Management Accounting: Balance Scorecard Analysis Report

VerifiedAdded on 2021/06/15

|17

|4129

|371

Report

AI Summary

This report provides a comprehensive overview of the Balance Scorecard (BSC) approach in management accounting. It begins with an introduction to the BSC, a strategic performance management tool, and its four key perspectives: financial, customer, internal processes, and learning & growth. The report then delves into the features of the BSC, highlighting its ability to connect cause-and-effect relationships, evaluate performance from multiple viewpoints, and facilitate data collection. A significant portion of the report contrasts the BSC with traditional performance measurement methods, emphasizing the limitations of the latter. The report then applies the BSC framework to Rockwater Limited, a UK-based underwater engineering and construction company, assessing the suitability of the BSC for the client's strategic goals. The report concludes that BSC is a beneficial strategic tool for measuring company performance and is well-suited for Rockwater Limited, enabling it to achieve its strategic objectives. References are included to support the information provided.

RUNNING HEAD: MANAGEMENT ACCOUNTING

Balance scorecard

Balance scorecard

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management accounting1

Contents

Introduction................................................................................................................................2

Part 1..........................................................................................................................................2

Client’s description – Rockwater Limited..............................................................................2

Part B..........................................................................................................................................3

Introduction of Balance scorecard and its features.................................................................3

Part c...........................................................................................................................................8

Traditional approaches VS Balance Scorecard......................................................................8

Part D.......................................................................................................................................11

Suitability of the approach to the client................................................................................11

Conclusion................................................................................................................................13

References................................................................................................................................15

Contents

Introduction................................................................................................................................2

Part 1..........................................................................................................................................2

Client’s description – Rockwater Limited..............................................................................2

Part B..........................................................................................................................................3

Introduction of Balance scorecard and its features.................................................................3

Part c...........................................................................................................................................8

Traditional approaches VS Balance Scorecard......................................................................8

Part D.......................................................................................................................................11

Suitability of the approach to the client................................................................................11

Conclusion................................................................................................................................13

References................................................................................................................................15

Management accounting2

Introduction

This report is an overview of the balance scorecard approach and features it possess. It

explains in detail all the aspects of the new performance measurement tool adopted by the

companies. The report provides a brief summary of BSC approach and its characteristics.

This new approach of balance scorecard measures the performance of company based on its

four perspectives called learning & growth, customer, financial, and internal process. The

main objective of preparing this report was to check the suitability of BSC in the firm’s

client. The first part deals with the detail description of the client which is Rockwater

Limited, a wholly owned subsidiary of Brown & Root/Halliburton which is a global

engineering and construction company.

The second part of the report deals with the introduction of BSC approach and explains its

features in detail. The later part contains a difference between the traditional performance

measurement tools and the new balance scorecard approach. The differences reveal that BSC

covers up all the weaknesses of the earlier used systems and provide greater insights to the

management. In the last section, report includes a brief discussion of sustainability of BSC to

Rockwater Limited and followed by the conclusion that suggests that the BSC is one of the

most beneficial strategic tools which is used to measure the performance of company. Also it

is best suitable for Rockwater because it helps the company to achieve its strategic goals.

Part 1

Client’s description – Rockwater Limited

A fully owned subsidiary of Halliburton Company, named as Rockwater Limited is an UK

based underwater Engineering and Construction Company. It was founded in 1990 and is

situated in Dyce, United Kingdom (Bloomberg.com. 2018). The company is a global leader

within its industry. It offers variety of services that include commercial diving, scour and

Introduction

This report is an overview of the balance scorecard approach and features it possess. It

explains in detail all the aspects of the new performance measurement tool adopted by the

companies. The report provides a brief summary of BSC approach and its characteristics.

This new approach of balance scorecard measures the performance of company based on its

four perspectives called learning & growth, customer, financial, and internal process. The

main objective of preparing this report was to check the suitability of BSC in the firm’s

client. The first part deals with the detail description of the client which is Rockwater

Limited, a wholly owned subsidiary of Brown & Root/Halliburton which is a global

engineering and construction company.

The second part of the report deals with the introduction of BSC approach and explains its

features in detail. The later part contains a difference between the traditional performance

measurement tools and the new balance scorecard approach. The differences reveal that BSC

covers up all the weaknesses of the earlier used systems and provide greater insights to the

management. In the last section, report includes a brief discussion of sustainability of BSC to

Rockwater Limited and followed by the conclusion that suggests that the BSC is one of the

most beneficial strategic tools which is used to measure the performance of company. Also it

is best suitable for Rockwater because it helps the company to achieve its strategic goals.

