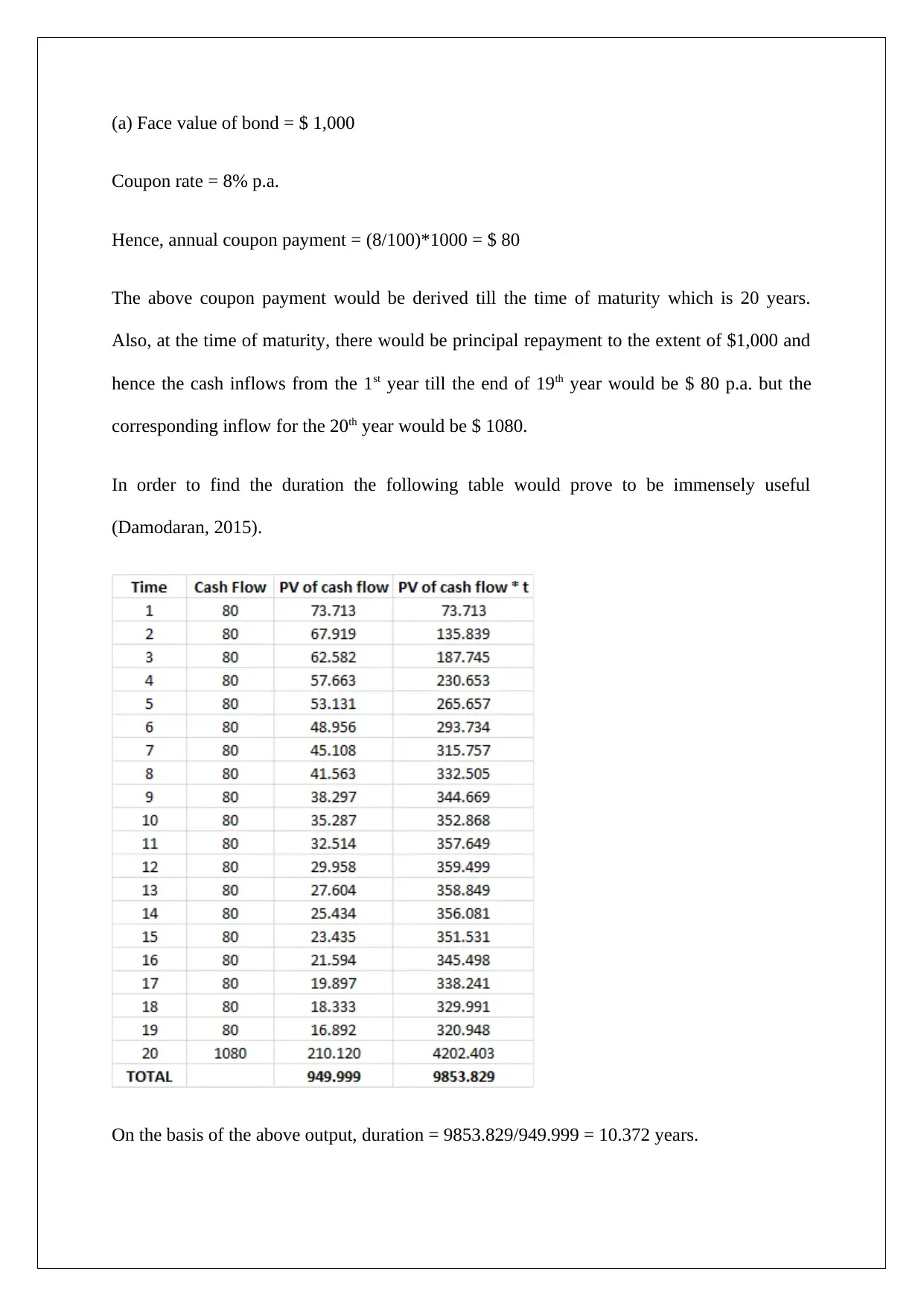

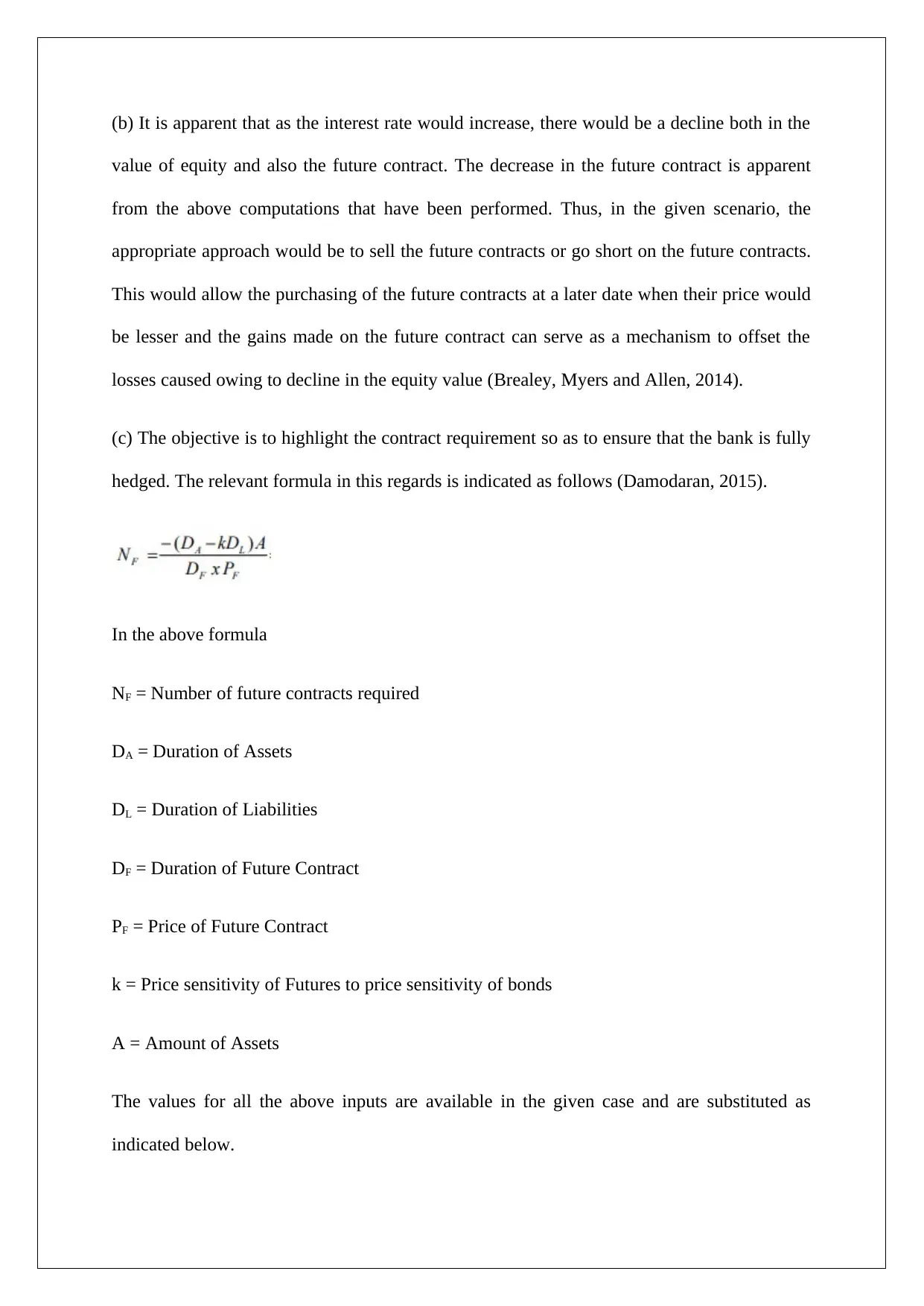

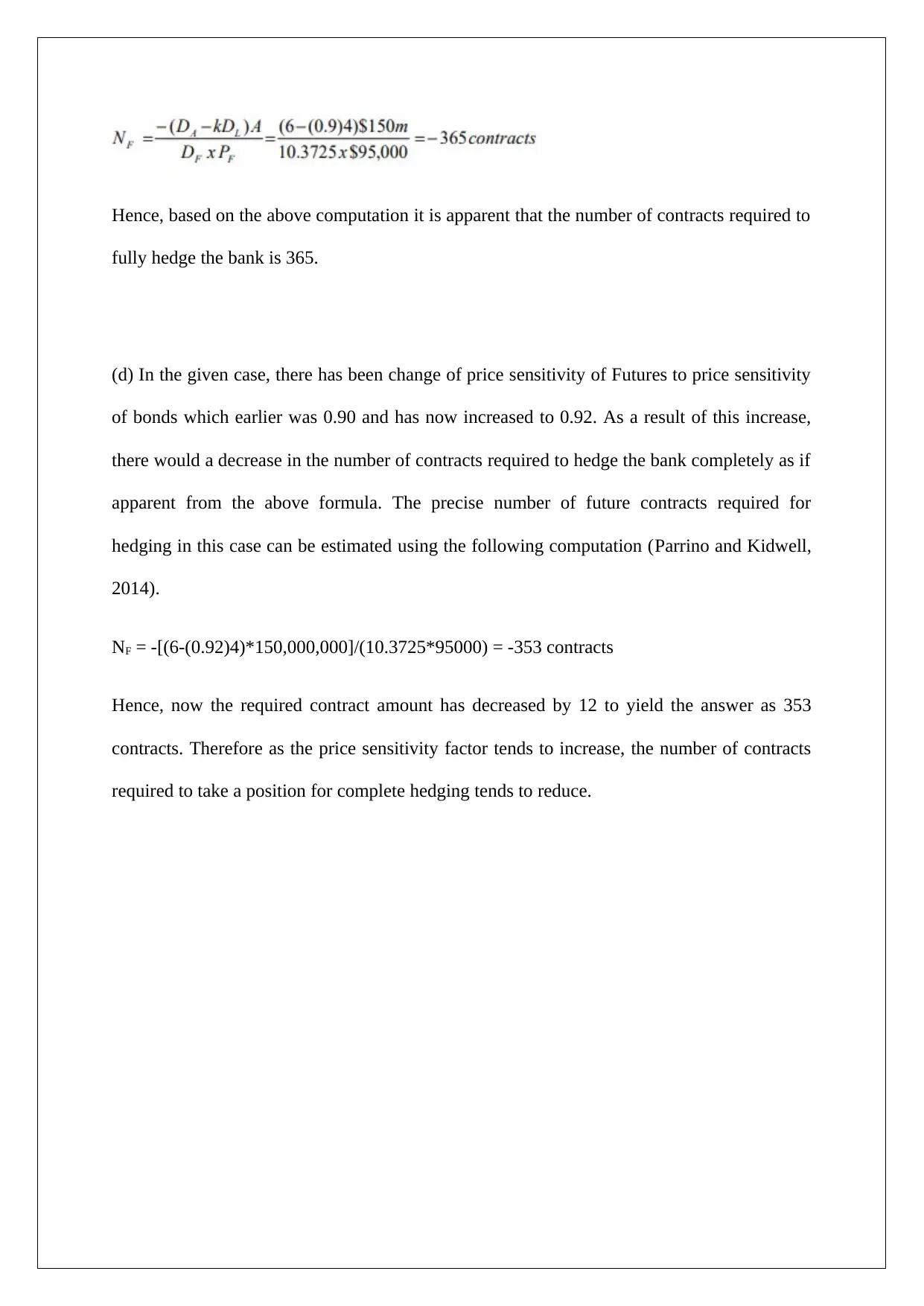

This case study solution addresses interest rate risk management using off-balance sheet instruments, specifically focusing on Austral Big Bank Limited. It involves calculating the duration of a future position, determining whether the bank should go short or long on futures contracts to establish a macro hedge, and calculating the number of contracts necessary to fully hedge the bank. The solution includes computations for duration, analysis of the impact of changing price sensitivity, and the final number of contracts required for complete hedging. The analysis leverages key financial concepts and formulas to provide a comprehensive risk management strategy for the bank. Desklib offers similar solved assignments and past papers for students.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.