Part 1

Client’s description – Rockwater Limited

A fully owned subsidiary of Halliburton Company, named as Rockwater Limited is an UK

based underwater Engineering and Construction Company. It was founded in 1990 and is

situated in Dyce, United Kingdom (Bloomberg.com. 2018). The company is a global leader

within its industry. It offers variety of services that include commercial diving, scour and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management accounting3

erosion, installation of marine structures and underwater coatings. The targeted customer

base of Rockwater are the oil companies whose deep-sea oil rigs are been serviced by

Rockwater Limited. The major clients of the company are oil, gas and offshore construction

companies. It has its headquarters in Aberdeen, Scotland and is an operating division of

Brown & Root Energy Services, which is also a part of Halliburton Corporation (Kaplan and

Norton, 1996).

The vision and mission of the company is to great services to its customers, enhance its

profitability and focus on increasing its growth in near future. The company was formed by

merging two independent construction companies which is focused on improving his

strategic management system and achieving its predetermined objectives.

Part B

Introduction of Balance scorecard and its features

Today all the companies have adopted BSC as a new strategic tool used for performance

measurement, to keep safe and check regularly their daily activity records which is essential

to achieve company’s long term goals.It helps the management in controlling the actions of

staff members and to monitor the consequences of the same. It is also explained as a

performance metrics which is used in strategic management with an objective to improve and

enhance the internal control measure of an organization. This new approach of balance

scorecard was first introduced to the world by Dr. Robert Kalpan and Dr. David Norton

which was published in one of the Harvard Business Articlesin 1992 (Niven, 2011).

If we consider the definition of balance scorecard given by Balance Scorecard Institute then it

is defined as a tool or system used for strategic planning and implementation of the

management that can be used to interlink several elements of the strategy of the company for

long term run. This includes the interlinking of target areas, core values, vision and mission

erosion, installation of marine structures and underwater coatings. The targeted customer

base of Rockwater are the oil companies whose deep-sea oil rigs are been serviced by

Rockwater Limited. The major clients of the company are oil, gas and offshore construction

companies. It has its headquarters in Aberdeen, Scotland and is an operating division of

Brown & Root Energy Services, which is also a part of Halliburton Corporation (Kaplan and

Norton, 1996).

The vision and mission of the company is to great services to its customers, enhance its

profitability and focus on increasing its growth in near future. The company was formed by

merging two independent construction companies which is focused on improving his

strategic management system and achieving its predetermined objectives.

Part B

Introduction of Balance scorecard and its features

Today all the companies have adopted BSC as a new strategic tool used for performance

measurement, to keep safe and check regularly their daily activity records which is essential

to achieve company’s long term goals.It helps the management in controlling the actions of

staff members and to monitor the consequences of the same. It is also explained as a

performance metrics which is used in strategic management with an objective to improve and

enhance the internal control measure of an organization. This new approach of balance

scorecard was first introduced to the world by Dr. Robert Kalpan and Dr. David Norton

which was published in one of the Harvard Business Articlesin 1992 (Niven, 2011).

If we consider the definition of balance scorecard given by Balance Scorecard Institute then it

is defined as a tool or system used for strategic planning and implementation of the

management that can be used to interlink several elements of the strategy of the company for

long term run. This includes the interlinking of target areas, core values, vision and mission

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management accounting4

of the company, results and outcomes of the strategy. Moreover, the approach also focuses on

the key goals of the companies and their Key performance indicators which are used to

measure the strategic performance (Balancedscorecard.org. 2018). As per the institute,

following are the reasons why organizations use BSC in their business.

To tell about their goals and objectives

To align the daily activities with the strategic targets

Prioritizing the projects, products and services

To monitor the overall performance of the organization (Balancedscorecard.org.

2018).

There are many industries, business, government and non-government organizations which

uses Balance Scorecard in their business worldwide. Now days, it the most common

measurement tool used by most of the companies. According to a research, it was found out

that over 50% of the companies that are operating in United States has used BSC in their

operations. Also, major companies of Asia and Europe are looking forward to do the same.

The global study of Brain & Co. ranked balance scorecard fifth in the list of top ten most

used tool for management by the organizations around the world. Also according to the

Harvard Business Review, BSc is the most influential business idea of past 75 years (Biazzo

and (Garengo, 2012).

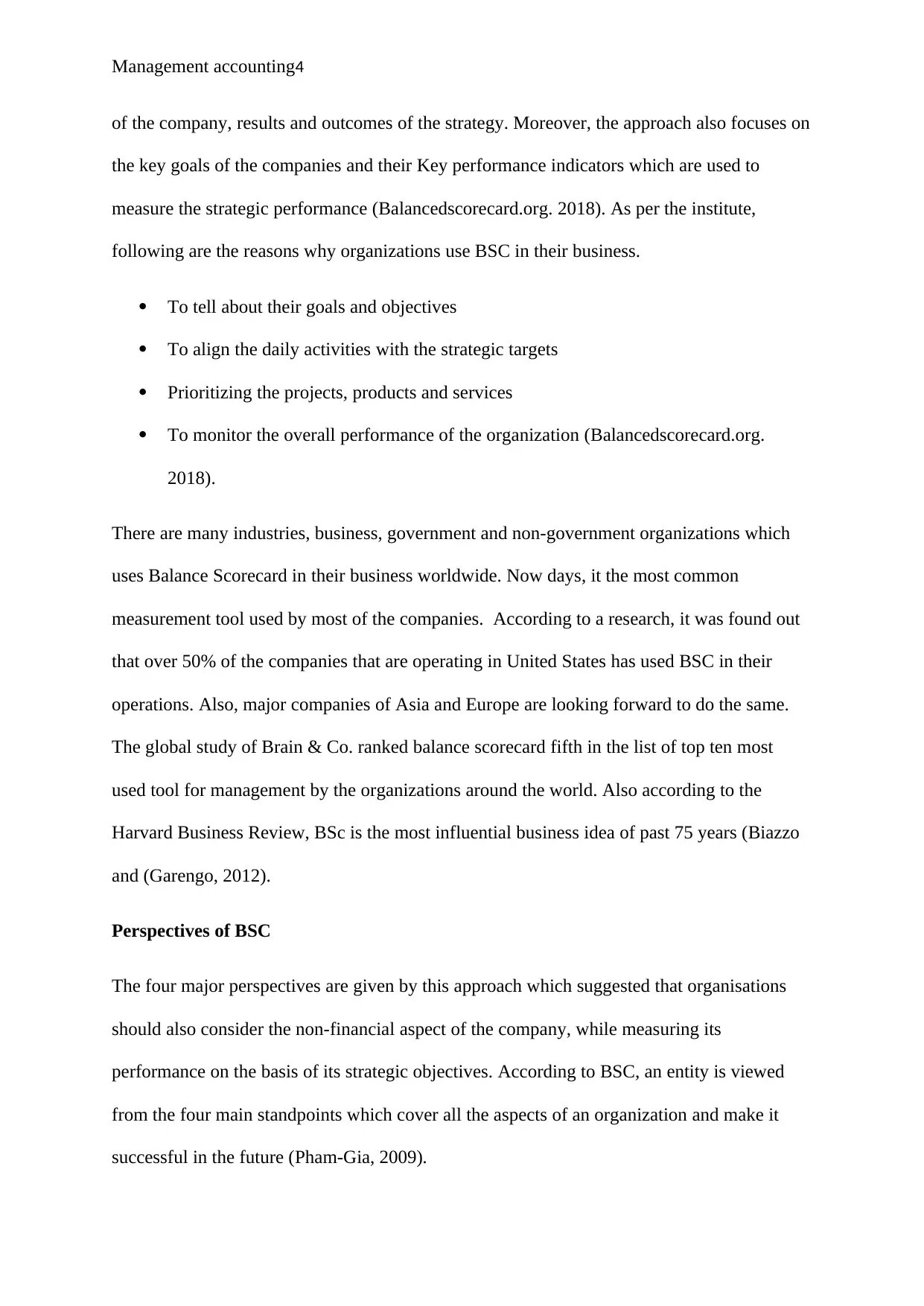

Perspectives of BSC

The four major perspectives are given by this approach which suggested that organisations

should also consider the non-financial aspect of the company, while measuring its

performance on the basis of its strategic objectives. According to BSC, an entity is viewed

from the four main standpoints which cover all the aspects of an organization and make it

successful in the future (Pham-Gia, 2009).

of the company, results and outcomes of the strategy. Moreover, the approach also focuses on

the key goals of the companies and their Key performance indicators which are used to

measure the strategic performance (Balancedscorecard.org. 2018). As per the institute,

following are the reasons why organizations use BSC in their business.

To tell about their goals and objectives

To align the daily activities with the strategic targets

Prioritizing the projects, products and services

To monitor the overall performance of the organization (Balancedscorecard.org.

2018).

There are many industries, business, government and non-government organizations which

uses Balance Scorecard in their business worldwide. Now days, it the most common

measurement tool used by most of the companies. According to a research, it was found out

that over 50% of the companies that are operating in United States has used BSC in their

operations. Also, major companies of Asia and Europe are looking forward to do the same.

The global study of Brain & Co. ranked balance scorecard fifth in the list of top ten most

used tool for management by the organizations around the world. Also according to the

Harvard Business Review, BSc is the most influential business idea of past 75 years (Biazzo

and (Garengo, 2012).

Perspectives of BSC

The four major perspectives are given by this approach which suggested that organisations

should also consider the non-financial aspect of the company, while measuring its

performance on the basis of its strategic objectives. According to BSC, an entity is viewed

from the four main standpoints which cover all the aspects of an organization and make it

successful in the future (Pham-Gia, 2009).

Management accounting5

The perspectives are as follows:

Financial

It contains all that indicators which are related to the profitability and financial goals of the

company. This perspective measure the overall financial performance of an entity by

critically analysing the financial measures. These measures include total revenue, net profit

margin, cash flow, return on assets, return on investment, operating profit margin and many

other which are generally used by every company to evaluate its performance (Keyes,

2016). In case of non-profit organizations, this perspective covers their budget and cost

saving targets. For the managers, it is very important to track the financial health of their

organization to keep all the financial data up to date. They are required to deliver the correct

information on time so that they can enhance and maintain their performance in financial

aspect (Joshi, et. al., 2015).

While evaluating the performance, BSC allows the managers to reduce their cost data by

deploying appropriate corporate systems and to derive the relevant financial information

The perspectives are as follows:

Financial

It contains all that indicators which are related to the profitability and financial goals of the

company. This perspective measure the overall financial performance of an entity by

critically analysing the financial measures. These measures include total revenue, net profit

margin, cash flow, return on assets, return on investment, operating profit margin and many

other which are generally used by every company to evaluate its performance (Keyes,

2016). In case of non-profit organizations, this perspective covers their budget and cost

saving targets. For the managers, it is very important to track the financial health of their

organization to keep all the financial data up to date. They are required to deliver the correct

information on time so that they can enhance and maintain their performance in financial

aspect (Joshi, et. al., 2015).

While evaluating the performance, BSC allows the managers to reduce their cost data by

deploying appropriate corporate systems and to derive the relevant financial information

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management accounting6

which is to be used for making forecast. According to the balance scorecard methodology the

improved financial performance of an organization is the outcome of its better performance

in other three perspectives of the scorecard.

Customer

This perspective allows the company to measure its performance through the perception of its

customers. It wanted them to focus on their performance targets as they are related to their

clients and the market. It covers company’s customer growth and service targets along with

its market share and objectives related to the branding. According to this terminology,

managers are required to determine their targeted customers and market segments in which

the company is going to compete. It consists of several strategic outcomes which are the

result of a well implemented strategy. The main KPIs of this perspective are customer

satisfaction, net promoter scores, market share, service labels, client retention, stakeholders’

needs and brand awareness.

Internal process

It focuses on evaluating the performance of a business through the standpoint of quality and

efficiency of products and services offered. By measuring on the basis of this criteria,

companies are able to attract their customers in the targeted markets and can also fulfil and

satisfy the need of its stakeholders. This perspective mainly focus on internal operation goals

of an organization and covers the objectives which are related to the process followed for

delivering the customer goals (Pramudita, 2016).

It allows the entities to outline their internal control process and the strategies to improve and

enhance the same. Wastage of the resources is of much concern and for this management

must focus on controlling the input of resources and producing reliable products. The main

which is to be used for making forecast. According to the balance scorecard methodology the

improved financial performance of an organization is the outcome of its better performance

in other three perspectives of the scorecard.

Customer

This perspective allows the company to measure its performance through the perception of its

customers. It wanted them to focus on their performance targets as they are related to their

clients and the market. It covers company’s customer growth and service targets along with

its market share and objectives related to the branding. According to this terminology,

managers are required to determine their targeted customers and market segments in which

the company is going to compete. It consists of several strategic outcomes which are the

result of a well implemented strategy. The main KPIs of this perspective are customer

satisfaction, net promoter scores, market share, service labels, client retention, stakeholders’

needs and brand awareness.

Internal process

It focuses on evaluating the performance of a business through the standpoint of quality and

efficiency of products and services offered. By measuring on the basis of this criteria,

companies are able to attract their customers in the targeted markets and can also fulfil and

satisfy the need of its stakeholders. This perspective mainly focus on internal operation goals

of an organization and covers the objectives which are related to the process followed for

delivering the customer goals (Pramudita, 2016).

It allows the entities to outline their internal control process and the strategies to improve and

enhance the same. Wastage of the resources is of much concern and for this management

must focus on controlling the input of resources and producing reliable products. The main

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management accounting7

key performance indicators used by this perspective are process improvements, optimization

of the quality and utilization of capacity (Schmeisser, et. al., 2011).

Learning and Growth

It considers the intangible aspects of an organization and is mainly divided into following

components:

1. Human capital which includes skills, knowledge, specialization and talent.

2. Information capital comprise of the databases, information systems, technology,

infrastructure and networks.

3. Organization capital consists of leadership, employee engagement, culture, and

teamwork and knowledge management.

All these components are been taken into account by this perspective and the management of

the company has to measure the performance by keeping these points in mind. The measures

or KPIs include employee satisfaction, assessment of skills, corporate culture audit and

performance management scores (Makhijani and Creelman, 2011).

Features of BSC

BSC approach has possess the following characteristics

It takes into account the cause and effect relationship which clearly reflects the

strategies of a business.

It is considered that the financial evaluation is most traditional feature of balance

scorecard as it makes the scorecard more useful and important for strategic

management of the company. It considers measures like net profit, revenues, ROA

and ROE.

key performance indicators used by this perspective are process improvements, optimization

of the quality and utilization of capacity (Schmeisser, et. al., 2011).

Learning and Growth

It considers the intangible aspects of an organization and is mainly divided into following

components:

1. Human capital which includes skills, knowledge, specialization and talent.

2. Information capital comprise of the databases, information systems, technology,

infrastructure and networks.

3. Organization capital consists of leadership, employee engagement, culture, and

teamwork and knowledge management.

All these components are been taken into account by this perspective and the management of

the company has to measure the performance by keeping these points in mind. The measures

or KPIs include employee satisfaction, assessment of skills, corporate culture audit and

performance management scores (Makhijani and Creelman, 2011).

Features of BSC

BSC approach has possess the following characteristics

It takes into account the cause and effect relationship which clearly reflects the

strategies of a business.

It is considered that the financial evaluation is most traditional feature of balance

scorecard as it makes the scorecard more useful and important for strategic

management of the company. It considers measures like net profit, revenues, ROA

and ROE.

Management accounting8

The new performance measurement toolis able to evaluate the performance of an

organization on the basis of customer perceptions and stakeholders’ expectations.

It allows the company to work according to the needs of its clients and shareholders.

It gives management full control on the administrative and other operations of the

company.

With help of BSC approach, data collection process becomes easy.

It is a communication tools which conveys the strategy of the company to all the key

people of company.

It highlights some potential decisions that are taken by the management while not

considering both the financial and non-financial factors.

It is able to reduce the number of measures used by the management for monitoring

the performance

The approach is flexible in both functional and operational terms (Monden, Imai and

Matsuo, 2012).

Part c

Traditional approaches VS Balance Scorecard

The need of adopting BSC in the business was to overcome the weakness of the traditional

approach to performance measurements. There were many issues and variances in them, due

to which companies were not able to achieve their strategic goals and objectives. In the

beginning, a Performance Measurement Action Team (PMAT) was created to its eyes on the

different companies to observe their pattern or tool used, and it was observed that most of the

companies used top-down approach in order to evaluate the activities and actions of the

company. However, later on PMAT suggested that this top-down approach was not enough

sufficient for their efficiency enhancement and also resulting in poor progress of the

processes.

The new performance measurement toolis able to evaluate the performance of an

organization on the basis of customer perceptions and stakeholders’ expectations.

It allows the company to work according to the needs of its clients and shareholders.

It gives management full control on the administrative and other operations of the

company.

With help of BSC approach, data collection process becomes easy.

It is a communication tools which conveys the strategy of the company to all the key

people of company.

It highlights some potential decisions that are taken by the management while not

considering both the financial and non-financial factors.

It is able to reduce the number of measures used by the management for monitoring

the performance

The approach is flexible in both functional and operational terms (Monden, Imai and

Matsuo, 2012).

Part c

Traditional approaches VS Balance Scorecard

The need of adopting BSC in the business was to overcome the weakness of the traditional

approach to performance measurements. There were many issues and variances in them, due

to which companies were not able to achieve their strategic goals and objectives. In the

beginning, a Performance Measurement Action Team (PMAT) was created to its eyes on the

different companies to observe their pattern or tool used, and it was observed that most of the

companies used top-down approach in order to evaluate the activities and actions of the

company. However, later on PMAT suggested that this top-down approach was not enough

sufficient for their efficiency enhancement and also resulting in poor progress of the

processes.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management accounting9

To deal with the above issues, BSC approach was introduced and is widely used by many

companies across the world. However, Traditional measurement tools and BSC approach

have many differences. The major difference is that the earlier used systems tracks only the

financial performance of the business which takes into account the points related to net profit

earned and capital needed. Different financial matrices like, revenue, return on equity, and

cash flow, were the main focus of these tools as reported in the annual report of company.

These metrics are known as lag indicators as they only shows the past historical data of the

business and cannot be used for predicting its future (Kaplan and Norton, 2015).

Another difference was that traditional systems make the management ignore the benefit of

value creation for the organization in long run. It only focuses on the financial aspect. These

tools have also been used by other companies which were dealing with mass production and

having several tangible assets like plant, equipment, and property. Moreover, the earlier

approaches were not aligned to the strategic objectives of the organizations(Griff,

2014). These goals or objectives of the companies were mainly focused on benefit of the

company in long term and an efficient allocation of their resources as per the requirement of

business. These objectives were also accounting the value and expectations of shareholders.

Traditional systems basically concerned at short term financial performance and does not

completely comply the business operations with its strategic goals. This results in making

these not fit for the dynamic environment of completely change world for business (Suri,

Ratnam and Gupta, 2004).

However, now, instead of mass production companies are switching on knowledge based

production. This requires them to cover each and every aspect whether financial or non-

financial. Also they have to consider the value of intangible assets along with their tangibles

such as customer relationships, human and intellectual capital and many others (Ashioya,

2015).In this way companies have adopted new performance measuring tools that allow them

To deal with the above issues, BSC approach was introduced and is widely used by many

companies across the world. However, Traditional measurement tools and BSC approach

have many differences. The major difference is that the earlier used systems tracks only the

financial performance of the business which takes into account the points related to net profit

earned and capital needed. Different financial matrices like, revenue, return on equity, and

cash flow, were the main focus of these tools as reported in the annual report of company.

These metrics are known as lag indicators as they only shows the past historical data of the

business and cannot be used for predicting its future (Kaplan and Norton, 2015).

Another difference was that traditional systems make the management ignore the benefit of

value creation for the organization in long run. It only focuses on the financial aspect. These

tools have also been used by other companies which were dealing with mass production and

having several tangible assets like plant, equipment, and property. Moreover, the earlier

approaches were not aligned to the strategic objectives of the organizations(Griff,

2014). These goals or objectives of the companies were mainly focused on benefit of the

company in long term and an efficient allocation of their resources as per the requirement of

business. These objectives were also accounting the value and expectations of shareholders.

Traditional systems basically concerned at short term financial performance and does not

completely comply the business operations with its strategic goals. This results in making

these not fit for the dynamic environment of completely change world for business (Suri,

Ratnam and Gupta, 2004).

However, now, instead of mass production companies are switching on knowledge based

production. This requires them to cover each and every aspect whether financial or non-

financial. Also they have to consider the value of intangible assets along with their tangibles

such as customer relationships, human and intellectual capital and many others (Ashioya,

2015).In this way companies have adopted new performance measuring tools that allow them

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management accounting10

to assess all the measurement aspects related to both quality and quantity of the production. It

also enables them to achieve their strategic goals and objectives. The tool adopted was

Balance Scorecard approach (Hoag and Cooper, 2006).

This new performance measurement tool is the best alternative for traditional tools as it

overcomes all the deficiencies and focuses on both the financial and non-financial aspects of

the company’s business. It takes into account the qualitative metrics and addresses the

changes in the modern business world. It allows the companies to align their actions with

their strategic goals and objectives. This new tool measures the performance of company on

the basis of different perspectives as, internal process, customer, financial, and learning and

growth of the company. BSC helps the companies to take correct decisions regarding their

strategies as it includes both the lag and lead indicators. These indicators or parameters

completely align business’s activities with its objectives (Nair, 2004).

Summarising the differences

Traditional systems Balance Scorecard

Only financial aspects are covered. Both the financial and non-financial

aspects are considered.

Different metrics like profit margins,

ROA and ROE are preferred.

Both the qualitative and quantitative

matrices are considered including

customer, finance, internal process, and

learning & growth of company.

Failed in establishing a proper link

between strategic goals and daily

activities.

Do set a link between the activities and

company’s goals.

Only financial performance measures. Overall performance measures.

No perspectives are there and only Four different perspectives used as the

to assess all the measurement aspects related to both quality and quantity of the production. It

also enables them to achieve their strategic goals and objectives. The tool adopted was

Balance Scorecard approach (Hoag and Cooper, 2006).

This new performance measurement tool is the best alternative for traditional tools as it

overcomes all the deficiencies and focuses on both the financial and non-financial aspects of

the company’s business. It takes into account the qualitative metrics and addresses the

changes in the modern business world. It allows the companies to align their actions with

their strategic goals and objectives. This new tool measures the performance of company on

the basis of different perspectives as, internal process, customer, financial, and learning and

growth of the company. BSC helps the companies to take correct decisions regarding their

strategies as it includes both the lag and lead indicators. These indicators or parameters

completely align business’s activities with its objectives (Nair, 2004).

Summarising the differences

Traditional systems Balance Scorecard

Only financial aspects are covered. Both the financial and non-financial

aspects are considered.

Different metrics like profit margins,

ROA and ROE are preferred.

Both the qualitative and quantitative

matrices are considered including

customer, finance, internal process, and

learning & growth of company.

Failed in establishing a proper link

between strategic goals and daily

activities.

Do set a link between the activities and

company’s goals.

Only financial performance measures. Overall performance measures.

No perspectives are there and only Four different perspectives used as the

Management accounting11

financial measures are used. main criteria.

Part D

Suitability in the approaching the client

Rockwater Limited, being the worldwide leader in underwater engineering and construction

applied the BSC approach to its business in order to improve its performance and enhance its

overall growth. Norman Chambers was the CEO of the company in 1989, the year in which

the industry’s competitive world has changed dramatically.

In order to overcome its problems, the company applied Balance scorecard in its business and

formed a new vision statement which stated that it will provide high standards of quality and

safety to its clients. In order to implement this, the company has created strategy which

consists of five elements that are:

Providing services according to the needs and expectations of the customers.

High level of client satisfaction.

Improving the standards of safety and becoming cost effective.

High quality employees

Realizing shareholder expectations

These elements are then converted in to the four perspectives of balance scorecard approach.

Rockwater Limited’s management and CEO can transform their vision and strategies into a

BSC approach which will appear like this:

financial measures are used. main criteria.

Part D

Suitability in the approaching the client

Rockwater Limited, being the worldwide leader in underwater engineering and construction

applied the BSC approach to its business in order to improve its performance and enhance its

overall growth. Norman Chambers was the CEO of the company in 1989, the year in which

the industry’s competitive world has changed dramatically.

In order to overcome its problems, the company applied Balance scorecard in its business and

formed a new vision statement which stated that it will provide high standards of quality and

safety to its clients. In order to implement this, the company has created strategy which

consists of five elements that are:

Providing services according to the needs and expectations of the customers.

High level of client satisfaction.

Improving the standards of safety and becoming cost effective.

High quality employees

Realizing shareholder expectations

These elements are then converted in to the four perspectives of balance scorecard approach.

Rockwater Limited’s management and CEO can transform their vision and strategies into a

BSC approach which will appear like this:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.